(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or OUR HARD LANDING BACK ON EARTH),

(SPY), (QQQ), (TLT), (VIX), (VXX), (MSFT), (JPM), (AAPL),

(DECODING THE GREENBACK),

(DUMPING THE OLD ASSET ALLOCATION RULES)

Truth be told, it’s the really boring, sedentary, go-nowhere markets that drive me nuts, cause me to tear my hair out, and urge me on to an early retirement.

The week started with such promise.

Sunday night I witnessed the first Space X landing of a rocket in California which I could clearly see from the top of Berkeley’s Grizzly Peak some 250 miles away. It was fascinating to see four separate jets steer the spacecraft earthward.

Financial markets had a different landing in mind, the hard kind, if not a crash.

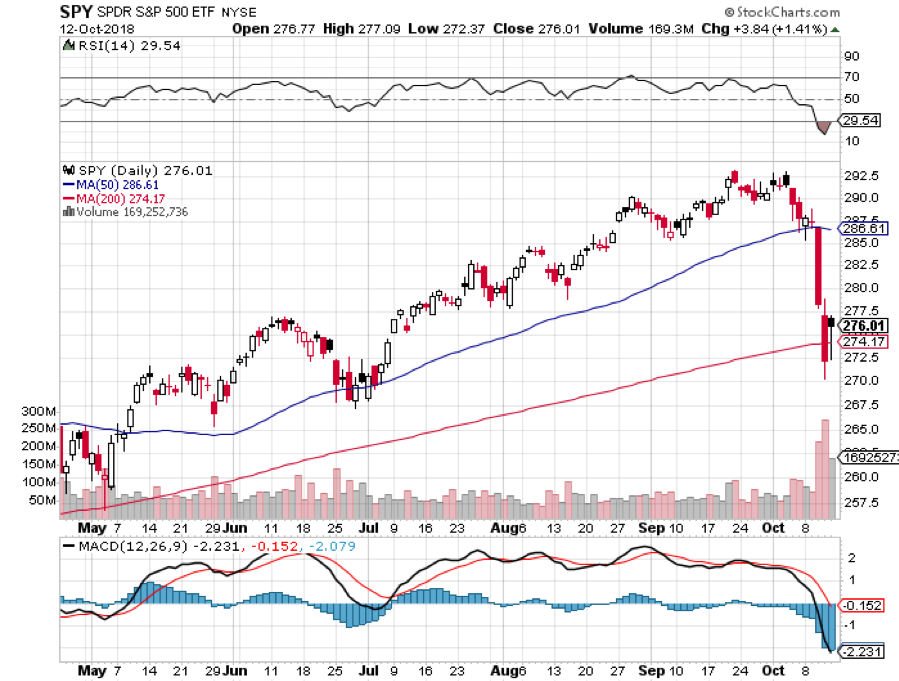

I absolutely love the market we had last week which saw the third biggest down day in history, volatility explode, and $2.6 trillion in stock market capitalization vaporize.

I had to blink when I saw NASDAQ (QQQ) down an incredible 350 points in one day. My Mad Hedge Market Timing Index hit an all-time low at 4.

No wonder insider selling hit $10.3 billion in August, another record. Maybe they know something we don’t.

Chinese Gamer Tencent Postponed their US IPO. It seems they noticed that market conditions had become unfavorable. I know investment bankers hate passing on an opportunity to ring the cash register. I used to be one.

There is no better feeling than being 100% cash going into one of these crashes and then having panicked investors puke their best quality positions to me at a market bottom.

On Thursday, I backed up the truck and issued four perfectly timed Trade Alerts, picking up Microsoft (MSFT), Apple (AAPL), and the S&P 500 (SPY), and covering my short position in the bond market (TLT).

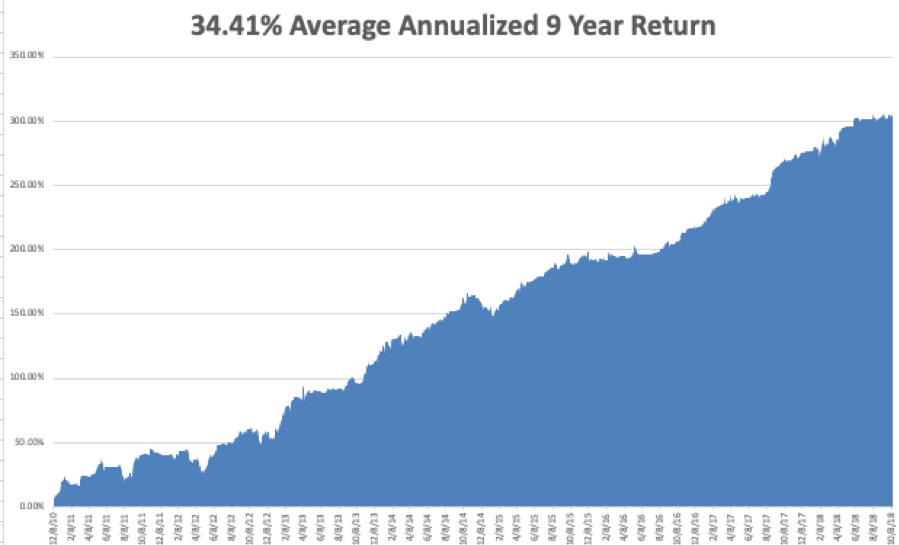

In fact, I believe I had my best week of the year even though I only added modestly to my annual return. Look at the charts below and you’ll see that I suffered a 9% drawdown during the February meltdown. Maybe I’m getting wiser as I get older? One can only hope.

This time, I managed to limit my loss to a modest 2.5% and am nearly unchanged on the month despite the Dow Average at one point nearly giving up all its gains for 2018. This is also against a horrific backdrop of hedge fund performance that is now showing losses for 2018.

The Volatility Index (VIX) made a move for the ages, at one point kissing the $29 handle, up from $11 two weeks ago. During the 600-point swoosh down on Thursday, I couldn’t get any of my staff on the phone. The entire company was logged into their personal trading accounts, buying puts on the iPath S&P 500 VIX Short-Term Futures ETN (VXX) as fast as they could.

Which leads me to believe that the bottom is near. Earnings and valuation support start kicking in big time at these levels, and the blackout period for company share buybacks started ending with the bank earnings last Friday.

When you take a $1 trillion buyer out of the market, it has a huge effect no matter how strong the fundamentals are. Start buying those dips. Their return is similarly eventful. I’ve already started to invest my 95% cash position.

Further eroding confidence was the president’s statement that the Federal Reserve is crazy. So, now we know the president appoints crazy people to the most important financial positions in the country. White House control of interest rates ahead of elections. Why didn’t I think of that?

Sparking the Friday melt-up was a statement by JP Morgan (JPM) CEO Jamie Diamond saying that a 40-basis point rise in rates is no big deal. The bull market is on. His earnings beat all expectations.

My 2018 year-to-date performance has bounced back to 27.56%, and my trailing one-year return stands at 35.87%. October is almost flat at -0.84%. Most people will take that in these horrific conditions.

My nine-year return appreciated to 304.03%. The average annualized return stands at 34.41%.

This coming week will be pretty sedentary on the data front. Monday, October 15 at 8:30 AM brings us September Retail Sales.

On Tuesday, October 16 at 9:15 AM, September Industrial Production is announced.

On Wednesday, October 17 at 8:30 AM, September Housing Starts are published.

Thursday, October 18 at 8:30, we get Weekly Jobless Claims. At 10:00 we learne the September Index of Leading Economic Indicators.

On Friday, October 19, at 10:00 AM, the September Housing Starts are out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will spend this week on my Southeastern US roadshow, giving strategy luncheons in Savannah, GA, Atlanta, GA, Miami, FL, and Houston, TX. I love meeting my readers mano a mano who are often a source of my best trading ideas. It looks like I’ll miss Hurricane Michael by three days.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Off to Lunch

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-on-a-camel.png454470MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-15 09:03:382018-10-15 08:11:07The Market Outlook for the Week Ahead, or Our Hard Landing Back on Earth

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Interest rates triggered a tsunami wave of selling tearing apart the tech sector with a vicious profit-taking few trading days.

No doubt that asset managers are frantically locking in profits for the rest of the year and protecting ebullient performance from a year to remember.

This week shouldn’t deter investors from picking up bargains that were non-existent for most of the year because the bulk of the highest quality tech names churned higher with lurching momentum.

Here are the names of five of the best stocks to slip into your portfolio in no particular order once the madness subsides.

Apple

Steve Job’s creation is weathering the gale-fore storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software-tilted tech company. The timing is perfect as China has enhanced their smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality. That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $100 billion in shares by the end of the year. Get into this stock while you can as entry points are few and far between.

Amazon

This is the best company in America hands down and commands 5% of total American retail sales or 49% of American e-commerce sales.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then oozing innovation and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft

The optics in 2018 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter and that is a good thing in 2018.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business.

Microsoft Azure grew 87% YOY last quarter. The previous quarter saw Azure rocket by 98%. Shares are cheaper than Amazon and almost as potent.

Square

CEO Jack Dorsey is doing everything right at this fin-tech company blazing a trail right to the doorsteps of the traditional banks.

The various businesses they have on offer makes me think of Amazon’s portfolio because of the supreme diversity. The Cash App is a peer-to-peer money transfer program that cohabits with a bitcoin investing function on the same smartphone app.

Square has targeted the smaller businesses first and is a godsend for these entrepreneurs who lack the immense capital to create a financial and payment infrastructure. Not only do they provide the physical payment systems for restaurant chains, they also offer payroll services and other small loans.

The pipeline of innovation is strong with upper management mentioning they are considering stock trading products and other bank-like products. Wall Street bigwigs must be shaking in their boots.

The recently departed CFO Sarah Friar triggered a 10% collapse in share price on top of the market meltdown. The weakness will certainly be temporary, especially if they keep doubling their revenue every two years like they have been doing.

Roku

Benefitting from the broad-based migration from cable tv to online streaming and cord-cutting, Roku is perfectly placed to delectably harvest the spoils.

This uber-growth company offers an over-the-top (OTT) streaming platform along with the necessary hardware and picks up revenue by selling digital ads.

Founder and CEO Anthony Woods owns 21 million shares of his brainchild and insistently notes that he has no interest in selling his company to a Netflix or Apple.

Roku’s active accounts mushroomed 46% to 22 million in the second quarter. Viewers are reaffirming the obsession with on-demand online streaming content with hours streamed on the platform increasing 58% to 5.5 billion.

The Roku platform can be bought for just $30 and is easy to set-up. Roku enjoys the lead in the over-the-top (OTT) streaming device industry controlling 37% of the market share leading Amazon’s Fire Stick at 28%.

The runway is long as (OTT) boxes nestle cozily in only 40% of American homes with broadband, up from a paltry 6% in 2010.

They are consistently absent from the backbiting and jawboning the FANGs consistently find themselves in partly because they do not create original content and they are not an off-shoot from a larger parent tech firm.

This growth stock experiences the same type of volatility as Square. Be patient and wait for 5-7% drops to pick up some shares.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-15 09:01:572018-10-15 08:40:25Five Stocks to Buy at the Bottom

I drove into San Francisco for a client dinner last night and had to wait an hour at the Bay Bridge toll gate. When I finally got into town, the parking attendant demanded $50. Dinner for two at Morton’s steakhouse? How about $400.

Which all underlines the fact that we have reached “Peak” San Francisco. San Francisco just isn’t fun anymore.

The problem for you is that if the City by the Bay has peaked, have its much-loved big cap technology stocks, like Facebook (FB), Alphabet (GOOGL), and Netflix (NFLX) peaked as well?

To quote the late manager of the New York Yankees baseball team, Yogi Berra, “Nobody goes there anymore because it’s too crowded.”

What city was the number one creator of technology jobs in 2017?

If you picked San Francisco, you would have missed by a mile. Anyone would be nuts to start up a new business here as rents and labor are through the roof.

Competition against the tech giants for senior staff is fierce. What, no fussball table, free cafeteria, or on-call masseuses? You must be joking!

You would be much better off launching your new startup in Detroit, Michigan. Better yet, hyper-connected low-waged Estonia where the entire government has gone digital.

In fact, Toronto, Canada is the top job creator in tech now, creating an impressive 50,000 jobs last year. Miami, FL and Austin, TX followed. Silicon Valley was at the bottom of the heap.

It’s been a long time since peach orchards dominated the Valley.

Signs that the Bay Area economy is peaking are everywhere. Residential real estate is rolling over now that the harsh reality of no more local tax deductions on federal tax returns is sinking in.

To qualify for a home loan to buy the $1.2 million median home in San Francisco, you have to be a member of the 1%, earning $360,000 a year or better.

Two-bedroom one bath ramshackle turn of the century fixer uppers are going for $1 million in the rapidly gentrifying nearby city of Oakland, only one BART stop from Frisco.

Most school districts have frozen inter-district transfers because they are all chock-a-block with students. And good luck getting your kid into a private school like University or Branson. There are five applicants for every place at $40,000 a year each.

The freeways have become so crowded that no one goes out anymore. It’s rush hour from 6:00 AM to 8:00 PM every day.

When you do drive it’s dangerous. The packed roads have turned drivers into hyper-aggressive predators, constantly weaving in and out of traffic, attempting to cut seconds off their commutes. And there is no drivers ed in China.

I took my kids to the city the other day for a Halloween “Ghost Tour” of posh Pacific Heights. It was lovely spending the evening strolling the neighborhood’s imposing Victorian mansions.

The ornate gingerbread and stained-glass buildings are stacked right against each other to keep from falling down in earthquakes. It works. The former abodes of gold and silver barons are now occupied by hoody-wearing tech titans driving new Teslas.

We learned of the young girl forced into a loveless marriage with an older wealthy stock broker in 1888. She bolted at the wedding and was never seen again.

However, the ghost of a young woman wearing a white wedding address has been seen ever since around the corner of Bush Street and Octavia Avenue. Doors slam, windows shut themselves, and buildings make weird creaking noises.

Then I came to a realization walking around Fisherman’s Wharf as I was nearly poked in the eye by a selfie stick-wielding visitor. The tourist areas on weekdays are just as crowded as they were on summer weekends 30 years ago, except that now the number of languages spoken has risen tenfold, as has the cost.

It started out to be a great year for technology stocks. Amazon (AMZN) alone managed to double off its February mini crash bottom, while others like Apple (AAPL) rocketed by 56%. But traders may have visited the trough once too often

The truth is that technology stocks have not performed since June, right when the Mad Hedge Fund Trader dumped its entire portfolio. Only Microsoft (MSFT) and Amazon (AMZN) have managed to eke out new all-time highs since then, and only just.

The rest of tech has been moving either sideways in the most desultory way possible, or suffered cataclysmic declines like Facebook (FB) and Micron Technology (MU).

Of course, the trade wars haven’t helped. It’s amazing that big tech hasn’t already been hit harder given their intensely global business models.

Nor has rising interest rates. Big cap tech companies have such enormous cash balances that they are all net creditors to the financial system and actually benefit from higher interest rates. But dear money does slow the US economy and that DOES hurt their earnings prospects.

No, I’m not worried about tech for the long term. There is no analog company that can compete with a digital company anywhere in the world.

Accounting for 26% of the stock market capitalization and 50% of its profits, it’s only a question of when we get a major new up leg in share prices, not if.

The only unknown now is whether this next leg will take place before or after the next recession. Given the rate at which interest rates and oil prices are rising in the face of a slowing global economy, it’s looking like the recession may win the race.

As our tour ended, who did we see having dinner in the front window of one of the city’s leading restaurants? A young woman wearing a white wedding dress.

Yikes! Maybe the recession is sooner than I thought.

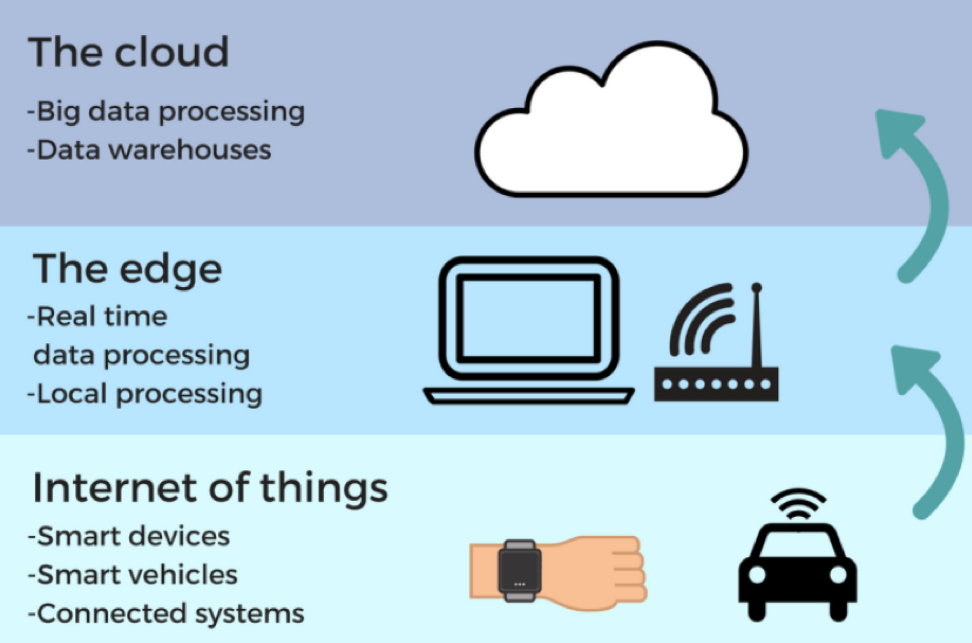

Edge computing is processing data at the edge of your network.

The data being generated will not only occur in a centralized data-processing storage server anymore, but at different decentralized locations closer to the point of data generation.

This is what everyone is talking about and is an epochal development for tech companies and the businesses they run.

The last generation of IT saw a massive migration to the cloud as centralized servers stored the sudden hoard of data that never existed before.

Edge computing bolsters data performance, boosts reliability, and cuts the costs of operating apps by curtailing the distance data must flow which effectively reduces latency and bandwidth headaches.

Edge computing is revolutionizing IT infrastructure as we know it.

No longer will we be forced to use these monolith-like giant server farms for all our data needs.

Epitomizing the Silicon Valley culture of becoming faster and more agile to disrupt, tech infrastructure is getting the same potent cocktail of performance enhancers underlying the same characteristics.

According to research firm Gartner, around 80% of enterprises will shutter legacy data servers by 2025, compared to 10% in 2018.

Keeping the data near the points of data creation is the logical step to enhance and optimize data processes.

Cloud computing depends on superior bandwidth to handle the data load.

This can create a severe bottleneck if bombarded with a heavy dose of devises all communicating with the centralized servers.

The edge computing industry already in the initial stages of ramping up will be worth $6.72 billion by 2022, up from $1.47 billion in 2017.

Underpinning this crucial IT is the imminent inauguration of 5G networks powering IoT devices.

Simply put, the amount of raw data which will need swift processing is about to explode. Relying on a slower, centralized servers is not the solution, and the edge offers a suitable solution to accommodate the new generation of technology.

And as technology starts to permeate every corner of the globe, data will need to be instantaneously processed locally in cutting-edge technology such as self-driving cars.

Waiting on communicating with a centralized server in another continent is just not plausible.

A self-driving car only has milliseconds to react in hazardous conditions.

Other critical and data heavy operations such as wind turbines, medical robots, airplanes, oil rigs, mining vehicles, and logistics infrastructure only function if operated at peak levels and an interruption to connectivity could be fatal.

Telecom companies and IT firms will experience the biggest sea of changes from edge computing in the next five years.

These two sectors are confronting a significant ramp up in network load and will find it challenging to deliver the results to operate the apps and services they are responsible to run.

This new IT technology is the answer.

The industry adopting edge computing the fastest is retail because of the troves of data collected by IoT sensors and cameras.

Companies will be able to analyze the performance of products and edge computing is the technology that will capture the data.

The adoption of edge computing will perfectly take advantage of the boom in IoT devices and uptick of internet speeds through 5G.

Sales of PC’s, tablets, and smartphones have matured, and aren’t seeing the same pop in growth rates like before.

However, the IoT industry will expand by 30% in the next five years boding well for the broad-based integration of edge computing.

In total, the number of connected devices in the next five years will balloon from 17.5 billion in 2017 to over 31 billion in 2023.

The first iteration of 5G IoT devices will be on the market in 2020 deploying industrial process monitoring and control.

This is not a flash in the plan technology and many firms already or are about to roll-out an edge computing strategy.

In a recent report, 72.7% of tech firms already possess a solid edge computing plan or it is in the works.

If you include all the tech firms who expect to invest in edge computing in the next year, the number catapults to 93.3%.

The same survey continued to delve into the mindset of edge computing for tech management by asking about the importance of the technology.

Over 70% of firms characterized edge computing as important, bifurcated into two categories with the first being “critically important” which 22.2% of respondent agreed with.

Another 49.6% of respondent described edge computing as “very important.”

Firms cited that improved application performance is the largest benefit of edge computing followed by real time data analytics and data streaming.

It is not the death of cloud computing yet.

Even though centralized, slower, and negatively affected by long distance, cloud computing still has a place in the future of IT.

About two-thirds of tech firms plan to utilize a hybrid centralized cloud – edge computing strategy.

Even if they did not combine this strategy, companies would most likely separate the operations responsible for two distinct set of tasks filtered by the level of time sensitivity.

The overwhelming and imminent adoption of IoT devices means IT departments are crafting a substantially higher budget for edge computing to satisfy their operational needs.

Large recipients of this technology will turn out to be companies related to manufacturing, smart cities and transportation as well as energy and healthcare.

This technology really cuts across the entire spectrum of global industries.

Data usually does not discriminate, and applications of new tech is fueling a rapid rise of performance optimization that no other sectors can claim.

Let’s do a quick rundown of the edge computing players.

The three cloud behemoths of Amazon Web Services (AWS), Microsoft (MSFT) Azure, and Google (GOOGL) Cloud are constructing edge gateways and edge analytics into their IoT offerings aiding workload distribution across edge and cloud services.

Microsoft has over 300 edge computing patents and launched its Azure IoT Edge service integrating container modules, an edge runtime, and a cloud-based management interface.

Amazon Web Services offers AWS CloudFront content delivery infrastructure and AWS Greengrass IoT service building on the momentum of pioneering centralized cloud technology.

Dell’s IoT division invested $1 billion in R&D to help drive Edge Gateways and VMware's Pulse IoT Center.

Hewlett Packard Enterprise (HPE) devoted $4 billion to its edge network portfolio. HPE operates edge services, mini-data centers, and smart routers.

These are just some of the initiatives from some of the main players in the field.

Expect companies to become a lot more connected while possessing the speed, high performance, and agility to optimally entertain this new-found connectivity.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Cloud-Edge-oct9.png643972MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-09 09:01:022018-10-08 18:06:09Living on the Edge

Pat yourself on the back if you pulled the trigger on Square (SQ) when I told you so because the stock has just lurched over an intra-day level of $100.

It was me aggressively pushing readers into buying this gem of a fin-tech company at $49. To read that story, please click here (you must be logged in to www.madhedgefundtrader.com).

Since then, the price action has defied gravity levitating higher each passing day immune to any ill-effects.

The Teflon-like momentum boils down to the company being at the cross-section of an American fin-tech renaissance and spewing out supremely innovative products.

At first, Square nurtured the business by targeting the low hanging fruit– small and medium size enterprises in dire need of a strong injection of fin-tech infrastructure.

It largely stayed away from the big corporations that adorn billboards across the Manhattan skyline.

That was then, and this is now.

Square is going after the Goliath’s fueling a violent rise in gross payment volume (GPV).

Modifying themselves for larger institutions is the next leg up for Square.

They recently inaugurated Square for Restaurants for larger full-service restaurants.

Business owners do not need technical backgrounds to operate the software and integrating Caviar into this program emphasizes the feed through all of Square’s software.

Dorsey has built an ecosystem that has morphed into a one-stop shop for comprehensively running a business.

Migrating into business with the premium corporations offers an opportunity to augment higher margin business.

This is the lucrative path ahead for Square and why investors are festively lining up at the door to get a piece of the action.

The downside with an uber-growth company like Square are lean profits, but they have managed to eke out three straight quarters of marginal spoils.

However, the absence of profits can be stomached considering the total addressable market is up to $350 billion.

Grabbing a chunk of that would mean profits galore for this too hot to handle company.

Expenses are always a head spinner for Silicon Valley firms and attracting a dazzling array of engineers to spin out breathtaking profits can’t be done on the cheap.

The Cash app download figures are sizzling and is one of the most popular apps in the app store.

Square’s marketing strategy is also turning a corner getting out their name leading to sale conversions.

These are just several irons in the fire.

The last two years has seen this stock double each year, could we be in for another double next year?

If measured by growth, then I see why not.

Growth is the ultimate acid test deciding whether this stock will be dragged down into the quick sand or let loose to run riot.

Other second-tier tech firms in the middle of a sweet growth spot pack a potent punch like Spotify (SPOT) and Grubhub (GRUB) which are growing annual sales around 50-60%.

Material profits are also irrelevant for the aforementioned tech juggernauts.

Square is expanding at the same fervent pace too, and the hyper-growth only makes payment processors like Visa (V) quasi-jealous of such staggering numbers.

And when Square trots out numbers to the public like that with (GPV) shooting out the roof, the stock does nothing but go gangbusters.

Either way, Square has popularized making credit card payments through smartphones and that in itself was a tough nut to crack amongst tough nuts.

Square also has a line-up of impressive point-of-sales products such as Caviar.

In fact, merchant sellers are adopting an average of 3.4 Square software apps with invoices, loans, marketing, and payroll software being the most beloved.

Square also offers other software that can handle back office tasks and manage inventory.

The software and services business is on pace to register over $1 billion in sales in 2019.

The breadth of functions that can boost a company’s execution highlights the quality of software Dorsey has produced.

I always revert back to one key ingredient that all tech companies must wildly indulge in to fire up the stock price – innovation.

Innovation in bucket loads is something all the brilliant tech firms crave such as Microsoft (MSFT), Amazon, and Salesforce (CRM).

Overperformance starts from the top and trickles down to the people they hand pick to manage and run the businesses.

Jack Dorsey is right up there with the best of them and his influence cannot be denied or ignored.

His stewardship over his other company Twitter (TWTR) is sometimes worrisome because of a pure scheduling conflict, but it’s obvious which company is having a better year.

Square steers clear of the privacy and regulatory minefields handcuffing Twitter.

And it could be safely assumed that Dorsey enjoys his afternoons more at Square than his mornings across the street at Twitter where he is bombarded by heinous problems up the wazoo.

When you conjure up an up-and-coming company that could rattle the establishment, Square is one of the first companies that comes to mind.

Some analysts even argue this company deserves to be lifted into the vaunted Fang group.

I would say they are on their merry way but they just aren’t big enough to command a spot on the Fang roster.

I have immense conviction this stock will be a deep influencer of our time, and its diversified software offerings add limitless dimensions underpinning massive revenue streams.

In Q2, the subscription revenue grew 127% YOY underscoring the success the software team is having, crafting productive apps applicable to business owners.

Business owners can even take out a loan through Square Capital which issues micro-loans to small business owners.

In need of financing? Ring up Dorsey’s company for a few quid.

Starkly contrasting Square in the payment processors space is Visa (V).

Visa is not a hyper-growth company going ballistic, but a stoic behemoth unperturbed.

The 3.283 billion visa cards that adorn its insignia represents scintillating brand awareness and efficiency.

When Tim Cook was asked if Apple (AAPL) plans to disrupt Visa, he smirked and said, “People love their credit cards.”

This is a prototypical steady as she goes-type of company.

They do not offer micro-loans to small businesses or dabble with any of the murky sort of products that can be found on the edge of the risk curve.

They are a safe and steady pure payment processor.

Its network can digest 65,000 transactions per second and is universally cherished as a brand around the world.

All of this led to an operating margin of 66% in 2017.

Square has identified other parts of the payment process to snatch and do not directly compete with Visa.

They partner with Visa and pay them a processing fee.

Subsequently, Square is paid a merchant fee after the payment is approved.

Visa has a monopoly and a moat around their business as wide as can be.

Square is a different type of beast – growing uncontrollably and hell-bent on spawning a revolutionary fin-tech paradigm shift.

The question is can Square eventually turn payment heavyweights like Visa on its head?

The path is fraught with booby traps and as Square generates the projected sales and bolsters its revenue, it could start to encroach on these legacy processors too.

Yet, it’s too early to delve into that threat yet.

Enjoy the ride with Square and better to lay off this potent stock until a better entry point presents itself.

This stock will go higher. Giddy-up!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-03 09:01:422018-10-03 08:59:28Our Home Run On Square (SQ)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.