Featured Trade:

(WHY THE DOW IS GOING TO 120,000),

(X), (IBM), (GM), (MSFT), (INTC), (DELL), ($INDU), (NFLX), (AMZN), (AAPL), (GOOGL),

(THE MAD HEDGE CONCIERGE SERVICE HAS AN OPENING),

(TESTIMONIAL)

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

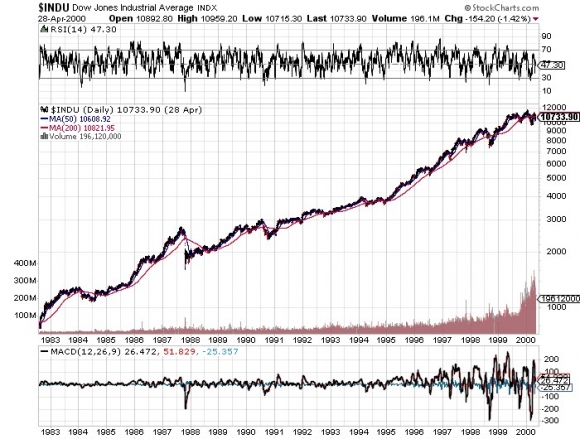

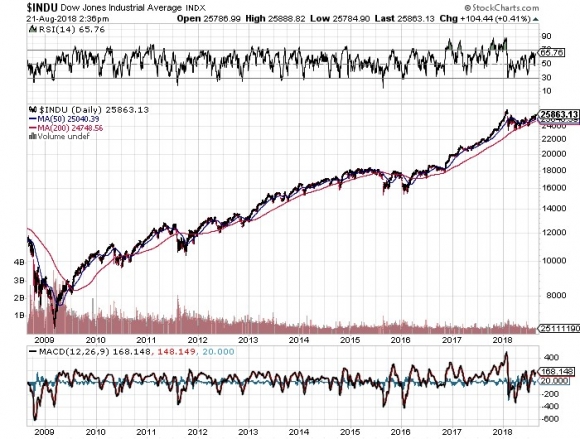

How high are we talking? How about a Dow Average of 120,000 by 2030, up another 465% from here? That is a 20-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion in corporate stock buybacks.

I’m not talking pie in the sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000 the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my Dad’s generation that meant loading your portfolio with U.S. Steel (X), IBM (IBM), and General Motors (GM).

For my generation that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on Netflix (NFLX), Amazon (AMZN), Apple (AAPL), and Alphabet (GOOGL).

That’s why these four stocks account for some 40% of this year’s 7% gain. Oh yes, and they bought a few Bitcoin along the way too, to their eternal grief.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 120,000 in 2030 we need to squeeze in a recession. That is increasingly becoming a topic of market discussion.

The consensus now is that an impending inverted yield curve will force a recession sometime between August 2019 to August 2020. Throwing fat on the fire will be a one-time only tax break and deficit spending that burns out sometime in 2019. These will be a major factor in U.S. corporate earnings growth dramatically slowing down from 26% today to 5% next year.

Bear markets in stocks historically precede recessions by an average of seven months so that puts the next peak in top prices taking place between February 2019 to February 2020.

When I get a better read on precise dates and market levels, you’ll be the first to know.

To read my full research piece on the topic please click here to read “Get Ready for the Coming Golden Age.”

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/John-on-mechanical-bull-story-1-image-3-e1534972073238.jpg313250MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-23 01:08:052018-08-22 21:23:50Why the Dow is Going to 120,000

Mad Hedge Technology Letter August 22, 2018 Fiat Lux

Featured Trade: (WHAT’S IN STORE FOR TECH IN THE SECOND HALF OF 2018?), (GOOGL), (AMZN), (FB), (UTX), (UBER), (LYFT), (MSFT), (MU), (NVDA), (AAPL), (SMH)

Tech margins could be under pressure the second half of the year as headwinds from a multitude of sides could crimp profitability.

It has truly been a year to remember for the tech sector with companies enjoying all-time high probability and revenue.

The tech industries’ best of breed are surpassing and approaching the trillion-dollar valuation mark highlighting the potency of these unstoppable businesses.

Sadly, it can’t go on forever and periods of rest are needed to consolidate before shares relaunch to higher highs.

This could shift the narrative from the global trade war, which is perceived as the biggest risk to the current tech market to a domestic growth issue.

Healthy revenue beats and margin growth have been essential pillars in an era of easy money, non-existent tech regulation, and insatiable demand for everything tech.

Tech has enjoyed this nine-year bull market dominating other industries and taking over the S&P on a relative basis.

The lion’s share of growth in the overall market, by and large, has been derived from the tech sector, namely the most powerful names in Silicon Valley.

Late-stage bull markets are fraught with canaries in the coal mine offering clues for the short-term future.

Therefore, it is a good time to reassess the market risks going forward as we stampede into the tail end of the financial year.

The shortage of Silicon Valley workers is not a new phenomenon, but the dearth of talent is going from bad to worse.

Proof can be found in the controversial H-1B visa program used to hire foreign tech workers mainly to Silicon Valley.

A few examples are Alphabet (GOOGL), which was granted 1,213 H-1B approvals in 2017, a 31% YOY rise.

Alphabet’s competitor Facebook (FB) based in Menlo Park, Calif., was granted 720 H-1B approvals in 2017, a 53% YOY jump from 2016.

This lottery-based visa for highly skilled foreign workers underscores the difficulty in finding local American talent suitable for a role at one of these tech stalwarts.

Amazon (AMZN) made one of the biggest jumps in H-1B approvals with 2,515 in 2017, a 78% YOY surge.

The vote of non-confidence in hiring Americans shines an ugly light on American youth who are not applying themselves to the domestic higher education system as are foreigners.

For the lucky ones that do make it into the hallways of Silicon Valley, a great salary is waiting for them as they walk through the front door.

Reportedly, the average salary at Facebook is about $250,000 and Alphabet workers take home around $200,000 now.

Pay packages will continue to rise in Silicon Valley as tech companies vie for the same talent pool and have boatloads of capital to wield to hire them.

This is terrible for margins as wages are the costliest input to operate tech companies.

United Technologies Corp. (UTX) chief executive Gregory Hayes chimed in citing a horrid “labor shortage in the U.S. and in Europe.”

He followed that up by saying the company will have to grapple with this additional cost pressure.

Certain commodity prices are spiraling out of control and will dampen profits for some tech companies.

Uber and Lyft, ridesharing app companies, are sensitive to the price of oil, and a spike could hurt the attractiveness to recruit potential drivers.

The perpetually volatile oil market has been trending higher since January, from $47 per barrel and another spike could damage Uber’s path to its IPO next year.

Will Uber be able to lure drivers into its ecosystem if $100 per barrel becomes the new normal?

Probably not unless every potential driver rolls around in a Toyota Prius.

If oil slides because of a global recession instigated by the current administration aim to rein in trade partners, then Uber will be hard hit abroad because it boasts major operations in many foreign megacities.

A recession means less spending on Uber.

Either result will be negative for Uber and ridesharing companies won’t be the only companies to be hit.

Other victims will be tech companies incorporating transport as part of their business model, such as Amazon which will have to pass on more delivery costs to the customer or absorb the blows themselves.

Logistics is a massive expense for them transporting goods to and from fulfillment centers. And they have a freshly integrated Whole Foods business offering two-hour free delivery.

Higher transport costs will bite into the bottom line, which is always a contentious issue for Amazon shareholders.

Another red flag is the deceleration of the global smartphone market evident in the lackluster Samsung earnings reflecting a massive loss of market share to Chinese foes who will tear apart profit margins.

Even though Samsung has a stranglehold on the chip market, mobile shipments have fell off a cliff.

Damaging market share loss to Chinese smartphone makers Xiaomi and Huawei are undercutting Samsung products. Chinese companies offer better value for money and are scoring big in the emerging world where incomes are lower making Chinese phones more viable.

The same trend is happening to Samsung’s screen business and there could be no way back competing against cheaper, lower quality but good enough Chinese imitations.

Pouring gasoline on the fire is the Chinese investigation charging Micron (MU), SK Hynix, and Samsung for colluding together to prop up chip prices.

These three companies control more than 90% of the global DRAM chip market and China is its biggest customer.

The golden days are over for smartphone growth as customers are not flooding into stores to buy incremental improvements on new models.

Customers are staying away.

The smartphone market is turning into the American used car market with people holding on to their models longer and only upgrading if it makes practical sense.

Chinese smartphone makers will continue to grab global smartphone market share with their cheaper premium versions that western companies rather avoid.

Battling against Chinese companies almost always means slashing margins to the bone and highlights the importance of companies such as Apple (AAPL), which are great innovators and produce the best of the best justifying lofty pricing.

The stagnating smartphone market will hurt chip and component company revenues that have already been hit by the protectionist measures from the trade war.

They could turn into political bargaining chips and short-term pressures will slam these stocks.

This quarter’s earnings season has seen a slew of weak guidance from Facebook, Nvidia (NVDA) mixed in with great numbers from Alphabet and Amazon.

Beating these soaring estimates is not a guarantee anymore as we move into the latter part of the year.

Migrating into the highest quality names such as Amazon and Microsoft (MSFT) with bulletproof revenue drivers would be the sensible strategy if tech’s lofty valuations do not scare you off.

Tech has had its own cake and ate it too for years. But on the near horizon, overdelivering on earnings results will be an arduous chore if outside pressures do not relent.

It’s been fashionable in the past for market insiders to call the top of the tech market, but precisely calling the top is impossible.

The long-term tech story is still intact but be prepared for short-term turbulence.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-22 03:05:032018-08-22 06:23:58What’s in Store for Tech in the Second Half of 2018?

Each generation grows up in its own unique environment.

Childhood experiences differ more and more as the world rapidly changes because of hyper-accelerating technology.

Millennials are usually defined as children born between 1981 to 1996.

They were the last generation to grow up outside breathing crisp, fresh air and meandering around the neighborhood with their friends looking for excitement.

Generation Z is the first generation in America generally raised indoors because of their overwhelming preference and broad-based addiction to technology.

Social media stocks have been a huge winner from this new paradigm shift in the behavior of young adults.

Instead of running around the block in packs, children are laser focused on these platforms communicating with the entire world and propping up their social lives.

Children meet a lot less than they used to and convening on a social media platform of choice has become the new normal.

Platforms such as Twitter (TWTR), Instagram and Snapchat (SNAP) have convincingly won over these new eyeballs even so much so that the new "going out" is congregating on Snapchat with a group of friends.

Facebook (FB) is now considered a legacy social media platform full of millennials and the older crowd.

Generation Z do not fancy drugs or drinking like the youth before them, rather, their panacea is video games and a lot of them.

These new societal trends will hugely affect your portfolio going forward.

A battle royal game is a video game category mixing the survival, exploration and scavenging elements together with last-man-standing gameplay.

These types of games predominantly contain 100 players sharing the same experience on a broadband connection.

This genre has been all the rage with PlayerUnknown's Battlegrounds (PUBG) piling up 400 million gamers across the globe selling 50 million copies of the game.

Of the 400 million gamers, 88% access the game via mobile devices highlighting the vigorous shift to mobile for younger generations.

PUBG made more than $700 million in sales in 2017.

The rise of the billion-dollar video games is alive and well.

In fact, Activision Blizzard (ATVI) stakes claim to eight gaming franchises commanding more than $1 billion in annual revenue with titles such as Overwatch, Candy Crush, and Call of Duty.

The popularity of video games will drive GPU manufacturers Nvidia (NVDA) and AMD (AMD) to new heights because gamers require high-quality GPUs to effectively game.

Nvidia CEO Jensen Huang even spouted that "the success of Fortnite and PUBG are just beyond comprehension" boosting GPU sales and capturing the imagination of global youth.

Fortnite, a "Hunger Games" style battle royal video game mirroring PUBG, has taken the world by storm in 2018.

This cultural juggernaut surpassed the 125 million gamer mark in just one year.

In February 2018, Epic Games, the maker of Fortnite, earned $126 million in one month, and it was the first time it passed PUBG in monthly sales.

In April 2018, it followed up monster February numbers by pulling in $296 million.

The growth trajectory is parabolic. Hold onto your hats.

Fortnite sparkles in the sunlight because its free-to-play model does not exclude anyone and is available on all devices.

At first, Fortnite was available for iOS customers and Samsung Android holders because it inked an exclusive deal with Samsung.

This week is the first week Epic Games is rolling out Fortnite to non-Samsung Android users with an interesting caveat.

The Android version of Fortnite bypasses Google Play (Google's app store on Android) preferring to sell the game direct for download from its official website.

This highlights that content is truly king.

Epic Games is betting the surge in popularity for its juggernaut game will sell itself.

This decision will cost Alphabet (GOOGL) $70 million per year in commission.

Apple makes it mandatory that any app downloaded to its devices must be downloaded from Apple's app store.

However, Android doesn't have the same requirements as its system is more functional, open, and a developer's dream.

Simply put, there are ways to download the game on Android without ever touching Google Play.

Going forward this could have a similar effect Spotify (SPOT) had on Wall Street on its IPO.

The middlemen or broker app could get bypassed in favor of direct sales.

Apple pockets commission on 30% of all in-app spending raking in around $60 million from Fortnite.

In-game add-on revenue is how Fortnite makes money from this free-to-play game.

The bulk of spending comes in the form of costumes better known as skins, where players pay to dress up their character in various garments selected for purchase.

The other revenue stream is a season subscription on sale for $10.

The tech sector has been migrating to subscription-based offerings and video games are no different.

This could play havoc with Alphabet's Google Play and Apple's app store down the line if prominent content producers choose to bypass their stores to sell directly.

The lack of video game exposure to the FANG group is mind-boggling. It seems they have their finger on the pulse of every other major trend in technology but have missed out on this one.

Microsoft (MSFT) is the closest FANG-like stock deep inside the video game ecosphere by way of its famous console Xbox.

In fact, Microsoft earns more than $10 billion per year from its gaming segment surpassing Nintendo at $9.7 billion per year.

This doesn't eclipse Sony's gaming revenue, which is $17 billion per year, but the 36% YOY growth in Xbox-related revenue signals its intent in the gaming industry that plays second fiddle to its cloud and software businesses.

Gaming is just a side business for Microsoft right now.

Ironically, Tencent has a 40% stake in Epic Games and is patiently waiting for government approval to sell Fortnite in China, which could be painstakingly arduous.

If Tencent gets the green light, Fortnite could develop into a monster business in 2018, and this is just the beginning.

Regrettably, Tencent has been mired in regulatory issues with the communist government reluctant to approve selling in-game products, which usually make up the bulk of revenue.

Recent blockbuster hit "Monster Hunter: World" was blocked by censors after debuting to great fanfare on August 8, 2018.

This title was expected to be one of the most popular video games of 2018.

Chinese state censors are on a short-term crusade to block the video game industry from receiving critical licenses and is the main reason for Tencent shares' headwinds.

Tencent shares peaked in January and are down almost 15% in 2018 because of uncertain gaming revenues.

Investors need to wake up and understand the gaming industry is about to mushroom because of demographics and the migration away from outdoor activity.

Following generations will have an even stronger bias toward technology-based indoor entertainment.

We are entering into the unknown of $4 billion per year video game businesses based on just one title and not one company.

Fortnite made PUBG's $700 million in revenue last year look paltry.

Gamers will soon see the rise of a $5 billion game franchise in 2019 and the sky is the limit.

This industry has growth, growth, and more growth and these single titles could surpass revenue of large semiconductor or hardware companies.

Don't underestimate the power of your child gaming away in your basement, he or she is part and parcel of a wicked tech growth driver about which not many people know.

Unfortunately, Epic Games is not a public company and shares cannot be purchased, but the success of Fortnite means that investors must pay heed to these new developments.

I am highly bullish on the video game sector and a big proponent of Activision (ATVI). A secondary name would be EA Sports (EA), which curates the Madden and FIFA franchises.

ATVI has felt the Fortnite effect in its share price selling off 11% because of investors' nervousness of Fortnite siphoning off ATVI gamers.

This short-term drop is a nice entry point into a solid video gaming company with various successful franchises that have withstood the test of time.

The 200-day moving average has provided ironclad support on the way up, and the Fortnite phenomenon won't last forever.

I would avoid the video game ETF ticker symbol GAMR because it includes one of my bona fide shorts - GameStop (GME).

It's mainly comprised of American, Japanese, and a Korean name but it would be sensible to focus on the companies with the highest quality comprehensive content.

The ETFs recent drop is also due to the strength of Fortnite.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-15 01:05:372018-08-15 01:05:37How to Play the New Fortnite Gaming Fad

Recently, a series of big tech earnings misses throttled the market tearing into the positive investor sentiment, which was holding up nicely after the early year sell-offs.

Every precipitous and steep drop this year has followed with a mammoth dip buying spree lifting stocks to newer highs.

This is the type of robustness investors rejoice in when talking about the price action of technology stocks.

Not only is the dip buying awe-inspiring, but the lack of hesitation in the dip buying is even more impressive.

Investors have scant time to pick up these precious names before the entry points disappear like an invisibility cloak.

Ditch these stocks at your peril, because the buying queue represents the likes of all the tech behemoths waiting to buy back their own stock, namely Warren Buffett, and the flight to quality brigade that view big cap stocks as a de-facto cash sanctuary.

The anxiety was palpable when Netflix's (NFLX) management badly miscalculated new subscription business after a brilliant earnings report from Microsoft.

Investors got another wrench in their stomach when Facebook (FB) followed Netflix with dismal guidance ripping apart the growth narrative and pivoting toward ameliorating its controversial business model giving investors a fresh dose of uncertainty.

All eyes were planted on Alphabet (GOOGL), Amazon (AMZN), and Apple to provide some calm to the markets.

That's exactly what they did.

Part of the problem now is that expectations are so exaggerated, these companies have little wiggle room to overdeliver.

Industry specialists largely believe tech profits to rise 20.9% YOY this earnings season. The lion's share of the growth has been contained to the headliner names such as Amazon, which has grown like no company has ever grown before.

Estimates show a slide in YOY tech profits for the third-quarter earnings decelerating down to less than 15%. While still good, it's not the 20% growth YOY, and over that it has been fueling tech's rise in increasingly precarious market conditions.

The downshift in profit growth has been anticipated for the past few quarters, as investors thought a trip wire would at some point bring down the entire FANG group.

What we have found out is that not all FANGs are created equal. Some are more equal than others.

The past earnings performance indicated this with Amazon's emphatic top-line growth numbers blowing away the most adamant bear.

Netflix's narrative is still intact, and consolidation is badly needed for a stock that has gone parabolic in 2018.

The short-term capitulation of Facebook and Netflix is proof that large cap tech also has downside risk embedded in its model.

It was starting to seem like down days were never in the cards.

Lowered tech guidance for next quarter will really test the market's resiliency during next earnings season.

If these numbers miss spectacularly, expect the tech sector to give back a good chunk of the year's gains back.

Decelerating profits is never a positive sign. However, after coming from Mt. Everest profit levels, will the markets brush it off and power higher?

There is a lot more juice left in this tech story, and sharp corrections should still be bought.

Tech is becoming quite frothy at these levels and choosing the right tech story will go a long way to sleeping well at night.

It will be excruciatingly difficult for tech companies to impressively beat on the upside next quarter.

However, the secular story and unique earnings growth are treasures compared to other sectors that are getting beaten into submission.

When you delve into the numbers, the success becomes comical.

Apple is the first company to cross the $1 trillion of market cap.

This company prints money to the tune of $11 billion in profits each quarter.

It possesses a devoted userbase, surging software and services segment, and premium grade smartphones allowing Apple to cash in profits to the extent they do.

CEO Tim Cook sent an email to Apple's employees downplaying the milestone, instead saying "financial returns are simply the result of Apple's innovation."

He is completely correct.

The innovation has fed back through spiking profits and boosting sales allowing Apple to make money hand over fist.

This in turn is a big reason why Apple's share price has almost quadrupled with Cook at the helm.

The best and brightest tech companies in 2018 share one unified trait: innovation.

And it is not a surprise that Amazon and Microsoft (MSFT) will be next to join the trillion-dollar club as they boast some of the most innovative staff in the world.

As these two companies pass the trillion-dollar market cap, it will encourage the next tier of flourishing tech companies to make the jump to the trillion-dollar club.

The tech sector is still eating everybody's lunch with every business in the world migrating to their front yard.

Some weakness in the extended tech shares have been a matter of when and not if.

Advanced Micro Devices, Inc. (AMD) is a stock gaining 22.8% just in the month of July underlining the overheated price action of some of these tech names.

I am largely staying away from chip stocks now because trade tensions have bred uncertainty around Chinese chip revenues.

The tech sector has many moving parts and a trade war can hurt one part of tech while others remain unblemished.

Another front of concern is data regulation headlines rearing their ugly heads from time to time.

There are more hurdles for tech stocks going forward, but that does not mean they will get tripped up.

I am in a tech holding pattern until I find an opening to issue my next slew of tech trade alerts.

"I will always choose a lazy person to do a difficult job because a lazy person will find an easy way to do it." - said founder of Microsoft Corporation Bill Gates.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-07 01:05:352018-08-07 01:05:35What to Do About Tech Now?

Apple (AAPL) is the first company in America to have a trillion-dollar market cap and won't be the last as Amazon (AMZN) is close behind.

This also opens up the door for one of our favorite companies Microsoft (MSFT), which will shortly cross the $1 trillion threshold as well.

The milestone underscores the reliability and power of the tech sector that has propped up this entire market in 2018 as we continue the late stage cycle of the nine-year bull market.

Apple has entered into a hyper-charged expansion phase, and I will explain how this will boost shares to new heights.

The Mad Hedge Technology Letter has been hammering away on the software and services narrative since its inception.

As legacy companies are pummeled in the financial markets, the cloud has enabled a revolutionary industry catering toward annual subscriptions of all types.

Users no longer have to store gobs of data on computers. The cloud allows the data to be stored on remote data servers giving access to the information from anywhere in the world with an Internet connection.

A plethora of modern hybrid apps boosting productivity integrated with the cloud offers business a new-found way to collaborate with coworkers around this increasingly multicultural, multilingual, and globalized world.

Apple is perfectly placed to take advantage of the current technology climate and will wean itself from the image of being a hardware company.

Investors wholeheartedly approve of the conscious move to bet the farm on service and subscriptions.

After Apple's earnings came out, the stock traded up whereas in past quarters, the total sales unit was the crucial number investors hung their hat on and the stock would dip.

Apple missed iPhone total sale units registering 41.3 million compared to the expected 41.79 million units.

This slight miss in the past was enough for the stock to sell off on and instead the stock rose 3%.

This is the new Apple.

A software services company.

Investors can feel at peace that iPhone sales aren't growing. It's not that important anymore.

Apple's software and services segment pocketed $9.55 billion in revenue, a 31% jump YOY from $7.27 billion.

This has been in the making for a while as software and services has been a five-star performer for the past few quarters.

However, the performance is material now and the pace of improvement will take Apple into the next phase of hyper-growth.

This is all good news for the stock price.

Software and services revenue now comprise 17.9% of Apple's total revenue.

By year-end, this division could topple the 25% mark.

In the earnings call, Apple CEO Tim Cook was smitten with the software and services growth saying this particular revenue will double by 2020.

In the next few years, software and services will eclipse the 40% mark, all made possible inside an incredibly sticky and top-quality ecosystem.

The iPhone continues to be the best smartphone the market has to offer. If you marry the best hardware with top-quality software, this stock will chug along to higher share prices unhindered.

As the technology sector matures, the flight to quality becomes even more glaring.

The inferior platforms will be found out quickly heightening the risk of massive intraday sell-offs and revenue-depleting penalties.

Facebook and Twitter have seen 20% sell-offs hitting investors in the mouth.

These platforms have issues rooting out the nefarious elements that seek to infiltrate its operations and manipulate the platform for self-serving interests.

Apple does not have this problem. Neither does Microsoft, Amazon, Netflix (NFLX) or Salesforce (CRM), and I will explain why.

When you offer services for free such as Facebook (FB) and Twitter (TWTR) do, you get the good, bad, and ugly bombarding the system.

Even though it's free to use these platforms, Facebook and Twitter must spend to make it useable for the good forces that made these companies into tech behemoths.

Instead of rooting out these rogue elements, they turned a blind eye describing their businesses as a distribution system and were not accountable.

Then sooner or later one of the evil elements would get these companies in hot water. It happened.

Big mistake, and the chickens are coming home to roost.

The flight to quality means avoiding public tech companies that only offer free services.

You pay for what you get.

Alphabet also has seen its free model penalized twice in Europe with hefty fines, and it probably won't be the last time.

Play with fire and you get burned.

It also offers Cook the moral high road, allowing him to non-stop criticize the low-quality platform companies, mainly Facebook, because it makes the whole tech sector look bad.

The bite back against technology in 2018 is largely in part due to these low-quality free platforms manipulating user data to ring in the profits.

Amazon has been public enemy No. 1 for the Washington administration but not to the public because the loathing of Amazon is largely a personal issue.

Amazon improves the lives of customers by giving users the best prices on the planet through its comprehensive e-commerce business.

Apple now constitutes 4% of the S&P 500 index.

Investors have been waiting for Apple's Cook to sweep them off their feet with the "next big thing."

Even though nearly not as sleek and sexy as a smartphone, the software and services unit are it.

Apple doubling down on high quality that I keep mumbling about shows up in average selling price (ASP) of the iPhone, which destroyed estimates of $694, coming in at $724 per unit.

The bump in (ASP) signals the high demand for its higher-end iPhone X model over the lower-tiered premium smartphones.

The iPhone X is the best-selling iPhone model because customers want the best on the market and will pay up.

The success of the iPhone X lays the pathway for Apple to introduce an even more expensive smartphone in the future with better functionality and performance.

If Apple can continue innovating and producing the best smartphone in the world, the price increases are justified, and demand will not suffer.

Perusing through some other parts of the earnings report, cloud revenue was up 50% YOY.

Apple pay has tripled in the volume of transactions YOY surpassing the billion-transaction mark.

China revenue has stayed solid even with the mounting trade tension. I have oftentimes repeated myself in this letter that Apple is untouchable in China because it provides more than 4 million jobs to local Chinese directly and indirectly through Apple's ecosystem.

This prognosis was proved correct when Apple announced revenue in China of $9.55 billion, a spike of 19% YOY.

Even though much of Apple's supply chain remains in China, Beijing isn't going to take a hammer and smash it up risking massive social upheaval and public fallout. In many ways, Apple is an American company masquerading as a Chinese one.

As for the stock price, the explosion to more than $208 means that Apple is overbought in the short term.

If this stock dips back to $200, it would serve as a reasonable entry point into this record-breaking hyper-growth software and services company.

And with the $234 billion in cash planned to be deployed in Apple's capital reallocation plan, the biggest hurdle is the federal daily limit Apple has in buying back its own stock according to Apple CFO Luca Maestri.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-06 01:05:352018-08-06 01:05:35Next Stop is $2 Trillion

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.