Global Market Comments

September 11, 2018

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS,

OR OPTIONS CALLED AWAY), (MSFT),

(TEN MORE REASONS WHY BONDS WON’T CRASH),

(TLT), (TBT), (ELD), (MUB)

Global Market Comments

September 11, 2018

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS,

OR OPTIONS CALLED AWAY), (MSFT),

(TEN MORE REASONS WHY BONDS WON’T CRASH),

(TLT), (TBT), (ELD), (MUB)

Mad Hedge Technology Letter

September 10, 2018

Fiat Lux

Featured Trade:

(GOOGLE’S BREAKFAST OF ROTTEN EGGS),

(TWTR), (FB), (GOOGL), (MSFT), (AMZN)

In a recent interview Google CEO Sundar Pichai admitted he is “not a morning person” and maybe that was his argument for skipping out on the grilling that his contemporaries Facebook (FB) COO Sheryl Sandberg and CEO of Twitter (TWTR) Jack Dorsey received in front of Congress.

Or maybe Pichai managed to down a rotten egg that morning when eating his favorite staple breakfast “omelet with toast," because his decision to abort his date with Congress was a shocking error of judgment for a CEO that has had a flair for controversy lately.

With the whole world watching, the empty chair with a simple name tag with Google plastered over it represents the arrogance and excesses of Silicon Valley all mixed into one incongruous mixture.

This rookie move will open a can of worms for the company made famous by its search algorithm that dominates the developed world.

Google will have a target on its back going forward while creating a massive public relations backlash for a company that must fiercely defend its ad-laden profit engine going forward.

Instead of taking it on the chin like Facebook and Twitter, Google has voluntarily veered into a sticky situation, and all to avoid a few stomach wrenching questions from Congress.

How did this all happen?

In the beginning of June, Google decided to scrap its relationship with the U.S. Department of Defense.

Project Maven, as it was known, provided Google’s artificial intelligence (A.I.) technology to systematically analyze drone footage for the U.S. government.

Pichai chose to avoid renewing the contract, and Google Cloud CEO Diane Greene agreed it was a black eye for the company that applied its own technology to conspire against damaging human life.

Throwing fat on the fire, Pichai followed up by dismantling Project Maven and giving the thumbs up for code-name Dragonfly. This was a secret project aimed at the mainland Chinese market and rolling out a censored version of Google’s search engine by altering its construction of unique search algorithms for a mainland Chinese audience.

This incensed the higher-ups on Capitol Hill, as this move was largely viewed as pandering toward the Chinese communist government for monetary purposes at an uber-sensitive time between the two powerhouse nations, which remain mired in a tumultuous trade war.

The timing couldn’t be worse for Pichai.

Dragonfly is already in beta mode and could be rolled out in the near future. However, I see it as dead on arrival, because there is no hope that Google can penetrate the fortress that is the Chinese business world.

Naturally, Google employees were dismayed and shocked by these startling revelations.

Pichai’s conspicuous no-show was in part driven by the potential wrath he would have faced by these recent reckless decisions that seemed to put the American government’s interests below the Chinese communist government.

The circus was there for everyone to see.

Sheryl Sandberg put on her bravest face.

It was obvious she had rehearsed every word to the utmost precision while Dorsey vehemently guarded his brainchild with honesty and zeal.

The testimonies made social media look perceivably criminal with a congressman even hinting the reason they aren’t allowed to do business in China was mainly a business model issue, and more specifically a legal issue.

Another congressman from West Virginia suggested Facebook’s Instagram was the source of the opioid epidemic ripping apart his state.

The only thing getting ripped apart during the intense grilling was Sheryl Sandberg’s well-practiced smile.

Dorsey and Sandberg were visibly uncomfortable with the line of questioning and rightly so.

Google would have looked worse if it showed up. But it managed to look 10 times worse than that by stonewalling the government’s invitation.

In a recent Pew Survey, data revealed 44% of youth between 18 to 29 last year deleted Facebook on their mobile phones.

Facebook is already a legacy platform in the throes of disruption cannibalized by its own asset - Instagram.

Instagram will be the sole survivor of Facebook by taking out Facebook itself, and that is bearish for overall business.

And that is if social media can hang on that long before it’s taken down by the hawks circling above in Washington.

When Facebook’s Cambridge Analytica scandal broke, the government was at sixes and sevens at attempting to figure out what on earth was going on behind the smoke and mirrors of the big data theatrics.

CEO Mark Zuckerberg was let off the hook with questions he wriggled out of, and Facebook shares powered on unabated.

This time it’s different.

Regulation is an imminent threat to social media revenues and could hurt earnings this quarter.

Investors need to migrate to higher tide, meaning Amazon (AMZN) and Microsoft (MSFT), because the waves still aren’t yet reaching those levels.

Amazon and Microsoft need to send a thank you note to Alphabet for screwing the pooch.

The administration has felt it convenient to barrage Silicon Valley to solidify the Republican base, and this tactic has resonated with the administration’s diehards.

A smorgasbord of FANG-bashing was the recipe to this madness. But now sights will be zoned in on dismantling Google, and Microsoft and Amazon will benefit from avoiding nasty, gut-churning headlines that turn up in the form of Twitter blitzkrieg.

Yes, Sheryl Sandberg, Facebook was “too slow” to react to foreign interference in the elections. But it is more accurate to characterize the battle social media faces against outside nefarious forces as impossible.

It is impossible for these social media platforms to police themselves while policing the whole world.

The incessant whack-a-mole scenario is the best-case outcome for the self-policing prospects of social media.

Once social media algorithms figure out how to stopgap one method of circumvention, the bad actors will move on to a more advanced way to manipulate the algorithmic police.

What does this mean for social media?

Costs are going up and will seep into profit margins.

Highlighting the upward trend of rising expenses for social media platforms is the daily cost of keeping CEO Mark Zuckerberg safe.

And remember, he lives in Palo Alto, California, one of the safest places on planet earth with a medium household income of $137,000.

In 2017, Facebook divvied up $7.3 million for Zuckerberg’s security detail and costs associated to it.

In 2018, shareholders approved a $10 million security package to keep Facebook’s head honcho safe. This underscored the ballooning risk of leading this controversial technology forum littered with conflict of interests, and on the verge of potentially perverting western democracy.

By the end of 2018, Facebook will increase its security division from 10,000 employees to 20,000.

And that is just the beginning.

Facebook’s security division is the fastest-growing division of fresh hires at Facebook.

Before Facebook and Twitter can ring in the profits, they face an exorbitant war against foreign “bot armies” intent on muddying the free flow of accurate information on domestic shores that target individuals deemed unaligned to the foreign actor’s interests.

There will be collateral damage and lots of it.

This does not sound like an easy road to profits, and it is not.

As midterm elections creep closer and closer, Facebook and Twitter must confront elevated headline risk, and any trading day could see shares wacked with a 10% haircut.

Following the government question-and-answer period, Twitter and Facebook will be designing a new resistance to stymie villainous foreign infiltration.

Ultimately, spending the bulk of employees’ work days realigning their business models to protect democracy, instead of creating new growth drivers, is not bullish for the stock price.

It is hard to breed much confidence in social media stock’s long-term narrative after listening to Dorsey and Sandberg speak.

They kept touching on needing help from government intelligence sources to aid them in catching the miscreants.

It makes sense to gradually nationalize social media platforms to unite the disconnect between social media’s war against foreign forces and the intelligence communities war against them.

It is clear hackers are exploiting the dislocation in cohesiveness between the cracks in social media and government intelligence.

But if that ever happens, it would be the end of Facebook and Twitter as we know it, as normal users would be averse to providing free content on a government-enabled platform as well as a strong blow to democracy itself.

It all makes sense now why Dorsey and Sandberg gave the answers they gave.

Their answers were akin to a faint plea for help while appearing contrite, hoping to persuade Congress to give them more time to figure it out.

This thinly veiled attempt to elongate the profit-making process and find a solution for a problem with no solution could end badly for these two companies.

Migrate to higher quality tech names in the short-term.

The resilient American economy powers on with the heavy lifting done by Silicon Valley albeit it with fewer lifters.

If social media stocks can get through the midterm elections unscathed, there is a trade on the table for these beleaguered companies rounding out a tumultuous year.

But getting to that point will be volatile, as this group of stocks have a rocky road ahead of them for the rest of the year.

________________________________________________________________________________________________

Quote of the Day

“I'm not a regular smoker of weed. Almost never,” – said CEO of Tesla Elon Musk on The Joe Rogan Experience podcast.

Global Market Comments

September 7, 2018

Fiat Lux

Featured Trade:

(MONDAY, OCTOBER 15, 2018, ATLANTA, GA,

GLOBAL STRATEGY LUNCHEON),

(SEPTEMBER 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(AMZN), (MU), (MSFT), (LRCX), (GOOGL), (TSLA),

(TBT), (EEM), (PIN), (VXX), (VIX), (JNK), (HYG), (AAPL)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 5 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Do you think the collapse of commodity prices in the U.S. will affect the U.S. election?

A: Absolutely, it will if you count agricultural products as commodities, which they are. We have thousands of subscribers in the Midwest and many are farmers up to their eyeballs in corn, wheat, and soybeans. It won’t swing the entire farm vote to the Democratic party because a lot of farmers are simply lifetime Republicans, but it will chip away at the edges. So, instead of winning some of these states by 15 points, they may win by 5 or 3 or 1, or not at all. That’s what all of the by-elections have told us so far.

Q: What will be the first company to go to 2 trillion?

A: Amazon, for sure (AMZN). They have so many major business lines that are now growing gangbusters; I think they will be the first to double again from here. After having doubled twice within the last three years, it would really just be a continuation of the existing trend, except now we can see the business lines that will actually take Amazon to a much bigger company.

Q: Is this a good entry point for Micron Technology (MU)?

A: No, the good entry point was in the middle of August. We are at an absolute double bottom here. Wait for the tech washout to burn out before considering a re-entry. Also, you want to buy Micron the day before the trade war with China ends, since it is far and away its largest customer.

Q: Is Micron Technology a value trap?

A: Absolutely not, this is a high growth stock. A value trap is a term that typically applies to low price, low book to value, low earning or money losing companies in the hope of a turnaround.

Q: I didn’t get the Microsoft (MSFT) call spread when the alert went out — should I add it on here?

A: No, I am generally risk-averse this month; let’s wait for that 4% correction in the main market before we consider putting any kind of longs on, especially in technology stocks which have had great runs.

Q: How do you see Lam Research (LRCX)?

A: Long term it’s another double. The demand from China to build out their own semiconductor industry is exponential. Short term, it’s a victim of the China trade war. So, I would hold back for now, or take short-term profits.

Q: Is this a good entry point for Google (GOOGL)?

A: No, wait for a better sell-off. Again, it’s the main market influencing my risk aversion, not the activity of individual stocks. It also may not be a bad idea to wait for talk of a government investigation over censorship to die down.

Q: Would you buy Tesla (TSLA)?

A: No, buy the car, not the stock. There are just too many black swans out there circling around Tesla. It seems to be a disaster a week, but then every time you sell off it runs right back up again. Eventually, on a 10-year view I would be buying Tesla here as I believe they will eventually become the world’s largest car company. That is the view of the big long-term value players, like T. Rowe Price and Fidelity, who are sticking with it. But regarding short term, it’s almost untradable because of the constant titanic battle between the shorts and the longs. At 26% Tesla has the largest short interest in the market.

Q: I’m long Microsoft; is it time to buy more?

A: No, I would wait for a bit more of a sell-off unless you’re a very short-term trader.

Q: What would you do with the TBT (TBT) calls?

A: I would buy more, actually; preferably at the next revisit by the ProShares Ultra Short 20 Year Plus Treasury ETF (TBT) to $33. If we don’t get there, I would just wait.

Q: What’s your suggestion on our existing (TLT) 9/$123-$126 vertical bear put spread?

A: It expires in 12 days, so I would run it into expiration. That way the spread you bought at $2.60 will expire worth $3.00. We’re 80% cash now, so there is no opportunity cost of missing out with other positions.

Q: Do you like emerging markets (EEM)?

A: Only for the very long term; it’s too early to get in there now. (EEM) really needs a weak dollar and strong commodities to really get going, and right now we have the opposite. However, once they turn there will be a screaming “BUY” because historically emerging nations have double the growth rate of developed ones.

Q: Do you like the Invesco India ETF (PIN)?

A: Yes, I do; India is the leading emerging market ETF right now and I would stick with it. India is the next China. It has the next major infrastructure build-out to do, once they get politics, regulation, and corruption out of the way.

Q: Do you trade junk bonds (JNK), (HYG)?

A: Only at market tops and market bottoms, and we are at neither point. When the markets top out, a great short-selling opportunity will present itself. But I am hiding my research on this for now because I don’t want subscribers to sell short too early.

Q: With the (VXX), I bought the ETF outright instead of the options, what should I do here?

A: Sell for the short term. The iPath S&P 500 VIX Short-Term Futures ETN (VXX) has a huge contango that runs against it, which makes long-term holds a terrible idea. In this respect it is similar to oil and natural gas ETFs. Contango is when long-term futures sell at a big premium to short-term ones.

Q: How much higher for Apple (AAPL)?

A: It’s already unbelievably high, we hit $228 yesterday. Today it’s $228.73, a new all-time high. When it was at $150, my 2018 target was initially $200. Then I raised it to $220. I think it is now overbought territory, and you would be crazy to initiate a new entry here. We could be setting up for another situation where the day they bring out all their new phones in September, the stock peaks for the year and sells off shortly after.

Mad Hedge Technology Letter

September 5, 2018

Fiat Lux

Featured Trade:

(WARREN BUFFETT’S GREAT TECH FIND IN INDIA),

(BRK/B), (AAPL), (GOOGL), (MSFT), (BABA), (NFLX)

Warren Buffett preaches searching among your “circle of competence” to find those gems of companies that will offer abundant value in the far future.

His time horizon has always been long – 10, 20, 30 years where a company has sufficient time to execute its business strategy.

The celebrated investor’s track record is unrivaled.

Another critical rule to his playbook of uncanny success is to invest in companies within your area of expertise to avoid erroneous investment decisions.

If an investor is uncertain if a company is within its “circle of competence,” then it is likely outside the circle and best to skip investing in the company for now.

The Oracle of Omaha has taken his investment playbook to the chicken tikka masala-loving country of India, dropping a few Benjamín’s on One97 Communications Ltd., the parent company of Paytm, an Indian fin-tech firm.

This disrupting digital payments company based in Noida, India, is the nation’s largest mobile-payments firm and quite an achievement in a country that loves paper cash.

It boasts a popular smartphone app used in daily lives, and mirrors digital payment businesses of the likes of China’s Alipay or Tencent’s WeChat payment platform.

When the Indian government laid down the heavy hand of fiscal regulation on the paper currency market with an eye toward the digital currency market, an outsized winner was Paytm.

The cost of printing paper money in India per year is more than $90 million by itself.

I am not saying that the Indian government is going into overdrive adopting bitcoin tomorrow, but its pivot toward fin-tech mobile payments and Buffett’s vote of approval show where all the deep lying tech value is marinating in the world.

It is not Silicon Valley that gets more expensive by the day.

Silicon Valley is largely saturated with venture capitalist firms cherry-picking the best firms before they go public and making many times their investment once they hit the New York public markets.

Well, we are still in the early stages of India’s rapidly developing tech scene. And 2018 has seen some blockbuster cash injections such as Walmart’s investment in e-commerce juggernaut Flipkart.

Buffett has championed investing into companies with a “margin of safety,” allowing him to buy stakes at levels he believes that are well below market value.

This allows him to sleep at night because even if the company tanks short-term, he knows that eventually it will pull it together.

India can now lay claim to more than 390 Internet users, and 300 million of those use Paytm.

When 77% of a country’s population is using an app, you know there is some staying power, as the first mover advantage in the tech world has a powerful and long-term network effect such as the AWS’s foray into the cloud business.

Paytm does have a crowded lineup of heavyweights breathing capital into its company in the form of investments from Masayoshi Son’s SoftBank Vision Fund and Jack Ma’s Alibaba (BABA).

China’s presence in the Indian tech scene is strong, but it has not doubled down there as it has in Southeast Asia, where it enjoys a healthier political connection that is largely void of border skirmishes.

India is the largest democracy in Asia and a strong ally of the United States. Although American tech companies won’t be welcomed with a pristine red carpet, they do have ample opportunity to invest in the burgeoning Indian tech scene.

Buffett’s stake amounts to a 3% to 4% stake in Paytm, and the valuation has spiked to more than $10 billion.

This comes on the heels of Buffett’s adding to his position in Apple (AAPL) that sees him now own 5%.

Apple’s services division is its new cash cow and is on track to eclipse $50 billion in annual revenue next year.

Apple’s services division surpassed $30 billion in the first three quarters of 2018. Its evolution comes at a timely period where smartphone growth has peaked while invaded by low-quality Chinese substitutes.

After sliding to annual low’s in April 2018 of $160, Apple has literally gone ballistic, powering past the $1 trillion valuation mark and is trading at all-time highs around $230.

Apple is another example of why this bull market is predominantly propped up by tech companies that continue to grow earnings at an insane pace.

Only a few companies have fallen into booby traps set forth by the regulatory hurdles first set by the Europeans and General Data Protection Regulation (GDPR).

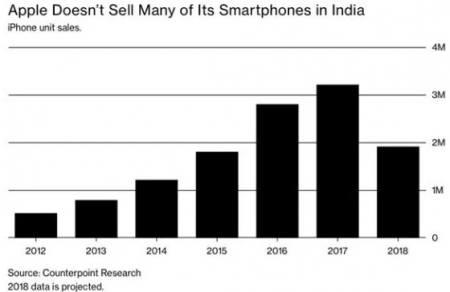

Apple is losing its smartphone battle in India, but Indians can’t afford iPhones yet and even Netflix (NFLX) is seen as an expensive streaming service.

The average Indian does not possess the purchasing power that North America and Europe have.

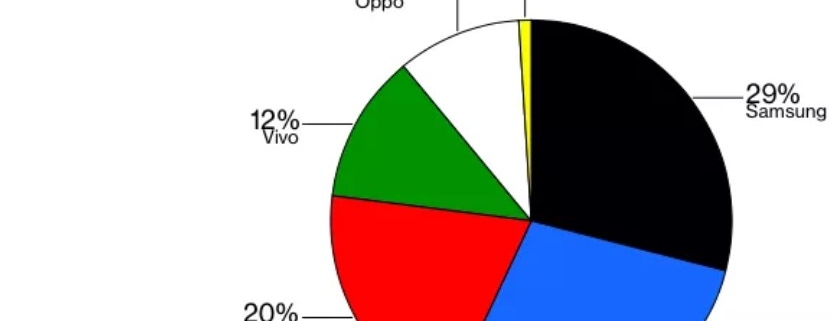

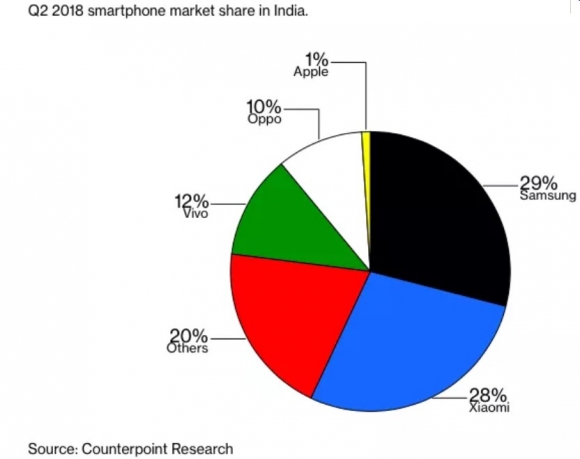

Apple has only extracted 1% of smartphone sales in India compared to leader Xiaomi, which leads the market with a 28% share. Further down-market Chinese phone maker Oppo lags with 10% and Vivo with 12%.

It doesn’t matter for Apple.

Apple continues to milk the North American and European markets to great effect padding profits with its high-quality services business.

China was the undeveloped market that launched Apple’s profits sky high. And American tech companies are ostensibly using this same strategy in India and hoping to cement the best strategy for revenue down the road.

Buffett’s investment is finally a green light for India if there ever was one, and every Silicon venture capitalist has to be licking their chops to squeeze value out of India.

The value is deep lying, but it will pay dividends within five to 10 years as India’s economy rises with its citizen’s discretionary income.

With every Tom, Dick, and Harry lusting after the India market, it will drive valuations firmly higher for the foreseeable future.

The fear of missing out (FOMO) will expedite the pivot toward India where many of the most conservative investors could ironically end up.

The tech relationship between America and India is demonstrably synergistic with Indian born CEOs heading Google (GOOGL) and Microsoft (MSFT) among other influential tech companies.

Berkshire’s (BRK/B) funds join the Chinese, Japanese, and Silicon Valley venture capitalist’s capital queuing at India’s front door awaiting to unlock value.

Buffett even opted out of investing in ride-sharing behemoth Uber, because apparently the “margin of safety” was not sufficient enough in the proposal.

Buffett was even quoted on a local Indian television station gushing about the country saying, “If you’ll tell me a wonderful company in India that might be available for sale, I’ll be there tomorrow.” That day has surfaced in the form of his investment in Paytm.

Apparently, Buffett’s expertise lies in India now and Indian-born Ajit Jain is one of four Berkshire executives running the company on a day-to-day basis.

This will pave the way for more tech investments in the swiftly evolving Indian tech scene, and Berkshire will ring in the profits of these Indian assets down the road.

________________________________________________________________________________________________

Quote of the Day

“Our favorite holding period is forever,” – said legendary American investor Warren Buffett.

Global Market Comments

September 4, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON GLOBAL STRATEGY LUNCHEON),

(DON’T MISS THE SEPTEMBER 5 GLOBAL STRATEGY WEBINAR),

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or

THE WAR WITH CANADA STARTS ON TUESDAY),

(MSFT), (VXX), (TLT), (AAPL), (KO), (GM), (F)

I have spent all weekend sitting by the phone, waiting for the call from Washington D.C. to re-activate my status as a Marine combat pilot.

Failure of the administration to reach a new NAFTA trade agreement by the Friday deadline makes such a conflict with Canada inevitable.

And while you may laugh at the prospect of an invasion from the North, the last time this happened Washington burned. You can still see the black scorch marks inside the White House today.

This is all a replay for me, when in 1991, I enjoyed an all-expenses paid vacation courtesy of Uncle Sam. That’s when I spent a year shuttling American fighter pilots from RAF Lakenheath to forward bases at Ramstein, Aviano, Cyprus, and Dharan, Saudi Arabia.

It may seem unlikely that our nation’s military would require the services of a decrepit 66-year-old. However, in my last conflict I ran into another draftee who was then 66. It seems that the Air Force then had a lot of F-111 fighter bombers left over from Vietnam that no one knew how to fly.

That’s the great thing about the military. It never throws anything away. Not even me. The life of our remaining B-52 Stratofortress bombers at their final retirement in 2050 will be 100 years.

Perhaps Canada will decide that discretion is the better part of valor, and simply wait for the World Trade Organization to declare the Trump tariffs illegal, which they obviously all are.

That would then force the administration to withdraw from the organization the U.S. created at the end of WWII to regulate fair trade and go rogue. But then what else is new?

And while there was immense media time devoted to the NAFTA talks, which only oversees trade with partners with around $2 trillion each, China, the 800-pound gorilla, is still lurking out there. It has a $12.2 trillion GDP and Trump is imposing tariffs on another $200 billion of their imports there today.

The corner that Trump has painted himself into is that he has made himself SO unpopular abroad, insulting virtually everyone but Russia, that no leader is willing to risk doing a deal with him lest they get kicked out of office.

I certainly felt this in Europe this summer where the discussion was all about Trump all of the time. When you insult a nation’s leader you insult everyone in that country. I haven’t received that kind of treatment since the Vietnam War was running hot and heavy in 1968.

I’ll tell you, I’d much rather be flying combat missions over enemy territory without a parachute than trading a market like we had last week. For months now, it has been utterly devoid of low risk/high return entry points for all asset classes.

It’s been a slow-motion melt-up virtually every day against the most horrific news backdrop imaginable. Such is the wonder of massive global excess liquidity. It Trumps everything.

NASDAQ topped 8,000, proving that if you aren’t loaded to the gills with technology stocks, as I have been pleading all year, you are out of your freaking mind. If you don’t own Apple, you are doubly screwed.

I doubt that such data is available, but I bet the illiterate and the uneducated have been beating more literate types in performance by a huge margin.

The unresponsiveness to news isn’t the only thing afflicting this market. As the summer coughs and sputters its way to a close, we enter September, notorious as the most horrific trading month of the year. And we are launching into it with the Mad Hedge Market Timing Index stuck in the 70s, overbought territory, for weeks now.

Blockbuster earnings, the principal impetus for rising share prices in 2018, are now firmly in the rearview mirror, and won’t make a reappearance for another month. Then they die completely in 2019.

Perhaps this is why my long volatility position in the (VXX) is doing moderately well, even though the indexes have been hitting new all-time highs, with the S&P 500 briefing kissing $292. I rather practice my golf swing rather than try to outtrade this market, even though I don’t play golf.

Other than NAFTA, there was little to trade off of last week. Apple (AAPL) shares continue to break new records, hitting an incredible $228, in front of their big iPhone launch this month. Trump announced he was freezing wages on 1 million-plus federal employees next year. That will solve their tax problems for sure.

Coca-Cola (KO) bought British owned Costa for $5 billion, where I regularly breakfast while traveling abroad, in the hopes that perhaps its 501st new drink launch this year will be successful.

Amazon (AMZN) is within sofa change of becoming the next $1 trillion market cap company, making the parents of founder Jeff Bezos the most successful angel investors in history, worth $30 billion.

U.S. auto sales are in free fall. Car company shares (GM), (F) continued their slide as they are pummeled on every side by administration economic policies. One has to ask the question of how long the American economy can survive after losing a major leg like this one. Home sales, another vital component, are also suddenly awful.

Trump attacked big tech. The market yawned.

With the Mad Hedge Market Timing Index at 71 and bounces around in the 70s all week, I am not inclined to reach for trades here. All three of my current positions are making money, my longs in Microsoft (MSFT) and volatility (VXX) and my short in the U.S. Treasury bond market (TLT).

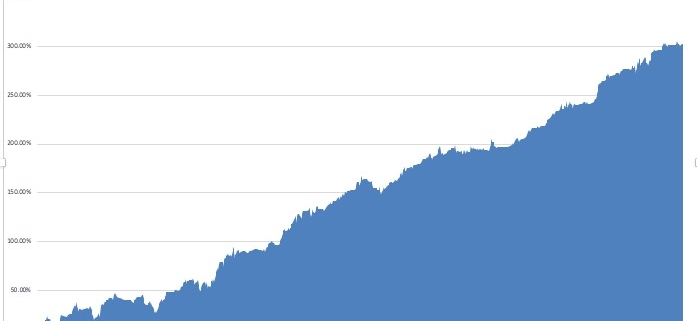

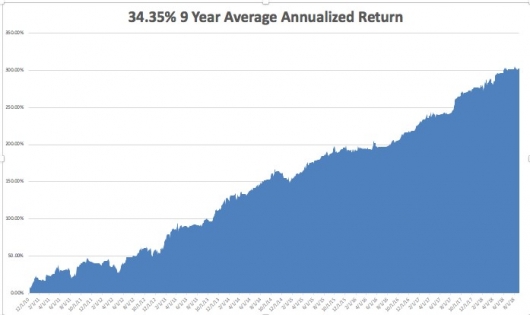

August finally brought in a performance burst in the final days, leaving us with a respectable return of 2.13%. My 2018 year-to-date performance has clawed its way back up to 25.30% and my nine-year return appreciated to 303.48%. The Averaged Annualized Return stands at 34.35%. The more narrowly focused Mad Hedge Technology Fund Trade Alert performance is annualizing now at an impressive 28.59%.

This coming week housing statistics will give the most important insights on the state of the economy.

On Monday, September 3, there was a national holiday, Labor Day.

On Tuesday, September 4, at 9:45 AM the PMI Manufacturers Index is out. August Construction Spending is out at 10:00 AM.

On Wednesday, September 5 at 7:00 AM, we learn MBA Mortgage Applications for the previous week.

Thursday, September 6 leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a rise of 3,000 last week to 213,000. Also announced at 9:45 AM are the August PMI Services Index.

On Friday, September 7 the Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, the high point of my weekend was the funeral services for Senator John McCain. Boy, the Squids really know how to put on a ceremony. I suspect it may market a turning point for our broken American politics.

In the meantime, King Canute sits in his throne at the seashore ordering the tide not to rise.

Good luck and good trading.

Mad Hedge Technology Letter

September 4, 2018

Fiat Lux

Featured Trade:

(READY PLAYER ONE’S INSIGHT INTO THE FUTURE OF TECHNOLOGY),

(MSFT), (SQ), (TTWO), (AMD), (NVDA), (EA), (ATVI), (PYPL), (GOOGL), (FB)