Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Modern tech has an unseen dark side to it.

Coders relish the opaqueness surrounding the industry infatuated with developing the next big thing to take Silicon Valley by storm.

There is nothing opaque about the Mad Hedge Technology Letter.

I grind out recommendations and you follow them. Period. End of story.

To put it mildly, the letter has gotten off to a flying start since its inception in February 2018, and there is no looking back, only looking forward.

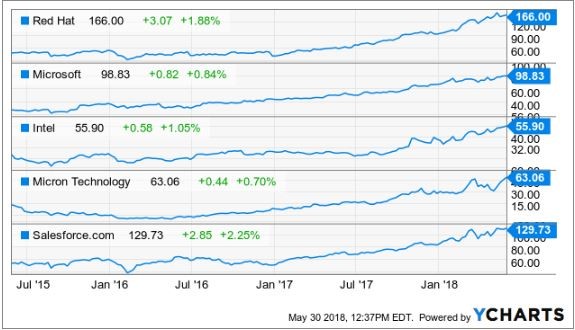

Micron (MU), Red Hat (RHT), Microsoft (MSFT), and Intel (INTC), just to name a few, have been solid recommendations standing up to all the nonsense and mayhem permeating throughout the periodically irrational markets.

Have you noticed lately when you open up the morning paper while sipping on a steaming mug of Blue Bottle Coffee, that almost every story is about technology?

It's not a mistake. I swear.

Technology is permeating into the nooks and crannies of our society and the leaders of this movement are laughing all the way to the bank.

One of those aforementioned pioneers is no other than local lad, Salesforce CEO and perennial Facebook basher Marc Benioff.

I recommended Salesforce at $110 and it was one of the first positions in the Mad Hedge Technology portfolio.

You can't blame me.

I saw this stock pick from a million miles away and I will explain why.

Salesforce set ambitious targets that nobody thought were realistic at the time.

How high in the sky does Benioff want to build his castles?

By 2022, Marc Benioff set out sales targets of a colossal $20 billion per year.

Then Benioff gushed that Salesforce would pass the $40 billion mark, done and dusted by 2028 and $60 billion by 2034.

Remember that tech CEOs are incentivized to forecast ludicrous sales targets because it lures in the unknowledgeable investor.

Unknowledgeable or pure genius, it does not matter, Salesforce is an emphatic buy.

Salesforce is the ultimate growth stock.

In 2016, annual revenue came in at $6.67 billion, which is about the same size as a middle level semiconductor company.

They followed that up with $8.38 billion in 2017, demonstrating the parabolic shaped trajectory of the company.

At the end of fiscal year 2017, Salesforce announced that it expects revenue of around $12.60 billion in 2019.

The latest earnings report, Benioff disclosed full year guidance of $13.13 billion.

This puts Salesforce in the running to achieve its lofty aspirations.

Apparently, the castles Benioff is building aren't in the sky after all.

Theoretically, if Benioff expands the business into a $16 billion to $16.5 billion business by 2019, Salesforce will have a more than likely chance to pass the $20 billion mark by the end of 2020, a full two years than initially thought.

Salesforce will have ample wiggle room on the way to $20 billion if it is 2022 for which it aims.

Why am I rambling on about revenue?

It's the only metric that Salesforce investors value.

The company registered two straight years of less than $200 million in profits then followed it up with a less than stellar 2016 where it lost almost $50 million.

Don't expect any dividends from this neck of the woods anytime soon especially after acquiring MuleSoft, an integration software company, for $6.5 billion last quarter.

This purchase will add another $315 million of annual revenue to Salesforce's quest of eclipsing its future sales targets. This was after MuleSoft made $296.5 million in 2017 before it became a part of Marc Benioff's stable.

Benioff has proved a shrewd dealmaker, taking advantage of cheap capital to add suitable parts to his business.

Since 2016, Benioff has snapped more than 50 niche software companies that he rebrands as Salesforce products and sells them as add-on products.

This is further evidence that any funds available will be allocated toward reinvestment into products and services deeming any future dividend inconceivable, especially with the elevated revenue targets to surpass.

As for the business. Do we still need to talk about it?

Rip-roaring growth was seen across the board with total revenue increasing 25%.

Investors should stay away from any cloud company that is growing less than 20%.

Market intelligence firm International Data Corporation (IDC) voted Salesforce as the No. 1 client relationship management (CRM) platform for the fifth consecutive year.

It is the industry leader in sales, marketing, service, and increased market share in 2017, more than its closest competitors.

Larry Ellison must be tearing his hair out as Oracle's (ORCL) share price has been excommunicated to purgatory indefinitely.

Oracle is a company that I have been pounding on the tables to stay away from.

The Mad Hedge Technology Letter seldom recommends legacy companies that are still legacy companies.

Driving past his former estate, emanating from a sparkling perch in Incline Village overlooking Lake Tahoe, my neighbor gives me the goose bumps.

The property was later sold for $20.35 million. All told, Larry has around $100 million invested in real estate dotted around Incline Village. I sarcastically mentioned to him last time we bumped into each other to call me immediately when his $90 million estate in Kyoto, Japan, hits the market.

Oracle's position in the pecking order is a telltale sign of the inability to land the creme de la creme government contracts that ostensibly fall into Amazon (AMZN), Alphabet (GOOGL), and Microsoft's lap.

And it's not surprising that Larry is spending more time tending to his vast array of glittering luxury properties around the world rather than running Oracle.

Oracle is like a deer caught in the headlights and Marc Benioff is at the wheel.

On the Forbes 500 rankings, Salesforce has moved up almost 200 spots.

This position will rise as Salesforce is under contract booking a further $20.4 billion of commitments driven by its subscription services offering cloud products.

On the domestic contract front, it was much of the same for Salesforce, which inked premium deals with the U.S. Department of Agriculture, Kering, and sports apparel giant Adidas.

International companies such as Philips and Santander UK are expanding their relationships with Salesforce. A firm nod of approval.

Salesforce has been voted in the top three of most innovative companies for the past eight years by reputable Forbes magazine. The list was started in 2011, and it has never dropped out of the top three.

The gobs of innovation are the main logic behind the top five financial institutions expanding their relationship with Salesforce by an extra 70%.

Once companies start using the CRM platform, they become mesmerized with the premium add-ons that help companies run more efficiently.

Benioff has been a huge proponent of artificial intelligence (A.I.) and is an outsized catalyst to product enhancement gains.

Salesforce has taken Einstein, it's A.I. platform, and allowed all the applications to run through it.

The integration of Einstein has resulted in more than 2 billion correct predictions per day paying homage to the quality of A.I. engineering on display.

Instead of hiring a whole team of in-house data scientists, Salesforce is A.I. functionality by the bucket full and it is easy to use on its platform.

In some cases, incorporating Salesforce's A.I. into the business has bolstered other companies' top line by 15%.

Often, Salesforce's A.I. tools are declarative meaning the technology can identify solutions without a fixed formula.

Benioff has choreographed his strategy perfectly.

He is betting the ranch on unlocking data from legacy companies that migrate to his platform.

MuleSoft will help in this process of extracting value, then A.I. will supercharge the data, which is being unlocked.

What does this mean for Salesforce?

Higher revenue and more clients leading to accelerated growth. The share price has powered on north of $130, and after I recommended it at $110, I am convinced this stock will surge higher.

Salesforce is an absolute no-brainer buy on the dip.

Growth Means Shiny New Office Buildings

_________________________________________________________________________________________________

Quote of the Day

"If we become leaders in Artificial Intelligence, we will share this know-how with the entire world, the same way we share our nuclear technologies today." - said current President of Russia, Vladimir Vladimirovich Putin.

Mad Hedge Technology Letter

May 29, 2018

Fiat Lux

Featured Trade:

(HERE ARE SOME EARLY 5G WIRELESS PLAYS),

(T), (VZ), (INTC), (MSFT), (QCOM), (MU), (LRCX), (CVX), (AMD), (NVDA), (AMAT)

How would you like to be part of the biggest business development in the history of mankind?

This revolution will increase business functionality up to 10 times while flattening costs by up to 90%.

Still interested?

Enter the Internet of Things (IoT).

The Internet of Things (IoT) can be boiled down to Internet connectivity with things.

Your luxury juice maker, hair removal kit, and multi-colored Post-its will soon be online.

No, you won't be able to have Tinder chats with the new connectivity, but embedded sensors, tracking technology, and data mining software will aggregate a digital dossier on how products are performing.

The data will be fed back to the manufacturing company offering a comprehensive and accurate review without ever asking a human.

The magic glue making IoT ubiquitous and stickier than a hornet's nest is the emergence and application of 5G.

4G is simply not fast enough to facilitate the astronomical surge in data these devices must process.

5G is the lubricant that makes IoT products a reality.

Verizon Communications (VZ) and AT&T (T) have been assiduously rolling out tests to select American cities as they lay the groundwork for the 5G revolution.

The aim is for these companies to deliver customers a velocious 1 Gbps (gigabits per second) wireless connection speed.

Delivering more than 10 times the average speed today will be a game changer.

America isn't the only one with skin in the game and some would say we are not even leading the pack.

China Mobile (CHL) is carrying out a bigger test in select Chinese cities, and Chinese telecom company Huawei can lay claim to 10% of the 5G patents.

Americans should start to notice broad-based adoption of 5G networks around 2020.

Once widespread usage materializes, watch out!

It will go down in history books as a transformational headline.

The IoT revolution will follow right after.

Until the 5G rollout is done and dusted, tech companies are licking their chops and preparing for one of the biggest shifts in the tech ecosphere affecting every product, service, and industry.

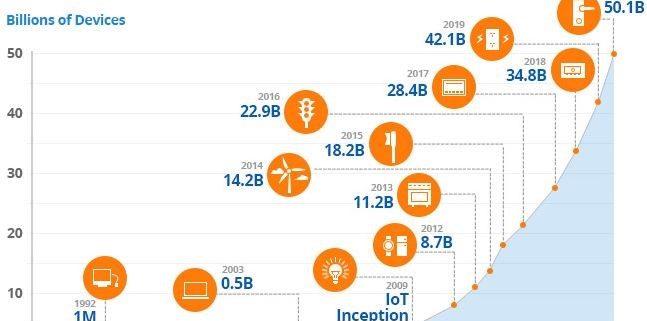

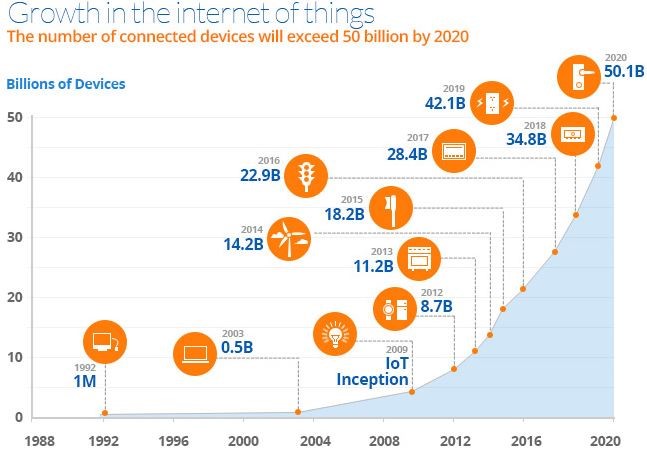

The worldwide IoT market is poised to mushroom into a $934 billion market by 2025 on the back of cloud computing, big data, autonomous transport technology, and a host of other rapidly emerging technology.

The arrival of 5G will have an astronomical network effect. Companies will be able to enhance product specs faster than before because of the feedback of data accumulated by the tracking technology and sensors.

The appearance of this flashy new technology will spawn yet another immeasurable migration to technological devices by 2020.

In just two years, the world will play host to more than 50 billion connected devices all pumping out data as well as consuming data.

What a frightful thought!

IoT's synergies with new 5G technology will have an unassailable influence on the business environment.

For instance, industrial products in the form of robots and equipment will be a huge winner with 5G and IoT technology.

The industrial IoT market is expected to sprout to $233 billion by 2023.

Robots will pervade deeply into economic provenance acting as the mule for brute strength heavy labor plus more advanced tasks as they become more sophisticated.

Total global spending related to IoT products will surpass 1.4 trillion dollars by 2021, according to the International Data Corporation (IDC).

IoT growth will become most robust in the thriving Asian markets fueled by a bonus tailwind of the fastest growing region in the world.

The advanced automation abilities of Germany and the U.K. will also give them a seat at the table.

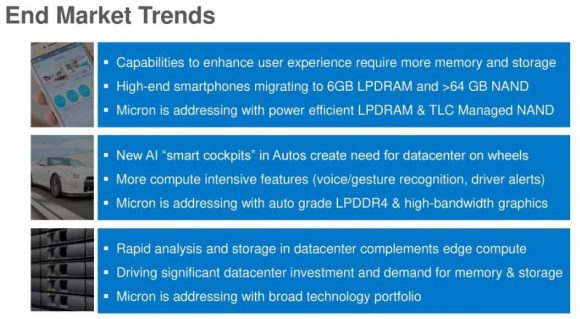

Micron CEO Sanjay Mehrotra gushed about the future at Micron's investor day celebrating IoT and data as the way forward. Mehrotra explained that the explosion of IoT products will create a new tidal wave of "growing demand for storage and memory."

Chips are a great investment to grab exposure to the 5G, IoT, and big data movement.

Up until today, the last generation of technological innovation brought consumers computers and smartphones.

That world has moved on.

Open up your eyes and you will notice that literally everything will become a "data center on wheels or on feet."

To arrive at this stage, products will need chips.

As many high-grade chips as they can find.

Data centers are one segment in dire need of chips. This market will more than double from $29 billion in 2017 to $62 billion in 2021.

The general-purpose chip market for servers is cornered by Intel.

Industry insiders estimate Intel's market share at 98% to 99% of data center chips. Clientele are heavy hitters such as Amazon Web Services, Google, and Microsoft Azure along with other industry peers.

The only other players with data server chips out there are Qualcomm (QCOM) and Advanced Micro Devices Inc. (AMD).

However, there have been whispers of Qualcomm shutting down the 48-core Centriq 2400 chip for data centers that was launched only last November after head of Qualcomm's data center division, Anand Chandrasekher, was demoted via reassignment.

AMD's new data center chip, Epyc, has already claimed a few scalps with Baidu (BIDU) and Microsoft Azure promising to deploy the new design.

IoT integration is the path the world will take to adopting full-scale digitization.

Microsoft just announced at its own Build 2018 conference its plans to invest $5 billion into IoT in the next four years.

The Redmond, Washington-based company noted operational savings and productivity gains as two positive momentum drivers that will benefit IoT production.

Consulting firm A.T. Kearny identified IoT as the catalyst fueling a $1.9 trillion in productivity increases while shaving $177 billion off of expenses by 2020.

These cloud platforms give tech companies the optimal stage to win over the hearts and dollars of non-tech and tech companies that want to digitize services.

Many of these companies will have IoT products percolating in their portfolio.

Examples are rampant.

Schneider Electric in collaboration with Microsoft's IoT Azure platform brought solar energy to Nigeria by the bucket full.

The company successfully installed solar panels harnessing its performance using IoT technology through the Microsoft cloud.

Kohler rolled out a new lineup of smart kitchen appliances and bathroom fixtures coined "Kohler Konnect" with the help of Microsoft's Azure IoT platform.

Consumers will be able to remotely fill up the bathtub to a personalized temperature.

Real-time data analytics will be available to the consumer by using the bathroom mirror as a visual interface with touch screen functionality giving users the option to adjust settings to optimal levels on the fly.

Kohler's tie-up with Microsoft IoT technology has proved fruitful with product development time slashed in half.

To watch a video of Kohler's new budding relationship with Microsoft's Azure IoT platform, please click here.

It is safe to say operations will cut out the wastefulness using these new tools.

Look no further than legacy American stocks such as oil and gas producer Chevron (CVX), which wants a piece of the IoT pie.

Chevron announced a lengthy seven-year partnership with Microsoft's Azure platform.

The fiber optic cables inside oil production facilities generate more than 1 terabyte of data per day.

In the Houston, Texas, offices, sensors installed six miles below the surface shoot back data to engineers who monitor human safety and system operations on four continents from the Lone Star State.

The newest facility in Kazakhstan, using state-of-the-art technology, will produce more data than all the refineries in North America combined.

Using the aid of artificial intelligence (A.I.), computers will analyze seismic surveys. This pre-emptive technology customizes solutions before problems can germinate.

The new smart-work environment will multiply worker productivity that has been at best stagnant for the past generation.

To get in on the IoT action, buy shares of companies with solid IoT cloud platforms such as Microsoft and Amazon.

Buy best-of-breed chip companies such as Nvidia (NVDA), Intel (INTC), Advanced Micro Devices (AMD) and Micron (MU).

And buy tech companies that produce wafer fab equipment such as Applied Materials (AMAT) and Lam Research (LRCX).

_________________________________________________________________________________________________

Quote of the Day

"Don't be afraid to change the model." - said cofounder and CEO of Netflix Reed Hastings.

Mad Hedge Technology Letter

May 24, 2018

Fiat Lux

Featured Trade:

(MICRON'S BLOCKBUSTER SHARE BUYBACK)

(MU), (AMZN), (NFLX), (AAPL), (SWKS), (QRVO), (CRUS), (NVDA), (AMD)

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

Growth - Check. Accelerating Revenue - Check. Margins - Check. Earnings beat - Check. Guidance hike - Check.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

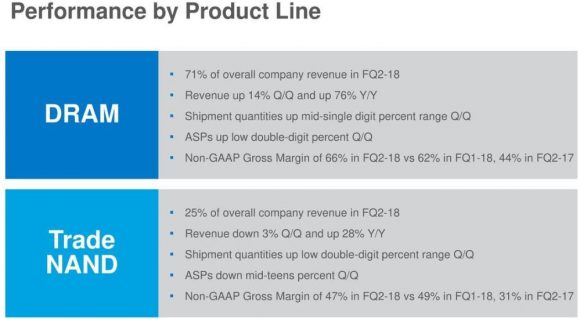

Half way into 2018, and there is still a dire shortage of DRAM chips.

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

_________________________________________________________________________________________________

Quote of the Day

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.

Mad Hedge Technology Letter

May 23, 2018

Fiat Lux

Featured Trade:

(WHY THE BIG DEAL OVER ZTE?),

(MU), (QCOM), (INTC), (AAPL), (SWKS), (TXN), (BIDU), (BABA)

Here's the conundrum.

Beyond cutting-edge technology, there's nothing that China WANTS OR NEEDS to buy from the U.S. China's largest imports are in energy and foodstuffs, both globally traded commodities.

China is playing the long game because it can.

Earlier this year, China altered its constitution to remove term limits and any obstacle that would hinder Chairman Xi to serve indefinitely.

If it's two, four, eight or 10 years, no problem, China will wait it out.

As it stands, China is enjoying the status quo, which is a robust economic trajectory of 6.7% economic growth YOY and at that rate will leapfrog America as the biggest economy in the world by 2030.

China does not need handouts.

It already has its mooncake and is eating it.

The Chinese are also betting that Donald Trump fades away with the passage of time, possibly soon, and that a vastly different administration will enter the fray with an entirely different strategy.

The indefinite "hold" pattern is a polite way to say we surrender.

ZTE Corporation is a Chinese telecommunications equipment manufacturer and low-end smartphone maker based in Shenzhen, China.

This seemingly innocuous company is ground zero for the U.S. vs China trade practice dispute.

The U.S. Department of Commerce banned American tech companies from selling components to ZTE for seven years, crippling its supply chain after violating sanctions against Iran and North Korea.

ZTE uses about 30% of American components to produce its smorgasbord of telecom equipment and down-market cell phones.

What most people do not know is that ZTE is the fourth most prevalent smartphone in America, only behind Apple, Samsung, and LG, commanding a 12.2% market share, and its phones require an array of American made silicon parts.

In 2017, the company shipped more than 20 million phones to the United States.

The ruling effectively put ZTE out of business because the lack of components shelved production.

Low-end smartphones account for almost one-third of total revenue.

ZTE could very well have survived with a direct hit to its consumer phone business, but the decision to ban components made the telecom equipment division inoperable.

This segment accounts for a heavy 58.2% of revenue. Therefore, disrupting ZTE's supply chain would effectively take down more than 91% of its business for a company that employs 75,000 employees in over 160 countries.

Upon news of ZTE's imminent demise, the administration made a U-turn on its initial decision stating "too many jobs in China lost."

The reversal made America look bad.

It shows that America is being dictated to and not the other way around.

When did it become the responsibility of the American administration to fill Chinese jobs for a company that is a threat to national security?

The Chinese refused to continue talks with the visiting delegation until the ZTE situation was addressed.

Treasury Secretary Steve Mnuchin and company were able to "continue" the talks then were politely shown the door.

Bending the rules for ZTE should have never been a prerequisite for talks, stressing the lack of firepower in the administration's holster.

However, stranding the delegation in Chinese hotel rooms for days waiting in limbo, without offering an audience, would have caused even more humiliation and anguish for the administration.

China is not interested in buying much from America, but one thing it needs -- and needs in droves -- are chips.

Long term, this ZTE ban is great for China.

I believe China will use this episode to rile up the nationalistic rhetoric and make it a point to wean itself from American chips.

However, for the time being, American chips are the most valuable import America can offer China, and that won't change for the foreseeable future.

The numbers back me up.

Micron (MU) earns more than $10 billion in revenue from China, which makes up over 51% of its total revenue.

Qualcomm (QCOM), mainly through its lucrative licensing division, makes more than $14.5 billion from its Chinese revenue, which comprises over 65% of revenue.

Texas Instruments (TXN) earns more than 44% of revenue from China, and almost a quarter of Intel's (INTC) revenue is derived from its China operations.

The biggest name embedded in China is Apple (AAPL), which earned almost $45 billion in sales last year. Its China revenue is three times larger than any other American company.

In less than a decade, China has caught up.

China now has adequate local smartphone substitutes through Huawei, Oppo, Vivo, and Xiaomi phones.

Skyworks Solutions (SWKS), a chip company reliant on iPhone contracts, is most levered toward the Chinese market capturing almost 83% of revenue from China.

You would think these chips would be the first on the chopping block in a trade war. However, you are wrong.

China needs all the chips it can get because there is no alternative.

Stopping the inflow of chips is another way of stopping China from doing business and developing technology.

The Chinese economy has been led by the powerful BATs of Baidu (BIDU), Tencent, and Alibaba (BABA) occupying the same prominent role the American FANGs hold in the American economy.

They are not interested in digging their own grave.

To execute the 2025 plan to become the world leaders in advanced technology, they need chips that power all modern electronic devices.

The most likely scenario is that China maintains development using American chips for the time being and slowly pivots to the Korean chip sector, which is vulnerable to Chinese political pressure.

Remember that South Koreans have two of the three biggest chip companies in the world in Samsung and SK Hynix. China has used economic coercion to get what it wants from Korea in the past or to prove a point.

Korean multinational companies, shortly after the Terminal High Altitude Area Defense (THAAD) installation on the Korean peninsula, were penalized by the Chinese government shutting down mainland Korean stores, temporarily banning Chinese tourism in South Korea, and blocking K-pop stars from performing in the lucrative Chinese market.

The Chinese communist government can turn the screws when it wants and how it wants.

Therefore, the next battleground for tech could migrate to South Korean chip companies as China is on a mission to suck up as much high-grade tech ingenuity as possible while it can.

China has some easy targets to whack down if the administration forces it into a corner with a knife to its throat.

Non-tech companies are ripe for massacre because they do not produce chips.

Companies such as Procter & Gamble, Starbucks, McDonald's, and Nike could be replaced by a Chinese imitation in a jiffy.

Apple is the 800-pound gorilla in the room.

An attack on Apple would hyper-accelerate tension between two leaders to the highest it's ever been and would be the straw that breaks the camel's back.

Technology has transformed the world.

Technology also has been adopted by nations as a critical component to national security.

Nothing has changed fundamentally, and nothing will.

China will become the biggest economy in the world by 2030.

China will kick the proverbial can down the road because it can. It never has to cooperate with America again.

Contrary to expectations, American chip companies are untouchable, and investors won't see Micron suddenly losing half its revenue over this trade war.

Until China can produce higher quality chips, it will lap up as much of Uncle Sam's chips until it can force transfer the chip technology from the Koreans.

American chip companies can breathe a sigh of relief.

_________________________________________________________________________________________________

Quote of the Day

"If we go to work at 8 a.m. and go home at 5 p.m., this is not a high-tech company and Alibaba will never be successful. If we have that kind of 8-to-5 spirit, then we should just go and do something else." - said Alibaba founder and executive chairman Jack Ma.

Global Market Comments

May 11, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 13, 2018, PHILADELPHIA, PA, GLOBAL STRATEGY LUNCHEON),

(MAY 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (MU), (NVDA), (AMZN), (GOOGL),

(TLT), (SPX), (MSFT), (DAL),

(MAD HEDGE DINNER WITH BEN BERNANKE)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader May 9 Global Strategy Webinar with my guest co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Would you still short Facebook (FB)?

A: Right now, no. I thought the dynamics changed off the last earnings report, so the answer is no. We have made a ton of money trading Facebook this year, and all of it has been from the long side.

Q: How will the election affect the market?

A: It will go down into the election, but you'll then get a strong rally as the uncertainty fades away. It really makes no difference who wins. It is the elimination of uncertainty that is the big issue.

Q: Do you have a price to buy Micron Technology (MU) or NVIDIA (NVDA), or do you want to wait for a crash day?

A: I want to wait for a crash day, because even though these are great companies, on the down days, they fall twice as fast as any other stock. Your entry point is very important in that situation.

Q: Do you see opportunities to sell short the U.S. Treasury bond market (TLT) again?

A: Yes. But wait for the four-point rally not the two-point rally.

Q: Rising interest rates should benefit banks - why are they such horrible performers?

A: The double in bank stocks in 2017 fully discounted this year's interest rate move. For banks to really perform interest rates have to move higher still, which they will eventually.

Q: When will the yield curve invert and what will be the implications?

A: You can take the Fed's current rate of interest rate rises (which is 25 basis points every three months) and essentially calculate that the yield curve inverts at the end of 2018 or the beginning of 2019. Recessions and bear markets always follow six months after that inversion takes place. That's when interest rates start to rise very sharply as bond investors panic and unwind all their leveraged long positions.

Q: Why are you not involved with Amazon (AMZN) and Google (GOOGL)?

A: I've already taken big profits in both of these and I'm just waiting for another serious dip before I get back in again.

Q: What happens to stock buybacks?

A: While other investors are pulling out of the market, stock buybacks are doubling. But, that is only happening, essentially, in the tech stocks - they're the buyback kings. If you don't have a serious buyback program this year, your stock is falling. Companies are the sole net buyers of the market this year, and they are only buying their own stocks.

Q: What do you see the upper and lower end of the S&P 500 (SPY) range to November?

A: I think we've already got it: 2,550 on the low side, 2,800 on the high side - that a 10% range and you can expect it to get narrower and narrower going into November. After that, we get an upside breakout to new all-time highs.

Q: When will rates be negative next?

A: In the next recession, the bottom of which will be in 2 to 2.5 years; that's when interest rates in the U.S. could go negative, as they did in Japan and Europe for several years.

Q: What is your No. 1 pick in the market today?

A: We love Microsoft (MSFT) long term. However, right now the background macro picture is more important than stock selection than any single name, so we're keeping a position in Microsoft in the Mad Hedge Technology Letter, but not in Global Trading Dispatch. We're sort of hanging back, waiting for another sell-off before we touch anything on the long side in GTD. Remember, the money is made on a buy in the new position, not on the sell going out.

Q: Was the semiconductor chip sell-off overdone?

A: Absolutely - the negative report was put out by a new analyst to the industry who doesn't know what he's talking about. If you ask all the end users of the chips, all they talk about is A.I., and that means exponential growth of chip demand.

Q: Is it a good time to buy airline stocks (DAL)?

A: No, until we get a definitive peak in oil, and a speed up again in the economy, you don't want to touch economically sensitive sectors like the airlines.