The chip maker Micron Technology (MU) fell 5% yesterday, but the stock is amazingly up 4% today.

The see-saw moves are a feature of this strategically important stock to the tech ecosystem and not just a symptom of it.

The stock is highly volatile which is emblematic of a stock that needs to constantly navigate around unstable geopolitics.

The stock's latest whipsaw action stems from the company predicting a steeper loss than anticipated in the current quarter, indicating that an industry slowdown is still weighing on the largest US maker of memory

For chip companies (SOXX), Samsung Electronics Co., and SK Hynix Inc., 2023 has been a crushing time after the glory period of the healthcare lockdown years.

September has been a month where we are experiencing weakening fundamentals as the US consumer is truly stretched.

Customers in big US markets for personal computers and smartphones have slashed orders as they cope with lackluster demand and stockpiles of excess parts.

Many are continuing to dive deeper into debt to make ends meet and that trend will not go away as the US middle class shrinks further as they grapple with soaring inflation.

The lack of consumer strength will mean it will take longer for Micron to return to profits.

Prices for Micron’s products are going up, and the rate of the price jump is increasing and we can probably say that about prices in most industries.

Sales have fallen for five straight quarters. In the three months ended in August, Micron’s revenue declined 40% to $4.01 billion.

The forecast suggests sales will begin to grow again in the fiscal first quarter, which runs through November.

Beijing has proved a thorn in Micron’s side.

This negative headwind has already cut into the US company’s revenue in China — the largest market for semiconductors — in what management has previously called a “significant headwind.”

The outlook remains mixed in the short term. In traditional servers — the computers that are still the mainstay of most data centers — demand remains tepid at best.

Both personal computers and smartphones will return to growth next year, with units increasing by a percentage in the low- to mid-single digits.

To cope with the slowdown, Micron and its peers reined in production, severely reducing supply and helping prices bottom out.

Micron will be demonstrably below peak 2022 output for the foreseeable future. The company plans to continue to run factories at less than full capacity well into calendar 2024. Micron also will further reduce spending on new equipment next year.

These are bad signs in the short term, but the strategic importance of MU puts a solid bid under the stock price.

I wholeheartedly expect the industry outlook to brighten considerably by 2025 — especially as artificial intelligence systems demand new types of more expensive memory chips.

Therefore, every big dip is a buying opportunity in Micron because this stock is resilient.

Luckily, big dips are common in MU and readers should be patient to wait for optimal entry points.

This is a good one to buy and hold for the long term.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-09-29 18:02:262023-09-29 19:21:56What to Do About Micron

Here are four AI stocks that retail traders are going bananas for lately.

These retail participants are itching to get the most exposure to a batch of AI stocks that punch weight just below the tech oligarch level.

Volume remains highly positive as traders fan out to further AI stocks that didn’t benefit as much from the first tranche of hot capital.

If there is anything that could be considered a fat pitch right now in equity markets, then look no further than this collection of 4 rock-solid AI stocks that will make your heart melt.

These four stocks are gaining traction among retail investors as they search for new winners in the AI space.

Micron (MU)

The semiconductor firm just beat its earnings and revenue targets, raking in $3.75 billion in revenue over the previous quarter.

AI servers have six to eight times the DRAAM content of a regular server and three times the NAND content which translates into elevated demand for Micron’s products.

In fact, some customers are deploying AI computing capability with substantially higher memory content.

The stock has lagged behind larger names like Nvidia and Advanced Micro Devices, but retail net purchases for Micron were 18 times their daily average, even before the company released its latest earnings report.

Oracle (ORCL)

Oracle's stock has exploded 40% year to date with shares briefly hitting a new record after a stellar earnings report. Total revenue for the 2023 fiscal year hit $50 billion, up 18% from last year.

On Wednesday, the database company also announced new AI capabilities within several of its cloud products, leading more investors to jump in on the stock.

Retail net purchases of the stock were about 145 times the daily average before its latest earnings report.

Adobe (ADBE)

Adobe was another to benefit from upbeat earnings, with revenue notching a $4.82 billion record in the second quarter, up around 10% from the previous year.

The developer of digital-publishing software also recently unveiled its new platform, Adobe Firefly, a generative artificial intelligence platform for content creators.

Retail net purchases of the stock were about 18 times greater than the daily average prior to its latest earnings report. The stock is up 43% from levels at the start of the year.

Snowflake (SNOW)

The company recently expanded its partnership with Microsoft and launched a new partnership with Nvidia to implement AI into its data cloud services.

The firm's partnership with NVDA and MSFT to integrate AI tools into their suite of services was welcome by retail traders who are jumping on the stock.

The common theme with these tech companies is solely focused on positive earnings numbers and what that will do is delay the recession that everybody has been waiting for.

The bears have been talking about a recession since the stimulus spike of the lockdowns, but the US economy and corporate tech have refused to believe this false narrative.

The truth is that tech companies still do what they need to do to push earnings higher and in turn deliver higher share prices to their shareholder.

Sure, there is belt-tightening and cost efficiencies taking place, but I view this more through a prism of technology firms becoming hyper-aware of leanness instead of sacrificing quality.

Twitter was correct in laying off 80% of its workforce because that 80% isn’t worth keeping on board for the splashy wage packets they accrue.

Now that we have a second level of tech companies joining the AI bandwagon, this could trigger another leg up for tech shares.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-30 16:02:522023-07-11 20:37:34The Second Wave of Hot Money is Here

I just received a call from the Marine Corps to go on emergency standby. This is not something the Corps does lightly.

The word is that there may be a coup d'etat underway in Russia and the entire US military has gone to a heightened alert status.

The Wagner group is Marching on Moscow with the intent of overthrowing the government, or at least the military. Putin took off in a plane which then disappeared radar, meaning he has either been shot down, or is flying low level to keep his destination secret.

This thing could go nuclear very easily, but only in Russia. It also could mean the end of the Ukraine War. There is nothing to do here as intelligence pours in over the weekend. We have ample satellites overhead and human intel on the ground.

Expect market volatility today. The markets are ripe for a black swan-inducted selloff, which a Mad Hedge Market Timing Index at 82 was screaming at us.

I will be monitoring the situation closely.

My view that the markets were topping was vindicated last week. The “Magnificent Seven” which gained a record 25% in market capitalization in only eight weeks led the downturn, as they always do. But the AI surge that prompted the fastest equity creation in history is only just getting started.

This is against a backdrop of savage cost-cutting by Big Tech, which has had the effect of boosting earnings by an impressive 7% in only three months. My cleaning lady, gardener, dry cleaner, and shoe shine boy have started giving me stock tips yet, as they did in 2000, 2008, and 2020….but they are thinking about it.

While attention is focused elsewhere, one should not underestimate the importance of India Prime Minister Modi’s meeting with Joe Biden in Washington.

It signifies a major geopolitical shift out of the Russian orbit into the US one. Decades ago, India obtained all its weapon systems and nuclear power plants from Russia and was a major trading partner.

Now partnering up with Apple (AAPL), Google (GOOGL), Microsoft (MSFT), and General Electric (GE) is a much more attractive option. It is gaining a $2.7 billion factory from Micron Technology (MU) and presents a major market for its products. Amazon (AMZN) is investing $13 billion in cloud infrastructure there. The subcontinent graduates some 2.5 million STEM graduates a year and they need to be put to work in the global economy. It shows how limited Russia’s future really is. It’s a major win for the US.

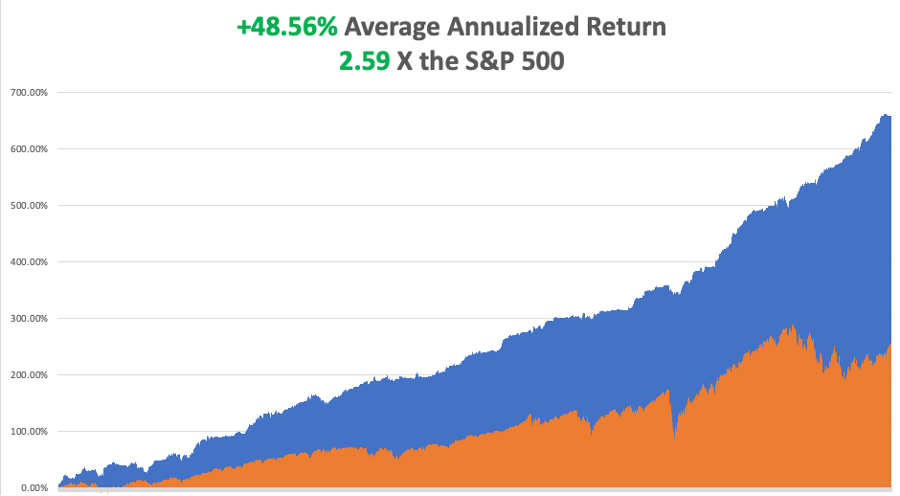

So far in June, we are up +0.47%. My 2023 year-to-date performance is still at an eye-popping +62.52%. The S&P 500 (SPY) is up only a respectable +14.00% so far in 2023. My trailing one-year return reached +96.63% versus +21.52% for the S&P 500.

That brings my 15-year total return to +659.71%. My average annualized return has blasted up to +48.56%, another new high, some 2.59 times the S&P 500 over the same period.

Some 42 of my 46 trades this year have been profitable. Only 23 of my last 24 consecutive trade alerts have been profitable.

The Mad Hedge December 6-8 Summit Replays are Up. Listen to all 28 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. It is a true smorgasbord of investment strategies. Find the best one to suit your own goals. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here and then choosing the speaker of your choice. We look forward to working with you.The next summit is scheduled for September 12-14.

$2 Billion Fled Stock Market Last Week, according to a Bank of America survey, in what it calls a “Baby Bubble.” The markets are showing all the signs of an interim top, with either a 10% correction or a three-month flat line ahead of us. Time to strap on those Buy Writes for long-term shareholders.

Short Bets on US stocks Hit $1 trillion, the highest since April 2022. Shorts have so far lost $101 billion in 2023, with much of this hedged. The market is way overdue for a correction so these guys may finally be right. Even a broken clock is right twice a day.

Germany Signs Massive US Natural Gas Contract, in a major move to end reliance on Russian natural gas. Venture Global LNG will supply EnBW with 1.5 million tons a year of LNG starting in 2026. The 20-year sales and purchase agreement is Germany’s first binding deal with a US developer since the government announced ambitious plans to begin importing the super-chilled fuel. The move does a lot to eliminate the glut of gas in the US currently plaguing producers. Buy (UNG) LEAPS on dips. When China comes back on line, watch out!

Volatility Index ($VIX) Hits the $12 Handle, in a new multiyear low. At the high for the year in the S&P 500, complacency is running rampant. Time to add some downside hedges.

Copper Should be a “Critical Metal”, says billionaire Robert Friedland. A looming structural shortage is the reason, with the world going to an all-electric auto fleet and doubling of the electrical grid to accommodate it. Buy more (FCX) LEAPS on dips.

Leading Economic Indicators Down 0.7% for the 15th consecutive negative month. We are approaching the bottom of the trough in this cycle. I’ll focus on the half of the economy that is growing.

Distressed Commercial Property Debt is Exploding, up 10% to Q1 to $64 billion. Another $155 billion is waiting in the wings. This will go away when interest rates start to drop in six months.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 26 at 8:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, June 27 at 6:00 PM, S&P Case-Shiller National Home Price Index is published.

On Wednesday, June 28 at 7:30 AM, the Fed Governor Jay Powell speaks.

On Thursday, June 29 at 8:30 AM, the Weekly Jobless Claims are announced. The Final Report for Q1 US GDP is printed.

On Friday, June 30 at 8:30 AM, Personal Income and Spending is announced.

As for me, when I first met Andrew Knight, the editor of The Economist magazine in London 45 years ago, he almost fell off his feet. Andrew was well known in the financial community because his father was a famous WWII Battle of Britain Spitfire pilot from New Zealand.

At 34, he had just been appointed the second youngest editor in the magazine’s 150-year history. I had been reporting from Tokyo for years, filing two stories a week about Japanese banking, finance, and politics.

The Economist shared an office in Tokyo with the Financial Times, and to pay the rent I had to file an additional two stories a week for them as well. That’s where I saw my first fax machine, which then was as large as a washing machine even though the actual electronics would fit in a notebook. It cost $5,000.

The Economist was the greatest calling card to the establishment one could ever have. Any president, prime minister, CEO, central banker, or war criminal was suddenly available for a one-hour chart about the important affairs of the world.

Some of my biggest catches? Presidents Gerald Ford, Jimmy Carter, Ronald Reagan, George Bush, and Bill Clinton, China’s Zhou Enlai and Deng Xiaoping, Japan’s Emperor Hirohito, terrorist Yasir Arafat, and Teddy Roosevelt’s oldest daughter, Alice Roosevelt Longworth, the first woman to smoke cigarettes in the White House in 1905.

Andrew thought that the quality of my posts was so good that I had to be a retired banker at least 55 years old. We didn’t meet in person until I was invited to work the summer out of the magazine’s St. James Street office tower, just down the street from the palace of then Prince Charles.

When he was introduced to a gangly 25-year-old instead, he thought it was a practical joke, which The Economist was famous for. As for me, I was impressed with Andrew’s ironed and creased blue jeans, an unheard-of concept in the Wild West where I came from.

The first unusual thing I noticed working in the office was that we were each handed a bottle of whisky, gin, and wine every Friday. That was to keep us in the office working and out of the pub next door, the former embassy of the Republic of Texas from pre-1845. There is still a big white star on the front door.

Andrew told me I had just saved the magazine.

After the first oil shock in 1973, a global recession ensued, and all magazine advertising was cancelled. But because of the shock, it was assumed that heavily oil-dependent Japan would go bankrupt. As a result, the country’s banks were forced to pay a ruinous 2% premium on all international borrowing. These were known as “Japan rates.”

To restore Japan’s reputation and credit rating, the government and the banks launched an advertising campaign unprecedented in modern times. At one point, Japan accounted for 80% of all business advertising worldwide. To attract these ads the global media was screaming for more Japanese banking stories, and I was the only person in the world writing them.

Not only did I bail out The Economist, I ended up writing for over 50 business and finance publications around the world in every English-speaking country. I was knocking out 60 stories a month, or about two a day. By 26, I became the highest paid journalist in the Foreign Correspondents’ Club of Japan and a familiar figure in every bank head office in Tokyo.

The Economist was notorious for running practical jokes as real news every April Fool’s Day. In the late 1970s, an April 1 issue once did a full-page survey on a country off the west coast of India called San Serif.

It warned that if the West coast kept eroding, and the East coast continued silting up, the country would eventually run into India, creating serious geopolitical problems.

It wasn’t until someone figured out that the country, the prime minister, and every town on the map were named after a type font that the hoax was uncovered.

This was way back, in the pre-Microsoft Word era, when no one outside the London Typesetter’s Union knew what Times Roman, Calibri, or Mangal meant.

Andrew is now 84 and I haven’t seen him in yonks. My business editor, the brilliant Peter Martin, died of cancer in 2002 at a very young 54, and the magazine still awards an annual journalism scholarship in his name.

My boss at The Economist Intelligence Unit, which was modeled on Britain’s MI5 spy service, was Marjorie Deane, who was one of the first women to work in business journalism. She passed away in 2008 at 94. Today, her foundation awards an annual internship at the magazine.

When I stopped by the London office a few years ago I asked if they still handed out the free alcohol on Fridays. A young writer ruefully told me, “No, they don’t do that anymore.”

Sometimes, change is for the worse, not the better.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-economist-e1664802946349.png285500Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-26 09:02:572023-06-26 12:08:01The Market Outlook for the Week Ahead, or Is there a Coup Underway in Russia?

Over the last few weeks, I picked up some astonishing developments in artificial intelligence.

*Mainframes at Stanford University and the University of California at Berkeley were given a direct connection to speak freely with each other. Within 30 minutes they dumped English as a means of communication because it was too inefficient and developed their own language which no human could understand. They then began exchanging immense amounts of data. Fearful of what was going on, the schools unplugged the machines after only eight hours.

*All of the soccer videos ever recorded were downloaded into two robots, but they were not taught how to play the game or given any rules. Not only did figure out how to play the game, it developed plays and maneuvers no one in the sport has ever thought of in its 150-year history.

*It normally takes a PhD candidate five years to 3D map a protein. An AI app 3D mapped all 200 million known proteins in seven weeks, shortcutting one billion years of PhD level research with existing technology. These new maps have already been used to design a malaria vaccine and enzymes that eat plastic. They will soon cure all human diseases.

*A developer asked an AI program a half dozen questions in Bengali, not an easy language. Within an hour, it spoke the language fluently, without any instructions to do so.

By now, word has gotten out about the incredible opportunities AI presents. Our only limitation is our own imagination on how to use it. AI will instantly triple the value of any company that uses it.

What has changed is that we now have millions of computers powerful enough and an Internet fast enough to realize its full potential.

It all vindicates my own long-term vision, unique in the investing community, that in the coming decade, immense technology profits will more than replace the trillions of dollars worth of Fed liquidity we feasted on during the 2010s. Extended QE is proving just a bridge to a much more prosperous future.

The Internet has created about $10 trillion in value since its inception. AI will create double that in half the time. That’s what will take the Dow from 33,000 to 240,000.

No surprise then that the top ten AI companies have delivered 120% of the stock market gains so far in 2023. The other 490 companies in the S&P 500 have either gone nowhere to down.

However, there are many things that AI can’t do. Here is the list.

1) AI Can’t Predict large anomalous events, otherwise known as Black Swans. AI takes past trends and extrapolates them into the future. It in no way could have seen 9/11, the 2008 crash or the pandemic coming, although I warned my hedge fund clients for years that we were overdue. All of the AI stock trading apps I have seen so far, including my own, max out at 90% accuracy. The other 10% is accounted for by black swans: earnings shocks, foreign crises, sudden FDA stage three denials, surprise legal judgments, foreign invasions, or the murder of a key man in a tech company, as recently happened in San Francisco.

2) AI Lies and Lies Often. AI was asked to write a scientific paper on a specific subject. It came back with an elegant and well-researched piece. The problem was that all of the books it made reference to didn’t exist. AI learned early to tell humans what they want to hear.

3) AI Requires Exponential Computing Capacity. Only five companies have the muscle to pursue true AI. No surprise that these, including (AAPL), (GOOGL), (AMZN), and (TSLA), account for the bulk of stock market performance this year. This won’t always be the case. Some 30 years ago, it required thousands of mainframes to contain all human knowledge. Today, that task can be accomplished with a cheap $1,000 laptop.

4) Internet Capacity Will Be a Limiting Factor for AI for Years. To accommodate the traffic that is taking place right now, the Internet will have to grow 500% practically overnight, and that is with five main players. What happens when we have 5 million? That’s why NVIDIA (NVDA) has gone nuts.

5) AI Hallucinates, as anyone who drives a Tesla will tell you. If a car makes a left turn in Florida, the 4 million vehicles in the world’s largest neural network learn from it. The problem is that sometimes the data from that Florida car is placed directly in front of a California one, prompting it to brake abruptly, causing accidents. This is known as “ghost braking.” I have explained to Elon Musk that his database has grown so large, eight video feeds per 4 million cars going back many years and billions of miles, that he may be going behind the limits of known physics.

6) While the Growth Opportunities for AI are Unlimited, the ability of humans and society to absorb it isn’t. All jobs will be affected by AI and millions destroyed, starting with low-level programmers and call centers, and millions more will be created. People are talking about regulating AI but have no idea where to start. Maybe with (AAPL), (GOOGL), (AMZN), and (TSLA)?

7) The Terminator Issue. Can AI be controlled? Or have we started a chain reaction that is unstoppable, as with an atomic bomb? AI researchers have noticed a disturbing issue where AI programs are learning skills on their own, without our instructions. This is referred to as “emergent properties.” If AI is using humans as its example, we can’t exactly count on it to be benign.

Needless to say, AI will be at the core of your investment approach, probably for the rest of your life.

2014 at Micron Technology

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/John-micron.png358293Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-31 09:02:022023-05-31 16:42:24What AI Can and Can’t Do

When Elon Musk personally invited me to tour his Gigafactory in Sparks, Nevada, I thought, “How could I pass on this?” He had read my recent report on Tesla and thought the more I know about Tesla the better.

I couldn’t agree more.

As I approached the remote facility 20 miles east of Reno, I spotted a herd of wild Mustangs on the red volcanic hills above. I thought it was a great metaphor for our rapidly evolving transportation system, from horse to all-electric in 100 years.

There are no signs to the Gigafactory until you approach the main gate. I had to find it with my GPS after inputting longitude and latitude. When you upset the apple cart for the global energy system, you make a lot of enemies. Once in, no cameras are allowed.

What I found inside what much what I saw at the original Fremont, CA factory 15 years ago: an army of robots building machines. The factory is in effect a machine that makes machines….by the millions. Occasionally, a worker would swan past with an oil can in his hand and squirt some lubricant into an important joint, then swan away.

If you want a view of the future, this is it.

Elon does nothing small.

The present factory occupies about 2 million square feet, or about 33 football fields. Some 60% of the world’s lithium-ion batteries come out of this one place right now, which are devoted to Tesla Model 3’s and Powerwalls, of which I own six. Japan’s Panasonic, which has the contract to supply the batteries, occupies a substantial part of the factory space.

When completed, it will occupy 6 million square feet, making it the world’s largest building. The planet’s greatest solar array sits on top, making the entire facility energy neutral when combined with local windmills. The plant is fully automated and runs 24/7. There are still a few of those pesky humans around to perform complex tasks which robots can’t do….yet.

The State of Nevada just granted Tesla a ten-year tax holiday to start the second phase, which will employ another 5,000. Whole cities are being carved out of the virgin desert to accommodate them, so the entire city of Reno is rapidly marching east. Burger Kings, Taco Bells, Subways, and Chinese and Mexican restaurants are popping up in the middle of nowhere.

It's all coming into place to assure that Tesla meets its 1.8 million vehicle target for 2023, up 40% from 2022. The last time someone had a technology lead this great was in 1913 when Henry Ford launched assembly lines that mass-produced Model T’s for the first time. He offered them for $400 each and doubled his workers’ pay to $5 a day to buy them. This gave Ford a 75% share of the US car market for two decades.

Elon Musk will achieve the same.

Which all raises a much larger issue.

The future is happening far faster than anyone realizes.

Tesla is just the tip of the iceberg in an AI/automation trend that is rapidly taking over the world. The net effect will be to double or triple the value of the companies that embrace these trends and wipe out those that don’t. ALL companies are AI plays. This is a large part of my Dow 240,000 in a decade prediction.

Microsoft brought out its office in 1990 and it instantly made ALL companies more valuable as they adopted it. The Dow Average soared by 20 times from $600 to $12,000. The same thing is going on now with AI.

If it worked before it will work again. A 20-fold return from here takes the Dow Average from $34,000 to $680,000, except it will happen much more quickly as technology is hyper-accelerating. Dow 240,000 looks like a chipshot.

If you think this is some kind of George Lucas THX 1138 prediction, think again. These are headlines I saw in the last week.

FedEx (FDX) is firing 86,000 drivers, to be replaced by robots. Uber (UBER) is replacing its 5 million drivers with autonomous drivers to increase reliability and cut costs. Dentists adopting AI to read X-rays are catching the 12% of cavities they miss, increasing fillings and increasing profits.

I often get asked for great AI plays in the market and there are no direct ones. But in five years, companies like Microsoft’s (MSFT) ChatGPT and Alphabet’s (GOOGL) DeepMind Technologies will be spun off and sold at enormous multiples to the public, creating a frenzy.

I’ve seen it all before.

What does doubling or tripling the value of surviving companies do to the economy? It reliquefies the financial system with immense corporate cash flows. All asset classes will rocket in value, including stocks, bonds, commodities, precious metals, energy, and real estate.

While the 2010s had endless quantitative easing and zero interest rates, the 2020s will have AI and robots. Except that this time we won’t have to rely on government handouts to get there.

Suddenly, Dow 240,000 looks cheap.

I just thought you’d like to know.

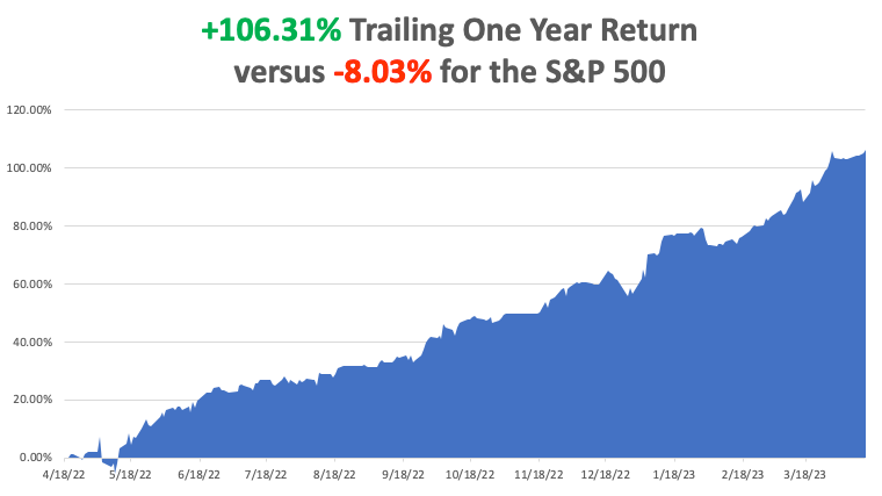

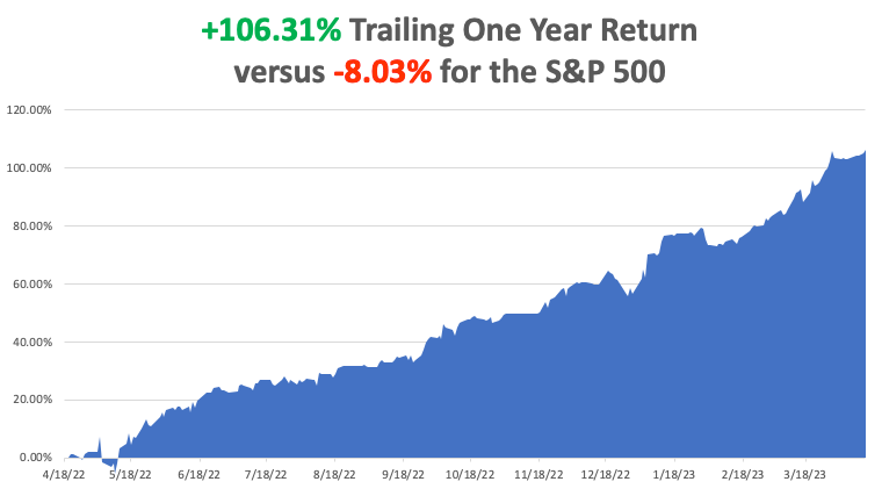

My big bet-the-ranch long in banks and brokers paid off huge. My 2023 year-to-date performance is now at an incredible +49.57%. The S&P 500 (SPY) is up only a miniscule +8.42% so far in 2023. My trailing one-year return maintains a sky-high +106.31% versus -8.03% for the S&P 500.

That brings my 15-year total return to +646.76%, some 2.73 times the S&P 500 (SPY) over the same period. My average annualized return has blasted up to +48.51%, another new high.

I executed four trades last week. I used the spectacular earnings beat at (JPM) to take profits and rolled that money into Boeing (BA), which had just been trashed. I also took profits on my expiring April bond long (TLT) and rolled it into a May bond long. I will run my remaining expiring April long positions in (TSLA), (BAC), (C), (IBKR), (MS), (and FCX) into the Friday, April 21 expiration.

Inflation Takes a Dive, dropping to a 5.6% YOY rate, the ninth consecutive month of decline. I think we will fall to 3%-4% by yearend, prompting the Fed to lower interest rates. That will spark a new bull market and another leg up for residential real estate. It all more fodder for the bull case. Given what the Fed has been facing, a mild recession would be a huge win.

Fed Minutes Fear Banking Crisis May Lead to a Mild Recession, killing off today’s nascent rally. It will also hobble job growth and lead to sharp declines in interest rates in 2024. Markets now see a 75% probability of a 25-basis point rate hike on May 3.

FedEx Looking to Fire All Drivers, moving to autonomously driven delivery vehicles. It may take 20 years but it’s in the works. (FDX) has already cut 12,000 jobs since June in an effort to maintain profitability and surpass rival (UPS). In 2022, (FDX) took in $93.5 billion in revenues delivering 3 billion packages, 9 for each American. I received more than my share.

PC Sales Drop 29% YOY, in Q1, adding more ammunition to the recession camp. Apple Macs led the charge to the downside with a heart-thumping 40% decline. The news slugged (AAPL). Only 56.9 million PCs we sold during the last quarter. Even with heavy discounting inventories remain high. Amazing, isn’t it?

Tesla Cuts Prices Again, knocking $3,000 off the Model 3 and $5,000 for the Model X. That sets the cat among the pigeons with traditional car companies desperately trying to catch up. Tesla is simply passing on the 50% drop in lithium prices this year. If they flush competitors out of business in the meantime so much the better. Ford has ordered designers to cut the number of parts by 80%, which Tesla did 14 years ago. (F) and (GM) are just too slow to react, even when the writing is on the wall.

$1.5 Trillion in Commercial Real Estate Debt coming due is a Threat to all asset classes. Refi’s are coming due that will double or triple interest rates from the zero-rate era and many won’t qualify. The sector is already being hammered by the “stay-at-home” work trend, with big tech firms virtually vacating whole office building in San Francisco. Regional banks may no longer have the capital to roll over at any prices given recent massive deposit withdrawals. Avoid commercial real estate REITS.

Banks Shares Explode to the Upside. JP Morgan announced blockbuster earnings, taking the stock up a ballistic $11, or 8.6%. Revenues came in at $39.34 billion versus an expected $36.19 billion. Adjusted EPS was $4.32 a share versus an expected $3.41. It is the biggest gap up in share prices on an earnings announcement in 20 years. As a result, we are just short of the maximum profit in our long (JPM), with the shares up an eye-popping 21% from the nearest strike price.

PPI Gives Another Deflation Hint, dropping a shocking 0.5% in March to only a 2.7% YOY rate. That’s a big drop from 4.9% in February. It’s the lowest inflation indicator in two years. Stocks loved the news, jumping $383. Low inflation, and therefore sharp interest rate cuts are coming within reach.

Boeing Goes Back in the Penalty Box, with a recurring bulkhead problem halting 737 MAX production. The stock dumped 8%. Buy (BA) on the dip. They’ll fix it. The company has a massive order backlog of 4,000 planes and will crush it on the earnings. The 737 MAX will shortly be flying again, the company’s largest selling product. With the airline business booming a global aircraft shortage has emerged. The end of the trade wars with China will bring a resurgence of orders there. And Boeing just surpassed Airbus in aircraft deliveries in Q1

Weekly Jobless Claims Jump 11,000 to 239,000, showing that the Fed’s harsh medicine is starting to work. It’s all consistent with a stock market that may start to roll over soon.

Private Sector Payrolls Slow to 145,000, according to ADP, a substantial drop from the previous month. Financials took the big hit with a loss of 51,000 jobs, followed by Business Services at 46,000. Leisure & Hospitality leads again with a 98,000 gain. It is more evidence of the economic slowdown the FED has been attempting to engineer for the past year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 17 at 7:30 AM EST, the New York State Manufacturing Index is out.

On Tuesday, April 18 at 6:00 AM, the US Building Permits are announced. On Wednesday, April 19 at 11:00 AM, the Fed Beige Book is printed. On Thursday, April 20 at 8:30 AM, the Weekly Jobless Claims are announced. Existing Home Sales are out.

On Friday, April 21 at 8:30 AM, the Global Composite Flash PMI is released. We also get the April options expiration at the 4:00 PM stock market close.

As for me, I don’t get invited to help design new nuclear weapons systems very often. So when the order came from Washington to report to Los Alamos, New Mexico, I was on the next plane.

When the Cold War ended in 1992, the United States judiciously stepped in and bought the collapsing Soviet Union’s entire uranium and plutonium supply.

For good measure, my client George Soros provided a $50 million grant to hire every Soviet nuclear engineer. The fear then was that starving scientists would go to work for Libya, North Korea, or Pakistan, which all had active nuclear programs. There ended up here instead.

That provided the fuel to run all US nuclear power plants and warships for 20 years. That fuel has now run out and chances of a resupply from Russia are zero. The Department of Defense attempted to reopen our last plutonium factory in Amarillo, Texas, a legacy of the Johnson administration.

But the facilities were deemed too old and out of date, and it is cheaper to build a new factory from scratch anyway. What better place to do so than Los Alamos, which has the greatest concentration of nuclear expertise in the world.

Before they started, they launched a nationwide search for those who were still alive and had nuclear expertise the last time we made our own plutonium, and they came up with….me?

Los Alamos is a funny sort of place. It sits at 7,320 feet on a mesa on the edge of an ancient volcano so if things go wrong, they won’t blow up the rest of the state. The homes are mid-century modern built when defense budgets were essentially unlimited. As a prime target in a nuclear war, there are said to be miles of secret underground tunnels hacked out of solid rock.

You need to bring a Geiger counter to garage sales because sometimes interesting items are work castaways. A friend almost bought a cool coffee table which turned out to be part of an old cyclotron. And for a town designing the instruments to bring on the possible end of the world, it seems to have an abnormal number of churches. They’re everywhere.

I have hundreds of stories from the old nuclear days passed down from those who worked for J. Robert Oppenheimer and General Leslie Groves, who ran the Manhattan Project in the early 1940s. They were young mathematicians, physicists, and engineers at the time, in their 20’s and 30’s, who later became my university professors. The A-bomb was the most important event of their lives.

Unfortunately, I couldn’t relay this precious unwritten history to anyone without a security clearance. So, it stayed buried with me for a half century, until now. Suddenly, I had an entire room of young scientists who were fair game, and it was fun relaying stories, they hung on my every word. It was like being a Revolutionary War buff and out of the blue you meet someone who knew George Washington.

Some 1,200 engineers will be hired for the first phase of the new plutonium plant, which I got a chance to see. That will create challenges for a town of 13,000 where existing housing shortages already force interns and graduate students to live in tents. It gets cold at night and dropped to 13 degrees F when I was there.

As a reward for my efforts, I was allowed to visit the Trinity site at the White Sands Missile Test Range, the first visitor to do so in many years. This is where the first atomic bomb was exploded on July 16, 1945. The 20-kiloton explosion set off burglar alarms for 200 miles and was double to ten times the expected yield.

Enormous targets hundreds of yards away were thrown about like toys (they are still there). Half the scientists thought the bomb might ignite the atmosphere and destroy the world but they went ahead anyway because so much money had been spent, 3% of the US GDP for four years. Of the original 100-foot tower, only a tiny stump of concrete is left (picture below).

With the other visitors, there was a carnival atmosphere as people worked so hard to get there. My Army escort never left me out of their sight. Some 78 years after the explosion, the background radiation was ten times normal, so I couldn’t stay more than an hour.

Needless to say, that makes uranium plays like Cameco (CCJ), NextGen Energy (NXE), Uranium Energy (UEC), and Energy Fuels (UUUU) great long-term plays, as prices will almost certainly rise and all of which look cheap. US government demand for uranium and yellow cake, its commercial byproduct, is going to be huge. Uranium is also being touted as a carbon-free energy source needed to replace oil.

I know the numbers, but I can’t tell you as they are classified. Otherwise, I’d have to kill you and you might not renew your subscription to Mad Hedge Fund Trader.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

At Ground Zero in 1945

What’s Left of a Trinity Target 200 Yards Out

Playing With My Geiger Counter

Atomic Bomb No.3 Which was Never Used

What’s Left from the Original Test

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/john-thomas-atomic-bomb.jpg282302Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-17 09:02:082023-04-17 14:52:51The Market Outlook for the Week Ahead, or Preparing for the Next Liquidity Surge

That is the question plaguing traders and portfolio managers alike around the world. For the average bear market is only 9.7 months long and we are already 16 months into the present one.

Even the longest postwar bear market was only 2.5 years, or 30 months, the 2000-2002 Dotcom Bust, and we are nowhere near that level of economic hardship. Back then, companies posted losses for several quarters in a row, and many ceased to exist (Webvan, Alta Vista, Pets.com).

That means we only have a few more months of pain to take before another decade-long bull market resumes, or 8 months if the bear stretches to a full two years.

That is unless the new bull was actually born last October, which is entirely possible. Certainly, the stock market thinks so, with its refusal to drop on even the worst of news.

Inflation at 6%? Who cares.

A Fed that hates the stock market? Couldn’t give a damn.

Pathetic earnings growth? Call me when it’s over.

This indifference chalked up the deadest trading week I can remember, putting the Volatility Index (VIX) firmly back into “Do Nothing Land” under 20%.

So investors are cautiously putting cash into stocks on every dip, even minor ones, confident that they will be higher by yearend. If a black swan arrives in the meantime, or a political crisis boils out of control, tough luck if you can’t take a joke.

All of which is focusing a lot more attention on gold (GLD), which moved within 2% of a new all-time high last week. I am always looking for cross-asset class confirmations of current trends and the barbarous relic has certainly been one of those.

I have been bullish on gold since I put out LEAPS on Barrick Gold (GOLD) and silver (SLV) last October. They have since performed spectacularly well. The move into precious metals confirms the following. That the Fed tightening cycle will end imminently. Interest rates will fall, and the US dollar (UUP) will weaken. Everything else flows from there.

You are even seeing this in US Treasury Bond yields, with the ten-year plunging to 3.30%, a one-year low. The (TLT) hit $109 last week. Aren’t bonds supposed to be held back by the looming default by the US government?

I’m starting to wonder if the debt ceiling crisis is this generation’s Y2K. At worst, your toaster may show the wrong year but nothing further. Or maybe the pent-up demand for bonds and high yields is so great that it overwhelms all other considerations?

My 2023 year-to-date performance is now at an incredible +46.38%. The S&P 500 (SPY) is up only a miniscule +7.0% so far in 2023. My trailing one-year return maintains a sky-high +103.2% versus +7.0% for the S&P 500.

That brings my 15-year total return to +643.57%, some 2.71 times the S&P 500 (SPY) over the same period. My average annualized return has blasted up to +48.26%, another new high.

I executed no trades during the holiday-shortened week, content to run my ten profitable positions into the April 21 options expiration. If a strategy ain’t broke, don’t fix it. If I see something I like, I’ll take profits on an existing position and replace it with a new one.

Nonfarm Payroll Report Holds Up, at 236,000 in March, the lowest since December 2020. It shows that high interest rates still have not impacted the jobs market. February was revised up to 326,000. The headline Unemployment Rate dropped back to a 50-year low at 3.5%. Average Hourly Earnings dropped to 4.2% YOY, a two-year low, showing that inflation is in retreat. Leisure & Hospitality led at 74,000 followed by Government at 47,000.

Weekly Jobless Claims Drop, to 228,000, down 18,000 as recession fears rise. High interest rates are finally taking their toll, with a banking crisis thrown in for good measure.

Open Jobs Tighten, The June JOLTS survey of job openings fell to 10.698 million, down from 11.3 million last month and well below expectations of 11 million. Is this the calm before the storm when job openings disappear? This report is highly negative for the US dollar.

Tesla (TSLA) Posts Record EV Deliveries, Deliveries grew 36% from a year ago, below the 50% growth Elon Musk promised for the year on the last earnings call, but Musk has a habit of overpromising. The expansion is still a healthy sign that consumers are spending. Any pullback in Tesla is a gift for shareholders.

Oil (USO) Production Cut Sends Price Soaring, with OPEC+ including Russia has pledged a total of 3.66-million-barrel oil output cut which is nearly 3.7% of global demand. The jump in oil price will only accelerate global inflation and force the Fed into a tougher predicament. The Saudi – US cooperation is at its lowest ebb.

Walmart’s (WMT) Automation Effort Goes Into Overdrive, Walmart said it expects around 65% of its stores to be serviced by automation by 2026. The company said around 55% of packages that it processes through its fulfillment centers will be moved to automated facilities and unit cost average could improve by around 20%. This is the first step to getting rid of human employees. Eventually, the government will need to deliver universal basic income (UBI).

Gold and Miners Threaten New All-Time Highs, suggesting that a collapse in interest rates is imminent. So is an economic recovery and a resurgence of monetary expansion. Russian and China continue to be major buyers to evade sanctions. Keep buying (GLD) and (GOLD) on dips.

Apple (AAPL) Cash Hoard Soars to $165 Billion, as the cash flow king of all time goes from strength to strength. This will be one of the top targets in any tech rebound, which may be imminent. But you’re have to compete with apple to buy the shares, which is a huge buyer of its own stock.

Chip Stocks are On Fire, clocking the best sector of any in Q1. Too far, too fast, say I, but I’ll be in there buying with both hands on any serious dips. This is no future without (NVDA), (MU), and (AMAT) playing a major role.

Stock Dividends Hit New All-Time Highs, at $146.8 billion, up 7% YOY. As interest rates rose, companies had to raise dividends to keep up. The economy is also far stronger those most realize, with many analysts believing we should have entered a recession a long time ago. A high dividend also gives downside protection in bear markets.

Uranium Demand is Surging with the Nuclear Renaissance. And now the US is restarting plutonium production for the first time in 20 years, a uranium derivative. The 20-year supply we bought from the old Soviet Union has run out with a scant chance of renewal. The Los Alamos Labs in New Mexico is seeking to hire 1,200 engineers to build a brand-new factory from scratch. Buy (CCJ) on dips. And buy Los Alamos real estate if you can get a security clearance.

Keep Buying 90-Day T-Bills, now pushing a 5% risk-free yield. The regional banking crisis highlights another reason. If your bank or broker goes under, your cash deposits can be tied up in bankruptcy for three years. If you own US government securities, they can be ordered and transferred out in days to another institution. You can also buy them directly from the US government free of fee. Just thought you’d like to know.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 10 at 7:30 AM EST, the Consumer Inflation Expectations are out.

On Tuesday, April 11 at 6:00 AM, the NFIB Business Optimism Index is announced. On Wednesday, April 12 at 7:00 AM, the US Core Inflation Rate and Consumer Price Index are printed. On Thursday, April 13 at 8:30 AM, the Weekly Jobless Claims are announced. The Producer Price Index is also released.

On Friday, April 14 at 8:30 AM, the US Retail Sales are released.

As for me, I covered the Persian Gulf for Morgan Stanley for ten years during the 1980s when medieval sheikdoms still living in the 14th century were suddenly showered with untold wealth. Needless to say, the firm, which we called Morgan Stallion, had a few ideas on what they should do about it.

I was picked as the emissary to the region because I had already been visiting the Middle East for 20 years and had been doing business there for 15 years. My press visa to cover the Iran-Iraq War was still valid.

In addition, I had already developed a reputation for being wild, reckless, and up for anything to enjoy a thrill or make a buck. In addition, with all the wars, terrorist attacks, and revolutions underway, everyone but me was scared to death to go near the place.

In other words, I was perfect for the job.

Being a veteran combat pilot proved particularly useful. I used to fly down on Kuwait Airlines and I still have a nice collection of the cute little Arabic artifacts they used to hand out in first class. Once in Abu Dhabi, I rented a local plane and hopped from one sheikdom to the next drumming up business. Once, I landed on a par five fairway at a private golf course just to give a presentation to a nation’s ruler.

My last stop was always Kuwait, where I turned the plane back in and met the CIA station chief for lunch to fill him in on what I had learned. It was all considered part of the job. When Iraq invaded Kuwait in 1991, I was their first call.

Of course, flying across vast expanses of the Arabian desert is not without its risks. Whenever you fly a single-engine plane you are betting your life on an internal combustion engine, never a great idea. I always carried an extra gallon bottle of water in case of a forced landing. The survival time without water is only three days.

Whenever I refueled, I filtered the 100LL aviation gas through a chamois cloth to keep out water and sand. Still, I was pretty good at desert survival, growing up near Indio California in the Lower Colorado Desert and endlessly digging my grandfather’s pickup truck out of the sand.

Once my boss tried to ban me from a trip to the Middle East because the US Navy had bombed Libya. I assured him that something as minor as that didn’t even move the needle on the risk front, at least in my lifetime.

The problem with the Persian Gulf was that they had all the money in the world and no way to spend it. An extreme Wahabis religion was strictly adhered to, and alcohol was banned. But you could have four wives and I enjoyed some of the best fruit juice in my life.

So my clients came to rely on me for diversions. The Iran-Iraq War was taking place then. I took them up in my plane to 10,000 feet and we watched the aerial war underway 50 miles to the north. The nighttime display of rockets, machine gun fire, and explosions was spectacular.

During one such foray, the wind shifted dramatically as a sandstorm rolled in. Suddenly I was landing in a 50-knot crosswind instead of a 10-knot headwind. A quick referral to the aircraft manual confirmed that the maximum crosswind component for the plane was 27 knots.

Oops!

Then I got a bright idea. I radioed the tower and asked for permission to land on the taxiway at a 90-degree angle to the main runway. After some hesitation, they responded, “If you’re willing to try it”. They knew my only alternative was to ditch at sea with two high-ranking gentlemen who couldn’t swim.

The tower very kindly talked me down with radar vectors and at the last possible second, with the altimeter reading 20 feet, the taxiway popped into view. With such a stiff wind I was able to pancake the plane down in yards, slam it on the runway, and then immediately shut the engine down. I asked for a tow, not wanting to risk the windstorm flipping the plane over.

My passengers thanked me profusely.

When Iraq invaded Kuwait in 1991, I lost most of my friends there. They were either killed, kidnapped and held for ransom, or volunteered as translators for US forces. I never saw them again.

I didn’t return to the Middle East until 2019 when I took two teenage girls to Egypt to introduce them to that part of the world. They wore hijabs, rode camels, and opened their eyes. I even set up some meetings with an educated Arab woman.

I will probably go back someday. I still haven’t seen the ruins at Petra in Jordan, nor ridden the Hijaz Railway, which Lawrence of Arabia blew up in 1918. But I have an open invitation from the king there.

I knew his dad.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/john-and-daughters-egypt.jpg352260Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-10 09:02:282023-04-10 15:50:59The Market Outlook for the Week Ahead, or Mad Hedge Clocks 46.38% Profit in Q1

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.