Mad Hedge Technology Letter

October 17, 2022

Fiat Lux

Featured Trade:

(THE BIG TALK)

(SOXX), (CHINA), (NVDA), (MU), (LNG)

Mad Hedge Technology Letter

October 17, 2022

Fiat Lux

Featured Trade:

(THE BIG TALK)

(SOXX), (CHINA), (NVDA), (MU), (LNG)

A lot of people haven’t talked about what’s going on in China. Other world events have lessened the focus in the East.

Yet people should be talking about China now.

Authoritarian China is a way bigger deal than what’s happening in the backwaters of Eastern Europe, and I’ll explain.

What on earth could overshadow all of that?

The US administration announced Chinese semiconductor bans, essentially blocking the transfer of intellectual property to China and forcing American executives to quit en masse or face the risk of losing US citizenship.

To say this is escalatory is an understatement.

Remember that previous US president Donald Trump forced the same interests to apply for special licenses, but never ramped up the tension to fever pitch and allowed business to advance.

The result is every American executive and engineer working in China’s semiconductor manufacturing industry resigning, paralyzing Chinese manufacturing overnight.

When combined with a global demand reduction, this is a heavy blow to the short-term prospects of American chip companies (SOXX) that have deep interests in China such as Applied Materials, Intel, Micron (MU), Nvidia (NVDA) and AMD.

US Commerce department also levied a bevy of restrictions on supplying US machinery that’s capable of making advanced semiconductors. It’s going after the types of memory chips and logic components that are at the heart of state-of-the art designs.

For companies with plants in China, including non-US firms, the rules will create additional hurdles and require government signoff.

South Korea’s SK Hynix Inc. is one of the world’s largest makers of memory chips and has facilities in China as part of a supply network that sends components around the world.

The biggest name to be added to the list ban is Yangtze Memory Technologies Co. The memory-chip maker is considered the most successful chip company in China wielding the best technology obviously thanks to American technology.

I found it interesting that at almost the same time, China instructed local resellers to stop selling liquid natural gas (LNG) to Europe as mounting proof China views Europe and America through the same lens.

The rapid escalation means the fragmenting of the United States economy and China will accelerate into the future resulting in the inevitable on-shoring of American chip factories back to the United States which we are already seeing.

Other industries will need to be on-shored back to United States and other friendly countries too.

In the short to mid-term, this means higher costs for the American chip companies as reinvesting into capital projects are a multi-billion dollar proposition.

Also, the pain of losing the large China market hurts badly for the stock and is damaging to the annual revenue outlook.

Expect many revenue downgrades coming down the pipeline.

Inflationary costs is another driver of revenue downgrades too as paying these specialists and keeping the lights on have gotten more expensive.

The chip companies won’t be able to substitute the China demand when we are on the verge of recessions in the United States and Europe.

Ultimately, the infamous boom-bust cycle for the chip stocks will get a more prolonged bust this time around as demand and supply are both painfully reduced.

The boom also will be larger because of coming from a lower cost basis.

However, I would highly doubt a bounce back of any chips stocks in the short-term unless broader market forces drag up stocks which could happen.

We will most likely experience strong bear market rallies met by thundering selloffs.

I would avoid any long term investments into chip companies now and just trade the bounces short-term.

Global Market Comments

October 10, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or EATING YOUR SEED CORN),

(SPY), (TLT), (PANW), BRKB), (JPM), (MS), (V),

(USO), (MU), (RIVN), (TWTR), (TSLA)

You know that 10% downside risk I talked about? In other words, you may have to eat a handful of your seed corn.

We may have to eat into some of that 10% this week. With the September Consumer Price Index out on Thursday, and the big bank earnings are out Friday, there is more than a little concern about the coming trading week.

That’s why all my remaining positions are structured to handle a 10% correction or more and still expire at their maximum profit point in nine trading days.

Even in the worst-case Armageddon scenario, which we are unlikely to get, the S&P 500 is likely to fall below 3,000, or 627.90 points or 17.25% from here.

That’s what you pay me for and that’s what you are getting.

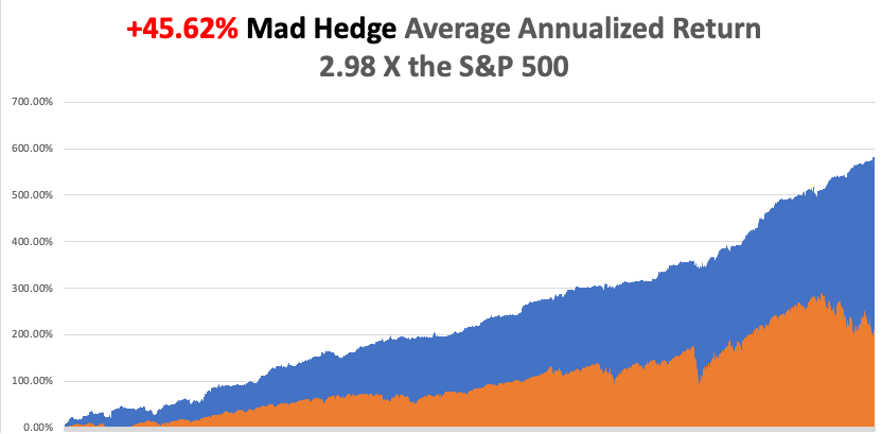

I shot out of the gate with an impressive +3.25% gain so far in October. My 2022 year-to-date performance ballooned to +72.93%, a new high. The Dow Average is down -19.3% so far in 2022 or a gob-smacking -7,000 points. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +81.35%.

That brings my 14-year total return to +585.49%, some 3.03 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.62%, easily the highest in the industry.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

I used last week’s extreme volatility to rearrange positions, adding longs in Morgan Stanley (MS), JP Morgan (JPM), and Visa (V). That takes me to 80% long, 20% short, and 0% cash. I wisely rolled down the strikes on my Tesla position from $230-$240 to $200-$210. I covered one short in the S&P 500 (SPY). All of my options positions expire in only nine trading days.

I know that you’re probably getting boatloads of advice the sell all your stocks now, sell your house, and head for those generous 5% short term interest rates, and 8% in junk. Even I went 100% cash….in December last year. The problem is that these other gurus are giving you advice that is only a year late with perfect 20/20 hindsight.

To bail now, you risk giving up on the 100% gains in years to come. If I’m wrong, you lose 10%, if I’m right, you get a double or more. Sounds like a pretty good bet to me.

People always want to know how I pick market bottoms, something I have been doing since the Dow Average was at a miniscule $753.

The lower the market is, the less aggressive the Fed is going to be

Every single input into the Consumer Price Index is now turning down sharply, especially rents and housing costs, meaning we can expect a blockbuster decline when the next report comes out on October 13

We now have two outsiders doing the Fed’s job for it, the British economy, which is clearly collapsing, and a strong US dollar that is rapidly shrinking the foreign revenues of our multinationals, like big tech.

Capitulation indicators, occasionally spotted here and there, are now coming in volleys, the Volatility Index at $35, the (VIX) curve inversion, the RSI below 30, the ten-year US Treasury yield hit 4.0% and then instantly backed off, the British pound plunged to $1.03, and we saw absolutely massive retail selling in September.

The froth is now out of all tech stocks.

All of this brings forward the last Fed hike in interest rates and the next bull market in stocks. If the last Fed rate hike is two months away on December 14, then the reasons to sell stocks are disappearing like the last sands in an hourglass.

In my mere half century in the market, every time the CPI starts to fall, stock market “V” bottoms and begins classic “rip your face off’ rallies as the shorts panic to cover. It happened in 1970, 1974, 1980, 1990, and 2009. It will happen again in 2022. The market will smell that inflation is done, the Fed is done, and volatility becomes a distant memory.

And I hate to be so obvious, but if you sell in May, what do you do in October? You buy with both hands. Just do it on the right day. That could get you a 10% to 20% move by yearend. The S&P 500 earnings multiple has collapsed by eight points in nine months and that is too far, too fast.

How do midterm years perform? October is the best month of the year followed by November. Of the entire 16-month presidential election cycle, the coming first quarter of 2023 is the best of the entire lot.

Nonfarm Payroll Falls Short at 263.000 in September. The headline unemployment rate matched a 2022 low at 3.5%. The long-term unemployment rate, the U-6 also matched this year’s low at 6.7%. The report keeps the Fed on its current interest raising schedule. Stocks, bonds, and gold sold off 500-points.

JOLTS Drops Sharply, from an expected 11.0 million to only 10.05 million. This is the job openings report from the Department of Labor. It’s one of the sharpest declines in history. The jobs market is finally starting to deteriorate, which is just what the Fed wanted. Factory Orders for August were unchanged.

OPEC+ Cuts Quotas by 2 million, and production by 1 million, in one of the largest reductions in history. It’s an effort to maintain oil prices at current prices in the face of falling demand from a global recession. The Arabs are not your friends. It’s also a slap in the face of the anti-oil posture, pro-climate posture of the Biden administration, which responded with a further release of 10 million barrels from the Strategic Petroleum Reserve. Energy stocks soar across the board. Don’t get caught standing when the music stops playing. Avoid (USO).

Why Did Russia Blow Up Their Own Pipeline? International analysts are puzzled by Putin’s latest hostile move. Is this a prelude to limited nuclear war in Ukraine? My view is that Putin expects to be deposed soon and wants to make it difficult for the next government to resume relations with Europe. Others argue that the true motivation is to enable Nordstream to file a $10 billion insurance claim. Good luck collecting on that one.

Advanced Micro Devices Bombs on weak PC sales and supply chain problems, taking the stock down 5% aftermarket. Profit margins were cut. The news could take the stock down to new lows, which didn’t really participate in this week’s monster rally. The rest of the tech sector sold off in sympathy.

Tesla Breaks Production Records in Q3, manufacturing 365,000 EVs and delivering 365,000, a record high. Sales prices have risen three times this year, while commodity costs have fallen dramatically, widening profit margins. This is the most volatile stock in the market, with one 52% correction so far this year, and another 23% correction in recent weeks. It’s the reason we just saw a “buy the rumor, sell the news” type correction that took us to the bottom of a three-month range.

Another factor is that now that big tech is rallying again, people are rotating out of Tesla, which held up well in Q3. Below here, long term Tesla bulls like my friend Ron Baron, Cathie Wood, and I start adding to big positions. With OPEC+ threatening a million barrel a day production cut, taking crude up 6%, oil alternative Tesla should be rising.

Elon Musk Pays Full Price for Twitter at $54.20 a share, completely caving on pending litigation. Wall Street consensus is that the company is worth $15 a share. It may be years before we learn what’s really going on here, leaving many scratching their heads, including me. Tesla (TSLA) plunged $15 on the news, killing off a nascent rally. The distraction of management time will be huge. Avoid (TWTR).

Rivian Raises 2025 Production Goal, from 20,000 to 25,000, after a better-than-expected 7,363 third quarter. Mass production is reaching the sweet spot for the next Tesla. The company is planning a $5 billion investment in non-union Georgia. Buy (RIVN) on dips, sell short puts and buy LEAPS.

Micron Technology to Invest $100 Billion in New York Plant. It’s all part of a retreat from China and paring war risk in Taiwan. Massive government subsidies from the Chips Act helped. Biden also expanded restrictions on the export of key semiconductor manufacturing equipment, America’s crown jewels. It means more expensive buy safer supplied chips for US industry. Buy (MU) on dips.

Hurricane Ian to Cost Insurers $63 Billion, and deaths, and the federal government may be on the hook for more. The storm double-dipped, cutting a wide swath across Florida and the Carolinas. Some 95% of the costs are carried by foreign insurers through the reinsurance market. There are too many billionaire mansions on the beach which are fully insured. This paves the way for major rate increases by insurance companies, which is why Warren Buffet loves the insurance business. Many thanks to the many foreign Mad Hedge subscribers who expressed sympathy over the storm losses.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil in a sharp downtrend and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 10, no data of note is released.

On Tuesday, October 11 at 7:00 AM, the 6:00 AM, the NFIB Business Optimism Index for September is released.

On Wednesday, October 12 at 8:30 AM, Producer Price Index for September is published. At 11:00 AM, the FOMC minutes from the last Fed meeting is released.

On Thursday, October 13 at 8:30 AM, Weekly Jobless Claims are announced. We also get the blockbuster Consumer Price Index.

On Friday, October 14 at 8.30 AM, US Retail Sales for September is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, with the 35th anniversary of the October 19, 1987 crash coming up, when shares dove 22.6% in one day, I thought I’d part with a few memories.

I was in Paris visiting Morgan Stanley’s top banking clients, who then were making a major splash in Japanese equity warrants, my particular area of expertise.

When we walked into our last appointment, I casually asked how the market was doing (Paris is six hours ahead of New York). We were told the Dow Average was down a record 300 points.

Stunned, I immediately asked for a private conference room so I could call the equity trading desk in New York to buy some stock.

A woman answered the phone, and when I said I wanted to buy, she burst into tears and threw the handset down on the floor. Redialing found all Transatlantic lines jammed.

I never bought my stock, nor found out who picked up the phone. I grabbed a taxi to Charles de Gaulle airport and flew my twin Cessna as fast as the turbocharged engines could take me back to London, breaking every known air traffic control rule.

By the time I got back, the Dow had closed down a staggering 512 points, taking the Dow average down to $1,738.74. Then I learned that George Soros asked us to bid on a $250 million blind portfolio of US stocks after the close. He said he had also solicited bids from Goldman Sachs, Merrill Lynch, JP Morgan, and Solomon Brothers, and would call us back if we won.

We bid 10% below the final closing prices for the lot. Ten minutes later he called us back and told us we won the auction. How much did the others bid? He told us that we were the only ones who bid at all!

Then you heard that great sucking sound. Oops!

What has never been disclosed to the public is that after the close, Morgan Stanley received a margin call from the exchange for $100 million, as volatility had gone through the roof, as did every firm on Wall Street.

We ordered JP Morgan to send the money from our account immediately. Then they lost it! After some harsh words at the top, it was found. That’s when I discovered the wonderful world of Fed wire numbers.

The next morning, the Dow continued its plunge, but after an hour managed a U-turn, and launched on a monster rally that lasted for the rest of the year. We made $75 million on that one trade from Soros.

It was the worst investment decision I have seen in the markets in 53 years, executed by its most brilliant player. Go figure. Maybe it was George’s risk control discipline kicking in?

At the end of the month, we then took a $75 million hit on our share of the British Petroleum privatization, because Prime Minister Margaret Thatcher refused to postpone the issue, believing that the banks had already made too much money.

That gave Morgan Stanley’s equity division a break-even P&L for the month of October 1987, the worst in market history. Even now, I refuse to gas up at a BP station on the very rare occasions I am driving an internal combustion engine.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 26, 2022

Fiat Lux

Featured Trade:

(AUGUST 24 BIWEEKLY STRATEGY WEBINAR Q&A),

(UNG), (AAPL), (MU), (AMD), (NVDA),

(META), (VIX), (MCD), (UBER)

Below please find subscribers’ Q&A for the August 24 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: I’ve heard another speaker say that we are not heading for a Roaring Twenties; instead, we are heading for a Great Depression. Who is right?

A: There are many different possible comments to this. Number one, in the newsletter business, the easiest way to make money is to predict the Great Depression and panic people. Stock market Gurus have been predicting the next Great Depression for all of the 54 years that I have been in the financial markets. We’ve gone through a whole series of Dr. Doom's over this time. We had Nouriel Roubini, we had Henry Kaufman, and before that, there was Joe Granville who predicted Dow 300 when the Dow was at 600 and never gave up. The reason is very simple: the people making these dire forecasts are based in depressionary places. If you live in Puerto Rico, or Ukraine, or Europe, it’s easier to be depressed right now, because the economy is falling to pieces. If you live in Silicon Valley, like I do, and you see these incredible technologies delivering every day, it’s easy to be bullish about the future. So, that is another part of it. On top of that, we’ve just had a recession. And even during this last recession, earnings continued to grow at 5% for the main market, and 20-30% for individual technology companies. The market goes up 80% of the time so if you’re bullish, you’re right 80% of the time. In fact, that may increase going into the future because we just had six months of down days behind us.

Q: How do you know when to buy?

A: Well, I have about 100 different market indicators that I look at, but my favorite one is the Volatility Index (VIX). The (VIX) is the perfect contrary indicator because when fear is high the payoff for taking on risk is huge. The risk/reward swings overwhelmingly in your favor. The simplest indicators are usually the best ones. When (VIX) gets to $30—I don’t think I’ve ever lost money in my life adding on a new trade with (VIX) at $30. If I add positions with the (VIX) at under $30, the loss rate goes up; so, I’m inclined to only do trades when the (VIX) gets close to $30. If that means doing nothing for a month, that’s fine with me. If telling you to stay out of the market makes more money than getting you into the market, I’ll keep you out of the market. I’m not a broker so, I don’t get paid commission; I get paid to give you the highest annual returns so you’ll renew because I only get paid if you renew. Our renewal rate is about 80% these days, and the other 20% either die or retire.

Q: What about the Tesla (TSLA) 3:1 split?

A: In the short term I would stand back and do nothing because you often get a “buy the rumor sell the news” selloff in stocks after splits. Long term, Tesla is a strong buy; short term, we are up close to 60% in a couple of months. Betting that Tesla would rise going into this split was one of the most successful trades that I’ve ever done.

Q: Did you know Julian Robertson?

A: Yes, I did. Julian was one of the first investors in my hedge fund, and then he was one of the first buyers of my Mad Hedge newsletter. He was also my first concierge client. He had one heck of a temper; if you didn’t know your stuff cold, he would just absolutely blow up at you. But he did tend to surround himself with geniuses. He drew on Morgan Stanley people a lot, so I knew a lot of the tiger cubs. But he certainly knew stocks, and he knew markets.

Q: What do we do on the SPDR S&P 500 ETF (SPY) position?

A: Just run it into expiration. As it is my only position, I don’t really have anything else to do and I don’t really see any explosive upside moves in markets this month. And then after that, we will be 10 days to expiration; so there may be enough profit there at that time.

Q: As a long-term investor, should I take Tesla profits now?

A: If you're really a long-term investor and sell now, you’ll miss the move to $10,000. However, if you’re a trader, you should take some profits now and look to buy and scale in down $50 and more down $100, and so on, depending on what the market does.

Q: What are your thoughts on Nvidia Corporation (NVDA) and semis?

A: When recession fears exist, you will have sharp downturns in the semis, because this is the most volatile sector in the market. However, in the long term in Nvidia you might be looking at a 20% of downside, and 200% of upside on a three-year view. It just depends on how much pain you want to take while keeping your long-term position.

Q: Why is September typically the worst month of the year for stocks?

A: You need to go back 120 years when farmers accounted for 50% of the US population. In the farming business, September/October is your maximum stress point, because you’ve put out all your money for seed, for water, for fertilizer, but you don’t get paid until you sell your crop in September/October. That creates a point of maximum stress—when farmers have to max out the loans from the banks, and that creates cascading stresses in the financial system. That’s why almost every stock market crash happened in October. And of course, since that cycle started, it has become a self-fulfilling prophecy to this day. Even though only 2% of the population is in farming now, that selloff in September/October is still there. There’s no real current reason behind it.

Q: How do you find good spreads?

A: You find a good stock first, then a good chart, and then wait for the market to come to you with a high Volatility Index (VIX) with a good micro and macro tailwind. It’s that simple.

Q: Do you think healthcare will sell off once the recession fear is gone?

A: It may not because it had a massive selloff across the entire industry when COVID went away. They've taken that COVID hit. That's a recession if you’re a healthcare company. Now COVID is essentially gone, so they haven’t got it left to lose. In the meantime, technology continues to hyper-accelerate in the healthcare area, just in time for old people like me.

Q: How would you invest $1 million in a retirement portfolio today?

A: Call me—that’s a longer conversation. Or better yet, sign up for the concierge service, and we can talk as long as you want.

Q: Any hope for Facebook (META)?

A: No, when you’re advertising that you’re going to lose money and that you’re not going to make money for five years, that’s bad for the stock. I’m sorry Mr. Zuckerberg, but you should have taken those financial markets classes instead of just doing the programming ones.

Q: Will Powell be dovish or hawkish in his speech?

A: I think he has to go hawkish because he needs to justify the next interest rate hike in September. That’s why I’m 90% cash. The market is set up here not to take disappointments on top of a 4,000-point rally in two months. It’s very sensitive to disappointment, so it’s a good time to be in cash.

Q: What stocks go down the most if we get a 5-10% correction?

A: Semiconductors. Nvidia (NVDA), Advanced Micro Devices (AMD), Micron Technology (MU) are your high beta stocks. Having said that, those are the ones you want to buy at market bottoms. I’ve caught many doubles on Nvidia over the years just using that strategy. When you’ve had a horrible market, you want to go for the highest beta stocks out there, and those are the semis. Plus, semis have a long-term undercurrent of always making more money, always improving their products, always increasing market shares. So, you want to invest with tailwinds behind you all the time. 30 years ago, a new car needed ten chips. Now they need 100. That accelerates exponentially as the entire auto industry goes EV.

Q: What’s your opinion on Lithium companies?

A: You know, I haven’t really done much in this area because it is a basic commodity. The profit margins are minimal, there is no Lithium shortage in the world like there is an oil shortage. Plus, no one has a secret method of mining Lithium that is more profitable than another. No one has an advantage.

Q: Is there a logical maximum number of stocks to have in a share portfolio?

A: I keep mine at ten. You should be able to cover every good sector in the market with ten. When I talk to new concierge customers and review their portfolios, one of the most common mistakes is they own too many stocks – there can be 50, 100, 200 stocks, even several gold stocks. And you never want to own more than you can follow on a daily basis. It’s better to follow ten stocks very closely than 100 stocks just occasionally.

Q: How low do you think Apple (APPL) will go on this dip?

A: Minimum 10%, maybe 20%. Just depends on how weak the market will go in this correction.

Q: What was your defensive plan when you sold short Tesla puts?

A: If they got exercised against me and the Tesla shares were sold to me at my strike price, I was going to take the stock, then let the stock rally. If my long-term view for Tesla is $10,000, it’s not such a problem having a $500 put exercise against you—you just take the stock and run the stock. That was always the strategy. Never sell short more puts than you can take delivery of in the stock. Your broker won’t let you do it anyway to protect themselves.

Q: Do you think we could get a strong rally on the next CPI report?

A: Yes. The report is due out on September 13. But some of a sharp drop in the CPI in the next report is already in the market, so don’t expect another 2,000-point stock market rally like we got last time. It’ll be a much lesser move and after that, we’ll need to see more data. We may get 1,000 points out of it, probably not much more. After that, the November midterm election becomes the dominant factor in the market.

Q: When is natural gas (UNG) going to roll over?

A: When the Ukraine War ends, and that day is getting closer and closer. I think it’ll be sometime in 2023. And if you get an end to the war (and the resumption of Russian supplies is not necessarily a sure thing) you’d get a move in natgas from $9 down to $2. So, that’s why I’m very cautiously avoiding energy plays right now. The big money has been made; next to happen is that the big money gets lost.

Q: What are your thoughts on Florida’s pension fund now banning ESG stocks? I live on Florida state pension fund payments.

A: You might start checking out other income opportunities, like becoming an Uber (UBER) driver or working at MacDonalds (MCD). What the Florida governor has done is ban the pension fund from the sector that is most likely to go up over the next ten years and restricted them to the sector (oil) which is most likely to go down. That is very bad for Florida’s pension fund and any other pension funds that follow them. And I’ve seen this happen before, where a pension fund gets politicized, and it’s 100% of the time a disaster. Governors aren't great market timers; politicians are terrible at making market calls. There are too many examples to name. ESG stocks were one of the top performing sectors of the market for 5 years until we got the pandemic crash. So, that is an awful idea (and one of the many reasons I don’t live in Florida besides hurricanes, humidity, alligators, and the Bermuda Triangle).

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, or BITCOIN LETTER, whichever applies to you, then select WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 12, 2022

Fiat Lux

Featured Trade:

(AUGUST 10 BIWEEKLY STRATEGY WEBINAR Q&A),

(NVDA), (TSLA), (GOOGL), (ROM), (FCX), (AMZN), (AAPL), (MSFT), (MU), (ARKK), (TSLA), (F), (GM)

Below please find subscribers’ Q&A for the August 10 Mad HedgeFund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What are your yearend targets for Nvidia (NVDA), Tesla (TSLA), and Google (GOOGL)?

A: Higher for all but I can’t give you the exact date and time. Google has a special situation in that they might be hit with an anti-trust suit in September, so that could cap things. For Tesla, we have the Twitter overhang, and Elon Musk sold $6.9 billion worth of stock last week to fund that. And then Nvidia could have another dive, depending on how much of a glut in chips there is, but I'd be buying any chips from here on. By the way, if Tesla breaks the old high of $1,200, which I expect by the end of the year, we could get to $2,000 very rapidly on yet another massive short squeeze against the permanent Tesla haters, who’ve already been completely decimated by the last 60% move.

Q: How would I play Amazon (AMZN) going forward?

A: Buy the dips. I think they’re going to be the world's dominant retailer going forward and they’re doing the right things and going crazy.

Q: Which sectors?

A: Well, for ETFs, you can look at the ProShares Ultra Technology ETF (ROM). That’s 2x leveraged long tech. But only do that on dips because the volatility of the ROM is enormous since it’s 2x in the most volatile sector. Also, I think we can start taking a look at banks again, what with interest rates rising and a recovery on the horizon, banks could come back into play after sitting at the bottom for the last 3 or 4 months.

Q: I’m doing a LEAP on Freeport-McMoRan Inc. (FCX); should I go for January 2025 or 2024?

A: I’d go longer dated—that way you can get a bigger move and will almost certainly be on a full-on economic recovery, and massive electrification of the auto fleet by 2025, thanks to the climate bill that will be passed Friday. That means the demand for copper is about to go absolutely through the roof—I'm looking for (FCX) to go from $30 to $100 in the next 3 years.

Q: Thoughts on Disney (DIS)?

A: No one can believe how cheap Disney has gotten, it’s been a disaster. Obviously (DIS) took it on the nose with the recession and some of the parks still have limitations on the number of visitors. It should do better and I'm amazed it got this cheap. I would expect a move to the $200 level by the end of next year.

Q: What LEAPS do you recommend for January 2023?

A: Well it’s not really a LEAPS if you’re only going out 6 months; that’s just a long-dated call spread. LEAPS are usually a year or longer. I’d say pretty much anything in any sector will be higher except maybe energy by 2023. We’re not at LEAPS territory yet, but we’re getting close. The next major selloff I might start putting LEAPS out there.

Q: Is the Consumer Price Index (CPI) dropping from 9.1% YOY down to 8.5% meaning the top is in and deflation’s over?

A: I think so, because there are a lot of price declines that were not reflected in this July number that have yet to come. I'm talking about wheat, lumber, and energy. So yes, we could get another big move down in August, and if that’s the case, the Fed may only raise by 50 basis points in September. That's the hope. The things that aren’t going to go down are rental costs and labor costs. We may never get back to the inflation rate that we had 2 years ago of 2%. The long-term average for the last 100 years is 3% and certainly a move down to 4% is possible this year (and would be very welcome by the stock market as part of my long-term bull case).

Q: What are your thoughts on Elon Musk selling $6.9 billion worth of Tesla shares?

A: It’s amazing he sold that amount of stock last week and only went down $100. It does remove a big overhang on the stock and paves the way on a much bigger move up later in the year. By selling the $9 in January and $7 now, that’s $16 billion he sold this year. He could almost pay for Twitter with a little outside bank financing.

Q: How far above current prices should I place a LEAPS?

A: It depends on where the market is; if we’re having a cataclysmic selloff down 1,000-point days, then you can have the luxury of going 10%, 20%, or even 30% out-of-the-money; and that of course gets you a 100%, 200% and 300% returns. If we have a higher low, then you may want to go lower risk and go at the money, that might get you a 50% return. On LEAPS that are only slightly in-the-money, even those generate 25% returns one year out with the most conservative possible position.

Q: Would you load the boat on dips?

A: I would but remember: a dip is not one hour or on down days, it’s like half of the recent gain, which would be down 1,500 Dow points, or all of the recent gain, which would be down 3,000 points. So be careful that you don’t get too aggressive just because you’ve gotten bullish.

Q: Do you think the semiconductor chips will lead the tech recovery in the second half of the year?

A: I do, but we do have an inventory problem to digest first, and we have to figure out the implications of the CHIPS act that was signed this week which makes available a couple hundred billion dollars to build new chip factories in the US. Chip companies are particularly challenged right now because they have to provision for a recession which is going to cut chip demand, and they also have to provision for a potential oversupply created by the CHIPS Act. Remember that for the industry, creating safe supplies of chips means more lots of chips at lower prices for consumers. Great for us, great for the auto industry, not so great for chip companies. You have to be careful. On the other hand, on the bullish side, chips are being designed into more products faster and in larger numbers than ever before. This is the main reason why most investors underestimated the chip industry for the last 10 years. That also is a factor that’s accelerating. The average car now has 100 chips. 20 years ago they had maybe 10 chips, and 30 years ago they had none.

Q: Will the eventual big win of Ukraine against Russia result in inflation going back to 2%?

A: No, but it will result in it going back to 3% or 4%, which we could hit next year. You get oil back down below $50, gasoline down to $2/gallon, and the world's food supply opened up once again, and inflation will disappear in a heartbeat.

Q: What’s the deal with the 1% buyback tax in the inflation reduction package?

A: Well they had to get revenue somewhere, and 1% is so small it won’t inhibit anyone from buying back stock, especially if it makes the CEO a billionaire. That is a great incentive—even if you had a 50% tax, they would still be doing buybacks for things like Apple (AAPL), Microsoft (MSFT), and the other buyback players.

Q: What will high energy prices do to crypto?

A: It might actually make it go up because the cost of electricity feeds straight into the manufacturing/programming cost of crypto. And if you notice, Bitcoin bottomed at $17,000 per bitcoin. But that's exactly where the new mining cost is. Just like all of the commodities, when you hit cost of production, the supply suddenly dries up because nobody can make any money at it.

Q: Will US homebuyers buy the dip since mortgage rates have come down?

A: Yes, and we’re already seeing that in the statistics. The fact is we still have a huge housing shortage in the United States. You don’t get big price falls when you have a shortage of supply, and you have 10 million millennials who still need to trade up from their one and two-bedroom apartments all over the country. So, things may stall a bit in home buying, but I don’t think you get very big price drops.

Q: Do you think the US consumer is strong?

A: They never stopped being strong, even throughout recession fears. Never, ever bet against the propensity of Americans to spend money, both individuals and governments.

Q: What are the chances the US goes to war with China over Taiwan?

A: Zero. # 1 China doesn't have ships, #2 we have the 7th Fleet there, and #3 they have been threatening to invade Taiwan for 70 years and done nothing. The Taiwanese are used to this. Though there is the other side issue that most of the other private companies in Taiwan are already owned by the Chinese and have Chinese capital, so it’s unlikely they want to blow up their own facilities. So, the answer is no.

Q: What is the Long term outlook for gold and silver?

A: It’s been dead for so long that I’m not inclined to rush into gold. But you have to expect that when you get a recovery in the commodity boom, it’s going drag gold and silver along with it. I see upsides for both of these, especially silver.

Q: Should student loans be paid off by the federal government?

A: I think yes, because as long as these people have massive debts, they cannot borrow and they cannot enter the US economy as consumers. If you forgive all student debt, you unleash 10 million new customers onto the market who can now borrow, get credit cards, and take out home mortgages. As long as they have massive debts, they can’t do that.

Q: With all the major companies in the world moving to EVs, where are we going to get these commodities?

A: We’re not. Tesla (TSLA) has already locked up major supplies of commodities over the next 10 years, and everyone else will have to pay more money. Some of the weaker producers like Ford (F) and General Motors (GM), are being restrained on shortages of not just chips but also basic commodities like chromium for stainless steel. They’re going to have a real problem competing with Tesla, which is why you own Tesla.

Q: What do you think about the unprofitable tech companies like those in the ARK ETFs (ARKK)?

A: I would avoid those for now. Why take on additional risk buying a non-earning company when the highest quality companies are selling at the cheapest valuations in ten years? Maybe when the big companies like Apple get overvalued—go up another 100% — then you might look at the smaller companies if they’re still cheap. But the risk/reward on the nonearners right now is no good, while it’s fantastic in the large tech companies. That is my opinion and I’m sticking to it.

Q: It seems Russia’s strategy has mirrored those of the Czars.

A: Actually, what they’re doing is repeating their WWII strategy, which worked in 1945— not so much in 2022; and that was massive artillery barrages against retreating Germans. Except this time Ukrainians are not retreating and have far more modern weapons than the Russians.

Q: Would you buy Micron Technology (MU) on bigger dips?

A: Absolutely yes; but again, wait for the down days. You have plenty of volatility in chip stocks, no need to pay up or chase higher prices.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

July 8, 2022

Fiat Lux

Featured Trade:

(THE END OF SAMSUNG)

(SAMSUNG), (QCOM), (MU), (AAPL)

Samsung, Korea’s stalwart chaebol, is toast.

Remember the past two years when lockdowns were in vogue?

Digital products were the hottest item in the world as everybody was stuck in their homes.

Growth brought forward is never a bad thing for a company, especially tech companies.

However, it sets the stage for hard comps to topple and a reversion back to the mean which can look messy.

The world needed chips and phones back then, the world is now traveling, getting on planes, and taking cruise ships to the Caribbean.

This is why video game growth is quite subdued this year.

Samsung internally has also been taking a machete to its forward-looking estimates multiple times in order to front-run collapsing demand.

The boom bust nature of chips and devices is an inherent beast in the industry that is hard to tame.

Samsung was able to hit watered-down targets in the second quarter, but that was mainly due to a 7% currency tailwind of the Korean won sliding fast just like many Asian currencies.

Take a look at the Japanese yen, it’s gone off a cliff all the way to 136 per $1.

I remember when I took a vacation to Tokyo in 2011, Japan felt awfully expensive at 77 yen to $1.

The currency tailwinds are a transitory elixir yet under the hood, these economies are weakening fast.

The aging population and cost of living crisis are also crushing sales.

Internal data reveals deeper damage than initially thought.

Operating profit missed by a wider margin than revenue beat and prices for its premium products isn’t fetching the prices they once did.

For example, Samsung markets its Exynos 2200 chips as on-par rivals to the Snapdragon 8 Gen 1 and Apple’s (AAPL) A15 Bionic chip found in smartphones.

However, the Exynos fails to compete with its supposed flagship chip comps, performing at levels lagging almost a generation behind in speed and functionality.

It’s clear that devices made with Exynos chips simply won’t be able to sell for as much as flagship Android phones with Snapdragon 8 Gen 1 or Apple iPhones with A15 Bionic chips.

I fully expect the operation profit to go from 6% to 3% for Samsung.

US rival Micron (MU) has already rung the alarm. While the world’s third-largest maker of DRAM posted revenue and operating profit for the quarter in line with estimates, its forecast for the coming three months was 20% lower than expectations.

It now sees the PC and smartphone markets much weaker than previously thought.

Tech has experienced a massive downgrade in terms of sentiment and sales while massive pressure on the supply side costs.

Cloud computing and streaming services which all need chips have been the poster boys of underperformance.

Growth stocks have also gotten killed.

I do believe this is more a signal of deeper individual malaise at Samsung and an indication they are getting trounced by Chinese firms who just do it better for cheaper.

Margins won’t ever come back up for Samsung as they lack the nimbleness of the Chinese and brute power of the American tech.

They are essentially stuck between a rock and a hard place where products will become less competitive, face rapidly shrinking margins, and participate in a Korean economy that lacks vibrancy.

Once chip stocks bottom, avoid Samsung, and get into Qualcomm (QCOM) and Micron (MU).