Remember the past two years when lockdowns were in vogue?

Digital products were the hottest item in the world as everybody was stuck in their homes.

Growth brought forward is never a bad thing for a company, especially tech companies.

However, it sets the stage for hard comps to topple and a reversion back to the mean which can look messy.

The world needed chips and phones back then, the world is now traveling, getting on planes, and taking cruise ships to the Caribbean.

This is why video game growth is quite subdued this year.

Samsung internally has also been taking a machete to its forward-looking estimates multiple times in order to front-run collapsing demand.

The boom bust nature of chips and devices is an inherent beast in the industry that is hard to tame.

Samsung was able to hit watered-down targets in the second quarter, but that was mainly due to a 7% currency tailwind of the Korean won sliding fast just like many Asian currencies.

Take a look at the Japanese yen, it’s gone off a cliff all the way to 136 per $1.

I remember when I took a vacation to Tokyo in 2011, Japan felt awfully expensive at 77 yen to $1.

The currency tailwinds are a transitory elixir yet under the hood, these economies are weakening fast.

The aging population and cost of living crisis are also crushing sales.

Internal data reveals deeper damage than initially thought.

Operating profit missed by a wider margin than revenue beat and prices for its premium products isn’t fetching the prices they once did.

For example, Samsung markets its Exynos 2200 chips as on-par rivals to the Snapdragon 8 Gen 1 and Apple’s (AAPL) A15 Bionic chip found in smartphones.

However, the Exynos fails to compete with its supposed flagship chip comps, performing at levels lagging almost a generation behind in speed and functionality.

It’s clear that devices made with Exynos chips simply won’t be able to sell for as much as flagship Android phones with Snapdragon 8 Gen 1 or Apple iPhones with A15 Bionic chips.

I fully expect the operation profit to go from 6% to 3% for Samsung.

US rival Micron (MU) has already rung the alarm. While the world’s third-largest maker of DRAM posted revenue and operating profit for the quarter in line with estimates, its forecast for the coming three months was 20% lower than expectations.

It now sees the PC and smartphone markets much weaker than previously thought.

Tech has experienced a massive downgrade in terms of sentiment and sales while massive pressure on the supply side costs.

Cloud computing and streaming services which all need chips have been the poster boys of underperformance.

Growth stocks have also gotten killed.

I do believe this is more a signal of deeper individual malaise at Samsung and an indication they are getting trounced by Chinese firms who just do it better for cheaper.

Margins won’t ever come back up for Samsung as they lack the nimbleness of the Chinese and brute power of the American tech.

They are essentially stuck between a rock and a hard place where products will become less competitive, face rapidly shrinking margins, and participate in a Korean economy that lacks vibrancy.

Once chip stocks bottom, avoid Samsung, and get into Qualcomm (QCOM) and Micron (MU).

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-07-08 15:02:262022-07-12 20:41:43The End of Samsung

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

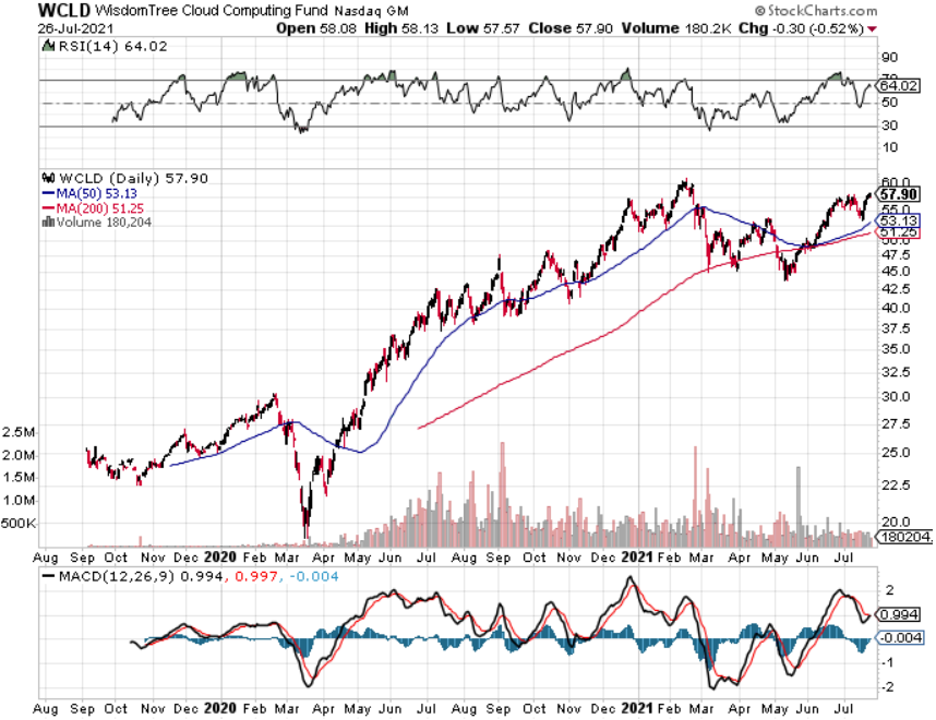

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

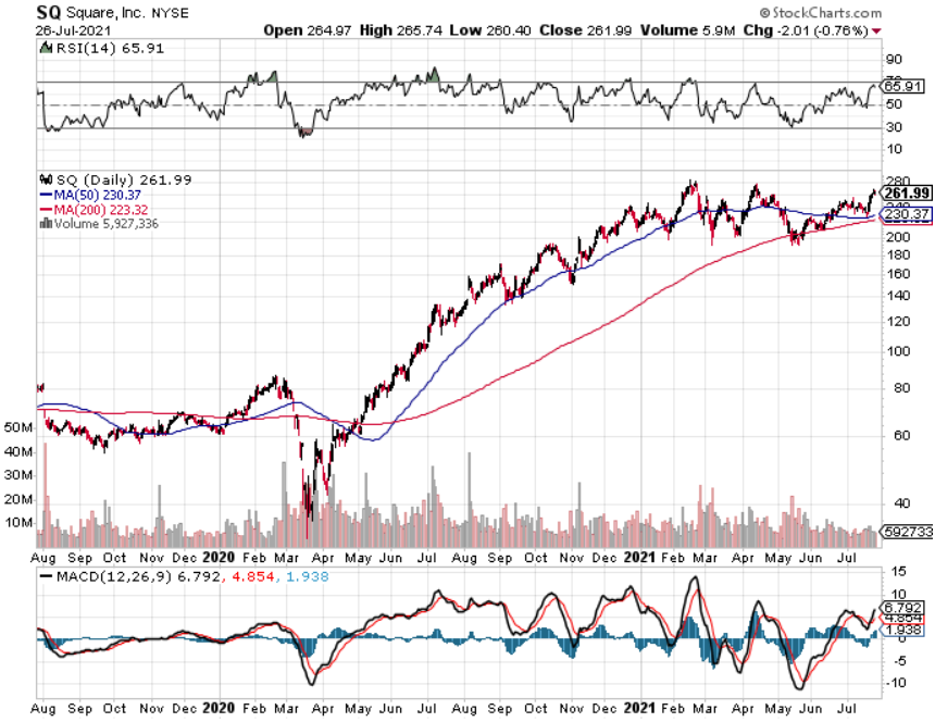

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, instead of scouring the grains of sand to find a diamond, I have a quick fix for you and your friends.

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate ten-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-25 15:02:202021-08-27 17:47:18The Best Way to Alpha Your Tech Portfolio

Signs are creeping in of a cyclical downturn in memory chips starting in the first quarter of 2022.

This is all brought about by cycle indicators signaling that we are shifting out of 'midcycle' to 'late-cycle' for the first time since 2019 and this phase change has historically meant a challenging backdrop for forward returns.

The investments have been pouring in from chip companies to build more foundries and to improve chip performance.

Incrementally, new supply will eventually come online to address the giant chip shortage that many industries are grappling with.

However, I will say that whispers of an imminent collapse in the chip dynamics are exaggerated at best.

I don’t believe that the next cyclical downturn begins from Q1 2022 exacerbated by inventory builds.

We are still far from that happening even if the chip environment has tensed up more so now.

Micron (MU) has said that the order-filling time for chipmakers now exceeds 20 weeks.

The order-filling time represents the period from ordering a semiconductor to receiving it. That metric added on more than eight days in July, putting the total at 20.2 weeks.

Businesses from automakers to consumer-electronics companies are suffering from the chip shortage. Carmakers are expected to miss out on $100 billion in sales due to the lack of critical components.

Another industry-wide headwind is the UK's possible blocking of Nvidia’s (NVDA) planned $40 billion acquisition of Arm Holdings over national security issues.

A possible downturn in the chip cycle would also mean heavyweight South Korean memory-chip maker SK Hynix will severely underperform as well.

There are forecasts of contract prices for memory chips used in personal computers that decline by as much as 5% in the December quarter from the September quarter.

The PC market is only 20% of the DRAM market. Smartphone DRAM accounts for 40% of the market and server DRAM is 30% of the market. Miscellaneous device markets make up the remaining 10%.

Therefore, it is safe to say that not all the eggs are in one basket.

However, an analyst downgrade has set the tone for all makers of dynamic random access memory chips and puts the onus on the entrenched to prove the supposed downturn is not the case.

A world in which all relevant companies have hoarded chips because of the fear of not be able to source the right chips would be a transitory issue.

I don’t see demand falling off a cliff.

Many of these DRAM companies have moats around their business models and the case of businesses snapping up a high volume of chips and their inventories peaking out is a problem many companies would love to have.

As we progress into 2022, companies will start to plan their next iterations of devices and gadgets, and no doubt the next generation will need at least 50% more high-performing chips compared to the last version.

The pricing pressure is almost analogous to what happened with lumber prices and builders started buying at whatever prices during the short squeeze earlier this year.

This doesn’t mean the housing industry is doomed, but I understand it more as moderating prices will be a tailwind for the overall health of the industry.

Chips are famous for that boom and bust dynamic.

The price gains in chips cannot be absorbed in the same rate and as prices moderate, companies will start to look at acquiring the next batch of chips even if inventory is high.

In the short term, chip stocks are on course for a short correction that could take around a quarter to digest, but I highly doubt this will last into next year.

The 30,000-foot view shows us that many chip firms are enjoying record demand for their best chips driven by cloud customers’ capital expenditures, and even upside from the popularity of cryptocurrency-related chip products.

Demand is everywhere to be found.

The leading-edge manufacturers will take this dip in stride and adjust for the new environment in 2022.

Lower pricing expectations is something that nobody wants to hear as a chip CEO and absorbing a more challenging pricing environment into 4Q does not beat price spikes.

It gets lost that DRAM prices increased 35% over the past two quarters, with expectations for a “further modest increase” through the end of this year.

The industry can afford a little reversion to the mean pricing and shareholders will mostly stay in these stocks long term.

I understand that this dip in chip shares like Micron caused by moderation of pricing power translates into a great entry point into the stock for new buyers.

Quite quickly will investors start to shrug off this negative element to the industry and pile back into premium names or just stick with Nvidia who doesn’t sell DRAM chips.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-13 15:02:092021-08-22 01:24:09Are the Wheels Falling Off the Chip Industry?

A better headline for this piece would be “The Future of You,” as artificial intelligence is about to become so integral to your work, your investment portfolio, and even your very existence that you won’t be able to live without it, quite literally.

Well, do I have some great news for you. A blockbuster book about the state of play on all things AI will be released on September 25, and I managed to obtain and read an advanced copy. It is entitled: AI Superpowers: China, Silicon Valley, and the New World Order by Dr. Kai-Fu Lee.

The bottom line: The future is even more unbelievable than you remotely imagined. We are at the very early days of this giant megatrend, and the investment opportunities will be nothing less than spectacular.

And here is a barn burner. The price of AI is dropping fast as hundreds of thousands of new programmers pour into the field. Those $10 million signing bonuses are about to become a thing of the past.

Dr. Lee is certainly someone to take seriously. He obtained one of the first Ph.D.’s in AI from Carnegie Mellon University. He was the president of Google (GOOG) China and put in stints at Microsoft (MSFT) and Apple (AAPL). Today, he is the CEO of Sinovation Ventures, the largest AI venture capital firm in China, and is a board director of Alibaba (BABA).

AI is nothing more than deep learning, or super pattern recognition. Dr. Lee dates the onset of artificial intelligence to 1952, when an IBM mainframe computer learned to play checkers and beat human opponents. By 1955, it learned to develop strategies on its own.

Dr. Lee sees the AI field ultimately divided into two spheres of dominance, the U.S. and China. No one else is devoting a fraction of the resources needed to become a serious player. The good news is that Russia and Iran are nowhere in the game.

While the U.S. dominates in the original theory and algorithms that founded AI, China is about to take the lead in applications. It can do this because it has access to mountains of data that dwarf those available in America. China processes three times more mobile phones, five times more Internet customers, 10 times more eat-out orders, and 50 times more mobile transactions. In a future where data is currency, this is huge.

The wake-up call for China in applications took place two years ago when U.S. and Korean AI programs beat grandmasters in the traditional Chinese game of Go. Long a goal of AI programmers, this great leap forward took place 20 years earlier than had been anticipated. This created an AI stampede in the Middle Kingdom that led to the current bubble.

The result has been applications that are still in the realm of science fiction in the U.S. The Chinese equivalent of eBay (EBAY), Taobao, doesn’t charge fees because its customer base is so big it can remain profitable on ad revenues only. Want to be more beautiful in your selfies sent to friends? A Chinese app will do that for you, Beauty Plus.

The Chinese equivalent of Yelp, Dianping, has 600,000 deliverymen on mopeds. The number of takeout meals is so vast that it has been able to drop delivery costs from $6 a meal to 60 cents. As a result, traditional restaurants are dying out in China.

Teachers in Chinese schools no longer take attendance. Students are checked off when they enter the classroom by facial recognition software. And heaven help you if you jaywalk in a Chinese city. Similar software will automatically issue you a citation with a fine and send it to your home.

Credit card fraud is actually on the decline in China as dubious transactions are blocked by facial matching software. The bank simply calls you, asks you to look into your phone, takes your picture, and then matches it with the image they have on file.

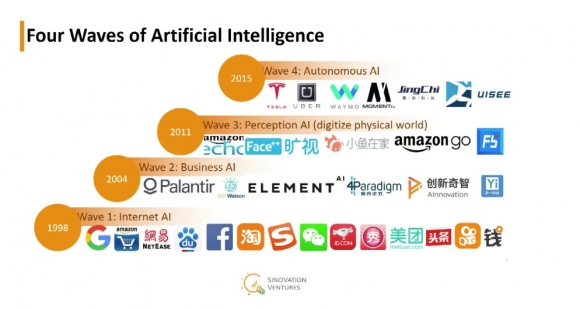

Dr. Lee sees AI unfolding in four waves, and there are currently companies operating in every one of these (see graph below):

1) Internet AI

The creation of black boxes and specialized algorithms opened the door to monetizing code. This was the path for today’s giants that dominate online commerce today, Google (GOOG), Amazon (AMZN), JD.com (JD), and Facebook (FB). Alibaba (BABA), Baidu (BIDU), and Tencent followed.

2) Business AI

Think big data. This is the era we just entered, where massive data from online customers, financial transactions, and health care led to the writing of new algorithms that maximize profitability. Suddenly, companies can turn magic knobs to achieve desired goals, such as stepping up penetration or monetization.

3) Perception AI

Using trillions of sensors worldwide, analog data on any movement, facial expression, sound, and image are converted into digital data, and then mined for conclusions by more advanced algorithms. Cameras are suddenly everywhere. Amazon’s Alexa is the first step in this process, where your conversations are recorded and then mined for keywords about your every want and desire.

Think of autonomous fast food where you walk in your local joint and it immediately recognizes you, offers you your preferred dishes, and then auto bills your online account for your purchase. Amazon has already done this with a Whole Foods store in Seattle.

4) Autonomous AI

Think every kind of motion. AI will get applied to autonomous driving, local shuttles, factory forklifts, assembly lines, and inspections of every kind. Again, data and processing demand take an enormous leap upward. Tesla (TSLA), Waymo (GOOG), and Uber are already very active in this field.

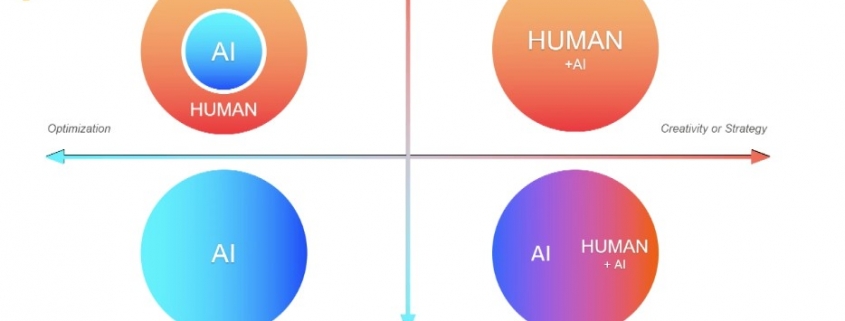

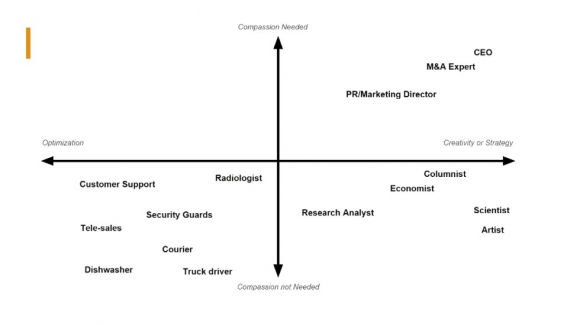

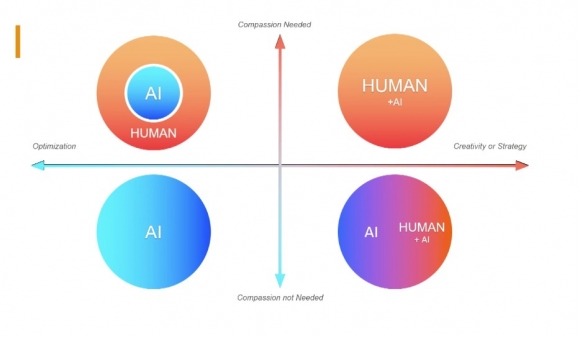

The book focuses a lot on the future of work. Dr. Lee creates a four-part scatter chart predicting the viability of several types of skills based on optimization, compassion, creativity, and strategy (see below).

If you are a truck driver, in customer support, or a dishwasher, or engage in any other repetitive and redundant profession your outlook is grim. If you can supplement AI, such as a CEO, economist, or marketing head you’ll do fine. People who can do what AI can’t, such as teachers and artists, will prosper.

The Investment Angle

There have been only two ways to invest in AI until now. You can buy shares in any of the seven giants above, whose shares have already risen for 100- or 1,000-fold.

You can invest in the nets and bolts parts providers, such as NVIDIA (NVDA), Advanced Micro Devices (AMD), Micron Technology (MU), and Lam Research (LRCX), which provide the basic building blocks for the Internet infrastructure.

Fortunately for our paid subscribers, the Mad Hedge Trade Alert Service caught all of these very early.

What’s missing is the “in-between companies,” which are out of your reach because they are locked up in university labs or venture capital funds. Many of these never see the light of day as public companies because they get taken over by the tech giants above. It’s effectively a closed club that won’t let outsiders in. It’s a dilemma that vexes any serious technology investor.

When quantum computing arrives in a decade, you can take all the functionality above and multiply it by a trillion-fold, while costs drop a similar amount. That’s when things really get interesting. But then, I’ve seen trillion-fold increases in technology before.

I hope I live to see another.

Personally, I Prefer the Original

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Human-and-AI-chart-image-3-e1536698568163.jpg337580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2021-08-05 09:02:522021-08-05 15:59:33The New AI Book that Investors are Scrambling For

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance, and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many techportfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a techportfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-30 15:02:502021-08-03 01:47:18The Best Way to Streamline Your Portfolio

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-30 13:04:292021-07-30 14:07:50July 30, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.