American oil imports from the Middle East are in free fall, down 35% in two years. They are quickly being replaced by tar sands imports from Canada, which are ballooning to 2 million barrels a day and at all time highs. American energy production is surging, thanks to new finds of natural gas showing up in everyone?s back yard, taking the country rapidly on its way to energy independence.

So why is the price of oil so damn high?

Everywhere you go to seek a shortage, you find a glut. Storage facilities at the Cushing, Oklahoma hub are practically overflowing. The Strategic Petroleum Reserve is close to its 727 million barrel maximum capacity, or 36 days of national consumption.

Traditionally, the beginning of the summer driving season heralded higher crude prices. But gasoline consumption has been sliding for five years, thanks to the widespread adoption of hybrids and electric cars, and the improved mileage of conventional automobiles.

Even the Iranian election results auger poorly for the price of oil. The win by moderate Hassan Rohani, who boasts a doctorate from a Scottish university, promises to ease tensions with the United States over the nuclear issue.

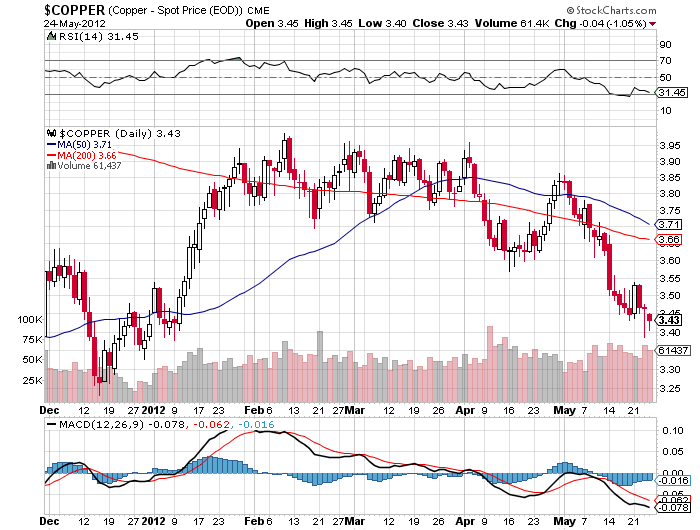

More mysterious is the fact that the price of oil has been levitating in the face of the utter collapse of virtually every other commodity. Dr. Copper is handing out ?F?s? these days, the red metal down 30% this year. Iron ore is close to 50% down from its peak, to the deep distress of many Australians and their beleaguered dollar. Even the barbarous relic is off, gold falling 31% from its high. How come the Chinese economic slowdown is dragging down the price of everything except the one it needs the most?

The US decision to send weapons to Syria is, no doubt, positive for oil prices, but it is only worth a bump for a day. America has also announced joint military maneuvers with Jordan. How much do you want to bet that they accidentally leave their weapons behind?

Iran responded by sending 4,000 troops into the battered country to join Hezbollah from Lebanon, who are already there. Syria is turning into the Spanish Civil War of our age. But as it produces no oil, it shouldn?t materially impact prices.

Looking at speculative long positions held by hedge funds, I find them at multiyear highs. My guess is that investment demand, not consumption, accounts for up to $30 of the current $98 price of black gold.

Maybe we should just write all this off to another instance of prices moving the opposite direction of fundamentals, which has become so common this year. Or perhaps President Obama is right? Is it the work of evil speculators?

How To Get a Price Rise From a Global Glut?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/06/World-in-Oil.jpg450449Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-06-18 09:33:292013-06-18 09:33:29The High Oil Mystery

Four years ago, the dreams of a nuclear renaissance seemed close to coming to fruition. President Obama supported it. Congress passed a raft of new subsidies, tax breaks, liability caps, and cost overrun indemnifications, to grease the works. The goal was to bring the private sector back in a non-oil, non-carbon energy source which had seen no new construction in 34 years.

For a while, things were looking good. The Nuclear Regulatory Commission was flooded by 24 new applications for plants to join America?s 104 existing ones, from utilities largely in the southeast. Then a development far more devastating than the most egregious environmentalist lawsuit stopped the movement dead in its tracks. The price of natural gas crashed (UNG).

In 2008, CH4 peaked at $14/MM btu in 2008 in the wake of the last big oil spike to $149. It then utterly collapsed to $1.90, a vaporization of 86%. It was like someone snuffed your pilot light, turned all you gas burners on, and let your house blow up. Much of the industry was decimated, and gas investors got wiped out in droves. It also became one of my favorite short plays. Although gas has since recovered to $4/MM btu, it has completely demolished the economics of new nuclear.

At current prices, analysts now peg operating costs for new gas fired power plants at four cents a kilowatt-hour, compared to ten cents for nuclear. And this turns a blind eye to other problems endemic to nuclear, like expensive waste disposal, environmental litigation, lender nervousness, consumer backlash, humongous capital costs, and a long history of spectacular cost overruns.

It?s not like gas is going away anytime soon. Over the last five years, a new 100-year supply has been discovered in the US. Another 100 years is there, but exploration companies basically quit looking. What?s the point, when you are already drowning in the stuff. It turns out that about half of the land area of the United States is sitting on an exploitable natural gas field.

The finds assure US energy independence within 3-5 years, and will change the economy beyond all recognition. The risk is that gas gets cheaper, yet again, rather than ease nuclear?s competitive predicament. Just to bring nuclear back to even, gas has to roar back to $10/btu

The utilities have read the writing on the wall and are scrambling to lose their plans behind the radiator, post haste. Duke Energy (DUK), the poster child for new nuclear, has said it is calling off plans to build six new behemoths. Dominion Resources (DRU), in Wisconsin, is closing a nuclear plant which still has 20 years remaining on its license because it is simply too expensive to run. NRG Energy (NRG) dumped plans to build two Texas plants after blowing $331 million on preliminary planning and applications.

The new malaise in nuclear has placed a giant black cloud over the sector?s beleaguered ETF?s, including Market Vector Uranium + Nuclear Energy ETF (NLR) and Cameco (CCJ). Not only did these securities get the stuffing knocked out of them in the wake of Japan?s Fukushima tsunami and nuclear disaster, they have also suffered from this year?s general antipathy towards commodities.

I always had my misgivings about the return of big nuclear, the constructions of plants based on 50-year-old designs. There are too many other intelligent ways to do this from an engineering point of view. On the short list are alternative, cooler, non-weaponizeable fuels, like thorium. Small, modular, and even portable designs that mitigate and distribute risk is another idea. We may have to wait a while until better, more competitive nuclear strategies hit the market.

In the meantime, there are too many better fish to fry. Shop elsewhere.

What?s the Market for a Half Built Nuclear Plant?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/06/NATGAS-6-6-13.jpg449573Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-06-07 09:19:202013-06-07 09:19:20New Nuclear Demolished By New Natural Gas

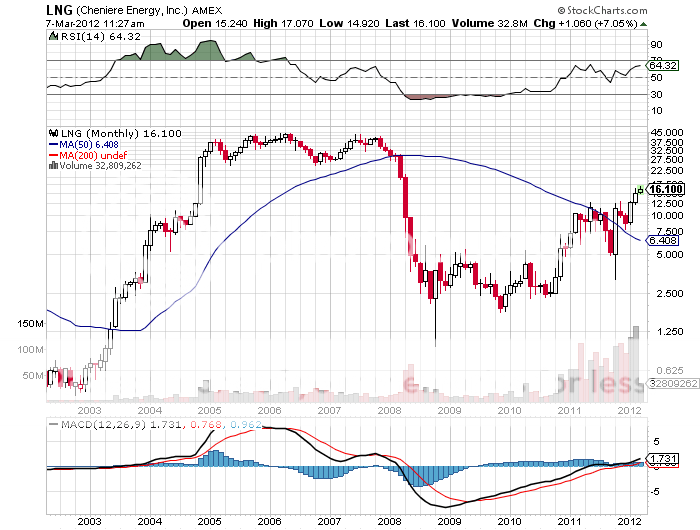

Occasionally, I so totally knock the ball out of the park that I qualify for a place in the stock picker?s Hall of Fame. That was the case when I put out a recommendation to buy LNG exporter, Cheniere Energy (LNG), a year ago (click here? for Take a Look at Cheniere Energy (LNG).

Since then, the stock has soared an eye popping 85%. The great thing here is that I think the stock is still a buy. An upside target of $30 is a chip shot, and the all time high at $45 is within range. So get a 10%-20% dip in the price, and you might shovel some into your long-term portfolio. I quote below the entire original piece:

?I am constantly asked if there are any ways investors can take advantage of the collapse of the natural gas market, where at $2.34/MMBTU prices are plumbing decade lows. I have recently made good money buying puts on the ETF (UNG), but these are not for the faint of heart. They call this contract the ?widow maker? for a good reason.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices are probably going to stay down for years. Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

However, there is one company that delivers a narrow rifle shot that could do extremely well in coming years, and that is Cheniere Energy (LNG). I first started following (LNG) a decade ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a loft $5/MBTU, Qatar invested $50 billion in in developing its own substantial gas resources. The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline. It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100-year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MMBTU down to $2/MMBTU. Any plans to import LNG from the other side of the world were rendered utterly worthless. Chenier?s billion-dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed low single digits as the firm flirted with bankruptcy.

Enter China. The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil (USO) to soar from a 2008 low of $30 to $110. Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages. This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been spiking, gas has been crashing. Gas is now selling at 15% of the cost of oil on an adjusted BTU basis. Another way of saying this is that you can buy oil for $16 a barrel instead of $110. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

Enter the long-term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day. Because very expensive and hard to get, offshore supplies were tapped, the price was set at $16/MBTU. Those contacts are now expiring. Do you think they?ll renew at the old price, or go to Cheniere for the $2 stuff? Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown last March prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice. Power companies there have been scrambling to obtain conventional energy supplies, and have been a major factor in driving oil up from $75 to $100 since the fall. Cheap gas supplies from the US would meet this demand nicely.

The trigger. Last May, Cheniere got US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquifaction plant, something that can be done with some expensive re-engineering. It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant. My hedge fund buddies have been accumulating this stock since October, when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better left to long term players.

Then last week, Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $2 billion, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt. The Stock has just run up from $3 to $17. And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren. As a result, local permits for these are very hard to come by.

But as you can see, a whole host of geopolitical, technology and economic strands tie together in this one company, all of which are positive for the share price. If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please click here for their website at http://www.cheniere.com/default.shtml .?

Did Somebody Light a Match?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/Homes-rubble.jpg260385Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-03-21 23:01:552013-03-21 23:01:55Revisiting Cheniere Energy (LNG)

I have been pounding the table on the attractions of Cheniere Energy (LNG) since last spring. Yesterday, the stock hit a new all time high of $21.50.

There is never any guarantee that a government agency will not do something idiotic. Last year it didn?t, thankfully. The Federal Energy Regulatory Commission (FERC) granted the final license needed by Cheniere Energy (LNG) to build the first of two liquefaction plants at Sabine Pass on the Texas Louisiana border on the Gulf of Mexico. These will be the first such plants built in the US in 40 years.

FERC gave to go ahead despite vocal opposition from the Sierra Club, which claimed that fracking caused environmental damage. This, of course, is complete bunk. MIT recently published a study of 50 incidents where gas made it into local water supplies. In every case, it was shown to be the cause of subcontractor incompetence and inexperience, not because of any fundamental flaws with the technology.

The move was a crucial step towards turning the US into a major natural gas (UNG) exporter. The company has already contracted to sell 89% of the plants? planned annual output of 16 million tons. Buyers include BG Group of the UK, Gas Natural Fenosa of Spain, Gail of India, and Kogas of South Korea. Initial deliveries are expected to commence at the end of 2015.

You may recall that I recommended this stock to readers back on March 7 when it was trading at $16.10 a share (click here for ?Take a Look at Cheniere Energy (LNG)? at http://madhedgefundradio.com/take-a-look-at-cheniere-energy-lng/). I think it is just a matter of time before the stock surpasses its next hurdle at $30, especially if natural gas continues to stabilize here around $2/MM BTU.

Now, We?re Cooking With Gas

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Gas-Fire.jpg346452Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-01-31 09:39:182013-01-31 09:39:18Cheniere Energy (LNG) Gets the Green Light

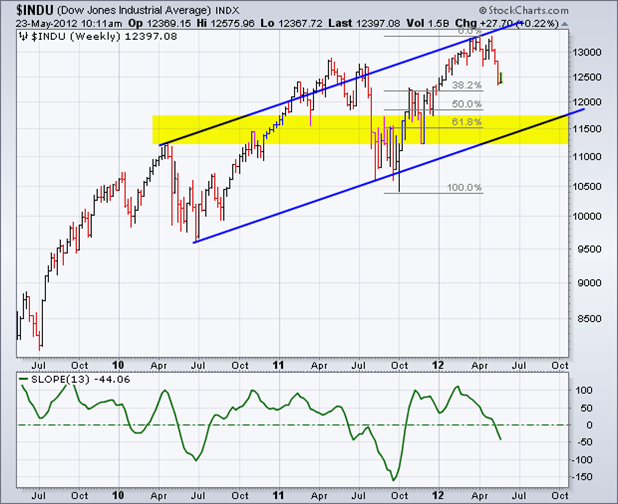

The easy money has been made on the short side this year for a whole range of asset classes. While we will probably see lower lows from here, the risk/reward ratio for taking short positions in (SPX), (IWM), (FXE), (FXY), (GLD), (SLV), (USO), and (CU) are less favorable than they were two months ago.

Of course, the ultimate arbiter will be the news play and the economic data releases. It they continue to worsen as they have done, you can expect a brief rally in the (SPX) up to the 1,340-1,360 range before the downtrend resumes. First, we will revisit the old low for the move at 1,290. Then 1,250 cries out for attention, which would leave us dead unchanged on the year. Lining up next in the sites is 1,200. But to get that low, probably by August, we would need to see something dramatic out of Europe, which we may well get. For the Russell 2000, look to sell it at the old support range of $78-80, which now becomes overhead resistance, to target $72 on the downside.

Don?t underestimate the devastating impact the Facebook (FB) debacle will have on the overall market. Retail investors lost $6 billion on the deal after institutional investors were given the heads up on the impending disaster and stayed away in droves. The media has plenty of blood on its hands on this one. The day before the pricing, one noted Cable TV network reported that the deal was oversubscribed in Asia by 30:1. Morgan Stanley reached for the extra dollars, increasing the size, and boosting the price by 15%. It all came to tears.

Expect investigations, subpoenas, congressional hearings, prosecutions, multi million out of court settlements, thousands of lawsuits, and many careers ended ?to spend more time with families.? Horrible thought of the day: Apply Apple?s (AAPL) 8X multiple, which is growing at 100% a year, to Facebook, which is not, and you get a (FB) share price of $5. None of this exactly inspires confidence in the stock market.

Notice that emerging markets have really been sucking hind teat this year, dragged down by falling commodity prices, a slowing China, and a general ?RISK OFF? mood. This is probably the first sector you want to go back in at the summer bottom to take advantages of their higher upside betas.

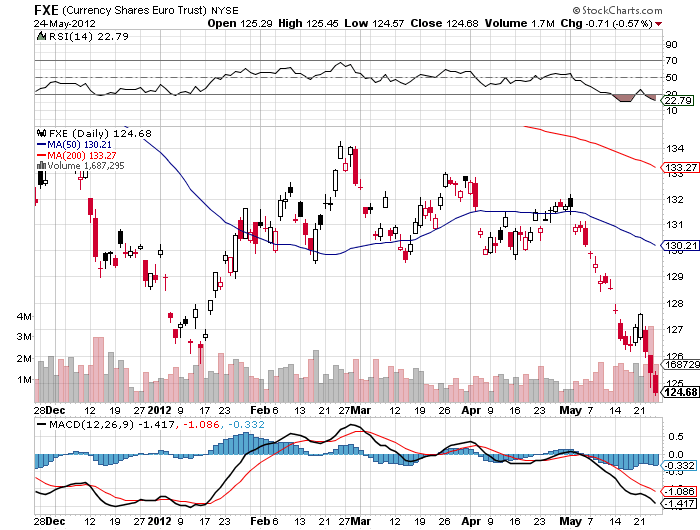

The Euro went through the old 2012 low at $1.260 like a hot knife through butter. On the breach, a lot of momentum programs automatically kicked in and doubled up their short positions. That is what has taken us all the way down to the high $124 handle in the cash. Let?s see how the market digests this breakdown. The commitment of traders report out on Friday should be exciting, as we already have all-time highs in short positions in the beleaguered European currency.

The problem is that any good news whispers or accidental tweets on the sovereign debt crisis could trigger ferocious short covering and gap openings which the continental traders will get a head start on. So again, this is not the low risk trade that it was months ago.

Still, the 2010 lows at $1.18 are now on the menu. I would sell all the ?good news? rallies from here two cents higher. Aggressive traders might consider selling penny rallies, like the one we got today. Notice that the Euro is rallying into the US close every day. This is caused by American traders covering shorts, not wishing to run them into any overnight surprises.

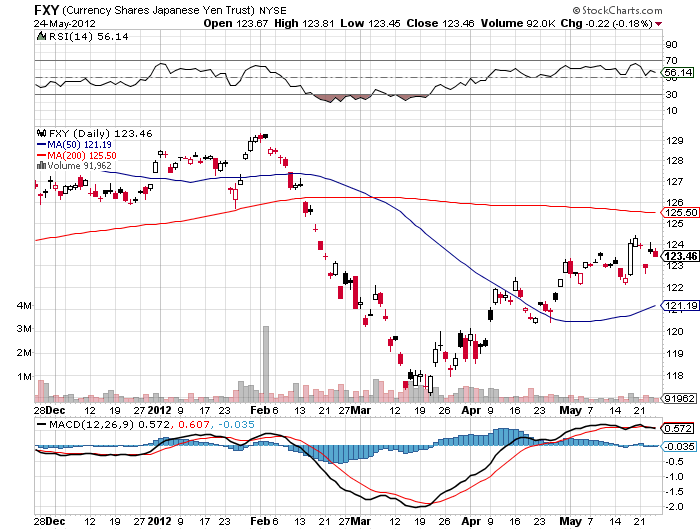

The Japanese yen seems to be stagnating here once again, now that the Bank of Japan has passed on another opportunity to exercise more much needed quantitative easing. Therefore, I will use the next dip to get out of my September put options at a small loss. There is a better use of capital and bigger fish to fry these days.

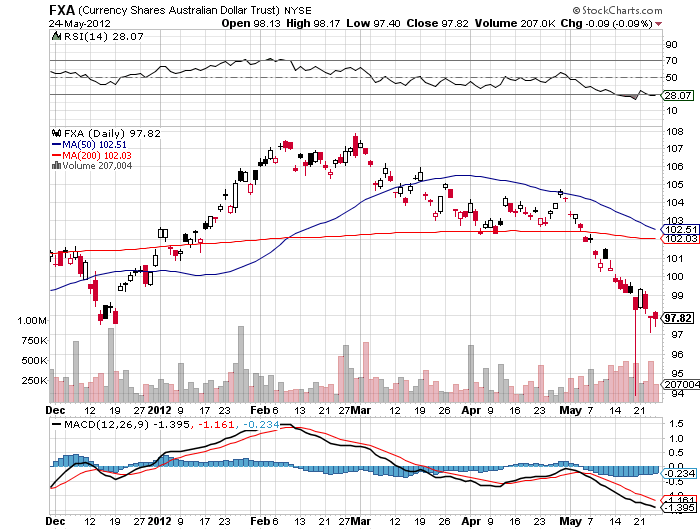

The Australian dollar has been far and away the world?s worst major currency this year, falling from $110 all the way down to $94 on a spike. It now languishes at $97. I long ago stopped singing ?Waltzing Matilda? in the shower. I hope all my Ausie friends took my advice at the beginning of the year and paid for their European and American vacations while their currency was still dear. We could see as low as $90 in the months to come.

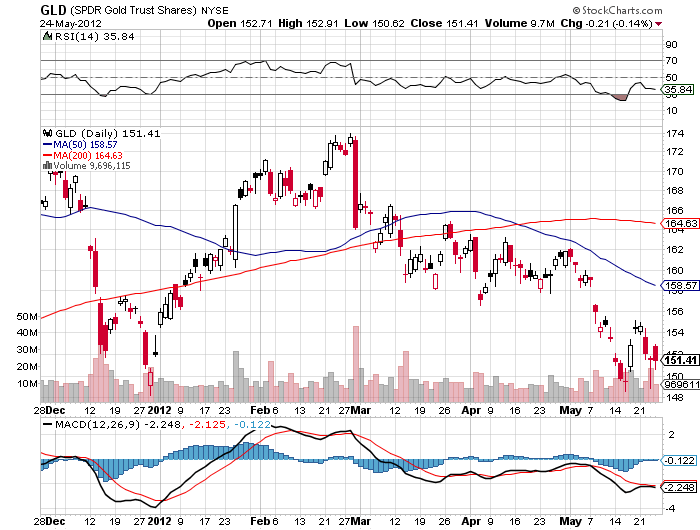

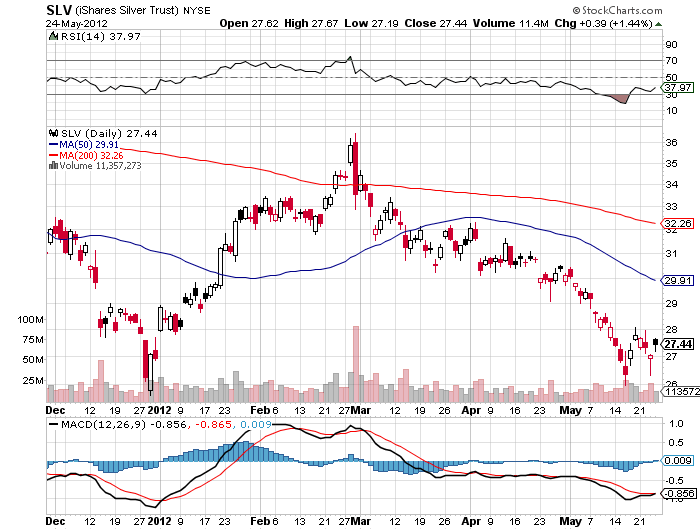

Gold (GLD) and silver (SLV) still look week, as this week?s failed rally attests. The strength of the Indian rupee still has the barbarous relic high priced for the world?s largest buyer, and this will continue to weigh on dollar based owners. But we are also reaching the tag ends of this move down from $1,922. Speculative short positions are at a multi-year low. It would take something pretty dramatic to get me to sell short gold again. For the time being, I am targeting gold at $1,500 on the downside, $1,450 in an extreme case, and $25 in silver.

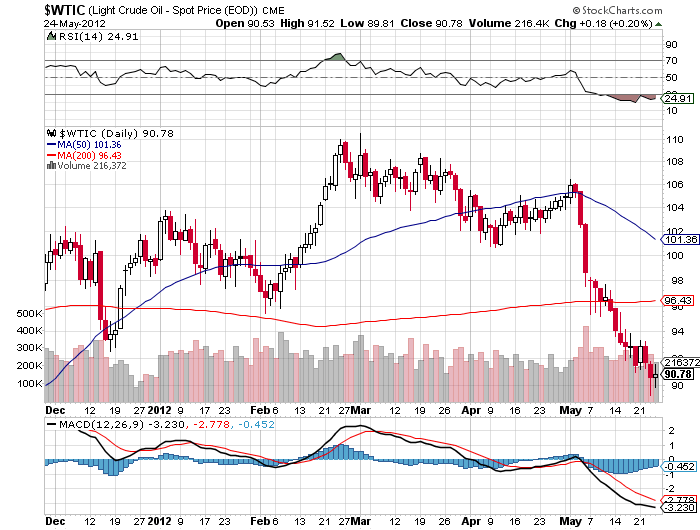

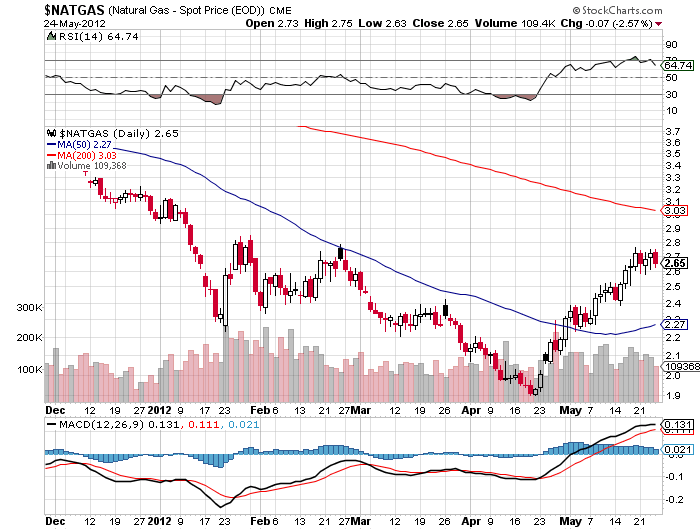

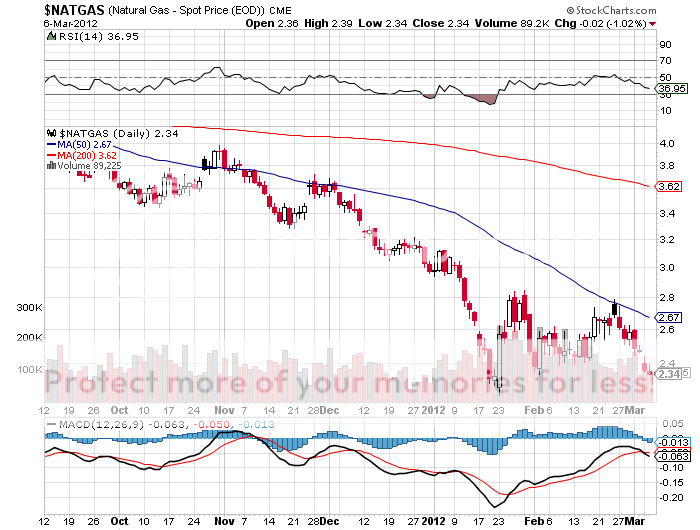

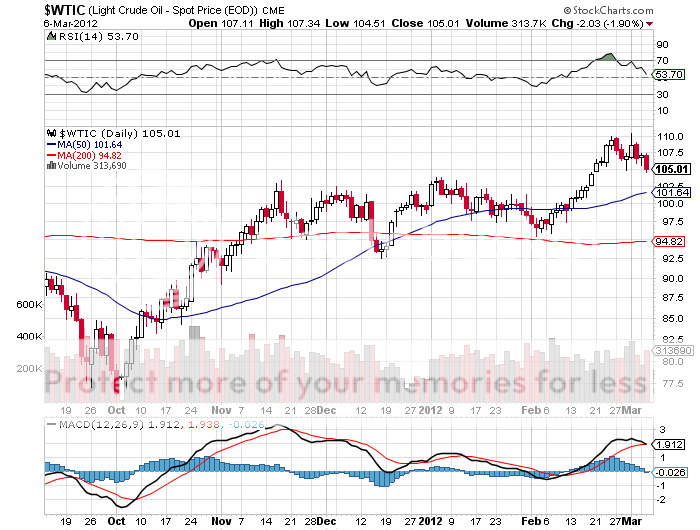

We are well into the move south for oil, which peaked just at the March 1 Iranian elections just short of $110/barrel. The market now seems to be targeting $87 for the short term. The global economic slowdown is the clear culprit here. But in the US, we are starting to see a clear drag on oil prices caused by the insanely low price of natural gas. You can see this clearly on the charts below where gas has been rising while Texas tea has been plunging. Utilities and industry are switching over to the cleaner burning ultra cheap fuel source as fast as they can. As a result, greenhouse gas emissions are falling faster in the US than any other developed country, according to the Paris based International Energy Agency. Sell any $4 rally in crude and keep a tight stop.

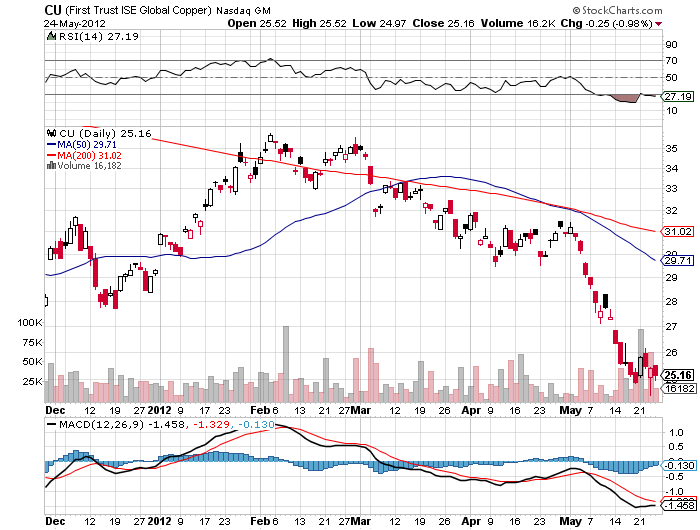

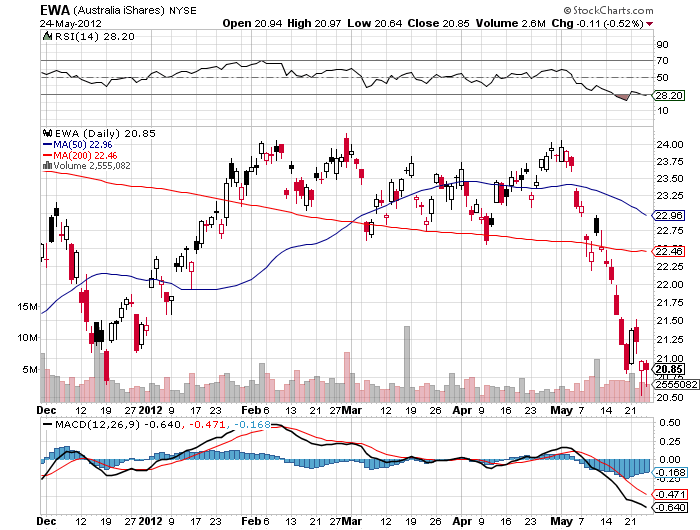

When China catches cold, copper gets pneumonia. So does Australia (FXA), (EWA), for that matter. The China slowdown will most likely continue on into the summer, knocking the wind out of the red metal. If copper manages to rally back up to $3.60, grab it with both hands and throw it out the window. Cover when you hear a loud splat. That works out to about $26.50 in the ETF (CU).

It all points to a highly choppy and volatile ?RISK ON? rally that could last a week or two. It will be a time when you wish you took your mother in law?s advice to get a real job by becoming a cardiologist or plastic surgeon. Do you want to know when I want to reestablish my shorts? If you get a modestly positive nonfarm payroll on at 8:30 am on Friday, June 1, that could deliver a nice two day rally that would be ideal to sell into.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-05-24 23:03:212012-05-24 23:03:21My Tactical View of the Market

I am constantly asked if there are any ways investors can take advantage of the collapse of the natural gas market, where at $2.34/MBTU prices are plumbing decade lows. I have recently made good money buying puts on the ETF (UNG), but these are not for the faint of heart. They call this contract the ?widow maker? for a good reason.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices are probably going to stay down for years. Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

However, there is one company that delivers a narrow rifle shot that could do extremely well in coming years, and that is Cheniere Energy (LNG). I first started following (LNG) a decade ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a loft $5/MBTU, Qatar invested $50 billion in in developing its own substantial gas resources. The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline. It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100 year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MBTU down to $2/MBTU. Any plans to import LNG from the other side of the world were rendered utterly worthless. Chenier?s billion dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed low single digits as the firm flirted with bankruptcy.

Enter China. The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil to soar from a 2008 low of $30 to $110. Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages. This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been spiking, gas has been crashing. Gas is now selling at 15% of the cost of oil on an adjusted BTU basis. Another way of saying this is that you can buy oil for $16 a barrel instead of $110. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

Enter the long term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day. Because very expensive, hard to get or offshore supplies were tapped, the price was set at $16/MBTU. Those contacts are now expiring. Do you think they?ll renew at the old price, or go to Cheniere for the $2 stuff. Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown last March prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice. Power companies there have been scrambling to obtain conventional energy supplies, and have been a major factor in driving oil up from $75 to $100 since the fall. Cheap gas supplies from the US would meet this demand nicely.

The trigger. Last May, Cheniere got US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquifaction plant, something that can be done with some expensive re-engineering. It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant. My hedge fund buddies have been accumulating this stock since October, when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better lead to long term players.

Then last week, Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $2 billion, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt. The Stock has just run up from $3 to $17. And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren. As a result, local permits for these are very hard to come by.

But as you can see, a whole host of geopolitical, technology and economic strands tie together in this one company, all of which are positive for the share price. If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please click here for their website at http://www.cheniere.com/default.shtml.

Did Somebody Light a Match?

https://www.madhedgefundtrader.com/wp-content/uploads/2012/03/gas.jpg246400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-03-07 23:02:352012-03-07 23:02:35Take a Look at Cheniere Energy (LNG)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.