Just as millions of people in the United States are sensing that life has returned to something that resembles normalcy, the Coronavirus’ delta variant has emerged as American technology stocks biggest upcoming inflection point.

This certainly ups the ante in the struggle to grapple with the pandemic and has wide-reaching consequences for your technology portfolio.

Fresh data from the U.S. Centers for Disease Control and Prevention shows that more than half of all new cases in the U.S. were attributed to the delta variant, which is believed to be easily transmissible.

About 50% of Americans are fully unvaccinated meaning 50% are not, which could lead to hellacious autumn for the 175 million who are not.

The tech market has sniffed this out.

Data suggesting this variant is three times as infectious as the original coronavirus strain is the catalyst for a massive rotation into premium big tech who boast glamorous balance sheets.

It is still unclear if this virus is actually deadlier or leads to more severe illness, but the health of Facebook, Google, Apple, Microsoft, and Amazon aren’t reliant on the outcome of the delta variant or at least relative to companies that have physical storefronts.

I believe the momentum in these names will continue in the short term as more countries prepare to carve up new movement restrictions and quasi lockdowns to combat the new variant.

The recent tech rotation has been inconspicuous but powerful and the who’s who of big tech are enjoying a stellar run in the past month with FB up 6%, GOOGL up 4.5%, AAPL up 13%, MSFT up 8%, and AMZN up 11%.

These premium tech stocks are acting almost like U.S. treasuries and are increasingly defined as a perceived flight to safety because of

the net high quality of the assets.

Whether there is another virus that kills another 4 million globally again, investors are confident that these prioritized tech stocks are immune to any meaningful weaknesses.

On a granular level, pullbacks are becoming highly rare and mini pullbacks are becoming the only practical entry points into these stocks.

Readers waiting for a 5% drop are still waiting.

Reading waiting for 10% drops risk never getting in when the going is good.

Fresh news of Japan banning spectators for the upcoming and badly organized Tokyo Olympics took down GOOGL and FB 2% intraday only for shares to make up half the losses in one afternoon.

The delta variant has strengthened the “buy the dip” philosophy that is deeply entrenched in these 5 tech names.

The strength of tech can be seen further down the totem pole in inferior names.

Shopify (SHOP), Canada’s ecommerce crown jewel, is another winner with shares up 19% in the past 30 days.

If this rotation continues, I can realistically expect dips or sideways price action in Uber (UBER), Lyft (LYFT), and Airbnb (ABNB) because their investment case weakens relative to the big 5 in a delta variant world.

Netflix (NFLX) is another one that will harvest the low-hanging fruit with strong near-term action resulting in a 9% gain in the past 30 days.

It’s highly likely that in more than several regions around the world, the delta variant will re-silo consumers and hamstring businesses.

Crushing any green shoots that the reopening is supposed to deliver isn’t an ideal runway to growth.

Epidemiologists are starting to come out of the woodwork with Hungarian virologist Ferenc Jakab saying Hungary will be lucky to “get away with August” when referring to a possible 4th wave.

This hasn’t been fully priced into the U.S. tech market and tech will enjoy a full-scale rotation if the 4th wave arrives in full force.

However, I don’t believe we are on the cusp of another $12+ trillion bailout for the delta like last time go around, which does cap momentum to the upside.

There will also be a lack of meme stock profit-taking and bitcoin profit-taking that can be rolled into the big tech safety trade.

Sensibly, this could be a short-term boost for emerging growth tech as well with the likes of DocuSign (DOCU), Zoom Video (ZM), and Teladoc (TDOC) benefiting from investors dusting off the 2020 playbook again.

I forgot to mention that U.S. treasuries falling to $1.36% is the primary reason why at the balance sheet level, growth tech will also get the benefit of the doubt in the short term.

This won’t just be a big 5 momentum encore, others will enjoy the fruits of labor.

Loss-making tech is inordinately reliant on rates being low to subsidize losses and as the 10-year rate has gone from 1.72% to 1.36%, it’s no surprise that growth tech looks like eye candy now too.

Big tech is certainly more durable and has the capacity to navigate around rising rates which is the deal-clincher for me.

I am inclined to get back into the market with any delta scare that cheapens tech before the next leg up.

The embarrassing loss in the judicial system against FB by the Feds is the cherry on top.

I am bullish tech in the short term.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-12 13:02:372021-07-15 18:32:16Ride the Momentum

Chinese regulators announced on our Independence Day that they were banning downloads of Uber’s China DiDi in the app stores in the country because it poses cybersecurity risks and broke privacy laws.

This was after DiDi raised $4.4 billion by listing its shares in New York.

However, unnamed sources leaked that China's cybersecurity watchdog suggested to DiDi that it delay its IPO before it happened.

Delaying a wealth generating event like the IPO is controversial.

At this point, DIDI, the Uber of China, is worth a speculative trade at $1 and that’s if the Chinese tech firm doesn’t delist before that.

No — scratch that — it’s not even worth your time at $1 if you hold currency denominated in USD or anything even half as credible.

But if you’re from somewhere like Venezuela wielding infamous bolivars then take a wild stab around $1 or double up at $0.50 for a trade.

There is a reason that I have never in the history of the Mad Hedge Technology Letter recommended buying a Chinese technology stock.

The astronomical risk isn’t justified.

The evidence is now out in public with Chinese big tech and the Chinese Communist Party (CCP) airing their dirty laundry.

Most sensitive business dealings are usually dealt with in-house in the land of pan-fried dumplings and Beijing roasted duck, so things must be spiraling out of control on the inside.

No doubt that inflation spikes are causing chaos everywhere, but China is particularly vulnerable because of the high volume of Chinese living in poverty.

It’s unrelated to this IPO, but another valid reason why Chinese “growth” is weakening fast.

Stateside, cashing out is normal for tech growth companies who want to reward earlier seed investors, their own management teams, and in this case the early-stage investors were Japanese Softbank (21.5%), Silicon Valley’s Uber (12.8%), and China’s Tencent (6.8%).

This was pretty much a big middle finger to these three along with the other Chinese investors which were about to profit big.

This is on the heels of the CCP nixing the Jack Ma Alipay IPO.

Chinese big tech has gone from darlings to pariahs in a short time proving that in the U.S., you get too big to fail, but in China, you get too big to exist.

Silicon Valley tech princelings are also validated for leaving China such as Facebook (FB), Google (GOOGL), Amazon (AMZN) and Netflix (NFLX).

If local Chinese tech can’t flourish in China, then forget about foreign tech in China.

It’s a non-starter.

Apple (AAPL) is the only exception because they are grandfathered in when China had no smartphone and now they provide too many local jobs to be kicked out.

There is definitely a plausible case that U.S. retail investors who were part of that $4.4 billion holdings should be refunded their capital because DiDi didn’t truthfully disclose the risk of potential Chinese regulations properly.

There is also the logic that Chinese companies should never be able to list in New York in the first place which would be sensible.

As it stands, Chinese companies don’t need to follow U.S. GAAP accounting standards and cannot be prosecuted by the U.S. legal system if they commit fraud, embezzlement, or any other financial crime and decline to leave Chinese soil.

This incentivizes Chinese companies listed in the U.S. to cheat U.S. investors with fraudulent accounting and deceitful behavior because they aren’t accountable at the end of the day.

The Invesco Golden Dragon China ETF (PGJ), which tracks the performance of US-listed Chinese stocks, has lost more than one-third of its value since February.

I can tell you from close friends who call themselves frontier investors that investing in China is not worth your time and the fear of missing out (FOMO) rationale is all marketing chutzpah and nothing much else.

China’s economy hasn’t had any positive growth in the past 10 years according to Chinese insiders off record.

This FOMO narrative is often peddled by Wall Street “professionals” who are making exorbitant fees for selling retail investors Chinese junk stocks masquerading as real companies.

Out of many financial pros I have talked to, China leads in terms of horror stories from foreign investors.

The Chinese financial system is a hoax created to lure foreign capital in and for it to never leave often viewed as a free lunch for the local recipients.

And I am not only talking about Chinese tech, but this phenomenon also extends to every reach of the financial system there.

At the end of the day, China’s tech aristocracy wished they originated in the United States which is why they went public here because our markets work and theirs don’t.

They got to New York in the first place by marketing false numbers to U.S. investors and concealing regulatory issues, and U.S. investors must not fall for this trap.

If you look at the Shanghai Stock Exchange Composite Index ($SSEC), it’s gone nowhere in the past year and rightly so.

Even Chinese investors don’t buy Chinese stocks because there is no trust in their financial system. They buy property instead or buy U.S. tech stocks.

Don’t be the next sucker.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/07/DIDI-1.png414876Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-09 15:02:092021-07-15 16:01:16Buyer Beware

If you are a believer in the FANGS (FB), (AAPL), (AMZN), (MSFT), (NFLX), with NVIDIA (NVDA) as an add-on, last week was definitely your week.

They rose every day, ending the week with a melt-up of epic proportions. After eight months in the penalty box, tech came back with a vengeance and is now two months into their comeback tour.

The icing on the cake was Facebook’s big win in the antitrust suit from the FTC. That suitably deep-sixes the issue not just for (FB) but all of big tech, possibly for years. The five stocks above now account for a hefty 22% of the S&P 500 (SPY).

The question now on everyone’s mind is what’s next for tech? 25%? 30% 50%? The answer is all of the above, but you have to give it some time, like years.

We are now in an overbought market where big tech has become the cheapest sector. In addition, the global chip shortage promises to get worse before it gets better, with some products seeing a 10X increase in a single generation.

Companies that can’t get the chips they want are resigning products around the chips they can get on the fly.

This has created enormous spillover demand for marginal suppliers like Advanced Micro Devices (AMD) and Micron Technology (MU). It has also accelerated the evolution of technology.

Companies that already have decade-long supply chains already set up, like Tesla, now have a big advantage. That’s why (TSLA) has managed a healthy 27% gain in six weeks.

The severity of the chip shortage is wildly estimated if you look at future design plans of the biggest industries. A tech rally lasting months, if not years, was a totally natural progression.

I’ll tell you who else is dropping the ball. Analysts and strategists are consistently underestimating the strength of the economic recovery and the torrid growth of earnings. They are lagging by about six months. That is why 80% of announcements have delivered upside surprises.

There are more surprises to come.

When markets peaked in April, an eye-popping 92% of shares were above their 50-day moving average. Now, we are only at 52%. That suggests we have another month of excitement before we get another short-term correction.

June Nonfarm Payroll Report comes in hot, up 850,000, an eye-popping 150,000 better than expected. The headline Unemployment Rate moved up slightly to 5.9%. Accommodation gained 269,000, and Food Services & Drinking Places were up 194,000. It was a true Goldilocks number for the stock market, but not the million some had hoped for. My 30% forecast for the Dow Average is looking good.

The Infrastructure Bill extends the hot economy well into 2023 and longer. Analysts better start upgrading now, who have been badly lagging behind the recovery. Tech stocks saw this six weeks ago and began their torrid rally. Buy everything on dips and stick with the barbell strategy to catch all of the rotations.

Rents will continue to go through the roof. Good thing you don’t live in Boise, ID, which is seeing the fastest rent increases in the county at 39% YOY. Of course, having the Micron Technology (MU) HQ there is a major push. Don’t expect any respite. With home prices soaring, rents will get dragged up as prospective buyers are priced out of the market.

Weekly Jobless Claims moderate further, 364,000 Americans filed new claims for unemployment benefits last week - lowest since pandemic. Still elevated from a typical pre-pandemic week when we would see about 210,000 claims.

Softbank’s capital flooding into Crypto, with Japan's SoftBank Group Corp has invested $200 million in Mercado Bitcoin, one of the largest cryptocurrency exchanges in Latin America signaling the start of the first phase of big institutional money hoping to take advantage of the digital currency craze.

Goldman Sachs is the top financial pick according to JP Morgan Chase. All cylinders are firing and we’ve just come off a fabulous 15% dip. A move to more sustainable revenue streams, like wealth management, is the reason, which Morgan Stanley did decades ago under my watch. I’m looking for $450 on dips. Buy (GS) on dips.

Morgan Stanley doubles its dividend, now that it has passed the Fed stress test and the tethers are off. It also announced a share buyback of $12 billion over the next year which may be increased. Buy (MS) on dips.

S&P Case Shiller National Home Price Index for April hits new high, up 14.6%, the biggest increase in 30 years. Phoenix leads at +22.3%, followed by San Diego at +21.6% and Seattle at +20.2%. The numbers run from incredible to unbelievable.

CRISPR Therapeutics goes through the roof, up 12% at the highs, on successful drug trials by Intellia Therapeutics (NTLA) and Regeneron (REGN). The Mad Hedge Biotech Letter core holding provided the gene-editing technology behind the 45% gain in (NTLA) today. It enabled the 85% elimination of a rare inherited fatal liver disease, transthyretin amyloidosis. Say that fast three times. Buy (CRSP) on dips. With Editas, there are only three small companies that have a monopoly here.

Facebook wins antitrust action, a federal judge dismissing an FTC action against the company. The move set the entire tech sector on fire. It looks like all of NASDAQ is going to much higher highs. I bet you had a great day. The court found that (FB) did not enjoy a monopoly which might have forced them to sell off Instagram and WhatsApp.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

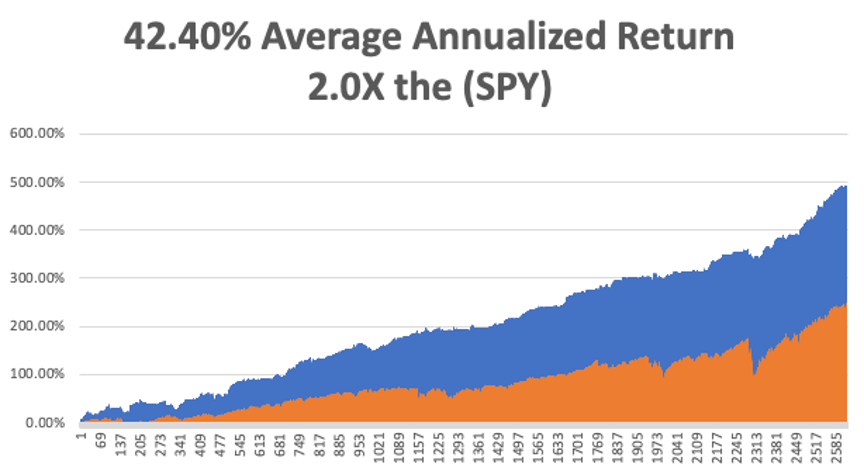

My Mad Hedge Global Trading Dispatch profit reached 0.71% gain so far in June on the heels of a spectacular 8.13% profit in May. That leaves me 100% in cash.

My 2021 year-to-date performance appreciated to 68.60%. The Dow Average is up 13.7% so far in 2021.

I spent the week sitting in 100% cash, waiting for a better entry point on the long side. Up this much this year, there is no reason to reach for the marginal trade, then maybe instead of the certainty. I’ll leave that for the Millennials.

That brings my 11-year total return to 491.15%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.40%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 112.59%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.7million and deaths topping 606,000, which you can find here.

The coming week will be a weak one on the data front.

On Monday, July 5, markets are closed for the US Independence Day celebration.

On Tuesday, July 6 at 10:00 AM, the ISM Non-Manufacturing Index for June is released.

On Wednesday, July 7 at 10:00 AM, the Federal Open Market Committee Meeting from the last meeting are published.

On Thursday, July 8 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, July 9 at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, with all the hiking I have been doing during the pandemic, I have been listening to a lot of WWII audio books lately. That reminds me of an old friendship I had with Toshiro Mifune, then the most movie famous star in Japan.

Mifune was drafted into the Japanese army during WWII where he served as an aerial reconnaissance photographer. After the war, that led him to work as a cameraman at Toho Productions, then the largest movie company in Japan.

A friend submitted his photo with an application for a casting call without his knowledge, and Toshiro, a good-looking guy, was one of 48 picked out of 4,000. He then met the legendary director, Akia Kurosawa, and the two launched the golden age of Japanese cinema in the late 1940s.

In just a couple of years, they produced blockbuster classic films like the Seven Samurai, Rashomon, and Throne of Blood, all of which are now required viewing by every American film school, and where Mifune demonstrated his impressive skills with a sword he picked up in the army.

I met Toshiro late in his career when he was cast as Admiral Isoroku Yamamoto for the 1976 Universal movie Midway. The problem was that Mifune couldn’t speak a word of English. I was brought in to bring Toshiro up to par in a crash course held at his west Tokyo mansion every afternoon seven days a week. We became good friends.

After a heroic effort, Mifune’s English was still awful, so the producers brought in a voice actor to dub Mifune’s part in Midway. That was Paul Frees, who provided the voice for the Disneyland’s Haunted House and Pirates of the Caribbean rides, as well as the cartoon Boris Badenov. His voice is still attached to those rides today, and I recognize it every time I take the kids.

Midway was a huge success and Mifune’s next big role was to play Commander Mitamura in Stephen Spielberg’s 1941. He followed that up with a role as Toranaga in James Clavell’s 1980 miniseries, Shogun, another old friend. (Clavell is a story for another day). My tutoring skills came back into demand once again, with better results.

Mifune died in 1997 at 77 and I miss him still.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/06/thumbsup.jpg514688Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-06 09:02:202021-07-06 11:11:20The Market Outlook for the Week Ahead, or All Eyes on the FANGS

The United States has long been the world leader in science and technology, but lately, they are falling asleep at the wheel.

At a psychological level, the feeling of threat has led to all sorts of unintended consequences, and it has been no accident we are seeing at a trade war.

The one key ingredient that has been missing is sustained investment in our research enterprise.

Without relentless investment into scientific and technological leadership, don’t expect any new breakthroughs, and the stagnation of US technology is evident in the evolution of a product that goes on sale to the consumer.

What happened to 5G? It’s been hyped for the past 3 years, but people have felt no need to upgrade for the spotty 5G that is available.

What happened to automated cars?

I thought by now, we would be able to get around with our flying cars.

What we do have are bigger iPads, faster iMacs, and the Microsoft Surface which is a tablet with an attachable keyboard.

I wouldn’t call that success.

But what the pandemic did was allow these big tech firms to get away without innovating, and I am not talking about the incremental innovation that makes a Model 3 Tesla 4% better than the prior iteration.

The hype of 10 years of digital transformation into one year has been profusely disseminated but misunderstood.

I can tell you that we didn’t experience 10 years of digital development pulled forward into 1 year.

That definitely was not the case over the past 15 months.

More accurately said, we had 10 years of expandable margin opportunities squeezed into one and the biggest beneficiary of this is the balance sheet of big tech.

What we did was give a reason for tech to not ditch this over-reliance on the smartphone which is going strong into its 13th year.

It was 2007 when Steve Jobs delivered us the iPhone and by 2008, many consumers were using it.

In 2021, the iPhone and variants still have a stranglehold on human life and the way business models are put together.

That won’t go away because of the pandemic and now these big tech behemoths have no reason to dip too far into capital expenditures.

Not only that, but they are also cutting back spend on office space and business travel too while sneakily reducing salaries of remote employees who move to cheaper cities.

In fact, the pandemic will elongate the smartphone dynasty, and any other meaningful tech has been put back on the backburner for the time being.

Then there are companies like Uber that are busy sorting out its decimated ride-sharing business before they can even dream about flying uber cars.

So, I am not surprised that the House Science Committee is taking up two bipartisan bills to try to push the agenda forward.

The need to act is best captured by two data points. First, as much as 85% of America’s long-term economic growth is due to advances in science and technology. There’s a direct connection between investment in research and development and job growth in the U.S.

Second, China increased public R&D by 56% between 2011 and 2016, but U.S. investment in the same period fell by 12% in absolute terms. China has likely surpassed the U.S. in total R&D spending and — through both investment and cyber theft — is working to overtake the U.S. as the global leader in science and technology.

America’s continued scientific leadership requires a comprehensive and strategic approach to research and development that provides long-term increased investment and stability across the research ecosystem. And it must focus on evolving technologies that are crucial to our national and economic security, like semiconductors and quantum sciences.

Now that the U.S. government has identified this issue as a national security issue, money will be thrown at the problem, but don’t expect anything to change tomorrow.

We are still a way off from forcing big tech to change their profit models and that will happen when they need to keep up with the next big thing.

There is no big next thing yet.

Until then, expect more incremental progress from your smartphone and Tesla.

It’s certainly not a bad situation to wield a smartphone that is 4% better each year or drive a Tesla that performs just a bit better as well.

Effectively, these enormous and profitable revenue models will stay in place and investors have no reason to worry about big tech moving forward.

This benefits the likes of Amazon, Tesla, Facebook, Google, Apple, and Netflix.

The only risk to U.S. tech is a threat that the U.S. government is absorbing themselves. What a great industry to be in.

Net-net, this is a great win for big tech and I don’t expect anything to drastically change, but get ready for a lot more digital ads in your daily consumption of digital content and more of the same products.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/06/smartphones.png412872Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-16 13:02:422021-06-23 01:33:53Smartphones Aren't Going Away

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:04:402021-04-26 10:44:52April 26, 2021

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

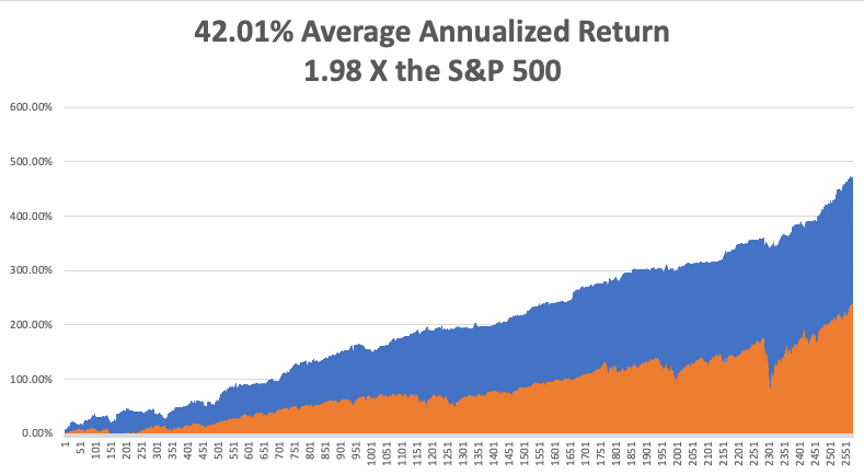

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/g-bebe-e1647874970894.png295450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:02:432021-04-26 10:45:23The Market Outlook for the Week Ahead, or The Correction is Over

(THE IRS LETTER YOU SHOULD DREAD),

(PANW), (CSCO), (FEYE),

(CYBR), (CHKP), (HACK), (SNE)

(FB), (AAPL), (NFLX), (GOOGL), (MSFT), (TSLA), (VIX)

(TESTIMONIAL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-06 10:06:022021-04-06 10:37:10April 6, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.