Mad Hedge Technology Letter

January 22, 2019

Fiat Lux

Featured Trade:

(HOW TO PLAY TECHNOLOGY STOCKS IN 2019),

(NFLX), (AAPL), (TSLA), (STT), (BLK)

Mad Hedge Technology Letter

January 22, 2019

Fiat Lux

Featured Trade:

(HOW TO PLAY TECHNOLOGY STOCKS IN 2019),

(NFLX), (AAPL), (TSLA), (STT), (BLK)

In the past week, the tech sector has received information allowing investors to sketch a concise roadmap of what to expect in the tech sector for the rest of 2019.

One – the bull story in technology isn’t dead and the December sell-off in tech growth stocks was overdone.

Two – the path to tech profits is filled with more booby traps than in year’s past.

Three – the migration to digital is becoming more pronounced by the millisecond.

If you go back about a month ago when tech stocks were at their trough, traders were pricing in about a 60% chance of a recession in 2019 or early 2020 and the data didn’t support it.

What people were confusing themselves with was slowing growth instead of a lack of growth.

Then we got the disastrous news from Apple (AAPL) indicating business in China was petering out forcing them to change tactics cutting iPhone prices.

The tech market went into full-on panic mode and the revelation of weak China data did not help either.

Netflix (NFLX) reported and the online streaming app offered some respite with outperforming growth numbers.

Netflix has been a favorite of the Mad Hedge Technology Letter since its inception but the caveat with Founder and CEO of Netflix Reed Hastings brainchild is that the extreme volatility makes it difficult to trade around on a short-term basis.

The stock is up 50% from its nadir and its growth story is solid and will perpetuate.

The next bastion of juiced-up growth for Netflix is the international audience and these numbers are examined closely with a fine-tooth comb by investors attempting to understand the direction of the company.

The company audaciously added 8.8 million in new international subscribers last quarter which handily beat the 7.6 million estimates by 1.2 million.

Netflix also announced a few days earlier that it would raise the price of a monthly subscription between 13%-18%, and investors treated the news with celebratory shots of tequila.

It has been consensus for years that Netflix was severely underpricing their premium content, and analysts have been screaming and kicking trying to get Hastings to push up their monthly prices.

The price hike coincides with a year where I believe Netflix can grow revenue over 30%.

The mix of these two developments illuminate a few things about Netflix.

Netflix has the content that consumers want and even if competition rears its ugly head, they aren’t even in the same ballpark in terms of breadth and potency of content.

They are the king of contents and I don’t see anyone knocking them off their elevated perch in 2019.

In many ways, the Netflix long-term thesis mirrors the tech industry’s long-term thesis emphasizing supercharged growth by any means possible.

Even though this strategy is risky, it is working for Netflix and the capital isn’t drying up to go after the best content producers money can buy.

This earnings report should put to rest the growth warning sirens for now, tech will grow this year, but earnings results will be more of a mixed bag with the occasional miss.

This is in stark comparison to early 2018 where every tech company and their mother were scorching earnings forecasts by a magnitude of two or three.

Last September, the tech market looked above its head and saw a few boulders about to crush the herd, but investors shrugged it off.

As we move forward, the tech sector and the overall market is inching closer to a recession.

The low-hanging fruit has been pocketed and incremental gains aren’t no-brainers anymore – this can be gleaned from Tesla (TSLA) curtailing their workforce by 7%.

This news was delivered by a letter from CEO of Tesla Elon Musk noting that these decisions have been made with the goal of “increasing the Model 3 production rate and making many manufacturing engineering improvements in the coming months.”

Basically, Musk has telegraphed that staff needs to perform better, identify efficiencies that will save costs which in turn will boost profit margins.

This doesn’t mean that the era of tech growth is over, but this signals that tech companies are becoming more fidgety about loss-making operations and have ultimately targeted profits which shout at investors' late-cycle economics.

Musk needs to turn Tesla into a perennial profit machine to prove naysayers wrong, and now is the time to turn the page and max out his rocket fuel.

If the recession hits, investors could turn against Tesla and capital could dry up.

This newfound modesty towards the e-car business model is, in no doubt, exacerbated by the ratcheting up of fierce competition from the traditional automobile makers.

Tesla is in the e-car lead for battery technology, revolutionary production processes, and have a treasure trove of data that German companies would do anything to get their hands on.

Musk knows Tesla has fought this hard to get to this point, and he'd rather have the ball in his hands with 10 seconds left and a tie game just like Michael Jordan of the Chicago Bulls did.

Shaving off the excess has meant removing the customer referral program that was too costly that included benefits like half a year of free charging.

Part of this also has to do with Tesla losing their tax credit at the end of the year as well as giving more impetus to trimming costs.

Becoming a mass-market car manufacturer means it is important to price the car at affordable price points and that will be extremely difficult.

The goal is to deliver a $35,000 e-car that performs comparably to the rest of the fleet but produced with 7% less hands.

Can Musk do it?

I wouldn’t bet against him.

Musk means business and is hellbent for revenge against his arch enemies – the Tesla short community who he has habitually dragged under the bus through the media.

Piggybacking on this tougher profit-making climate is Boston-based finance company State Street Corporation’s (STT) announcement reducing headcount by 1,500 amounting to 6% of the global workforce.

The firm cited the urgent need to automate processes that will give the company a bigger foothold into the digital sphere.

The same theme was echoed at BlackRock Inc. (BLK), the world’s largest asset manager, who will eliminate 3% of its global workforce, or 500 people, amid an existential threat from the temporary ineffectiveness of passive investing.

In a rising market, it is guaranteed that assets at these types of funds almost always go up.

However, with an injection of recent volatility, passive investors have seen their balances dwindle with the market spawning abrupt outflows.

The need to zig and zag with the market is now painfully obvious and using technology to plug in the gaps will be cheaper and more appropriate for late cycle price action.

This is a suitable segue way into the third point – the fluid follow-through of the digital migration and the debacle of Sears prove my point.

Hedge fund manager Eddie Lampert and his firm ESL have navigated this famous American retailer into the ground.

This is what happens when the entire retail industry goes online when you don’t.

To make matters worse, Lampert has probably never set foot into his own investment.

Each time I roam the aisles of Sears, it’s about as crowded as a mortuary at midnight – an elementary story of a mismanaged enterprise.

Sears is an example of digital ignorance and it’s not the only one.

Gymboree Group, the baby clothing company, is another one to put on the list – the firm filed for Chapter 11 bankruptcy protection.

The company will close more than 800 Gymboree and Crazy 8 stores, this is the second time they have filed for bankruptcy protection in the past two years.

Unsurprisingly, the firm cited a sudden decrease in mall traffic and a surge in online alternatives as the reason for the economic softness.

The economy does not operate in a vacuum and any analog company who voluntarily misses the pivot to digital is voluntarily digging their own grave.

These three trends will only become more exaggerated moving forward threatening companies like Apple who fail to innovate after more than a decade of selling the same product, other companies don’t have the balance sheets to handle the same weakness.

Mad Hedge Technology Letter

January 16, 2019

Fiat Lux

Featured Trade:

(3D PRINTING GETS A SECOND WIND),

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

Global Market Comments

December 17, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THERE’S NO SANTA CLAUS IN CHINA)

($INDU), (SPY), (TLT), (AAPL), (AMZN), (NVDA), (PYPL), (NFLX)

On Friday, five serious hedge fund managers separately called me out of the blue and all had the same thing to say. They had never seen the market so negative before in the wake of the worst quarter in seven years. Therefore, it had to be a “BUY”.

I, on the other hand, am a little more cautious. I have four 10% positions left that expire on Friday, in four trading days, and on that day I am going 100% into cash. At that point, I will be up 3.5% for the month of December, up 31.34% on the year, and will have generated positive return for one of the worst quarters in market history.

I’m therefore going to call it a win and head for the High Sierras for a well-earned Christmas vacation. After that, I am going to wait for the market to tell me what to do. If it collapses, I’ll buy it. If it rockets, I’ll sell short. And I’ll tell you why.

These are not the trading conditions you would expect when the economy is humming along at a 2.8% annual rate, unemployment is running at a half-century low, and earnings are growing a 26% year on year. You can’t find a parking spot in a shopping mall anywhere.

However, the lead stocks like Apple (AAPL), Amazon (AMZN), and Netflix (NFLX) have plunged by 30%-60%. Price earnings multiples dropped by a stunning 27.5% from 20X to 14.5X in a mere ten weeks. Half of the S&P 500 (SPY) is in a bear market, although the index itself isn’t there yet. I would rather be buying markets on their way up than to try and catch a falling knife.

There is only one catalyst for that apparent yawning contradiction: The President of the United States.

Trump has created a global trade war solely on his own authority. Only he can end it. As a result, asset classes of every description are beset with uncertainty, confusion, and doubt about the future. Analysts are shaving 2019 growth forecasts as fast as they can, businesses are postponing capital spending plans, and investors are running for the sidelines in droves. Business confidence is falling like a rock

To paraphrase a saying they used to teach you in Marine Corps flight school, “It’s better to be in cash wishing you were fully invested than to be fully invested wishing you were in cash.”

The Chinese have absolutely no interest in caving into Trump’s wishes. They read the New York Times, see the midterm election result and the opinion polls, and are willing to bet that they can get a much better deal from a future president in two years.

I have been dealing personally with both Trump and the Chinese government for four decades. The Middle Kingdom measures history in Millenia. The president lives from tweet to tweet. The Chinese government can take pain by simply ordering its people to take it. We have elections every two years with immediate consequences.

The best we can hope for is that the president folds, declares victory, and then retreats from his personal war. This can happen at any time, or it may not happen at all. No one has an advantage in predicting what will happen with any certainty. Not even the president knows what he is going to do from minute to minute.

It is the possibility of trade peace at any time that has kept me out of the short side of the stock market in this severe downturn. That robs a real hedge fund manager of half his potential income. Trade peace could be worth an instant rally of 10% in the stock market. Even a lesser move, like the firing of trade advisor Peter Navarro, would accomplish the same.

The market was long overdue for a correction like the one we have just had. Investors were getting overconfident, cocky, and excessively leveraged. In October, we really needed the tide to go out to see who was swimming without a swimsuit. But if the tide goes out too far, we will all appear naked.

Thanks to some very artful trading, my year to date return recovered to +27.54% boosting my trailing one-year return back up to 27.54%. I covered an aggressive short position in the bond market (TLT) for a welcome 14.4% profit. I also took profits with an instant winner in PayPal (PYPL). On the debit side, I stopped out of an Apple call spread for a minimal loss.

December is showing a very modest loss at -0.26%. The market has become virtually untradeable now, with tweets and China rumors roiling markets for 500 points at a pop. And this is against a Dow Average that is down a miserable -2.8% so far in 2018. I should have listened to my mother when she wanted me to become a doctor.

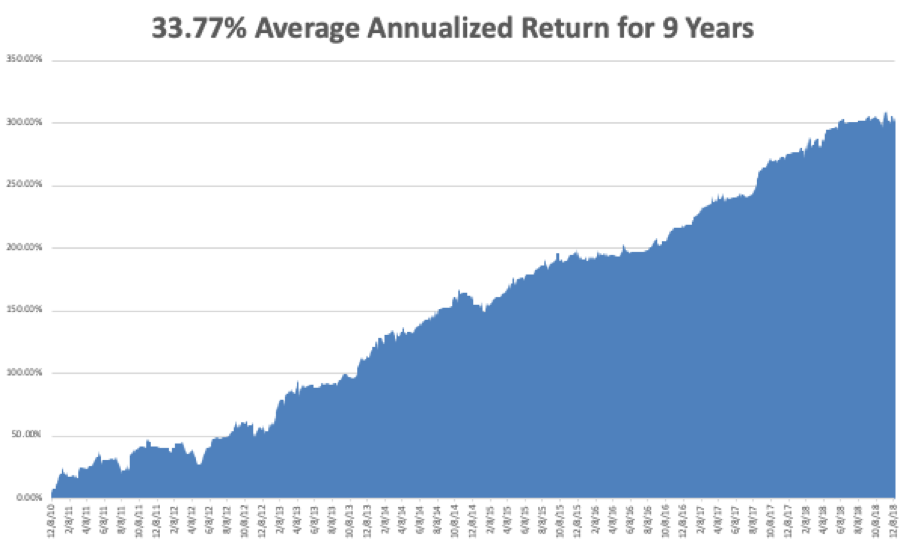

My nine-year return nudged up to +304.01. The average annualized return revived to +33.77.

The upcoming week is all about housing data, with the big focus on the Fed’s interest rate hike on Wednesday.

Monday, December 17 at 10:00 AM EST, the November Homebuilders Index is out.

On Tuesday, December 18 at 8:30 AM, November Housing Starts are published.

On Wednesday, December 19 at 10:00 AM EST, November Existing Home Sales are released.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

At 2:00 PM the Federal Reserve Open Market Committee announces a 25 basis point rise in interest rates, taking the overnight rate to 2.25% to 2.50%. An important press conference with governor Jay Powell follows.

Thursday, December 20 at 8:30 AM EST, we get Weekly Jobless Claims.

On Friday, December 21, at 8:30 AM EST, we learn the latest revision to Q3 GDP which now stands at 2.8%.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be battling snow storms driving up to Lake Tahoe where I’ll be camping out for the next two weeks. Mistletoe, eggnog, and endless games of Monopoly and Scrabble await me.

Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 13, 2018

Fiat Lux

Featured Trade:

(WHAT’S THE MATTER WITH APPLE?),

(AAPL), (MSFT), (KO), (AMZN), (CLX), (NFLX),

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

It was 38 years ago today that Apple (AAPL) went public and has generated a 43,000% return since its $22 IPO price. If you bought one share of Apple way back then for $22 it would be worth a breathtaking $95,000 today.

I waited until the next crash and then bought it at $4, and it sits in one of my “no touch” ultra-long-term retirement portfolios today.

Suddenly, the torture I endured taking Steve Jobs around to visit the New York institutional investors during the early 1980s was worth it.

The great rule of thumb I have learned after 50 years of investment is that if you hold a stock long enough, the dividend will exceed your original capital cost, giving you a 100% a year annual cash flow.

Three months ago, Apple was the Teflon stock of the entire market, the company that could do no wrong, the only “safe” stock that traded. Any selling met a wave of buying from Oracle of Omaha Warren Buffet and Apple itself, limiting corrections to a feeble 4%.

What a difference three months make!

Now the shares have become a market pariah, targeted by algorithms and hedge funds alike, and beaten like the proverbial red-headed stepchild. As a result, the shares have plunged an eye-popping 29.61%, vaporizing $311 billion in market capitalization.

Which begs one to ask the question, “What’s the matter with Apple?” How can things go from so right to so wrong?

Just like success has many fathers, failure is an orphan.

The harsh truth is that Apple became too much of a good thing to too many people. Expectations had become excessive and it had become too widely owned by traders with weak hands. In other words, people like me.

I had been cautious of Apple for a while because if its massive China exposure. You don’t want to own a company that relies entirely on Middle Kingdom production during a running trade war. Apple sold an incredible 216 million iPhones in 2017, and all of them are made at the Foxconn factories in southern China.

Apple has become the whipping boy for both sides in the trade conflict. The company has always run the risk of its Foxconn workers arriving at work late someday, or not showing up at all at the prodding of Beijing. Recently, Trump said iPhones imported from China could be subject to the current 10%, soon to be 25% tariff.

The final nail in the coffin came on Monday morning when we learned of a lower Chinese court’s ruling against Apple in a lawsuit from QUALCOMM (QCOM). Never mind that the suit was years old and applied only to the company’s older phones. With the shares in free fall, that is just what investors DIDN’T want to hear.

However, Apple is not dead, it is just resting. Or, call it ripening.

Not only could Apple recover strongly from these abysmal levels, IT COULD DOUBLE IN VALUE.

The core of my argument (no pun intended) is that Apple is in the process of fundamentally evolving its business model. It is rapidly morphing from a one-time sale only hardware company to a recurring subscription services company. And that is where the big money is in the future.

Microsoft (MSFT) is already doing it, so are Amazon (AMZN) and Netflix (NFLX). In fact, everyone is doing it, even the Diary of a Mad Hedge Fund Trader.

In fact, Apple's services revenue could balloon to $100 billion in five years, compared to its estimated total sales this year of $265 billion.

This accomplishes several important things. It moves the company out of a 30% gross margin business to a 70% gross margin. It converts Apple from a highly cyclical to stable earnings growth. Stable earnings growth companies are awarded much higher share price multiples.

Look no further than my next-door neighbor, Clorox (CLX), which trades at a much loftier 23X multiple and Coca-Cola (KO) which can be found at generous 19X multiple. Earnings visibility is worth its weight in gold. This could make Apple’s current 14X multiple a thing of the past.

Of course, we are not going to see a straight line move from one dominant business to another, and the road along the road could be bumpy. We could easily see one more meltdown which takes us to the subterranean $160 handle.

But $10 of downside risk versus $170 of upside? I’ll take that all day long. I bet you will too!

Global Market Comments

November 26, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or ARE WE IN OR OUT?)

(FB), (AAPL), (AMZN), (NFLX),

(GOOG), (SPY), (TLT), (USO), (UNG), (ROM)

Are we already in a recession or still safely out of one?

That is the question painfully vexing investors after the stock market action of the past seven weeks.

There is no doubt that the economic data has suddenly started to worsen, setting off recession alarms everywhere.

October Durable Goods were down a shocking 4.4%. Weekly Jobless Claims hit 224,000, continuing a grind up to a 4 ½ month high. Is the employment miracle ending? Goldman Sachs says growth is to drop below 2% in 2019, well below Obama era levels. Maybe that’s what the stock market crash is trying to tell us?

The Washington political situation continues to erode confidence by the day. We have already lost real estate, autos, energy, semiconductors, retailers, utilities, and banks. But as long as tech held up, everything was alright.

Now it’s not alright.

The tech selloff we have just seen was far steeper and faster than we saw in the 2008-2009 crash. You have to go all the way back to the Dotcom Bust 18 years ago to see the kind of price action we have just witnessed. The closely watched ProShares Ultra Technology Fund (ROM) has cratered from $123 to $83 in a heartbeat, off 32.5%.

Which begs the question: Are we already ten months into a bear market? Or is this all one big fake-out and there is one more leg up to go before the fat lady sings?

I vote for the latter.

If this is a new bear market, then it is the first one in history with the lead sectors, technology, biotechnology, and health care, announcing new all-time profits going in.

So, either Facebook (FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and Google (GOOG) are all about to announce big losses in coming quarters, which they aren’t, or the market is just plain wrong, which it is.

Which leads us to the next problem.

Markets can be wrong for quite a while which is why I cut my positions by half at the beginning of last week. To quote my old friend, John Maynard Keynes, “Markets can remain irrational longer than you can remain liquid,” who lists his entire fortune in the commodities markets during the Great Depression.

To see this all happen in October was expected. After all, markets always crash in October. To see it continue well into November is nearly unprecedented when the strongest seasonals of the year kick in. This was the worst Thanksgiving week since 2011 when we were still a wet dog shaking off the after-effects of the great crash.

There are a lot of hopes hanging on the November 29 G-20 Summit to turn things around which could hatch a surprise China trade deal when the leaders of the two great countries meet. The Chinese stock market hit a one month high last week on hopes of a positive outcome. Do they know something we don’t?

There were multiple crises in the energy world. You always find out who’s been swimming without a swimsuit when the tide goes out. James Cordier certainly suffered an ebb tide of tsunami proportions when his hedge fund blew up taking natural gas (UNG) down 20% in a day.

Cordier got away with naked call option selling for years until he didn’t. All of his investors were completely wiped out. I have always told followers to avoid this strategy for years. It’s picking up pennies in front of a steamroller. Same for naked puts selling too.

The Bitcoin crash continued slipping to $4,200. I always thought that this was an asset class created out of thin air to absorb excess global liquidity. Remove that liquidity and Bitcoin goes back to being thin air, which it is in the process of doing.

Oil (USO) got crushed again, down an incredible 35.06% in six weeks, from $77 a barrel all the way down to $50 as recession fears run rampant. Panic dumping of wrong-footed hedge fund longs accelerated the slide. They all had expected oil to rocket to $100 a barrel in the wake of the demise of the Iran Nuclear Deal and the economic sanctions that followed.

Apparently, Saudi Arabia’s deal with the US now is that they can chop up all the journalists they want at the expense of a $27 a barrel drop in the price of oil. That will cut their oil revenues by a stunning $97 billion a year. That’s one expensive journalist!

Watch the price of Texas tea carefully because a bottom there might signal a bottom for everything including tech stocks. And I don’t see oil falling much from here.

As for performance, Thanksgiving came early this year, at least in terms of the skinning, gutting, and roasting of my numbers. If you do this long enough, it happens. Every now and then, markets instill you with a strong dose of humility and this is one of those time.

My year to date return dropped to +25.72%, and chopping my trailing one-year return stands at 31.71%. November so far stands at a discouraging -3.91%. And this is against a Dow Average that is down -2.01% so far in 2018.

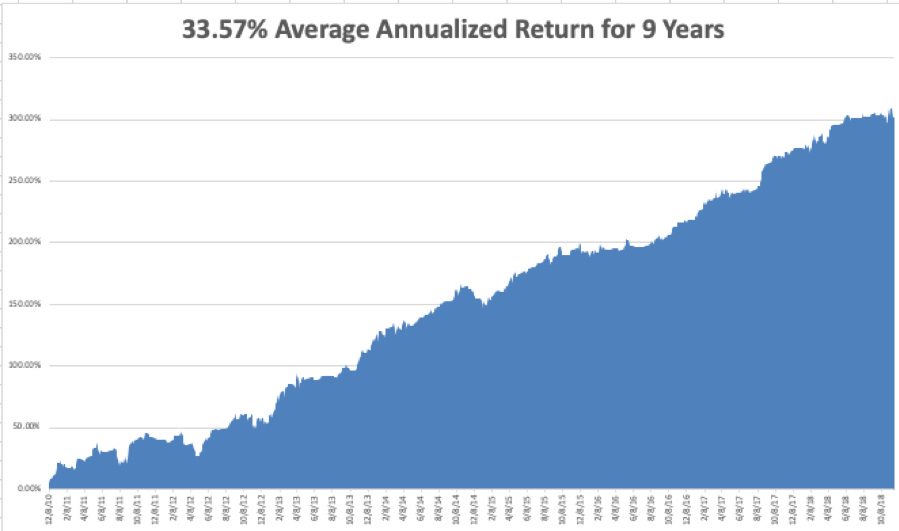

My nine-year return withered to +302.19%. The average annualized return retraced to +33.57%.

The upcoming week has some important real estate data coming. However, all eyes will be upon the Friday G-20 announcement from Buenos Aires. Will the trade war with China end, or get worse before it gets better?

Monday, November 26 at 8:30 EST, the Chicago Fed National Activity Index is published.

On Tuesday, November 27 at 9:00 AM, the all-important CoreLogic Case-Shiller National Home Price Index is out. It will be interesting to see how fast it is falling.

On Wednesday, November 28 at 8:30 AM, Q3 GDP is updated. How fast is it shrinking?

At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 29 at 8:30 we get Weekly Jobless Claims which have been on a four-month uptrend. At 10:00 AM, October Pending Home Sales are printed.

On Friday, November 30, at 9:45 AM, the week ends with a whimper with the Chicago Purchasing Managers Index.

The Baker-Hughes Rig Count follows at 1:00 PM. At some point, we will get an announcement from the G-20 Summit of advanced industrial nations.

As for me, I drove through the first blizzard of the year over Donner Pass to finally crystal clear skies of San Francisco. Long-awaited drenching rains had finally cleansed the skies. Every Tahoe hotel was packed with Californians fleeing the smokey skies.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 23, 2018

Fiat Lux

Featured Trade:

(SURVIVING THANKSGIVING)

(SPY), (TLT), (TBT), (GLD), (FXE), (FXY), (USO), (VIX), (VXX), (NVDA), (NFLX), (AMZN)