Below please find subscribers’ Q&A for the May 29 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Since Elon Musk is raising tons of money for his AI startup called xAI, will this impact Tesla’s (TSLA) stock price?

A: Yes, it's a very positive move for Tesla because anytime Elon Musk raises money anywhere in his network, it takes the need off of him to sell Tesla shares for cash. And I think his xAI will be the next trillion-dollar company, and SpaceX is in front of it as another trillion-dollar company. Those stocks, he can sell any time and raise a lot of money, but the other two are still private companies. We can't buy them yet unless we buy some of the public vehicles offered by venture capitalists like Ron Baron who has heavy positions in both Tesla and SpaceX. So, no direct plays yet on these companies, but no doubt when they become incredibly valuable, he'll take them all public and become the richest man in the world two or three times over. So yes, that is a positive.

Q: Where do you think (TLT) will be in the next few months?

A: In a narrow trading range. I think we're basically in a $86 to $91 trading range, and we'll go nowhere until we get clarification on Fed interest rate cuts. At the rate the economy is slowing, we may get one in September, and even if the Fed doesn't cut, the rest of the world will, including Japan, Europe, Great Britain, and so on. So we may get our interest rates dragged down here by foreign countries that all have much weaker economies than the US.

Q: Should I keep buying big tech stocks after Nvidia's (NVDA) blowout earnings?

A: Well, if you recall back in the ancient times of April, Nvidia had a 20% sell-off, and most of the tech stocks were down at least 10%. So, I would wait for the next 20% sell-off of Nvidia not only to buy Nvidia but all other big tech stocks as well, because it basically is a big tech story and will continue for the rest of the year like that. So we're really looking to buy dips among the big tech winners, and those would include Amazon (AMZN), Meta (META), Microsoft (MSFT), and so on.

Q: How long can the US economy go without a recession?

A: Five years. The way our economic cycle works is after a long period of growth, companies get overconfident, over-invest, create excessive capacity in the markets for everything, and that leads to a crash and a recession, deflation, and lower interest rates. So even if we don't get major moves in the (TLT) upside now, you always will over the long term get interest rates going back to 2 or 3% for the 10-year so it’s a great long-term hold. That is the economic cycle—that's what creates bear markets and it’s known as “Boom and Bust”. Long may it live because that’s where we traders earn our crust of bread. But this time may be different. We may go longer than 5 years because AI is still in its infancy, still rolling out, and the number of companies making actual profits in AI will go from 3 to 300 over the next five years.

Q: I'm looking to buy gold in an investment account (GLD). Would you do that now, if so, what would you recommend?

A: I would recommend GLD (SPDR Gold Trust) because the metals are still outperforming the miners, miners being held back by the inflation rates unique to the mining industry, which are much higher than the 3.3% for the general economy. And if you want to add a little more spice to your portfolio, buy some silver (SLV) because it is rising at three times the rate of gold thanks to Chinese speculation. You might buy some copper while you're at it too—it's moving almost as fast as gold is.

Q: Which big tech firm is next to issue a dividend?

A: That's an easy answer, it's Netflix (NFLX). But there's a more important question out here— Which is the next tech stock to issue a stock split? And guess what the answer is? Netflix again, which needs to declare both a dividend and a stock split. It's at an all-time high, has a very high share price, and over time, stocks that split deliver double the performance of the S&P 500. So, the mere announcement will suck in a lot of new retail investors as we just saw with Nvidia (NVDA), where we got a $250 move on the split announcement. So, watch your splits, and in fact, I'm going to be devoting a major piece of next Monday's newsletter to splits and how to play them.

Q: Why has the stock market been so strong this year when interest rates are high?

A: The answer to that is AI. We are still in the very early days of AI, and as I mentioned earlier, only three companies are making money from AI right now. That's Nvidia (NVDA), Microsoft (MSFT), and Google (GOOG). That number will increase as AI moves down the food chain and everybody starts using it, including you and me. I view the AI development as similar to 1995 when all of a sudden we got Netscape, a navigator that made the Internet available to the public, Dell Computers (DELL), and Microsoft (MSFT) software all at once hitting the market and creating the online economy essentially from scratch. Something of that magnitude is what the stock market is discounting now. Think of it in terms of the revolutionary new technologies of 1995, which means we have another 5 or 6 years to go, and that's why the stock market is so strong.

Q: Should I invest in Berkshire Hathaway (BRK/B), or do you think their magic will run out soon?

A: I don't think their magic will ever run out. Of course, the day that Warren Buffett dies it'll be down 10%, but then you'll want to buy it with both hands because Warren has already replaced himself with a first-class management team who is carrying on his strategy. Any selloffs in Berkshire you get this summer, go in there and buy the calls, the call spreads, the stock, the LEAPS, and the kitchen sink. Still a great long-term BUY, and I see $500 either late this year or next year in (BRK/B).

Q: I'm a member of IM Academy.

A: Oh my gosh. I would let your membership expire, except you're probably on auto-renewal, and the only way to stop your subscription is to call your credit card company and ask them to block the billings. That is the problem with these predatory financial newsletters, they're impossible to get out of, even when they promise refunds anytime.

Q: Are there any Chinese stocks you like now?

A: No, but the highest quality stock in China is Alibaba (BABA). It's basically a combination of Amazon and PayPal in China, but you still have a very high political risk investing in anything in China. The currency is very weak, so better fish to fry is my opinion. And I tend to avoid countries suffering from demographic implosions.

Q: Should we buy (TLT) now or wait?

A: I would wait until we get some upside momentum going and we complete a few more downside tests.

Q: What's the best place to put cash in the summer?

A: The answer is always good old 90-day US Treasury bills. They are still paying 5.25%.

Q: What are your thoughts on PayPal (PYPL)?

A: I'm avoiding that sector because of over-competition crushing profit margins; that has been a problem for a couple of years now. Don't confuse “gone down a lot” with cheap.

Q: Which oil companies are the best to invest in right now?

A: You can buy Exxon Mobil (XOM) for the high dividend and the sheer size of the company. My second is Occidental Petroleum (OXY), because Warren Buffett owns 25% of the company, has shrunk the float, and that has a result in magnifying any moves up in the stock. Also, I somewhat admire Warren Buffett's stock-picking ability. And of course, I’ve been following the California company OXY since 1970, back when it was run by Armand Hammer, a friend of Vladimir Lenin, so my connections with the company go back a very long time.

Q: Do you like DuPont (DD) for the three-way split?

A: I do, but DuPont has a major problem looming with lawsuits over the PFAS chemicals—those are the forever chemicals which are all over the country, all over the food supply, and cause cancer. So that could be sort of like a Johnson & Johnson-type liability problem with the talcum powder. So again…why look for trouble? Buying a stock facing that kind of liability could be another tobacco situation.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There comes a time in every trader’s life when it’s time to face harsh reality and admit that you’re just dead wrong.

As much as I thought a I had strong case for the best stocks to move sideways before continuing their upward drive, the markets decided otherwise. One thing I have learned over my half-century of trading is that you never argue with Mr. Market. He is always right.

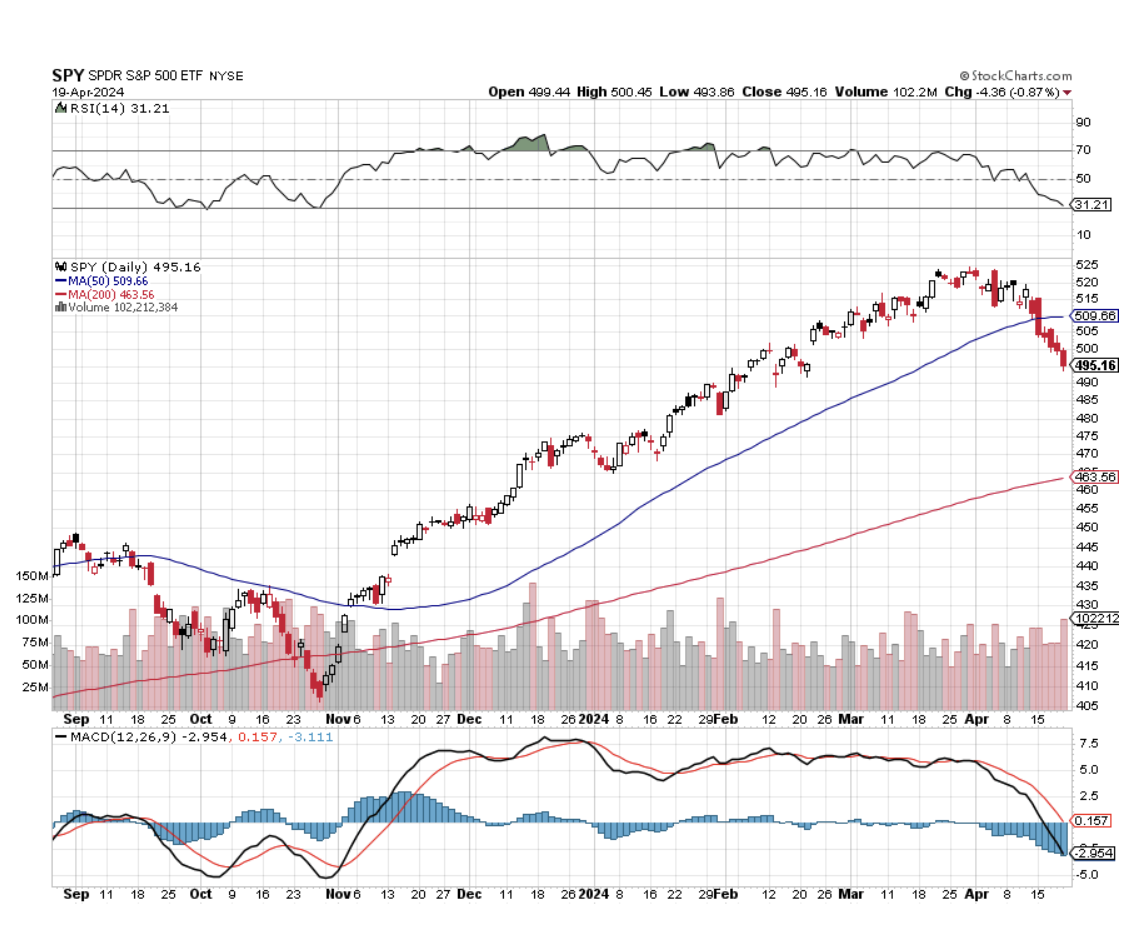

So it was with some dismay that on Friday, I watched NVIDIA (NVDA) shares slice through its 50-day moving average at $840 like a hot knife through butter putting the shares into a free-fall. Virtually the next print was the low of the day at $760, down 10% on the day.

There was no new news about (NVDA). Its prospects look as bright as ever, and there are a series of conferences of earnings reports over the coming month to remind us of that. But sometimes, the market just doesn’t care.

(NVDA) has had a great run, up some 144% since October. During this time, I executed a dozen profitable long-side trades. But when you’re that aggressive you know in advance that the last trade is going to kill you and that is the case today. (NVDA) is falling because of the sheer weight of its price.

New flash: while (NVDA) is still the cheapest big tech stock in the market, cheap stocks can get cheaper as we all know.

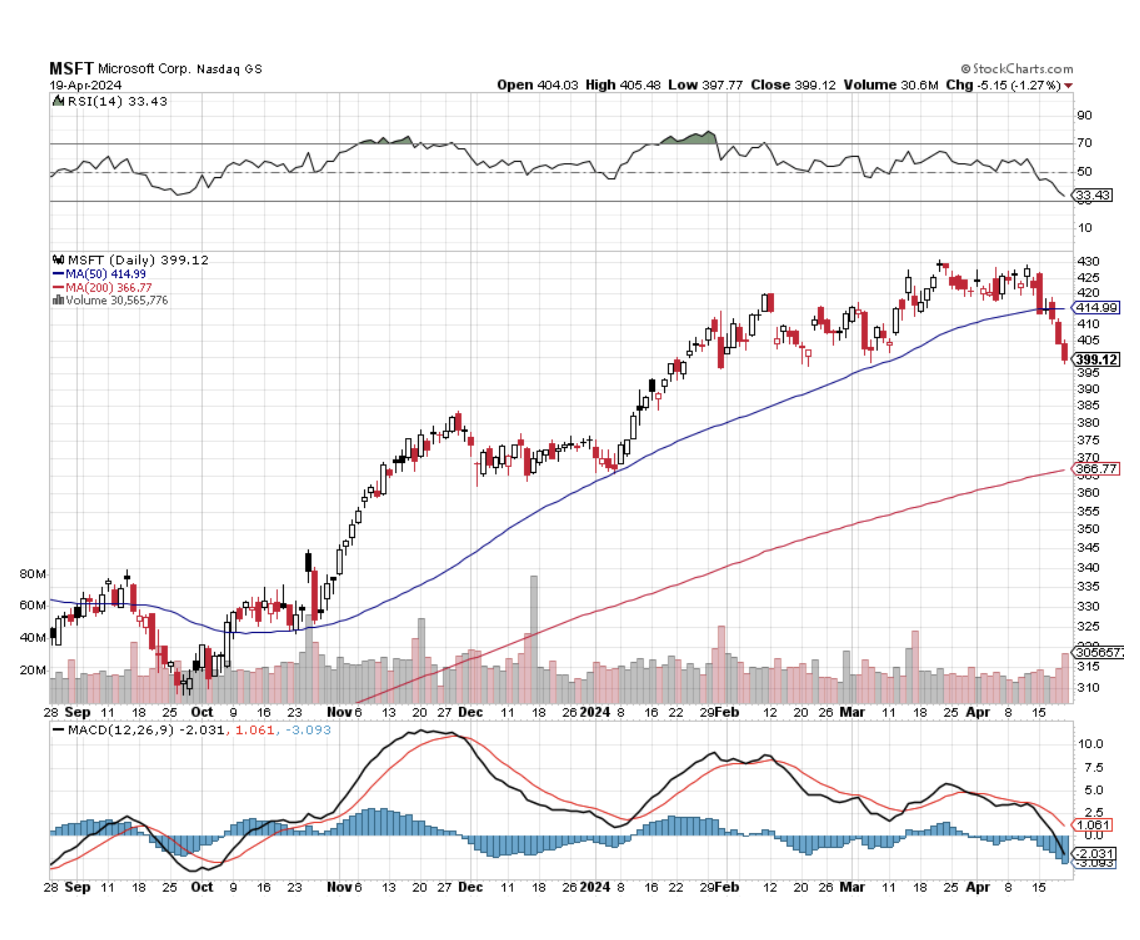

With the advantage of 20/20 hindsight, I should have been paying more attention to the Magnificent Seven 50-day moving averages which have been falling like dominoes. First went Tesla (TSLA) in February and Apple in March. The S&P 500 (SPY) gave it up on Monday and Microsoft (MSFT) on Wednesday. Amazon (AMZN), (META), and (NVDA) were the last to go on Friday.

Sure you can blame the April 19 option expiration when traders were loaded to the hilt with expiring longs with all these stocks they had to dump. The dreaded month of May, when traders go to die, and the summer doldrums are just two weeks away. Algorithms poured gasoline on the fire exaggerating the moves, as they always do. But still, wrong is wrong.

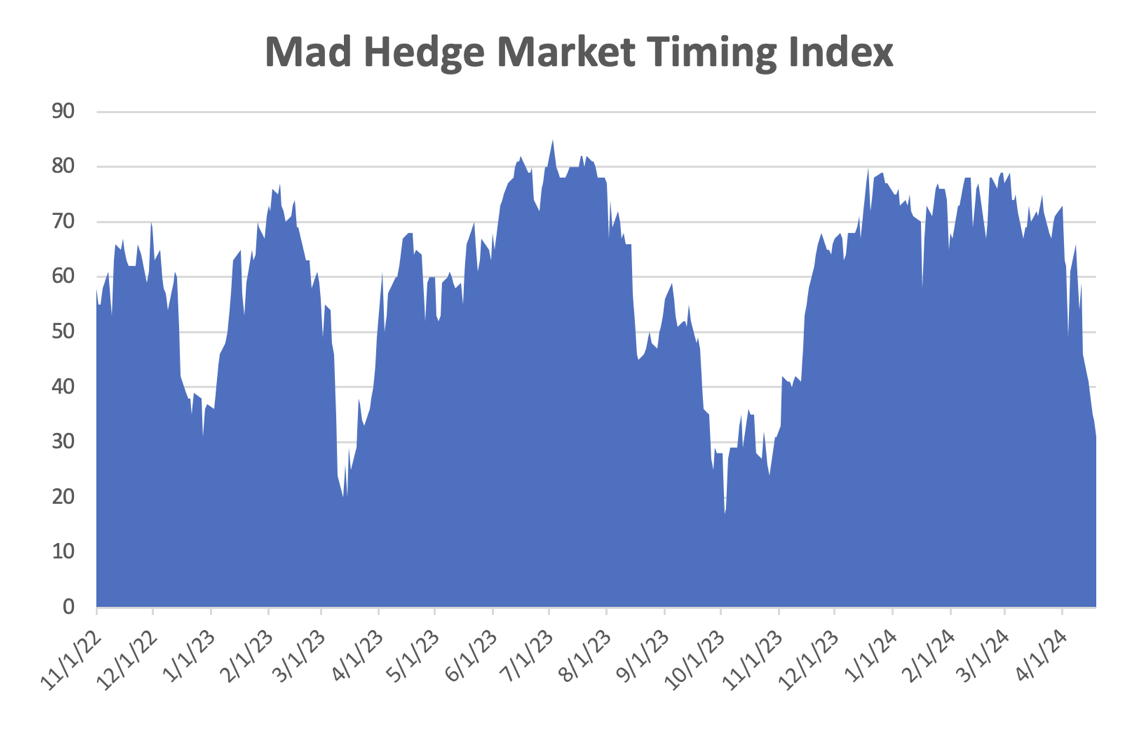

And there’s my mea culpa for 2024. I am human after all. I’m not right all the time, I just act like it. If the horrific market action last week has one silver lining, it’s that it sets up the next great trades, for which there will be many. With my Mad Hedge AI Market Timing Index down to a lowly 31 that may not be far off.

Your next question is “How far down is down?” In the worst-case scenario, the 200-day moving average is in play for all of these. That is pegged at $463 for the S&P 500, $569 for (NVDA), $377 for (MSFT), $150 for (AMZN), and $308 for (META). (AAPL) and (TSLA) already lost their 200-days a long time ago. In other words, the market is in the process of giving up all its 2024 gains and then some.

Sure, the 200 days are all rising sharply so it's unlikely we’ll hit these dire numbers. Still, it's best to prepare your boss for the worst and then let serendipity work its magic.

Remarkably, my commodity and precious metal stocks, where I had eight of ten long positions, stuck to the script and moved sideways instead of down. If you throw bad news on a stock and it refuses to fall, you buy the hell out of it. So that will be my next move in the market, once I clean all the mud off my face and pull the arrows out of my rear.

Those of us who have been trading gold for a long time, I’ve been doing it for 50 years and 60 if you count the Kennedy silver dollars I collected, will tell you that this new bull market in the barbarous relic is a very strange one.

None of the traditional factors that drive gold up are present. Interest rates have lately been rising, not falling. ETF financial demand fell all last year, and much of that money was diverted to Bitcoin. Retail demand, especially from Asia, has also been falling off a cliff. Gold miners have in no way been leading the price of the yellow metal because of their excess leverage as they usually do. But gold has seen a 34% rally off the October low.

Go figure.

It turns out that central bank buying has increased dramatically, especially from China, enough to offset all the other no-shows. The conflict in the Middle East is also drawing in more flight to safety demand. The good news is that the Chinese buying will continue. The bad news is that this might be a precursor to the invasion of Taiwan as it flees the Western financial system.

What does all this mean? When the traditional demand for gold returns, interest rates, ETFs, and retail, the price of gold will move a lot higher. The barbarous relic can easily reach $2,800 this year and possibly $3,000. The miners will play catch up. Buy (GLD) on dips and silver (SLV) as well, which has a lot of catching up to do.

I just thought you’d like to know.

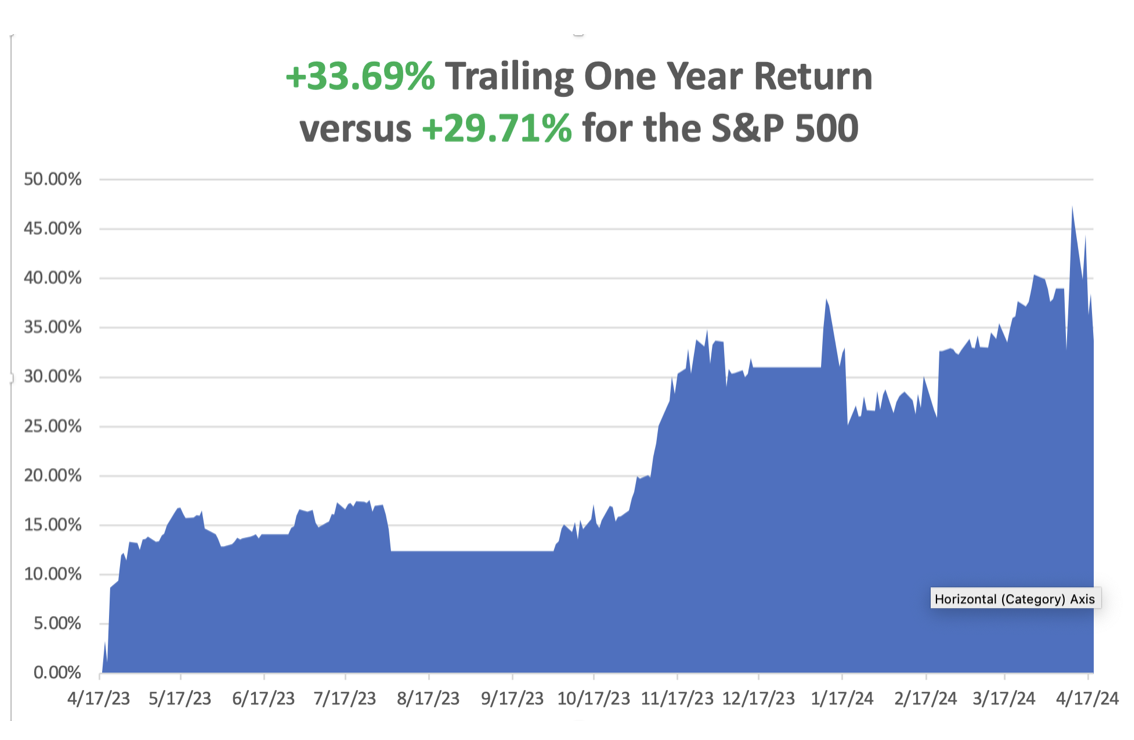

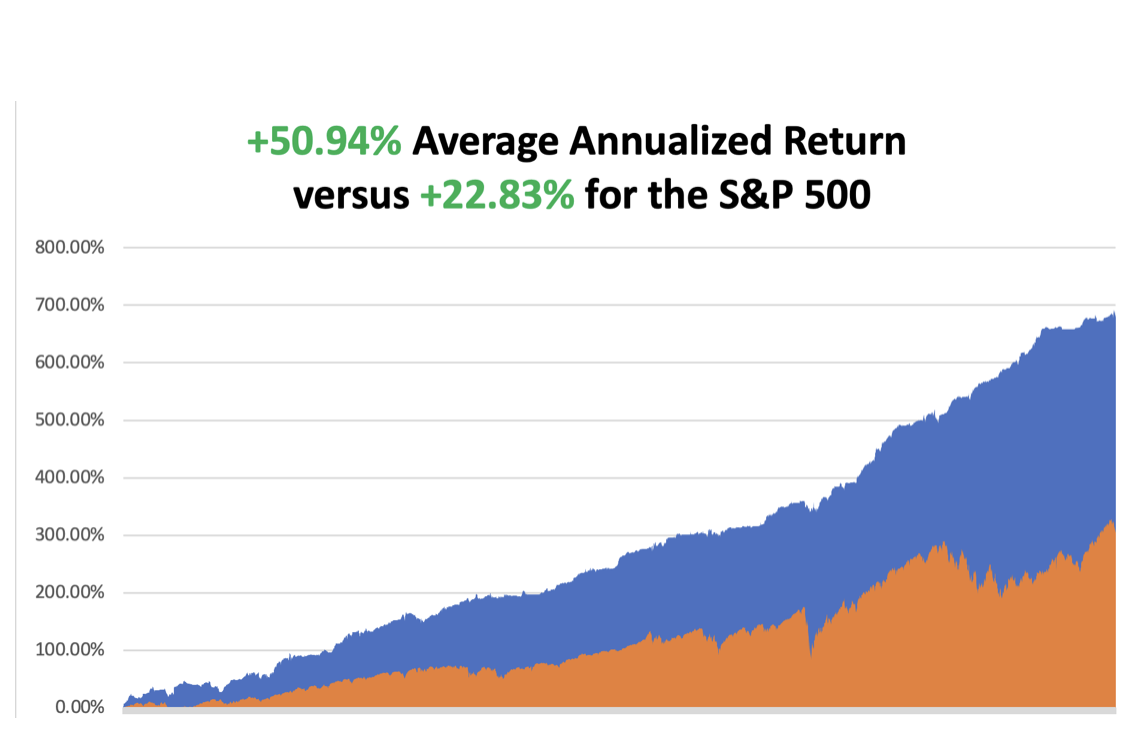

So far in April, we are down a heartbreaking -6.69%. My 2024 year-to-date performance is at +14.47%.The S&P 500 (SPY) is up +2.68%so far in 2024. My trailing one-year return reached +33.69% versus +29.71% for the S&P 500. That brings my 16-year total return to +676.63%.My average annualized return has recovered to +50.94.

Some 63 of my 70 round trips were profitable in 2023. Some 20 of 28 trades have been profitable so far in 2024.

I stopped out of my long in Tesla last week at cost, expecting further downside, which happened. A week early the position had been at max profit. I let my April longs expire at a max profit on April 19 in Freeport McMoRan (FCX), Occidental Petroleum, ExxonMobile (XOM), Wheaton Precious Metals (WPM), and Gold (GLD).

That leaves me with my remaining May longs in (TLT) and (FCX) a double long in (NVDA) and 60% in cash. Volatility Index ($VIX) Hits Six-Month High, on threats of a New Iran War, Oil Supply Cut-offs, and topping stocks. It’s been a long and dry desert crossing, but we are finally back to reach the $20 handle. The volatility trade is back. For a double bonus, the Mad Hedge Market Timing Index also dropped below 50 for the first time since October. Options traders will love it!

Junk Bonds See Biggest Outflows in a Year, as the Federal Reserve’s hawkish approach to inflation makes investors wary, sending yields soaring to 6.33%. Yields won’t peak until the Fed actually cuts rates. Buy (JNK) and (HYG) on dips.

Netflix (NFLX) Adds 9.33 Million New Subscribers, nearly double analyst forecasts, including my five kids who aren’t allowed to share my password anymore. But the shares dropped on weak Q2 guidance. Netflix has rebounded from a slowdown in 2021 and 2022 to grow at its fastest rate since the early days of the coronavirus pandemic. That is due in large part to its crackdown on people who were using someone else’s account. The company estimated more than 100 million people were using an account for which they didn’t pay.

Mortgage Rates Top 7.0% for the first time in 2024, adding dead weight to the housing market. Most borrowers are now taking out adjustable 5/1 ARMS and then praying for a Fed rate cut later this year.

Existing Home Sales Dive by 4.3% in March to 4.19 million units on a sign-contract basis. Inventories rose 4.47% to a 3.2-month supply, up 14% YOY. The median price of an existing home sold in March was $393,500, up 4.8% from the year before. Regionally, sales fell everywhere except in the North, where they rose 4.2% month-to-month. Sales fell hardest in the West, down 8.2%. Prices are highest in the West. Housing Starts Plunge, down 14.5% in March. Permits for future construction of single-family houses fell to a five-month low. Residential investment rebounded in the second half of 2023 after contracting for nine straight quarters, the longest such stretch since the housing market collapse in 2006. But the recovery appears to be losing steam. China Surprises with Q1 GDP Growth at 5.3%, but who knows how real these numbers really are? They don’t line up with individual data like international trade. Peak China is behind us. Avoid (FXI).

Tariff Wars Heat Up, US President Joe Biden is threatening China again, and this time he wants to triple the China tariff rate on steel and aluminum imports. On Wednesday, the president will visit the United Steelworkers headquarters in Pittsburgh and has vowed his saber-rattling is not just empty threats. His rhetoric on China could make relations between the US and the Middle Kingdom that much frostier as we enter into the heart of the US election race.

Biden Boosts the Cost of Alaska Oil Drilling Leases, from $10,000 to $160,000, the first increase since 1920. There is also a bump in the royalty on extracted oil, from 12.25% to 16.27%. The government is no longer giving away oil found on its land for free. Coddling of the oil companies is over. Oil companies will no longer bid for cheap oil leases with the intention of sitting on them for decades. The US is currently the largest oil (USO) producing country in history at 13 million barrels/day and hardly needs any subsidies, which date back to the Great Depression. Buy energy stocks on dips, like (XOM) and (OXY), which are posting record profits.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 22, at 7:00 AM EST, the Chicago Fed National Activity Index is announced.

On Tuesday, April 23 at 8:30 AM, New Home Sales are released.

On Wednesday, April 24 at 2:00 PM, Mortgage applications come out.

On Thursday, April 25 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, April 26 at 8:30 AM, Consumer Expectations. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I spent a decade flying planes without a license in various remote war zones because nobody cared.

So, when I finally obtained my British Private Pilot’s License at the Elstree Aerodrome, home of the WWII Mosquito twin-engine bomber, in 1987, it was cause for celebration.

I decided to take on a great challenge to test my newly acquired skills. So, I looked at an aviation chart of Europe, researched the availability of 100LL aviation gasoline in Southern Europe, and concluded that the farthest I could go was the island nation of Malta.

Caution: new pilots with only 50 hours of flying time are the most dangerous people in the world!

Malta looms large in the history of aviation. At the onset of the Second World War, Malta was the only place that could interfere with the resupply of Rommel’s Africa Corps, situated halfway between Sicily and Tunisia. It was also crucial for the British defense of the Suez Canal.

So, Malta was mercilessly bombed, at first by Mussolini’s Regia Aeronautica, and later by the Luftwaffe. By April 1942, the port at Valletta became the single most bombed place on earth.

Initially, Malta had only three obsolete 1934 Gloster Gladiator biplanes to mount a defense, still in their original packing crates. Flown by volunteer pilots, they came to be known as “Faith, Hope, and Charity.”

The three planes held the Italians at bay, shooting down the slower bombers in droves. As my Italian grandmother constantly reminded me, “Italians are better lovers than fighters.” By the time the Germans showed up, the RAF had been able to resupply Malta with as many as 50 infinitely more powerful Spitfires a month, and the battle was won.

So Malta it was.

The flight school only had one plane they could lend me for ten days, a clapped-out, underpowered single-engine Grumman Tiger, which offered a cruising speed of only 160 miles per hour. I paid extra for an inflatable life raft.

Flying over the length of France in good weather at 500 feet was a piece of cake, taking in endless views of castles, vineyards, and bright yellow rapeseed fields. Italy was a little trickier because only four airports offered avgas, Milan, Rome, Naples, and Palermo. Since Italy had lost the war, they never experienced a postwar aviation boom as we did.

I figured that if I filled up in Naples, I could make it all the way to Malta nonstop, a distance of 450 miles, and still have a modest reserve.

Flying the entire length of Italy at 500 feet along the east coast was grand. Genoa, Cinque Terra, the Vatican, and Mount Vesuvius gently passed by. There was a 1,000-foot-high cable connecting Sicily with the mainland that could have been a problem, as it wasn’t marked on the charts. But my US Air Force charts were pretty old, printed just after WWII. But I spotted them in time and flew over.

When I passed Cape Passero, the southeast corner of Sicily, I should have been able to see Malta, but I didn’t. I flew on, figuring a heading of 190 degrees would eventually get me there.

It didn’t.

My fuel was showing only a quarter tank left and my concern was rising. There was now no avgas anywhere within range. I tried triangulating VORs (very high-frequency omnidirectional radar ranging).

No luck.

I tried dead reckoning. No luck there either.

Then I remembered my WWII history. I recalled that returning American bombers with their instruments shot out used to tune in to the BBC AM frequency to find their way back to London. Picking up the Andrews Sisters was confirmation they had the right frequency.

It just so happened that buried in my pilot’s case was a handbook of all European broadcast frequencies. I looked up Malta, and sure enough, there was a high-powered BBC repeater station broadcasting on AM.

I excitedly tuned in to my Automatic Direction Finder.

Nothing. And now my fuel was down to one-eighth tanks and it was getting dark!

In an act of desperation, I kept playing with the ADF dial and eventually picked up a faint signal.

As I got closer, the signal got louder, and I recognized that old familiar clipped English accent. It was the BBC (I did work there for ten years as their Tokyo correspondent).

But the only thing I could see were the shadows of clouds on the Mediterranean below. Eventually, I noticed that one of the shadows wasn’t moving.

It was Malta.

As I was flying at 10,000 feet to extend my range, I cut my engines to conserve fuel and coasted the rest of the way. I landed right as the sun set over Africa.

While on the island, I set myself up in the historic Excelsior Grand Hotel. Malta is bone dry and has almost no beaches. It is surrounded by 100-foot cliffs. I paid homage to Faith, the last of the three historic biplanes, in the National War Museum in Valetta.

The other thing I remember about Malta is that CIA agents were everywhere. Muammar Khadafy’s Libya was a major investor in Malta, recycling their oil riches, and by the late 1980s owned practically everything. How do you spot a CIA agent? Crewcut and pressed, creased blue jeans. It’s like a uniform. What they were doing in Malta I can only imagine.

Before heading back to London, I had to refuel the plane. A truck from air services drove up and dropped a 50-gallon drum of avgas on the tarmac along with a pump. Then they drove off. It took me an hour to hand pump the plane full.

My route home took me directly to Palermo, Sicily to visit my ancestral origins. On takeoff to Sardinia, wind shear flipped my plane over, caused me to crash, and I lost a disk in my back.

But that is a story for another day.

Who says history doesn’t pay!

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Faith”

The Andrews Sisters

Spitfire

Grumman Tiger

https://www.madhedgefundtrader.com/wp-content/uploads/2024/04/andrews-sisters.png582506april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-22 09:02:302024-04-22 12:00:50The Market Outlook for the Week Ahead, or Facing Harsh Reality

For certain segments of the technology sector, it sure does feel like they are fully saturated.

I am not referring to AI, because that is in the early innings of a seismic movement.

However, let’s take a look at streaming.

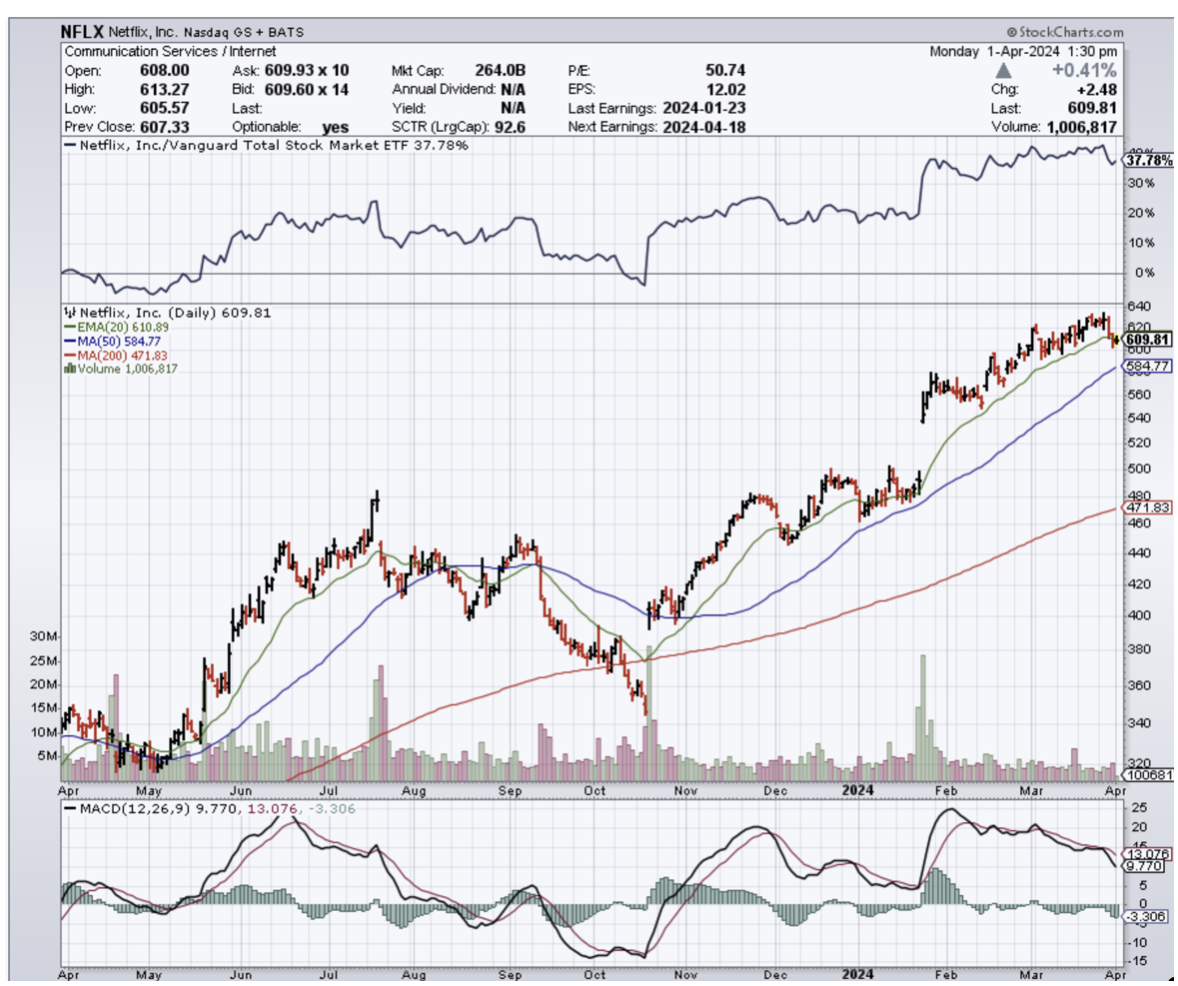

This category was invented by Netflix (NFLX) and now the whole country pays for streaming.

Netflix had the first-mover advantage and took the initiative.

For the leftovers, the pain and struggle with creating a profitable streaming business is real.

Is the year 2024 the year when streaming management has that Aha moment?

Many have instructed us to stay on board the ship while losses bleed uncontrollably.

Everyone is fighting to be one of the three or four streaming services people can’t live without.

Paramount Global (PARA) is under pressure to abandon its namesake streaming service, and Warner Bros. Discovery (WBD) is desperate for partners that offer Max a better chance to compete with the likes of Netflix.

Let’s look at Disney right now.

Streaming grew quickly from launch in 2019 — we’re talking now about Disney+, ESPN+, and Hulu — but even with strong sales, they are sitting on big losses.

Disney board member Nelson Peltz is unhappy, as outlined in a 133-page manifesto published March 4, that Disney “belatedly” entered the streaming game and has a “poorly planned" strategy to catch up with the likes of Netflix.

He takes issue with Disney trying to achieve scale in streaming by buying Fox’s entertainment assets for $71 billion in 2019 because he thinks it exposed the company more to the dying linear TV business.

He also can’t believe that a company reporting more than $22 billion of run-rate streaming revenue annually is still losing money.

Peltz wants a digital strategy for the ESPN sports assets..

Peltz wants a succession plan put in place for current CEO Bob Iger, who extended his contract with Disney last year after a coming-out-of-retirement return to the company in 2022.

In February, Disney teamed up with Fox and Warner Bros. Discovery to create a streaming service for college and pro sports that you can currently only find on TV.

That seems like what Peltz was asking for. Disney also invested $1.5 billion in Epic Games and gave access to the Fortnite maker for gaming portrayals of Star Wars, Marvel, and Avatar.

The bottom line here is that streaming is not nearly as profitable as many insiders first thought.

Streamers thought they could scale up and acquire subscribers at a loss and then raise prices.

That business model was only for Netflix to accomplish because they started so much earlier than anyone else.

The best of the rest are now saddled with loss-making companies and the cost of content post-covid has never been pricier.

Netflix shares have had a nice run in the last 365 days going from $180 per share to over $600 per share.

A lot of that price movement was an acknowledgement that they are dominating streaming compared to the other legacy corporations that have tried their hand in this game.

Instead of jumping into the legacy TV players turned streamers, I would tell readers to wait for Netflix on the dip.

It’s been tried and tested over time and any big dip should and will be bought by investors.

There is not a lot of room for stocks other than Netflix in a sub-sector of rather scarce any AI.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-01 14:02:472024-04-01 16:32:49The Streaming Wars Wind Down

Below please find subscribers’ Q&A for the February 7 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Have you ever flown an ME-262?

A: There's only nine of the original German jet fighters left from WWII in museums. One hangs from the ceiling in the Deutsches Museum in Munich (click here for the link), I have been there and seen it and it is truly a thing of beauty. You would have to be out of your mind to fly that plane, because the engines only had a 10 hour life. That's because during WWII, the Germans couldn't get titanium to make jet engine blades and used steel instead, and those fell apart almost as soon as they took off. So, of the 1,443 ME-262’s made there’s only nine left. The Allies were so terrified of this plane, which could outfly our own Mustangs by 100 miles per hour, that they burned every one they found. That’s also why there are no Japanese Zeros.

Q: Thoughts on Palantir (PLTR) long term?

A: I love it, it’s a great data and security play. Right now, markets are revaluing all data plays, whatever they are. But it is also overvalued having almost doubled in a week.

Q: What do you make of all these layoffs in Silicon Valley? What does this mean for tech stocks?

A: It means tech stocks go up. The tech stocks for a long time have practiced over-employment. They were growing so fast, they always kept a reserve of about 10% of extra staff so they could be put them to work immediately when the demand came. Now they are switching to a new business model: fire everybody unless you absolutely have to have them right now, and make everybody you have work twice as hard. That greatly increases the profitability of these companies, as we saw with META (META), which had its profits triple—and that seems to be the new Silicon Valley business model. If you're one of the few 100,000 that have been laid off in Silicon Valley, eventually the economy will grow back to where they can absorb you. That's how it's going to play out. In the meantime, go take a vacation somewhere, because you're not going to get any vacations once you get a new job.

Q: I have had shares of Alibaba (BABA) since 2020 and the stock has been in free fall since. Should I take the 80% loss or hold?

A: Well, number one, you need to learn about risk control. Number two, you need to learn about stop losses. I stop out when things go 10% against me; that's a good level. At 80%, you might as well keep the stock. You've already taken the loss and who knows, China may recover someday. It's not recovering now because no foreigners want to invest in China with all the political risk and invasion risk of Taiwan. After all, look at what happened to Russia when they invaded Ukraine—that didn't work out so well for them.

Q: On the Chinese economy (FXI), is the poorer performance due to the decision to move to a war economy? The move in the economic front was described in Xi's speech to the CCP in January of 2023.

A: The real reason, which no one is talking about except me, is the one child policy, which China practiced for 40 years. What it has meant is you now have 40 years of missing consumers that were never born. And there is no solution to that, at least no short-term solution. They're trying to get Chinese people to have more kids now, and you're seeing three and four child families for the first time in 40 years in China. But there is no short-term fix. When you mess with demographics, you mess with economic growth. We warned the Chinese this would happen at the time, and they ignored us. They said if they hadn't done the one child policy, the population of China today would be 1.8 billion instead of 1.2 billion. Well, they’re kind of damned no matter what they do so there was no good solution for them. Of course, threatening to invade your neighbors is never good for attracting foreign investment for sure. Nobody here wants to touch China with a 10-foot pole until there’s a new leader who is more pacifist.

Q: What do you think of Eli Lilly (LLY)?

A: I absolutely love it. If there's a never-ending bull market in fat Americans, which is will go on forever, they're one of two companies that have the cure at $1,000 a month. On the other hand, the stock has tripled in the last 18 months, so it’s kind of late in the game to get in.

Q: Are there any stocks that become an attractive short in the event of a Taiwan invasion, such as Taiwan Semiconductor (TSM)?

A: All stocks become attractive shorts in the event of another war in China. You don't want to be anywhere near stocks and the semis will have the greatest downside beta as they always do. You don't want to be anywhere near bonds either, because the Chinese still own about a trillion dollars’ worth of our bonds. Cash and T-bills suddenly looks great in the event of a third war on top of the two that we already have in Gaza and Ukraine.

Q: What do you think about the prospects of the Japanese stock market now?

A: I think the big move is done; it finally hit a new high after a 34-year wait. The next big move in Japan is when the Yen gets stronger, and that is bad for Japanese stocks, so I would be a little cautious here unless you have some great single name plays like Warren Buffett does with Mitsubishi Corp. (MSBHF). So that's my view on Japan—I'm not chasing it after being out for 34 years. Why return? The companies in the US are better anyway.

Q: What is the deal with Supermicro Computer (SMCI)? It went up 23 times in a year to $669 after not clear $30 for a decade.

A: The answer is artificial intelligence. It is basically creating immense demand for the entire chip ecosystem, including high end servers, which Supermicro makes. It also has the benefit of being a small company with a small float, hence the ballistic move. It was too small to show up on my radar. I’ll catch the next one. There are literally thousands of companies like (SMCI) in Silicon Valley.

Q: Will JP Morgan (JPM) bank shares keep rising, or will they fall when the Fed cuts rates?

A: (JPM) will keep rising because recovering economies create more loan demand, allow wider margins, and cause default rates to go down. It becomes a sort of best case scenario for banks, and JP Morgan is the best of the breed in the banking sector. It also benefits the most from the concentration of the US banking sector, which is on its way from 4,000 banks to 6 with help from the US government.

Q: Is India a good long-term play? Which of the two ETFs I recommend are the better ones?

A: Yes, India is a good long-term play. You buy both iShares India 50 (INDY) and the iShares MSCI India (INDA), which I helped create yonks ago. India is the new China, and the old China is going nowhere. So, yes, India definitely is a play, especially if the dollar starts to weaken.

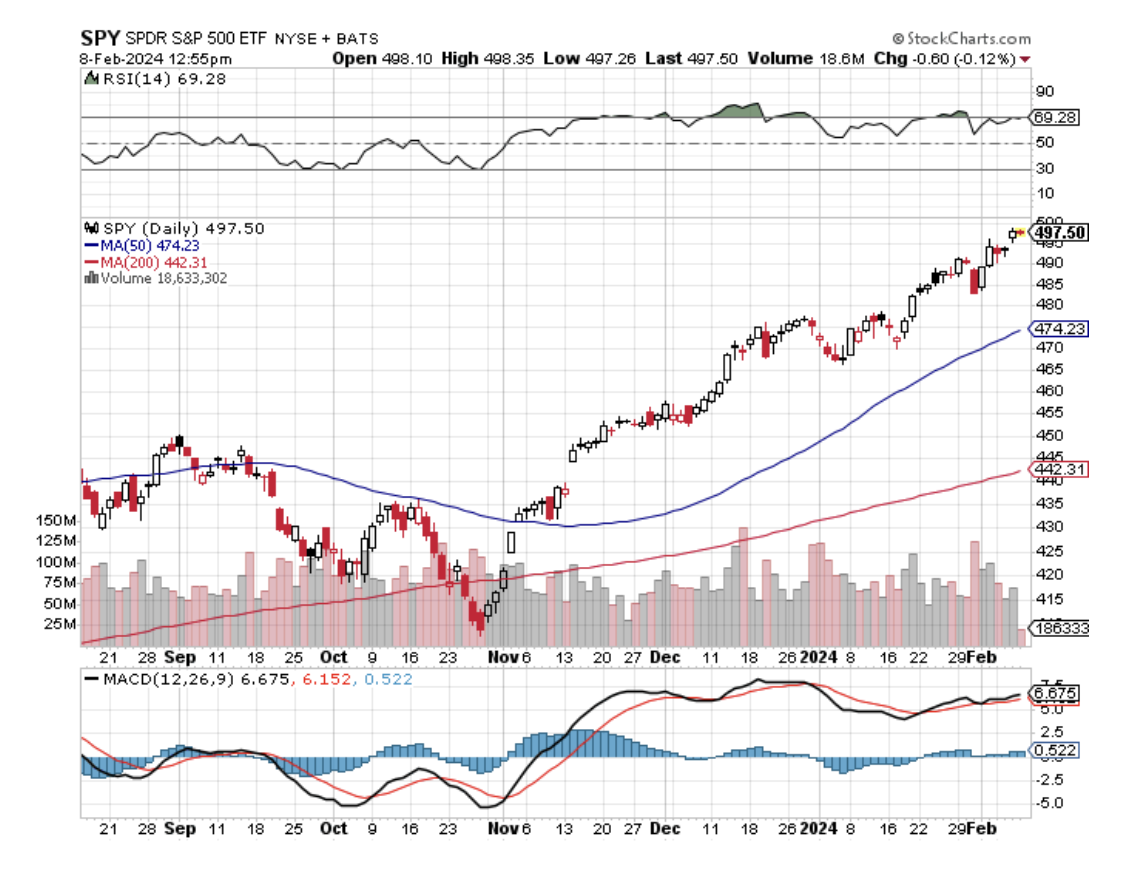

Q: Do you expect to pull back in your market timing index?

A: Yes, probably this month. Have I ever seen it go sideways at the top for an extended period? No, I haven't. On the other hand, we’ve never had a new thing like artificial intelligence hit the market, nor have we seen five stocks dominate the entire market like we're seeing now. So, there are a lot of unprecedented factors in the market now which no one has ever seen before, therefore they don't know what to do. That is the difficulty.

Q: Does India have an in-country built EV, and what is their favorite EV in India?

A: No, but Tesla (TSLA) is talking about building a factory there. And I would have to say BYD Motors (BYDDF) because they have the world’s cheapest EV’s. There is essentially no car regulation in India except on imports. Car regulation and safety requirements is what keeps the BYDs out of the United States, and it's kept them out for the last 15 years. So that is the issue there.

Q: What do you think about META as a dividend play?

A: I think META will go higher, but like the rest of the AI 5, it is desperately in need of a pull back and a refresh to allow new traders to come in.

Q: Why does Netflix (NFLX) keep going up? I thought streaming was saturated—what gives?

A: Netflix won the streaming wars. They have the best content and the best business strategy; and they banned sharing of passwords, which hit my family big time since it seemed like the whole world was using my Netflix password. And no, I'm not going tell you what my password is. I’ve already paid for Griselda enough times. Seems there is a lot of demand for strong women in my family. Netflix they seem to be enjoying a near monopoly now on profits.

Q: Has the NASDAQ come too far too fast, and does it have more to run?

A: Well it does have more to run, but needs a pull back first. I'm thinking we'll get one this month, but I'm definitely not shorting it in the meantime.

Q: Have you ordered your Tesla (TSLA) Cybertruck?

A: I actually ordered it two years ago and it may be another two year wait; with my luck the order will come through when I'm in Europe and I'll miss it. Some of my friends have already gotten deliveries because they ordered on day one. They love it.

Q: What happened to United States Natural Gas (UNG)?

A: A super cold spell hit the Midwest, froze all the pipes, and nobody could deliver natural gas just when the power companies were screaming for more gas. That created the double in the price which you should have sold into! Usually, people don't need to be told to take a profit when something doubles in 2 weeks, but apparently there are some out there as I've been here getting emails from them. Further confusing matters further is that (UNG) did a 4:1 reverse split right at this time. They have to do this every few years or the 35% a year contango takes the price below $1.00 and shares can’t trade below $1.00 on the New York Stock Exchange.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.