(The Mad MARCH traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HIGHER HIGHS)

(NVDA), (META), (IWM), (AMZN), (RIVN), (SNOW), (GLD), (GOLD), (NEM), (FXI), DELL), (AAPL), (TSLA), (CCJ), ($NIKK), (USO), (GOLD)

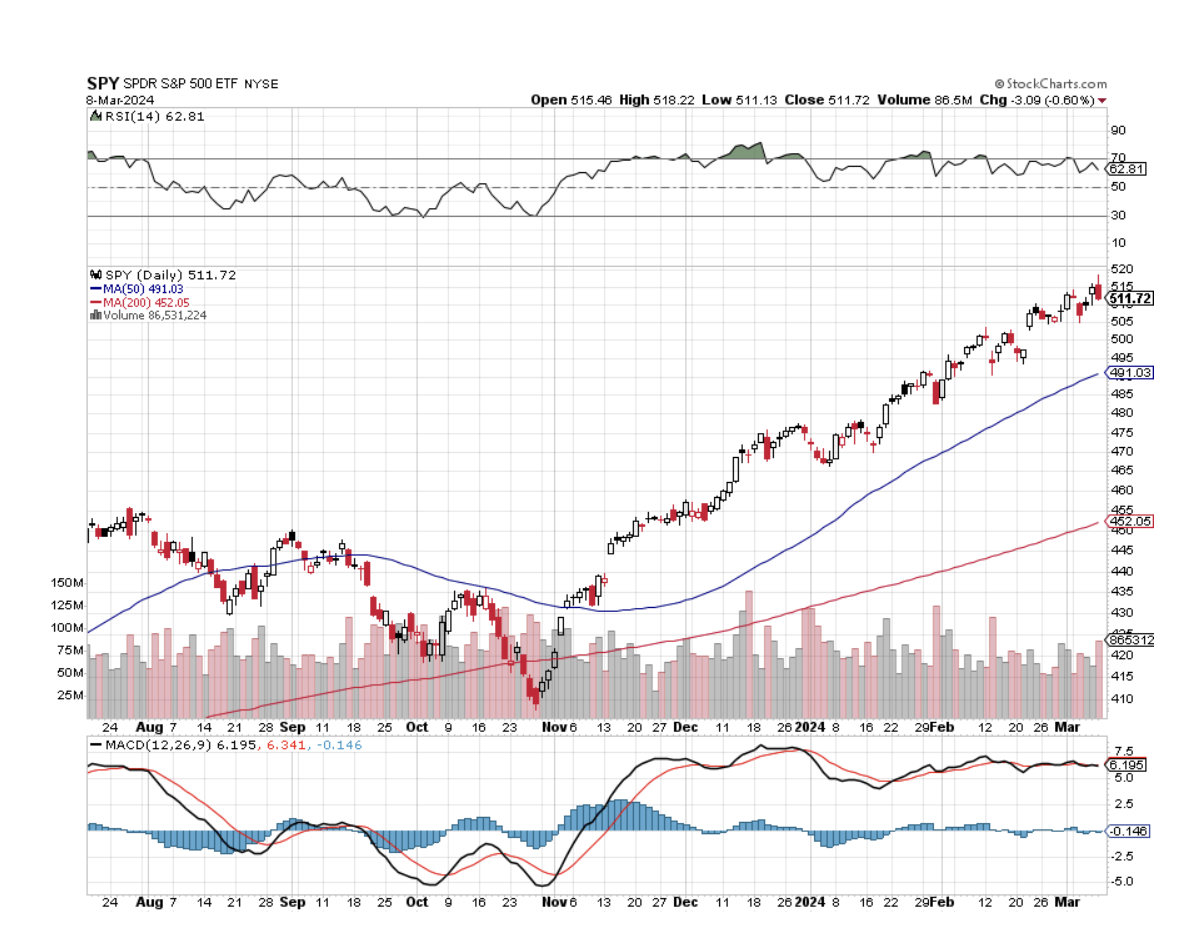

I was all ready to write another hyper-bullish report for the week. That was at least until noon EST on Friday. That’s when NVIDIA (NVDA) Peaked at $955 and then free fell $100 to $855. New all-time and then a new intraday low on huge volume and that is the textbook definition of a market top.

Not that we should be complaining. At the high, (NVDA) was up an unimaginable 105% so far this year. I spent my week buying back short put options for 50 cents that I initially sold for $20. With a quarterly quadruple witching due this Friday, anything can happen.

By the end of February, more than half of all analyst 2024 yearend targets were met. The response was a rush to raise yearend targets, triggering the current melt-up.

It always ends in tears.

And I’m about to tell you something that you will absolutely love to hear. Lower interest rates dramatically increase corporate stock buybacks, already set at $1.25 trillion for 2024. That’s because of the lower cost of capital.

What do more share buybacks automatically bring? High stock prices, especially for large positive cash flow companies like big tech.

As much as the permabears hate to admit it, good news really is good news.

With all of the media obsession with NVIDIA (NVDA), my largest holding, and Meta (META), the fact is that the rally is broadening out. More than half of all industrial stocks are trading at all-time highs. Long-forgotten small caps (IWM) are also approaching 2021 all-time highs.

Going into this week managers were either overweight big tech and extremely nervous or out of big tech and kicking themselves. The urge to rotate is strong. But your standby rotation sectors, industrials, biotech, and banking have also seen big moves.

Which brings us to the subject of gold (GLD).

After a tedious one-year sideways consolidation, the barbarous relic blasted out to the upside above $2,200 an ounce, a new all-time high. After soaking up as much gold as they could over the past decade, China and Russia have finally taken the gold market net short, which is why we saw such dramatic price action.

With interest rates in the US soon to fall, the opportunity cost of owning non-yielding gold is about to shrink. That will cut the knees out from under the US dollar prompting a stampede into precious metals and Bitcoin.

Except this time, it’s different.

Gold miners usually outperform the yellow metal by four to one to the upside. Not so this time. Barrick Gold (GOLD) and Newmont Mining (NEM) were barely able to keep pace with the barbarous relic. That’s because inflation has boosted their costs and cut profit margins. After all, they are stock first and gold plays second.

Still, if gold reaches my $3,000 target in 2025 the LEAPS I sent out for (GOLD) last June should easily hit its maximum profit point of 298%.

That other weak dollar play, oil (USO) may not deliver the joys of past cycles and may in fact be trapped in a fairly narrow $60-$80 range. The futures markets are saying that the price of Texas tea will be lower in a year.

The US is now the world’s top oil producer at 13 million barrels/day and that is rising (thanks to enormously generous tax breaks), capping prices. Non-OPEC+ production is increasing, especially from Brazil and Canada. China, the world’s largest oil importer is missing in action. But low inventories, especially at the American Strategic Petroleum Reserve, are preventing a crash as well. Shale production is growing.

Still, even a $20 rally can have a dramatic impact on the share prices of the big US producers, like Exxon (XOM) and Occidental Petroleum (OXY), some 25% of which is now owned by Warren Buffet. Even without some sexy price action, this sector pays some of the highest dividend yields in the markets.

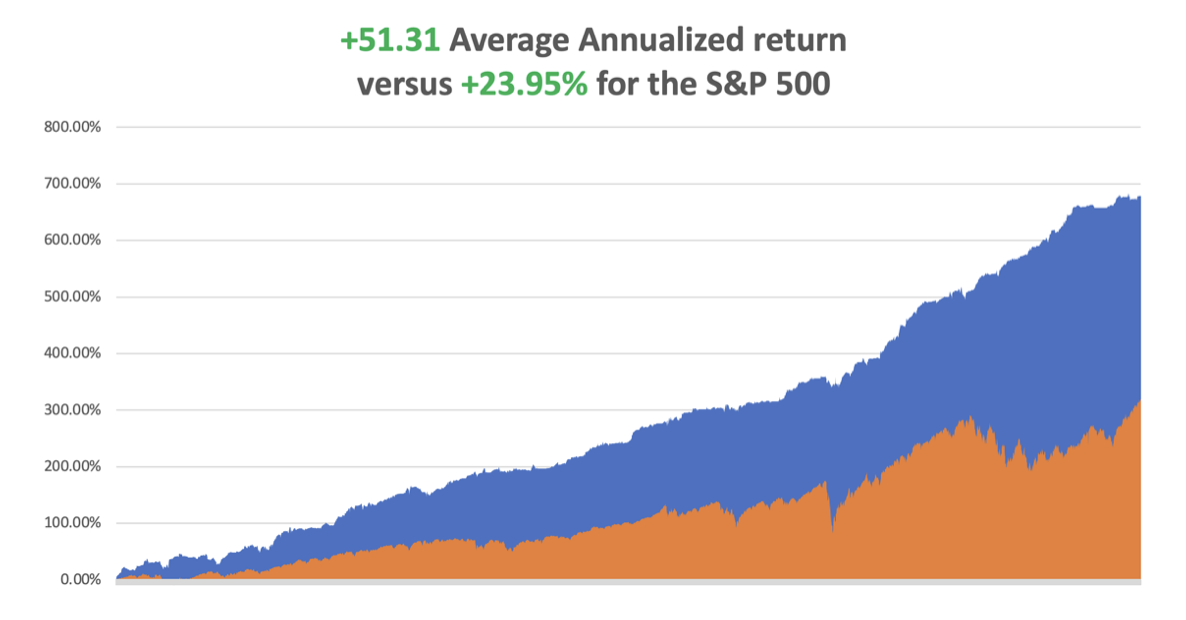

In February we closed up +7.42%. So far in March, we are up +0.70%. My 2024 year-to-date performance is at +3.21%. The S&P 500 (SPY) is up +7.11% so far in 2024. My trailing one-year return reached +54.28% versus +40.94% for the S&P 500.

That brings my 16-year total return to +689.74%. My average annualized return has recovered to +52.05%.

Some 63 of my 70 trades last year were profitable in 2023. Some 11 of 15 trades have been profitable so far in 2024.

I used the ballistic move in (NVDA) to take profits in my double long there. I am maintaining longs in (AMZN) and Snowflake (SNOW). I am both long and short the bond market (TLT) and I am 60% in cash given the elevated level of the stock markets.

Nonfarm Payroll Report Rose 275,000 in February. The Headline Unemployment Rate rose to 3.9%, a two-year high. The report illustrates a labor market that is gradually downshifting, with more moderate job and pay gains that suggest the economy will keep expanding without much risk of a reacceleration in inflation. These are very Fed friendly numbers.

JOLTS Job Openings Report Rises by 140,000 to 8,890,000, less than expected. Leisure and hospitality led with 41,000 new jobs, construction added 28,000 and trade, transportation and utilities contributed 24,000. Growth was concentrated among larger companies, as establishments with fewer than 50 employees contributed just 13,000 to the total.

Rivian Shares Soar, on news it is halting plans to build a new $2.25 billion factory in Georgia, an abrupt reversal aimed at cutting costs while the company prepares to launch a cheaper electric vehicle. Shifting planned production of the forthcoming R2 model to an existing facility in Illinois will allow Rivian to begin deliveries in the first half of 2026, earlier than expected. Buy (RIVN) on dips.

New York Community Bancorp Bailed Out, with a cash infusion led by former Treasury secretary Steve Mnuchin. The shares soared from $2 to $3.41. That takes the heat off the sector….until the next one. The US is shrinking from 4236 banks to only six banks. Who says politics doesn’t pay?

Europe Moves Towards Interest Rate Cuts, igniting a global bond market rally. Staff projections now see economic growth of 0.6% in 2024, from a previous forecast of 0.8%. They presented a more positive picture of inflation, with the forecast for the year brought to an average 2.3% from 2.7%. Market bets increased on rate cuts taking place as early as June, with the euro trading 0.35% lower against the British pound following the news.

Beige Book Comes in Moderate, saying "labor market tightness eased further," in February but noted "difficulties persisted attracting workers for highly skilled positions." The Beige Book is a review of economic conditions across all 12 Fed districts. Fed Chair Jerome Powell told Congress on Wednesday that the U.S central bank expected "inflation to come down, the economy to keep growing," but shied away from committing to any timetable for interest rate cuts.

China Targets 5% Growth for 2024, but nobody buys it for a second. A covid hangover, residential real estate crisis triggering a financial crisis, and constant invasion threats over Taiwan, make this target a pipe dream. Avoid (FXI) and all Middle Kingdom plays.

Gold Hits New All-Time High, at $2,141 an ounce on expectations of imminent rate cuts by the Fed. Gold, often used as a safe store of value during times of political and financial uncertainty, has climbed over $300 dollars since the start of the Israel-Hamas war. Buy (GLD), (GOLD), and (NEM) on dips.

Dell (DELL) Becomes an AI Stock, sending the shares up 47% in a Day. That’s been changing over the past year, as Dell has been reporting strong orders of servers designed to power generative AI workloads—many of which use chips supplied by AI kingmaker Nvidia. The company’s fourth quarter results convinced any doubters. Can Apple (AAPL) do the same?

Tesla Plunges on Poor China Sales, down $14.50 on sales data dimmed the outlook for Tesla's global deliveries, at a time when the top EV maker is battling a decline in demand and is weighed down by a lack of entry-level vehicles and the age of its product line-up. Not the time to be in EVs or solar. Buy (TSLA) on bigger dip.

US National Debt is Rising by $1 Trillion Every 100 Days. A trillion here, a trillion there, sooner or later that adds up to a lot of money. Eventually, someone is going to have to do something about this. The US national debt stands at $34.5 trillion, or $104,545 per person.

The Uranium Shortage is Getting Extreme, with yellow cake up 112% in a year. Owners of left-for-dead uranium mines are restarting operations to capitalize on rising demand for the nuclear fuel. Most of those American mines were idled in the aftermath of Fukushima when uranium prices crashed and countries like Germany and Japan initiated plans to phase out nuclear reactors. Now, with governments turning to nuclear power to meet emissions targets and top uranium producers struggling to satisfy demand, prices of the silvery-white metal are surging. Buy (Cameco (CCJ) on dips.

Japan’s Nikkei ($NIKK) Tops 40,000, a new 34-year high. The ultra-weak Japanese economy is giving the economy there a free lunch, but better hedge your currency exposure. Good thing I missed a dead market for 34 years.

NVIDIA Replaces Tesla as Top Traded Stock, with volumes migrating to the options market as well. Blockbuster profits are catnip for traders, while EV price wars aren’t. Tesla is down 52% from its all-time high two years ago and is one of the biggest percentage decliners in the Nasdaq 100 Index this year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 11 at 7:00 AM EST, the Consumer Inflation Expectations are announced.

On Tuesday, March 12 at 8:30 AM, Inflation Rate for February is released.

On Wednesday, March 13 at 2:00 PM, MBA Mortgage Applications are published

On Thursday, March 14 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, March 15 at 2:30 PM, the University of Michigan Consumer Sentiment is published. At 2:00 PM the Baker Hughes Rig Count is printed.

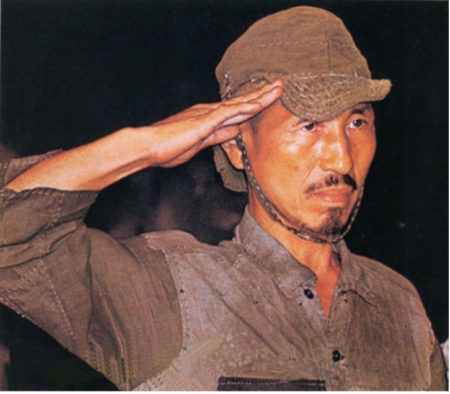

As for me, I have met many interesting people over a half-century of interviews, but it is tough to beat Corporal Hiroshi Onoda of the Japanese Army, the last man to surrender in WWII.

I had heard of Onoda while working as a foreign correspondent in Tokyo. So, I convinced my boss at The Economist magazine in London that it was time to do a special report on the Philippines and interview President Ferdinand Marcos. That accomplished, I headed for Lubang island where Onoda was said to be hiding, taking a launch from the main island of Luzon.

I hiked to the top of the island in the blazing heat, consuming two full army canteens of water (plastic bottles hadn’t been invented yet). No luck. But I had a strange feeling that someone was watching me.

When the Philippines fell in 1945, Onoda’s commanding officer ordered the remaining men to fight on to the last man. Four stayed behind, continuing a 30-year war.

As a massive American military presence and growing international trade raised Philippine standards of living, the locals eventually were able to buy their own guns and kill off Onoda’s companions one by one. By 1972 he was alone, but he kept fighting.

The Japanese government knew about Onoda from the 1950s onward and made every effort to bring him back. They hired search crews, tracking dogs, and even helicopters with loudspeakers, but to no avail. Frustrated, they left a one-year supply of the main Tokyo newspaper and a stockpile of food and returned to Japan. This continued for 20 years.

Onoda read the papers with great interest, believing some parts but distrusting others. His worldview became increasingly bizarre. He learned of the enormous exports of Japanese automobiles to the US, so he concluded that while still at war, the two countries were conducting trade.

But when he came to the classified ads, he found the salaries wildly out of touch with reality. Lowly secretaries were earning an incredible 50,000 yen a year, while a salesman could earn an obscene 200,000 yen.

Before the war, there was one Japanese yen to the US dollar. In the hyperinflation that followed the yen fell to 800, and then only recovered to 360. Onoda took this as proof that all the newspapers were faked by the clueless Americans who had no idea of true Japanese salary levels.

So he kept fighting. By 1974 he had killed 17 Philippino civilians.

After I left Lubang island, a Japanese hippy named Norio Suzuki with long hair, beads, and sandals followed me, also looking for Onoda. Onoda tracked him as he had me but was so shocked by his appearance that he decided not to kill him. The hippy spent two days with Onoda explaining the modern world.

Then Suzuki finally asked the obvious question: what would it take to get Onoda to surrender? Onoda said it was very simple, a direct order from his commanding officer. Suzuki made a beeline straight for the Japanese embassy in Manila and the wheels started turning.

A nationwide search was conducted to find Onoda’s last commanding officer and a doddering 80-year-old was turned up working in an obscure bookstore. Then the government custom-tailored a prewar Imperial Japanese Army uniform and flew him down to the Philippines.

The man gave the order and Onoda handed over his samurai sword and rifle, or at least what was left of it. Rats had eaten most of the wooden parts. You can watch the surrender ceremony by clicking here on YouTube.

When Onoda returned to Japan, he was a sensation. He displayed prewar mannerisms and values like filial piety and emperor worship that had been long forgotten. Emperor Hirohito was still alive.

When I finally interviewed him, Onoda was sympathetic. I had by then been trained in Bushido at karate school and displayed the appropriate level of humility, deference, mannerisms, and reference.

I asked why he didn’t shoot me. He said that after fighting for 30 years he only had a few shells left and wanted to save them for someone more important.

Onoda didn’t last long in the modern Japan, as he could no longer tolerate modern materialism and cold winters. He moved to Brazil to start a school to teach prewar values and survival skills where the weather was similar to that of the Philippines. Onoda died in 2014 at the age of 91. A diet of coconuts and rats had extended his life beyond that of most individuals.

Onoda wasn’t actually the last Japanese to surrender in WWII. I discovered an entire Japanese division in 1975 that had retreated from China into Laos and just blended in with the population. They were prized for their education and hard work and married well.

During the 1990’s a Japanese was discovered in Siberia. He was released locally at the end of the war, got a job, married a Russian woman, and forgot how to speak Japanese. But Onoda was the last to stop fighting.

The Onoda story reminds me of the fact that journalists learn very early in their careers. You can provide all the facts in the world to some people. But if they conflict with their own deeply held beliefs, they won’t buy them for a second.

Hiro Onoda Surrenders

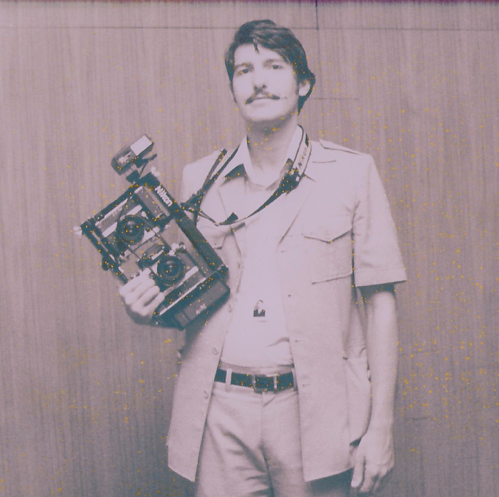

Budding Journalist John Thomas

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-11 09:02:232024-03-11 12:13:02The Market Outlook for the Week Ahead, or Higher Highs

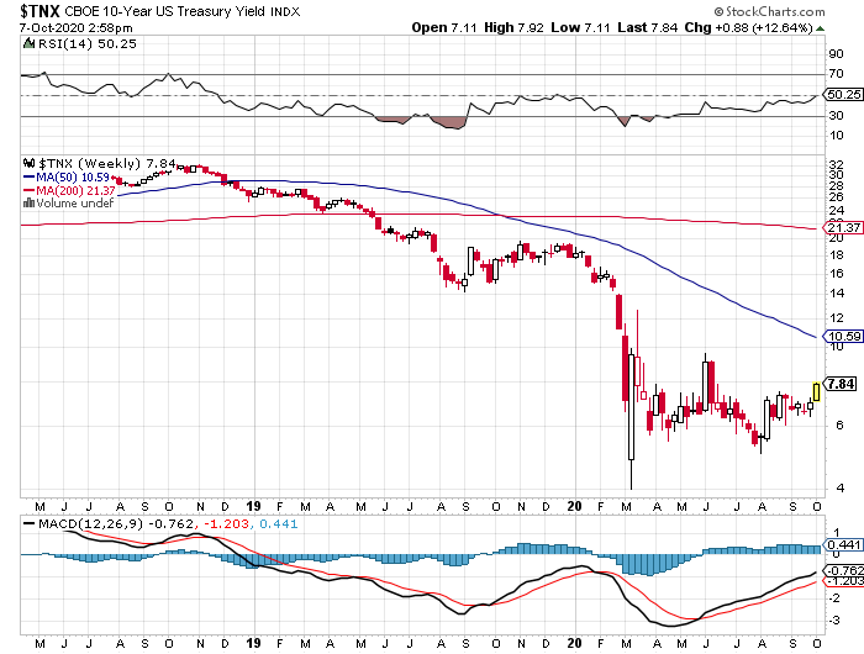

The U.S. Treasury bond market has suddenly ground to a halt, puzzling traders, investors, and hedge fund managers alike.

Today, the yield on the 10-year Treasury bond (TLT), (TBT) traded as low as 0.77%.

This is despite the U.S. economy delivering a horrific negative GDP growth during Q2. Growth is expected to rebound to 2-5% in Q3, depending on if there is another stimulus package from Washington, or not. 2021 could bring economic growth as high as an astronomical 10%.

If I blindfolded any professional money manager, told him the above and asked him where the 10-year Treasury yield should be, most would come in at around the 5% level.

So what gives?

I have put a great deal of thought into this and the answer can be distilled down to two letters: QE.

Global quantitative easing has created about $30 trillion in new money over the past 10 years. It has not been spent, it hasn’t disappeared, nor has it gone to money heaven. It is still around.

The U.S. Federal Reserve, the first to start QE in November 2008 during the Great Recession, ended it in October 2014. From start to finish, it created $4.5 trillion in new money. Over the past five years was wound down to $3.8 trillion by letting debt on its balance sheet mature.

Enter the pandemic. The expectation is that the new round of QE could exceed another $10 trillion or more.

Japan actually began its QE program in 2001, long before anyone else, to deal with the aftermath of the 1990 Japanese stock market crash and a massive demographic headwind (they’re not making Japanese anymore).

Some 20 years later, the Japanese government now owns virtually all of the debt in the country. When you hear about Japan’s prodigious 240% debt to GDP ratio, it’s all nonsense. Net out government holdings and there is no national debt in Japan at all. That’s why the Japanese yen is consistently strong.

After the 2008 crash, the Japanese government expended its QE to include equities as well. As a result, the government is now the largest single buyer of stocks in the Land of the Rising Sun. The Nikkei Average has risen by 234% since the 2009 bottom despite a miserable economic performance, and the yield on 10-year JGBs stand at a lowly 0.03%.

The European Central Bank got into the QE game very late, not until 2015, and its program continues anew, although at half its peak rate. The ECB has just renewed its plan to print a ton of new money.

Part of the problem is that the ECB is running out of bonds to buy, as it already owns most of the paper issued by European entities. That’s why 10-year German bunds are yielding a paltry -0.50%.

As a result, there is excess liquidity everywhere and this has broad implications for your investment or retirement portfolio. It could take as long as a decade before all of this artificial cash is removed from the global financial system.

For a start, bonds may not fall much from here, even if the Fed continues its near-zero interest rate policy for three more years, as promised.

Stocks can’t fall either with this much cash underpinning the market, at least not for a while and not by much. While company share buybacks have virtually disappeared this year, foreign investors have stepped in to pick up the slack.

It also means you can’t have a global contagion leading to a financial crisis. There is ample money available to refinance your way out of any problem when 70% of the world’s debt is still yielding close to zero.

The bottom line here is that global excess liquidity can cover up a multitude of sins. It means the price of everything has to go up, or at least stay level until that liquidity runs out. That includes stocks, bonds, your home, classic cars, and even that rare coin collection of yours gathering dust in a safe deposit box somewhere.

Yes, when the excess free cash runs out in a decade, there will be hell to pay. Until then, make hay while the sun shines.

Hay

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/hay.png387622MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2020-10-08 09:04:122020-10-08 09:38:44If Bonds Can’t Go Down, Stocks Can’t Either

I often see one stock index outperform another, as different segments of the economy speed up, slow down, or go nowhere. Sometimes the reasons for this are fundamental, technical, or completely arbitrary.

Many analysts have been scratching their heads this year over why the S&P 500 has been moving from strength to strength for the past year, while the Dow Average has gone virtually nowhere. Since January, the (SPX) has tacked on a reasonable 7.9%, while the Dow has managed only a paltry 3.4% increase.

What gives?

The problem is particularly vexing for hedge fund managers, who have to choose carefully which index they use to hedge other positions. Do you use the broad based measure of 500 large caps or a much more narrow and stodgy 30?

What?s a poor risk analyst to do?

The Dow Jones Industrial Average was first calculated by founder Charles Dow in 1896, later of Dow Jones & Company, which also publishes the Wall Street Journal. When Dow died in 1902, the firm was taken over by Clarence Barron and stayed within family control for 105 years.

In 2007, on the eve of the financial crisis, it was sold to News Corporation for $5 billion. News Corp. is owned by my former boss, Rupert Murdoch, once an Australian, and now a naturalized US citizen. News then spun off its index business to the CME Corp., formerly the Chicago Mercantile Exchange, in 2010.

Much of the recent divergence can be traced to a reconstitution of the Dow Average on September 20, 2013, when it underwent some major plastic surgery.

It took three near-do-wells out, Bank of America (BAC), Hewlett Packard, (HPQ), and Alcoa (AA). In their place were added three more robust and virile companies, Goldman Sachs (GS), Visa (V), and Nike (NKE).

Call it a nose job, a neck lift, and a tummy tuck all combined into one (Not that I?ve been looking for myself!).

And therein lies the problem. Like many attempts at cosmetic surgery, the procedure rendered the subject uglier than it was before.

Since these changes, the new names have been boring and listless, while the old ones have gone off to the races. Hence, the differing performance.

This is not a new problem. Dow Jones has been terrible at making market calls over its century and a half existence. As a result, these rebalancings have probably subtracted several thousand points over the life of the Dow.

They are, in effect, selling lows and buying highs, much like individual retail investors do. It is almost by definition the perfect anti-performance index. When in doubt, always measure your own performance against the Dow.

Dow Jones takes companies out of its index for many reasons. Some companies go bankrupt, whereas others suffer precipitous declines in prices and trading volumes. (BAC) was removed because, at one point, its shares took a 95% hit from its highs and no longer accurately reflected a relevant weighting of its industry. Citigroup (C) suffered the same fate a few years ago.

Look at the Dow Average of 1900 and you wouldn?t recognize it today. In fact, there is only one firm that has stayed in the index since then, Thomas Edison?s General Electric (GE). Buying a Dow stock is almost a guarantee that it will eventually do poorly.

This is why most hedge funds rely on the (SPX) as a hedging vehicle and how its futures contracts, options and ETF?s, like the (SPY), get the lion?s share of the volume.

Mind you, the (SPX) has its own problems. Apple (AAPL) has far and away the largest weighting there and is also subject to regular rebalancings, wreaking its own havoc.

Because of this, an entire sub industry of hedge fund managers has sprung up over the decades to play this game. Their goal is to buy likely new additions to the index and sell short the outgoing ones.

Get your picks right and you are certain to make money. Every rebalancing generates massive buying and selling in single names by the country?s largest institutional investors, which in reality are just closet indexers, despite the hefty fees they charge you.

Given their gargantuan size these days, there is little else they can do. Rebalancings also give brokerage salesmen talking points on otherwise slow days and generate new and much needed market turnover.

What has made 2014 challenging for so many managers is that so much of the action in the Dow has been concentrated in just a handful of stocks.

Caterpillar (CAT), the happy subject of one of my recent Trade Alerts, accounts for 35.3% of the Index gain this year. Walt Disney (DIS) speaks for 24.2% and Intel (INTC) 23.4%.

Miss these three and you are probably trolling for a new job on Craig?s? List by now, if you?re not already driving a taxi for Uber.

It truly is a stock picker?s market; a market of stocks and not a stock market.

Believe it or not, there are people that are far worse at this game than Dow Jones. The best example I can think of are the folks over at Nihon Keizai Shimbun in Tokyo (or Japan Economic Daily for most of you), who manage the calculation of the 225 stocks in the Nikkei Average (once known as the Nikkei Dow).

In May, 2000, out of the blue, they announced a rebalancing of 50% of the constituent names in their index. Their goal was to make the index more like the American NASDAQ, the flavor of the day. So they dumped a lot of old, traditional industrial names and replaced them with technology highfliers.

Unfortunately, they did this literally weeks after the US Dotcom bubble busted. The move turbocharged the collapse of the Nikkei, probably causing it to fall an extra 8,000 points or more than it should have.

Without such a brilliant move as this, the Nikkei bear market would have bottomed at 15,000 instead of the 7,000 we eventually got. The additional loss of stock collateral and capital probably cost Japan an extra lost decade of economic growth.

So for those of you who bemoan the Dow rebalancings, you should really be giving thanks for small graces.

Rebalancing? Yikes!

Miss This One, And You?re Toast

It Truly is a Stock Picker?s Market

The Key to Your 2014 Performance

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/Mickey-Mouse.jpg352339Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-07-10 01:05:012014-07-10 01:05:01Why is the S&P 500 Beating the Dow?

The big talk in the financial markets this year was of the ?Great Reallocation? out of bonds and into stocks.? The problem is that it was just that: talk. While redemptions of retail bond mutual funds have topped $147 billion since June, the big money has yet to move in size.

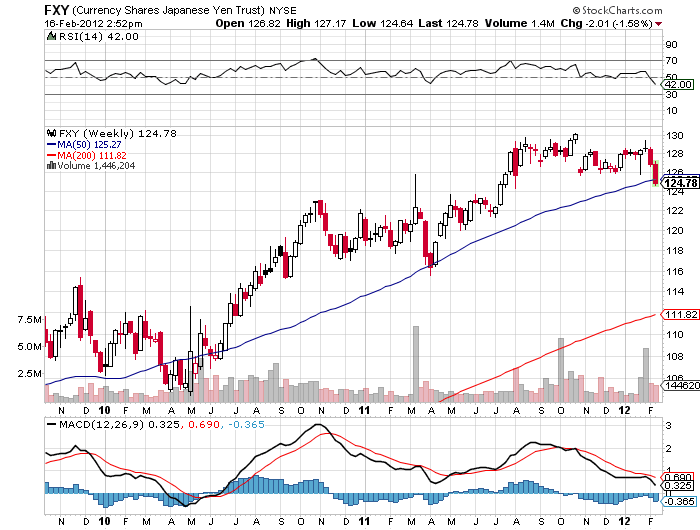

However, there is a great reallocation that is already well under way. In fact, it already completed its first leg earlier this year, and has just begun the second. That is the ?Great Reallocation? out of yen (FXY), (YCS) and into the dollar. It is being executed not only by Japanese institutional investors, but foreign ones as well.

Take a look at the chart below, and you will see that the beleaguered Japanese currency broke to a new four year low this morning. Nothing like a jolt of fresh (FXY) to wake you up first thing in the day, and clear out those cobwebs.

This freefall was on the heels of my doubling up of my yen short positions for my model-trading portfolio with my Trade Alert on Black Friday. The (FXY), now trading at $94.80, is clearly targeting the $90 low set in 2008 for the short term, and after that, the $81 low last seen in 2007.

To understand why this is happening, take a look at this from the point of view of the Japanese money manager, who is running the world?s second largest pool of investable assets, after the US. After a 23-year performance drought, you have just had one of your best years in history.

The Nikkei rocketed by 48%. Better yet, the yen has fallen by 16% against the dollar, which directly translates into an equivalent increase on your foreign investments.

Why not visit the well a second time? Why wait until 2014, when everyone else is going to do the same thing again? In fact, why not drink twice as much this time, as the water is so sweet? What is the conclusion of all of this? Sell more yen, and lots of them. That was what I clearly saw unfolding a month ago. This is why you are making so much money now.

This explains why I have been running big shorts in the yen for almost all of the last two years, doubling up, taking profits, and then doubling up again. I have no doubt that when I total up my numbers for 2014, the yen will pop out as my most profitable trade. Domo Arigato Abe-san!

As for the original ?Great Reallocation? from bonds to stocks, take a look at the chart of Treasury bond futures below lifted from the Gartman Report, reproduced from my friend, Dennis Gartman. Veteran traders will immediately recognize the ?head and shoulders top? that is unfolding in the US Treasury bond market. This is the chart that promises of great things to come in the bond market in 2014?.on the downside.

Look Out Below for the (TLT)

New Lows for the Yen

https://www.madhedgefundtrader.com/wp-content/uploads/2013/11/Woman-Hari-Kari.jpg280396Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-12-03 09:25:062013-12-03 09:25:06That Other ?Great Reallocation? Out of the Yen

The Japanese government is about to introduce Individual Retirement Account for individual investors for the first time. The move is part of prime minister Shinzo Abe?s multifaceted efforts to revive Japan?s economy, and could unleash as much as $690 billion in net buying into Japanese equities by 2018.

The move was inspired American IRA?s, which were first introduced in 1981. After that, the Dow average soared 25 times. It is amazing to what lengths people will go to avoid the taxman.

Starting October 1, individuals will be permitted to contribute up to ?1 million a year into Nippon Individual Savings Accounts (NISA) or some $10,200, while married couples can chip in ?2 million. These funds will be exempt from capital gains and dividend taxes for five years. At the same time, capital gains taxes will rise from 10% to 20%.

Thanks to a 22-year long bear market, only 7.9% of personal assets in Japan are currently invested in stocks, compared to 34% in the US. Individuals account for only 28% of the daily trading volume in Tokyo, while foreigners take up 63%. Still, that?s up from only 21% a year earlier.

Over the past 10 years, individuals sold a net $214 billion in equities, keeping their eyes firmly on the rear view mirror. Almost all of the funds were deposited into bank accounts yielding near zero. Even 10 year Japanese Government Bonds are yielding only 0.68% as of today, the lowest on the planet. That doesn?t buy you much sushi in your retirement.

Over the past year, Japan has enjoyed the world?s fastest growing industrialized economy. The latest data show that it is expanding at a white hot 3.5%, versus a far more modest 2% rate in the US, and only 1% in Europe.

Early indications are that the NISA?s will be hugely popular. Japanese brokers have launched a massive advertising effort to promote the program, which promises to substantially boost their own earnings. Firms have had to lay on extra customer support staff to assist with online applications, where clueless investors have spent two decades in hiding.

To get some idea of the potential, take a look at how Merrill Lynch?s stock performed after 1981, which rose by many multiples. The bear market has lasted for so long that many applicants confess to investing in equities for the first time in their lives.

Since Shinzo Abe announced his candidacy for prime minister and his revolutionary economic and monetary program nearly a year ago, the Japanese stock market (DXJ) has soared by an amazing 80% in US dollar terms. The Japanese yen (FXY), (YCS) has similarly collapsed by a huge 25%.

The need to bolster Japan?s retirement finances is overwhelming. It has the world?s oldest population, with some 26% of their 127.6 million over the age of 65. The average life span in Japan is 82.6 years. That is a lot of people to support for a $6 trillion GDP. Thanks to plummeting fertility rates, the population is expected to decline to 106 million by 2055.

By yanking $690 billion out of the banks and moving out the risk spectrum, Abe?s new IRA?s provide additional means through which the economy can permanently return to health. Higher stock prices will provide cheap equity financing for public companies, which can then reinvest in the domestic economy and create jobs.

I have written endlessly on the fundamental case for a strong Japanese stock market this year (to read my previous articles on yen, please click the following links: ??Rumblings in Tokyo?, ?New BOJ Governor Craters Yen" and "New BOJ Governor Crushes the Yen").

And thank the US congress for behaving like such idiots. Their standoff is providing a decent entry point for a position here.

So How Does This Order App Work?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/09/Girl-Ticker.jpg315494Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-10-01 01:04:282013-10-01 01:04:28Japan to Launch IRA?s

The Bank of Japan renewed its membership in the international quantitative easing club last week, announcing that it was substantially expanding its bond repurchases.

Specifically, it will increase them from ?55 trillion to ?65 trillion, a jump equivalent to $830 billion. To understand how big this is, consider that Japan?s GDP is one third the size of the US. That would be the same as the Federal Reserve announcing a repo program with $2.5 trillion here. Imagine what your asset prices would do if that happened.

For good measure, the Japanese also announced an inflation target of 1%, which is entirely wishful thinking for a country that is entering its 23rd year of deflation. It?s like a man on skid row planning on how to spend his prospective lottery winnings.

The government was prompted to action by the 2011 full year GDP figure, which came in at an appalling -0.9%, compared to a robust growth of 4.5% in 2010. The tsunami reconstruction program has fallen woefully behind schedule due to extreme mismanagement and incompetence by the authorities, despite being more than adequately funded. But after watching the Land of the Rising Sun for the last 20 years, I have come to expect incompetence. Slowdowns in Europe and China, plus the Thai floods and the Fukushima nuclear meltdown have provided additional headwinds.

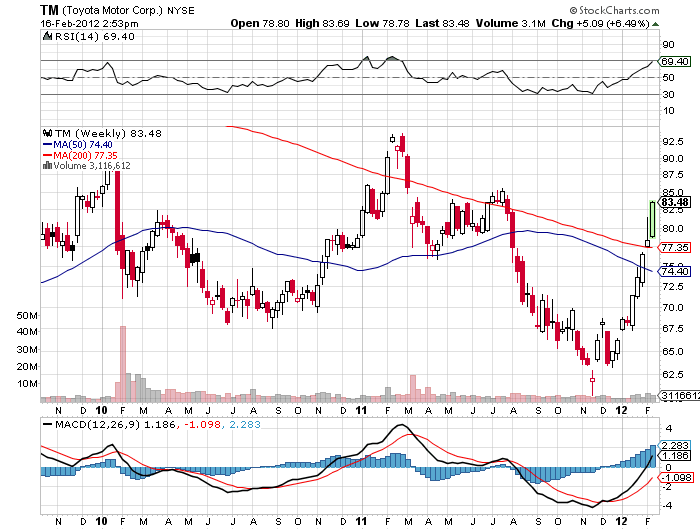

The immediate impact was to trigger a sharp selloff in the yen, delivering an immediate windfall to readers of my Trade Alert Service who were already long yen puts. Traders like myself are always looking for confirming cross market correlations.? You can find one in the movement of the Nikkei stock average, which has been the world?s most despised asset class for the last two decades.

As you can see from the chart below, it is threatening an important multi month breakout to the upside. The reasons for this are simple. A cheaper yen makes Japanese exports more competitive. It also makes the foreign earnings of Japanese multinationals more valuable when translated back into yen. Look no further than the chart of Toyota Motors (TM), which have leapt by a blistering 30% this year.

If you are still unsure about the integrity of the yen collapse, check out the chart for the long dollar basket (UUP). It is setting up for a multiyear head and shoulders breakout to the upside. Uncle Buck has recently taken a steroid shot from the continuing weakness in Europe and the new recession in Japan.

Bottom line: keep selling the yen on rallies, possibly for the next several years.

Those Steroid shots are Definitely Helping Uncle Buck

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-02-20 23:03:112012-02-20 23:03:11Nikkei Shows the Yen Move is Real

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.