Global Market Comments

October 8, 2019

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL),

Global Market Comments

October 8, 2019

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL),

Global Market Comments

August 6, 2019

Fiat Lux

Featured Trade:

(I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE),

(DON’T MISS THE AUGUST 7 GLOBAL STRATEGY WEBINAR),

(HAVE WE SEEN “PEAK AUTO SALES”),

(GM), (TM), (F), (HMC), (TSLA), (NSANY),

There is no limit to my desire to get an early and accurate read on the US economy, which at the end of the day is what dictates the future returns on our investments.

I flew over one of my favorite leading economic indicators only last week.

Honda (HMC) and Nissan (NSANY) import millions of cars each year through their Benicia, California facilities where they are loaded on to hundreds of rail cars for shipment to points inland as far as Chicago.

In 2009, when the US car market shrank to an annualized 8.5 million units, I flew over the site and it was choked with thousands of cars parked bumper to bumper in their white plastic wrappings, rusting in the blazing sun and bereft of buyers.

Then, “cash for clunkers” hit (remember that?). The lots were emptied in a matter of weeks, with mile-long trains lumbering inland, only stopping to add extra engines to get over the High Sierras at Donner Pass. The stock market took off like a rocket, with the auto companies leading.

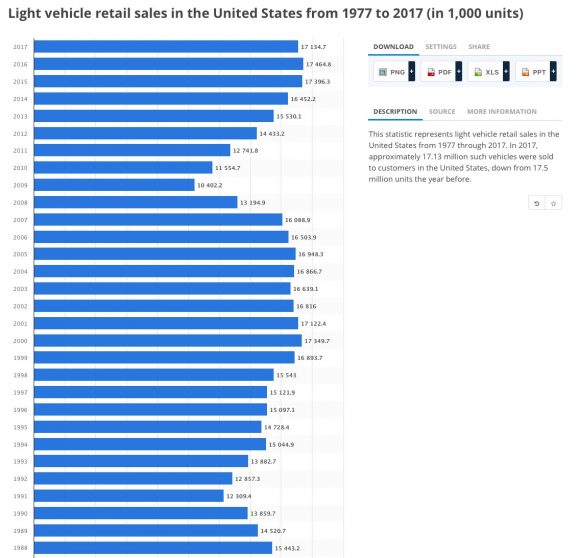

I flew over the site last weekend, and guess what? The lots are full again. Not only that, the trains lined up to take them away are gone. US Auto Sales peaked in October 2017 when they fell just short of a 19 million annualized rate. As of the end of June this year, they had fallen to a 15.1 million annualized rate. July is looking worse still.

And this is what I’m worried about. Auto Sales may not only be peaking for this economic cycle. They may be peaking for all time.

This is my logic.

As they slowly age, Millennials are about to become the principal buyers of automobiles. The problem is that Millennials are purchasing cars at a far slower rate than previous generations.

This is because they have a much higher concentration in urban areas where the cost of car ownership is the most expensive in history. $40 for parking for an evening? Give me a break. But good luck finding free on-street parking, and if you do, your windows will probably get smashed.

In cities like San Francisco, public transportation, bicycles, and electric scooters are the preferred mode of transportation.

It doesn’t help that this generation is shouldering the burden of the bulk of $1.5 trillion in student loan debt. When you owe $2,000 a month in interest, there is little room for a car payment, and you probably don’t have the credit rating to buy a car anyway.

When they do buy cars, all-electric is their first choice, if they can get access to overnight charging. A lot of companies are making this easy by offering free charging for electric commuters in corporate parking lots. This explains why Tesla (TSLA) has taken deposits from 400,000 for their low-end Tesla 3, which has a two-year waiting list for new buyers.

When Millennials do drive, such as on business, for weekend trips or summer vacations, they either rent or “share.” Driving around the city, you see cars parked everywhere with bizarre names like Upshift, Getaround, Zipcar, Turo, and Casual Carpool.

Indeed, Detroit takes the car-sharing threat so seriously that the Big Three have all bought into the technology, with General Motors taking a stake in Maven. (GM) plans to start its own peer-to-peer car-sharing service this summer.

This is all a mystery for my generation, which grew up tearing apart old cars and putting them back together. I spent a year trying to put the engine on my 1955 Volkswagen back together. When I gave up, I towed the car and a big box full of greasy parts to a local mechanic, a German Army veteran. When he finished, even he had four parts left over.

Do you know who believes my rash, possible MAD theory? Investors in auto stocks, one of the worst-performing sectors of the stock market this year. Shares like those of General Motors (GM) keep breaking new valuation lows.

What was (GM)’s price earnings multiple today? Try a miserable zero since the company loses money, one of the lowest of all S&P 500 stocks. Hapless portfolio managers keep getting sucked into the shares, which have become one of the ultimate value traps.

It is all further evidence that my cautious view on the US economy is correct, that multiple crises overseas are ahead of us, and that the stock market could drop 5%-10% at any time. The auto industry should lead the charge to the downside, especially General Motors (GM) and Ford (F).

As for Tesla (TSLA), better to buy the car than the stock.

Sorry, the photo is a little crooked, but it's tough holding a camera in one hand and a plane's stick with the other while flying through the turbulence of the San Francisco Bay’s Carquinez Straight.

Air traffic control at nearby Travis Air Force base usually has a heart attack when I conduct my research in this way, with a few joyriding C-130s having more than one near miss.

Global Market Comments

July 8, 2019

Fiat Lux

Featured Trade:

(STANDBY FOR THE COMING GOLDEN AGE OF INVESTMENT),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

I believe that the global economy is setting up for a new Golden Age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly.

This is not some pie in the sky prediction.

It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call “intergenerational arbitrage” will be the principal impetus. The main reason that we are now enduring two “lost decades” of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million “Gen Xers”.

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and “RISK ON” assets like equities, and more buyers of assisted living facilities, health care, and “RISK OFF” assets like bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward six years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the “millennial” generation trying to buy their assets.

By then, we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

The stock market rockets in this scenario.

Share prices may rise very gradually for the rest of the teens as long as tepid 2-3% growth persists.

After that, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 100,000 by 2030.

If I’m wrong, it will hit 200,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well.

The 100-year supply of natural gas (UNG) we have recently discovered through the new “fracking” technology will finally make it to end users, replacing coal (KOL) and oil (USO).

Fracking applied to oilfields is also unlocking vast new supplies.

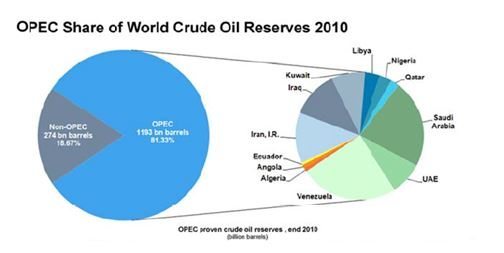

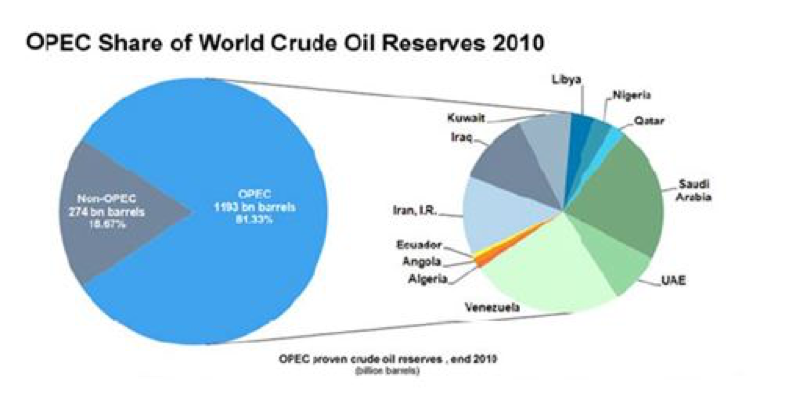

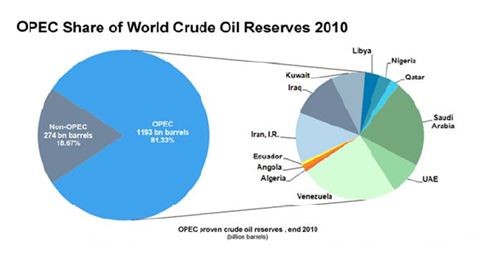

Since 1995, the US Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC’s share of global reserves is collapsing.

This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.

Mileage for the average US car has jumped from 23 to 24.7 miles per gallon in the last couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low.

Alternative energy technologies will also contribute in an important way in states like California, accounting for 30% of total electric power generation by 2020.

I now have an all-electric garage with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow.

The net result of all of this is lower energy prices for everyone.

It will also flip the US from a net importer to an exporter of energy with hugely positive implications for America’s balance of payments.

Eliminating our largest import and adding an important export is very dollar-bullish for the long term.

That sets up a multiyear short for the world’s big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it’s great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos.

But at the enterprise level, this is enabling speedy improvements in productivity that is filtering down to every business in the US, lower costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high.

Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past which are also being spearheaded in the San Francisco Bay area.

This is because the Golden State thumbed its nose at the federal government ten years ago when the stem cell research ban was implemented.

It raised $3 billion through a bond issue to fund its own research even though it couldn’t afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years, they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver’s seat on these innovations? The USA.

There is a political element to the new Golden Age as well. Gridlock in Washington can’t last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but nobody wants to be blamed for.

That means raising the retirement age from 66 to 70 where it belongs, and means-testing recipients. Billionaires don’t need the maximum $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cut defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them for free. That’s why they have recently bought a second used aircraft carrier. The Middle East is now their headache.

The national debt then comes under control, and we don’t end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens.

The reality is that the global economy is already spinning off profits faster than it can find places to invest them, so the money ends up in bonds instead.

Sure, this is all very long-term, over the horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won’t kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

Global Market Comments

December 12, 2018

Fiat Lux

Featured Trade:

(STANDBY FOR THE COMING GOLDEN AGE OF INVESTMENT),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

Global Market Comments

September 27, 2018

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL),

(TUESDAY, OCTOBER 16, 2018, MIAMI, FL,

GLOBAL STRATEGY LUNCHEON)

Global Market Comments

May 15, 2018

Fiat Lux

Featured Trade:

(FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(GET READY FOR THE COMING GOLDEN AGE),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly.

This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call "intergenerational arbitrage" will be the principal impetus. The main reason that we are now enduring two "lost decades" of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million "Gen Xers."

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and "RISK ON" assets such as equities, and more buyers of assisted living facilities, health care, and "RISK OFF" assets such as bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward six years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the "millennial" generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

The stock market rockets in this scenario. Share prices may rise very gradually for the rest of the teens as long as tepid 2% growth persists. A 5% annual gain takes the Dow to 28,000 by 2019.

After that, after a brief dip, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 100,000 by 2030. If I'm wrong, it will hit 200,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well.

The 100-year supply of natural gas (UNG) we have recently discovered through the new "fracking" technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies.

Since 1995, the United States Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC's share of global reserves is collapsing.

This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.

Mileage for the average U.S. car has jumped from 23 to 24.7 miles per gallon in the past couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low.

Alternative energy technologies will also contribute in an important way in states such as California, accounting for 30% of total electric power generation by 2020, and 50% by 2030.

I now have an all-electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the U.S. from a net importer to an exporter of energy, with hugely positive implications for America's balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term.

That sets up a multiyear short for the world's big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it's great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos.

But at the enterprise level this is enabling speedy improvements in productivity that are filtering down to every business in the U.S., lowering costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area.

This is because the Golden State thumbed its nose at the federal government 10 years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn't afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver's seat on these innovations? The USA.

There is a political element to the new golden age as well. Gridlock in Washington can't last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but for which nobody wants to be blamed.

That means raising the retirement age from 66 to 70 where it belongs and means-testing recipients. Billionaires don't need the maximum $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them. That's why they have recently bought a second used aircraft carrier. The Middle East is now their headache.

The national debt then comes under control, and we don't end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens. The Fed has already told us as much by indicating that the Federal Reserve will only raise interest rates at an infinitesimally slow rate of 25 basis points a quarter.

Sure, this is all very long-term, over-the-horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won't kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

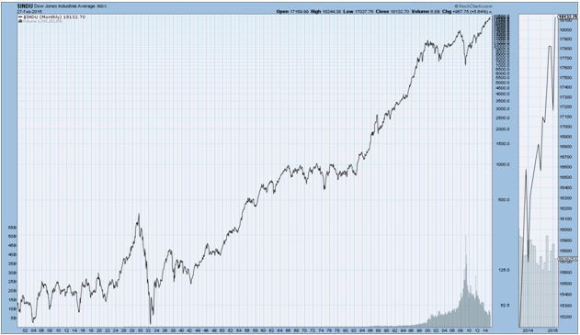

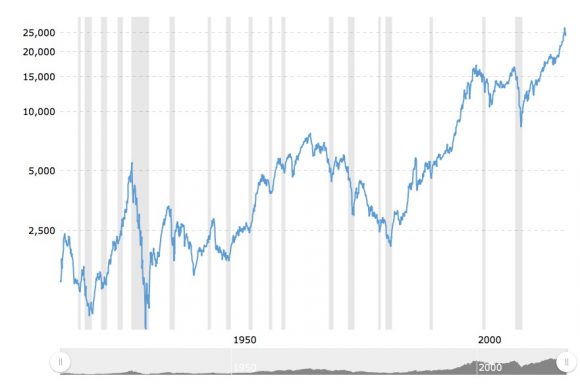

Dow Average 1908-2018

Another American Golden Age is Coming

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950?s, and which I still remember fondly. This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call ?intergenerational arbitrage? will be the principal impetus. The main reason that we are now enduring two ?lost decades? is that 80 million baby boomers are retiring to be followed by only 65 million ?Gen Xer?s?. When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and ?RISK ON? assets like equities, and more buyers of assisted living facilities, health care, and ?RISK OFF? assets like bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward ten years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home. That is when you have 65 million Gen Xer?s being chased by 85 million of the ?millennial? generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes. The middle class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990?s.

The stock market rockets in this scenario. Share prices may rise very gradually for the rest of the teens as long as tepid 2% growth persists. A 5% annual gain takes the Dow to 20,000 by 2020. After that, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 80,000 by 2030. Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well. The 100-year supply of natural gas (UNG) we have recently discovered through the new ?fracking? technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies.

Since 1995, the US Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC?s share of global reserves is collapsing. This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.? Mileage for the average US car has jumped from 23 to 24.7 miles per gallon in the last couple of years. Total gasoline consumption is now at a five year low.

Alternative energy technologies will also contribute in an important way in states like California, accounting for 30% of total electric power generation. I now have an all-electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the US from a net importer to an exporter of energy, with hugely positive implications for America?s balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term. That sets up a multiyear short for the world?s big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it?s great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos. But at the enterprise level this is enabling speedy improvements in productivity that is filtering down to every business in the US, lower costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin. Profit margins are at an all time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development. When the winners emerge they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area. This is because the Golden State thumbed its nose at the federal government ten years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn?t afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 40 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday. What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver?s seat on these innovations? The USA.

There is a political element to the new Golden Age as well. Gridlock in Washington can?t last forever. Eventually, one side or another will prevail with a clear majority. Conservatives may grind their teeth, but if Hillary Clinton wins in 2016, the Democrats will control the White House until 2025. Right now, she is leading by a 60% margin with Republican women.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but nobody wants to be blamed for. That means raising the retirement age from 66 to 70 where it belongs, and means-testing recipients. Billionaires don?t need the $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up. A Pax Americana would ensue. That means China will have to defend its own oil supply, instead of relying on us to do it for them. That?s why they have recently bought a second used aircraft carrier.

Medicare also needs to be reformed. How is it that the world?s most efficient economy has the least efficient health care system, with the worst outcomes? This is going to be a decade long workout and I can?t guess how it will end. Raise the growth rate and trim back the government?s participation in the credit markets, and you make the numerous miracles above more likely.

The national debt comes under control, and we don?t end up like Greece. The long awaited Treasury bond (TLT) crash never happens. Ben Bernanke has already told us as much by indicating that the Federal Reserve may never unwind its massive $3.5 trillion in bond holdings.

Sure, this is all very long-term, over the horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won?t kick in for another decade. But some individual industries and companies will start to discount this rosy scenario now. Perhaps this is what the nonstop rally in stocks since November has been trying to tell us.

Dow Average 1970-2012

Dow Average 1970-2012

Another American Golden Age is Coming

Another American Golden Age is Coming