Mad Hedge Technology Letter

July 8, 2024

Fiat Lux

Featured Trade:

(ARM SHINES BRIGHT)

(ARM), (NVDA), (AMD)

Mad Hedge Technology Letter

July 8, 2024

Fiat Lux

Featured Trade:

(ARM SHINES BRIGHT)

(ARM), (NVDA), (AMD)

With the US Central Bank’s policy being quite accommodative, this advantageous backdrop has really set the platform for certain strategic tech companies to shine on the public markets.

In particular, chip stocks have been the darlings of the AI revolution and will continue to be in the limelight.

Part of this is about investors not knowing in particular what software firms will benefit from AI.

It is really a crapshoot to know how the software will look like in the future, but investors do know that software will be powered by the backend infrastructure which is why AI chips are fetching a premium at market in today’s stock market.

Once the software part of it starts to reveal itself, then it is highly likely the software winners will start to experience the same sort of price appreciation in shares that AI chip companies are experiencing right now.

That trend reversal is still years off so it is better to spend our energy on chip stocks.

The no-brainers are the likes of Nvidia and AMD, but the lineup is dee.

Look at the 2nd and 3rd tier of chip stocks like British chip company ARM (ARM).

Arm is also right in the mix of the AI boom. The positive market sentiment toward AI advancements continues to propel Arm's stock upwards. Furthermore, the company's former focus on low-power embedded and mobile chips is changing before your eyes. These days, you'll find Arm-based chips all over modern data centers and PC systems.

The broader market dynamics also played a role in Arm's rise. A softer-than-expected jobs report in May fueled hopes for potential interest rate cuts by the Federal Reserve, which would benefit growth stocks. The semiconductor sector is full of growth stories, including Arm.

Industry news also contributed to Arm's strong performance. Reports that Taiwan Semiconductor Manufacturing was investing in extreme ultraviolet lithography suggested a robust demand for next-generation chip technologies. As TSMC is a leading manufacturer of Arm-based chips, this investment indicated a positive outlook for Arm's future growth.

Arm's strategic positioning in the AI ecosystem highlights its potential for sustained growth. The company's advanced v9 architecture and its power-efficient processor platforms are increasingly interesting to major industry players, strengthening Arm's competitive edge in the semiconductor market.

ARM and its ticker symbol were added to the Nasdaq-100 Index on June 24.

This move guarantees more capital flow into ARM as it becomes part of a bigger ETF meaning pension and institutional money will own a piece of ARM and help the stock rise.

Arm's rapid inclusion in the index after an initial public offering last September reminds investors of its growing importance in the global technology ecosystem. As CEO Rene Haas highlighted in that announcement, this achievement validates Arm's business strategy and its critical role in providing foundational compute solutions for AI workloads.

Don’t forget that ARM agreed to be purchased by Nvidia which speaks volumes of what Nvidia believes about ARM.

Unfortunately for both, the deal was shut down due to regulatory issues, and imagines the future trajectory of ARM if that deal went through.

In the past 365 days, the stock is up over 200% and just looking at a 2024 chart, readers can understand how investors have complete belief in the future of ARM.

ARM will continue to maintain an important position in the future of AI and they are a juicy takeover target.

I do believe that AI stocks like ARM will continue to grind up, but we are inching closer to a point where investors will take profits before the next leg up.

Global Market Comments

July 8, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

and NORTH TO ALASKA),

(NVDA)

Yes, I’m back from the Frozen Wasteland of The North.

Except it was anything but a wasteland. It was far more beautiful than I remember 57 years ago. In a world beset with accelerating change everywhere, Alaska is unchanged from the primordial age. It is a natural paradise blessed with spectacular scenery and filled with wild animals.

But more on that later.

Now on with the most important question of the day.

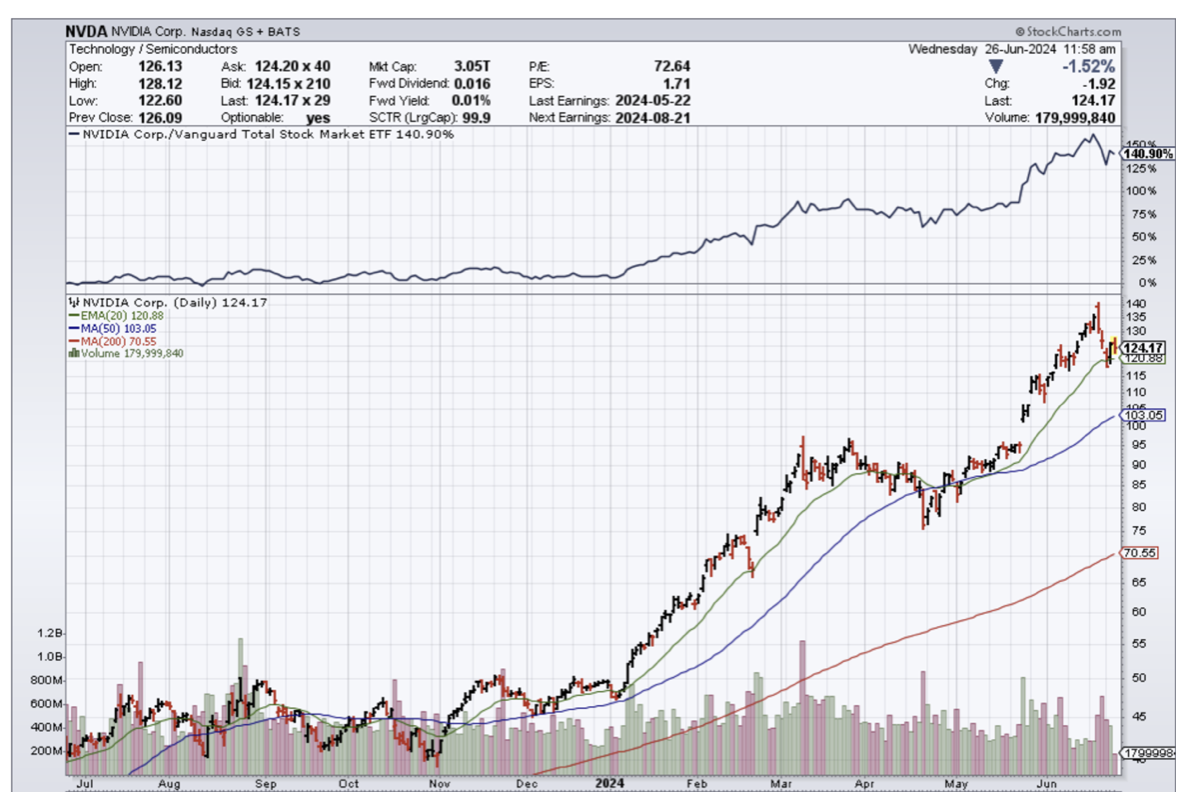

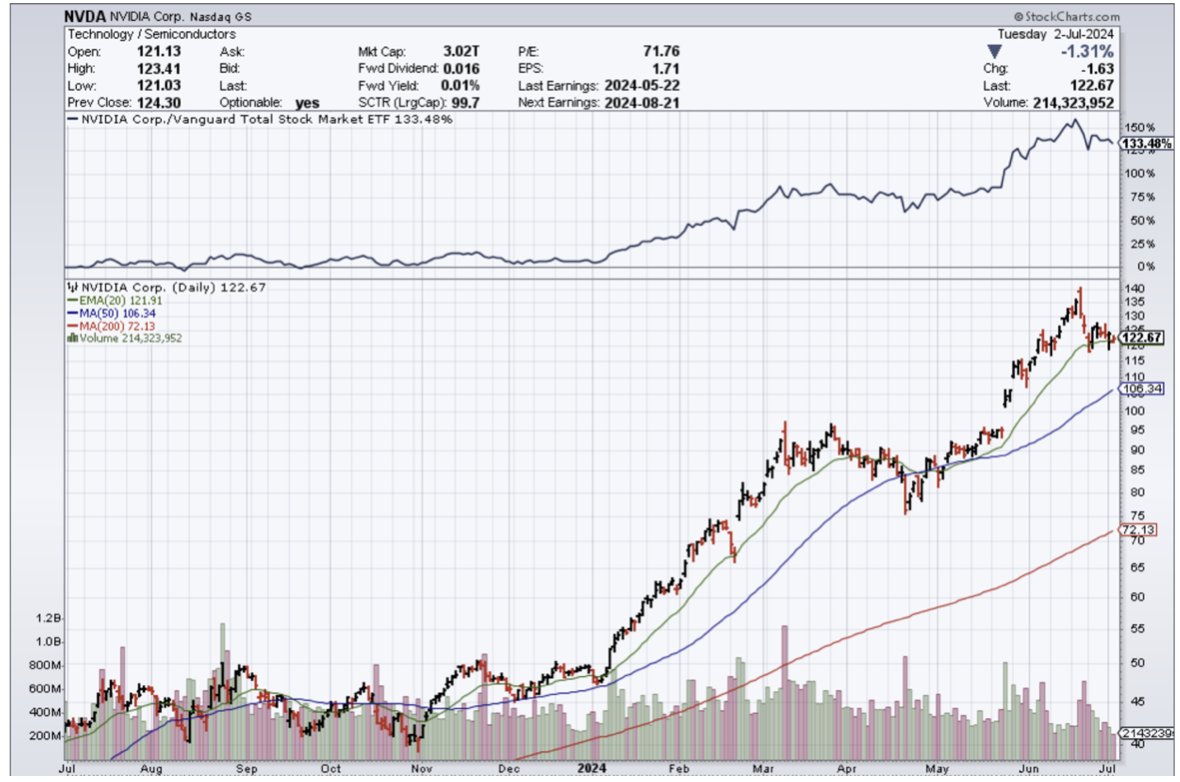

What to do about NVIDIA?

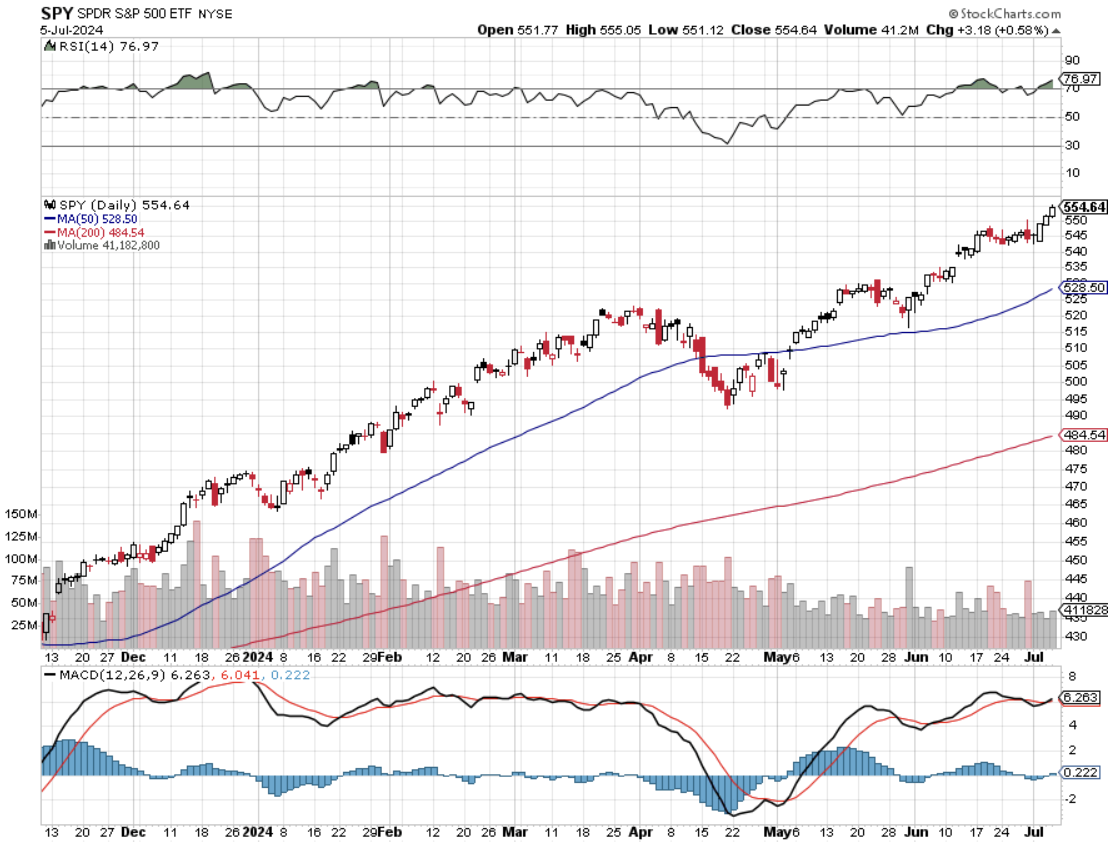

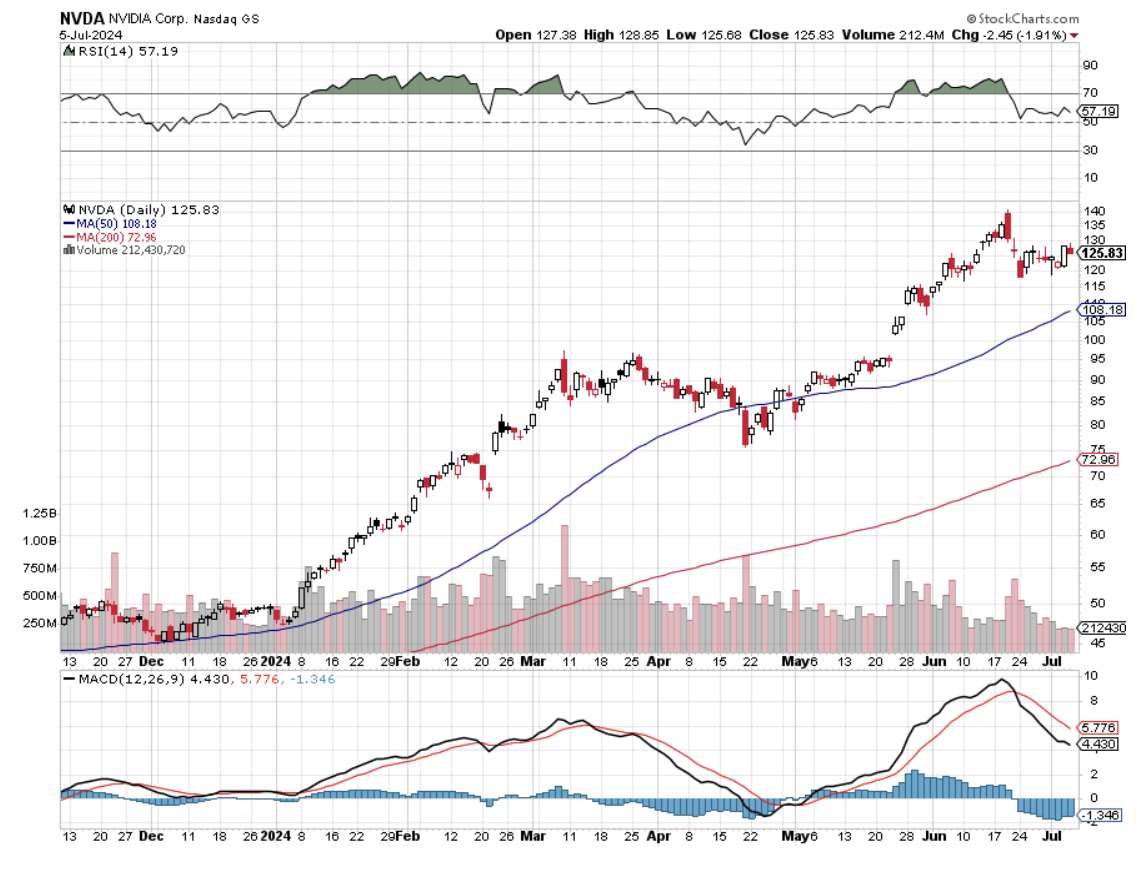

Those who heeded my advice to load up on the Silicon Valley graphics card maker are facing a dilemma. (NVDA) is now such an outsized share of the entire stock market, some 6% of the S&P 500. Even if you don’t own (NVDA) directly, if you are an index investor in the (SPX), it is still your largest holding.

If you sell NVIDIA and it doubles again, you look like an idiot. If you hold it and it drops by half, you look like a bigger idiot. Here is my five cents worth. It will do both in the coming years.

Fortunately, there is another solution. Sell short (NVDA) out-of-the-money calls against your existing long stock position. If the shares rise, you will think you died and went to heaven. If it falls, at least your cost basis falls by the amount of option premium you received.

I’ll give you an example.

Let’s say you still have 100 shares of (NVDA) that no one has talked you out of selling yet that you bought last October at a split-adjusted $40. You can sell short the August 16, 2024 $140 calls for $3.50 which expire in six weeks and pays you $350 in options premium. If NVIDIA fails to rise above $140 and they expire worthless, you get to keep $350 ($3.50 X 100 shares per option). This reduces your cost basis \by $3.50 to $36.50.

If the shares rise above $140, they will get called away and your upside breakeven point is now $143.50 ($140 + $3.50). You get to make an extra $18.50 in capital gain to get there from Friday’s $125 close.

It’s win, win, win.

The only downside is that shares called away are treated as a sale for tax purposes. Remember, you are being taxed on a much larger profit. You can always offset the gain by taking a loss in another stock, such as in the energy sector.

I just thought you’d like to know.

Silver has been a star performer as the top precious metal this year, up 30% at the highs, but has recently been faltering. A round of profit-taking has knocked the wind out of not just the white metal, but all precious metals. Most silver ETFs have seen outflows this year, while sales of silver Eagle coins from the US mint have dropped by half.

However, while financial demand for silver has been going down the toilet, industrial demand is still soaring. This is a new development in the history of silver.

The great mystery among long-time silver watchers like myself is that silver has gone up at all this year. High interest rates and inflation and a strong economy are not the usual backdrop for a bull market in silver.

But like so many other markets recently, it has irrevocably changed. Industrial demand is taking over. Silver is the world’s best conductor of electricity. Al Capone’s Duesenberg V12 was entirely wired with silver for this reason. And the fivefold demand in the size of the national electrical grid demanded by AI has put a new spotlight on the poor man’s gold.

In 2023 silver demand from the solar panel industry jumped by 64% and it is expected to rise by another 20% this year. In the meantime, supplies of silver from Companies like Wheaton Precious Metals (WPM) have fallen marginally. It's that old supply/demand thing. Never fight it.

So any further falls in in silver prices should be bought with both hands. If you’re lucky, you might get another 10% drop. And if I’ve really hooked you with this piece, buy the 2X long silver ETF (AGQ). It will be up huge by yearend.

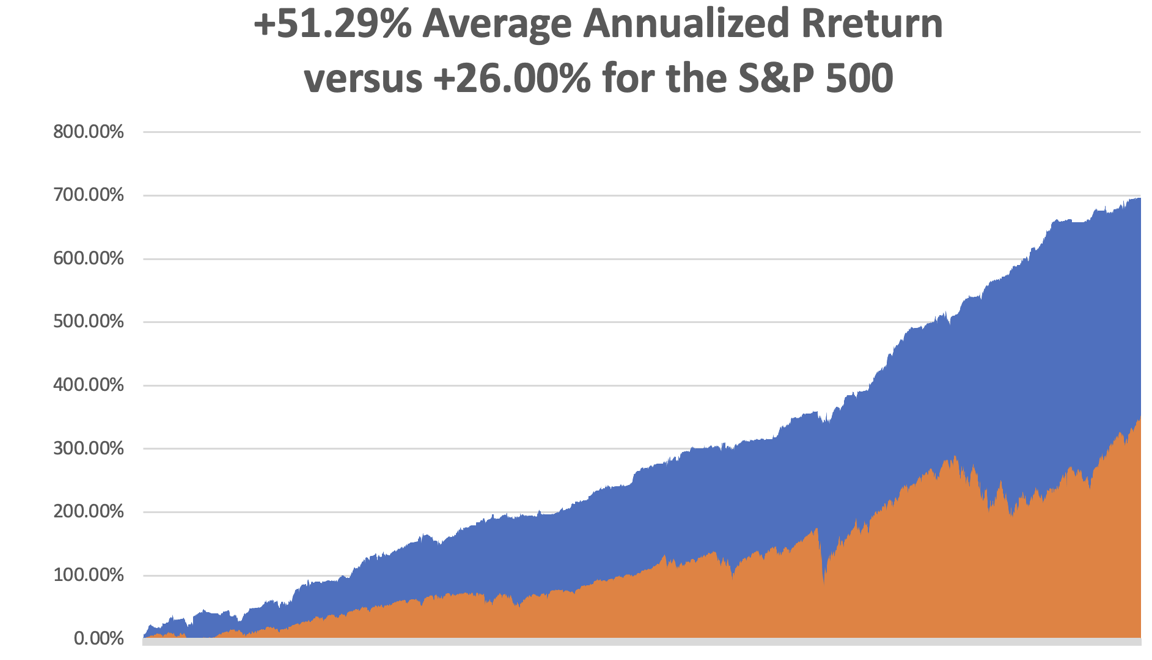

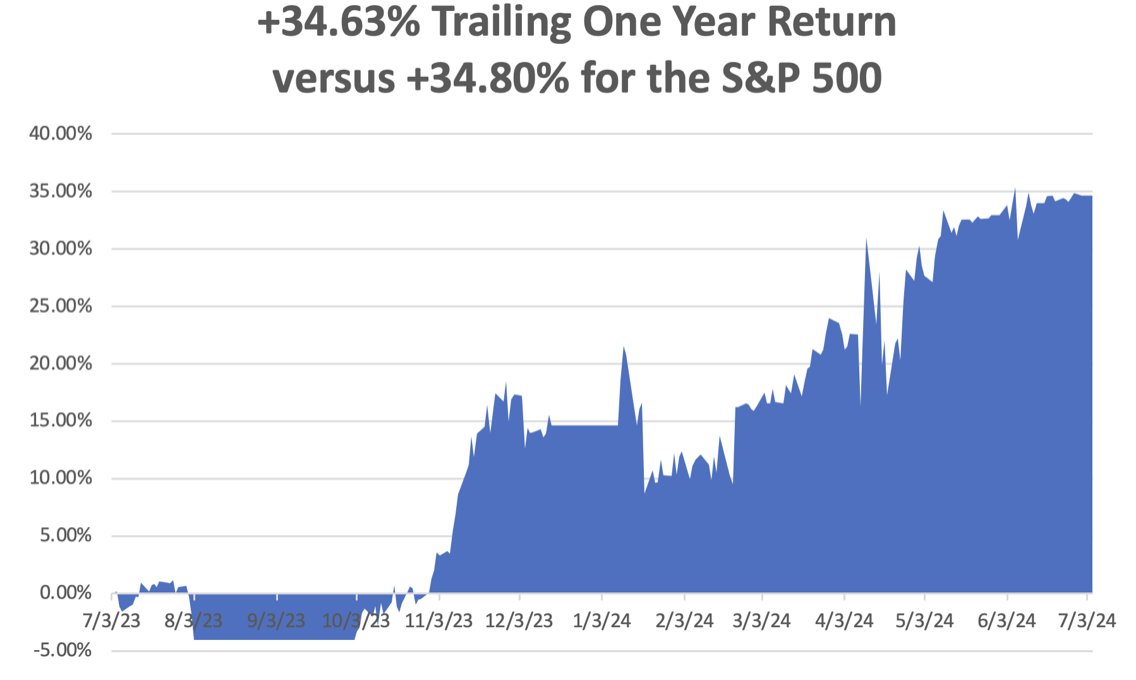

So far in July, we are up +0%. My 2024 year-to-date performance is at +20.02%. The S&P 500 (SPY) is up +16.14% so far in 2024. My trailing one-year return reached +34.63%.

That brings my 16-year total return to +696.65%. My average annualized return has recovered to +51.29%.

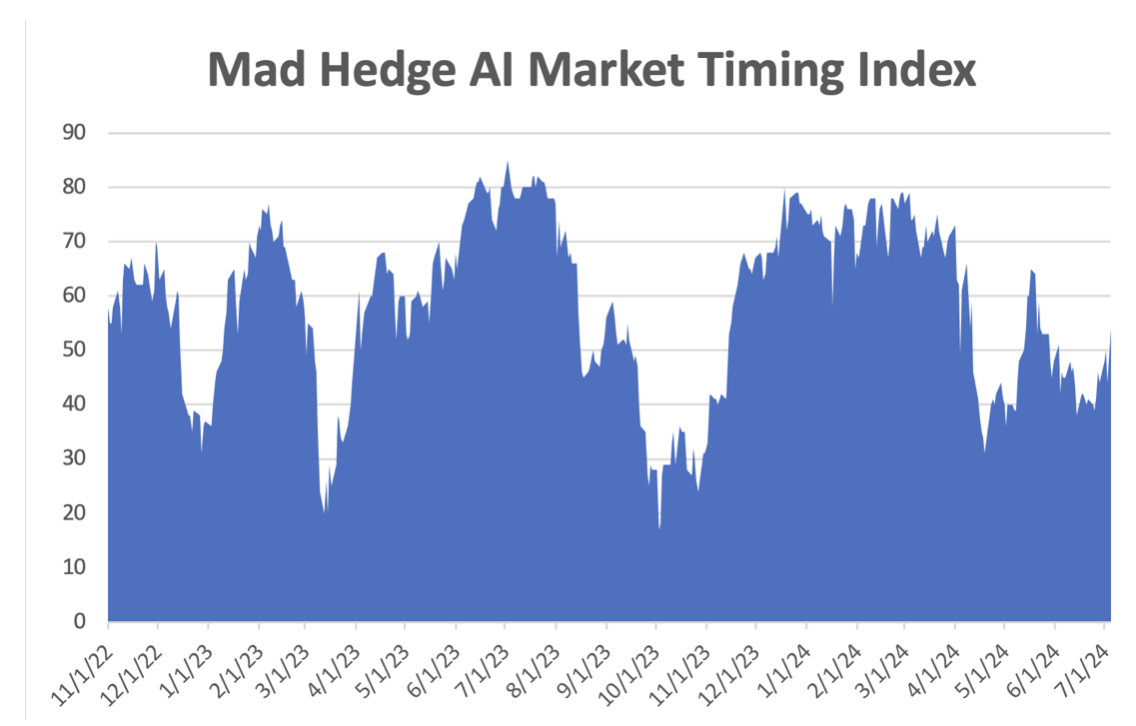

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I am currently in a very rare 100% cash position.

Some 63 of my 70 round trips were profitable in 2023. Some 29 of 38 trades have been profitable so far in 2024, and several of those losses were really break-even.

Nonfarm Payroll Report Comes up Short in June at 200,000. The Headline Unemployment Rate rose to 4.1% nearly a three-year high.

Price of Bitcoin Sputters, Bitcoin price tanks as traders worry over the likely dumping of tokens from defunct Japanese exchange Mt. Gox and further selling by leveraged players after the cryptocurrency's strong run.

Bezos Cashes Out, Founder and executive chair Jeff Bezos will sell almost $5 billion worth of shares in Amazon as his e-commerce company hits all-time highs.

Trade War Between China And The E.U. Heating Up, China will investigate European brandy imports after the E.U. slapped tariffs on Chinese-made electric vehicles. This will effectively make the price of goods a lot higher in the Old Continent.

US Venture Capitalists Flood into AI Investments, U.S. venture capital funding surged to $55.6 billion in the second quarter, marking the highest quarterly total in two years. The latest data represents a 47% jump from the $37.8 billion U.S. startups raised in the first quarter. Most of these investments will go into AI.

Volkswagen Will Not Produce Rivian Cars, Rivian announced that it has no plans to produce vehicles with Volkswagen after a media report said Rivian is in early talks with the German automaker to extend a recent partnership beyond software.

Inflation Inches Up, The core personal consumption expenditures price index increased just a seasonally adjusted 0.1% for the month and was up 2.6% from a year ago. This inflation number is called the PCE.

Google Buys Solar Power Firm Google will snap up Taiwan's New Green Power and could buy up to 300 megawatts of renewable energy from the BlackRock fund-owned firm to help cut its carbon emissions and those of suppliers.

EU set to charge Meta, the European Union is set to penalize Meta for breaking the bloc's landmark digital rules. Regulators are targeting Meta's "pay or consent" model. It’s illegal in Europe.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, July 8, the Consumer Inflation Expectations are released.

On Tuesday, July 9 at 7:00 AM EST, the NFIB Business Optimism Index is published.

On Wednesday, July 10, Mortgage Applications are out.

On Thursday, July 11 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Consumer Price Index.

On Friday, July 12 at 8:30 AM, the Producer Price Index is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, it was with great fondness that I returned to Alaska for the first time in 57 years.

But instead of hitchhiking heavily armed with a high-powered rifle and a pistol, this time I embarked on Cunard’s Queen Elizabeth, one of the finest cruise ships afloat.

While before I battled Grizzley bears and torrential rainstorms, in 2024 I observed the ailments that beset old age. Here’s a knee replacement, there goes a new hip, sorry about the emphysema, and hello Mr. Arthritis.

To say that America’s 49th state is enjoying boom times would be a vast understatement. Because of the Gaza War, every cruise line canceled their Middle Eastern tours and moved the ships to the Caribbean in winter and Alaska in the summer.

As a result, you have six gigantic ships disgorging 25,000 passengers and crew onto Juneau, a town of just 30,000. Try to imagine Times Square on New Year's Eve solely occupied by sober waddling obese 70-year-olds. Juneau only has dock space for five ships so one forlorn Celebrity ship had to use shuttles to ferry passengers ashore.

Welcome to the T-shirt-based economy.

Franklin Street was lined door to door with souvenir shops hawking every kind of local knick-knack. Maybe 99% of the souvenirs were made in China. There were no less than 25 jewelry stores. And if you ever had a desire for salmon or king crab for lunch, this is your place.

It has also collapsed cruise prices. The cheapest inside cabin with no windows on my ten-day cruise cost $799 with all the food included. That’s cheaper than staying at the Motel 6 and eating at Taco Bell every day. Cruising is now far and away the cheapest form of vacation travel today.

The demands on the local economy were so great that most shore excursions were sold out. In any case, mushing with sled dogs didn’t really appeal to me, nor did whale watching or sea kayaking with the orcas.

I would have done the fly fishing in a heartbeat, but it was the first to sell out. The Great American Eagle Experience offered only one sorry example which was missing half a wing after getting hit by a car.

As with every large corporation in America today, Cunard is doing everything it can to squeeze every penny of profit out of their business. Recently added were branded Cunard red and white wine, gin, whiskey, and vermouth. Oh, and the penuriously underpaid staff are now billed $1,000 for room and board, which includes a tiny cabin below the waterline with no porthole.

And many of the locals are here only temporarily. Freshly graduated college students come up from the lower 48 to work as drivers, guides, cooks, and dishwashers to handle the summer surge. Many take two or three jobs and bank enough to buy houses back home.

They live in RVs, tents, and abandoned buses. That’s no fun when it rains every day, and you have hungry raiding bears looking for dinner every night.

The population drops by half in September when the cruise ships depart for warmer climes. What do the remaining residents do for the ensuing eight months? Hunt, fish, fix things around the house, watch movies, keep the town bars in business, work on art projects, and dream about next summer. Juneau only gets three hours of sun around the winter solstice.

At one point, fed up with the melee downtown, I took a city bus 20 miles just to enjoy Alaska in its pristine natural state. It was clear that the Inside Passage received massive amounts of rain, over 120 inches a year, and 100 feet of snow. The forest was so thick that you couldn’t walk through it and the ground was covered in moss.

You would think this would make cruise line stocks a screaming buy, and in fact, it has. Carnival Corporation (CCL), the largest, owning nine cruise lines, carried a staggering 12 million passengers last year.

Royal Caribbean Cruises (RCL) has jumped by 35%, Carnival by 40%, and Norwegian Cruise Line Holdings (NCLH) by 20%. Viking Holdings (VIK) only went public in April and was met with a warm reception, tacking on 27% since then.

It's not so much the booming Alaska business that is driving share prices. Remember, these are discount offerings at the expense of higher-margin Middle Eastern business. It has more to do with the expectation of falling interest rates. All the cruise lines took on massive debt to keep from going under during Covid and a Fed interest rate cut will be a shot in the arm for these heavily indebted companies.

At the farthest north point of the trip, some 60 degrees north latitude, I enjoyed the famed Midnight sun. It was fully bright until 10:30 PM and never became completely dark. That explains the legendary size of Alaska’s summer vegetables. When I was in Fairbanks at 70 degrees, the sun came in for a landing, then took off again, never dipping below the horizon. There the Northern Lights were awesome.

The ship hosted two formal nights, a “Fire and Ice” perfect for my white dinner jacket and a “Venetian Masquerade Ball” with masks that had black written all over it. Cunard has been dialing back the formal nights over the years. Perhaps they’re just catering to the US market, or maybe society is just becoming more casual.

Many ship activities are oriented around selling you junk, like “The Excitement of Investing in Tanzanite” and “The Fine Art of Collecting Watercolors” which I learned to pass on a long time ago as blatant rip-offs.

Of course, no cruise is complete without a singles night. I put on my cleanest shirt and pressed jeans and was introduced to a dozen white-haired wealthy widows all in the 70s and 80s. No luck this time.

Maybe next year.

All in all, it was the perfect rest from this year’s tempestuous markets….until the next cruise.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

July 3, 2024

Fiat Lux

Featured Trade:

(SHOULD I INVEST IN AI CHIPS OR AI SERVERS?)

(SMCI), (NVDA), (DELL)

The AI server market is booming and so are the AI chip markets.

I’ll talk about 2 prestigious companies right in the mix of things.

For long-term portfolios, it’s essential to not miss out on these supercharge growth companies.

I just don’t think that average investors will be able to make up the performance if they miss the boat of these 2 companies. The law of large numbers will just put you too far behind.

All the hot new money is going into AI which adds to the momentum of the share price trajectories.

Even the old money, after not being convinced by Bitcoin, is starting to come around to AI partly because most of the companies involved in AI are publicly listed companies on the New York Stock Exchange.

It makes it a lot easier when the source of exponential growth isn’t on some alternative exchange in some alternate currency in some backwater jurisdiction.

With a few clicks and moving a few dollars here and there, investors can be part of the AI future whether it be in AI chips or AI servers like the companies I am about to talk about.

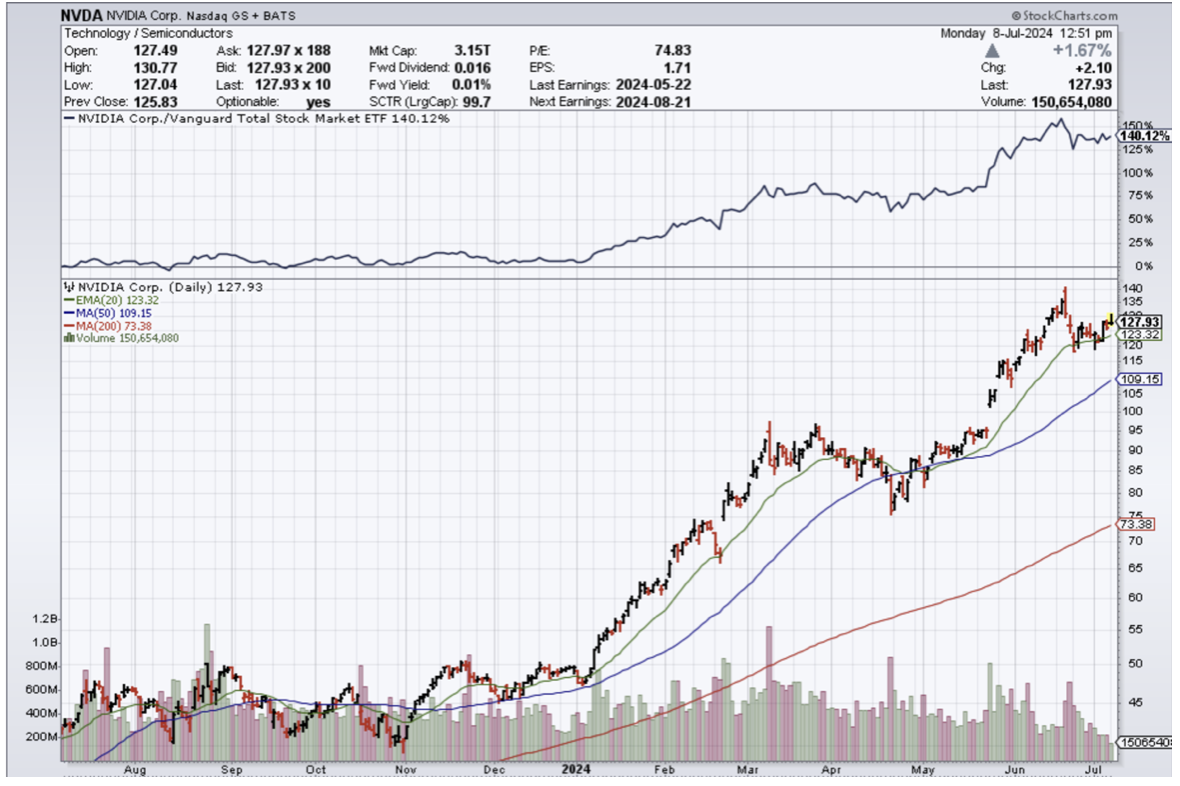

What up with Nvidia?

Nvidia (NVDA) dominates an impressive 94% of the AI chip market. It’s basically a monopoly or close to it.

Revenue is rising a stunning 262% year over year.

Even more interesting, emerging growth avenues in the nascent AI market indicate that Nvidia could end up doing even better than that.

For instance, governments are also betting the ranch on AI and this stable source of revenue will highly likely grow substantially for the foreseeable future.

Nvidia's customer base is diversifying beyond the major cloud infrastructure providers that have been deploying its chips in large numbers to train and deploy AI models.

Spending on AI chips is expected to grow more than 10-fold over the next decade, generating $341 billion in revenue in 2033 compared to $23 billion last year.

Nvidia should remain the Tom Brady of AI stocks as the race to develop AI applications by companies and governments alike has created a secular growth opportunity.

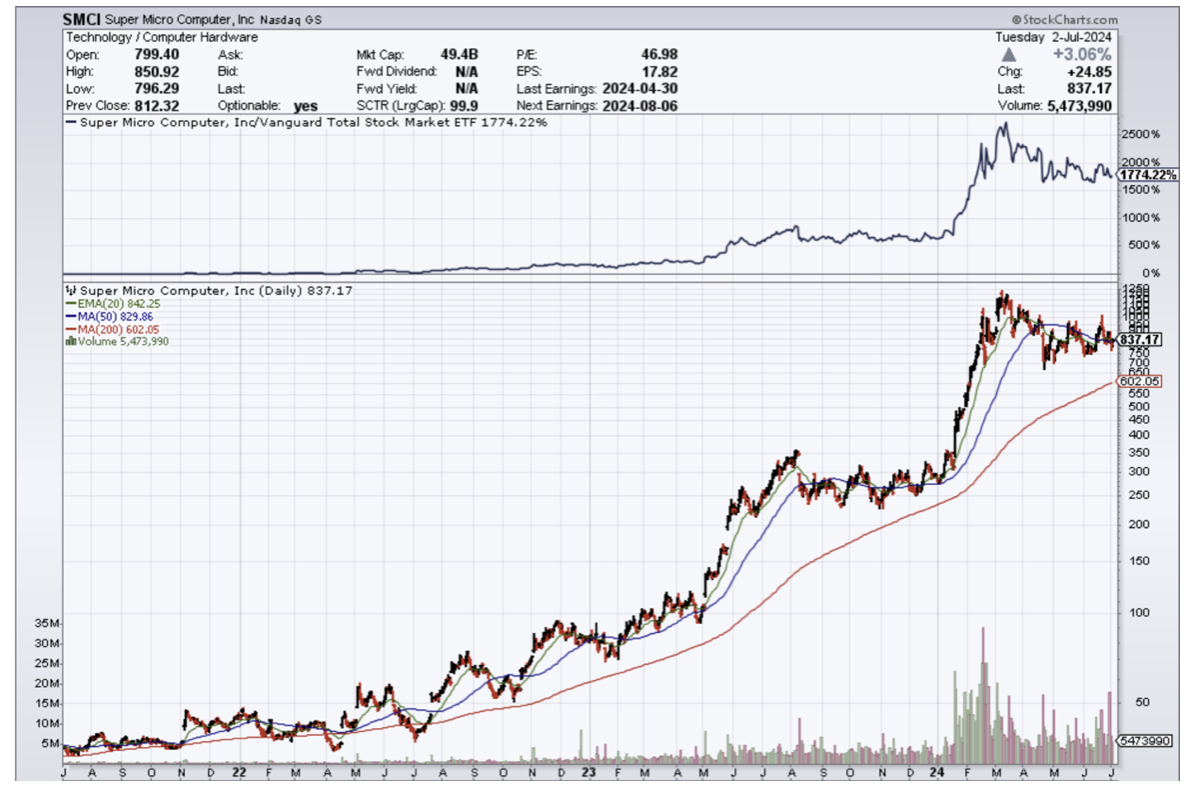

What about Super Micro Computer?

Supermicro's future prospects are attached to some extent with that of Nvidia’s.

Data center operators require server rack solutions of the type that Supermicro sells to mount the processors sold by Nvidia and other chipmakers.

Revenue jumped 200% year over year and Supermicro isn't all that far behind Nvidia when it comes to how AI has supercharged its fortunes.

I expect its top line to nearly double over the next couple of years.

Demand for AI servers is expected to expand at a compound annual rate of 25% through 2029.

Supermicro is growing at a faster pace than the AI server market right now. As it turns out, its growth is faster than that of more established companies such as Dell.

How to invest?

Supermicro is cheaper than Nvidia and Nvidia’s run-up to a more than $3 trillion market valuation has got to scare some people with sticker shock.

People with a time advantage of more than a few years should invest in Super Micro, whereas investors looking for that quick sugar high should buy the dips in Nvidia.

In short, anyone under the age of 40 and many years in front of them should invest long-term in Super Micro at a market cap of $50 billion. With Nvidia, I could easily see its market cap climbing to $4 trillion soon, but a wicked pullback would mean its market cap going from $4 to $3 trillion.

Either way, these are two tech firms with great prospects in the current and future.

Mad Hedge Technology Letter

July 1, 2024

Fiat Lux

Featured Trade:

(SOFTBANK BETS THE RANCH ON AI)

(SFTBY), (NVDA)

SoftBank Group raised about $1.86 billion via dollar and euro bond sales in one of the biggest foreign-currency deals by a Japanese company this year.

This is big news.

Softbank is one of the most prominent venture capitalist funds in the world and they plan on deploying the capital solely into generative artificial intelligence.

Many of these heavyweights from Asia, and the Middle East, and other billionaires around the finance world are chomping at the bit to get a piece of American AI firms.

This trend is in the early innings and won’t slow down.

It’s interesting that Softbank raised the currency in dollars and euros which is another bet on the Japanese yen strengthening and the Fed cutting rates.

The Yen has been one of the worst-performing currencies in the past few years and there is a chance this move could blow up in Softbank’s face.

The dollar is strong and has been increasingly strong lately as the Fed stays higher for longer.

However, if the dollar does get stronger, it will mean that Softbank will need to pay higher costs. Even that said, they will still dive head-first into AI.

My belief is that their CEO Masayoshi Son, who I know very well, will bet the ranch on AI considering he sold out of his Nvidia shares in 2022 and calls it the “fish that got away.”

He rues leaving hundreds of billions of dollars in profits on the table and I don’t believe he is willing to allow that to happen again.

So he will approach these new investments as an “all or nothing” all guns blazing type of strategy.

In its first non-yen debt offering since 2021, billionaire Masayoshi Son’s company priced two dollar tranches totaling $900 million and two euro tranches raising €900 million ($964 million).

It’s not only Softbank, it’s also other Japanese companies looking for ample liquidity.

SoftBank joins a bond bonanza by issuers from Asia and elsewhere including even bigger deals from fellow Japanese borrowers such as Takeda Pharmaceutical and Rakuten.

The Japanese firm this year directly invested $200 million into Tempus AI, a startup that analyzes medical data for doctors and patients to come up with better treatments. More recently, it backed Perplexity AI at a $3 billion valuation, betting on a firm that aims to use AI to compete with Alphabet’s Google search.

Longer term, SoftBank is working on a plan to deploy some $100 billion into AI-related chips in a project dubbed Izanagi, Bloomberg News reported in February.

My belief here is that Softbank and other Japanese companies are on the verge of deploying over $1 trillion of new money into generative artificial companies in America.

There is a reason why leading AI companies like Nvidia (NVDA) have surged to the skies and a lot of it is foreign money coming chasing the new hot trend.

I don’t believe this trend will stop will money from all corners of the globe from flooding the US markets chasing the few quality AI companies.

The ultimate takeaway is that the best companies connected the generative artificial intelligence are at the beginning of a huge run in share price that will extend years into the future.

Don’t fight the trend – especially the biggest ones in the world.

Mad Hedge Technology Letter

June 26, 2024

Fiat Lux

Featured Trade:

(FISKER BLOWS UP)

(FSRNQ), (NVDA), (TSLA)

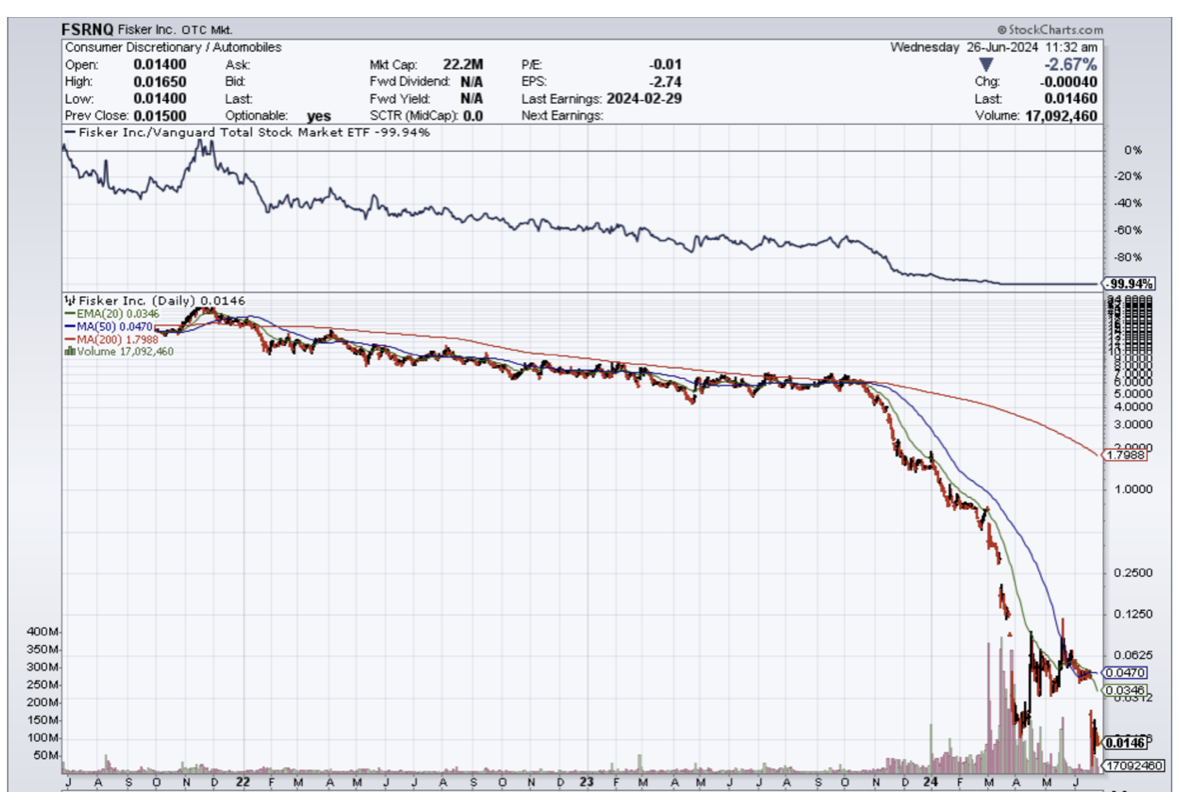

Fisker (FSRNQ) is bankrupt and I can tell you that I am not surprised.

The sushi has hit the fan.

The non-Nvidia (NVDA) tech firms minus big tech are really having a tough time staying liquid and dare I might say profitable.

Many already knew Fisker was in trouble.

They also have a terrible car which doesn’t help its case.

If Tesla (TSLA) is having a hard time selling EVs then imagine what it is like for Fisker to sell an utter clunker.

FSRNQ’s car has been coined as the worst EV on the market by many prominent bloggers.

Fisker management told us they might run out of cash before 2024 is over.

Definitely not shareholders like to hear in an industry that is looking more like a race to zero than an industry able to price itself at a premium.

I believe many car executives are ruing the fact of the multi-decade knowledge transfer to the Chinese about building quality cars.

How do we take tabs of the situation at Fisker?

It only sells one car called the Fisker Ocean electric SUV. Last year, around 10,000 of the SUVs were made but only about half had been delivered to customers.

In a recent interview with Automotive News, the company’s founder and CEO Henrik Fisker admitted that the Ocean had quality problems. He blamed the issues on software from different suppliers that worked poorly together and said they were being addressed through updates.

Worldwide sales of plug-in vehicles could rise 21% this year, which represents a smaller rise than the 35% increase in 2023.

The company listed between $500 million and $1 billion of assets, and between $100 million and $500 million of liabilities, in its petition filed in Delaware. The filing protects Fisker from creditors while it works out a plan to repay them.

While Fisker Ocean sport utility vehicle production started on schedule in November 2022, the first SUVs lacked basic features including cruise control. The California-based company told customers it would deploy capabilities it had promised them the following year, via over-the-air software updates.

Fisker produced 10,193 Oceans last year but delivered only 4,929 vehicles to customers.

Fisker follows a handful of other EV startups into bankruptcy, including Charge Enterprises, the installer of EV charging stations that filed for Chapter 11 protection in March. Other EV makers that have filed for bankruptcy include Lordstown Motors, Proterra and Electric Last Mile Solutions.

Anecdotally, EVs didn’t calculate properly how difficult it is to convince the 2nd wave of buyers.

For example, everyone in my family that will buy an EV has already bought one.

One Gen Z relative of mine swears he will never buy an EV because it doesn’t amount to more than a “toy car” with a battery that needs to be plugged in. He prefers a Ferrari or a Maserati where he can hear the engine roar. There is a high chance he will never be persuaded to buy an EV or if he does get persuaded, it will take 10-20 years for him to come around.

That is what EV makers face in bringing forward the next buyer.

Therefore, look at the bottom of the barrel EV production, they are all facing Chapter 11 and this is just the beginning.

Fisker’s share price peaked at around $30 per share in 2021 and now shares trade at $.02 per share. I would not buy the stock even at these levels.

Tesla’s halving of its share price also most likely means it is fairly priced for right now as we wait for a catalyst to send us either up or down.

The walls are closing in on the EV industry in the short-term and I advise readers to head to higher ground, let’s say the chip industry for a better crack at tech stocks.