Faced with an aging blockbuster pipeline and a competitive landscape where some of its rivals are sprinting ahead, AstraZeneca (AZN) is making a bold move - doubling down on Artificial Intelligence (AI).

This isn't just about keeping up with the Joneses (or in this case, their industry rivals); it's a calculated gamble with the potential to redefine drug discovery. The million-dollar question is: will this tech-savvy move send its shares soaring or just keep it in the running?

Let's address the elephants in the room of drug development. It's a long and winding road, with more dead ends than a maze in a horror movie. The usual grind? Spend ages finding a glimmer of hope in therapy targets and molecules, only for a paltry 21% to get the regulatory thumbs up after clinical trials.

So, you can bet your bottom dollar that if there’s a technology promising to up those odds and speed things up, companies will be jumping on the bandwagon faster than you can say "biotech boom."

And AstraZeneca? They are fully committing to AI, making significant waves in the field.

Case in point: their recent team-up with Absci, an AI drug discovery outfit. They're talking about developing a cancer-fighting antibody, with a potential payout of up to $247 million in milestone payments. If this pans out, it could be the first of many high-fives between the two.

But AstraZeneca's history with AI extends beyond this collaboration. Last September, they put up to $840 million on the line with Verge Genomics, aiming to tackle neurodegenerative diseases.

Add to that their work with Illumina (ILMN) and Nvidia (NVDA) in 2021 for some supercomputing firepower, and you've got a company that's serious about its AI game. They’ve even got a couple of AI-bred candidates in their pipeline, though it’s hush-hush on how those are faring.

And before you think it’s all about the new kids on the block, AstraZeneca has been rubbing elbows with Schrodinger (SDGR) since before 2020, working on making their biological medicine modeling sharper than a tack.

However, AstraZeneca is far from being the lone ranger in this new frontier.

Exscientia (EXAI) and Sanofi (SNY) are pairing up to take on COPD with an AI-driven approach. Meanwhile, BenevolentAI (BAIVF) played matchmaker between baricitinib and its new role as a COVID-19 treatment contender.

Over at Google’s (GOOGL) DeepMind, they’ve cooked up AlphaFold, an AI program adept at unraveling protein structures – a feat that’s akin to finding a map to hidden treasure in drug design.

And let's not forget the big guns. Pfizer (PFE) has teamed up with IBM’s (IBM) AI and supercomputing prowess, a partnership that’s been pivotal in accelerating the development of COVID-19 treatments like Paxlovid.

Novartis (NVS) is another key player, wielding AI to shave years off its drug development timeline, a strategy that could redefine the pace of pharmaceutical innovation.

Not to be outdone, Roche (RHHBY) is utilizing AI for a spectrum of tasks, from target identification to the virtual screening of molecules, illustrating the technology’s versatility in the drug discovery process.

Bayer (BAYRY) is also making a significant bet on AI to uncover new therapies, focusing on areas like immuno-oncology and cardiovascular diseases, areas with immense potential for groundbreaking treatments.

Vertex Pharmaceuticals (VRTX) and Johnson & Johnson (JNJ) are part of this evolving landscape as well, leveraging AI to enhance various stages of drug development. Their involvement underscores the widespread adoption of AI across different phases of the pharmaceutical process, from initial research to clinical trials.

Now, let’s go back to AstraZeneca. Best-case scenario? They cut their R&D budget, which was a cool $9.8 billion in 2022 while keeping the pedal to the metal on their clinical trials.

Worst case? Their AI bets don't pay off big time. But let's be real, with AI tech moving faster than a New York minute, that's looking less and less likely.

So, should you invest in AstraZeneca stocks right now? Not so fast. Jumping on the AI bandwagon isn't a golden ticket on its own.

Remember, everyone and their mother in big pharma is chasing the same AI dream. For now, it’s a case of watch, wait, and see how this fusion of AI and pharmaceuticals reshapes the landscape of drug discovery and development. Keep your ears to the ground – this is one race you don't want to miss.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-23 12:00:332024-01-23 11:15:28Pharma's AI Play: A Masterstroke or Misfire?

Stocks and firms tethered to artificial intelligence won’t always have a one-way joyride to profits.

The honest truth is that the road will be met with drawbacks some years and the sector will need time to digest the new developments.

Mainstream tech has made most people believe that AI can do no wrong in the short-term future.

There is a consensus that it’s the panacea for everything and anything.

The Magnificent 7 tech firms are priced for an AI boom and the hype is there, but it will take some time for AI to really filter into meaningful balance sheet development.

We are still in the beginning stages.

It’s not surprising that the Massachusetts Institute of Technology published a study that sought to address fears about AI replacing humans in a swath of industries and found that artificial intelligence can’t ACTUALLY replace the majority of jobs right now in cost-effective ways.

It’s important to note this report because much of AI has been celebrated with no mention of cost control or benefit versus the price or expenses incurred.

Any corporate tech will need to evaluate whether it’s worth gutting whole divisions to replace it with AI.

In many cases in early 2024, this type of strategy to a workforce could turn into an unmitigated disaster.

For instance, a new AI study found only 23% of workers, measured in terms of dollar wages, could be effectively supplanted. In other cases, because AI-assisted visual recognition is expensive to install and operate, humans did the job more economically.

The adoption of AI across industries accelerated last year after OpenAI’s ChatGPT and other generative tools showed the technology’s potential. Tech firms from Microsoft and Alphabet in the US to Baidu and Alibaba in China rolled out new AI services and ramped up development plans which could serve as a canary in the coal mine for things to come. Fears about AI’s impact on jobs have long been a central concern.

Computer vision is a field of AI that enables machines to derive meaningful information from digital images and other visual inputs, with its most ubiquitous applications showing up in object detection systems for autonomous driving or in helping categorize photos on smartphones.

The cost-benefit ratio of computer vision is most favorable in segments like retail, transportation, and warehousing.

The study was funded by the MIT-IBM Watson AI Lab and used online surveys to collect data on about 1,000 visually assisted tasks across 800 occupations. Only 3% of such tasks can be automated cost-effectively today, but that could rise to 40% by 2033 if data costs fall and accuracy improves.

When getting academic about the subject, many projections feel way too ambitious.

AI won’t take over the workforce in the next few years and will struggle to make inroads before 2030.

That doesn’t mean firms like Nvidia, AMD, Qorvo, and Broadcom will not sell AI-based chips promising better AI.

That doesn’t mean firms like Google, Apple, Microsoft, Amazon, and Meta won’t feel a small AI bump in revenue.

There certainly will be some changes, but wholesale transformation is a ways off.

I believe the AI hype has gotten too far over its skis.

Tech needs to slow down and make sure it’s properly implemented and the real effects will be seen after 2030.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-22 14:02:212024-01-22 15:18:21Take A Deep Breath With AI

Today, let's talk about something that's stirring up quite the buzz in the investment community, something that's not just about numbers and charts, but about potentially changing lives.

Now, I'm sure you've heard of Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Microsoft (MSFT), Meta Platforms (META), and Nvidia (NVDA). These tech titans aren't just playing around with gadgets and gizmos; they're digging deep into the world of knowledge to uncover stuff we didn't even know was missing. And let's be clear, this isn't just some fancy artificial intelligence show-off; it's bigger, much bigger.

But, recently, other industries aren’t letting tech have all the fun.

The pharma industry, led by stars like Moderna (MRNA), Eli Lilly (LLY), and Novo Nordisk (NVO), is on the brink of what I'd call medical miracles.

We're looking at treatments that might kick some serious diseases to the curb – illnesses that we thought were just part of the unlucky draw in the genetic lottery.

Admittedly, figuring out the real worth of these innovations is a bit like trying to nail jelly to the wall – traditional financial analysis scratches its head at this sort of thing.

But for those of you who don't mind a bit of a rollercoaster ride, investing in these themes could be as rewarding as finding a forgotten winning lottery ticket in your old jeans.

Let's chew on obesity for a second. It's a big deal, literally and figuratively. It's the root of all sorts of nasty stuff like heart disease and diabetes.

Here's where Lilly and Novo Nordisk come in, swinging like heroes with their weight-loss drugs. These aren't just your average diet pills; we're talking about drugs that could turn the tables on major illnesses and even some curveballs like Alzheimer’s and sleep apnea.

Lilly's stock has been on a joyride, up 77% in the past year. Sure, by the bookworms' metrics, it's overvalued, but if you ask me, those numbers are playing catch-up to what these drugs could really do.

For context, imagine if you had bought Amazon or Apple back when they were just a bookstore and a computer company. Looking at their history and trajectory, Lilly and Novo Nordisk could be cooking up something similar.

And with over 20 studies lined up in the next five years, Lilly's stock, hanging around $625, could jump to a cool $840 by 2028 if things go well.

Keep in mind that the obesity treatment market is huge, and I mean, really huge. We're talking over 100 million potential customers in the U.S. alone.

And get this: insurance companies, those penny pinchers, are likely to cover these drugs because they're cheaper than surgeries.

Getting down to the specifics with Lilly, they've been making waves in the weight loss market with Mounjaro, raking in a sweet $2.9 billion in just nine months. And with Zepbound, it's like they've hit the jackpot twice.

Still, it's not a solo race; Novo Nordisk is right there with Wegovy and Ozempic. The demand is so hot that there were shortages last year. Talk about being in high demand!

But here's where Lilly might just have the upper hand. Their molecule, tirzepatide, is like the Usain Bolt of weight loss drugs – up to three times more effective than Novo Nordisk’s semaglutide.

And with the market expected to balloon to $100 billion by 2030, we're just seeing the opening act of what could be a blockbuster show.

With all this obesity talk, it’s important to understand that Lilly is no one-trick pony. They've got a whole stable of drugs treating everything from lymphoma to ulcerative colitis. And with over 20 programs in phase 3 studies, they're not running out of steam anytime soon.

Plus, here's the cherry on top: Lilly isn't just about making money; they're sharing the love with a 15% hike in their dividend.

That means if you jump on the Lilly train by Feb. 15, you're in for a treat in early March.

So, is Lilly a solid bet for the long haul? It sure looks like it. The excitement around their weight loss treatments is just one piece of the puzzle.

With a variety of drugs in their arsenal and an impressive pipeline, Lilly isn't just a flash in the pan. Sure, there are the usual hiccups like patent expiries and pipeline flops, but with their portfolio, they look set to weather any storms and keep the growth party going. I suggest you buy the dip.

CrowdStrike (CRWD) is expensive by any metric, but so are other tech stocks like Nvidia (NVDA).

The trajectory of the stock still looks bright.

The cybersecurity company truly dishes out impressive growth numbers.

They are expected to grow sales by 39% over the next year and growth remains voluminous with no headwinds appear in the short term.

I’d be foolish not to mention one of the largest tailwinds in the tech sector in the form of defending and deterring digital malicious actors.

It’s real and capital is being allocated towards it.

The global cost of cybercrime is expected to double by 2028.

Sporting a market capitalization of $68 billion, CrowdStrike would need annualized returns of 18% to reach the $1 trillion club by 2040.

What do they mainly do?

Sifting through trillions of data points every week, CrowdStrike's single-agent, cloud-based cybersecurity platform grows more robust for each additional customer that joins its platform.

Quickly expanding its solutions from focusing primarily on endpoint protection (think laptops, printers, and servers) to becoming a complete security platform, CrowdStrike has grown from three security modules in 2016 to 27 today.

Each module provides a unique security solution and can be added by customers to fit their specific needs - all by relying upon just one agent, CrowdStrike's Falcon platform. The average number of agents on an endpoint today is 13 or more, so CrowdStrike's platform offers much-needed vendor consolidation for businesses looking to simplify their operations.

CrowdStrike is gradually becoming a one-stop shop for businesses' cybersecurity needs. Its growth potential and optionality seem almost boundless as it releases new modules tailor-made for its customers' desires. Look no further than two of its recent module advancements, each highlighting the company's ongoing shift toward becoming a complete security platform:

Falcon ID: CrowdStrike's identity protection and detection modules could become the company's next massive growth outlet. With 80% of global attacks stemming from exploited IDs, sales for these solutions grew from $7 million in annual recurring revenue (ARR) in Q3 of 2021 to over $200 million in Q2 of 2024.

Falcon Cloud: Bolstered by its recent acquisition of Bionic, which focuses on identifying and protecting items in the cloud, CrowdStrike now offers a complete cloud security solution. Growing its ARR from $106 million in Q4 of 2022 to nearly $300 million today, this cloud unit operates in a market expected to be worth over $32 billion by 2028.

Crowdstrike also landed an eight-figure deal from the federal government in its latest quarter. It counts less than 1% of the public sector as customers, so deals like this ignite a juicy channel of new revenue.

Thanks partly to its land-and-expand business model, CrowdStrike sees increasing profit margins for each additional module it sells to existing clients and each new customer it adds.

Who doesn’t like accelerating revenue and hypergrowth?

That’s what you get from CRWD.

The stock has been in overdrive pushing to new heights so I wouldn’t chase it right here.

It was only 365 days ago that the stock was at $101 and just touched $283.

That extraordinary rise is not the norm but is common with hyper-growth stocks.

It’s time to take the foot off the pedal and wait for a large dip which I do believe we will get.

That will be the next buying opportunity around $240 per share for CRWD.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-17 14:02:492024-01-17 16:23:05Grow With Crowdstrike

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHAT WILL KILL THIS MARKET)

(MSFT), (BA), (AMZN), (DAL), (V), (PANW), (CCJ), (TLT), (NVDA), (META), (TSLA), (GOOGL)

What if Goldilocks decided to hang around for a while? I’ve always been in favor of a long-term relationship.

It could be weeks. It could be months.

Certainly, the widely predicted New Year selloff has failed to materialize.

Failure to fall after the first week of 2024 has delivered a rally almost as ferocious as the one that launched in October. (NVDIA) up 15% in a week? Good thing I have a double position. Cameco (CCJ) up 25%? The market action was so positive that it rushed me into a rare 100% fully invested portfolio.

Which all begs the question of what WILL eventually kill this market. After all, nothing goes up forever.

It's very simple.

If the coming Fed interest rate cuts become so certain that companies start aggressively investing for the recovery NOW, there could be a problem. The headline Unemployment Rate never falls, inflation reaccelerates, and even the idea of interest rate cuts gets pushed off until 2025. That would thrust a dagger through the heart of the current rally post haste, which has been interest rate-driven from day one.

If there’s anyone who will save our bacon from this dire scenario, it is the legion of dour analysts out there who are perpetually behind the curve with their ultra-conservative earnings forecasts. That is scaring companies from expanding too quickly and is why every announcement delivers an upside surprise. That alone could provide enough of a drag on the economy to keep the Goldilocks scenario on track.

Watch Out Above!

If that is the case, then the ten positions I added last week to achieve a rare 100% invested portfolio should do pretty well, which has a strong technology bent. In the AI-dominated world, data is king. Let’s see who owns the data.

Microsoft (MSFT) – knows every keystroke you have executed since you bought your first PC in 1990.

Google (GOOGL) – knows every search you have performed since 2005 plus every YouTube video you have watched, even the X-rated ones (oops!).

Tesla (TSLA) – knows every function your car has performed since 2010 and has 12 videos of where you have been (double oops!).

Meta (META)– knows every keystroke you have performed on your social media accounts.

If all of this sounds scary, it should be. But it also means that while these stocks may be expensive relative to 2023 earnings, they are still in the bargain basement regarding 2024 and 2025 earnings. Buy everything on dips. Investors are adding to what they already own because it’s been working big time, including me.

On a completely different topic, Uranium is going nuclear again. Yellow cake, the fuel used by nuclear power plants, has seen prices up 45% since May. Before the Ukraine war, Russia produced 50% of the world’s nuclear fuel. Now it is banned due to sanctions. The US has announced the creation of a nuclear fuel stockpile.

Congress is about to vote on a ban on Russian fuel. France just announced the addition of 14 large nuclear plants. Oh, and it’s green.

Uranium prices endured a long nuclear winter starting with the Three Mile Island accident in 1979, followed by Chernobyl in 1986, and Fukushima in 2011. That time is now over, thanks to more advanced reactor designs and better risk control.

I used to collect Czech uranium glass, which emits a very low level of gamma radiation and glows in the dark under ultraviolet light. Time to collect some of Canadian uranium miner Cameco (CCJ) also … again.

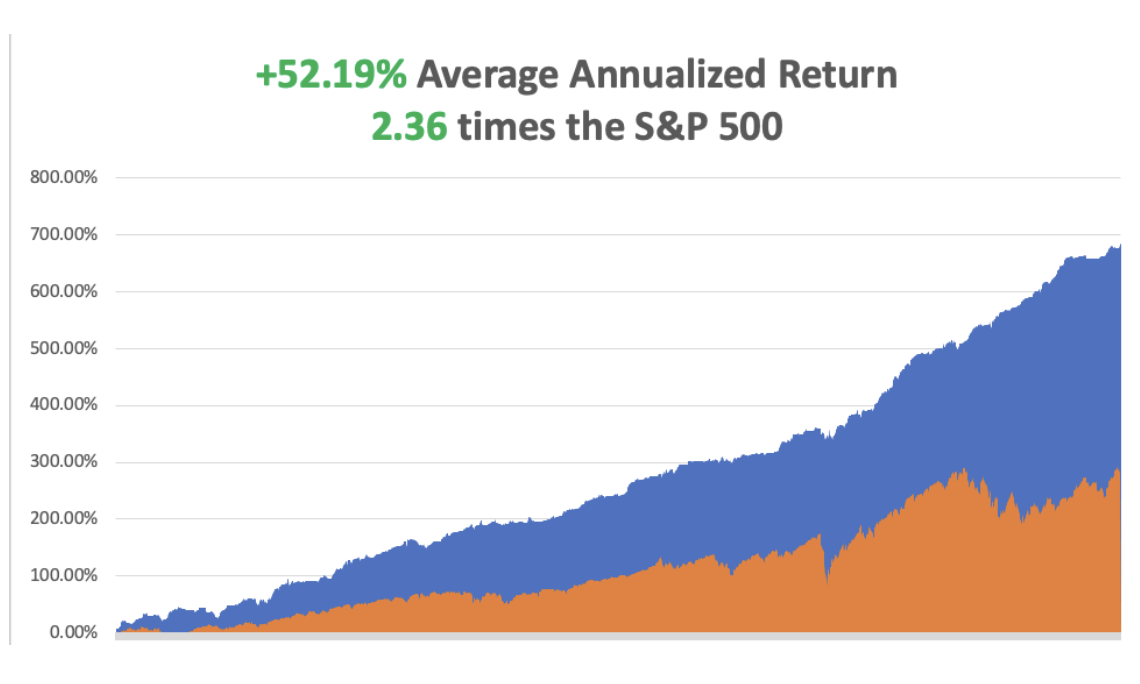

So far in January, we are up +6.19% with a 100% invested position. My 2024 year-to-date performance is also at +6.19%.The S&P 500 (SPY) is down -0.07%so far in 2024. My trailing one-year return reached +67.65% versus +37.82%for the S&P 500.

That brings my 15-year total return to +682.82%. My average annualized return has exploded to +52.19%,another new high.

Some 63 of my 70 trades last year were profitable in 2023.

I am going into 2024 with longs in (MSFT), (BA), (AMZN), (DAL), (V), (PANW), (CCJ), (TLT), and a double long in (NVDA).

FAA Grounds the Boeing 737 Max….Again, after a huge chunk of the fuselage fell off on a passenger flight which made an emergency landing in Portland. Dozens of the troubled aircraft were grounded. The move affects about 171 planes worldwide. The 737 Max is by far Boeing’s most popular aircraft and its biggest source of revenue. United Airlines is the biggest operator of the type followed by Alaska. Use any major dips to buy (BA) stock, which is facing a golden age.

NVIDIA Ramps Up its Graphics Cards. Nvidia is playing up its strength in consumer GPUs for so-called “local” AI that can run on a PC or laptop from home or an office. The new chip can be used to generate images on Adobe Photoshop’s Firefly generator to remove backgrounds in video calls, or even make games that use AI to generate dialogue. Buy (NVDA) on dips, as I did this last week.

Energy Prices Collapse Again, with Texas tea diving 4% to $70 on Saudi price cuts. This is despite steady buying from the US government for the SPR. The kingdom is moving to shortcut cheating by lesser OPEC members, as it usually does. If you throw good news in the market and it fails to go up, you sell it. Avoid (USO), (XOM), and (OXY).

Natural Gas Goes Ballistic, up 50% in three weeks. The 2026 $8-9 LEAPS I recommended over Christmas have already doubled. Expansion of export facilities to China is the reason, for accommodating more demand. BUY (UNG) on dips.

Mortgage Demand Soars by 10% in the first week of the year, and the next leg in the bull market for residential housing begins anew. Applications to refinance a home loan jumped 19% from the previous week and were 30% higher than the same week one year ago.

Consumer Price Index Flies, coming in at 0.3% for December instead of the anticipated 0.2%, a 3.4% annual rate. Fed rate cuts just got pushed back from March to June, where they belong. Used car and apparel prices get the blame. Car insurance was up a shocking 20% YOY. Go figure.

Bitcoin ETF’s SEC Approved, after a ten-year wait, potentially marking a market top. The SEC is still warning about market risks, even if the ETF sellers don’t. During the last crypto spike, there was an absence of cheap quality growth stocks. Now there is an abundance. Bitcoin prospered when we had a cash surplus and asset shortage. Now we have the opposite.

Global EV and Hybrid Sales Jump by 31% in 2023, compared to only 10% for internal combustion driven cars. Global sales of fully electric and plug-in hybrid vehicles (PHEVs) rose 31% in 2023, down from 60% growth in 2022, according to market research firm Rho Motion. For 2024, there are forecasts of global EV sales growth of between 25% and 30%. That’s really quite amazing given the weak 2023 global economy.

Microsoft Tops Apple, as the world’s most valuable publicly traded company, with a $3 trillion market cap. A huge lead in AI and a growing storage presence with Azure are the reasons. I’m long (MSFT) lower down.

US Budget Deficit Tops $500 Billion in Q1, starting October 1, 2023. But the frenetic price action, up a mind-blowing $19 in 2 ½ months proves the government isn’t borrowing too much money, it isn’t borrowing enough! There is a severe bond shortage in the marketplace. Never argue with Mr. Market as he is always right. Buy the (TLT) on dips, as I have.

Tesla to Halt Production in Germany, thanks to soaring shipping costs in the Red Sea. Tesla has been selling Berlin-made Model Ys to China via the Suez Canal. Shipping costs have doubled to $5,000 per container since October.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, January 15, markets are closed for Martin Luther King Day.

On Tuesday, January 16 at 8:30 AM EST,the New York Empire State Manufacturing Index will be released.

On Wednesday, January 17 at 2:00 PM, the Retail Sales are published.

On Thursday, January 18 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Building Permits for December.

On Friday, January 19 at 2:30 PM, the December University of Michigan Consumer Sentiment is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

Uranium Glass

As for me, when you make millions of dollars for your clients, you get a lot of pretty interesting invitations. $5,000 cases of wine, lunches on superyachts, free tickets to the Olympics, and dates with movie stars (Hi, Cybil!).

So it was in that spirit that I made my way down to the beachside community of Oxnard, California just north of famed Malibu to meet long-term Mad Hedge follower, Richard Zeiler.

Richard is a man after my own heart, plowing his investment profits into vintage aircraft, specifically a 1929 Travel Air D-4-D.

At the height of the Roaring Twenties (which by the way we are now repeating), flappers danced the night away doing the Charleston and the bathtub gin flowed like water. Anything was possible, and the stock market soared.

In 1925, Clyde Cessna, Lloyd Stearman, and Walter Beech got together and founded the Travel Air Manufacturing Company in Wichita, Kansas. Their first order was to build ten biplanes to carry the US mail for $125,000.

The plane proved hugely successful, and Travel Air eventually manufactured 1,800 planes, making it the first large-scale general aviation plane built in the US. Then, in 1929, the stock market crashed, the Great Depression ensued, aircraft orders collapsed, and Travel Air disappeared in the waves of mergers and bankruptcies that followed.

A decade later, WWII broke out and Wichita produced the tens of thousands of the small planes used to train the pilots who won the war. They flew B-17 and B-25 bombers and P51 Mustangs, all of which I’ve flown myself. The name Travel Air was consigned to the history books.

Enter my friend Richard Zeiler. Richard started flying support missions during the Vietnam War and retired 20 years later as an Army Lieutenant Colonel. A successful investor, he was able to pursue his first love, restoring vintage aircraft.

Starting with a broken down 1929 Travel Air D4D wreck, he spent years begging, borrowing, and trading parts he found on the Internet and at air shows. Eventually, he bought 20 Travel Air airframes just to make one whole airplane, including the one used in the 1930 Academy Award-winning WWI movie “Hells Angels.”

By 2018, he returned it to pristine flying condition. The modernized plane has a 300 hp engine, carries 62 gallons of fuel, and can fly 550 miles in five hours, which is far longer than my own bladder range.

Richard then spent years attending air shows, producing movies, and even scattering the ashes of loved ones over the Pacific Ocean. He also made the 50-hour round trip to the annual air show in Oshkosh, Wisconsin. I have volunteered to copilot on a future trip.

Richard now claims over 5,000 hours flying tailwheel aircraft, probably more than anyone else in the world. Believe it or not, I am also one of the few living tailwheel-qualified pilots in the country left. Yes, antiques are flying antiques!

As for me, my flying career also goes back to the Vietnam era as well. As a war correspondent in Laos and Cambodia, I used to hold Swiss-made Pilatus Porter airplanes straight and level while my Air America pilot friend was looking for drop zones on the map, dodging bullets all the way.

I later obtained a proper British commercial pilot license over the bucolic English countryside, trained by a retired Battle of Britain Spitfire pilot. His favorite trick was to turn off the fuel and tell me that a German Messerschmidt had just shot out my engine and that I had to land immediately. He only turned the gas back on at 200 feet when my approach looked good. We did this more than 200 times.

By the time I moved back to the States and converted to a US commercial license, the FAA examiner was amazed at how well I could do emergency landings. Later, I added on additional licenses for instrument flying, night flying, and aerobatics.

Thanks to the largesse of Morgan Stanley during the 1980s, I had my own private twin-engine Cessna 421 in Europe for ten years at their expense where I clocked another 2,000 hours of flying time. That job had me landing on private golf courses so I could sell stocks to the Arab Prince owners. By 1990, I knew every landing strip in Europe and the Persian Gulf like the back of my hand.

So, when the first Gulf War broke out the following year, the US Marine Corps came calling at my London home. They asked if I wanted to serve my country and I answered, “Hell, yes!” So, they drafted me as a combat pilot to fly support missions in Saudi Arabia.

I only got shot down once and escaped with a crushed L5 disk. It turns out that I crash better than anyone else I know. That’s important because they don’t let you practice crashing in flight school. It’s too expensive.

My last few flying years have been more sedentary, flying as a volunteer spotter pilot in a Cessna-172 for Cal Fire during the state’s runaway wildfires. As long as you stay upwind, there’s no smoke. The problem is that these days, there is almost nowhere in California that isn’t smokey. By the way, there are 2,000 other pilots on the volunteer list.

Eventually, I flew over 50 prewar and vintage aircraft, everything from a 1932 De Havilland Tiger Moth to a Russian MiG 29 fighter.

It was a clear, balmy day when I was escorted to the Travel Air’s hanger at Oxnard Airport. I carefully prechecked the aircraft and rotated the prop to circulate oil through the engine before firing it up. That reduced the wear and tear on the moving parts.

As they teach you in flight school, better to be on the ground wishing you could fly than be in the air wishing you were on the ground!

I donned my leather flying helmet, plugged in my headphones, received a clearance from the tower, and was good to go. I put on max power and was airborne in less than 100 yards. How do you tell if a pilot is happy? He has engine oil all over his teeth. After all, these are open-cockpit planes.

I made for the Malibu coast and thought it would be fun to buzz the local surfers at wave top level. I got a lot of cheers in return from my fellow thrill seekers.

After a half hour of low flying over elegant sailboats and looking for whales, I flew over the cornfields and flower farms of remote Ventura County and returned to Oxnard. I haven’t flown in a biplane in a while and that second wing really put up some drag. So, I had to give a burst of power on short finals to make the numbers. A taxi back to the hangar and my work there was done.

There are old pilots and there are bold pilots, but there are no old, bold pilots. I can attest to that.

Richard’s goal is to establish a new Southern California aviation museum at Oxnard airport. He created a non-profit 501 (3)(c), the Travel Air Aircraft Company, Inc. to achieve that goal, which has a very responsible and well-known board of directors. He has already assembled three other 1929 and 1930 Travel Air biplanes as part of the display.

The museum’s goal is to provide education, job training, restoration, maintenance, sightseeing rides, film production, and special events. All donations are tax-deductible. To make a donation, please email the president of the museum, my friend Richard Conrad at rconrad6110@gmail.com

Who knows, you might even get a ride in a nearly 100-year-old aircraft as part of a donation.

To watch the video of my joyride, please click here.

Where I Go My Kids Go

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/01/Joh-Thomas-pilot.png8121080april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-16 09:02:062024-01-16 11:43:18The Market Outlook for the Week Ahead, or What Will Kill this Market

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.