Global Market Comments

August 16, 2021

Fiat Lux9

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MY REVOLUTIONARY NEW STRATEGY,

(SPY), (TLT), (NVDA), (ROKU), (HOOD), (GS), (JPM)

Global Market Comments

August 16, 2021

Fiat Lux9

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MY REVOLUTIONARY NEW STRATEGY,

(SPY), (TLT), (NVDA), (ROKU), (HOOD), (GS), (JPM)

Friday saw the stock market’s lowest volume day of the year, and shares rose almost every day last week to new all-time highs.

The way this usually ends is that the slow grind explodes into a high-volume spike marking an interim market top. That makes new investment now extremely risky.

August usually markets the best buying opportunity of the year with a cataclysmic selloff. Remember the 2010 flash crash, down 1,100 points in two hours? So far, no cigar.

I have tons of people asking me what to buy right now. That is usually another market-topping indicator. I tell them to keep their cash. Cash is a position. A dollar at a market top is worth $10 at a market bottom.

Under an index that is making excruciatingly slow gains are constant sector rotations bring pretty dramatic moves. Play those dramatic moves.

May saw money suddenly shift into tech stocks, with the best, like NVIDIA (NVDA) leaping 56%.

The day the ten-year US Treasury yield (TLT) bottomed at 1.10%, tech went back to sleep. While big tech ground sideways, small tech brought more heart-rending downside moves, such as the 27% plunge in Roku (ROKU).

In the meantime, financials and commodities have moved to the fore. Goldman Sachs (GS) melted up 20% off of blockbuster earnings, while Freeport McMoRan popped 26%, thanks to a Chilean copper union strike.

Let me propose a revolutionary new investment strategy to you. It’s called “buy low, sell high.” Everybody talks about it but actually executes the opposite.

I employ this money-making ploy through my “barbell” strategy, with equal weightings in technology and domestic recovery stocks like financials, industrials, and commodities.

It's quite simple. You just sell whatever has just delivered the most recent spectacular upside gains and roll that money into what has recently become ignored, cheap, and out of favor.

It is a market approach that is really devoid of the thought process.

All eyes will be on Jackson Hole, Wyoming next week, the annual meeting of the world’s top central bankers. That is when we get the next hint about the intentions of the Federal Reserve as to, not "if", but "when" they reduce quantitative easing.

You would think that a 6.5% GDP growth rate and a 5.4% inflation rate would do it, but these days, nothing is certain. A hot jobs report in September would do it for sure.

We may have to wait until then before we see any serious move in stocks and a return of volatility (VIX). In the meantime, catch up on reading your research, pay your bills, and work on your golf swing.

Bitcoin staged a recovery for the ages, rallying 55% in two weeks. The “battle of $30,000” is over and the cryptocurrency won. It really is becoming too big to fail. I might have to do something about that.

July Inflation Read at a hot 5.4%, but core inflation showed a small decline. In June, used car prices accounted for a third of the total price increases, but last month, it was zero. So far, there is no move in rents, but it’s coming. All Fed eyes will remain laser-focused on this number.

Taper talk is back! With the ballistic increase in the July Nonfarm Payroll report and the 2 ½ point dive in the bond market. I think the top is in for finds and the bottom for long term rates. It means tech stocks will lag from now, while interest rate sensitives like banks, brokers, and fund managers will lead. Buy (JPM), (MS), (V), and (GS) on dips.

US Budget Deficit hits a record $302 Billion in July. Covid benefits are remaining high, while tax revenues are lagging YOY. Keep selling those (TLT) rallies. The generational crash may have just begun.

Fed’s Rosengren Says QE is not creating jobs, causing bonds to drop a full point in the after-market. No kidding. I have been arguing that our nation’s central bank has been pushing on a string all year. Atlanta Fed governor Bostic couldn’t agree more. Time for more action than words?

Gold Hits four-month low, breaking key support. Bitcoin is clearly stealing its thunder, which has risen by 50% in two weeks. If you’re considering gold, go take a long nap first.

Oil dives on delta surge, off $9, or 12% in a week, the lowest in three weeks. Delta is now rampaging throughout China, the world’s largest consumer of Texas tea., putting $63 in play.

Weekly Jobless Claims hit 375,000, down 12,000 on the week. Moving in the right direction but still incredibly high.

Berkshire Hathaway announces solid earnings, but scales back share buybacks at these elevated levels. Oracle of Omaha Warren Buffett bought back $6 billion of his own stock in Q2, leaving him with a staggering $144 billion in cash. Almost no stocks meet Buffett’s value standards in the current environment. Buy (BRKB) on dips. It’s a high-class problem to have.

Ed Yardeni is bullish, along with David Kostin, and is the only manager who comes close to my own $475 target for the (SPY) by the end of the year. The U.S. economy will be in nominal terms around 8% higher this year than pre-pandemic 2019. Sales for the S&P 500 companies will be 15% higher and earnings will be 34% higher. That is a representation of the operating leverage that exists in so many companies. The Roaring Twenties lives!

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +4.86% in July. My 2021 year-to-date performance appreciated to 74.07%. The Dow Average was up 16.00% so far in 2021.

I stuck with three positions, a long in (JPM) and a double short in the (TLT), all of which expire on Friday. My double short in the (SPY) punched me in the nose, forcing me to stop out for losses when I hit the lowest strike prices.

I then jumped into a very deep in-the-money call spread in Robinhood (HOOD) made possible only by the stock’s astronomically high volatility. Its 44% drop helped too. I also added a third short in the bond market.

That leaves me 30% in cash. I’m keeping positions small as long as we are at extreme overbought conditions.

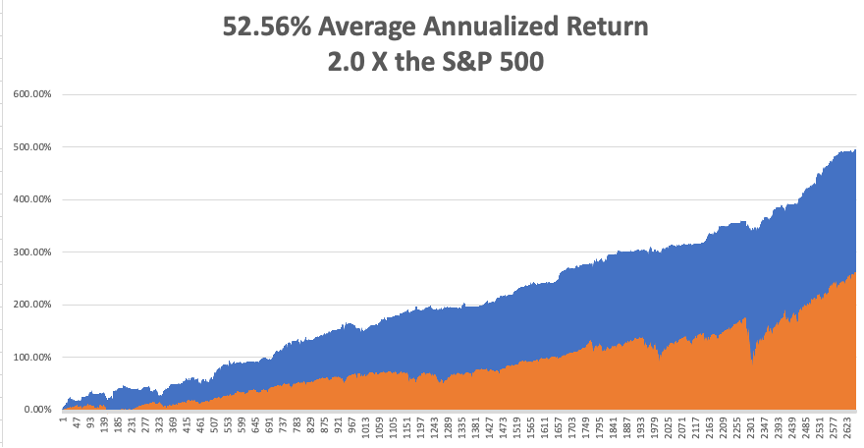

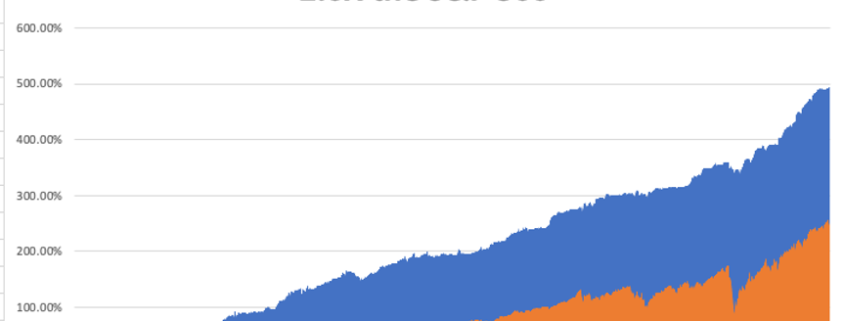

That brings my 11-year total return to 496.62%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 12.56%, easily the highest in the industry.

My trailing one-year return retreated to positively eye-popping 106.69%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 36.7 million and rising quickly and deaths topping 622,000, which you can find here at https://coronavirus.jhu.edu.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 16 at 7:00 AM, the New York Empire State Manufacturing Index is out.

On Tuesday, August 17 at 7:30 AM, US Retail Sales for July are published.

On Wednesday, August 18 at 5:30 AM, the Housing Starts for July are printed. At 2:00 PM, the minutes from the last FOMC are released.

On Thursday, August 19 at 8:30 AM, Weekly Jobless Claims are announced. Square (SQ) reports.

On Friday, August 20 at 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, upon graduation from high school in 1970, I received a plethora of scholarships, one of which was for the then astronomical sum of $300 in cash from the Arc Foundation.

By age 18, I had hitchhiked in every country in Europe and North Africa, more than 50. The frozen wasteland of the North and the Land of Jack London beckoned.

After all, it was only 4,000 miles away. How hard could it be? Besides, oil had just been discovered on the North Slope and there were stories of abundant high-paying jobs.

I started hitching to the Northwest, using my grandfather’s 1892 30-40 Krag & Jorgenson rifle to prop up my pack and keeping a Smith & Wesson .38 revolver in my coat pocket. Hitchhikers with firearms were common in those days and they always got rides. Drivers wanted the extra protection.

No trouble crossing the Canadian border either. I was just another hunter.

The Alcan Highway started in Dawson Creek, British Columbia, and was built by an all-black construction crew during the summer of 1942 to prevent the Japanese from invading Alaska. It had not yet been paved and was considered the great driving challenge in North America.

The rain started almost immediately. The legendary size of the mosquitoes turned out to be true. Sometimes, it took a day to catch a ride. But the scenery was magnificent and pristine.

At one point, a Grizzley bear approached me. I let loose a shot over his head at 100 yards and he just turned around and lumbered away. It was too beautiful to kill.

I passed through historic Dawson City in the Yukon, the terminus of the 1898 Gold Rush. There, abandoned steamboats lie rotting away on the banks, being reclaimed by nature. The movie theater was closed but years later was found to have hundreds of rare turn-of-the-century nitrate movie prints frozen in the basement, a true gold mine.

Eventually, I got a ride with a family returning to Anchorage hauling a big RV. I started out in the back of the truck in the rain, but when I came down with pneumonia, they were kind enough to let me move inside. Their kids sang “Raindrops keep falling on my head” the entire way, driving me nuts. In Anchorage, they allowed me to camp out in their garage.

Once in Alaska, there were no jobs. The permits required to start the big pipeline project wouldn’t be granted for four more years. There were 10,000 unemployed.

The big event that year was the opening of the first McDonald’s in Alaska. To promote the event, the company said they would drop dollar bills from a helicopter. Thousands of homesick showed up and a riot broke out, causing the stand to burn down. It was rumored their burgers were made of moose meat anyway.

I made it all the way to Fairbanks to catch my first sighting of the wispy green contrails of the northern lights, impressive indeed. Then began the long trip back.

I lucked out catching an Alaska Airlines promotional truck headed for Seattle. That got me free ferry rides through the inside passage. The driver wanted the extra protection as well. The gaudy, polished tourist destinations of today were back then pretty rough ports inhabited by tough, deeply tanned commercial fishermen and loggers who were heavy drinkers always short of money. Alcohol features large in the history of Alaska.

From Seattle, it was just a quick 24-hour hop down to LA. I still treasure this trip. The Alaska of 1970 no longer exists, as it is now overrun with summer tourists. It now has more than one McDonald’s. And with runaway global warming, the climate is starting to resemble that of California than the polar experience it once was.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Alcan Highway Midpoint

The Alaska-Yukon Border in 1970

Mad Hedge Technology Letter

August 13, 2021

Fiat Lux

Featured Trade:

(ARE THE WHEELS FALLING OFF THE CHIP INDUSTRY?)

(MU), (SK HYNIX), (NVDA)

Is the chip industry about to freeze over?

Signs are creeping in of a cyclical downturn in memory chips starting in the first quarter of 2022.

This is all brought about by cycle indicators signaling that we are shifting out of 'midcycle' to 'late-cycle' for the first time since 2019 and this phase change has historically meant a challenging backdrop for forward returns.

The investments have been pouring in from chip companies to build more foundries and to improve chip performance.

Incrementally, new supply will eventually come online to address the giant chip shortage that many industries are grappling with.

However, I will say that whispers of an imminent collapse in the chip dynamics are exaggerated at best.

I don’t believe that the next cyclical downturn begins from Q1 2022 exacerbated by inventory builds.

We are still far from that happening even if the chip environment has tensed up more so now.

Micron (MU) has said that the order-filling time for chipmakers now exceeds 20 weeks.

The order-filling time represents the period from ordering a semiconductor to receiving it. That metric added on more than eight days in July, putting the total at 20.2 weeks.

Businesses from automakers to consumer-electronics companies are suffering from the chip shortage. Carmakers are expected to miss out on $100 billion in sales due to the lack of critical components.

Another industry-wide headwind is the UK's possible blocking of Nvidia’s (NVDA) planned $40 billion acquisition of Arm Holdings over national security issues.

A possible downturn in the chip cycle would also mean heavyweight South Korean memory-chip maker SK Hynix will severely underperform as well.

There are forecasts of contract prices for memory chips used in personal computers that decline by as much as 5% in the December quarter from the September quarter.

The PC market is only 20% of the DRAM market. Smartphone DRAM accounts for 40% of the market and server DRAM is 30% of the market. Miscellaneous device markets make up the remaining 10%.

Therefore, it is safe to say that not all the eggs are in one basket.

However, an analyst downgrade has set the tone for all makers of dynamic random access memory chips and puts the onus on the entrenched to prove the supposed downturn is not the case.

A world in which all relevant companies have hoarded chips because of the fear of not be able to source the right chips would be a transitory issue.

I don’t see demand falling off a cliff.

Many of these DRAM companies have moats around their business models and the case of businesses snapping up a high volume of chips and their inventories peaking out is a problem many companies would love to have.

As we progress into 2022, companies will start to plan their next iterations of devices and gadgets, and no doubt the next generation will need at least 50% more high-performing chips compared to the last version.

The pricing pressure is almost analogous to what happened with lumber prices and builders started buying at whatever prices during the short squeeze earlier this year.

This doesn’t mean the housing industry is doomed, but I understand it more as moderating prices will be a tailwind for the overall health of the industry.

Chips are famous for that boom and bust dynamic.

The price gains in chips cannot be absorbed in the same rate and as prices moderate, companies will start to look at acquiring the next batch of chips even if inventory is high.

In the short term, chip stocks are on course for a short correction that could take around a quarter to digest, but I highly doubt this will last into next year.

The 30,000-foot view shows us that many chip firms are enjoying record demand for their best chips driven by cloud customers’ capital expenditures, and even upside from the popularity of cryptocurrency-related chip products.

Demand is everywhere to be found.

The leading-edge manufacturers will take this dip in stride and adjust for the new environment in 2022.

Lower pricing expectations is something that nobody wants to hear as a chip CEO and absorbing a more challenging pricing environment into 4Q does not beat price spikes.

It gets lost that DRAM prices increased 35% over the past two quarters, with expectations for a “further modest increase” through the end of this year.

The industry can afford a little reversion to the mean pricing and shareholders will mostly stay in these stocks long term.

I understand that this dip in chip shares like Micron caused by moderation of pricing power translates into a great entry point into the stock for new buyers.

Quite quickly will investors start to shrug off this negative element to the industry and pile back into premium names or just stick with Nvidia who doesn’t sell DRAM chips.

Global Market Comments

August 5, 2021

Fiat Lux

Featured Trade:

(THE NEW AI BOOK THAT INVESTORS ARE SCRAMBLING FOR),

(GOOG), (FB), (AMZN), MSFT), (BABA), (BIDU),

(TENCENT), (TSLA), (NVDA), (AMD), (MU), (LRCX)

A better headline for this piece would be “The Future of You,” as artificial intelligence is about to become so integral to your work, your investment portfolio, and even your very existence that you won’t be able to live without it, quite literally.

Well, do I have some great news for you. A blockbuster book about the state of play on all things AI will be released on September 25, and I managed to obtain and read an advanced copy. It is entitled: AI Superpowers: China, Silicon Valley, and the New World Order by Dr. Kai-Fu Lee.

The bottom line: The future is even more unbelievable than you remotely imagined. We are at the very early days of this giant megatrend, and the investment opportunities will be nothing less than spectacular.

And here is a barn burner. The price of AI is dropping fast as hundreds of thousands of new programmers pour into the field. Those $10 million signing bonuses are about to become a thing of the past.

Dr. Lee is certainly someone to take seriously. He obtained one of the first Ph.D.’s in AI from Carnegie Mellon University. He was the president of Google (GOOG) China and put in stints at Microsoft (MSFT) and Apple (AAPL). Today, he is the CEO of Sinovation Ventures, the largest AI venture capital firm in China, and is a board director of Alibaba (BABA).

AI is nothing more than deep learning, or super pattern recognition. Dr. Lee dates the onset of artificial intelligence to 1952, when an IBM mainframe computer learned to play checkers and beat human opponents. By 1955, it learned to develop strategies on its own.

Dr. Lee sees the AI field ultimately divided into two spheres of dominance, the U.S. and China. No one else is devoting a fraction of the resources needed to become a serious player. The good news is that Russia and Iran are nowhere in the game.

While the U.S. dominates in the original theory and algorithms that founded AI, China is about to take the lead in applications. It can do this because it has access to mountains of data that dwarf those available in America. China processes three times more mobile phones, five times more Internet customers, 10 times more eat-out orders, and 50 times more mobile transactions. In a future where data is currency, this is huge.

The wake-up call for China in applications took place two years ago when U.S. and Korean AI programs beat grandmasters in the traditional Chinese game of Go. Long a goal of AI programmers, this great leap forward took place 20 years earlier than had been anticipated. This created an AI stampede in the Middle Kingdom that led to the current bubble.

The result has been applications that are still in the realm of science fiction in the U.S. The Chinese equivalent of eBay (EBAY), Taobao, doesn’t charge fees because its customer base is so big it can remain profitable on ad revenues only. Want to be more beautiful in your selfies sent to friends? A Chinese app will do that for you, Beauty Plus.

The Chinese equivalent of Yelp, Dianping, has 600,000 deliverymen on mopeds. The number of takeout meals is so vast that it has been able to drop delivery costs from $6 a meal to 60 cents. As a result, traditional restaurants are dying out in China.

Teachers in Chinese schools no longer take attendance. Students are checked off when they enter the classroom by facial recognition software. And heaven help you if you jaywalk in a Chinese city. Similar software will automatically issue you a citation with a fine and send it to your home.

Credit card fraud is actually on the decline in China as dubious transactions are blocked by facial matching software. The bank simply calls you, asks you to look into your phone, takes your picture, and then matches it with the image they have on file.

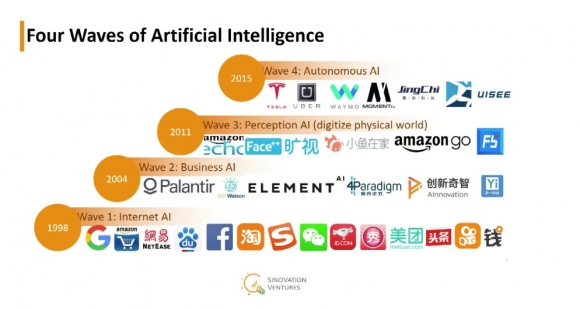

Dr. Lee sees AI unfolding in four waves, and there are currently companies operating in every one of these (see graph below):

1) Internet AI

The creation of black boxes and specialized algorithms opened the door to monetizing code. This was the path for today’s giants that dominate online commerce today, Google (GOOG), Amazon (AMZN), JD.com (JD), and Facebook (FB). Alibaba (BABA), Baidu (BIDU), and Tencent followed.

2) Business AI

Think big data. This is the era we just entered, where massive data from online customers, financial transactions, and health care led to the writing of new algorithms that maximize profitability. Suddenly, companies can turn magic knobs to achieve desired goals, such as stepping up penetration or monetization.

3) Perception AI

Using trillions of sensors worldwide, analog data on any movement, facial expression, sound, and image are converted into digital data, and then mined for conclusions by more advanced algorithms. Cameras are suddenly everywhere. Amazon’s Alexa is the first step in this process, where your conversations are recorded and then mined for keywords about your every want and desire.

Think of autonomous fast food where you walk in your local joint and it immediately recognizes you, offers you your preferred dishes, and then auto bills your online account for your purchase. Amazon has already done this with a Whole Foods store in Seattle.

4) Autonomous AI

Think every kind of motion. AI will get applied to autonomous driving, local shuttles, factory forklifts, assembly lines, and inspections of every kind. Again, data and processing demand take an enormous leap upward. Tesla (TSLA), Waymo (GOOG), and Uber are already very active in this field.

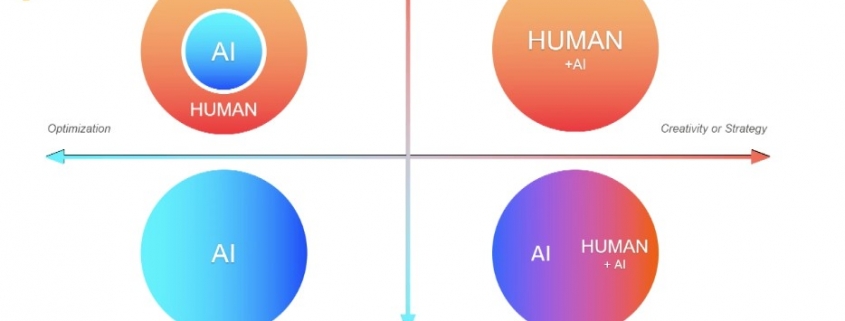

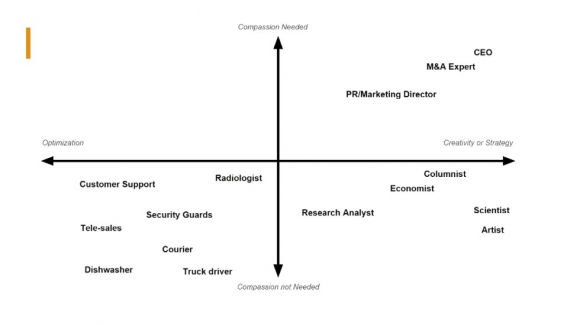

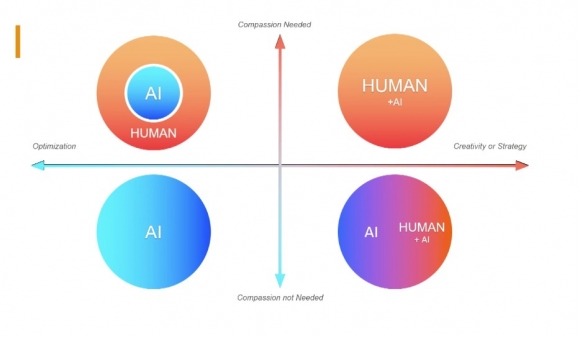

The book focuses a lot on the future of work. Dr. Lee creates a four-part scatter chart predicting the viability of several types of skills based on optimization, compassion, creativity, and strategy (see below).

If you are a truck driver, in customer support, or a dishwasher, or engage in any other repetitive and redundant profession your outlook is grim. If you can supplement AI, such as a CEO, economist, or marketing head you’ll do fine. People who can do what AI can’t, such as teachers and artists, will prosper.

The Investment Angle

There have been only two ways to invest in AI until now. You can buy shares in any of the seven giants above, whose shares have already risen for 100- or 1,000-fold.

You can invest in the nets and bolts parts providers, such as NVIDIA (NVDA), Advanced Micro Devices (AMD), Micron Technology (MU), and Lam Research (LRCX), which provide the basic building blocks for the Internet infrastructure.

Fortunately for our paid subscribers, the Mad Hedge Trade Alert Service caught all of these very early.

What’s missing is the “in-between companies,” which are out of your reach because they are locked up in university labs or venture capital funds. Many of these never see the light of day as public companies because they get taken over by the tech giants above. It’s effectively a closed club that won’t let outsiders in. It’s a dilemma that vexes any serious technology investor.

When quantum computing arrives in a decade, you can take all the functionality above and multiply it by a trillion-fold, while costs drop a similar amount. That’s when things really get interesting. But then, I’ve seen trillion-fold increases in technology before.

I hope I live to see another.

Global Market Comments

July 30, 2021

Fiat Lux

Featured Trade:

(JULY 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CRSP), (TLT), (TBT), (BABA), (BIDU), (FXI), (RAD), (TSLA), (NASD), (NKLA), (NIO), (INTC), (MU), (NVDA), (AMD), (TSM), (VXX), (XVZ), (SVXY), (FCX), (ROM), (SPG)

July 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the July 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV.

Q: What is your plan with the (SPY) $443-$448 and the $445/450 vertical bear put spreads?

A: I’m going to keep those until we hit the lower strike price on either one and then I’ll just stop out. If the market doesn’t go down in August, then we are going straight up for the rest of the year as the earnings power of big tech is now so overwhelming. Sorry, that’s my discipline and I’m sticking to it. Usually, what happens 90% of the time when we go through the strike, and then go back down again by expiration for a max profit. But the only way to guarantee that you'll keep your losses small is by stopping out of these things quickly. That’s easy to do when you know that 95% of the time the next trade alert you’ll get is a winner.

Q: Are you still expecting a 5% correction?

A: I am. I think once we get all these great earnings reports out of the way this week, we’re going to be in for a beating. I just don't see stocks going straight up all the way through August, so that’s another reason why I'm hanging on to my short positions in the S&P 500 (SPY).

Q: What’s the best way to play CRISPR Therapeutics (CRSP) right now?

A: That is with the $125-$130 vertical bull call spread LEAPS with any maturity in 2022. We had a run in (CRSP) from $100 up to $170 and I didn’t take the damn profit! And now we’ve gone all the way back down to $118 again. Welcome to the biotech space. You always take the ballistic moves. Someday I should read my own research and find out why I should be doing this. For those who missed (CRSP) the last time, we are one proprietary drug announcement, one joint venture announcement, or one more miracle cure away from another run to $170. So that will probably happen in the next year, you get the $125-$130 call spread, and you will double your money easily on that.

Q: I’m down 40% on the United States Treasury Bond Fund (TLT) January $130-$135 vertical bear put spread LEAPS. What would you do?

A: Number one, if you have any more cash I would double up. Number two, I would wait, because I would think that starting from the Fall, the Fed will start to taper; even if they do it just a little bit, that means we have a new trend, the end of the free lunch is upon us, and the (TLT) will drop from $150 down to $132 where it was in March so fast it will make your head spin. I'm hanging onto my own short position in (TLT). If you are new to the (TLT) space and you want some free money, put on the January 2020 $150-$155 vertical bear put spread now will generate about a 75% return by the January 21, 2022 options expiration. I just didn't figure on a 6.5% GDP growth rate generating a 1.1% bond yield, but that’s what we have. I'm sorry, it’s just not in the playbook. Historically, bonds yield exactly what the nominal GDP growth rate is; that means bonds should be yielding 6.50% now, instead of 1.1%. They will yield 6.5% in the future, but not right now. And that's the great thing about LEAPS—you have a whole year or 6 months for your thesis to play out and become right, so hang on to those bond shorts.

Q: Do you have any ideas about the target for Facebook (FB) by the end of the year?

A: I would say up about 20% from current levels. Not only from Facebook but all the other big tech FANGS too. Analysts are wildly underestimating the growth of these companies in the new post-pandemic world.

Q: Do you think the worst of the pandemic will be over by September?

A: Yes, we will be back on a downtrend by September at the latest and that will trigger the next leg up in the bull market. Delta with its great infectious and fatality rates is panicking people into getting shots. The US government is about to require vaccinations for all federal employees and that will get another 5 million vaccinated. Americans have the freedom to do whatever they want but they don’t have the freedom to kill their neighbors with fatal infections.

Q: What should I do with my China (BABA), (BIDU), (FXI) position? Should I be doubling down?

A: Not yet, and there’s no point in selling your positions now because you’ve already taken a big hit, and all the big names are down 50% from the February high. I wouldn't double down yet because you don’t know what's happening in China, nobody does, not even the Chinese. This is their way of addressing the concentration of the wealth in the top 1% as has happened here in the US as well. They’re targeting all the billionaire stocks and crushing them by restricting overseas flotations and so on, so it ends when it ends, and when that happens all the China stocks will double; but I have absolutely no idea when that's going to happen. That being said, I have been getting phone calls from hedge funds who aren’t in China asking if it's time to get in, so that's always an interesting precursor.

Q: What happened to the flu?

A: It got wiped out by all the Covid measures we took; all the mask-wearing, social distancing, all that stuff also eliminates transmission of flu viruses. Viruses are viruses, they’re all transmitted the same way, and we saw this in the Rite Aid (RAD) earnings and the 55% drop in its stock, which were down enormously because their sales of flu medicines went to zero, and that was a big part of their business. I didn’t get the flu last year either because I didn’t get Covid; I was extremely vigilant on defensive measures in the pandemic, all of which worked.

Q: Why would the Fed taper or do much of anything when Powell wants to be reappointed in February 2022?

A: I don’t think he is going to get reappointed when his four-year term is up in early 2022. His policies have been excellent, but never underestimate the desire of a president to have his own man in the office. I think Powell will go his way after doing an outstanding job, and they will appoint another hyper dove to the position when his job is up.

Q: What are your thoughts on the Chinese electric auto company Nio competing here in the U.S.?

A: They will never compete here in the U.S. China has actually been making electric cars longer than Tesla (TSLA) has but has never been able to get the quality up to U.S. standards. Look what happened to Nikola (NKLA) who’s founder was just indicted. Avoid (NIO) and all the other alternative startup electric car companies—they will never catch up with Tesla, and you will lose all your money. Can I be any clearer than that?

Q: You recently raised the ten-year price target up for the Dow Average from 120,000 to 240,000. What is Nasdaq's target 10 years out?

A: I would say they’re even higher. I think Nasdaq (NASD) could go up 10X in 10 years, from 14,000 to 140,000 because they are accounting for 50% of all earnings in the U.S. now, and that will increase going forward, so the stocks have to go ballistic.

Q: What do you think of Intel (INTC)?

A: I don’t like it. They had a huge rally when they fired their old CEO and brought in a new one. There was a lot of talk on reforming and restructuring the company and the stock rallied. Since then, the market has started insisting on performance which hasn’t happened yet so the stock gave up its gains. When it does happen, you’ll get a rally in the stock, not until then, and that could be years off. So I'd much rather own the companies that have wiped out Intel: (MU), (NVDA), (AMD), and (TSM).

Q: When you do recommend buying the Volatility Index (VIX), do you recommend buying the (VIX) or the (VXX)?

A: You can only buy the VIX in the futures market or through ETFs and ETNs, like the (VXX), the (XVZ), and the (SVXY), or options on these. I would be very careful in buying that because time decay is an absolute killer in that security, and that's why all the professionals only play it from the short side. That's also why these spikes in prices literally last only hours because you have professionals hammering (VIX). Somebody told me once that 50% of all the professional traders in the CME make their living shorting the (VIX) and the (VXX). So, if you think you’re better than the professionals, go for it. My guess is that you’re not and there are much better ways to make money like buying 6-to-12-month LEAPS on big tech stocks.

Q: Can the Delta variant get a bigger pullback?

A: Yes. I expect one in August, about 5%. But if Delta gets worse, the selloff gets worse. You saw what it did last year, down 40% in the (SPY) in only two months, so yes, it all depends on the Delta virus. I'm not really worrying about Delta, it's the next one, Epsilon or Lambda, which could be the real killer. That's when the fatality rate goes from 2% to 50%, and if you think I'm crazy, that's exactly what happened in 1919. Go read The Great Influenza book by John Barry that came out 20 years ago, which instantly became a best seller last year for some reason.

Q: Does the Matterhorn have enough flat space on the top to stand on it?

A: Actually, there is a 6’x6’ sort of level rock to stand on top of the Matterhorn. If you slip, it’s a 5000’ fall straight down on any side, and on a good weather day in the summer, there are 200 people climbing the Matterhorn. There's sometimes a one-hour line just to take your turn to get to the top to take your pictures, and then get down again to make space for the next person. So that's what it's like climbing the Matterhorn, it's kind of like climbing Mount Everest, but I still like to do it every year just to make sure I can do it, and one year I hope to win the prize for the oldest climber of the year to climb the Matterhorn. Every year this German guy beats me; he’s two years older than me.

Q: When will Freeport McMoRan (FCX) start going up? I have the 2023 LEAPS

A: Good thing you have the two-year LEAPS because that gives you two years for inflation to show its ugly face once again. You just have to be patient with these. I think we’ll get a rally in the Fall along with all the other interest rate plays like banks, industrials, money management companies, and so on. (FCX) will certainly participate in that. In the meantime, if we get all the way down to $30 in Freeport McMoRan, I would double up your position.

Q: Why is oil (USO) not a buy? Oil is the ultimate inflation hedge.

A: Yes, unless all of the cars in the United States become electric in the next 15 years, which they will, wiping out half of all demand from the largest oil consumer. The United States consumes about 20 million barrels of oil a day, half of that is for cars, and if you take that out of the demand picture you dump 10 million barrels a day on the market and oil goes back to negative numbers like we saw last year. Never do counter-trend trades unless you’re a professional in from of a screen 24 hours a day.

Q: Should I take profits on my ProShares Ultra Technology ETF (ROM) November $90-$95 vertical bull spread and then enter a new spread when tech sells off?

A: Absolutely! When you have that much leverage and you get these price spikes, you sell! The leverage on this position is 2X on the ETF and 10X on the options for a total of 20X! Well done, nice trade and nice profit, go out and buy yourself a new Tesla and wait for the next dip in tech, which may have already started, and which could power on for the rest of August.

Q: What’s the next move for REITs?

A: REITs came off of historic lows last year; a lot of people thought they were going to go bankrupt, and for companies like (SPG) it was a close-run thing. I would be inclined to take profits on REITs here. The next thing to happen is for interest rates to go up and REITs don’t do that great in a rising rate environment.

Q: When is the off-season in Incline Village?

A: It’s the Spring and the Fall, in between ski season and the summer season. That means there are four months a year here, May/June and September/October, where I’m the only one here and the parking lots are empty. There is no one on the trails, the weather is perfect, the leaves are changing colors, and the roads aren’t crowded, so that is the time to be here. It’s a mob scene in the winter and a worse mob scene in the summer!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 26, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GETTING INTO STUDIO 54),

(AAPL), (AMZN), (TSLA), (GOOGL), (FB), (NVDA), (TLT)

During the heyday of my Morgan Stanley career in the 1980s, back when I had an unlimited expense account, a favorite place to take clients was Studio 54.

The place was full of rock stars, the music was piercing, and strange things were happening in dark corners. It was all the perfect adventure for the impressible visitor from the sedentary Midwest.

Studio 54 was notoriously difficult to get into. There were these hefty doormen dressed in black with big gold chains who did the vetting. If you were famous or a free-spending investment banker, the red ropes were cast aside, and you glided right in. $100 tips spoke volumes too. The hoi polloi could only watch with envy, even after spending hours in line.

The stock market has become a lot like Studio 54. It’s not letting you in. I had ten trade alerts lined up to get into the market on Friday and Monday. I only got off four. After a scant 3.2% decline, stocks turned around so fast it made your head spin. There are strange things happening in dark corners too.

Next week is the first time in a decade when the top five tech companies report earnings. If history is any guide, they will sell off sharply on the reports, form a base in August, then begin their yearend ramp up. This is why I have been hanging on to my short positions.

I continue to belie that the major miss by the markets is how much they are underestimating tech earnings. Maybe they have fully discounted 2021 earnings, but what about 2022-2030?

Let me give you the example of Apple alone. 5G wireless technology is rolling out now which is improving performance by ten times. What about 6G, 7G, and 8G? The cumulative performance gains of a decade of technological improvement is 10,000 times at zero cost!

Do you think Apple will buy more of its own stock in anticipation of this? Do you think everyone else will too?

You bet!

The “Delta” Correction lasted a day, with deaths in some states up 100% in a week. It is a pandemic of the unvaccinated and of children. The stock market was already ripe for a 5% correction. That’s what happens when you double in 16 months. The bond market at a 1.10% yield thinks the recovery is over and we’re going below 1.00% for the ten year.

Facebook is killing people, says Biden, through enabling the spread of vaccine information. Right-wing website says the vaccine causes sterility, alters your DNA, and enables the government to track your location. (FB) says members have the right to lie to each other. This isn’t going away. (FB) shares hit a new all-time high, taking its market cap into the trillion-dollar club.

That was the shortest recession in history in 2020, lasting only two months. Straight down and then straight up, making it the shortest recession in history. But what two months it was, with an eye-popping 22 million jobs disappearing in March and April. We have since made more than half back.

The month-end selloff is back in play, with the 800-point bounce behind us. That’s when big tech reports. With trillions of dollars struggling to get into the market on any dip, a two-day, 3.2% correction is all we are going to get. I managed to strap on stock longs and bond shorts yesterday, but even I got left on the sidelines with my other trade alerts.

Bitcoin breaks $30,000, then bounces back up. It seems to be an inflation/rising interest rate play which does poorly when ten-year yields hit 1.12%. It’s almost trading 1:1 with Freeport McMoRan (FCX). That has to mean we’re soon entering “BUY” territory.

Rents are soaring, up 6.6% in May YOY, according to data collection firm Corelogic. It’s the biggest gain since 2005. Single-family homes, about half of the rental market, are leading the charge. Phoenix is delivering the biggest increases, up 14% YOY, followed by Dallas and Atlanta. What a great time to own!

Share buybacks are turbocharging this market, which could reach an eye-popping record $1 trillion in 2021 and another $550 billion in dividends. Q2 has already seen $350 billion in buybacks. Apple (AAPL) is leading the charge with a monster $250 billion in cash. Alphabet (GOOGL), Microsoft (MSFT), and Berkshire Hathaway (BRKB) follow. Even companies that have never bought the stock before may enter the fray, like Netflix (NFLX), which is a cash flow cow. My yearend target of an S&P 500 at 4,750, up 9.2% from here, is now looking totally attainable.

Existing Home Sales are up 1.4% in June to 5.86 million units, less than expected. Inventories are down 18.8% YOY to 1.25 million units to a 2.6-month supply. The Northeast was the leader, up 2.8%. Median home prices are still soaring to $363,000 and up an eye-popping 23.4% YOY. Sales of homes priced over $1 million are up 147%. No typo here. Some 14% of homes are now sold to investors, while 23% were to all-cash buyers.

GM recalls 69,000 bolts over recharging fire risk. The Ev's use will be severely restricted until fixed, citing “rare manufacturing defects.” Bolts use imported Korean batteries from LG. It’s what happens when you move into a new technology a decade late and rush to catch up. GM will never catch (TSLA). Avoid (GM) and buy (TSLA).

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch profit suffered a -1.65% loss so far in July. My 2021 year-to-date performance appreciated to 66.95%. The Dow Average is up 14.57% so far in 2021.

Two of my positions, a long in (JPM) and a short in the (TLT) did great. But I really took it on the nose with my short positions in the (SPY) when the market melted up on Friday. That should turn out OK when all five big tech companies report this week, which historically marks a market top. That leaves me 60% in cash. I’m keeping positions small as long as we are at extreme overbought conditions.

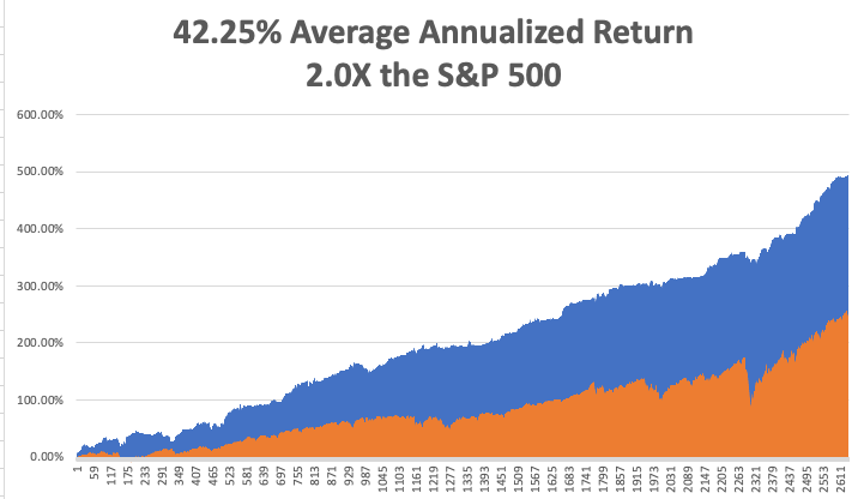

That brings my 11-year total return to 489.50%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.25%, easily the highest in the industry.

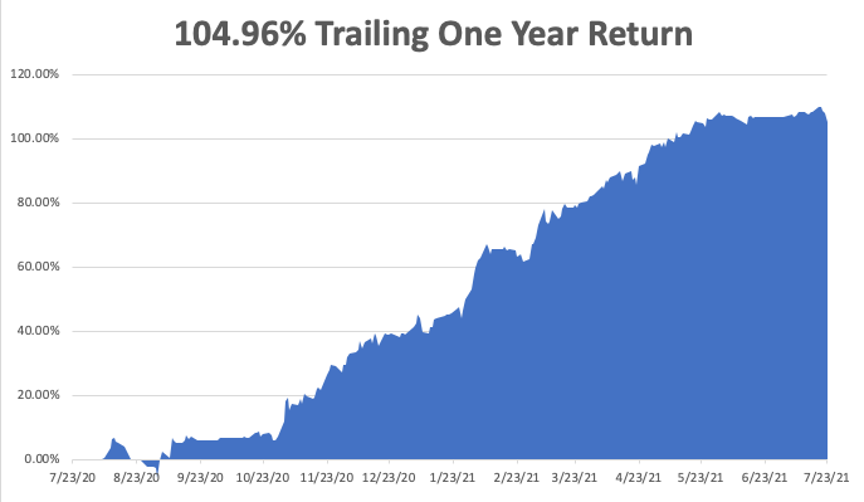

My trailing one-year return exploded to positively eye-popping 104.96%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 34.4 million and rising quickly and deaths topping 611,000, which you can find here. Some 34.1 million Americans have contracted Covid-19.

The coming week will be a weak one on the data front.

On Monday, July 26 at 11:00 AM, New Homes Sales for June are released. Alphabet (GOOGL), Tesla (TSLA), and Amazon (AMZN) report.

On Tuesday, July 27 at 10:00 AM, the S&P Case Shiller National Home Price Index for May is published. Apple (AAPL) reports.

On Wednesday, July 28 at 9:30 AM, the Wholesale Price Index for June is disclosed. Facebook (FB) and Microsoft (MSFT) report.

On Thursday, July 29 at 8:30 AM, we get Weekly Jobless Claims. We also learn the first look at Q2 US GDP, which should be a blockbuster.

On Friday, July 30 at 8:30 PM, we get Personal Income & Spending for June.

As for me, when I was shopping for a Norwegian Fiord cruise for next summer, each stop was familiar to me because a close friend had blown up bridges in every one of them.

During the 1970s at the height of the Cold War, my late wife Kyoko flew a monthly round trip from Moscow to Tokyo as a British Airways stewardess. As she was checking out of her Moscow hote, someone rushed at her and threw a bundled typed manuscript that hit her in the chest.

Seconds later, a half dozen KGB agents dog-piled on top of her. It turned out that a dissident was trying to get Kyoko to smuggle a banned book to the West and she was arrested as a co-conspirator and bundled away to Lubyanka Prison.

I learned of this when the senior KGB agent for Japan contacted me, who had attended my wedding the year before. He said he could get her released, but only if I turned over a top-secret CIA analysis of the Russian oil industry.

At a loss for what to do, I went to the US Embassy to meet with ambassador Mike Mansfield, who as The Economist correspondent in Tokyo I knew well. He said he couldn’t help me as Kyoko was a Japanese national, but he knew someone who could. Then in walked William Colby, head of the CIA.

Colby was a legend in intelligence circles. After leading the French resistance with the OSS, he was parachuted into Norway with orders to disable the railway system. Hiding in the mountains during the day, he led a team of Norwegian freedom fighters who laid waste to the entire rail system from Tromso all the way down to Oslo. He thus bottled up 300,000 German troops, preventing them from retreating home to defend themselves from an allied invasion.

During Vietnam, Colby became notorious for running the Phoenix assassination program.

I asked Colby what to do about the Soviet request. He replied, “give it to them.” Taken aback, I asked how. He replied, “I’ll give you a copy.” Mansfield was my witness so I could never be arrested for being a turncoat. Copy in hand, I turned it over to my KGB friend and Kyoko was released the next day and put on the next flight out of the country. She never took a Moscow flight again.

I learned that the report predicted that the Russian oil industry, its largest source of foreign exchange, was on the verge of collapse. Only massive investment in modern western drilling technology could save it. This prompted Russia to sign deals with American oil service companies worth hundreds of millions of dollars.

Ten years later, I ran into Colby at a Washington event and I reminded him of the incident. He confided in me, “You know that report was completely fake, don’t you?” I was stunned. The goal was to drive the Soviet Union to the bargaining table to dial down the Cold War. I was the unwitting middleman. It worked. That was Bill, always playing the long game.

After Colby retired, he campaigned for nuclear disarmament and gun control. He died in a canoe accident in the lake in from of his Maryland home in 1996.

Nobody believed it for a second.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader