Global Market Comments

July 7, 2021

Fiat Lux

Featured Trade:

(JUNE 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (BRKB), (GOOG), (NVDA), (FB), (TSLA), (JPM), (BAC), (C), (GS), (MS), (NASD), ((X), (FCX), (AMZN), (MSFT), (AAPL), (FCX)

Global Market Comments

July 7, 2021

Fiat Lux

Featured Trade:

(JUNE 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (BRKB), (GOOG), (NVDA), (FB), (TSLA), (JPM), (BAC), (C), (GS), (MS), (NASD), ((X), (FCX), (AMZN), (MSFT), (AAPL), (FCX)

Global Market Comments

July 6, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ALL EYES ON THE FANGS)

(FB), (AAPL), (AMZN), (MSFT), (NFLX), (NVDA), (AMD), (MU)

If you are a believer in the FANGS (FB), (AAPL), (AMZN), (MSFT), (NFLX), with NVIDIA (NVDA) as an add-on, last week was definitely your week.

They rose every day, ending the week with a melt-up of epic proportions. After eight months in the penalty box, tech came back with a vengeance and is now two months into their comeback tour.

The icing on the cake was Facebook’s big win in the antitrust suit from the FTC. That suitably deep-sixes the issue not just for (FB) but all of big tech, possibly for years. The five stocks above now account for a hefty 22% of the S&P 500 (SPY).

The question now on everyone’s mind is what’s next for tech? 25%? 30% 50%? The answer is all of the above, but you have to give it some time, like years.

We are now in an overbought market where big tech has become the cheapest sector. In addition, the global chip shortage promises to get worse before it gets better, with some products seeing a 10X increase in a single generation.

Companies that can’t get the chips they want are resigning products around the chips they can get on the fly.

This has created enormous spillover demand for marginal suppliers like Advanced Micro Devices (AMD) and Micron Technology (MU). It has also accelerated the evolution of technology.

Companies that already have decade-long supply chains already set up, like Tesla, now have a big advantage. That’s why (TSLA) has managed a healthy 27% gain in six weeks.

The severity of the chip shortage is wildly estimated if you look at future design plans of the biggest industries. A tech rally lasting months, if not years, was a totally natural progression.

I’ll tell you who else is dropping the ball. Analysts and strategists are consistently underestimating the strength of the economic recovery and the torrid growth of earnings. They are lagging by about six months. That is why 80% of announcements have delivered upside surprises.

There are more surprises to come.

When markets peaked in April, an eye-popping 92% of shares were above their 50-day moving average. Now, we are only at 52%. That suggests we have another month of excitement before we get another short-term correction.

June Nonfarm Payroll Report comes in hot, up 850,000, an eye-popping 150,000 better than expected. The headline Unemployment Rate moved up slightly to 5.9%. Accommodation gained 269,000, and Food Services & Drinking Places were up 194,000. It was a true Goldilocks number for the stock market, but not the million some had hoped for. My 30% forecast for the Dow Average is looking good.

The Infrastructure Bill extends the hot economy well into 2023 and longer. Analysts better start upgrading now, who have been badly lagging behind the recovery. Tech stocks saw this six weeks ago and began their torrid rally. Buy everything on dips and stick with the barbell strategy to catch all of the rotations.

Rents will continue to go through the roof. Good thing you don’t live in Boise, ID, which is seeing the fastest rent increases in the county at 39% YOY. Of course, having the Micron Technology (MU) HQ there is a major push. Don’t expect any respite. With home prices soaring, rents will get dragged up as prospective buyers are priced out of the market.

Weekly Jobless Claims moderate further, 364,000 Americans filed new claims for unemployment benefits last week - lowest since pandemic. Still elevated from a typical pre-pandemic week when we would see about 210,000 claims.

Softbank’s capital flooding into Crypto, with Japan's SoftBank Group Corp has invested $200 million in Mercado Bitcoin, one of the largest cryptocurrency exchanges in Latin America signaling the start of the first phase of big institutional money hoping to take advantage of the digital currency craze.

Goldman Sachs is the top financial pick according to JP Morgan Chase. All cylinders are firing and we’ve just come off a fabulous 15% dip. A move to more sustainable revenue streams, like wealth management, is the reason, which Morgan Stanley did decades ago under my watch. I’m looking for $450 on dips. Buy (GS) on dips.

Morgan Stanley doubles its dividend, now that it has passed the Fed stress test and the tethers are off. It also announced a share buyback of $12 billion over the next year which may be increased. Buy (MS) on dips.

S&P Case Shiller National Home Price Index for April hits new high, up 14.6%, the biggest increase in 30 years. Phoenix leads at +22.3%, followed by San Diego at +21.6% and Seattle at +20.2%. The numbers run from incredible to unbelievable.

CRISPR Therapeutics goes through the roof, up 12% at the highs, on successful drug trials by Intellia Therapeutics (NTLA) and Regeneron (REGN). The Mad Hedge Biotech Letter core holding provided the gene-editing technology behind the 45% gain in (NTLA) today. It enabled the 85% elimination of a rare inherited fatal liver disease, transthyretin amyloidosis. Say that fast three times. Buy (CRSP) on dips. With Editas, there are only three small companies that have a monopoly here.

Facebook wins antitrust action, a federal judge dismissing an FTC action against the company. The move set the entire tech sector on fire. It looks like all of NASDAQ is going to much higher highs. I bet you had a great day. The court found that (FB) did not enjoy a monopoly which might have forced them to sell off Instagram and WhatsApp.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 0.71% gain so far in June on the heels of a spectacular 8.13% profit in May. That leaves me 100% in cash.

My 2021 year-to-date performance appreciated to 68.60%. The Dow Average is up 13.7% so far in 2021.

I spent the week sitting in 100% cash, waiting for a better entry point on the long side. Up this much this year, there is no reason to reach for the marginal trade, then maybe instead of the certainty. I’ll leave that for the Millennials.

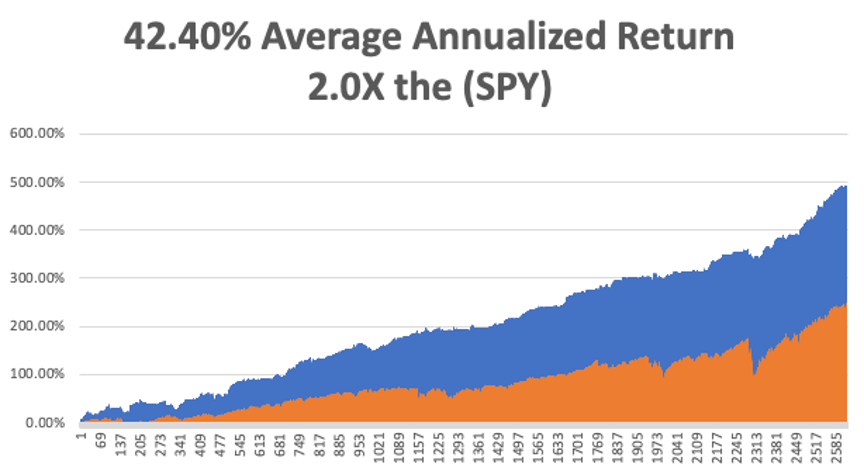

That brings my 11-year total return to 491.15%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.40%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 112.59%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.7 million and deaths topping 606,000, which you can find here.

The coming week will be a weak one on the data front.

On Monday, July 5, markets are closed for the US Independence Day celebration.

On Tuesday, July 6 at 10:00 AM, the ISM Non-Manufacturing Index for June is released.

On Wednesday, July 7 at 10:00 AM, the Federal Open Market Committee Meeting from the last meeting are published.

On Thursday, July 8 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, July 9 at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, with all the hiking I have been doing during the pandemic, I have been listening to a lot of WWII audio books lately. That reminds me of an old friendship I had with Toshiro Mifune, then the most movie famous star in Japan.

Mifune was drafted into the Japanese army during WWII where he served as an aerial reconnaissance photographer. After the war, that led him to work as a cameraman at Toho Productions, then the largest movie company in Japan.

A friend submitted his photo with an application for a casting call without his knowledge, and Toshiro, a good-looking guy, was one of 48 picked out of 4,000. He then met the legendary director, Akia Kurosawa, and the two launched the golden age of Japanese cinema in the late 1940s.

In just a couple of years, they produced blockbuster classic films like the Seven Samurai, Rashomon, and Throne of Blood, all of which are now required viewing by every American film school, and where Mifune demonstrated his impressive skills with a sword he picked up in the army.

I met Toshiro late in his career when he was cast as Admiral Isoroku Yamamoto for the 1976 Universal movie Midway. The problem was that Mifune couldn’t speak a word of English. I was brought in to bring Toshiro up to par in a crash course held at his west Tokyo mansion every afternoon seven days a week. We became good friends.

After a heroic effort, Mifune’s English was still awful, so the producers brought in a voice actor to dub Mifune’s part in Midway. That was Paul Frees, who provided the voice for the Disneyland’s Haunted House and Pirates of the Caribbean rides, as well as the cartoon Boris Badenov. His voice is still attached to those rides today, and I recognize it every time I take the kids.

Midway was a huge success and Mifune’s next big role was to play Commander Mitamura in Stephen Spielberg’s 1941. He followed that up with a role as Toranaga in James Clavell’s 1980 miniseries, Shogun, another old friend. (Clavell is a story for another day). My tutoring skills came back into demand once again, with better results.

Mifune died in 1997 at 77 and I miss him still.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 23, 2021

Fiat Lux

Featured Trade:

(WHY YOU MISSED THE TECHNOLOGY BOOM AND WHAT TO DO ABOUT IT NOW),

(AAPL), (AMZN), (MSFT), (NVDA), (TSLA), (WFC), (FB)

I often review the portfolios of new concierge subscribers looking for fundamental flaws in their investment approach and it is not unusual for me to find some real disasters.

The Armageddon scenario was quite popular a decade ago. You know, the philosophy that said that the Dow ($INDU) was plunging to 3,000, the US government would default on its debt (TLT), and gold (GLD) was rocketing to $50,000 an ounce?

Those who stuck with the deeply flawed analysis that led to those flawed conclusions saw their retirement funds turn to ashes.

Traditional value investors also fell into a trap. By focusing only on stocks with bargain basement earnings multiples, low price to book values, and high visible cash flows, they shut themselves out of technology stocks, far and away the fastest-growing sector of the economy.

If they are lucky, they picked up shares in Apple a few years ago when the earnings multiple was still down at ten. But even the Giant of Cupertino hasn’t been that cheap for years.

And here is the problem. Tech stocks defy analysis because traditional valuation measures don’t apply to them.

Let’s start with the easiest metric of all, that of sales. How do you measure the value of sales when a company gives away most of its services for free?

Take Google (GOOG) for example. I bet you all use it. How many of you have actually paid money to Google to use their search function? I would venture none.

What would you pay Google for search if you had to? What is it worth to you to have an instant global search function? Probably at least $100 a year. I would pay $10,000 as I use it all day long. With 92.05% of the global search market comprising 2 billion users, that means $200 billion a year of potential Google revenues are invisible.

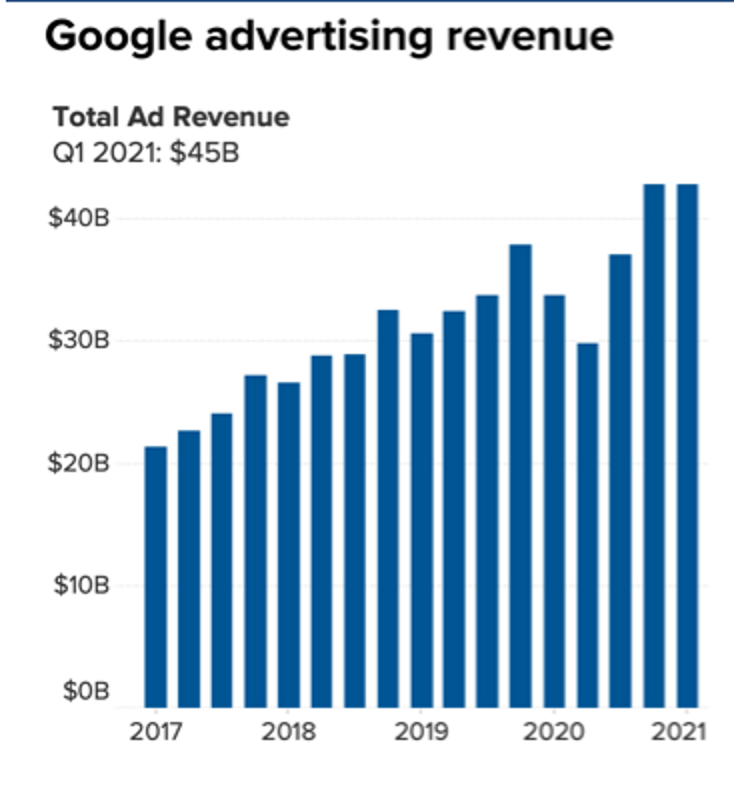

Yes, the company makes a chunk of this back by charging advertisers access to these search users, generating some $55.31 Billion in revenues and $17.93 billion in net income in the most recent quarter.

But much of the increased value of this company is passed on to shareholders not through rising profits or dividend payments but through an ever-rising share price. If you’re looking for dividends, Google doesn’t exist. It is also very convenient that unrealized capital gains are tax-free until the shares are sold, which may be never.

I’ll tell you another valuation measure that investors have completely missed, that of community. The most successful companies don’t have just customers who buy stuff, they have a community of members who actively participate in a common vision, which is then monetized. There are countless communities out there now making fortunes, you just have to know how to spot them.

Facebook (FB) has created the largest community of people who are willing to share personal information. This permits the creation of affinity groups centered around specific interests, from your local kids’ school activities to municipality emergency alerts, to your preferred political party.

This creates a gigantic network effect that increases the value of Facebook. Each person who joins (FB) makes it worth more, raising the value of the shares, even though they haven’t paid it a penny. Again, it’s advertisers who are footing your tab.

Tesla (TSLA) has one million customers willing to lend it $400 billion for free in the form of deposits on future car purchases because they also share in the vision of a carbon-free economy. When you add together the costs of initial purchase, fuel, and maintenance savings, a new Tesla Model 3 is now cheaper than a conventional gasoline-powered car over its entire life.

REI, a privately held company, actively cultivates buyers of outdoor equipment, teaches them how to use it, then organizes trips. It will then pursue you to the ends of the earth with seasonal discount sales. Whole Foods (WFC), now owned by Amazon (AMZN), does the same in the healthy eating field.

If you spend a lot of your free time in these two stores, as I do, The United States is composed entirely of healthy, athletic, good-looking, and long-lived, intelligent people.

There is another company you know well that has grown mightily thanks to the community effect. That would be the Diary of a Mad Hedge Fund Trader, one of the fastest-growing online financial services firms of the past decade. What is the value of our community? To give you a hint, the price of my Global Trading Dispatch has soared from $29 a month to $3,000 a year.

We have succeeded not because we are good at selling newsletters, but because we have built a global community of like-minded investors with a common shared vision around the world, that of making money through astute trading and investment.

We produce daily research services covering global financial markets, like Global Trading Dispatch, the Mad Hedge Technology Letter, and the Mad Hedge Biotech & Healthcare Letter. We teach you how to monetize this information with our books like Stocks to Buy for the Coming Roaring Twenties and the Mad Hedge Options Training Course.

We then urge you to action with our Trade Alerts. If you want more hands-on support, you can upgrade to the Concierge Service. You can also meet me in person to discuss your personal portfolios and my Global Strategy Luncheons.

The luncheons are great because long-term Mad Hedge veterans trade notes on how best to use the service and inform me on where to make improvements. It’s a blast.

The letter is self-correcting. When we make a mistake, readers let us know in 60 seconds and we can shoot out a correction immediately. The services evolve on a daily basis.

It all comes together to enable customers to make up to 20% to 100% a year on their retirement funds. And guess what? The more money they make, the more products and services they buy from me. This is why I have so many followers who have been with me for a decade or more. And some of my best ideas come from my own subscribers.

So, if you missed technology now what should you do about it? Recognize what the new game is and get involved. Microsoft (MSFT) with the fastest-growing cloud business offers good value here. Amazon looks like it will eventually hit my $5,000 target. You want to be buying graphics card and AI company NVIDIA (NVDA) on every 10% dip. It’s going to $1,000.

You can buy the breakouts now to get involved or patiently wait until the 10% selloff that usually follows blowout quarterly earnings.

My guess is that tech stocks still have to double in value before their market capitalization of 26% matches their 50% share of US profits. And the technologies are ever hyper-accelerating. That leaves a lot of upside even for the new entrants.

Global Market Comments

June 21, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S CORRECTION TIME),

(SPY), (TLT), (JPM), (BRKB), (AMZN), (ADBE), (NVDA)

OK, I’ll give it to you straight.

The market has just entered a correction that will take the Dow Average down precisely 7.81% from the recent 35,050 high down to 32,515. That just so happens to be the 150-day moving average.

During this time, interest rates will rise, possibly taking the ten-year US Treasury bond yield to 1.30% and the United States Treasury Bond Fund (TLT) to $151.

Technology stocks will take the lead this summer. After not moving for nearly a year, Amazon (AMZN) will take the lead, discounting last year’s 44% growth in sales. NVIDIA (NVDA) and Adobe will follow.

Bank stocks and other financials like JP Morgan Chase (JPM) and Berkshire Hathaway (BRKB) will suffer, dropping 10% so far and 20% before the crying is all over.

In other words, we just flipped from one half of the barbell to the other in a heartbeat. That will last until late summer to the fall. After that, we shift to the other side of the barbell.

That means the best opportunity to buy financials and sell short bonds in a year is setting up in the coming weeks, if not months.

That takes us until the end of 2021 when I expect another liquidity surge to take everything up. Then we all walk together hand in hand into the sunset signing glory halleluiah. It doesn’t get any easier than that.

I saw all of this coming at the beginning of the year, which is why I raced to rack up a 68.60% profit in the first half of the year and went 100% cash with the June 18 option expiration. I succeeded right on the money.

As for 2022, that is a different story entirely.

The big view here that the stock market is transitioning from an 80% gain to a 30% gain to a more normal average annualized 15% gain. The big game is how far in advance stocks will discount these smaller gains.

It will take a lot to get me off the bench and risk any of this hard-won profit. A Volatility Index (VIX) of over $35 would help (we closed at $20.70 on Friday). So would a Mad Hedge Market Timing Index under 20. So would JP Morgan under $127.

The Fed Takes a Turn, leaning towards more inflation. It is keeping interest rates unchanged at 0%-0.25% and continuing bond purchases at $120 billion a month. It is still sticking with the “transitory” argument on inflation but raised its full-year target from 2.4% to 3.4%, more than most expected. It went more specific on rate rises, predicting two 0.25% increases by the end of 2023. Bonds and technology stocks crashed, and inflation plays like banks, Bitcoin, and Berkshire Hathaway soared. The barbell strategy wins again!

The Big Rotation is On, with traders moving out of inflation plays and into big tech. That is the outcome of the shocking bond market spike that came out of last week’s 5% print for the Consumer Price Index. The Fed is telling the world that any inflation is temporary, and the world is believing them. It could give us a bond and tech rally that lasts a couple of months.

Commodities Crash, on a soaring US dollar and shrinking interest rates. The 15-month bull move is taking a summer vacation, unwinding 2X-10X moves racked up since the 2020 lows. Palladium took an 11% hit, with platinum off 7%, corn 6%, and copper 4%. Banks also sold off big as the whole inflation trade unwinds. Buy all of these on the next bottom for a rebound.

Shipping Costs are out of control for everything from everywhere to everywhere else. Transporting a 40-foot steel container of cargo by sea from Shanghai to Rotterdam now costs a record $10,522, up a whopping 547%. Tens of thousands of containers are on the wrong side of the Pacific. Shortages of truck drivers are extreme, with $50,000 signing bonuses rampant. It is one thing that could make continuing inflation pernicious.

If Copper sells off, it won’t be by much. Conventional internal combustion cars use 40 pounds of copper for wiring. EVs use 200 pounds for the heavy copper rotors in each wheel, in addition to two ounces of silver (SLV). EV production will rise from 700,000 units last year to 25 million by 2030. You do the math. There aren’t enough copper mines in the world to accommodate this demand and it takes five years to build a new one. Buy (FCX) on the next big dip. It’s going to $100 in five years.

Paul Tudor Jones says the Taper Tantrum is coming, despite last week’s perverse reaction by the bond market to the red hot 5% inflation rate. The Fed’s obsession with jobs only and not inflation will end in tears. My old client and legendary investor has 20% of his assets in inflation plays, including gold (GLD), Bitcoin, commodities, and short US Treasury bonds (TLT). When Paul is wrong, it’s usually not for very long.

Housing Starts up only 3.6% in May, to a seasonally adjusted 1.57 million units, with sky-high lumber and other materials prices a major drag. New Permits hit a seven-month low.

Weekly Jobless Claims jump to 412,000, the largest increase since March. Could the economy be slowing?

Tech Soars, getting a new lease on life with the collapse of interest rates last week. My favorite, Amazon (AMZN), picked up a healthy $80 yesterday on a 44% YOY gain in sales. Even Apple (AAPL) is coming back from the dead, up $2.00. I sent out long-term at-the-money LEAPS on these last week. It's hard to hold quality down for the long term.

Factory activity fell in June, for the second month in a row according to the Philly Fed, backing off from an all-time high in the spring. Parts and materials shortages are plaguing manufacturers everywhere as the economy struggles to escape from its pandemic torpor.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 0.71% gain so far in June on the heels of a spectacular 8.13% profit in May. That leaves me 100% in cash.

My 2021 year-to-date performance appreciated to 68.60%. The Dow Average is up 8.8% so far in 2021.

I spent the week taking profits on the 40% in remaining positions either by selling or running them into the Friday expiration. My goal was to go 100% before the market completely fell to pieces and I succeeded handily. It’s going to be a grim summer.

I rang the cash register on Berkshire Hathaway (BRKB) and the S&P 500 (SPY), and my short in the (SPY). Perhaps my best trade of the year was stopping out of my short in the (TLT) for an $800 loss when it topped $140.

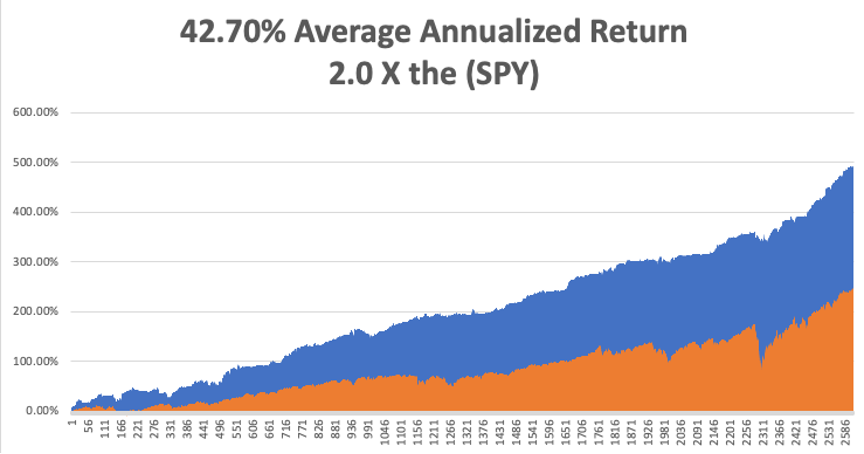

That brings my 11-year total return to 491.15%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.70%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 126.07%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.1 million and deaths topping 600,000, which you can find here. Some 33.1 million Americans have contracted Covid-19.

The coming week will be a weak one on the data front.

On Monday, June 21 at 8:30 AM, the Chicago Fed National Activity Index is out.

On Tuesday, June 22 at 10:00 AM, Existing Home Sales for May is released

On Wednesday, June 23 at 10:00 AM, New Home Sales for May is published.

On Thursday, June 24 at 8:30 AM, the Weekly Jobless Claims are published. We also get US Durable Goods Orders for May.

On Friday, June 25 at 8:30 AM, US Personal Income & Spending for May are disclosed. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, with all the recent violence in the Middle East, I am reminded of my own stint in that troubled part of the world. I have been emptying sand out of my pockets since 1968, when I hitchhiked across the Sahara Desert, from Tunisia to Morocco.

During the mid-1970s, I was invited to a press conference given by Yasser Arafat, founder of the Al Fatah terrorist organization and leader of the Palestine Liberation Organization, at the Foreign Correspondents Club of Japan. His organization then rampaging throughout Europe, attacking Jewish targets everywhere.

Japan recognized the PLO to secure their oil supplies from the Persian Gulf, on which they were utterly dependent.

It was a packed room on the 20th floor of the Yurakucho Denki Building, and much of the world’s major press were represented, as the PLO had few contacts with the west.

Many placed cassette recorders on Arafat’s table in case he said anything quotable. Then Arafat ranted and raved about Israel in broken English.

Mid-sentence, one machine started beeping. A journalist jumped up to turn his tape over. Suddenly, four bodyguards pulled out Uzi machine guns and pointed them directly at us.

The room froze.

Then a bodyguard deftly set his Uzi down on the table, flipped over the offending cassette, and the remaining men stowed their weapons. Everyone sighed in relief. I thought it was interesting that the PLO was using Israeli firearms.

The PLO was later kicked out of Jordan for undermining the government there. They fled Lebanon for Tunisia after an Israeli invasion. Arafat was always on the losing side, ever the martyr.

He later shared a Nobel Prize for cutting a deal with Israel engineered by Bill Clinton in 1993, recognizing its right to exist. He died in 2004.

Many speculated that he had been poisoned by the Israelis. My theory is that the Israelis deliberately kept Arafat alive because he was so incompetent. That is the only reason he made it until 75.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Middle East Does Have Some Advantages

Mad Hedge Technology Letter

May 28, 2021

Fiat Lux

Featured Trade:

(THIS CUTTING-EDGE CHIPS STOCK IN HYPERGROWTH MODE)

(NVDA)

Nvidia (NVDA) is another multilayered business with revenues coming from east and west and basically everywhere and really at a time when the gaming market is the largest ever.

Let’s make this clear: Nvidia isn’t a gaming stock, but its best business is centered around the secular gaming trend.

They have this massive installed base of GeForce users (Nvidia branded graphics processing units).

They have reinvented computer graphics as well as resetting the install base — created a pipeline of profits that take advantage of the boom in gaming which many as you know went gangbusters because of the shelter-at-home conditions.

There has been substantial development on the gaming front — at a time when gaming market is expanding fast, and peeling back the layers it sports — eSports — it's infused into art.

It is infused into social.

And so, gaming has such a large cultural footprint now, even to the point that it’s the largest form of entertainment in the world.

The emphasis of this experience is going to resonate for the long term and not only that, the phenomenon called crypto — Nvidia’s Crypto graphic cards named CMP will funnel GeForce supply to gamers.

The Nvidia CMP 30HX is a dedicated crypto mining card. The CMP 30HX is essentially a mid-range graphics card powered by Nvidia’s TU116 processor.

There is strong demand for this product, and I expect to see elevated sales for quite some time because of the dynamics of crypto and the avalanche of capital gravitating towards it not only institutional but from retail too.

And hopefully, in the combination of gaming, crypto, and data, Nvidia is primed to experience strong growth in core businesses through the year.

The data backs up Nvidia’s ambition with Q1 exceptionally strong with revenue of $5.66 billion and year-on-year growth accelerating to 84%.

They set a record in total revenue in Gaming, Data Center, and Professional Visualization, driven by their best product lineups and structural tailwinds across our businesses.

Starting with Gaming, revenue of $2.8 billion was up 11% sequentially and up 106% from a year earlier.

Channel inventories are still leading and Nvidia expects to remain supply-constrained into the second half of the year.

Now Laptops continue to drive strong growth this quarter with all major PC original equipment manufacturers (OEM) launching GeForce RTX 30 Series laptops based on the 3080, 3070, and 3060, as part of their spring refresh.

This is the largest ever wave of GeForce gaming laptops, over 140 in total as OEMs address the rising demand for gamers, creators, and students for NVIDIA's powered laptops.

They believe gaming also benefited from crypto mining demand, and Nvidia is separately addressing mining demand with cryptocurrency mining processors or CMPs.

The crypto CMP revenue was $155 million in Q1, reported as part of the OEM and other category. And our Q2 outlook assumes CMP sales of $400 million.

Data Center continues to be a growth driver with revenue topping $2 billion for the first time, growing 8% sequentially and up 79% from the year-ago quarter, which did not include acquisition Mellanox.

And then lastly, supercomputing; supercomputing centers all over the world are building out and Nvidia is in a great position to fuse together time simulation-based as well as data-driven-based approaches, which are called artificial intelligence.

Across the board, data center is gaining momentum and is the largest segment of computing and will continue to train deep neural networks with rising computational intensity led by two of the fastest growing areas of AI; natural language understanding.

Demand is booming across Nvidia’s markets and readers can expect increase in CMP, but they still expect the lion share of growth to come from Data Center and Gaming.

In Data Center business, their product lineup couldn't be better and they have a strong overall portfolio both for training and inferencing and they are experiencing strong demand across hyperscales and vertical industries.

The foundation has been laid to be a three-chip data center scale computing company with GPUs, DPUs and CPUs.

Fortunately for Nvidia, AI is the most powerful technology force of our time.

Nvidia partners with cloud and consumer Internet companies to scale out and commercialize AI-powered services.

They are democratizing AI for every enterprise and every industry.

With pre-trained models for conversational AI, language understanding, recommender systems, and broad partnerships across the IT industry, Nvidia is removing the barriers for every enterprise to access state-of-the-art AI.

From gaming, metaverses, cloud computing, AI, robotics, self-driving cars, genomics, computational biology, Nvidia is engaging in important work and innovating in the fastest-growing markets today.

Now to look at our outlook for Q2, revenue is expected to be $6.3 billion, and remember that the prior year when Q2 revenue was $3.87 billion.

This company is mesmerizing, growing from $11 billion in annual revenue to $16.68 billion in just one year says it all.

Growing revenue in the mid-80% means it will easily surpass the $9 billion in the first two quarters of the year paving the way for an almost $20 billion per year business.

Sure it’s not Apple or Microsoft but for what it does, they are best in show in an industry that is going through a massive supply headwinds.

The quarterly performance only reinforces the thesis that chip companies are a great place to allocate funds to and the support is there for a buy the dip investor attitude because of growing EPS which promotes share buy backs and capital returns to shareholders.

It’s hard to believe that investors could put their money elsewhere because tech still secures the vast majority of earnings in the business world and that train isn’t slowing down and the bullet train is clearly the chip sector in 2021.

Global Market Comments

May 28, 2021

Fiat Lux

Featured Trade:

(MAY 26 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (DIS), (AMZN), (FCX), (X), (PLTR), (FXE), (FXA), (TLT), (TBT), (AMC), (GME), (ZM), (DAL), (AXP), (LEN), (TOL), (KBH), (DOCO), (ZM), (TSLA), (NVDA), (ROM)