Mad Hedge Technology Letter

April 8, 2021

Fiat Lux

Featured Trade:

(SHOULD I BUY CLOUD FIRM OKTA IN APRIL?)

(OKTA), (TWLO)

Mad Hedge Technology Letter

April 8, 2021

Fiat Lux

Featured Trade:

(SHOULD I BUY CLOUD FIRM OKTA IN APRIL?)

(OKTA), (TWLO)

The excess liquidity fueling the U.S. financial markets signal that investors are picking up the tab for heavy loss-making tech companies like never before.

Only in the U.S. can this happen at the scale it is happening as the U.S. controls its own currency, Central Bank, and possess the most reliable IPO process.

This phenomenon effectively supports a mindset of tech start-ups putting off profits for years and sometimes even decades.

Too much money chasing too few ideas and we have seen numerous examples of this with investors turning to ultra-leverage to figure out how to deliver real gains to investors.

Another heavy loss-making cloud company that I recommended buying “at the bottom” last March was identity-verification software maker Okta (OKTA) whose business was dramatically uplifted from the shift to remote work during the pandemic.

The recommendation worked like a charm with the stock essentially doubling from the time of that call.

But what’s in store for this password company moving forward?

First, let's rewind to the beginning of March when investors dumped the stock after a disappointing 2022 forecast and suffered from rumblings of the company paying too much to acquire Auth0 for about $6.5 billion.

The 30% sell-off was another example of growth companies’ ugly habit of volatility making it hard to time the entry points for heavy pocketed investors.

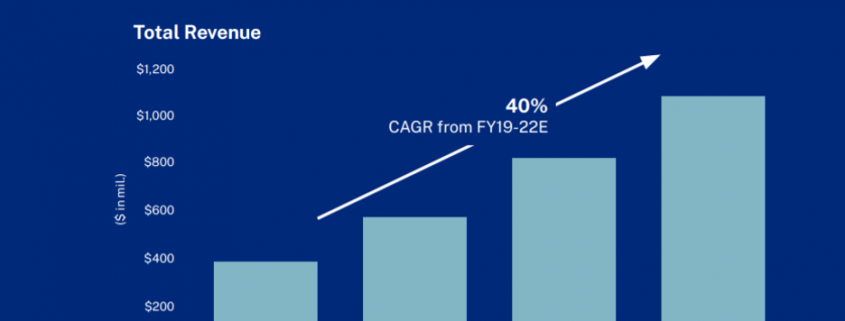

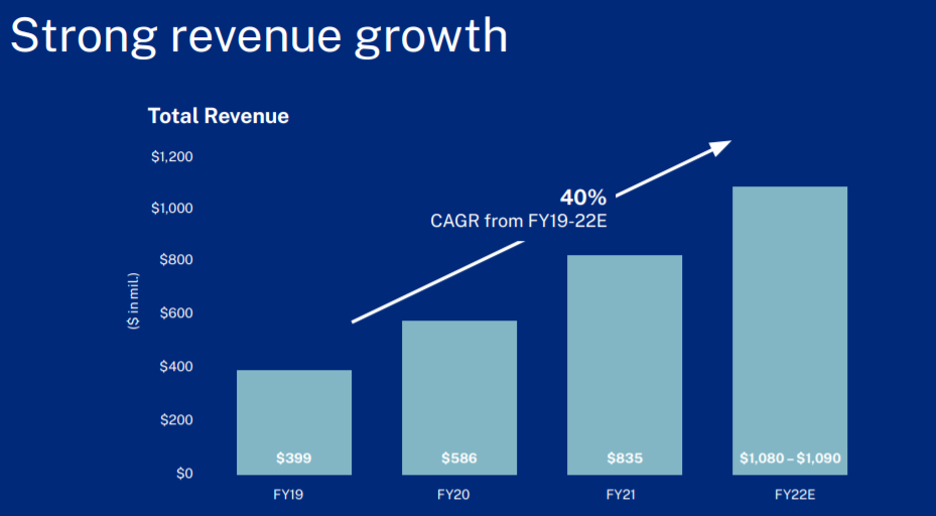

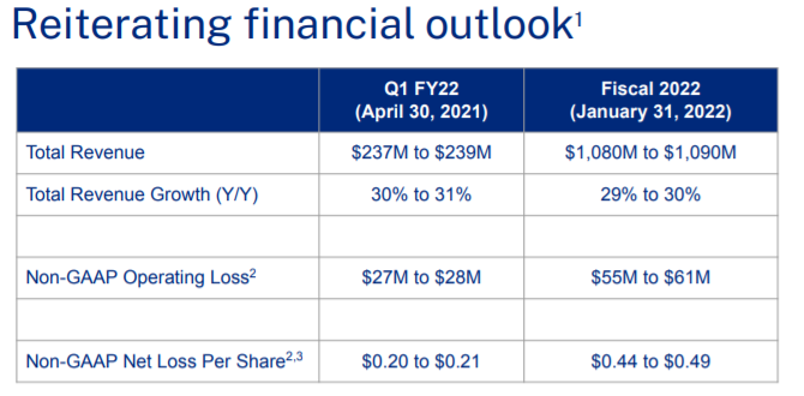

In the most recent analysts’ day, Okta projected sales will grow 30% in each of the next three years.

Revenue at the end of fiscal 2024 will be close to an annualized $2 billion, or about $500 million for the fourth quarter that year.

Yes, this is still a small company by any metric.

Demand for the software maker’s products, which help workers access corporate systems and consumers authenticate their identity online, has increased as more employees logged on from home in 2020.

For the 12 months through March 1, Okta was used more than 52 billion times to log into an app or website, almost 200% growth from the same period a year earlier.

Okta has retraced some of its losses when it announced it introduce 2 new products.

One, Identity Governance Administration, generates reports which show in an organization who has permission to see which parts of its systems.

The idea is to make sure people who’ve left the company or have changed roles don’t retain access to unauthorized areas.

Next, Privileged Access Management, governs who can view and change an organization’s critical systems.

The new areas expand the size of Okta’s total addressable markets to about $80 billion.

Management said these protections have become more critical as employees continue to work for home.

Many data breaches come down to server accounts that weren’t locked down when they should have been.

Admins change jobs at a rapid pace as companies look to poach talent more than ever now.

If it wasn’t the cause of the breach, it was a vector that the attackers used once they got in.

Being the cloud growth company it is, with only a market capitalization of $30 billion, the new announcements was the catalyst for Okta shares to surge 8% during intraday trading.

This is typical growth company price action.

The company is also dogged by persistent rumors it might sell to a larger tech company and I would say it’s a little surprising that the company is “buying growth” at such an early stage of its growth cycle.

But again, the subsidies keep flowing to these upstart tech guys because liquidity levels and bold risk appetites allow these types of aggressive financing that affect management decisions.

Overpaying to grow is where we are now in the tech cycle with the Central Bank effectively not allowing this bull market to die.

Okta CEO Todd McKinnon said he wants it to be one of five or six independent software clouds that every company needs.

And I also want to be one of five or six men in the world that every girl in the world wants to date.

I get it that McKinnon wants identity and access to remain Okta’s specialty rather than being subsumed into one of the other categories. Microsoft, which has identity software products that predate its cloud businesses, is already Okta’s main rival.

I would agree that Okta is prime for investors to buy the dip, but I would recommend traversing to higher waters because there are better cash burning, cloud names out there that are growing faster than Okta.

Honestly, Okta should be growing more for its small size, and “buying growth” seems like they are worried about an imminent collapse of growth which is a worrying sign.

Yes, I must agree that competition is stiff these days in the cloud ecosystem.

My conclusion with Okta is that any investor looking to buy Okta should instead buy communications-as-a-cloud firm Twilio (TWLO).

This is the communications platform operating behind the scenes of behemoths like Airbnb and Uber.

They have a 3-year revenue growth rate of 66% and grew 65% year-over-year last quarter.

That is what I call consistent!

And that is what I call cash-burning growth!

TWLO is also exactly double the size of OKTA at $62 billion and is predicting next quarter to grow 44% to 47%.

According to IDC, investments in digital transformation will nearly double by 2023 to $2.3 trillion, representing more than 50% of total IT spending worldwide, and it’s clear to me that more of this capital will flow into TWLO than OKTA.

OKTA is just a one-trick pony, but TWLO is a complex integrated system that Uber can’t live without. Many companies can live without Okta and plug in a substitute. The revenue is just way stickier with TWLO, and the strategic position is superior.

OKTA is a solid buy the dip candidate, but just buy TWLO instead.

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

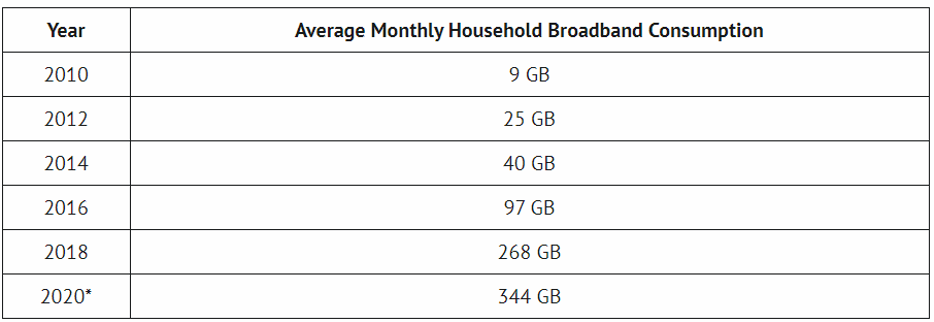

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Mad Hedge Technology Letter

July 6, 2020

Fiat Lux

Featured Trade:

(WHY AN OFFICE IN BELGRADE MAKES SO MUCH SENSE)

(OKTA), (SPLK), (CRM), (WKDAY), (TWLO), (NOW)

My nephew paid nothing for phone, transport, internet, utilities during the coronavirus. I’ll tell you how he did it and no, he did not live with his parents or anyone else footing the bills. The future and a massive deflationary wave of technology can be found in how my nephew lives his life.

This is a story about James.

His life is the reason why the U.S. economy will never be the same and highlights the level of metamorphosis going on in our newfound home offices.

The usual culprit of the element inciting change is tech with the aftermath a catalyst for another wave of gigantic deflation.

The statisticians need to check what they are doing because nothing adds up in the deflationary world anymore.

This downward pressure on inflation is likely to be relentless, not just transitory offering central banks more flexibility with corporate accommodative policies without threatening to invoke the specter of inflation.

This is part of the reason why the bull market in tech stocks will be infinite.

Many economists and officials are befuddled, and such worries have never been far from the surface in the period after the financial crisis, the Great Recession, and now Covid-19.

The only thing constant right now is uncertainty.

Technologies are spawning “supply side shocks” in many areas of the global economy by permitting a more intense and efficient utilization of resources.

Also, replacement often leads to the betterment of people’s lives as software disrupts and cannibalizes many established goods and services.

One recent example that couldn’t illustrate this better for the “have nots” is car rental company Hertz, who woke up one day and found their business model shattered into oblivion and obsolete.

James has a modest U.S. income of $4,000 per month, which does not get you anywhere in megacities like New York or San Francisco.

After taking into account car maintenance, gas bills, car insurance, utilities, and rent, there might be $1,000 left over if luck is on the right side.

This type of income just doesn’t cut it in many American cities.

James faced a daunting challenge to acquire the quality of life he desired in most American megacities.

James works for a small start-up tech company, and after he proved to management that he was a legitimate contributor, he quickly asserted his leverage by requesting his manager to sanction a move to a full-time remote position.

Management didn’t want to lose him and reluctantly agreed contingent on a rolling 6-month review.

But James didn’t settle on Bakersfield, California, or even Klamath Falls, Oregon where he could significantly cut his bills.

He chose to take his talents to Belgrade, Serbia.

Deflationary impulse is pervasively spread across economic sectors where its presence has been difficult to note and with James’ housing budget now abroad, his dollars are partially taken out of the U.S. financial picture.

How can such “supply-side shock” manifest itself so quickly? Surely, the supply of land is largely fixed, particularly in areas that have already been urbanized.

The answer lies with technology that created additional capacity of the second industrial revolution, such as increasingly taller high-rise buildings.

Fast forward to today.

A company like Airbnb showcases how digital technologies are allowing more intensive resource utilization. There was abundant accommodation capacity hidden in the world’s cities — but it was not accessible until the internet, smartphone adoption, and Airbnb’s founders’ ingenuity unlocked it.

James is taking advantage of these wrinkles cutting his housing and office bill and crashing his monthly budget to the bare minimum.

James didn’t even feel the need to pay a deposit on a 1-year rental lease choosing to forego rental stability for the optionality of movement.

His Belgrade Airbnb space doubled as his home office.

Airbnb usually offers a 28-day discounted price which is classified as a “long stay.”

Many of these discounts are 30% or more, meaning James only paid $350 per 28 days to live in the Belgrade city center and would move around to different neighborhoods he felt were palatable.

He especially liked the Austrian-Hungarian historical district Zemun and the hipster vibe in Dorchol near the Belgrade City Center.

After the coronavirus hit, these “long term” rentals went from $350 to $200 per 28 days as tourists fled the city centers of Europe, and Airbnb prices crashed with cratering demand.

Why doesn’t James pay for internet, phone, and utilities?

Utilities and Wi-Fi are included in the price of the Airbnb covered by the host along with the furniture and amenities like air conditioning, fully equipped kitchen, microwave, dishwasher, iron, and washing machine.

James has substituted his phone bill opting for chat apps WhatsApp, Skype, FaceTime, Signal, and calls over Wi-Fi.

He keeps a Google Fi phone account to maintain a U.S. number, but keeps it permanently “paused” and only uses it to receive security and verification codes from his U.S. bank, IRS to pay taxes, and mortgage service provider to pay his mortgage online.

He manages to log on to these important portals via a virtual private network (VPN) that routes through a U.S.-based server.

He leases his U.S. house, which he owns, out to a tenant who covers 100% of James’ monthly mortgage costs and handed over his property to a local property manager to be managed.

James doesn’t pay for any transport fees because his city center apartment is walking distance to every main artery in Belgrade giving him access to Turkish-style coffee houses, to Cevapi grilled barbecue shops, to designer Hookah lounges all within a 15-minute walk.

The 2 to 3 times he needs to jump on the tram network to attend a party or night event, he borrows his friend’s yearly transit pass or just skips the fare completely. If he needs to pay, it is 75 cents for a 1-way ticket anywhere in Belgrade.

James has been living out of 2 suitcases for as long as I can remember and has never owned a car, despite growing up in the U.S. and graduating high school and university here.

Although many in the family think he is overly extreme, his intensely minimalistic lifestyle is food for thought; even though he was the first I had ever seen live in such a simplistic, draconian way.

The fallout from the coronavirus and the trends of deflationary technology show that James was ahead of his times when nobody knew it and recently accelerating trends validate his life choices.

James has effectively been planning for a pandemic his whole life which is why he has successfully navigated it, while many Millennials his age have been wiped out, drowned into debt they can never get out of.

If the U.S. suddenly gets tens of millions of James living a variation of his life, many services and products just wouldn't sell in the U.S. anymore. And if they are as extreme as James, housing will crash in all American megacities.

The reality is somewhere in between.

Reinvention is the U.S.’s strong point, but now young people are arbitraging literally everything in their lives, applying a global perspective with a good dose of software to support ultimate goals.

I will assume that most goals end up with obtaining a higher life quality.

Moving forward, investors will need to reprogram their technology compasses around firms that support a “James” type of lifestyle simply because there will be more people like this every day.

Software companies that mesh with this overarching thesis are Okta (OKTA), Splunk (SPLK), Salesforce (CRM), Workday (WKDAY), Twilio (TWLO), and ServiceNow (NOW).

The broader conclusion is that high-quality software stocks will outperform any other sub-sector or sector from now until forever.

As for James, I heard he finally decided to cough up money for local phone data which comes in at a mind-boggling $1 per 1 GB in Belgrade only 10% the cost of the same GB in inexpensive western countries.

Mad Hedge Technology Letter

March 4, 2020

Fiat Lux

Featured Trade:

(THE BEST TECH STOCKS TO BUY AT THE BOTTOM)

(NFLX), (ZM), (PTON), (AMZN), (OKTA), (WORK), (ATVI), (EA), (TTWO)

Tech stocks that are begging to be picked up on the back of the coronavirus pandemic are Netflix (NFLX), Zoom Video Communications (ZM), workplace collaboration service Slack Technologies (WORK), and Peloton Interactive (PTON), the spin bike company.

Their short-term outperformance indicates that these stocks work well during mass pandemics shelving most outdoor activity and commerce.

The basket of 3 stocks has easily beat the S&P 500 since the coronavirus emerged as a threat in mid-January.

Home sitting doesn’t generate a net output of business activity unless that job is digital.

The majority of workers still commute in a physical car only to sit in an office, restaurant, or some other type of self-contained space.

That is the underlying problem that has no solution, and any rate cut by the Fed cannot ultimately solve consumers holed up in their house.

If the companies that could opt to go pure digital do take up the option, the number of remote workers would rise and digital products would be the ultimate beneficiary of this trend.

Companies that promote remote working such as Slack (WORK) and Google Hangouts are in pole position to reap the rewards.

These services include video conferencing software, logistical services, administrative services, network security services, ecommerce and any service that aids in generating digital content like Adobe and its umbrella of assets.

The trend was already transforming American culture, but the virus vigorously pulls forward a trend that was already in overdrive.

Enabling information workers to produce outside the traditional office environment is one of the lynchpins of the Silicon Valley model.

Companies will ultimately realize that spending big bucks on business travel to meet face to face for 30 minutes is probably not an optimal allocation of resources.

Business travel is getting cut with a cleaver such as Amazon.com (AMZN) who are forcing employees to avoid all nonessential travel for now, including within the U.S. Much of that travel could be replaced by video calls.

Other companies will get in on the action by directing their employees to work from home in the coming weeks.

Coronavirus mania has reached the U.S. shores with consumers stocking up on all the essentials at the local Costco.

If this gets worse, there is no solution unless a viable medical solution starts improving the health crisis.

There are still only 7 known fatalities from the coronavirus, all in the state of Washington, and limiting that number is critical to the health of the tech market.

Another company is Okta (OKTA), a leader in authentication security cloud software.

The company’s offering allows employees to use corporate applications on-site and remotely and protecting their access to their digital services is just as important as the work itself.

As consumer spurn movie theaters, concerts, and gyms, the entertainment space will give way to digital entertainment that includes Netflix (NFLX) and Roku (ROKU).

Roku is a great place to hide out in the world where Covid-19 meets daily consumers in the U.S. in a more meaningful way during 2020.

Netflix is a company that has defied gravity this year by bull-rushing its way through the competition and proving there is space for everyone.

The increase in incremental demand for digital content will only help Netflix claim a bigger part of the pie.

We can also lump the videogame industry into this cohort such as Activision Blizzard (ATVI), Electronic Arts (EA), and Take-Two Interactive Software (TTWO).

They have faced serious headwinds from gaming phenomenon Fortnite, but prolonged home sitting will even boost their shares.

The spine of digital services will receive a boost as well from the usual cast of characters such as Microsoft (MSFT), Apple (AAPL), Alphabet (GOOGL), and Facebook (FB).

As investors wait for the climax of the coronavirus and the Central Bank has indicated that they are open to more accommodative policy, we could be ripe for more volatility.

Chinese coronavirus cases have started to taper off and if the rest of the world trends in a similar fashion, this virus scare could be in the history books in 2-3 months.

However, the trajectory of the virus is still a massive unknown in the U.S. and winning the health battle is the only panacea to this dilemma.

Mad Hedge Technology Letter

July 12, 2019

Fiat Lux

Featured Trade:

(CLOUD SECURITY ON THE MARCH)

(OKTA), (ZS), (CRM), (AMZN)

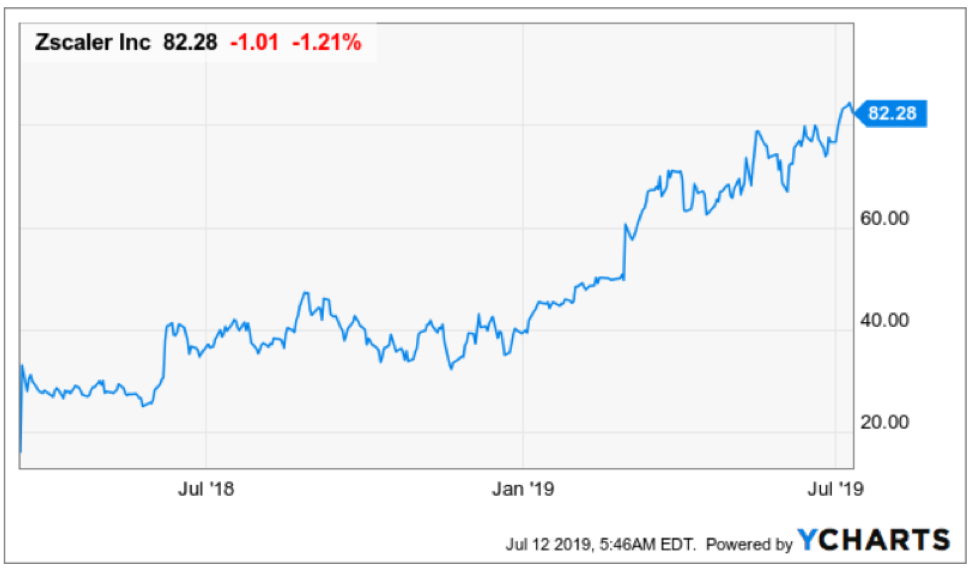

Take a look at these beauties that I recommended at the beginning of December 2018.

At that time, Okta (OKTA) was trading at $62 and Zscaler (ZS) was at $40 on the button – fast forward to today and Okta is now over $136 and Zscaler victoriously sitting at $82.

Oh, how do times change!

That was my reaction watching their performance for the past 7 months giving belief to my assessment that second-tier cloud companies will have a field day this year.

Cloud companies aren’t going away anytime soon, please tattoo that on your forehead.

There isn’t a hotter topic circulating the gossip winds these days than digital security pressured by geopolitics.

Okta is the best in show for identity management – a snazzy term for managing employees’ passwords.

Okta’s products are built on top of the Amazon Web Services cloud.

Coincidentally, Okta was erected in 2009 by a team of former Salesforce (CRM) executives. Salesforce is one of my favorite cloud-based software companies, offering a blueprint for success to other up-and-coming software companies.

Current Okta CEO and founder Todd McKinnon previously served as the Senior Vice President of Engineering at Salesforce.

Other founders include Okta COO Freddy Kerrest who also meandered through the corridors of Salesforce.

I can tell you that you could do much worse than starting a new software company with a collection of Salesforce upper echelon talent.

This all-star team is behind the insatiable growth of Okta whose revenue has grown over 600% since establishing itself.

Okta’s first-quarter results didn’t disappoint with revenues of $125 million—a rise of 50% year-over-year beating the consensus of $117 million.

Subscription revenues comprised 94% of sales and the company expects sales of $130 million amounting to a rise of 37% year-over-year.

Okta’s subscriber base has risen over 500% in the past 5 years and annual contract value of over $100,000 has expanded 60% annually.

The company still loses money but hopes to make some headway on this issue with projected EPS estimated to grow 25% annually in the next five years.

This year spawned a massive divergence between tech who has legs and tech who will be dragged down to the depths of the ocean floor by the heavy weight of regulation, overwhelming competition, or just flat out poor management or inferior product development.

Zscaler echoed similar positive sentiment of Okta by recording a quarter to remember growing revenue by 61% year-over-year while calculated billings grew 55% year-over-year.

In addition to the top line growth, operating margins improved 14% points year-over-year to 8%.

The quarterly results demonstrate the leverage in cloud security business models and the ability to drive growth and profitability.

String together a third consecutive quarter of profitability is just part of the battle, Zscaler will continue to aggressively invest for significant market opportunity that lie ahead.

Cloud security potential means going after a $20.3 billion Total Addressable Market in calendar 2019.

Let me divulge a tad bit about the competitive landscape and why Zscaler is brilliantly positioned for success.

As organizations increasingly make the shift to the cloud, traditional firewall and VPN vendors are finally acknowledging that the legacy security appliances can secure the new digital enterprise and are attempting to build a security cloud using single tenant software designed for on-premise appliances just like you can't create a Netflix service by stacking thousands of DVD players in the cloud.

You can't offer an inline high-performance security cloud by spinning up a bunch of virtual machines in a public cloud. This is a defensive strategy of cloud imitators which, in our view, serves the self-preservation of the vendor, not the needs of the customers.

Zscaler has a significant competitive advantage as a result of the technology, architecture and maturity of cloud security platform including one, Zscaler was born in the cloud, for the cloud just like Salesforce and Workday.

Two, Zscaler has a purpose built globally distributed multi-tenant cloud for fast user experience, unlike imitation cloud, Zscaler requires no back hauling from front doors to a central computing data center of a public cloud.

Three, Zscaler performs SSL inspection at scale as a purpose-built proxy for better security.

Lastly, Zscaler continues to deliver zero trust network access that provides application access without network access reducing business risk unlike firewalls and VPNs.

The duo of Okta and Zscaler are the bright lights of the cloud generation and leading the digital economy in digital security.