(MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S ALL ABOUT INTEREST RATES),

(HOOD), (CRWV), (BTC), (ORCL), (NFLX), (GS), (ZM), (MS), (BLK),

(GT), (WHR), ORCL), (INTC), (BABA)

The U.S. administration has kicked around the idea of Oracle (ORCL) chairman Larry Ellison as a possible buyer to one of the hottest social media assets TikTok.

Oracle isn’t intending to outright acquire a majority stake, but their involvement shows that Oracle is at the seat with the big boys in tech and that seat carries a great deal of clout today.

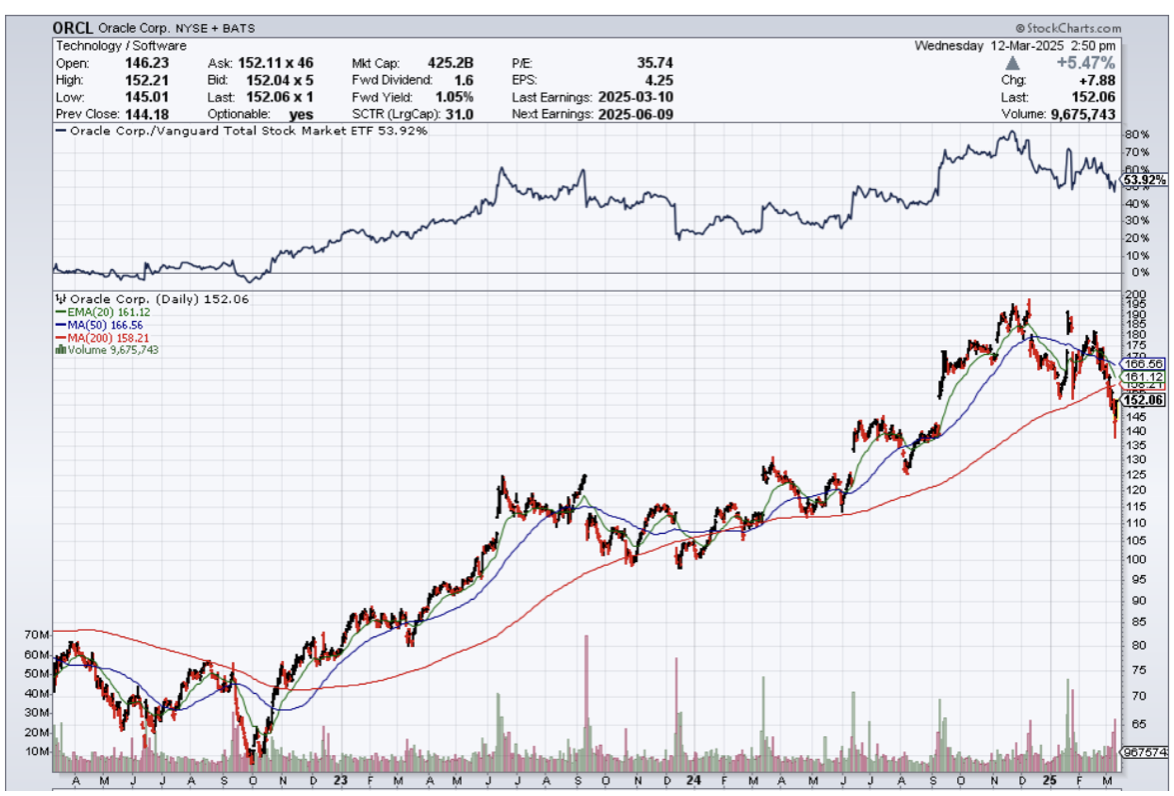

Remember that Oracle’s stock was dead as a doornail a few years ago.

But the AI revolution seemingly revived a slumbering stock jolting it to higher highs.

Before that AI boom, Oracle was known as the company with outdated database cloud software and even today, most people don’t know what they even do.

Oh, how do just a few years change everything?

Realistically, Oracle likely doesn’t have the cash to buy into the asset.

The company is spending much of its cash on building new AI data centers and has over $90 billion in debt, partly due to a prior acquisition. Plus, the infrastructure-focused company has little experience running a consumer-oriented app.

The likelier scenario, and the one that’s under consideration with Trump administration officials, would involve Oracle reprising its role in providing a security backstop for US users’ data backstop would guarantee that TikTok’s US operations under new ownership would not contain a back door that China’s government could exploit.

Under a prior arrangement, the cloud giant would have taken a minority ownership stake in TikTok’s global business and provided technology and data storage services for the app to protect US user data.

But the arrangement hit a snag when officials in Washington and Beijing disagreed over whether ByteDance would maintain any involvement in the new TikTok entity.

The second challenge is more technical. Chinese authorities are unlikely to approve a deal that involves selling the new buyer TikTok’s valuable content algorithm, which determines the posts that users see in their feeds.

We are still trying to analyze where the dust will settle because it is not clear to the outside lens.

As it stands, Oracle pouring capital into AI data centers is a strategic move that has benefited the stock price and there is a high chance that shareholders start to bid up the stock after the macro contagion passes.

If somehow Oracle can even finagle a massive contract to managing TikTok’s data, I do believe the stock will be up 12-15% on that news. That development isn’t in the price yet and investors haven’t been sniffing it out yet.

In short, there is a great deal of upside potential in Oracle’s share price and outsiders shouldn’t minimize or water down the possibility for a short-term short squeeze of monumental proportions.

At the very minimum, it is hard to bet against Oracle even if the stock is down YTD by 8% and investors should expect some sort of appreciation when the broader landscape settles down.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-19 14:02:292025-03-19 15:57:44One To Keep An Eye Out For

If readers want to know if the Oracle AI story is dead or not, then listen here.

The story is still alive, so don’t give up on a good thing.

Oracle is getting swept up with the wider macroeconomic scare that has been triggered by geopolitics.

The fear porn has reached fever pitch and is causing tech stocks to detour from their usual self.

The question now is if the sabre-rattling will result in the economic recession we have been waiting 6 years for.

The flood of government money for at least 4 of those years carried spending habits even if those jobs were unproductive or fraudulent.

As it relates to Oracle’s business model, there is no recession in the sub-sector they are in, but I believe they chose to tank the earnings result since all equities were getting dragged down.

The truth is that Oracle’s business is experiencing great growth in the cloud, and AI demand is accelerating sales growth.

The macroeconomic volatility gave Oracle’s management the perfect excuse to guide down since a high forecast would have resulted in a selloff anyway.

Oracle's leadership encouraged investors to focus on the potential for its cloud business to benefit from enterprise AI spending.

A growing backlog for cloud services is giving the company clear visibility for beating growth metrics.

Meanwhile, sales of Oracle's closely watched cloud-infrastructure business increased 49%, compared with 52% growth for the segment in Oracle's November-ended quarter. Oracle's guidance for the May-ending quarter of 9% revenue growth missed previous forecasts of 9.5% growth.

Oracle's cloud infrastructure business is racing to build out computing capacity for AI startups and other users of the cloud. The Oracle Cloud Infrastructure business rents computing power to other companies, competing against much larger hyperscalers Amazon.com (AMZN), Microsoft (MSFT), and Alphabet's (GOOGL) Google.

Chairman and Chief Technology Officer Larry Ellison said that Oracle is on track to double its data-center capacity during the calendar year. The company now expects capital expenditures to grow to $16 billion for its May-ending fiscal 2025, roughly doubling from a year earlier.

Ellison appeared at the White House in late January with President Donald Trump, OpenAI leader Sam Altman, and SoftBank Chief Executive Masayoshi Son to announce an AI infrastructure effort costing $100 billion called Stargate.

While tight data center capacity has demanded some patience from investors, I believe that we move past some of the capacity constraints in the second half of this calendar year.

The deep selloff from $190 per share to $140 has to hurt.

It was just only a short time ago when Oracle was a deadbeat tech stock left behind by the likes of Apple and Facebook.

They have reinvented themselves as an AI infrastructure company, and that has done wonders for their stock.

When they were down in the dumps, ORCL stock was trading below $50, so we are a far cry from that.

Once the tech market gets its mojo back, ORCL will definitely return back in form to that buy the dip stock that did so well in 2023 and 2024.

Just bide your time until we can jump back into ORCL.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-12 14:02:482025-03-12 16:10:23Should I Care About Oracle?

Last weekend, while organizing my home office, I stumbled across an old COVID vaccination card. Remember those? It got me thinking about Moderna (MRNA), the biotech darling that went from relatively unknown to household name faster than you can say "messenger RNA."

Now, in early 2025, this once up-and-coming company is already facing what my grandmother would call "champagne problems" - too much cash to be broke, but burning through it faster than a Tesla (TSLA) on Ludicrous mode.

First, let's talk about this biotech's cash burn. In just nine months of 2024, Moderna torched through over $4 billion - that's the same amount they burned in all of 2023, suggesting their cash cremation rate is actually accelerating.

This acceleration in spending wouldn't be as worrying if they had endless reserves, but their current position shows $7 billion in cash and $2 billion in non-current investments.

The math isn't complex: at this burn rate, their runway is shorter than many investors realize.

The recent Health and Human Services (HHS) grant of $176 million in July 2024 for bird flu research barely registers on their financial statements.

While we've seen about 70 bird flu cases in the U.S. with one fatality in an elderly patient with underlying conditions, this isn't going to be another COVID-style revenue stream.

I've analyzed enough pharmaceutical companies to know that betting on another pandemic windfall is like expecting lightning to strike twice in the same spot.

What really interests me is Moderna's position in the competitive landscape. I spent last week analyzing patent data and geographic reach metrics across the industry.

First, you've got the old-guard pharma giants like Novartis (NVS), Sanofi (SNY), and Johnson & Johnson (JNJ), who have been at this game since before mRNA was a gleam in a scientist's eye.

Then, there are companies like BioNTech (BNTX) and Roche (RHHBY) with significantly higher geographic reach, while Replimune Group (REPL) and CRISPR Therapeutics (CRSP) demonstrate superior application diversity.

In comparison, Moderna's position in this landscape shows relatively low scores on both metrics - not exactly what you want to see from a company burning cash at this rate.

Stéphane Bancel, Moderna's CEO, recently outlined their pipeline: 2 approved medicines, 7 Phase 3 trials, and 45 candidates in development. They're also targeting $1.1 billion in annual R&D cost reductions by 2027.

But here's what keeps bothering me: their SG&A expenses have ballooned to nearly 10 times their pre-COVID levels, yet management is focusing on R&D cuts instead of addressing this administrative bloat.

The insider trading patterns since early 2024 haven't exactly inspired confidence either.

When I see heavy selling from insiders while a company is promising future breakthroughs, I can't help but remember all the biotech stories I've covered where the promise didn't match the reality.

Speaking of promises, Oracle's (ORCL) Larry Ellison recently made headlines talking about 48-hour personalized cancer vaccines using AI and robots.

While the technology sounds promising, I'm more interested in the practical path to profitability. Moderna isn't alone in this race, and their well-capitalized competitors have the luxury of funding similar development programs while maintaining positive cash flow.

Given Moderna's cash burn trajectory, their next three quarters will be telling.

I'll be watching that $4 billion nine-month burn rate closely, along with their progress on cost reductions - particularly those inflated SG&A expenses that management seems reluctant to address.

I'm keeping my old vaccination card as a reminder of Moderna's impressive COVID-19 achievement, but I'm not ready to bet on lightning striking twice.

Sometimes the hardest part of investing is knowing when to appreciate history without banking on its repeat performance.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-02-04 12:00:322025-02-04 12:06:04Too Rich To Fail, Too Expensive To Succeed

Oracle plans to increase their amount of AI data centers from its current 85 to 2,000.

That is the most important number to take away from an analysts meeting with Oracle management.

Readers should ride on the coattails of this AI data center firm as throw billions upon billion at increasing the amount of AI infrastructure.

Readers absolutely need to know that a great swath of tech is dead and not innovating - growth rates collapsing faster than the U.S. birth rate.

It is important to position yourself at the cutting edge of innovation and growth and that is precisely companies who are knee deep in AI data center infrastructure investments that includes chip companies that produce GPUs like Nvidia.

In fact, Nvidia supplies Oracle and most other tech companies with data center chips called graphics processing units (GPU).

Nvidia has experienced an eye-popping surge in its revenue over the past year, and GPU demand continues to outstrip supply.

Oracle's data centers are unique because they are automated. Each one is operationally identical regardless of its size, and since they don't require human workers, it allows the company to build them quickly. Plus, Oracle's RDMA (random direct memory access) GPU networking technology allows data to flow from one point to another more quickly than traditional Ethernet networks.

Oracle has 85 data centers up and running with 77 more under construction as of the end of August.

Next year, Oracle intends to offer a cluster of 131,072 GPUs, which is a big step up from its largest clusters now, at around 32,000 GPUs. But there's another difference:

The new cluster will use Nvidia's latest Blackwell chips, which can perform AI inference at 30 times the pace of its flagship H100, which Oracle currently uses. Theoretically, it's going to allow developers to build the largest AI models in history.

In fact, Oracle spent $6.9 billion on data center infrastructure in 2024.

Oracle is going after the best technology in Nvidia’s Blackwell chip which is a solid reason to get interested in Oracle stock.

I don’t believe AI infrastructure spend will dissipate anytime soon and as the rest of the tech sub-sector growth falters, this one little area of AI will hold up the rest of tech.

This is why we are seeing extreme concentration of outperformance in just a handful of tech names and I don’t believe we will experience a scenario of spreading the wealth around to the less growth oriented subsectors.

In fact, I think the concentration will become even more outsized in a handful of names as a winner takes all mentality wins out in the tech sector.

We are just scratching the surface in what will become a massive explosion of AI data centers everywhere to satisfy the extreme demand of computing that it will require to pull this off.

Nothing indicates that this would be the wrong trend to follow and that assumption follows through to the astronomically high stock prices of the companies involved.

Oracle is one of these companies that readers should not dismiss.

It is at the heart of the AI infrastructure story that has legs.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-25 14:02:422024-09-25 15:16:03From 85 to 2,000 AI Data Centers

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.