Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

International Business Machines Corporation (IBM) shares do not need the squeeze of a contentious trade war to dent its share price.

It is doing it all by itself.

Stories have been rife over the past few years of shrinking revenue in China.

And that was during the golden years of China when American tech ran riot on the mainland before the dynamic rise of Baidu (BIDU), Alibaba (BABA), and Tencent, otherwise known as the BATs.

Then the Oracle of Omaha Warren Buffett drove a stake through the heart of IBM shares earlier this year by announcing he was fed up with the company’s direction and dumped a 35-year position.

Buffett unloaded all of his shares in favor of putting down an additional 75 million shares in Apple (AAPL) in the first quarter of 2018.

Topping off his Apple position now sees Buffett owning a mammoth 165.3 million total shares in the resurgent tech company.

Buffett’s shrewd decision has been rewarded, and Apple’s stock has rocketed more than 20% since he jovially declared his purchase in May.

IBM has been a rare misstep for Buffett, who took a moderate loss on his IBM position disclosing an average cost basis of $170 on 64 million shares that Berkshire bought in 2011.

IBM has flatlined since that Buffett interview, and slid around 25% since its peak in mid-2014.

IBM is grappling with the same conundrum most legacy companies deal with – top line contraction.

In 2014, IBM registered a tad under $93 billion in annual revenue, and followed up the next three years with even lower revenue.

A horrible recipe for success to say the least.

In an era of turbo-charged tech companies whose value now comprise over a quarter of the S&P, IBM has really fluffed its lines.

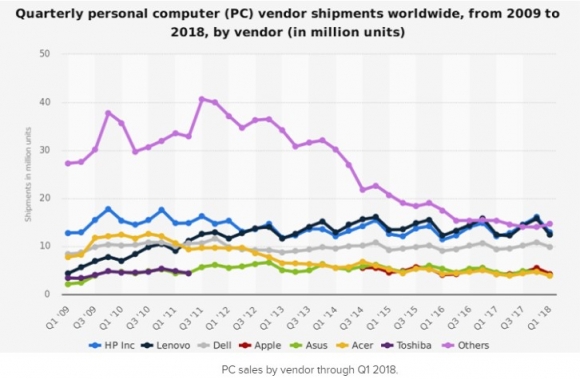

IBM’s prospects have been stapled to the PC market for years.

A recent JP Morgan note revealed the PC market could contract by 5% to 7% in the fourth quarter because of CPU shortages from Intel (INTC).

The report’s timing couldn’t have been worse for IBM.

The PC industry has been tanking for the past six consecutive years unable to shirk shrinking volume.

Intel is another company I have been lukewarm on lately because it is being outmaneuvered by chip competitor Advanced Micro Devices (AMD).

Even worse, this year has been a bad one for Intel’s management, which saw former CEO Brian Krzanich resign for sleeping with a coworker.

The poor management has had a spillover effect with Intel needing to delay new product launches as well.

To read more about my timely recommendation to pile into AMD in mid-August at $19, please click here.

Meanwhile, AMD shares have gone parabolic and surpassed an intraday price of $34 recently.

Investors should ask themselves, why invest in IBM when there are so many other tech companies that are growing, and growing revenue by 20% or more per year?

If IBM does manage to eke out top line growth in 2018, it will be by 1% to 2%, similar to Oracle’s recent performance.

Unsurprisingly, the price action of Oracle (ORCL) for the past year has been flatter than a bicycle ride around Beijing.

Live by the sword and die by the sword.

Thus, the Mad Hedge Technology Letter has been ushering readers into high-performance stocks that will bring technological and societal changes.

If you put a gun to my head and forced me to give sage investment advice, then the answer would be straightforward.

Buy Amazon (AMZN) and Microsoft (MSFT) on the dip and every dip.

This is a way to print money as if you had a rich uncle writing you checks every month.

Legacy tech is another story.

The IBMs and the Oracles of the world are bringing up the tech sector’s rear.

To add insult to injury, the lion’s share of IBM’s revenue is carved out from abroad, and the recent surge in the dollar is not doing IBM any favors.

IBM’s Watson initiative was billed as the savior for Big Blue.

The artificial intelligence initiative would integrate health care data into an actionable app.

The expectations were high hoping this division would drag up IBM from its long period of malaise.

IBM bet big on this division ploughing more than $15 billion into it from 2010-2015, predicting this would be the beginning of a new renaissance for the historic American company.

This game changing move fell on deaf ears and has been a massive bust.

IBM swallowed up three companies to ramp up this shift into the AI world - Phytel, Explorys, and Truven.

The treasure trove of health care data and proprietary analytics systems these companies came with were what this division needed to turn the corner.

These three companies were strong before the buy out and engineers were upbeat hoping Watson would elevate these companies to another level.

Wistfully, IBM Management led by CEO Ginni Rometty grossly mishandled Watson’s execution.

Phytel boasted 160 engineers at the time of IBM’s purchase and confusingly slashed half the workforce earlier this year.

Engineers at the firm even lamented that now, even smaller firms were “eating them alive.”

Unimpressed with the direction of the artificial intelligence division at IBM, many of these three companies’ best and brightest engineers jumped ship.

The inability for IBM to integrate Watson reared its ugly head in plain daylight when MD Anderson Cancer Center in Texas halted its Watson project after draining $62 million.

This was one of many errors that Watson AI accrued.

The failure to quicken clinical decision-making to match patients to clinical trials was an example of how futile IBM had become.

In short, a spectacular breakdown in execution mixed with an abrupt brain drain of AI engineers quickly imploded the prospect of Watson ever succeeding.

In 2013, IBM confidently boasted that Watson would be its “first killer app” in health care.

Internal leaks shined a brighter light on IBM’s subpar management skills.

One engineer described IBM’s management as having “no idea” what they were doing.

Another engineer said they were uncertain of a “road map” and “pivoted many times.”

Phytel, an industry leader at the time focusing on population health management, was bleeding money.

The engineers explained further, chiming in that IBM’s management had zero technical experience that led management wanting to create products that were “simply impossible.”

Not only were these products impossible, but they in no way took advantage of the resources these three companies had at their disposal.

Do you still want to invest in IBM?

Fast forward to today.

IBM is being sued in federal court with the plaintiff’s, former employees at the firm, claiming the company unfairly discriminated against elderly employees, firing them because of their age.

The documents submitted by the plaintiff’s state that “IBM has laid off 20,000 employees who were over the age of 40” since 2012.

This prototypical legacy company has more problems than the eye can see in every nook and cranny of the company.

If you have IBM shares now, dump them as soon as you can and run for cover.

It’s a miracle that IBM shares have eked out a paltry gain this year. And this thesis is constant with one of my overarching themes – stay away from all legacy tech firms with no cutting-edge proprietary technologies and stagnating growth.

________________________________________________________________________________________________

Quote of the Day

“Some say Google is God. Others say Google is Satan. But if they think Google is too powerful, remember that with search engines unlike other companies, all it takes is a single click to go to another search engine,” said Alphabet cofounder Sergey Brin.

Mad Hedge Technology Letter

September 12, 2018

Fiat Lux

Featured Trade:

(HOW TO PLAY “SOFTWARE AS A SERVICE”),

(AMZN), (IBM), (ADBE), (CRM), (BABA), (CSCO), (SAP), (ORCL), (GOOGL)

If you have read any of our content in the first year of the Mad Hedge Technology Letter, the content is distinctly bullish technology stocks.

A fundamental driver propelling this cogent argument is the dominant Software-as-a-Service (SaaS) industry booming inside the confines of Silicon Valley.

If you want to boil down your tech investment thesis to one indispensable rule – only invest in tech companies that carve out prominent SaaS businesses.

If you stick with this nostrum, you will be delivered profits in spades.

We have recently taken in a swarm of new tech letter subscribers and understanding the panacea that is SaaS will entrench your portfolio in a glorious position to reap untold profits.

What is SaaS?

SaaS is a distribution method in which software is diffused to paid subscribers, usually on an annual, reoccurring payment plan, and the software is remotely stored on a centralized cloud platform awaiting use.

Unsurprisingly, SaaS remains the most lucrative segment of the cloud market.

In 2017, the tech industry did $60.2 billion in annual SaaS sales, that number is poised to explode to $117.1 billion in 2021.

The near doubling of sales underscores the robust nature of these tech firms setting up businesses of this ilk, and the positive effects dripping down to the bottom line.

Simply put, no SaaS business, no reason to invest.

SaaS isn’t the only cloud revenue companies can carve out. Tech firms also offer platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS).

However, SaaS is by far the prominent growth lever in the high-margin cloud industry.

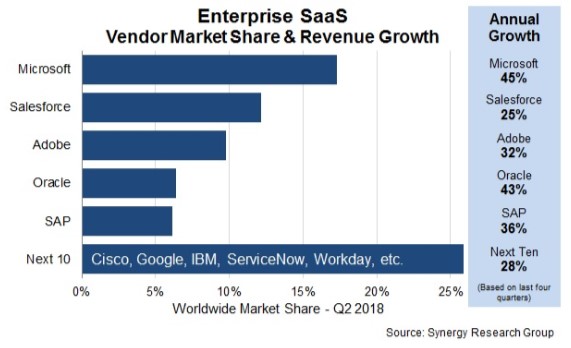

The indomitable presence inside the SaaS industry is Bill Gates’ creation Microsoft (MSFT).

Microsoft leads all companies with a 17% global share of the SaaS market.

The Redmond, Washington, outfit blew past stalwart Salesforce (CRM) nine quarters ago.

Microsoft’s sizzling SaaS business is an oversized contributor to its 45% revenue growth rate, which is head-and-shoulders above the industry average.

Salesforce (CRM), Adobe (ADBE), Oracle (ORCL) and SAP (SAP) fill out the top five largest global SaaS businesses, but it is really a tale of two stories.

Oracle and SAP, which are competing in the same market, are grappling with legacy database businesses and legacy tech, which are punished by investors.

John Dinsdale, a chief analyst at Synergy Research Group, mentioned two outliers of “Cisco (CSCO) and Google too who are making ever-bigger inroads into the SaaS market” leveraging Cisco’s multitude of software assets and Google’s G Suite.

The thing that makes SaaS the x-factor for tech companies is that inevitably every company from every walk of life will adopt this mode of software, giving legs to this distribution model.

Vendors are scrambling to put together some resemblance of a SaaS product together, and this trend is a vital contributor to an industry that is growing 32% YOY worldwide.

Kevin Cochrane, chief marketing officer of SAP Customer Experience lay bare his thoughts about this type of service describing it as the “Golden Age of SaaS.”

Companies are becoming digital first from end to end, explaining the sharp rise in IT professional salaries and rise in quality software products.

As we look around the corner to the IaaS part of the cloud industry, which is growing at around 30% YOY, there is one dominant player, and everybody knows its name.

Amazon (AMZN) is the No. 1 vendor with Microsoft, Alibaba (BABA), Google, and International Business Machines Corporation (IBM) trailing behind.

The top four IaaS players have carved out a total of 73% of the global market ravaging any resemblance of competition.

Amazon is the industry standard with the best record of customer success.

If Amazon branched off into the SaaS industry, it could unlock an additional $100 billion in annual revenue.

A shift into this direction could pad Amazon’s margin’s even more after successfully boosting North American e-commerce margins from 2.4% to 4.7%.

It’s not entirely inconceivable that Amazon could break the $2 trillion valuation in three to five years, as its revved up digital ad business registered growth of 129% YOY last quarter.

Microsoft seized the runner-up position in the IaaS market to Amazon by growing 98% YOY with sales eclipsing $3.1 billion in 2017.

Wherever you turn, whether toward the cloud business or gaming, investors can find Microsoft making sales.

Microsoft has been a favorite of the Mad Hedge Technology Letter and it’s hard pressed to find a better public tech company in operation now.

The SaaS industry is not a one-size-fits-all proposition.

Thus, there is abundant room for niche offerings that quench companies’ demand for specific services.

This is the reason why cloud companies have participated in a non-stop buying binge of smaller companies that fit their needs.

Microsoft purchased developer favorite GitHub for $7.5 billion earlier this year, and similar examples are scattered all over the tech ecosphere.

Artificial Intelligence (AI) will be the kicker that powers SaaS performance to new heights because incorporating this groundbreaking technology will enhance functionality and, in return, raise profits for all involved.

The scalability of SaaS products has allowed companies to offer software for affordable prices allowing the smallest of firms to adopt a digital-first strategy.

This software connects with other software seamlessly integrating an array of productive apps that help teams overperform and overdeliver.

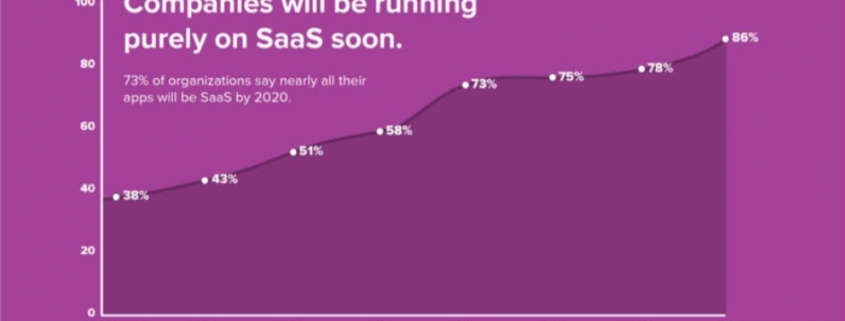

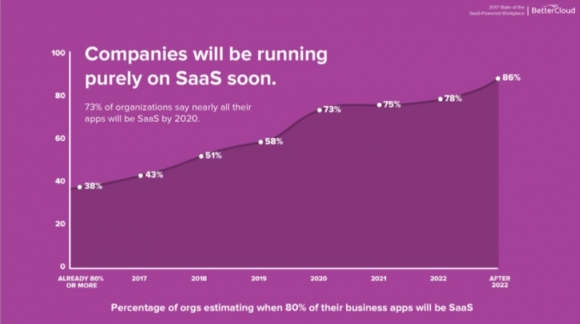

In the American workplace, 73% of companies will be exclusively using SaaS to function by 2020.

American companies are using 16 apps on average per day, a 33% jump in the number of apps they were using just two years ago.

The migration to mobile has swallowed up SaaS products as well with more mobile-specific software rolling out to mobile devices.

The meteoric rise of SaaS offerings has cut IT security budgets substantially as security has been delegated to the cloud instead of in expensive in-house security teams.

No longer do tech firms need to beef up guarding their own gates.

Protection is provided on a centralized cloud with a third-party company ensuring safety.

This development has helped a new industry rise – cloud security.

Whether people realize it or not, the SaaS industry is here to stay and will become more prevalent in every industry going forward.

This is incredibly bullish for companies that sell SaaS products as revenue will continue to rise.

________________________________________________________________________________________________

Quote of the Day

“Growth and comfort do not coexist,” – said CEO of IBM Ginni Rometty.

Mad Hedge Technology Letter

July 19, 2018

Fiat Lux

Featured Trade:

(AVOIDING THE BULLY),

(MSFT), (AMZN), (WMT), (GME), (ORCL), (GE), (CPB)

A bully stealing your lunch is not fun.

Partnering up to subdue a bully isn't only happening on the school playground.

Walmart (WMT) is doing it now, too.

Let me explain.

The Amazon (AMZN) effect is understood as the disruption of traditional brick-and-mortar business by Amazon's domination in e-commerce sales.

This phenomenon was all about how Amazon would take over, and by all means they are, and in brisk fashion.

That is why Amazon trade alerts from the Mad Hedge Technology Letter are nestled away in your email inbox.

Desperate times call for desperate measures.

Amazon competitors are facing an existential crisis they have never seen before.

The newest member of the FANG group, Walmart, is transforming into a tech company, and this metamorphosis is picking up steam.

To read my recent story about Walmart's headfirst dive into India, the newest battleground country, by way of its purchase of Indian e-commerce juggernaut Flipkart, please click here.

The second part of its strategy was revealed by announcing that Walmart would partner with Microsoft's (MSFT) cloud platform Azure to tap into the deep A.I. (artificial intelligence) and machine learning expertise.

If you can't beat them, find another competitor to help you change the status quo.

The five-year deal is a game changer in a coveted cloud industry pitting David vs. Goliath.

Amazon's footprint is wide reaching and bosses 33% of the cloud market it invented, far and away surpassing runner-up Microsoft, which garners just 13% market share.

Microsoft is catching up fast and that 13% was just 10% in 2016.

Microsoft and Walmart have a common foe that haunts them in their dreams.

These companies feel they are better served combining forces than being isolated from each other.

In an exclusive Wall Street Journal interview with Satya Nadella, Microsoft's CEO, Nadella directly confirmed what people already knew.

This strategic move "is absolutely core to this (Amazon threat)."

Walmart will use Microsoft's advanced cloud technology to optimize its operations from managing inventory, selecting the most suitable products to display, and running its equipment efficiently.

In 2016, Walmart's purchase of e-commerce company Jet.com was thoroughly integrated onto the Microsoft Azure. This further cooperation will help boost a company that has been aggressively vocal about its tech exploits.

High-quality products sell themselves and the story has played itself over again.

Microsoft is a master at luring in business through the front door, and padlocking the front gate procuring business for decades.

This case is no different and a vital reason the Mad Hedge Technology Letter has pinned down Microsoft as a top three tech stock.

Walmart also has made it crystal clear that a prerequisite for doing business with them is not doing business with Amazon Web Services (AWS), Amazon's lucrative cloud division.

Any profit dropping down to the (AWS) bottom line is used to wield against the retail landscape, damaging Walmart's prospects.

The Amazon effect is starting to work against Amazon, as the threat is forcing other businesses to adopt the same mind-set as Walmart.

Snowflake Computing, a private data firm focused on warehouse databases established by Bob Muglia in 2014, was exclusively available on the AWS platform.

However, more and more retailers such as Walmart started banging on Snowflake Computing's door demanding that it offer its cloud services on a cloud platform that is not its competitor.

Snowflake Computing obliged and is now up and running on Microsoft Azure.

Can you imagine the competition being able to sift through troves of data understanding every strength and weakness?

It's a one-way street to bankruptcy court.

Perhaps that explains why GameStop (GME) is such a poor performer, as its operations are entirely on (AWS).

GameStop is a stock that I am bearish on, because selling video games as a middleman is a legacy business.

Kids just download everything direct from the manufacturer from their broadband connection, making GameStop's business model obsolete.

It has a turnaround plan, apparently Oracle (ORCL) has one too, but it's barely begun.

Microsoft is a bad choice as well for GameStop, which is heart and center in the video game industry as well.

There are many alternatives; someone should notify recently installed GameStop CEO Daniel A. DeMatteo about one.

(AWS)'s dominance is benefitting Microsoft Azure explaining the rapid pace of cloud market share advancement.

This is just the tip of the iceberg. Walmart has some other irons in the fire.

Enter Project Kepler.

This is Walmart's response to Amazon Go stores, a partially automated retail store with no cashiers or checkout station, which currently has one functional location in Seattle.

Project Kepler is being developed by Jet.com co-founder and CTO Mike Hanrahan. And guess who is providing the technology for this alternative retail experience store - Microsoft.

Microsoft poached a computer vision specialist from Amazon Go who will help develop the appropriate sensors and computer vision algorithms necessary to get this store up and running.

These same sensors can be found in autonomous driving technology.

Shopping cart cameras could also be added to the mix to ensure quality and hopefully avoid the teething pains new technology grapples with.

Microsoft Azure CTO Mark Russinovich commented lately saying firms are on the front foot utilizing "A.I. and machine learning to automate processes to get insights into operations that they didn't have before."

Microsoft is perfectly set up to harvest many of these new contracts.

The deals have started to roll in.

Microsoft is successfully broadening its relationship with GE (GE), using the Azure data analytics capabilities to transform GE Digital's industrial IoT solutions.

This week also saw Microsoft scoop up Campbell Soup Company (CPB) as a new client, which decided on Microsoft Azure to modernize its IT infrastructure.

Campbell Soup will deploy Azure for real-time access to critical operations data, offering deeper intelligence for Campbell's senior management team.

This robust business activity is all because Microsoft is not Amazon, along with having a stellar product about which companies gloat.

Retailers have chosen Microsoft as the cloud platform of choice and expect the majority of retailers to tie their futures to Microsoft.

That's not the only iron in the fire.

Jetblack is another experimental retail service that Walmart is testing as we speak.

The service is still in beta mode in Manhattan targeting urban, high net worth mothers.

It emphasizes a personalized shopping experience in a narrow segment of goods that include household products, cosmetics, health and beauty products.

Shoppers will be able to snap photos of products and send them to Jetblack, receiving them at home with free shipping.

Customer service will be carried out by a high-quality lifelike bot, and Walmart intends to charge a membership fee to take part in this specialized shopping experience.

Microsoft subsidiary LinkedIn has also been leaning more on its parent company's technology lately.

LinkedIn software engineer Angelika Clayton wrote in her blog that "dozens of languages" are being converted into English via Microsoft Translator Text application programming interface, ballooning the candidate database for English speaking headhunters.

Could foreign language learning soon go way of the dodo bird and woolly mammoth?

Machine learning and A.I. have that type of power.

Tech analysts on the street must avoid issuing reports boasting that "everything is priced in," because these tech behemoths are driving innovation faster than people can understand it.

Walmart has turned into one of the most innovative companies around.

Who would have imagined this development a few years ago?

Nobody, not even Walmart itself.

Everything Microsoft touches lately turns into gold, along with being one of the more trusted tech titans out of the motley crew that has ruffled a few feathers this year.

Walmart is aggressively experimenting, systematically attempting to hop on new trends in retail hoping one or two will catch fire.

The credit must go to CEO Doug McMillon who has brought a tech first approach since being installed as CEO in 2014.

Even though conservative Walmart investors have penalized Walmart for the heavy spending, they must come to terms that Walmart's model is plain different now.

It's either spend or die in 2018.

Microsoft is in store to report its status on its pursuit of AWS, and I expect the company to inch closer with each earnings report.

Its outperforming Azure cloud business is in the first stages of a marathon, and sometimes it's not always salubrious to be the schoolyard bully because everybody starts avoiding you like the plague.

________________________________________________________________________________________________

Quote of the Day

"They broke the law on several occasions after being warned," said Larry Kudlow, director of the United States National Economic Council, when asked about Chinese company ZTE, which sold telecommunications equipment to Iran and North Korea.

Mad Hedge Technology Letter

June 25, 2018

Fiat Lux

Featured Trade:

(IT'S NOT HEAVEN FOR ALL CLOUD STOCKS)

(ORCL), (MSFT), (AMZN), (CRM), (GOOGL)

The year of the Cloud takes no prisoners.

Cloud stocks have been on a tear resiliently combating the leaky macro environment.

Many of my cloud recommendations have been outright winners such as Salesforce (CRM).

However, there are some unfortunate losers I must dredge up for the masses.

Oracle (ORCL) announced quarterly earnings and it was a real head-scratcher.

I have been banging on the table to ditch this legacy tech company since the inception of the Mad Hedge Technology Letter.

It was the April 10, 2018 tech letter where I prodded readers to stay away from this stock like the black plague.

At the time, the stock was trading at $45, click here to revisit the story "Why I'm Passing on Oracle."

The first quarter was disappointing and abysmal guidance of 1% to 3% for annual total revenue topped off a generally underwhelming cloud forecast.

Investors spotlight one part of the business requiring the utmost care and nurturing - its cloud business.

The second quarter was Oracle's chance to revive itself demonstrating to investors it is serious about its cloud direction.

What did management do?

They announced a screeching halt to the reporting of cloud revenue and it would avoid reporting on specific segments going forward.

Undoubtedly, something is wrong behind the scenes.

To withdraw financial transparency is indicative of Oracle's failure to pivot to the cloud and this has been my No. 1 gripe with Oracle.

It is simply getting pummeled by the competition of Amazon (AMZN), Alphabet (GOOGL), and Microsoft (MSFT).

Stuck with an aging legacy business focused on database software, transformation has been elusive.

To erect a giant cloak around its cloud business means that growth is far worse than initially thought to the point where it is better to sweep it under the carpet.

Instead of taking a direct hit on the chin, management decided to wriggle itself out of the accountability of bad cloud numbers.

A glaringly bad cloud business should be the cue for management to kitchen sink the whole quarter and start afresh from a lower base.

The preference to shroud itself with opaqueness is bad management. Period.

Instead of turning over a new leaf, Oracle could be penalized on future earnings reports for the way it reports financials for the simple reason it confuses analysts.

Wars were fought for less.

Bad management runs bad companies. The stock has floundered while other cloud stocks have propelled to new heights - another canary in the coal mine.

Amazon and Netflix are two examples of tech growth stocks that have celebrated all-time highs.

Even rogue ad seller Facebook broke to all-time highs lately.

The champagne is flowing for the top-level tech companies.

As expected, Oracle was punished heavily upon this news with the stock down almost 8% intraday to $42.70, and it sits throttled at $43.60 as I write this.

Diverting attention from the cloud will mire this stock in the malaise it deserves. Shielding its investors from the only numbers that really matter will give analysts a great reason to label this dinosaur stock with sell ratings.

Analysts are usually horrific stock predictors, but they will be able to wash their hands of this beleaguered stock.

Even if the stock goes up, analysts will still be geared toward sell ratings.

Oracle reported a $1.7 billion in total cloud revenue last quarter, a disappointing 9% increase QOQ.

Oracle's cloud revenue is only up 25% YOY.

For an up and coming cloud business, the minimum threshold to please investors is 20% QOQ, and the 9% QOQ expansion will do nothing to get investors excited.

The deceleration of growth is frightening for investors to stomach and Oracle's admission the cloud business is uncompetitive will detract many potential buyers from dipping in at these levels.

In short, Oracle is not growing much. There is no reason to buy this stock.

I always divert subscribers into the most innovative tech stocks because they are most in demand from investors.

Innovative inertia has reverberated through the corridors at its massive complex in Redwood City, California.

A major shake out in product development and business strategy is vital for Oracle clawing back to relevance.

This is the fourth sequential quarter with unhealthy guidance.

Much of the weakness comes from Amazon siphoning business out of Oracle.

Completed surveys suggest the conversion to AWS has one clear loser and that is Oracle.

Cloud vendors are now ramping up their smorgasbord of cloud offerings attracting more business.

The second and third cloud players, Alphabet and Microsoft, have been particularly active in M&A, attempting to make a run at AWS for pole position.

It is most likely that Oracle's capital spending will dip from $2 billion in 2017 to $1.8 billion in 2018.

Considering Salesforce spent $6.5 billion on MuleSoft, a software company integrating applications, an annual $1.8 billion capital expenditure outlay is a pittance and shows that Oracle is functioning at a pitiful scale.

Oracle won't be able to make any noteworthy transactions with such a miniscule budget.

Without enhancing its cloud offerings, Oracle will fall further behind the vanguard exacerbating cloud deceleration.

Oracle pinpointed data center expansion as the targeted cloud segment after which they would chase. Oracle will quadruple two data centers in the next two years.

One of the data centers will be placed in China collaborating with Tencent Holdings Limited to satisfy government rules requiring outsiders partnering with local companies.

Saudi Arabia is locked in for a data center, desperate to attract more tech ingenuity to the kingdom.

Saudi Arabia's iconic state-owned oil giant will form an "Aramco-Google partnership focused on national cloud services and other technology opportunities."

It will be interesting going forward to analyze the stoutness of the data center commentary considering foes such as Alphabet are boosting spending.

Alphabet quarterly spend tripled to $7.56 billion QOQ including the $2.4 billion snag of New York's Chelsea Market skyscraper Google will spin into new offices.

Alphabet has splurged on $30 billion on digital infrastructure alone in the past three years.

That bump up in infrastructure spending is to support the spike in computer power needed for the surging growth across Alphabet's ecosystem.

Apparently, Oracle is not experiencing the same surge.

If investors start to question global growth, investors will migrate into the top-grade names and the marginal names such as Oracle will be taken behind the woodshed and beaten into submission.

Oracle is much more of a sell the rally than buy the dip stock fueled by its growth deceleration challenges.

_________________________________________________________________________________________________

Quote of the Day

"If you don't have a mobile strategy, you're in deep turd," - said Nvidia CEO Jensen Huang.

Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Modern tech has an unseen dark side to it.

Coders relish the opaqueness surrounding the industry infatuated with developing the next big thing to take Silicon Valley by storm.

There is nothing opaque about the Mad Hedge Technology Letter.

I grind out recommendations and you follow them. Period. End of story.

To put it mildly, the letter has gotten off to a flying start since its inception in February 2018, and there is no looking back, only looking forward.

Micron (MU), Red Hat (RHT), Microsoft (MSFT), and Intel (INTC), just to name a few, have been solid recommendations standing up to all the nonsense and mayhem permeating throughout the periodically irrational markets.

Have you noticed lately when you open up the morning paper while sipping on a steaming mug of Blue Bottle Coffee, that almost every story is about technology?

It's not a mistake. I swear.

Technology is permeating into the nooks and crannies of our society and the leaders of this movement are laughing all the way to the bank.

One of those aforementioned pioneers is no other than local lad, Salesforce CEO and perennial Facebook basher Marc Benioff.

I recommended Salesforce at $110 and it was one of the first positions in the Mad Hedge Technology portfolio.

You can't blame me.

I saw this stock pick from a million miles away and I will explain why.

Salesforce set ambitious targets that nobody thought were realistic at the time.

How high in the sky does Benioff want to build his castles?

By 2022, Marc Benioff set out sales targets of a colossal $20 billion per year.

Then Benioff gushed that Salesforce would pass the $40 billion mark, done and dusted by 2028 and $60 billion by 2034.

Remember that tech CEOs are incentivized to forecast ludicrous sales targets because it lures in the unknowledgeable investor.

Unknowledgeable or pure genius, it does not matter, Salesforce is an emphatic buy.

Salesforce is the ultimate growth stock.

In 2016, annual revenue came in at $6.67 billion, which is about the same size as a middle level semiconductor company.

They followed that up with $8.38 billion in 2017, demonstrating the parabolic shaped trajectory of the company.

At the end of fiscal year 2017, Salesforce announced that it expects revenue of around $12.60 billion in 2019.

The latest earnings report, Benioff disclosed full year guidance of $13.13 billion.

This puts Salesforce in the running to achieve its lofty aspirations.

Apparently, the castles Benioff is building aren't in the sky after all.

Theoretically, if Benioff expands the business into a $16 billion to $16.5 billion business by 2019, Salesforce will have a more than likely chance to pass the $20 billion mark by the end of 2020, a full two years than initially thought.

Salesforce will have ample wiggle room on the way to $20 billion if it is 2022 for which it aims.

Why am I rambling on about revenue?

It's the only metric that Salesforce investors value.

The company registered two straight years of less than $200 million in profits then followed it up with a less than stellar 2016 where it lost almost $50 million.

Don't expect any dividends from this neck of the woods anytime soon especially after acquiring MuleSoft, an integration software company, for $6.5 billion last quarter.

This purchase will add another $315 million of annual revenue to Salesforce's quest of eclipsing its future sales targets. This was after MuleSoft made $296.5 million in 2017 before it became a part of Marc Benioff's stable.

Benioff has proved a shrewd dealmaker, taking advantage of cheap capital to add suitable parts to his business.

Since 2016, Benioff has snapped more than 50 niche software companies that he rebrands as Salesforce products and sells them as add-on products.

This is further evidence that any funds available will be allocated toward reinvestment into products and services deeming any future dividend inconceivable, especially with the elevated revenue targets to surpass.

As for the business. Do we still need to talk about it?

Rip-roaring growth was seen across the board with total revenue increasing 25%.

Investors should stay away from any cloud company that is growing less than 20%.

Market intelligence firm International Data Corporation (IDC) voted Salesforce as the No. 1 client relationship management (CRM) platform for the fifth consecutive year.

It is the industry leader in sales, marketing, service, and increased market share in 2017, more than its closest competitors.

Larry Ellison must be tearing his hair out as Oracle's (ORCL) share price has been excommunicated to purgatory indefinitely.

Oracle is a company that I have been pounding on the tables to stay away from.

The Mad Hedge Technology Letter seldom recommends legacy companies that are still legacy companies.

Driving past his former estate, emanating from a sparkling perch in Incline Village overlooking Lake Tahoe, my neighbor gives me the goose bumps.

The property was later sold for $20.35 million. All told, Larry has around $100 million invested in real estate dotted around Incline Village. I sarcastically mentioned to him last time we bumped into each other to call me immediately when his $90 million estate in Kyoto, Japan, hits the market.

Oracle's position in the pecking order is a telltale sign of the inability to land the creme de la creme government contracts that ostensibly fall into Amazon (AMZN), Alphabet (GOOGL), and Microsoft's lap.

And it's not surprising that Larry is spending more time tending to his vast array of glittering luxury properties around the world rather than running Oracle.

Oracle is like a deer caught in the headlights and Marc Benioff is at the wheel.

On the Forbes 500 rankings, Salesforce has moved up almost 200 spots.

This position will rise as Salesforce is under contract booking a further $20.4 billion of commitments driven by its subscription services offering cloud products.

On the domestic contract front, it was much of the same for Salesforce, which inked premium deals with the U.S. Department of Agriculture, Kering, and sports apparel giant Adidas.

International companies such as Philips and Santander UK are expanding their relationships with Salesforce. A firm nod of approval.

Salesforce has been voted in the top three of most innovative companies for the past eight years by reputable Forbes magazine. The list was started in 2011, and it has never dropped out of the top three.

The gobs of innovation are the main logic behind the top five financial institutions expanding their relationship with Salesforce by an extra 70%.

Once companies start using the CRM platform, they become mesmerized with the premium add-ons that help companies run more efficiently.

Benioff has been a huge proponent of artificial intelligence (A.I.) and is an outsized catalyst to product enhancement gains.

Salesforce has taken Einstein, it's A.I. platform, and allowed all the applications to run through it.

The integration of Einstein has resulted in more than 2 billion correct predictions per day paying homage to the quality of A.I. engineering on display.

Instead of hiring a whole team of in-house data scientists, Salesforce is A.I. functionality by the bucket full and it is easy to use on its platform.

In some cases, incorporating Salesforce's A.I. into the business has bolstered other companies' top line by 15%.

Often, Salesforce's A.I. tools are declarative meaning the technology can identify solutions without a fixed formula.

Benioff has choreographed his strategy perfectly.

He is betting the ranch on unlocking data from legacy companies that migrate to his platform.

MuleSoft will help in this process of extracting value, then A.I. will supercharge the data, which is being unlocked.

What does this mean for Salesforce?

Higher revenue and more clients leading to accelerated growth. The share price has powered on north of $130, and after I recommended it at $110, I am convinced this stock will surge higher.

Salesforce is an absolute no-brainer buy on the dip.

Growth Means Shiny New Office Buildings

_________________________________________________________________________________________________

Quote of the Day

"If we become leaders in Artificial Intelligence, we will share this know-how with the entire world, the same way we share our nuclear technologies today." - said current President of Russia, Vladimir Vladimirovich Putin.