Global Market Comments

September 19, 2025

Fiat Lux

Featured Trade:

(SEPTEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(GS), (HOOD), (DAX), (SPY), (TLT),

(GLD), (MSTR), (PFE), (FCX), (BITO)

Global Market Comments

September 19, 2025

Fiat Lux

Featured Trade:

(SEPTEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(GS), (HOOD), (DAX), (SPY), (TLT),

(GLD), (MSTR), (PFE), (FCX), (BITO)

Mad Hedge Biotech and Healthcare Letter

March 20, 2025

Fiat Lux

Featured Trade:

(WHEN SILENCE IS GOLDEN)

(ALNY), (PFE)

Mad Hedge Biotech and Healthcare Letter

March 20, 2025

Fiat Lux

Featured Trade:

(EVEN A PIG COULD MAKE MONEY HERE)

(OGN), (MRK), (RHHBY), (BAYRY), (PFE), (AZN)

I was camped out in Kyiv the other month when news of Organon's (OGN) earnings hit my phone.

While Russian drones buzzed overhead, I was studying pharmaceutical balance sheets—talk about surreal. Did I mention I've led a strange life?

In mid-February, Organon pleasantly surprised me with Q4 2024 results. Hadlima, their biosimilar to Humira, rocketed to $44 million in quarterly sales, up 83.3% year-on-year.

Meanwhile, Organon's dividend yield sits at a whopping 7.32%, blowing away the healthcare sector average.

Let me be blunt: this is an income investor's dream hiding in plain sight.

Organon emerged in 2021 when Merck (MRK) spun off its women's health, biosimilars, and off-patent drugs businesses. This allowed Merck to focus on its immunology and oncology pipeline while Organon became a pure-play commercial entity.

These spinoffs often create enormous value that the market misses in the early years.

Organon's share price has been trading sideways since early 2025 despite several wins: commercializing Hadlima, acquiring Dermavant, and maintaining a 23% operating margin even as some medications face generic competition.

The market clearly isn't paying attention. When stocks with this kind of dividend yield maintain solid margins, my antennae start twitching.

Their recent Phase 3 ADORING 3 study showed that even 79.8 days after stopping Vtama treatment, atopic dermatitis remained mild. That's patient retention gold, folks.

When patients can stop medication and still see benefits almost three months later, that's the kind of sticky customer base pharmaceutical execs dream about.

Revenue hit $1.59 billion in Q4 2024, down just 0.63% year-over-year but up 0.63% quarter-over-quarter.

Renflexis sales reached $64 million, down 16.9% due to competition from other Remicade biosimilars and superior new medications like AbbVie's (ABBV) Skyrizi.

But here's where things get interesting—this sales decline was expected and already priced in. Organon isn't being valued in Renflexis's future.

The real stars? Nexplanon and Vtama. Nexplanon sales reached $258 million in Q4, up 11.7% year-on-year.

Even better, its patent protection runs until August 2030. CEO Kevin Ali expects it to "comfortably get beyond $1 billion in 2025."

When a CEO uses words like "comfortably" about billion-dollar projections, I tend to listen.

Vtama, acquired in the $1.2 billion Dermavant purchase, brought in $12 million in partial Q4 sales.

The FDA expanded its label in December 2024 to include atopic dermatitis in patients over age 2—a condition affecting 31.6 million Americans. This approval significantly expands its market potential.

Remember, blockbuster drugs don't announce themselves with trumpets—they sneak up on you through expanded indications and growing prescriber bases.

Now, many folks will point to Organon's debt—$8.36 billion at 2024's end. But that's lazy analysis.

Look deeper and you'll see its net debt/EBITDA ratio improved from 5.01x to 4.74x over 12 months. They're steadily strengthening their financial position.

I've watched this happen before with pharma spin-offs—initial debt concerns gradually fade as strong cash flows tackle the balance sheet.

Management knows what they're doing. For 2025, they forecast a slight revenue dip but improved EBITDA margins of 31-32%, outperforming competitors like Perrigo, Alvotech, and Amneal.

In the broader pharmaceutical landscape, Organon competes with heavyweights like Roche (RHHBY), Ferring Pharmaceuticals, Bayer (BAYRY), Pfizer (PFE), and AstraZeneca (AZN)—but with a more specialized focus that gives them maneuverability these giants lack.

Wall Street's average price target is $20.50, suggesting a 33.9% upside. When was the last time you saw a 7.32% dividend yield with 33.9% upside potential?

I project non-GAAP EPS to reach $4.52 by 2029, slightly above analyst estimates, driven by Hadlima, Nexplanon, and Vtama growth, plus upcoming biosimilars HLX14 and HLX11. My friends at major healthcare funds are starting to take notice, but the broader market hasn't caught on yet.

At $15.31 per share, Organon trades at a non-GAAP P/E of 3.39x—80.8% below the sector median and 25.7% below its 5-year average. That's not just cheap—that's backing up the truck cheap.

You know what they say about bears and bulls making money, while pigs get slaughtered? Well, at these valuations, even a pig could make money on Organon.

Mad Hedge Biotech and Healthcare Letter

February 11, 2025

Fiat Lux

Featured Trade:

(SPLICING THROUGH SKEPTICISM)

(CSRP), (VRTX), (AMZN), (TSLA)

Mad Hedge Biotech and Healthcare Letter

February 6, 2025

Fiat Lux

Featured Trade:

(YOU MIGHT NEED ASPIRIN FOR THIS ONE)

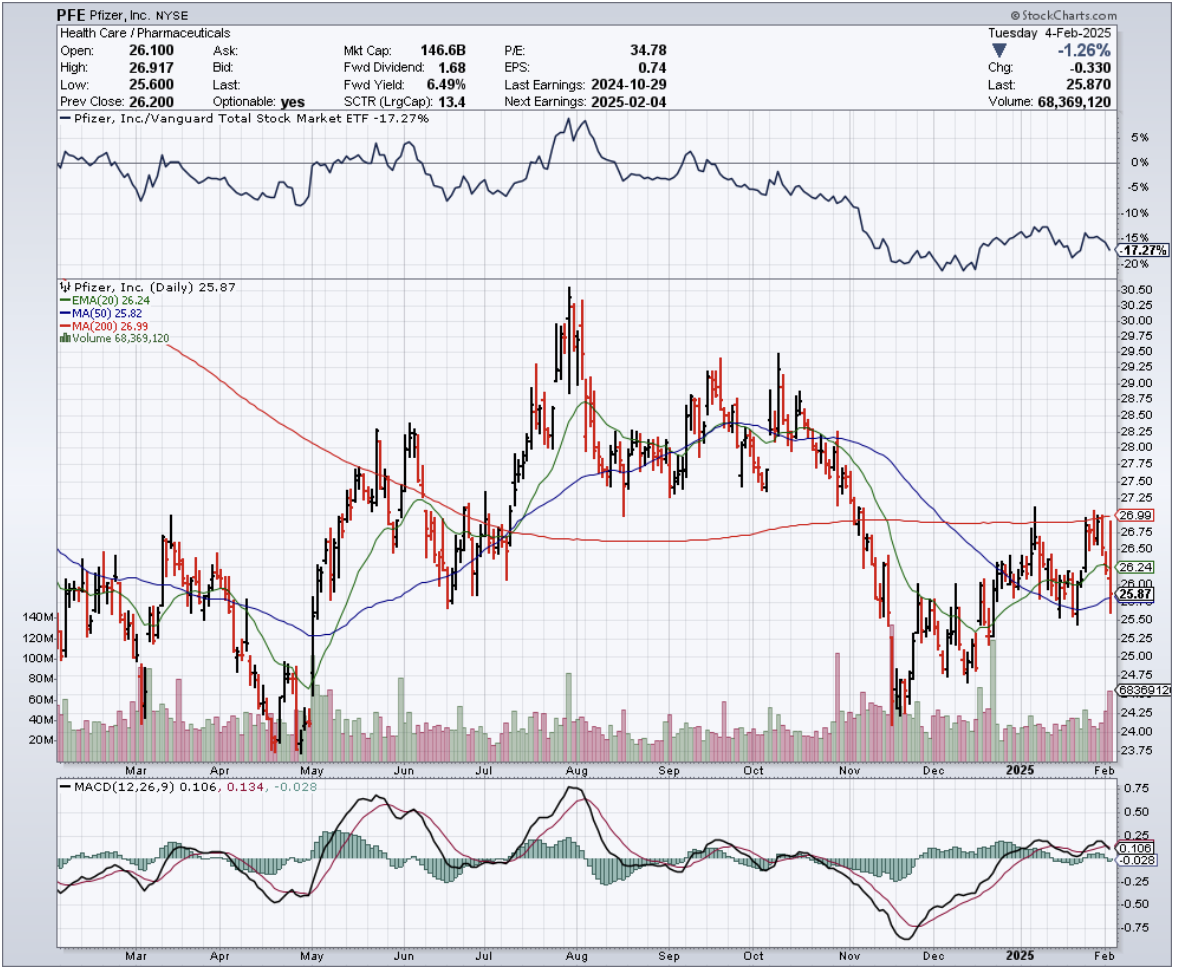

(PFE)

Last Tuesday, while filing away some tax documents, I found myself staring at an old prescription bottle from 2020. The Pfizer (PFE) logo caught my eye, and ironically, that same morning they dropped their Q4 earnings report.

The timing felt symbolic – much like that old bottle, Pfizer's COVID glory days are now just a memory on their financial statements.

The numbers looked good on the surface. EPS of $0.63 beat expectations by $0.17, and revenue came in at a healthy $17.8B, crushing estimates by $540M.

But in the pharmaceutical world, today's blockbuster is tomorrow's generic, and Wall Street knows it. After all, the market's reaction was about as enthusiastic as a patient reading medication side effects.

Let me paint you a picture of what we're dealing with here. Imagine going from making $100.3B in 2022 (those glory days of COVID) to $58.5B in 2023. That's not a haircut – that's a full-blown scalping.

Sure, they bounced back to $63.6B in 2024, but their 2025 guidance of $61.0B to $64.0B suggests they're treading water at best.

Now, here's where it gets interesting, and not in a good way. Remember how I always tell you to look under the hood? Well, Pfizer's engine is about to lose some major parts.

By 2030, they're saying goodbye to patents on Eliquis (a $6.7B revenue generator) and Ibrance (worth $4.8B). That's like losing your two best-performing stocks in your portfolio – it hurts.

Speaking of pain, I had lunch last week with a pharmaceutical industry veteran who couldn't stop talking about the "LOE wave" – that's "loss of exclusivity" in pharma-speak. CEO Albert Bourla puts it at about $17-18 billion in lost revenue over the next 3-4 years.

To put that in perspective, that's like losing the annual GDP of Mongolia. The company's solution? They're promising to deliver $20 billion in new revenues by 2030 through their pipeline of new drugs.

One bright spot worth watching is their oncology division, which grew an impressive 27.4% year-over-year in 2024.

Their promising candidate Atirmociclib, a CDK4i inhibitor for metastatic breast cancer, enters Phase 3 studies in the first half of 2025.

With a 44% historical success rate for these types of studies, it's targeting a massive market – the global breast cancer therapeutics market hit $34.63 billion in 2024 and is expected to reach $89.01 billion by 2034, growing at a healthy 9.90% annually.

That's the kind of growth potential that gets my attention.

The stock currently sports a 6.7% dividend yield, which might look tempting – like that last piece of chocolate cake in the refrigerator at midnight.

But here's the rub: pharmaceutical companies are like Silicon Valley startups with lab coats. They constantly need to innovate just to stay alive. It's not enough to have one hit wonder – you need a whole playlist of blockbusters.

Trading at 8.91x forward earnings with a PEG ratio of 0.20 and 2.5x price/sales, Pfizer does look cheap. But as I always say, sometimes things are cheap for a reason.

Want a shocking comparison? While attending the J.P. Morgan Healthcare Conference, I noticed that analysts are projecting Pfizer's 2029 revenues to be over $5 billion lower than 2024. That's not exactly the inspiring growth story I was hoping to hear.

For those of you hunting for yield (and I know many of you are), let me give you a reality check. That juicy 6.7% dividend looks appetizing until you realize it comes from a company that needs to spend billions just to replace what it's about to lose.

While I love a good yield as much as the next investor, watching a pharmaceutical company's patents march toward expiration is about as comforting as sitting in a dentist's waiting room.

Sometimes the best high-yield investment is the one you don't make – at least until the business fundamentals match the dividend's promise.

Want my advice? Keep an eye on their oncology developments, but keep your powder dry. There's a difference between buying a great company and buying a great stock at the right time.

Right now, Pfizer needs to prove it can fill an $18 billion revenue gap before I'm ready to write them a prescription for my portfolio.

Mad Hedge Biotech and Healthcare Letter

January 28, 2025

Fiat Lux

Featured Trade:

(READY, RESET, GO)

(JNJ), (AAPL), (PFE), (ABBV), (RHHBY), (AZN), (SNY), (NVS)

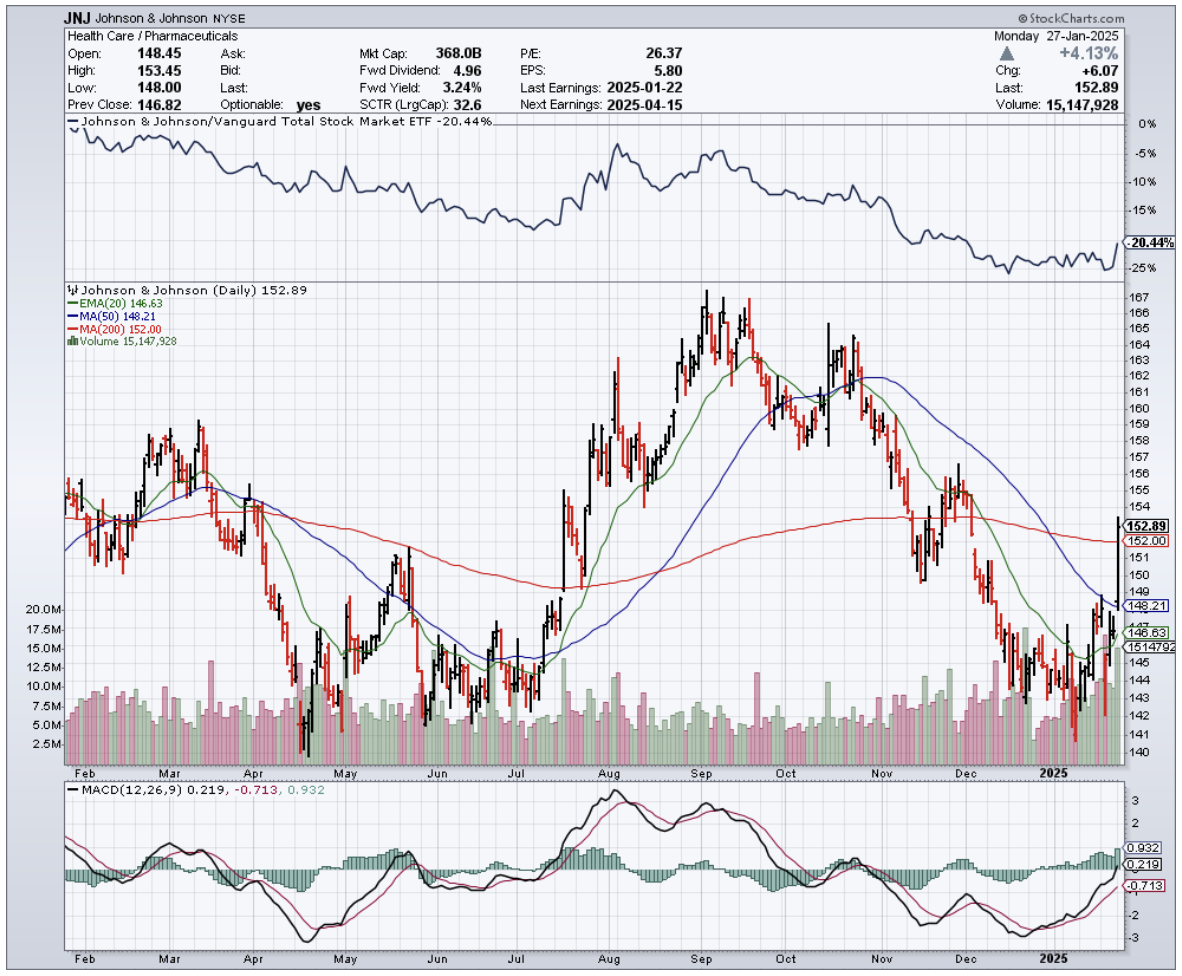

I had to laugh when I saw Johnson & Johnson's (JNJ) Q4 earnings hit my screen earlier this month.

Here we have Wall Street wringing its hands over a slight revenue miss, sending shares down 3.5%, while management is busy plotting its path to pharma industry dominance.

The numbers tell an interesting story.

Q4 revenues grew 5.3% (or 5.7% on an adjusted operational basis) to $22.5 billion. Wall Street got the vapors because earnings came in at $1.41 per share, well below their $2.04 consensus.

Reminds me of the time analysts completely missed Apple's (AAPL) transformation into a services company.

For the full year 2024, JNJ delivered 4.3% sales growth (5.4% operational) to $88.8 billion, with earnings per share landing at $5.79, or $9.98 adjusted after swallowing a $(0.67) hit from acquired IPR&D charges.

Not too shabby for a company in transition.

Looking into 2025, management is guiding for 2.5-3.5% operational sales growth ($90.9-91.7 billion) and adjusted operational EPS of $10.75-$10.95.

That's 8.7% growth at the midpoint, though they're careful to hedge around legal proceedings and acquisition costs.

And here's where it gets interesting.

During last week's JP Morgan Healthcare Conference, CEO Joaquin Duato was practically bouncing in his chair about their drug pipeline. Let's look at what's got him so excited.

Darzalex, their multiple myeloma superstar, raked in $11.67 billion in 2024, up 20%.

The new kid Carvykti exploded 93% higher to $963 million. Tecvayli landed $550 million in its rookie year.

Depression med Spravato jumped 56% to hit the magic $1 billion mark. Tremfya, their Stelara successor, grew 17% to $3.7 billion.

Speaking of Stelara – there's the elephant in the room.

JNJ's crown jewel is losing patent protection, already showing up in Europe with a >12% sequential decline in Q4 to $2.35 billion. Expect a 30% "haircut" this year.

But here's what Wall Street is missing: JNJ saw this coming years ago.

They just dropped $14.6 billion on Intracellular Therapies, mostly debt-funded (they can afford it with only $31.3 billion in long-term debt and $19.98 billion in cash).

This brings them Caplyta, an antipsychotic med with blockbuster potential that's already approved for schizophrenia and bipolar disorders.

The medical device business isn't sitting still either.

Q4 worldwide revenues jumped 6.7% year-on-year. While Surgery was flat at $2.5 billion and Orthopedics grew a modest 2.5% to $2.32 billion, Vision popped 9% to $1.3 billion.

But the real story? Cardiovascular surged 24% to $2.1 billion. Those Shockwave and Abiomed acquisitions are looking pretty smart right about now.

For the year, MedTech grew 4% to $31.56 billion. Operating margins slipped a bit – Innovative Medicines down from 42% to 39.4%, MedTech from 23.7% to 21.6%.

Late-stage pipeline products nearing approval should ease R&D expenses in 2025, just as JNJ gears up for its next growth phase.

The foundation looks rock solid - $19.98 billion in cash, $31.3 billion in long-term debt, 2025 adjusted EPS guidance of $10.75-$10.95, and that reliable $1.24 quarterly dividend.

But forget the current numbers - the real money's in what's coming next.

Here's what the market is missing: JNJ is promising 5-7% compound annual growth between 2025-2030, with ten drugs hitting $5+ billion in annual sales by decade's end.

Sound ambitious? Maybe. But they've got the pipeline to back it up – from immunology stars nipocalimab and icotrokinra to neuroscience contenders seltorexant and aticaprant, plus oncology plays like TAR-200 for bladder cancer.

I've seen this movie before with AbbVie (ABBV), which navigated the loss of $20+ billion Humira without missing a beat.

And JNJ looks even better positioned - their pharma division is targeting $58 billion in 2024 revenues, which would make them the biggest player in Big Pharma, ahead of Pfizer (PFE), AbbVie (ABBV), Roche (RHHBY), AstraZeneca (AZN), Sanofi (SNY) and Novartis (NVS).

The only real wildcard? That pesky talc litigation.

JNJ's latest move – spinning the lawsuits into Red River Talc LLC and filing for bankruptcy – could cap the damage at $8.5 billion. They claim 75% of claimants are on board, with a court ruling expected this month.

So, what's my take? I think JNJ's 2025 will be a "reset" year, especially the first half. But just like buying straw hats in winter, there might be an opportunity here for patient investors. Management says the back half will be stronger, setting up 2026 for what could be a very interesting guidance call.

While the market frets about Stelara's patent cliff, smart money is quietly building positions. That's why I'm maintaining my stand to buy the dip.

After all, sometimes the best trades are the ones that make you a bit uncomfortable at first. And if you're worried about patent cliffs, just ask any AbbVie shareholder how that worked out for them.

Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)