Mad Hedge Biotech & Healthcare Letter

May 20, 2021

Fiat Lux

FEATURED TRADE:

(REGENERATED REGENERON)

(REGN), (PFE), (JNJ), (AMGN), (BMY), (GILD), (MRK), (LLY), (SNY), (BAYRY), (NVS), (RHHBY)

Mad Hedge Biotech & Healthcare Letter

May 20, 2021

Fiat Lux

FEATURED TRADE:

(REGENERATED REGENERON)

(REGN), (PFE), (JNJ), (AMGN), (BMY), (GILD), (MRK), (LLY), (SNY), (BAYRY), (NVS), (RHHBY)

The biotechnology and healthcare sectors have become attractive investment targets for investors who recognize the value and essence of these industries along with the possible risks associated with them.

While not all companies in these areas are great investments, some offer remarkable growth opportunities.

One company worth considering is Regeneron (REGN), with its strong and stable investment thesis and steady organic growth.

Regeneron joins the ranks of Pfizer (PFE) and Johnson & Johnson (JNJ) as one of the handful of biopharmaceutical companies to release solid first quarter results this 2021 compared to other big names in the industry, including Amgen (AMGN), Bristol Myers Squibb (BMY), Gilead Sciences (GILD), Merck (MRK), and Eli Lilly (LLY).

The New York-based company reported a 38% boost in its revenue compared to the same period in 2020, reaching $2.5 billion for the first quarter of 2021 alone.

Virtually all of Regeneron’s products generated solid growth during this period, with the company’s COVID-19 antibody cocktail REGEN-COV delivering the highest sales at $262 million.

To underscore just how significant REGEN-COV is to Regeneron this quarter, its absence from the roster would take away 18% from the company’s overall revenue growth.

Riding the momentum of its COVID-19 program, Regeneron has developed Inmazeb, which is a treatment for Ebola virus infection.

Aside from its COVID-19 antibody cocktail, Regeneron also saw an impressive boost in the performance of its atopic dermatitis drug Dupixent.

Dupixent, which Regeneron sells in partnership with Sanofi (SNY), generated $1.26 billion in sales in the first quarter, showing off a notable 48% increase from its 2020 report.

Although Dupixent is a shared product with Sanofi, this dermatitis drug holds incredible promise for Regeneron.

To date, only 6% of eligible patients are being treated with Dupixent. This indicates a massive space that is yet to be explored by both companies.

Taking into consideration the pace at which Dupixent has been growing so far, this drug is projected to peak at roughly $12.5 billion in sales in the coming years.

Another high-selling drug for Regeneron is wet age-related macular degeneration (AMD) treatment Eylea.

Sales for this drug, which was developed in collaboration with Bayer (BAYRY), went up from $1.2 billion in the first quarter of 2020 to $1.3 billion this year.

The increase in sales for Eylea is a welcome surprise for both Regeneron and Bayer, especially since more and more competitors are attempting to topple the drug as the top product in the niche.

Cornering the AMD segment is an attractive venture for any biopharmaceutical company.

After all, Eylea generated $4.9 billion in sales in 2020 from the US market alone.

Thus far, two main competitors have come forward as the strongest.

One is Novartis (NVS), which released Beovu in 2019.

The second, and possibly the stronger competitor between the two, is Roche (RHHBY) with Faricimab.

To ensure its dominance in the AMD market, Regeneron has been expanding the use of Eylea.

The latest development is the drug’s enrollment in the Phase 3 program, which would allow extended periods in between treatments but still deliver the same level of efficacy and safety.

Aside from these, Regeneron is looking into additional revenue streams ahead.

One growth segment is its oncology program, particularly its cancer drug Libtayo, which may soon be marketed to cover a fourth type of cancer.

Regeneron aims to submit Libtayo for review as a treatment for advanced cervical cancer.

On top of this, the drug is also a strong contender in the development of several antibody treatments.

Thus far, the company has 12 oncology antibodies under clinical development.

Overall, Regeneron’s strong results for the first quarter of 2021 highlighted its continuous evolution into a company carrying multiple and diverse portfolios of products and pipeline programs that address an extensive range of serious diseases, from COVID-19 and rare diseases to cancer.

Mad Hedge Biotech & Healthcare Letter

May 18, 2021

Fiat Lux

FEATURED TRADE:

(AN UP-AND-COMER BIOPHARMA STOCK)

(ABBV), (ABT), (JNJ), (PFE)

Mad Hedge Biotech & Healthcare Letter

May 6, 2021

Fiat Lux

FEATURED TRADE:

(THE WHITE KNIGHT OF BIOPHARMA)

(PFE), (AMGN), (BMY), (LLY), (GILD), (MRK), (BNTX), (VTRS), (GSK)

After a week of dissatisfying earnings reports from huge biopharmaceutical firms like Amgen (AMGN), Bristol-Myers Squibb (BMY), Eli Lilly (LLY), Gilead Sciences (GILD), and Merck (MRK), one company has managed to buck the trend: Pfizer (PFE).

In its first quarter earnings report for 2021, Pfizer reported adjusted diluted earnings of 93 cents per share, surpassing the earlier experts’ estimate of 77 cents.

Even its reported revenue exceeded the earlier predictions of $13.4 billion, raking in $14.6 billion during the period instead.

Aside from those, Pfizer also massively boosted its projected revenue from the COVID-19 vaccine it developed with BioNTech (BNTX).

Pfizer’s COVID-19 vaccine is slated for approval to be used for 12- to 15-year-olds by next week.

On top of these, the company expects data from its third COVID-19 vaccine candidate. This recent trial is for a booster dose, which could have results by early July and possibly a full emergency approval later on the same month.

The company now estimates $26 billion in sales for the vaccine, which is notably up from its $15 billion projection in February 2021.

Pfizer is also confident in its capacity to manufacture at least 3 billion doses of the COVID-19 vaccine in 2022, with the company already negotiating agreements with countries for their 2022 supply and beyond.

While the huge boost in the company’s COVID-19 vaccine sales expectations definitely grabs headlines, Pfizer’s base business brought in notable results as well.

Apart from the vaccine, the company’s operational growth in the first quarter was mostly driven by the sales from its blood clot treatment Eliquis, which went up by 25% operationally.

Sales of its heart drug Vyndagel soared by 88%, while its cancer drug Xeljanz jumped 18%.

One of the most notable moves from Pfizer is spinning off its off-patent drug division, Upjohn, to form a new company with generic drug developer Mylan, called Viatris (VTRS).

This decision would rid Pfizer of several well-known products, such as Viagra, Lyrica, Lipitor, Celebrex, and Chantix, which were responsible for roughly 15% of its total revenues.

However, sales for these items fell by 30% in the first nine months of 2020 alone—a chronically falling performance since 2017.

By eliminating the products that no longer hold any exclusivity rights and signing them off to Viatris, Pfizer can focus on developing and marketing new and innovative treatments.

So far, this strategy has started to bear fruit.

At the moment, Pfizer has several attractive assets in its pipeline. One of them is non-small cell lung cancer (NSCLC) treatment Lorbrena, which could become one of the highest-selling products in the oncology market.

Lorbrena is estimated to grow to over $40 billion each year by the mid-2020s.

At this point, the drug is in its registration phase and was granted a priority-review status. That means approval is on the horizon in the not-so-distant future.

Other potential blockbuster oncology assets include prostate cancer drug Xtandi, NSCLC treatment Bavencio, and breast cancer medication Ibrance.

All these are in late-stage trials, which means they should be available to market soon.

In total, Pfizer currently has at least 33 drugs queued in either Phase 3 trials or registration. The list includes vaccine candidates, immunology treatments, and, of course, oncology assets.

While Pfizer lost Upjohn in 2020, it gained a new partner in GlaxoSmithKline (GSK). The two companies decided to merge their consumer healthcare programs.

This made them the biggest provider of non-prescription drugs across the globe.

By shedding its sluggishly growing assets, Pfizer managed to develop its culture into one that concentrates on developing and marketing new and innovative products.

Additionally, the company’s current portfolio holds several growing products with the potential for expansion.

Given all these changes, Pfizer raised its financial guidance for 2021 as well.

For this year, the company now estimates adjusted diluted earnings to be valued between $3.55 and $3.65 per share compared to the previous range of $3.10 to $3.20 per share.

In terms of its full-year revenue, the company raised it from its estimate between $59.4 billion and $61.4 billion to $70.50 billion and $72.5 billion.

In terms of its projected revenue compound annual growth rate, Pfizer reconfirmed that it could deliver at least 6% through 2025 and a double-digit growth on its bottom line.

Remarkably, this is still not taking into consideration its COVID-19 vaccine.

If you pull out the revenues from its COVID-19 vaccine, then the company’s projected EPS growth for 2021 is at 15%.

Adding the vaccine into the equation gives us an impressive 41% increase in its EPS.

If you consider the wild card that is Pfizer’s COVID-19 vaccine, which would include a price increase coupled with the possibility of booster shots administered annually, and combine it with its base business, then it’s easy to see how the company’s growth could be turbocharged in the next few years.

Mad Hedge Biotech & Healthcare Letter

May 4, 2021

Fiat Lux

FEATURED TRADE:

(A BAD NEWS BUY STOCK)

(AZN), (PFE), (BNTX), (MRNA), (JNJ)

Along with Pfizer (PFE), BioNTech (BNTX), and Moderna (MRNA), one of the biggest potential winners in the COVID-19 vaccine race is AstraZeneca (AZN).

While the company did manage to develop a vaccine nearly as fast as the others, its product is now suffering the same fate as Johnson & Johnson’s (JNJ) candidate and is getting bogged down by blood clotting issues.

As if that isn’t enough, AstraZeneca’s plan to use its diabetes drug Farxiga as another potential COVID-19 treatment also flopped.

Needless to say, it looks like not a lot of things are going well for AstraZeneca in the past months.

Looking at its fundamentals though, it’s worth noting that AstraZeneca stock might just be one of those rare prime candidates for being bad news buys.

After all, the company never really had plans to profit from its COVID-19 vaccine venture. In fact, AstraZeneca has long announced that it would sell its vaccine at cost. Hence, any bad news from the vaccine won’t really affect the company’s sales.

For years, AstraZeneca has been focused on creating a hyper-growth product lineup in several of the pharmaceutical industry’s most profitable submarkets.

In fact, the Phase 3 advanced pipeline candidates of the company are some of the most promising candidates in the industry, with these soon-to-be-launched drugs already generating 24% growth in revenue as early as 2017.

Not including cancer, there are at least 2.1 billion people globally who suffer from various chronic diseases. That accounts for over 25% of the entire human population, thereby representing a massive and lucrative addressable market--the very same market that AstraZeneca has been targeting.

In the years to come, AstraZeneca is projected to release at least six blockbuster drugs—each one of them estimated to rake in more than $1.3 billion in sales annually.

At the moment, one of the company’s major growth drivers is its oncology franchise, which has an early-stage pipeline anticipated to rake in roughly $1.3 billion each year by 2026.

In particular, AstraZeneca’s recently released cancer drugs Imfinzi and Tagrisso are well-positioned to dominate the segment thanks to their leading efficacy when it comes to hard-to-treat cancer types.

Meanwhile, other sub-sectors are expected to contribute $2.65 billion annually.

So far, AstraZeneca operates in more than 70 countries, ensuring its presence in practically all potential addressable markets.

In China alone, the company’s new product sales have risen by 68%, while the rest of the emerging markets recorded 56% growth.

Despite the negative publicity of its COVID-19 vaccine recently, AstraZeneca still managed to report positive data for its first quarter earnings.

Within this period, the company generated $7.2 billion in revenue, which is 15% more than its earnings during the same time last year. Its earnings per share rose by 100% to reach $1.19, while its core earnings were up 55%.

This is a welcome surprise, especially since analysts predicted $0.75 per share for the company.

The rise in AstraZeneca’s stock performance was driven mostly by its best-selling drugs, including Tagrisso with $1.15 billion in sales in the first quarter of 2021 alone and showing off a 17% jump year-over-year.

Even with the failed COVID-19 treatment, the diabetes drug Fargixa soared this quarter with $625 million, indicating a 54% increase from its previous performance during the same period.

More importantly, AstraZeneca has been consistently paying investors a dividend since it started doing it 20 years ago—a trend that’s expected to continue since the company is poised to become one of the fastest growing businesses in the world with 15% growth annually.

Given its pipeline programs and current portfolio of products, AstraZeneca is on track to continue its hypergrowth through 2023. At this pace, we can expect an estimated 105% in total returns and compound annual growth rate returns at 30.2%.

Currently, AstraZeneca stock is experiencing some turbulence due to the bad news linked to its COVID-19 vaccine. Now would be the best time to buy the dips on the bad news.

Global Market Comments

May 3, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE STAIR STEP MARKET IS HERE),

(SPY), (TLT), (MRK), (EL), (UNP), (PFE), (GM), (PYPL), (REGN), (ROKU)

The last six months have been the most successful in my 52 years of trading. The only thing that comes close were the last six months of 1989 when the Tokyo market went straight up and hit a 30-year peak.

Everything I tried worked. The trades I only thought about worked. And the 50 trade alerts I abandoned on the floor because the market moved too fast worked as well. That’s how I missed Facebook (FB) and Amazon (AMZN).

It is believed that if you set a team of monkeys loose, randomly hitting keys on typewriters, they would eventually produce Romeo and Juliet. In this market, they have been producing the entire works of Shakespeare on a daily basis.

It has been that good.

President Biden has been looking pretty good too, having presided over the best starting three-month stock market results since 1933. That is no accident. The massive stimulus and the remaking of the country he has proposed have Franklin Roosevelt’s New Deal-inspired handwriting all over them.

Yet, traders have been puzzled, perplexed, and befuddled by companies that announce the best earnings in history only to see their shares sell-off dramatically. However, the market has shown its hand.

We’ve now seen three quarters of tremendously improving earnings and stock dives. It’s a 12-week cycle that keeps repeating. Shares rally hard for six weeks into earnings, peak, and then go nowhere for six weeks. Wash, rinse, repeat, then go to new all-time highs.

But stocks don’t fall enough to justify getting out and back in again, especially on an after-tax basis. Therefore, it’s just best to lie back and think of England while your stocks do nothing.

If my analysis is correct, then it's best to imagine the rolling green hills of Kent and Wiltshire, the friendly neighborhood pub, and Westminster Cathedral until June. If you want to get aggressive, you might even sell short an out-of-the-money call option or two to protect your portfolio.

The Fed leaves rates unchanged, indicating that the economy is improving, but that interest rates are going nowhere. No surprise here. Jay Powell is still going for maximum dove. Strong Biden policy support and the rollout of the vaccine are major positives. $120 billion in bond buying continues. The Fed will keep interest rates at zero until the US economy reaches maximum employment by adding 8.4 million jobs. That could be a long wait as I suspect those jobs have already been destroyed by technology. Stocks popped on the news. The Bull lives!

Q1 GDP eExploded by 6.4%, and upward revisions are to come. That explains the 25% gain in the stock market during the first three months of the Biden administration, the best in 75 years. Coming quarters will show even stronger growth as the economy shakes off the pandemic and massive government spending kicks in. We will recover 2019 GDP peaks in the next quarter. Virtually, all economic data points will set records for the rest of 2021. Buy everything on dips.

Weekly Jobless Claims dive again to 553,000, a new post-pandemic low. One of a never-ending series of perfect data. It augurs well for next week’s April Nonfarm Payroll Report.

New Home Sales up a ballistic 20.7% YOY in March on the basis of a signed contract. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

Pending Home Sales fell 1.9%, far below expectations, but are still up 23% YOY. Higher prices and record low supply are the problems. The Midwest leads.

Amazon sales soar by 44% in Q1, producing some of the best earnings in American corporate history. Jeff is expecting sales to reach a staggering $110-$116 billion in Q2. That’s why he hired 500,000 last year, the most of any company since WWII. Prime subscribers have grown to 200 million, including me. Ad revenues jumped an eye-popping 77%. The shares of the huge pandemic winner leaped $140 on the news. It’s all another step toward my $5,000 target.

Tesla revenues explode for 74%, and earnings soar to an eye-popping $438 million. Sales are to double or more in 2021 and are up 104% YOY. Q1 is usually the slowest quarter of the year for the auto industry. Global demand is increasing far beyond production levels. It is ducking around chip shortages by designing in a new generation that is currently available. Production of high-end X and S Models has ceased to allow more focus on the profitable Y and 3 Models. Those will resume in Q3. The shares were unchanged on the news. Keep buying (TSLA) on dips. It’s headed for $10,000.

Copper hits new 10-year high, lighting a fire under Freeport McMoRan (FCX) which we are long. We still are in the early innings of a major commodity supercycle. The green revolution goes nowhere without increasing copper supplies tenfold. A copper shock is imminent.

US Capital Spending leaps ahead, up 0.9% in March and up 10.4% YOY. The stimulus spending is working. All is well in manufacturing land, which is 12% of the US economy.

Case-Shiller explodes to the upside, the National Home Prices Index soaring 12% in February. That’s the best report in 15 years. Phoenix (+17.4), San Diego (+17.0%), and Seattle (15.4%) continue to be the big winners. This was in the face of a 50-basis point jump in home mortgage interest rates during the month. The rush to buy homes is pulling forward future demand. The perfect storm continues.

The Fed could start tapering its $120 billion a month in bond purchases as early as October, believes the Blackrock’s (BLK) Rick Rieder. When it does, expect the sushi to hit the bond market. Keep piling on those bond shorts, as I have been doing monthly, and am currently running a triple short position. Keep selling short the (TLT) on every opportunity.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 13.54% gain during April on the heels of a spectacular 20.60% profit in March.

I used the post-earnings dip in Microsoft (MSFT) to add a new position there. I also picked up some Delta Airlines (DAL) taking advantage of a pullback there.

That leaves me 100% invested, as I have been for the last six months.

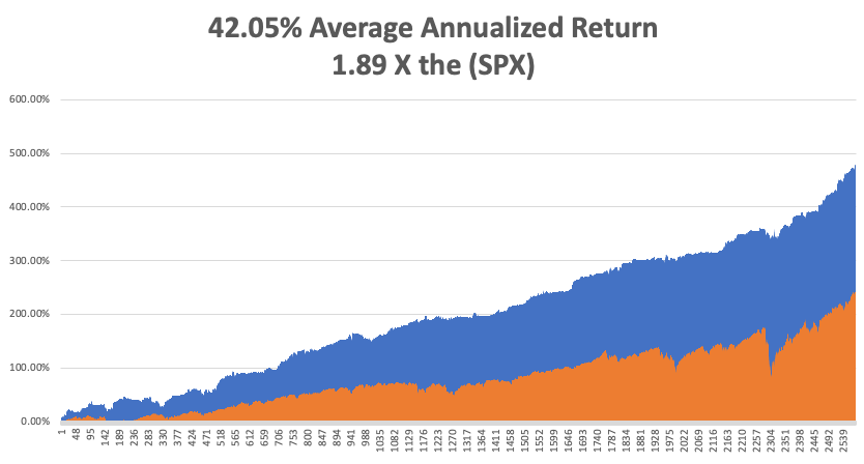

My 2021 year-to-date performance soared to 57.63%. The Dow Average is up 11.8% so far in 2021.

That brings my 11-year total return to 480.18%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.05%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 133.91%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9 million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, May 3, at 10:00 AM, the US ISM Manufacturing Index is published. Merck (MRK) and Estee Lauder (EL) report.

On Tuesday, May 4, at 8:00 AM, total US Vehicle Sales for April are out. Union Pacific (UNP) and Pfizer (PFE) report.

On Wednesday, May 5 at 2:00 PM, the ADP Private Employment Report is released. General Motors (GM) and PayPal (PYPL) report.

On Thursday, May 6 at 8:30 AM, the Weekly Jobless Claims are printed. Regeneron (REGN) and Roku (ROKU) report.

On Friday, May 7 at 8:30 AM, we learn the all-important April Nonfarm Payroll Report. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I received calls from six readers last week saying I remind them of Earnest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens, I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete works.

I visited his homes in Key West and Ketchum Idaho. His Cuban residence is high on my list, now that Castro is gone.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Earnest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was still being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are glued to the tables.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Life is a Bed of Roses Right Now

Global Market Comments

April 30, 2021

Fiat Lux

Featured Trade:

(APRIL 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(PFE), (MRNA), (USO), (DAL), (TSLA), (CRSP), (ROM), (QQQ), (T), (NTLA),

(EDIT), (FARO), (PYPL), (COPX), (FCX), (IWM), (GOOG), (MSFT), (AMZN)