I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I go downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up-to-date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 12X pro.

Here is the bottom line which I have been warning you about for months. In 2022, you are going to have to work twice as hard to earn half as much money with double the volatility.

It’s not that I’ve turned bearish. The cause of the next bear market, a recession, is at best years off. However, we are entering the third year of the greatest bull market of all time. Expectations have to be toned down and brought back to earth. Markets will no longer be so strong that they forgive all mistakes, even mine.

2022 will be a trading year. Play it right, and you will make a fortune. Get lazy and complacent and you’ll be lucky to get out with your skin still attached.

If you think I spend too much time absorbing conspiracy theories or fake news from the Internet, let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2022

1) How soon will the Omicron wave peak?

2) Will the end of the Fed’s quantitative easing knock the wind out of the bond market?

3) Will the Russians invade the Ukraine or just bluster as usual?

4) How much of a market diversion will the US midterm elections present?

5) Will technology stocks continue to dominate, or will domestic recovery, and value stocks take over for good?

6) Can the commodities boom get a second wind?

7) How long will the bull market for the US dollar continue?

8) Will the real estate boom continue, or are we headed for a crash?

9) Has international trade been permanently impaired or will it recover?

10) Is oil seeing a dead cat bounce or is this a sustainable recovery?

The Thumbnail Portfolio

Equities – buy dips Bonds – sell rallies Foreign Currencies – stand aside Commodities – buy dips Precious Metals – stand aside Energy – stand aside Real Estate – buy dips Bitcoin – Buy dips

1) The Economy

What happens after a surprise variant takes Covid cases to new all-time highs, the Fed tightens, and inflation soars?

Covid cases go to zero, the Fed flip flops to an ease and inflation moderates to its historical norm of 3% annually.

It all adds up to a 5% US GDP growth in 2022, less than last year’s ballistic 7% rate, but still one of the hottest growth rates in history.

If Joe Biden’s build-back batter plan passes, even in diminished form, that could add another 1%.

Once the supply chain chaos resolves inflation will cool. But after everyone takes delivery of their over orders conditions could cool.

This sets up a Goldilocks economy that could go on for years: high growth, low inflation, and full employment. Help wanted signs will slowly start to disappear. A 3% handle on Headline Unemployment is within easy reach.

The weak of heart may want to just index and take a one-year cruise around the world instead in 2022 (here's the link for Cunard).

So here is the perfect 2022 for stocks. A 10% dive in the first half, followed by a rip-roaring 20% rally in the second half. This will be the year when a big rainy-day fund, i.e., a mountain of cash to spend at market bottoms, will be worth its weight in gold.

That will enable us to load up with LEAPS at the bottom and go 100% invested every month in H2.

That should net us a 50% profit or better in 2022, or about half of what we made last year.

Why am I so cautious?

Because for the first time in seven years we are going to have to trade with a headwind of rising interest rates. However, I don’t think rates will rise enough to kill off the bull market, just give traders a serious scare.

The barbell strategy will keep working. When rates rise, financials, the cheapest sector in the market, will prosper. When they fall, Big Tech will take over, but not as much as last year.

The main support for the market right now is very simple. The investors who fell victim to capitulation selling that took place at the end of November never got back in. Shrinking volume figures prove that. Their efforts to get back in during the new year could take the S&P 500 as high as $5,000 in January.

After that the trading becomes treacherous. Patience is a virtue, and you should only continue new longs when the Volatility Index (VIX) tops $30. If that means doing nothing for months so be it.

We had four 10% corrections in 2021. 2022 will be the year of the 10% correction.

Energy, Big Tech, and financials will be the top-performing sectors of 2022. Big Tech saw a 20% decline in multiples in 2022 and will deliver another 30% rise in earnings in 2022, so they should remain at the core of any portfolio.

It will be a stock pickers market. But so was 2021, with 51% of S&P 500 performance coming from just two stocks, Tesla (TSLA) and Alphabet (GOOGL).

However, they are already so over-owned that they are prone to dead periods as long as eight months, as we saw last year. That makes a multipronged strategy essential.

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a 2022 business. This time, bonds face the gale force headwinds of three promised interest rates hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

For the first time in ages, I did no foreign exchange trades last year. That is a good thing because I was wrong about the direction of the dollar for the entire year.

Sometimes, passing on bad trades is more important than finding good ones.

I focused on exploding US debt and trade deficits undermining the greenback and igniting inflation. The market focused on delta and omicron variants heralding new recessions. The market won.

The market won’t stay wrong forever. Just as bond crash is temporarily in a holding pattern, so is a dollar collapse. When it does occur, it will happen in a hurry.

5) Commodities (FCX), (VALE), (DBA)

The global synchronized economic recovery now in play can mean only one thing, and that is sustainably higher commodity prices.

The twin Covid variants put commodities on hold in 2021 because of recession fears. So did the Chinese real estate slowdown, the world’s largest consumer of hard commodities.

The heady days of the 2011 commodity bubble top are now in play. Investors are already front running that move, loading the boat with Freeport McMoRan (FCX), US Steel (X), and BHP Group (BHP).

Now that this sector is convinced of an eventual weak US dollar and higher inflation, it is once more the apple of traders’ eyes.

China will still demand prodigious amounts of imported commodities once again, but not as much as in the past. Much of the country has seen its infrastructure build out, and it is turning from a heavy industrial to a service-based economy, like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase 11-fold in a decade to accommodate this increase, no easy task, or prices will have to ride.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate commodities on dips.

Snow Angel on the Continental Divide

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (USO), (XLE), (AMLP)

Energy may be the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero.

However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are drinking their own Kool-Aid. Instead of reinvesting profits back into their new exploration and development, as they have for the last century, they are paying out more in dividends.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and shares prices for the energy industry.

Energy stocks are also massively under-owned, making them prone to rip-you-face-off short squeezes. Energy now counts for only 3% of the S&P 500. Twenty years ago it boasted a 15% weighting.

The gradual shut down of the industry makes the supply/demand situation more volatile. Therefore, we could top $100 a barrel for oil in 2022, dragging the stocks up kicking and screaming all the way.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to them, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2021 was a terrible year for precious metals. With inflation soaring, stocks volatile, and interest rates going nowhere, gold had every reason to rise. Instead, it fell for almost all of the entire year.

Bitcoin stole gold’s thunder, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand was just not enough to keep gold afloat.

This will not be a permanent thing. Chart formations are starting to look encouraging, and they certainly win the price for a big laggard rotation. So, buy gold on dips if you have a stick of courage on you.

Would You Believe This is a Blue State?

8) Real Estate (ITB), (LEN)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

There is no doubt a long-term bull market in real estate will continue for another decade, although from here prices will appreciate at a 5%-10% slower rate.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xer’s who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xers since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis.

If they have prospered, banks won’t lend to them. Brokers used to say that their market was all about “location, location, location.” Now it is “financing, financing, financing.” Imminent deregulation is about to deep-six that problem.

There is a happy ending to this story.

Millennials now aged 26-44 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to Zoom, many are never returning to the cities. So has the migration from the coast to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market in 2021, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should rocket during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a coming labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are taken into account. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 13 years. The 50% of small home builders that went under during the crash aren’t building new homes today.

We are still operating at only a half of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with.

You will boast to your grandchildren how little you paid for your house, as my grandparents once did to me ($3,000 for a four-bedroom brownstone in Brooklyn in 1922), or I do to my kids ($180,000 for a two-bedroom Upper East Side Manhattan high rise with a great view of the Empire State Building in 1983).

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now. It’s also a great inflation play.

If you borrow at a 3.0% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free.

How hard is that to figure out? That math degree from UCLA is certainly earning its keep.

Crossing the Bridge to Home Sweet Home

9) Bitcoin

It’s not often that new asset classes are made out of whole cloth. That is what happened with Bitcoin, which, in 2021, became a core holding of many big institutional investors.

But get used to the volatility. After doubling in three months, Bitcoin gave up all its gains by year-end. You have to either trade Bitcoin like a demon or keep your positions so small you can sleep at night.

By the way, right now is a good place to establish a new position in Bitcoin.

10) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff has made the ten-mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 13 Pro, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-05 13:00:512022-01-05 18:26:592022 Annual Asset Class Review

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

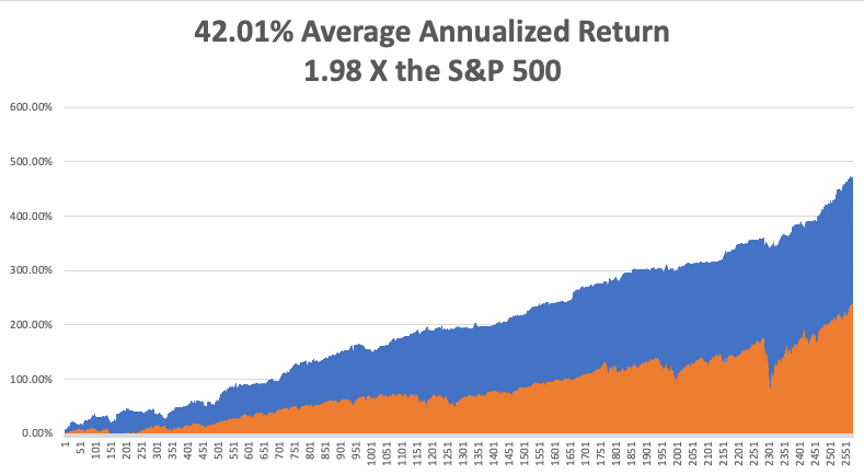

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/g-bebe-e1647874970894.png295450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:02:432021-04-26 10:45:23The Market Outlook for the Week Ahead, or The Correction is Over

Lately, I have been getting a lot of calls from concerned readers worried that we might be going into another 2008-2011 style real estate crash, when home prices cratered by 50%-70%, once the pandemic ends.

It’s not going to happen and there are a dozen reasons why. Worst case, I expect a short, shallow pause in the market, followed by a ballistic move to new all-time highs.

If you had any doubt, look no further than the superheated bond market which took interest rates to new all-time lows, sparking a refi boom in the process.

You see, there is a method to my madness.

Apple (AAPL) is planning on building a second new research and development campus that will need 20,000 new high-tech workers. Google (GOOGL) plans to spend $13 billion on real estate acquisitions, and Amazon (AMZN) just flushed out of New York, will move those 25,000 jobs to more hospitable climates.

It is all fresh fuel for a continuation in the bull market for US residential real estate, not just for this year, but for another decade, or more. More high paying jobs means more big spending home buyers.

Although prices seem high now, I am convinced that we are only at the beginning of a long-term secular bull market in housing. If you don’t believe me, check out the sky-high prices in Shanghai, Vancouver, and Sydney Australia.

Anything you purchase now is going to make you look like a genius ten years down the road.

The best is yet to come.

The big driver will be demographics, of course.

From 2022 onward, 65 million Gen Xers will be joined by 85 million late-blooming Millennials in a bidding war for the same houses. That will create a market of 150 million buyers, unprecedented in the history of the American real estate market.

In the meantime, 80 million baby boomers, net sellers, and downsizers of homes for the past decade will slowly die off and disappear from the scene as a negative influence. Only one-third are still working.

The first boomer, Kathleen Casey-Kirschling, born seconds after midnight on January 1, 1946, just turned 75 years old. A former schoolteacher, she took early retirement at 62.

The real fat on the fire here is that 10 million homes went missing in action this decade, thanks to the financial crisis. They were never built.

This is the result of the bankruptcy of several homebuilding companies and the new-found ultra-conservatism of the survivors, like DR Horton (DHI), Lennar Homes (LEN), and Pulte Group (PHM).

Did I mention that all of this makes this sector a screaming “BUY”?

Talk to any real estate agent and they will complain about the shortage of inventory (except in Chicago, the slowest growing market in the country).

Prices are so high already that flippers have been squeezed out of the market for good. Bottom feeders, like hedge funds buying at the bankruptcy auctions, are a distant memory. Some, like BlackRock (BLK), now own more than 40,000 homes and are the biggest landlords in the county.

And let’s face it, ultra-low interest rates aren’t going to be here forever. Borrow at 3.0% today against a long-term 3.0% inflation rate, and you are essentially getting your house for free.

The rising rents that are turning Millennials from renters to buyers may be the first sign of real inflation beyond the increasingly dear healthcare and higher education that we’re are already seeing.

And Millennials are having kids that demand a bigger living space! Who knew?

https://www.madhedgefundtrader.com/wp-content/uploads/2017/01/John-Fixer-Upper-e1484005396454.jpg367400The Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngThe Mad Hedge Fund Trader2021-01-26 09:02:142021-01-26 09:50:54Why the Real Estate Boom Has a Decade to Run

Below please find subscribers’ Q&A for the September 30 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Which is a better buy, NVIDIA (NVDA) or Advanced Micro Devices (AMD)?

A: NVIDIA is clearly the larger, stronger company in the semiconductor area, but AMD has more growth ahead of it. You’re not going to get a ten-bagger from NVIDIA from here, but you might get one from Advanced Micro Devices, especially if a global chip shortage develops once we’re out the other side of the pandemic. So, I vote for (AMD), and did a lot of research on that company last week. You can find the report at www.madhedgefundtrader.com but you have to be logged in to see it.

Q: Do you have any thoughts on the JP Morgan Chase Bank (JPM) spoofing cases, where they had to pay about a billion in fines? Is this a terrible time to invest in banks?

A: No, this is a great time to invest in banks because this is the friendly administration to banks now; the next one will be less than friendly. On the other hand, an awful lot of bad news is already in the price; buying these companies at book value or discount of book like JP Morgan, it's a once in a lifetime opportunity. All the bad behavior they’re being fined on now happened many years ago. So yes, I still like banks, but you really have to be careful to buy them on the dip, just in case they stay in a range. If you stay in a range, you’re buying them call spread, you always make money. The bigger drag on share prices will be the Fed ban on bank share buybacks but that may end after Q4.

Q: Is it time to buy Disney (DIS) after they laid off 28,000?

A: This is a company that practically every fund manager in the company wants to have in their portfolio. However, it could be at least a year before they get back to normal capacity in the theme parks, meaning customers packing in shoulder-to-shoulder. So, it could be another wait-for-a-turnaround, buy-on-the dip situation for sure. This company is so well managed that you’re always going to have to pay up to get into the Mouse House. By the way, my dad did business with Disney during the 1950s so we got Disneyland opening day tickets and I got to shake Walt Disney’s hand.

Q: How desperate is General Motors (GM) in buying the fake Tesla (TSLA) company, Nikola (NKLA), who've been exposed as giant frauds? Is GM hopeless?

A: Yes, the future is happening too fast for a giant bureaucracy like General Motors to get ahead of the curve. The fact that they’re trying to buy in outside technologies shows how weak their position is, and of course, it’s a great way to get stuck with a loser, as Tesla selling out to anyone. The Detroit companies are all stuck with these multibillion-dollar engine factories so they can’t afford to go electric even if they wanted to. So, I expect all the major Detroit car companies to go under in the next 5 years or so. Electric cars are already beating conventional internal combustion engines on a lifetime cost basis and will soon be beating them, within 3 years, on an up-front cost basis as well.

Q: Will Netflix (NFLX) pass $600 before the year's end?

A: I’m expecting a monster after-election rally to new all-time highs in the market and Netflix will be one of the leaders, so easy to tack on another hundred bucks to Netflix. That’s one of my targets for a call spread if we can get in at a lower price. And if you really want to be conservative, buy 2-year LEAPS, two-year call options spreads on Netflix, and you’ll get an easy 100% return on those.

Q: Who will win, Trump or Biden?

A: Neither. You will win. I am not a member of any political party as I would never join any club that would stoop to have me as a member. Groucho Marx told me that just before he died in the early 70s. Don’t ask me, ask the polls. Suffice it to say that the London betting polls are 60%-40% in favor of Biden, having just added another 5% for Biden after the debate. My expectation is that Biden picks up another point in the opinion polls in all the battleground states this weekend. So, Biden will be up anywhere from 6-10% in the 6 states that really count.

Q: What will the market impact be?

A: It makes no difference who wins. The mere fact that the election is out of the way is worth a 10% move up in the stock market.

Q: Should we keep the January 2022 (TLT) 140/143 bear put spread?

A: Absolutely, yes. That’ll be a chip shot and we in fact should go in the money on those number sometime next year. A huge cyclical recovery will create an enormous demand for funds and crowding out by the government will crush the bond market.

Q: Do you think it would be better to wait a week or two to lock in refis on home loans?

A: I think we are at the low in interest rates in the refi market. Even if the Fed lowers interest rates, banks aren’t going to lower their lending rates anymore because there's no money in it for them. It’s also taking anywhere from 2-4 months to close on a loan, as the backlogs are so enormous. If you can even get a loan officer to return a phone call, you’re lucky. So, I wouldn't be too fancy here trying to pick absolute bottoms; I would just refi now and whatever you get is going to be close to a century low.

Q: Why so few trade alerts?

A: Well, very simple. We only do trade alerts when we see really good sweet spots in the market. There aren’t sweet spots in the market every day; you’re lucky if you get 1 or 2 in a month. Then we tend to pour in and out of the market very quickly with a lot of alerts. There is no law that says you have to have a position every day of the year. That buys the broker’s yacht, not yours. You should only have positions when the risk reward is overwhelmingly in your favor. That is not now when our market timing index is hugging the 50 level. At 50, you actually have the worst possible entry point for new trades, long or short, so I’d rather wait for it to get away from that level before we get aggressive again. We have gone 100% invested multiple times in the last two months and made a ton of money. So, you just have to wait for your turn to get a sweet spot, and then you’ll make a very quick 10% or 15% in the market. Patience is rewarded in this business.

Q: Would you wait for the election because of the high implied volatility?

A: No, I would not wait. The game is to get in at the lowest price before the election. When the implied volatilities drop after the election, the profits you can make on these deep out of the money LEAPs drop by about half. Thank the volatility while it’s here because it’s creating great trading opportunities now, not in two months after the volatility Index (VIX) has collapsed.

Q: What about Zoom (ZM)?

A: As much as Zoom has had a 10-fold return since we recommended it a year ago, it looks like it wants to go higher. The Robinhood traders just love this stock; it’s a stay at home stock, stay at home is lasting a lot longer than anyone thought. Zoom is just coining it on that.

Q: Is the best outcome a Biden presidency and a Republican Senate?

A: No, that is the worst outcome. When you have a global pandemic going on, you don’t want gridlock in Washington. You want a very active Washington, controlled by a single party that can get things done very quickly. That is not now, which is possibly a major reason that we have the highest Covid-19 death rate in the world. It’s because Washington is doing absolutely nothing to stop the virus; the president won’t even wear a mask, so yes, you need one party to control everything so they can push stuff through. If it works, great, and if not then you kick them out of office next time and let the other guys have a try.

Q: Will property markets be up 20% by the end of the year?

A: If you live in a suburb of New York or San Francisco, then yes it will be up that much. For the whole rest of the country, the average is more like 5% gains year on year. In the burbs of these big money-making cities, prices are going absolutely nuts. My neighbor put his house up and it sold in a week for a $1 million over asking. So, the answer to that is yes, hell yes.

Q: Can you explain why the IPO market is suddenly booming now?

A: A lot of these companies like Palantir (PLTR) have been in development for 20 years, and prices are high. On valuation terms, we are at dot com bubble peaks now. That is the very best time to take your company public and get a huge premium for your stock. When the world is baying for paper assets, you print more of them.

Q: What is the best way to play real estate?

A: Buying the single home building companies like Pulte Homes (PHM), Lennar Homes (LEN), and KB Homes (KBH).

Q: What is your Tesla overview in China?

A: Tesla’s already announced that they’re doubling production of the Shanghai factory, from 250,000 units a year to 500,000. They built the last one in 18 months. It would take (GM) like 5 years to build something like that.

Q: Why has gold (GLD) lost its risk-off status?

A: It’s now a quantitative easing asset—like tech stocks, like bitcoin, and the stay at home stocks. It is being driven much more by QE-driven speculators flush with free cash than anyone looking for a flight to safety bid. When this group sells off, gold drops as well. The only risk-off asset right now is cash. That is the only “no risk” trade.

Q: What does reversal in lumber prices tell you?

A: Lumber was another one of those QE assets—it tripled. But you have this monster increase in new home building, huge demand for new homes in the suburbs, huge import duties leveled by the Trump administration on lumber coming from Canada. Also, a lot of people are getting COVID-19 in the lumber mills. So, they’re having huge problems on the production side in lumber, as a result of the pandemic.

Q: Are there any alternative ways to buy the Australian dollar besides (FXA)?

A: You go into the futures market and buy the Australian dollar futures. That is an entirely new regulatory regime so can be a huge headache. It requires you to register with the Commodities Futures Trading Commission, which is the worst of all the major regulators, but that is an alternative. If you’re an individual and not regulated instead of being a professional money manager, then it’s much easier.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-07-08 09:04:532020-07-08 08:57:08July 8, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.