At this point, it is possible that the president may lose the November election.

He is 14 points behind Democratic candidate Joe Biden in the polls. The odds at the London betting polls have him losing by a similar amount. My old employer The Economist magazine in London gives him a 10% chance of winning using a mix of economic and polling data.

And this assumes the election is held today. The fact is that the president is digging himself into a deeper hole every day, taking the wrong side of every issue confronting the country today. He seems to be refighting the Civil War….and taking the Confederate side when even the State of Mississippi is taking its symbol off its flag.

So, what will the post-Trump world look like? Will taxes go through the roof? Will the market crash? Is it time to go 100% cash, change our names, and move to a country with no US extradition treaty?

I don’t think so. In fact, with stocks soaring to meteoric new highs every day, the market expects that a Biden administration will be great news for stocks, perhaps the best ever.

Taxes will certainly go up. Favorable tax treatment of the energy, real estate, and private equity funds will get axed. Carried interest will finally become history. Marginal tax rate on net income over $1 billion could get hiked to the Roosevelt levels of 80-90%.

Biden has already announced an increase in the corporate tax rate from 21% to 28%. That will cut earnings for the S&P 500 by $9 a share. But the stock market is not the economy, with S&P earnings only accounting for 10% of US GDP.

And the $9 companies lose in taxes they will make back and more from new government spending, which isn’t slowing down any time soon. Some 14,000 American bridges need to be rebuilt. The Interstate Highway System is a shambles. High-speed broadband needs to go rural. The electrification of the US needs to accelerate to accommodate the millions of electric cars headed our way.

I believe that eventually, 51 million Americans will lose their jobs as a result of the pandemic. Perhaps a third of those are never coming back because the future has been so accelerated. That will leave the broader U-6 Unemployment rate stuck in double digits for years, maybe for decades.

So, we’re going to need some kind of Roosevelt style programs like the Works Progress Administration (WPA) and the Civilian Conservation Corps (CCC) who built much of the monolithic infrastructure that we all enjoy today.

At least 300,000 educated workers could immediately be put to work in contact tracing. Millions more could be employed in national infrastructure programs. One thing is certain. A new administration won’t stop massive government spending, it will simply redirect it.

And let's face it. A Biden win would bring a big expansion of Obamacare. With the best healthcare technology in the world, private industry has done the world’s worst job controlling the pandemic.

Countries with well-run national healthcare systems like Australia, New Zealand, Japan, and Singapore have almost wiped out the disease. This is why I am avoiding the healthcare sector for the foreseeable future.

Who are the big winners of all this? Big tech (FB), (AAPL), (MSFT), (AMZN), medium tech (ADBE), fintech (SQ), (PYPL), the cloud (CRM), and biotech (SGEN), (REGN), and (ILMN).

Cybersecurity will always be in demand (FEYE), (PANW). The global chip shortage will continue to worsen (AMD), (MU), (NVDA).

And Tesla (TSLA)? What can I say? It is already up nearly 100-fold from my initial $16.50 recommendation in 2010, and I’ve bought three Tesla’s (two S’s and an X).

Followers of the Mad Hedge Trade Alert service know that I am already long these names up the wazoo, and is why I am up 26% in 2020. It’s simply a matter of all pre-pandemic trends hyper-accelerating, which we were already tapped into.

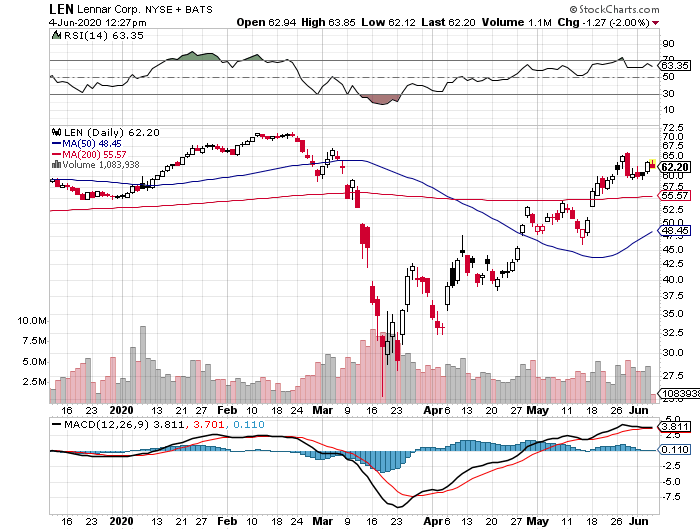

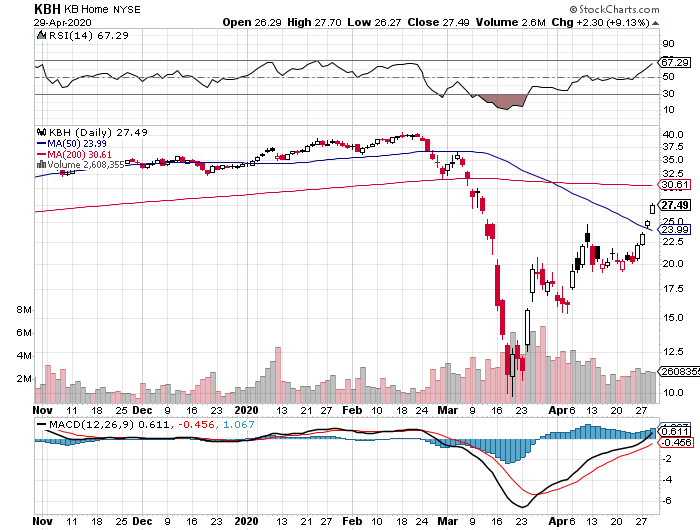

If you have to add a purely domestic sector, a gigantic Millennial tailwind will keep homebuilders bubbling for years like (LEN), (PHM), and (KBH).

And while you won’t find me as a player here, retail will recover. The sector has not prospered during the current administration, thanks to a trade war with China and the pandemic.

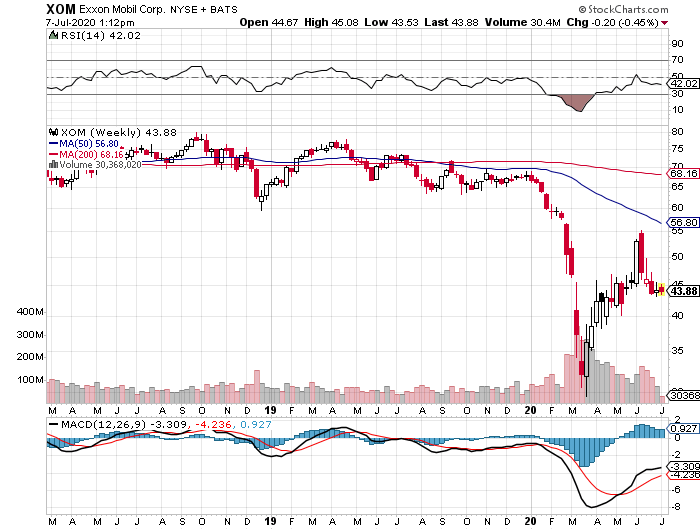

And the losers? There is a classification of “Trump” stocks you don’t want to be anywhere near. Energy will do terribly (XOM), (CVX), (XOM), with Texas tea possibly revisiting negative numbers. If you take away the tax breaks, energy hasn’t really made money in decades.

Defense stocks (RTN), (NOC), (LMT) will take a big hit from budget cutbacks and fewer wars. Coal (KOL) will finally get shut down for good, probably sold to China in bankruptcy proceedings. Industrials will continue to lag (X), (GE), with no more free handouts from the government and no technology advantage.

So if Biden wins, you don’t need to slit your wrists, hang yourself from the showerhead, or cease investing completely. Just take your stock market winnings and go out and get drunk instead.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-07-08 09:02:282020-07-08 08:56:44Trading the Blue Wave Stock Market

Below please find subscribers’ Q&A for the June 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Domino's Pizza (DPZ) is at all-time highs? Would you buy this name right here, right now?

A: No, I would not even buy their pizza. You would be crazy to buy them right now up here this high. I prefer Round Table, the pizza not the stock. All of these “reopening” stocks are way overextended.

Q: Will the riots delay the recovery?

A: Yes, they will, it could take as much as another 1% off the current GDP growth rate. It’s hitting the already worst-hit sector—retailers. Many retailers will not come back from these, especially the small ones. These businesses were just returning from being closed for two months when they got burned down. But we won’t see it in the macro data for many months because its happening largely at the micro level. If you didn’t like Macy’s (M) before when it was headed for Chapter 11, you definitely won’t like it now that it is burning down.

Q: If airlines like United Airlines (UAL) can’t use the middle seat, do you see ticket prices going up 10%, 25%, or 50%?

A: Yes. In theory, to just cover the middle seat, they have to increase prices 33%. And there will be a whole lot of new costs that the airlines have to endure as part of this pandemic, such as extra cleaning, disinfecting, and temperature taking. So, they’re really going to need to increase prices by 50% or more just to break even. My guess is that the airline industry will shrink in half in the fall when all the government bailout money runs out. So, I've been telling people to take profits on the airlines, especially if you have a double or triple in them, or if you have the LEAPS.

Q: Is Facebook (FB) immune from any big selloff?

A: No, nobody is immune—look how much Facebook sold off in March, some 35%. Mark Zuckerberg seems to be making a deal with the devil, accommodating the president with unrestricted incendiary Facebook posts. And the consequences of a Democratic win for Facebook could be hugely negative, so I am not participating in that one. Mark doesn’t have a lot of friends in congress right now so regulation looms.

Q: What do you think about buying Las Vegas Sands (LVS) or Wynn Resorts (WYNN) on the expectation of reopening?

A: I’m a Nevada resident and get frequently updated on the casino news. They’re only going to be allowed half of peak casino visitors that they had in January, so they will generate huge losses. Almost all companies are being allowed to reopen back to half the level that guarantees bankruptcy in 3-6 months. But we won’t see that in the numbers for many months either. I’m negative on any industry that depends on packing people in, like airlines, cruise lines, and movie theaters.

Q: What are the chances of a mass student debt cancellation?

A: That is a possibility if the Democrats win in November, and it has already been proposed. It is about a $1.5 trillion ticket. If you’re bailing out large companies, small companies, airlines, and the oil industry, why not students? It would have the benefit of adding 10 million more consumers to the economy, who are not current participants because they have massive student debts that are appreciating at 10% a year and have terrible credit ratings. So that would be another great economic stimulus measure. By the way, I paid off my student loans 40 years ago in a lump sum payment with my first paycheck from Morgan Stanley (MS). How much did four years of college cost during the 1960s? $3,000. Such a deal.

Q: What’s the next resistance level on the S&P 500 (SPX)?

A: The target we’ve been looking for is $3,125. I’m looking for roughly $40 points above that level—it should be about $3,165. We’re in uncharted territory here because nobody’s ever seen a market rise 40% in two months, so any technical recommendation has to be bearish except for a very short term, like intra-day or daily views.

Q: Any correlation between the 1918 epidemic and now?

A: Here is your History of Virology Lesson 101 for today. There is some similarity, but the 1918 flu actually originated on a farm in Kansas, had a 2% death rate, took a trip to Europe, mutated, came back months later, and then had a death rate of 50%. We haven't seen that second wave yet, or major mutations. We have seen a couple of different DNA strands out there though, meaning we would need multiple different vaccines when we get them. By the way, it was called the “Spanish Flu” because during WWI, every country had censorship except Spain because it was not a combatant. So, the pandemic was only reported in the Spanish newspapers.

Q: Would you get out of any of the previously recommended LEAPS?

A: Yes, I would be taking profits on all of your LEAPS—whether tech, domestic, “recovery”, or whatever else—so if we do get a correction over the summer, you can get back in at better prices, with longer expirations. You can go two years out from say August for example. The risk/reward today is terrible.

Q: Would you hold on to the (SDS) right now, or wait for the pullback

A: No, we have offsetting profits on all of our (SDS) positions, until today—if the market keeps accelerating to the upside, SDS losses will start to offset our profits on the positions, so that’s why I would get out.

Q: Should I buy the ProShares Ultra-Short 20 + Year Treasury Bond Fund (TBT)? I don’t do options.

A: You don’t need to do options, (TBT) is an ETF; anybody can buy that, it’s just like buying a stock.

Q: What is happening with the Australian market?

A: It will trade with the US stock market tick for tick, which means they’ve had a fantastic rally, overdue for a selloff. Wait to buy the next dip.

Q: If markets are going to go down soon, why exit the (SDS)

A: It may go up first before it goes down. And in any case, I have a great profit on the combined position of long (SDS) and short bonds. These days, I like taking big profits rather than praying they become bigger. It’s about risk control and knowing what you can get away with in certain market conditions.

Q: Is now the time to sell the highflyers in tech?

A: Yes, I would be selling Apple (AAPL), Facebook (FB), Microsoft (MSFT), and Amazon (AMZN). Get dry powder, which is worth a lot after you’ve seen a move like this; especially if the economy gets worse, which is likely. My late mentor Barton Biggs taught me to always leave the last 10% of a move for the next guy.

Q: At what point do you buy the ProShares Ultra Short S&P 500 ETF (SDS) outright?

A: Only if there is an immediate collapse in the market, which I can’t foresee with any certainty. When you play these bear ETFs, the costs are very high. You are short double the (SPX) dividend, which is about 5% a year, plus hefty management fees. So, you really have to catch a quick, large move to the downside to make any real money.

Q: Real estate seems like the big winner of the pandemic. Will prices be up by the end of the year or is this just a temporary spike?

A: They will be up at the end of the year. I have been telling readers all year that their home will be their best investment in 2020 and that is coming true. Real estate has a massive tailwind behind it which has really been in place for a couple of years now, and that is the millennials upgrading and buying houses. The pandemic has really poured gasoline on the fire and triggered a stampede out of the city and into the suburbs. Having 85 millennials ready to upgrade their homes is a huge positive for the real estate market, and I’d be looking to buy the homebuilders on any dip. That’s probably the best domestic play out there. Buy Lennar Corp. (LEN) and Pulte Homes (PHM) on dips.

Q: Post pandemic, will manufacturing have any way of helping US economic growth, or is bringing back the supply chains fake news?

A: It is fake news because if companies bring back production, it will be machines and not people making things. Unless you want to pay $10,000 for an iPhone, or $5,000 for a low-end laptop. Oh yes, and the stocks which made these things would be 90% lower as well. That’s what those products cost in today’s dollars if they were made in the United States. I wouldn't count on any repatriation of US jobs unless people want to work for $3 a day like the Chinese do. Offshoring happened for a reason.

Q: How do I hedge a municipal bond portfolio?

A: You might think about taking profits in muni bonds. They’re yielding around 2% and change. And they could get hit with a nice little 20-point decline if the US Treasury bond market (TLT) falls apart, which it will. Then you can think about buying them back. If you really want to hedge, you sell short the (TLT) against your long muni bond portfolio. But that is an imperfect hedge because the default rate on munis is going to be much higher than it is now than it was in 2008-2009, and much higher than US Treasuries, which never defaults despite what the president has said.

Q: What is dry powder?

A: It means having cash to buy stocks at market bottom. In the 1800s before cartridges were invented, black powder got wet whenever it rained causing guns to fail to shoot. That is the historical analogy.

Q: What do we do now if we’re getting started?

A: It will require a lot of discipline on your part as coming in at market tops is always risky. Wait for the next trade alert. Every one of these is meant to work on a standalone basis. I would do nothing unless you see one of these things happen; any 2 or 3-point rally in bonds (TLT), you want to sell short. We’re just at the beginning of a multiyear trade here so it’s not too late to get back into that. Gold (GLD) is probably safe to buy on the dip here since we are at the very beginning of a historic expansion of the global money supply. I wouldn’t touch any stocks unless we get at least a 10% drop and then I'll start putting out call spread recommendations on single stocks. But right here, on top of the biggest bounceback in stocks in market history, don’t do anything. Just read the research and make lists of things to buy when they do dip—something I do for you anyway.

Q: What about Beyond Meat (BYND)?

A: The burgers are not that bad, but the stock is way overpriced and you don’t want to touch it. It's one of the fad stocks of the day.

Q: Can we access the slides after the webinar?

A: Yes, we post it on the website under your “Account” section about two hours after we’re done.

Q: Are you saying sell everything currently profitable?

A: Yes, I would be selling everything on a short term basis, keep tech and biotech on a long term basis. We are the most overbought in history and you don’t get asked twice to sell tops. But yes, it could go higher before the turn happens. From a risk-reward point of view, it’s terrible to do anything right now.

Q: Could we get a pullback to the $260-$270 area in the S&P 500 (SPY)?

A: Yes, especially if we get a second worse wave of corona and the stimulus takes much longer than we thought to get into the economy, or if the rioting continues.

Q: Should you sell CCI now?

A: Yes, I actually would. You have a 57% gain in the stock in ten weeks, so why not? Long term, it’s a hold.

Q: Are any retail stocks a buy?

A: No, they aren’t because a lot of them are going to go under but you don’t know which ones. After shutting down and losing 60% of their revenues, they’re now being burned down. The pros who do well in the sector are bankruptcy specialists who have massive research teams that analyze every lease in every mall and then cherry-pick. You and I don’t have the ability to do that so stay away.

Q: What is the best way to play real estate?

A: Buy a house. If not, then you buy (LEN), (KBI), and (PHM).

Q: Is it too late to get back in the stock market?

A: Yes, I'm afraid it is. Buying, because it has gone up, is a classic retail investor mistake. After this meltdown, maybe you will learn to buy stocks when everyone else is throwing up on their shoes. That's what I was doing in March and we got returns of 50% to 100% on everything and 500% to 1,000% on the LEAPS (TSLA).

Q: Are you buying puts?

A: No, I am not taking outright short positions any more than I have now because we have a Fed-driven melt-up underway with a stimulus that's 20x larger than that seen during the 2008-2009 Great Recession. When I don’t know what’s going to happen, I get out.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Lately, my inbox has been flooded with emails from subscribers asking if the housing market is about to crash as a result of the pandemic and if they should sell their homes.

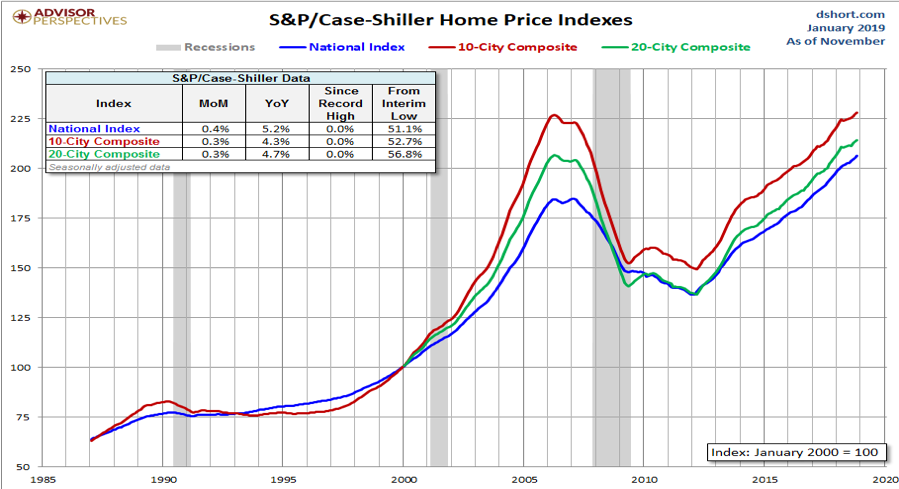

They have a lot to protect. Since prices hit rock-bottom in 2011 and foreclosures crested, the national real estate market has risen by 50%.

The hottest markets, like those in Seattle, San Francisco, and Reno, are up by more than 125%, and certain neighborhoods of Oakland, CA have shot up by 500%.

Looking at the recent housing statistics, I can understand their concern. The grim tidings are:

*2.9 Million Homes Now in Forbearance, and the number is certainly going to rise from here. Laid off renters are defaulting on payments, depriving owners of meeting debt obligations. It’s just a matter of time before this creates a financial crisis. Avoid the banks for now, no matter how cheap they get.

* Existing Home Sales Collapsed by 15.4%, in March. Realtors expect this figure to drop 40% in the coming months. Open houses are banned, sellers are pulling listings, and buyers low-balling offers. However, price declines in the few deals going through are minimal. When will the zero interest rates come through? Mortgage interest rates are higher now than before the pandemic because 6% of all home loans are now in default.

* Pending Home Sales Down a Staggering 20.8% in March, and off 16.3% YOY. The worst is yet to come. The West, the first into shelter-in-place, was down a monster 26.8%. Prices still aren’t moving because nobody can buy or sell.

*Chinese Buying of West Coast homes has vaporized over trade war fears, and then of the Covid-19 lockdown, which started with a shutdown of all flights from China.

I have a much better indicator of future housing prices than the depressing numbers above. The way homebuilder stocks like Lennar (LEN), KB Homes (KBH), and Pulte Homes (PHM) are trading, I’d say your home will be worth a lot more in a year, and possibly double in another five years. Many of these stocks are up nearly 100% since the March 23 bottom.

What I call “intergenerational arbitrage” will be the principal impetus. The main reason that we are now enduring two “lost decades” of economic growth over the last 20 years is that 85 million baby boomers are retiring to be followed by only 65 million “Gen Xer’s”. When you are losing 20 million consumers, economies don’t grow very fast. For more about millennial investing habits, please click here.

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and “RISK ON” assets like equities, and more buyers of assisted living facilities, healthcare, and “RISK OFF” assets like bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward to the other side of the pandemic and the reverse happens. The baby boomers will be out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xer’s being chased by 85 million of the “millennial” generation trying to buy their assets!

By then we will not have built new homes in appreciable numbers for 14 years and a severe scarcity of housing hits. Even before the pandemic, new home construction was taking place at half the 2008 peak. Residential real estate prices will naturally soar. Labor shortages will force wage hikes.

The middle-class standard of living will then reverse a 40-year decline. Annual GDP growth will return from the subdued 2% rate of the past three years to near the torrid 4% seen during the 1990s. It all leads to my “Return of the Roaring Twenties” scenario which you can learn about by clicking here.

It gets better.

It is certain that a future administration will restore tax deductions for state and local real estate taxes (SALT) lost in the 2017 tax bill. The cap on home mortgage interest rate deductions will also rise.

These two events will trigger an immediate 10% increase in the value of your home on an after-tax basis and more on the coasts.

So, if someone approaches you with a discount offer for your home, I would turn around and run a mile the other way.

You should also pile into the stocks, options, and LEAPS of housing stocks in any future market dip.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/04/home-sales2.png385685Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-04-30 08:02:332020-06-08 12:12:20Why a US Housing Boom is Imminent

Global Market Comments

September 11, 2019 Fiat Lux

Featured Trade:

(HAS THE VALUE OF YOUR HOME JUST PEAKED?),

(ITB), (PHM), (KBH), (LEN), (DHI), (NVR), (TOL), (JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA CONFERENCE, OCTOBER 25-26, 2019)

Lately, my inbox has been flooded with emails from subscribers asking how to hedge the value of their homes. This can only mean one thing: the residential real estate market has peaked.

They have a lot to protect. Since prices hit rock bottom in 2011 and foreclosures crested, the national real estate market has risen by 50%.

I could almost tell you the day the market bounced. That’s when a couple of homes in my neighborhood that had been for sale for years suddenly went into escrow.

The hottest markets, like those in Seattle, San Francisco, and Reno, are up by more than 125%, and certain neighborhoods of Oakland, CA have shot up by 400%.

The concerns are confirmed by data that started to roll over in the spring and have been dismal ever since. It is not just one data series that has rolled over, they have all gone bad. One bad data point can be a blip. An onslaught is a new trend. Let me give you a dismal sampling.

*Home Affordability hit a decade low, thanks to rising prices and interest rates and trade war-induced soaring construction costs

*July Housing Starts have been in a tailspin as tariff-induced rocketing costs wipe out the profitability of new homes

*New Home Sales collapsed YOY.

*14% of all June Real Estate Listings saw price cuts, a two-year high

*Chinese Buying of West Coast homes has vaporized over trade war fears

Fortunately, investors have a lot of options for either hedging the value of their own homes or making a bet that the market will fall.

In 2006, the Chicago Mercantile Exchange (CME) started trading futures contracts for the Corelogic S&P/Case-Schiller Home Price Index, which covered both U.S. residential and commercial properties.

The Case-Shiller index, originated in the 1980s by Karl Case and Robert Shiller, is widely considered to be the most reliable gauge to measure housing price movements. The data comes out monthly with a three-month lag.

This index is a widely-used and respected barometer of the U.S. housing market and the broader economy and is regularly covered in the Mad Hedge Fund Trader biweekly global strategy webinars.

The composite weight of the CSI index is as follows:

Boston 7.4%

Chicago 8.9%

Denver 3.6%

Las Vegas 1.5%

Los Angeles 21.2%

Miami 5%

New York 27.2%

San Diego 5.5%

San Francisco 11.8%

Washington DC 7.9%

However, these contracts suffer from the limitations suffered by all futures contracts. They can be illiquid, expensive to deal in, and you probably couldn’t get permission from your brokers to trade them anyway.

If you want to be more conservative, you could take out bearish positions on the iShares US Home Construction Index (ITB), a basket of the largest homebuilders (click here for their prospectus). Baskets usually present half the volatility and therefore half the risk of any individual stock.

If real estate is headed for the ashcan of history, there are far bigger problems for your investment portfolio than the value of your home. Real estate represents a major part of the US economy and if it is going into the toilet, you could too.

It is joined by the sickly auto industry. Thanks to the trade wars, farm incomes are now at a decade low. As we lose each major segment of the economy, the risk is looming that the whole thing could go kaput. That, ladies and gentlemen, is called a recession and a bear market.

On the other hand, you could take no action at all in protecting the value of your home.

Those who bought homes a decade ago, took a ten-year cruise and looked at the value of their residence today will wonder what all the fuss is about. By the way, I met just such a person on the Queen Mary 2 last summer. Yes, ten years at sea!

And the next recession is likely to be nowhere near as bad as the last one, which was a twice-a-century event. So it’s probably not worth selling your home and buying it back later, as I did during the Great Recession.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/home-sales-signboard.png345612MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-09-11 01:04:282019-10-14 09:48:32Has the Value of Your Home Just Peaked?

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX),

(WHY THE REAL ESTATE BOOM HAS A DECADE TO RUN),

(DHI), (LEN), (PHM), (ITB)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-20 01:08:042019-02-19 16:33:08February 20, 2019

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.