Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics are destiny, then America’s future looks bleak. You see, they’re just not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the number of middle-aged big spenders is falling, risk markets plunge.

Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

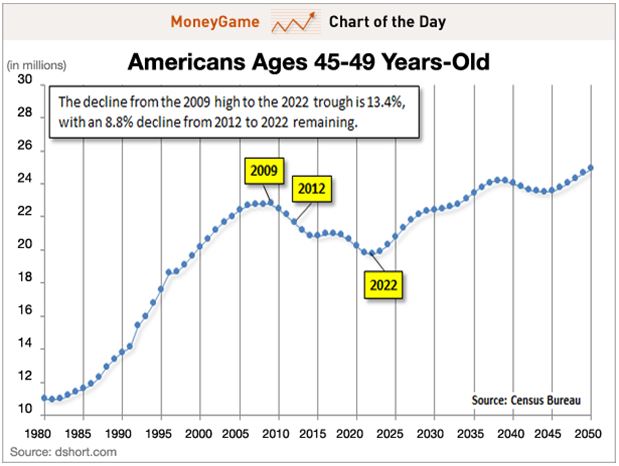

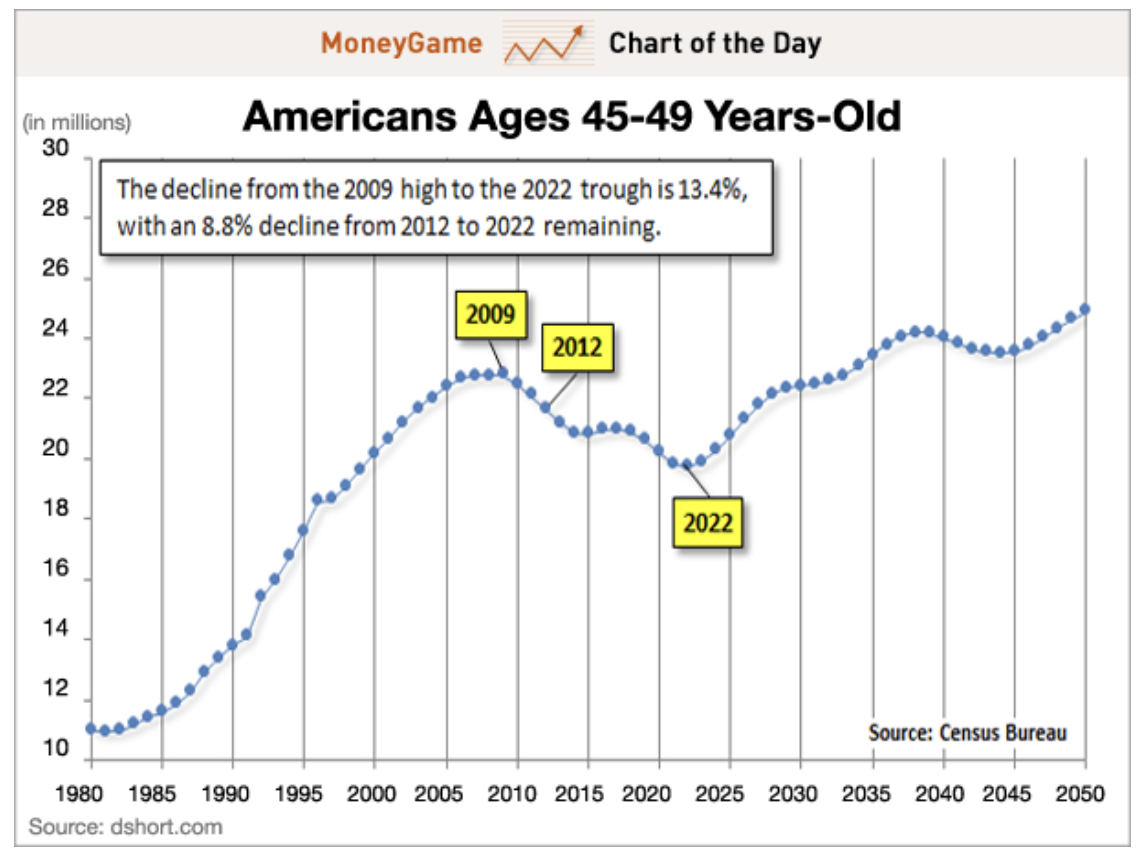

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

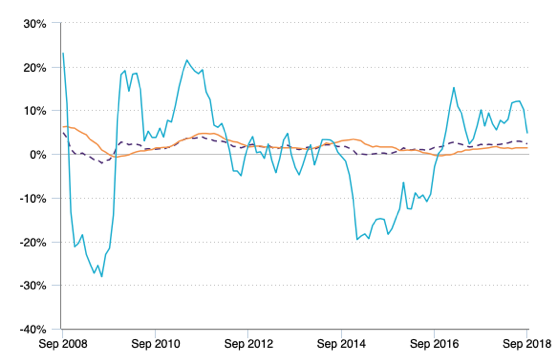

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, but they also backtest with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country, and you can develop a highly reliable timetable for when and where to invest.

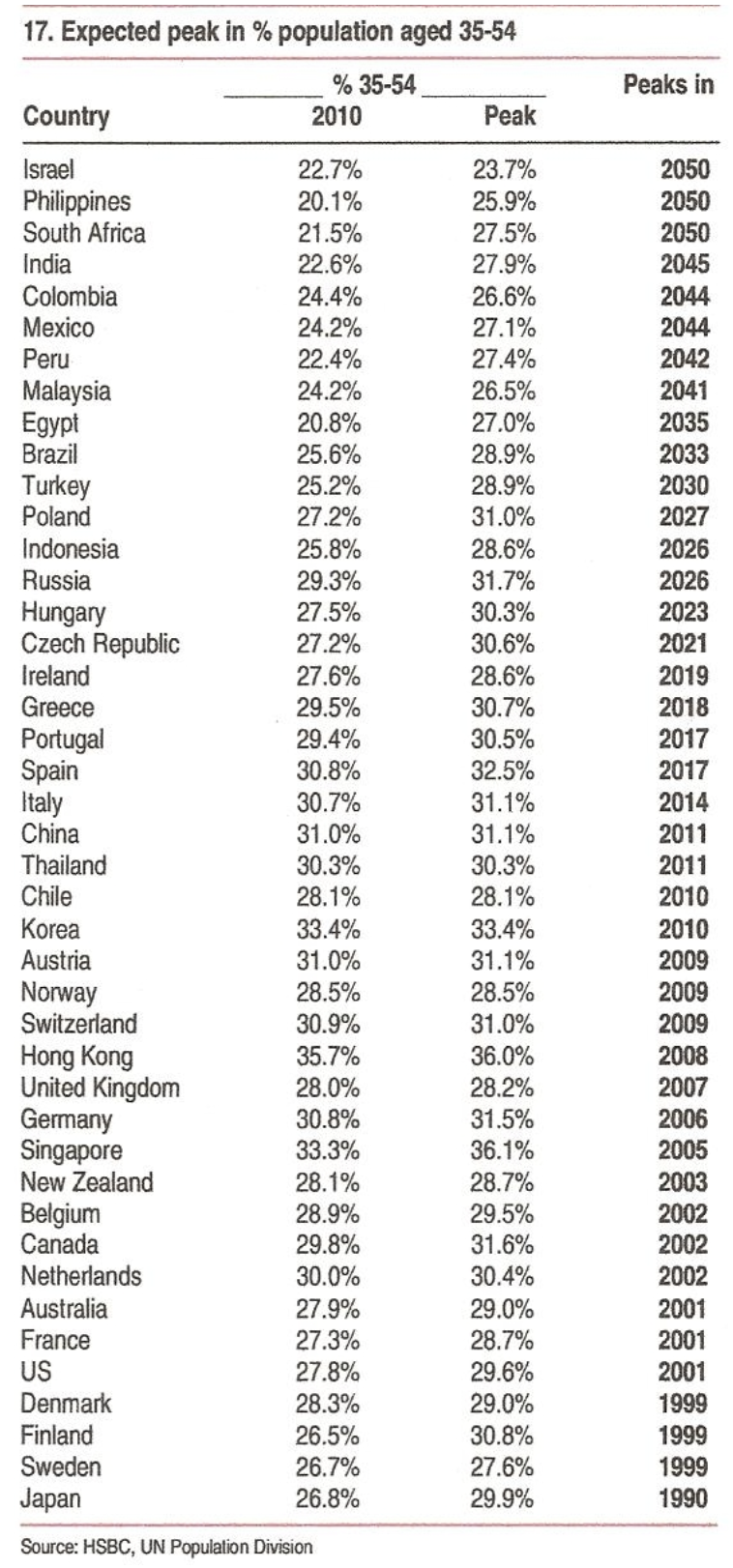

Instead of poring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice back test.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2,000’s, and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate, peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle-aged not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan), while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

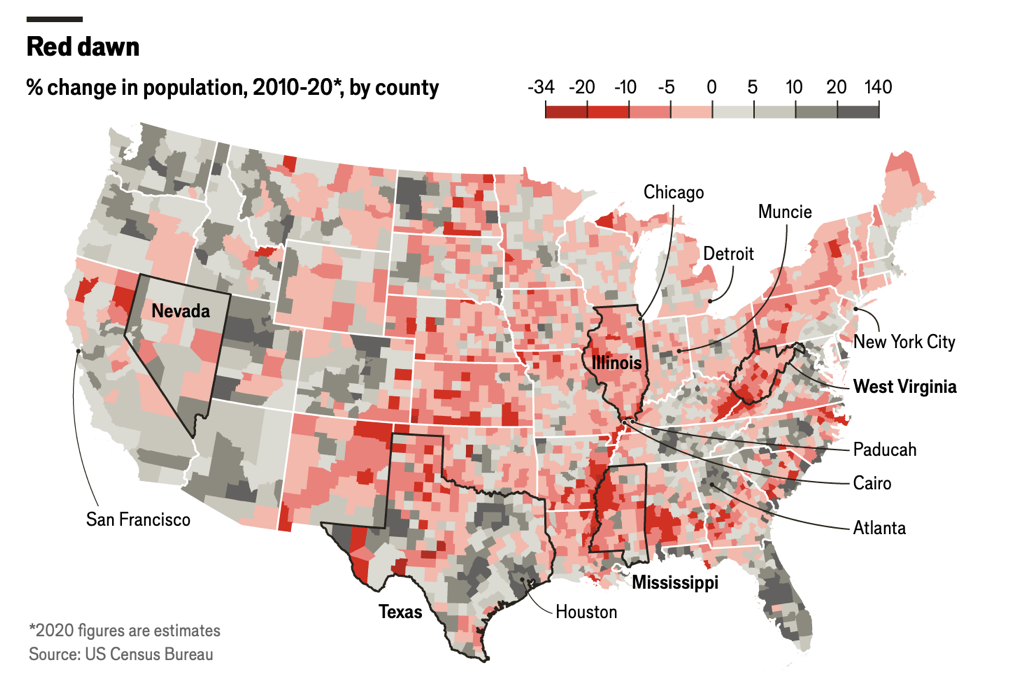

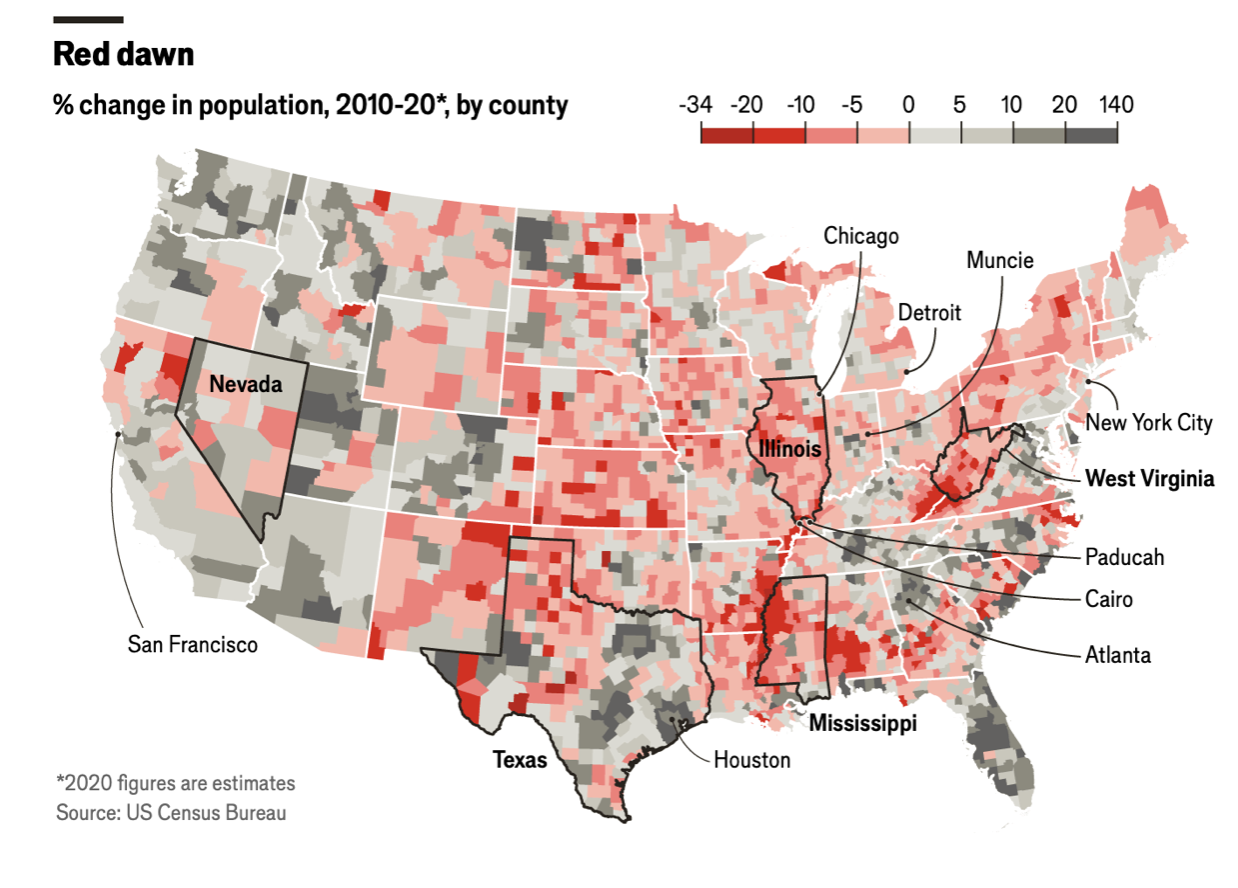

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills is picking up speed, and the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Global Market Comments

April 24, 2024

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics is destiny, then America’s future looks bleak. You see, they’re not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the numbers of the middle-aged big spenders are falling, risk markets plunge. Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, they also back-test with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country and you can develop a highly reliable timetable for when and where to invest.

Instead of pouring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice backtest.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2000s and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle age not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan) while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills picking up speed, the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Mad Hedge Technology Letter

April 1, 2019

Fiat Lux

Featured Trade:

(THE NEXT TECH BUBBLE TOP HAS STARTED)

(LYFT), (PIN), (UBER), (AAPL), (JPM), (FB)

Don't go chasing rainbows.

That is what the current tech IPO environment is hinting.

Even though market conditions are frothy, that doesn't mean I'm calling a market top today, hardly so.

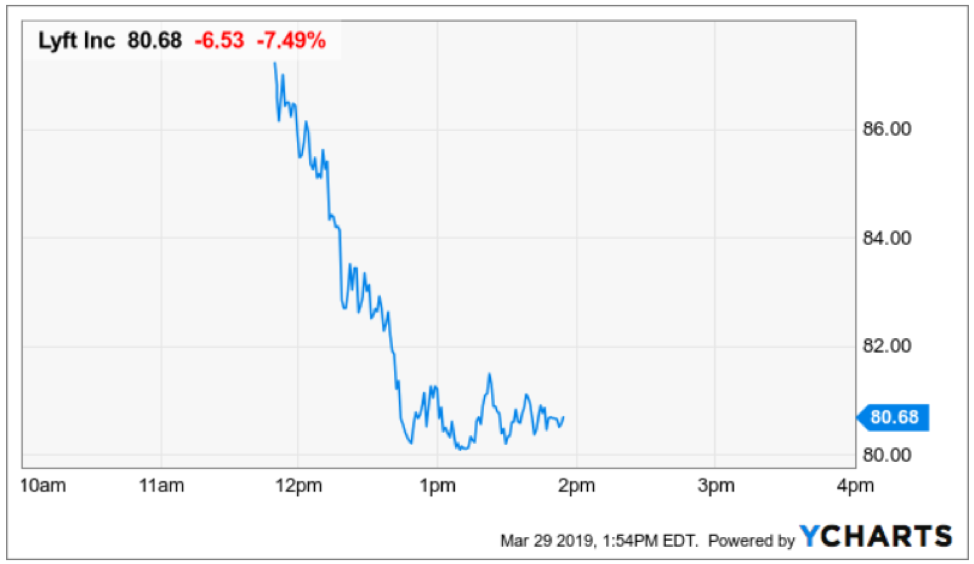

I predicted that Lyft (LYFT) would storm out of the gate like a bull on ecstasy, and I was vindicated when the stock flirted intraday with the $87 mark.

The scarcity value of these gig economy companies is hard to quantify.

Examples Uber unduly promise ambition and innovation leading to hopes of a possible air transport service and sharing network that I would need to see to believe.

The built-up expectations smell of over-promising and under-delivering, the majority won’t be able to deliver merely half of what their manifestos promulgate

As I put my analyst hat on, the 2019 IPO frenzy coming online has some of the same fingerprints of the infamous dot com bust of 2001.

The two main trends symbolic of the last time the tech industry disentangled were overly generous valuation, pricing in revenue expansion of 80% for the next five years when the leader of the pack Microsoft (MSFT) only grew at 50%.

A tantalizing clue was the utterly deficient cash flow generated back then.

The underlying premise revolved around putting the network effect on a pedestal irrespective of understanding that the network effect should have caused cash flow to accelerate which was conspicuously absent.

Losing money and losing a lot of it does lead to paralysis, examples were rife, for instance, priceline.com losing $30 on each air ticket sold.

Even more hard to fathom was that Priceline was stretching itself to the limits on the open market filling ticket orders because of a dearth of inventory steepening losses.

Priceline gushed about a unique business model of collecting excess ticket inventory that airlines couldn't sell at low cost and reskinning them to a digital audience hoping to take advantage of this price dispersion.

But in reality, this wasn’t always the case.

Priceline was on a suicide mission and expanding from 50 employees to 300 employees based upon misleading growth was madness.

In a nutshell, investors bypassed pragmatic arithmetic and were lifted by the fumes of exuberance that had manifested around the euphoria of the tech bubble.

Lyft is not revolutionary, they are a broker which occupy a low position in the spectrum of tech intellectual property.

Exploiting drivers, compensating them per hour, and letting them figure out their own cost structures for car insurance, fuel costs, and opportunity cost while offering zero benefits is a court battle waiting to happen in California.

And if your response was the way they craft value is by way of a proprietary app, well, Google, Apple, or even Netflix can produce the same type of app and quality of app in a few weeks with their legendary phalanx of top-tier engineering talent.

To Lyft’s credit, they have at least collected the treasure trove of data the app has compiled which is extraordinarily valuable.

The top of the tech bubble means that big tech is overreaching into any revenue they can get their hands on like a heroin addict yearning for the next syringe.

The environment has transformed into an eerily zero-sum game, such as Apple (AAPL) cooperating with JPMorgan Chase (JPM) to create Apple pay, and then instantly flipping around to compete with JPMorgan Chase in the credit card space with Apple Pay being an accomplice.

Big tech has sown the seeds of discord by quietly attempting to trample on any analog business they can get near.

Leveraging the network effect of billions of users in a proprietary walled garden to extract the incremental dollar for a new service is impossible to compete with for analog companies without a similar embedded on-demand audience.

Lyft co-founder and CEO Logan Green mentioned in an interview that in the next five year, he plans to deploy a subscription service coined as transportation-as-a-service like a software-as-a-service option which cloud platforms sell.

A fight to the bottom with Uber will cause major disruption in the pricing mechanisms of the subscription service and could force Lyft to earn less revenue per ride than the current pricing system.

Investors need to remember that Uber is bigger than Lyft and possessed more ammunition.

At the end of the day, the race to the bottom is never good for profitability or sustainability, and Lyft has yet to provide any substantial clues on how they will navigate through this quagmire.

My guess is that Lyft will have to do a deal with the devil of sorts to slang its branded broker app onto the cresting wave of Waymo as Waymo motors ahead and starts to materially monetize its self-driving program.

Remember that Alphabet already has a small stake in Lyft and these two could partner up with Alphabet dictating terms.

Lyft cannot compete with the holy grail of tech - self-driving technology – they are way down the tech value chain.

If we look at the bigger picture, the broader market has been riding the coattails of Federal Reserve Chairman Jerome Powell’s 180-degree turn from winter’s statement that interest rate tightening was on “autopilot.”

Now, there is only a 27% chance given by the market that the Fed will raise rates at all in 2019.

The market responded with strength begetting strength allowing the bull run to continue and even whispers of a possible rate cut later this year.

Sentiment will not change until we get to the point when earnings can’t surpass the expectation which have been lowered substantially.

I bet this won’t happen until late this year or next year.

This is inning 8 or 9 of the bull crusade, the closer is warming up in the bullpen.

Lyft’s opening day gallop is just one of the side effects from a market that is toppy.

Global Market Comments

November 2, 2018

Fiat Lux

Featured Trade:

(OCTOBER 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(EDIT), (TMO), (OVAS), (GE), (GLD), (AMZN), (SQ), (VIX), (VXX), (GS), (MSFT), (PIN), (UUP), (XRT), (AMD), (TLT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 31 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: I would like to keep CRISPR stocks as a one or two-year-old, or even longer if it is prudent. What do you think?

A: Yes, there is a CRISPR revolution going on in biotech—I’m extremely bullish on all these stocks, like Editas Medicine (EDIT), Thermo Fisher Scientific (TMO), and Ovascience Inc. (OVAS). If any of these individual companies don’t move forward with their own technology, they will get taken over. The principal asset of these companies is not the patents or the products, it’s the staff, and there is an extreme shortage in CRISPR specialists (and anybody who knows anything about monoclonal antibodies).

Q: Could you explain how to manage LEAPs? For example, the Gold (GLD) and the General Electric (GE) LEAPs. Sit and leave them or trade them short term?

A: You make a lot of money trading long-term LEAPs. Just because you own a year and a half LEAP doesn’t mean that you keep it for a year and a half. You sell it on the first big profit, and I happen to know that on both the Gold (GLD) and the (GE) LEAPs we sent out, people made a 50% profit in the first week. So, I told them: sell it, take the profit. The market always gives you another chance to get in and buy them cheap. You make the money on the turnover, on the volume—not hanging out trying to hit a home run.

Q: Why did you only close the Amazon (AMZN) November $1,550-$1,600 vertical bull call spread and not roll the strike prices down and out?

A: Well I actually did do the down and out strike roll out first, which is the super aggressive approach. By adding the November $1,350-$1,400 vertical bull call spread position on Monday at the market lows and doubling the size—we took a huge 30% position in Amazon and that position alone should bring in about $3600 in profits in two weeks, at expiration. And when I put on that second position I told myself that on the next big rally I would get out of the high-risk trouble making position, which was the November $1,550-$1,600 vertical bull call spread. So that’s how you trade your way out of a 30% drop in three weeks in one of the best tech stocks in the market.

Q: Is AT&T (T) no longer a good buy at these prices?

A: All of the telephone companies have legacy technology, meaning they are all dying. Basically, AT&T is about owning a bunch of rusting copper wire spread around the country. They haven’t been able to innovate new technologies fast enough to keep up with others who have. The only reason to own this is for the very high 6.56% dividend. That said, dividends can be cut. Look at General Electric which cut its dividend earlier this year. Whatever you make of the dividend can get lost in the principal.

Q: Do you think Square (SQ) is a good buy at this level?

A: Absolutely, it’s a screaming buy. It’s one of the favorite companies of the Mad Hedge Technology Letter and one of the preeminent disruptors of the banks. We think there’s another 400% gain in Square from here. It’s dominating FinTech now.

Q: When do you expect to close the short position in the iPath S&P 500 VIX Short-Term Futures ETN (VXX)?

A: If we can get the Volatility Index (VIX) down to $15, the (VXX) should crater. We’ll take a hit on the time decay and that’s why I say we may be able to sell it for 20 cents in the future when this happens. We’ll still take a 50% hit on the position, but half is better than none.

Q: What happened to Microsoft (MSFT) last week?

A: People sold their winners. They had a great earnings report and great long-term earnings prospects, but everyone in the world owned it. Buy the long-term LEAP on this one.

Q: If we want to double up on the iPath S&P 500 VIX Short-Term Futures ETN (VXX), how do you plan to do it?

A: Go out to further with your expiration date. When you go long the (VXX) you only buy the most distant expiration date. I would buy the February 15 expiration as soon as it becomes available.

Q: How do you see Goldman Sachs (GS) from here to the end of the year?

A: It may go up a little bit as we get some index money coming into play for year-end, but not much; I expect banks to continue to underperform. They are no longer a rising interest rate play. They are a destruction by FinTech play.

Q: Is it too soon for emerging markets in India (PIN)?

A: As long as the dollar (UUP) is strong, which is going to be at least another year, you want to avoid emerging markets like the plague. As long as the Federal Reserve keeps raising interest rates, increasing the yield differential with other currencies, the buck keeps going up.

Q: What are your thoughts on retail ETFs like the SPDR S&P Retail ETF (XRT)?

A: You may get lucky and catch a rally on that but the medium term move for retail anything is down. They are all getting Amazoned.

Q: Is it better to increase long exposure the day before the election?

A: No, what we saw starting on Tuesday was the pre-election move. That said, I expect it to continue after the election and into yearend.

Q: Any opinions on Advanced Micro Devices (AMD)?

A: Yes, this is a great level. It was extremely overbought two months ago but has now dropped 50%. It is a great long-term LEAP candidate.

Q: What about the W bottom in the stock market that everyone thinks will happen?

A: I’m one of those people. So far, the bottom for the move in the S&P 500 is looking pretty convincing, but we will test the faith sometime in the next week I’m sure. We got close enough to the February $252 low to make this a very convincing move. It sets up range trading for the market for the next year.

Q: How do you figure the inflation rate is 3.1%?

A: The year-on-year Consumer Price Index for September printed at 2.3%, and the most recent months have been running at an annualized 2.9% rate. Given that this data is months old we are probably seeing 3.1% on a monthly annualized basis now given all the anecdotal evidence of rising prices and wages that are out there. That is certainly what the bond market believes with its recent sharp selloff and why I will continue to be a fantastic short. Sell every United States US Treasury Bond Fund ETF (TLT) rally. Like hockey great Wayne Gretzky said, you have to aim not where the hockey puck is, but where it's going to be.

Q: Will rising interest rates kill the housing market?

A: It already has. A 5% 30-year mortgage rate shuts a lot of first time Millennial buyers out of the market. We are seeing real estate slowing all over the country. Los Angeles is getting the worst hit.

Q: How do you see the Christmas selling season going?

A: It’s going to be great, but this may be the last good one for a while. And Amazon is getting half the business.

Q: October was terrible. How do you see November playing out?

A: It could well be a mirror image of October to the upside. We are already $1,000 Dow points off the bottom. So far, so good. Throw fundamentals out the window and buy whatever has fallen the most….like Amazon.

Did I mention you should buy Amazon?

Good luck and good trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 7, 2018

Fiat Lux

Featured Trade:

(MONDAY, OCTOBER 15, 2018, ATLANTA, GA,

GLOBAL STRATEGY LUNCHEON),

(SEPTEMBER 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(AMZN), (MU), (MSFT), (LRCX), (GOOGL), (TSLA),

(TBT), (EEM), (PIN), (VXX), (VIX), (JNK), (HYG), (AAPL)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 5 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Do you think the collapse of commodity prices in the U.S. will affect the U.S. election?

A: Absolutely, it will if you count agricultural products as commodities, which they are. We have thousands of subscribers in the Midwest and many are farmers up to their eyeballs in corn, wheat, and soybeans. It won’t swing the entire farm vote to the Democratic party because a lot of farmers are simply lifetime Republicans, but it will chip away at the edges. So, instead of winning some of these states by 15 points, they may win by 5 or 3 or 1, or not at all. That’s what all of the by-elections have told us so far.

Q: What will be the first company to go to 2 trillion?

A: Amazon, for sure (AMZN). They have so many major business lines that are now growing gangbusters; I think they will be the first to double again from here. After having doubled twice within the last three years, it would really just be a continuation of the existing trend, except now we can see the business lines that will actually take Amazon to a much bigger company.

Q: Is this a good entry point for Micron Technology (MU)?

A: No, the good entry point was in the middle of August. We are at an absolute double bottom here. Wait for the tech washout to burn out before considering a re-entry. Also, you want to buy Micron the day before the trade war with China ends, since it is far and away its largest customer.

Q: Is Micron Technology a value trap?

A: Absolutely not, this is a high growth stock. A value trap is a term that typically applies to low price, low book to value, low earning or money losing companies in the hope of a turnaround.

Q: I didn’t get the Microsoft (MSFT) call spread when the alert went out — should I add it on here?

A: No, I am generally risk-averse this month; let’s wait for that 4% correction in the main market before we consider putting any kind of longs on, especially in technology stocks which have had great runs.

Q: How do you see Lam Research (LRCX)?

A: Long term it’s another double. The demand from China to build out their own semiconductor industry is exponential. Short term, it’s a victim of the China trade war. So, I would hold back for now, or take short-term profits.

Q: Is this a good entry point for Google (GOOGL)?

A: No, wait for a better sell-off. Again, it’s the main market influencing my risk aversion, not the activity of individual stocks. It also may not be a bad idea to wait for talk of a government investigation over censorship to die down.

Q: Would you buy Tesla (TSLA)?

A: No, buy the car, not the stock. There are just too many black swans out there circling around Tesla. It seems to be a disaster a week, but then every time you sell off it runs right back up again. Eventually, on a 10-year view I would be buying Tesla here as I believe they will eventually become the world’s largest car company. That is the view of the big long-term value players, like T. Rowe Price and Fidelity, who are sticking with it. But regarding short term, it’s almost untradable because of the constant titanic battle between the shorts and the longs. At 26% Tesla has the largest short interest in the market.

Q: I’m long Microsoft; is it time to buy more?

A: No, I would wait for a bit more of a sell-off unless you’re a very short-term trader.

Q: What would you do with the TBT (TBT) calls?

A: I would buy more, actually; preferably at the next revisit by the ProShares Ultra Short 20 Year Plus Treasury ETF (TBT) to $33. If we don’t get there, I would just wait.

Q: What’s your suggestion on our existing (TLT) 9/$123-$126 vertical bear put spread?

A: It expires in 12 days, so I would run it into expiration. That way the spread you bought at $2.60 will expire worth $3.00. We’re 80% cash now, so there is no opportunity cost of missing out with other positions.

Q: Do you like emerging markets (EEM)?

A: Only for the very long term; it’s too early to get in there now. (EEM) really needs a weak dollar and strong commodities to really get going, and right now we have the opposite. However, once they turn there will be a screaming “BUY” because historically emerging nations have double the growth rate of developed ones.

Q: Do you like the Invesco India ETF (PIN)?

A: Yes, I do; India is the leading emerging market ETF right now and I would stick with it. India is the next China. It has the next major infrastructure build-out to do, once they get politics, regulation, and corruption out of the way.

Q: Do you trade junk bonds (JNK), (HYG)?

A: Only at market tops and market bottoms, and we are at neither point. When the markets top out, a great short-selling opportunity will present itself. But I am hiding my research on this for now because I don’t want subscribers to sell short too early.

Q: With the (VXX), I bought the ETF outright instead of the options, what should I do here?

A: Sell for the short term. The iPath S&P 500 VIX Short-Term Futures ETN (VXX) has a huge contango that runs against it, which makes long-term holds a terrible idea. In this respect it is similar to oil and natural gas ETFs. Contango is when long-term futures sell at a big premium to short-term ones.

Q: How much higher for Apple (AAPL)?

A: It’s already unbelievably high, we hit $228 yesterday. Today it’s $228.73, a new all-time high. When it was at $150, my 2018 target was initially $200. Then I raised it to $220. I think it is now overbought territory, and you would be crazy to initiate a new entry here. We could be setting up for another situation where the day they bring out all their new phones in September, the stock peaks for the year and sells off shortly after.