Mad Hedge Technology Letter

November 18, 2024

Fiat Lux

Featured Trade:

(SPOTIFY WORTH A LOOK)

(SPOT), (META), (PINS)

Mad Hedge Technology Letter

November 18, 2024

Fiat Lux

Featured Trade:

(SPOTIFY WORTH A LOOK)

(SPOT), (META), (PINS)

If new research from Pew Research is anything close to accurate, there appears to be a massive shift underway that has major ramifications for the online media landscape.

Pew Research discovered that 40% of young adults rely on social media influencers without formal journalism training.

Gone are the days when journalists needed to cut their teeth doing coverage on the ground.

This phenomenon has reversed with social media influencers and podcasters dishing out the real media from the comfort of their home.

Yes, this has been happening for a while, but the data suggests we are on the cusp of the legacy media becoming the minority.

The evolving landscape was most notably taken advantage of the richest man in the world, Elon Musk, who used X.com to propel him into politics.

Most social media users relying on news influencers say the information they offer is unique and sometimes more helpful than what they’d find elsewhere and less likely to be fake.

Social media news is also reliant on ad revenue to stay afloat, so in that sense, it could be beholden to advertiser demands on viewpoint and ideology. The legacy media has the same ongoing problem with advertisers, and I believe there is no perfect model.

Yet, the direct connection of social media profiles to audience has grown and will remain attractive moving forward.

According to the survey, traditional journalism is dead, and 40% of young adults under 30 rely on these news influencers to stay updated on current events and politics.

While X, formerly Twitter, is the most popular platform for news influencers, video app TikTok and Google’s YouTube are home to the largest share of news influencers who monetize their content and have no formal background in journalism. Of the news influencers on TikTok, 84% haven’t worked in journalism, and roughly three-quarters of those influencers try to make money off their news analysis, whether by asking for tips, peddling merchandise, or touting separate subscriptions to additional exclusive material, Pew found.

The Pew report analyzed hundreds of news influencer accounts with more than 100,000 followers; surveyed more than 10,600 US adults about their news consumption habits; and reviewed content from more than 100,000 posts across Facebook, Instagram, TikTok, X, and YouTube from July and August.

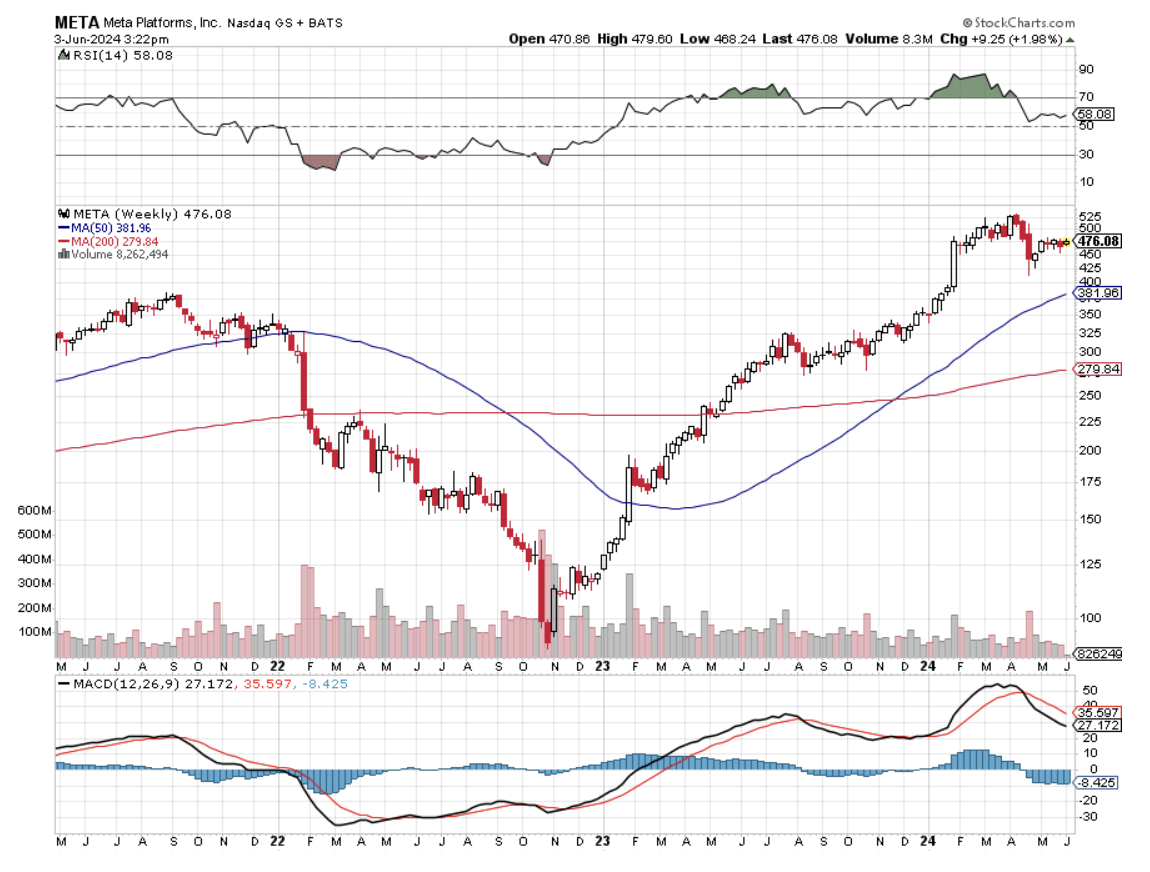

One of the reasons traders cannot short META stock is because of this cash cow business tied to social media.

Instagram and Facebook are still great businesses, even if they aren’t growing like they used to.

TikTok is a private company, and so is X.com, and there are no stock opportunities there.

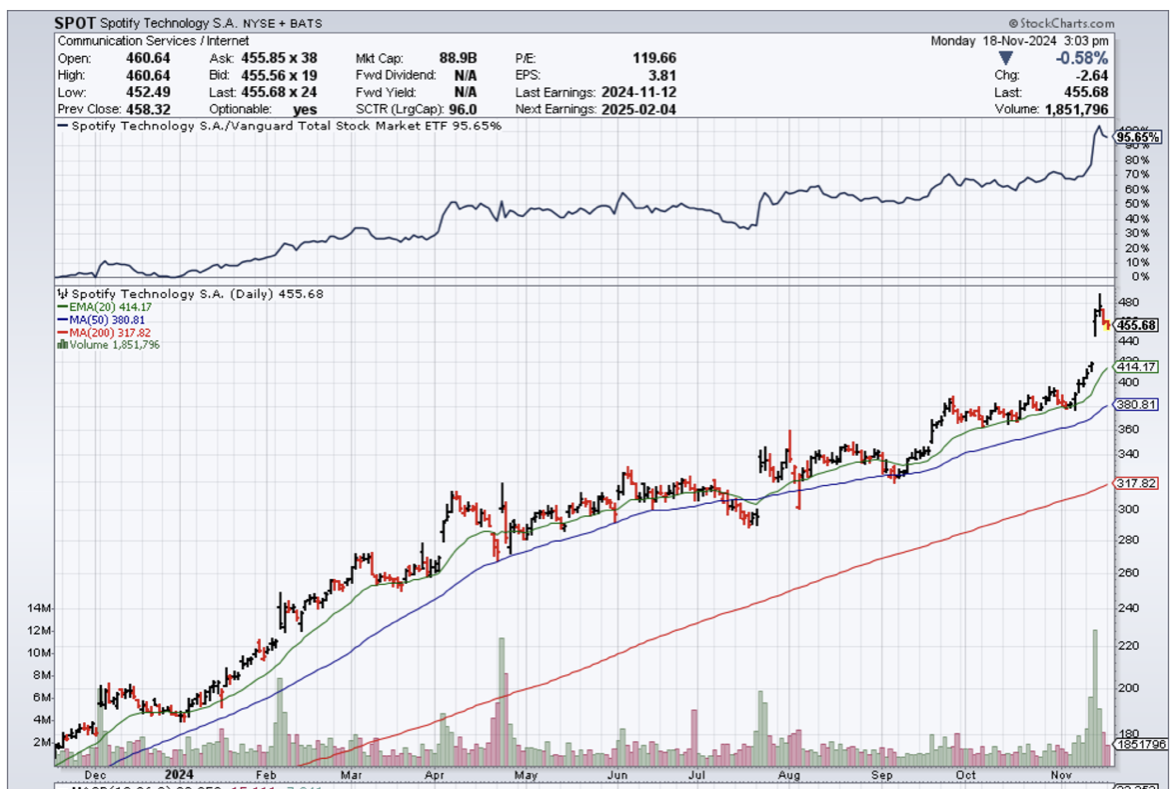

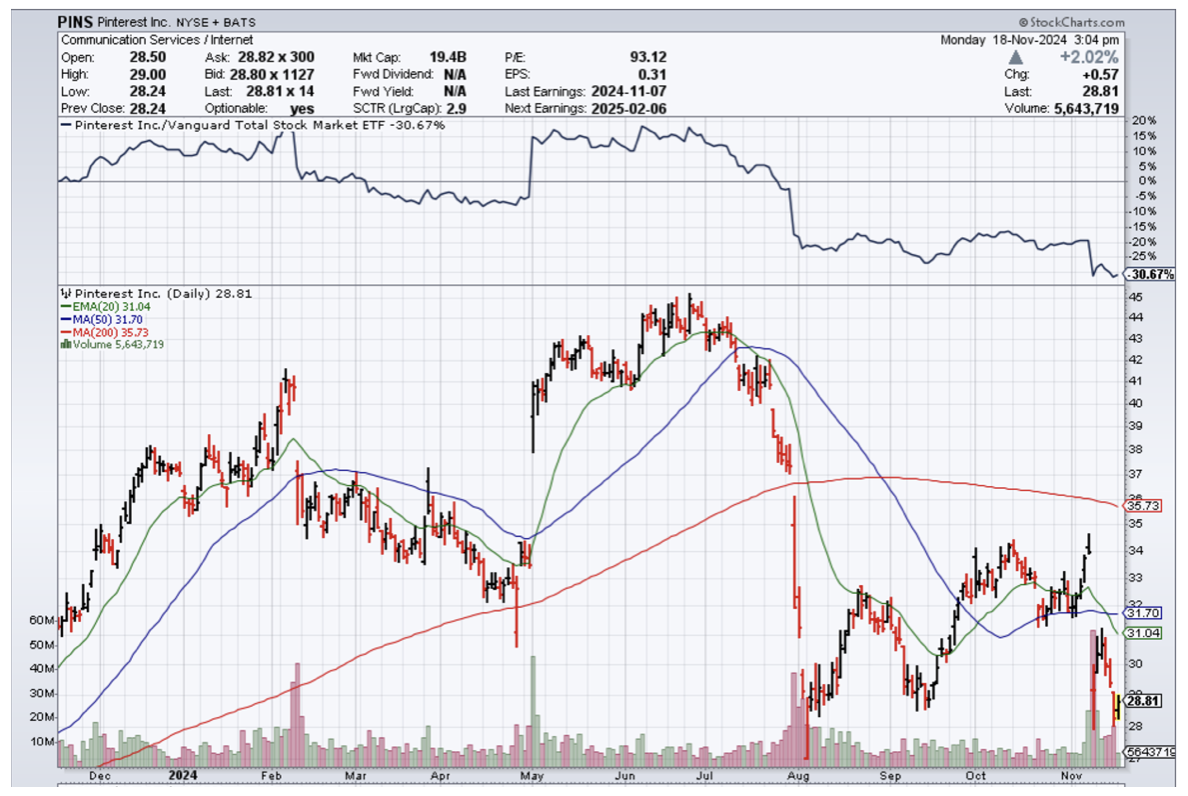

However, I would suggest readers take a look at Pinterest (PINS) and Spotify (SPOT).

PINS is still growing almost 20% per year, and I do believe the stock has an upside with the recent involvement of venture capitalists.

SPOT is in the podcast industry and has a locked-in quasi-monopoly in this sub-sector.

Podcasts and their popularity have exploded in the past few years, highlighted by SPOT signing podcaster Joe Rogan to a monster $100 million contract.

Legacy media has also followed up the election with terrible audience numbers, suggesting that the existing viewer base has decided to move on or temporarily pause participation.

META, PINS, and SPOT should be serious buy-the-dips candidates moving forward as the pivot to alternative media goes from a drip to a waterfall. As I am rereading this newsletter, the AP just fired 8% of its staff, citing “fast- changing conditions in the media industry.”

Mad Hedge Technology Letter

July 31, 2024

Fiat Lux

Featured Trade:

(CONSOLIDATION TIME)

(MSFT), (PINS), (NVDA)

The Nasdaq experiencing a big dip is in fact healthy for the tech sector long term.

Shaking out the weak hands is necessary a few times per year.

It doesn’t hurt that tech stocks boast the higher growth rates in the entire stock market.

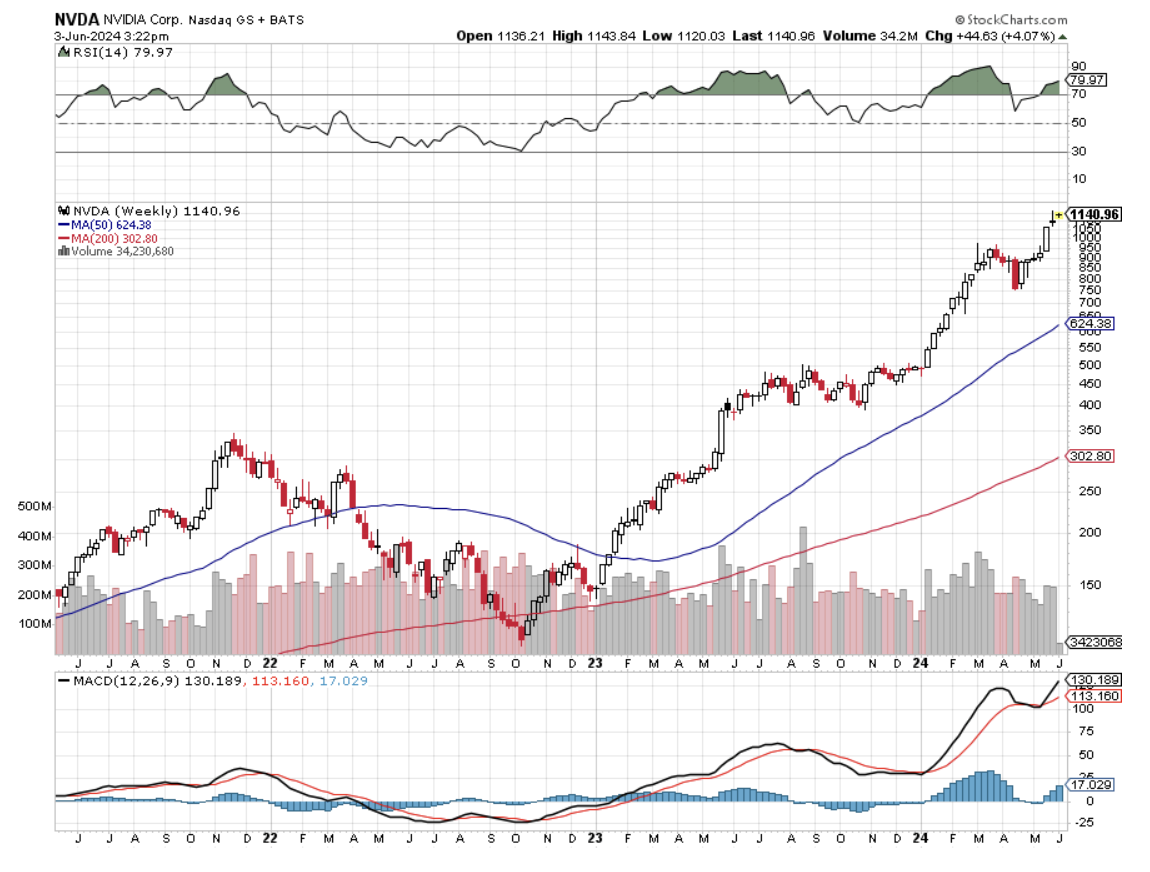

The price action has suggested a winner-take-all mentality with winners like Nvidia and other big tech companies experiencing outsized gains.

Chip stocks have been recent victors while smaller software stocks have been pounded.

Just take a look at social media stock Pinterest (PINS) which is down over 12% on a weak forecast.

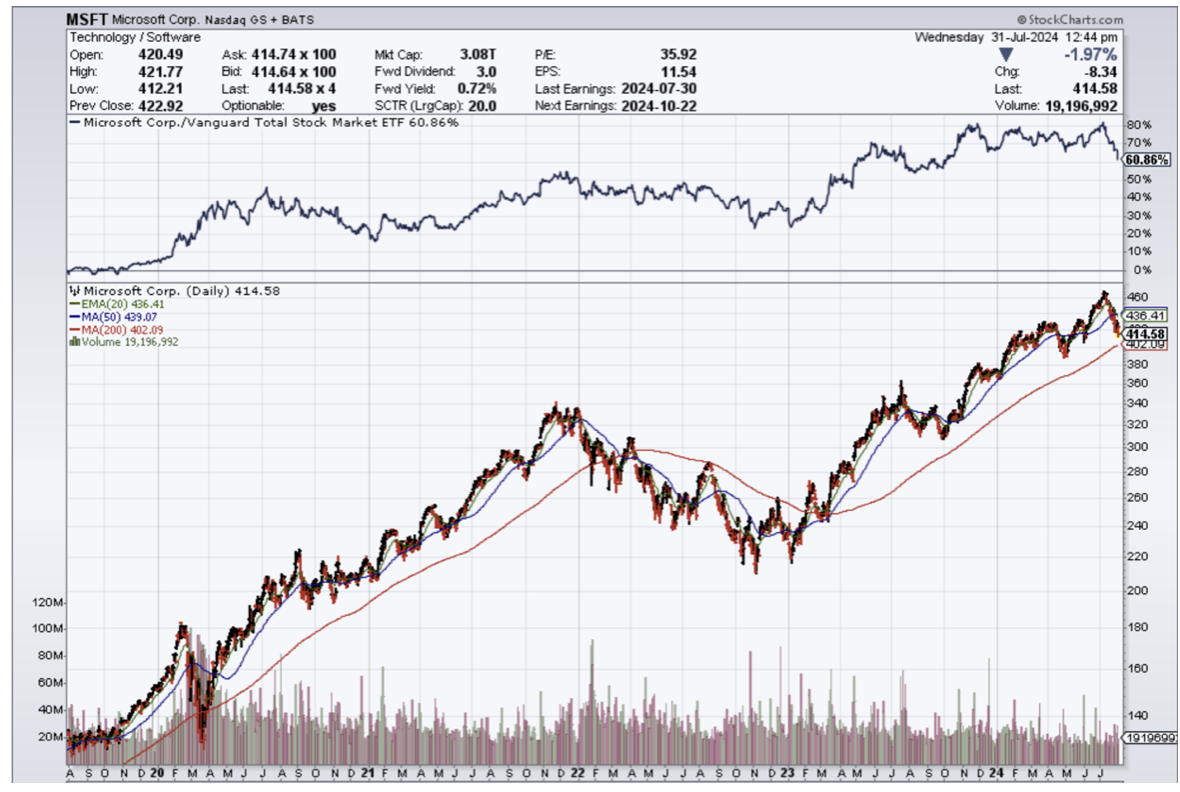

At the top end, Microsoft (MSFT) is the perennial flag bearer of cloud growth but this time it was different.

The stock sold off hard after earnings because the company missed cloud revenue expectations.

Cloud has been MSFTs bread and butter for years.

Even the CEO Satya Nadella came from the cloud division to grab the title of CEO.

Microsoft's overall cloud revenue came in at $36.8 billion, in line with expectations of $36.8 billion, but the company's Intelligent Cloud revenue, which includes its Azure services, fell short, coming in at $28.5 billion versus expectations of $28.7 billion.

While Microsoft's cloud business missed expectations, overall revenue still rose 21% year over year. Intelligent Cloud revenue, meanwhile, increased 19% year over year. What's more, Microsoft said AI services contributed 8 percentage points of growth to its Azure and other cloud services revenue, which increased by 29%.

The most consistent theme in this round of checks was the number of customers and partners that cited share gains by Microsoft resulting from its early lead on the AI front.

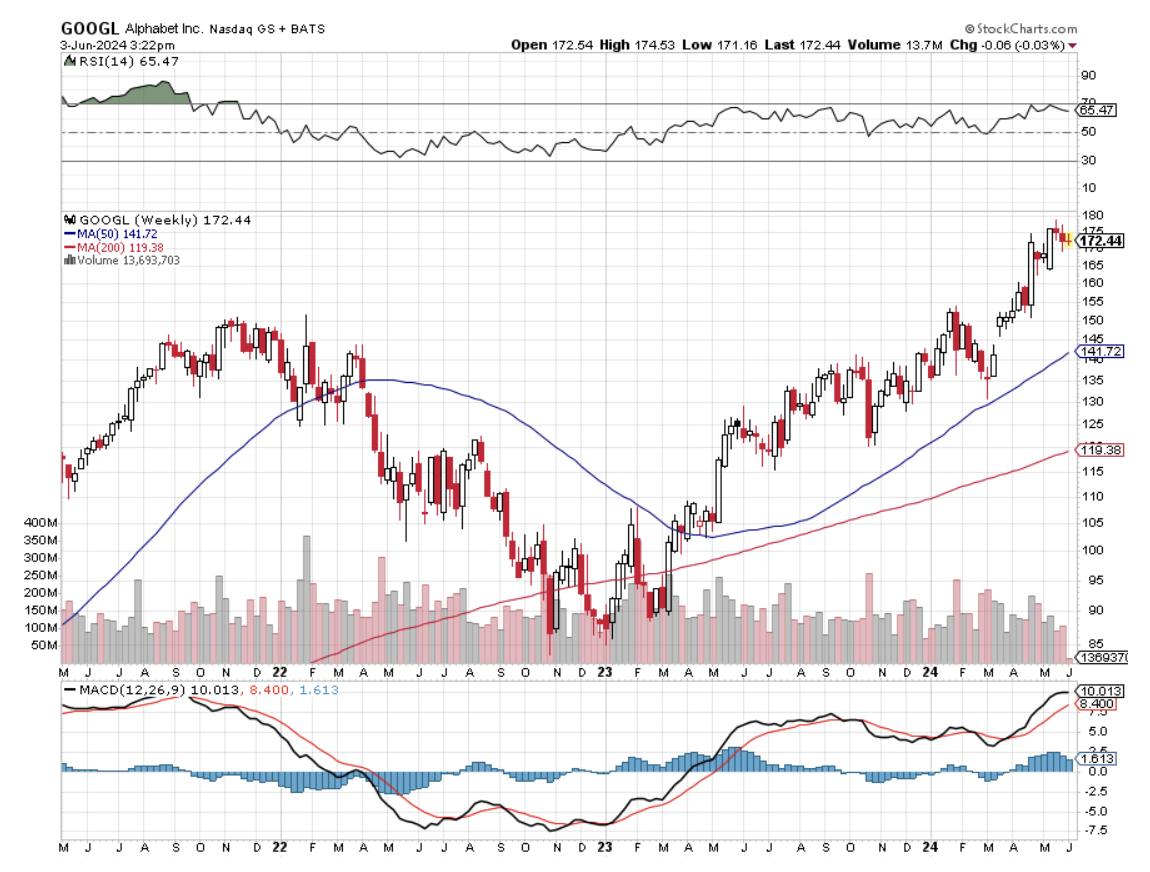

During Alphabet’s earnings call, CFO Ruth Porat said the company spent $13 billion on capital expenditures, up from $12 billion in the prior quarter, adding that the vast majority of that spending is going toward AI.

There are data points showing that growing the cloud is becoming something more similar to stealing rival clients from Google or Amazon.

That is a worrying sign because total addressable cloud revenue has been going up for a whole generation.

The cloud industry has never seen a scarcity mentality.

In the earnings rhetoric, the management talked as if growth is harder to come by in 2024.

I would be hard-pressed to find anyone who disagrees with that opinion.

The overall consensus starting to form is that these growing expenses related to AI won’t produce the blockbuster revenue projected so quickly.

The more likely case is that revenue from AI comes online in late 2025 or 2026 or maybe not at all.

The delay in the benefits of AI will mean shareholders pulling back temporarily and offer AI stocks a “prove it” period to show if they are legit or not.

Before winter, I do expect a consolidation phase in tech and in AI stocks that will set the stage for a Santa Claus rally.

MSFT stock is up over 200% in the past 5 years, and although this 11% or so dip in the past month is very unlike MSFT, this is a healthy and orderly dip.

I am still bullish MSFT in the long term.

Global Market Comments

June 4, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(THE BIGGEST “TELL” IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT)

I am constantly looking for “tells” in the market, little nuggets of information that no one else notices, but give me a huge trading advantage.

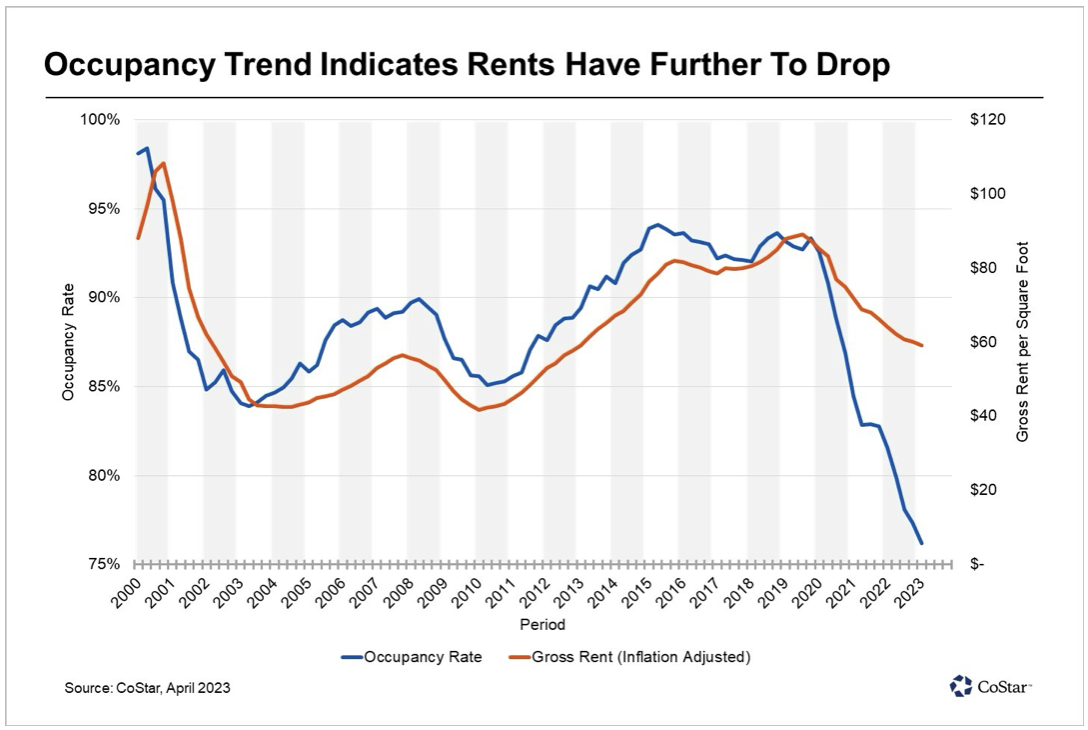

Well, there is a big one out there right now. The bottom feeders are pouring into San Francisco commercial real estate, taking advantage of valuations that sometimes reach negative numbers. Owners are walking away from buildings, mailing in the keys, and going into default rather than keeping up mortgage payments. What’s worse is refinancing at today’s lofty rates. That’s what you would expect with a 36% vacancy rate.

The message for you traders is loud and clear. You should be picking up the highest quality technology growth stocks on every substantial dip, such as Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and NVIDIA (NVDA). For they all know some things that you don’t. Their businesses are about to triple, if not quadruple over the coming decade thanks to AI. For every abandoned building out there are 200 new AI start-ups taking advantage of today’s bargain basement rates, and ALL of them use the services of the five companies above.

Technology stocks, which now account for an eye-popping 30% of stock market capitalization, will make up more than half of the market within ten years, much of that through stock price appreciation. And they are all racing to lock up the office space with which to do that….now.

San Francisco office rents reached a record pre-pandemic as the continued growth of tech — now turbocharged by nearly $100 billion in new capital raised in a series of initial public offerings — met a severe space crunch.

Asking rents rose to a staggering $84.16 per square foot annually for the newest and highest quality offices in the central business district, and citywide asking rents for such spaces, known as Class A, were up over 9% from the prior year. The citywide office vacancy rate was 5.5% in June, down from 7.4% a year ago.

In addition, local Bay Area home prices could get a turbocharger by the fall, when interest rates are expected to start falling.

San Francisco companies that have gone public continue to grow by leaps and bounds. Pinterest (PINS), Slack (WORK), and Uber (UBER) also signed office leases this year, with room for thousands of new employees.

Tech companies Autodesk (ADSK) and Glassdoor also signed deals at 50 Beale St. in the spring. In a sign of the city’s rapidly changing economy, old-line construction firm Bechtel and Blue Shield, the legacy health insurer, are both moving out of 50 Beale St. Sensor maker Samsara, software firm Workday (WDAY), and Sony’s (SNE) PlayStation video game division also expanded.

Globally, San Francisco has the seventh-highest rents in prime buildings. It’s still behind financial powerhouses Hong Kong, London, New York, Beijing, Tokyo, and New Delhi (San Francisco’s average office rents beat out New York.)

Only a handful of new office projects are being built, and future supply is further constrained by San Francisco’s Proposition M, which limits the amount of office space that can be approved each year. That is creating a steadily worsening structural shortage. Only two large office projects are under construction without tenant commitments.

Suddenly, it’s Not Crowded in San Francisco

Mad Hedge Technology Letter

December 11, 2023

Fiat Lux

Featured Trade:

(DIGITAL MARKETING REBOUND)

(PINS), (SNAP)

In prior years, big social media companies were the class of the tech industry.

It’s not so much like that today but they still have highly profitable models and a lot of juice left in the tank.

I do believe big social media companies will still do well in 2024 because they have proved themselves through the test of time.

However, now that media has fragmented, smaller social media stocks that are tailored to a certain niche are due to overperform in 2024.

This is happening at a time when cord-cutting is accelerating and the lowering of interest rates next year could serve as a catalyst to higher share prices for the likes of Snap and Pinterest.

Then there is the wider trend of potential beneficiaries from a recovery in the digital advertising market.

As marketing clients look to redeploy their dollars following post-pandemic cutbacks, stocks such as Snap and Pinterest could be next in line for a payday.

For Pinterest, I have been highly bullish on them ever since Elliot Management scooped them up and revamped management.

Snap is in the sweet spot catering to a growing demographic who are seeing their earning power rise as they come of age.

Still, the industry faces risks given an uncertain economic backdrop.

I anticipate higher ad sales of online retail platforms that will jump 20% versus last year. Moreover, online ad growth should accelerate meaningfully in 2024.

I believe the media will obtain about $17 billion in political ads next year when many U.S. campaigns will be in full swing.

It’s hard not to see social media stocks winning out in a presidential election year in one of the most polarizing contests in recent memory.

More and more consumers spend most of their days online and most of those funds likely will be spent on digital platforms where these consumers station eyeballs.

And worldwide, ad spending is expected to jump 8.2% next year, a sharp acceleration from the 4.4% gain anticipated this year.

Marketers spend money on platforms in direct proportion to the number of users that they attract.

Digital platforms, which include search, social, commerce, retail media, and digital video platforms, will account for about 64% of all advertising in 2023.

Digital platform-focused companies are expected to collectively grow 11%, led in large part by retail media, which will account for about $42 billion in advertising revenue in 2023, up 20% over 2022.

Traditional television, both national and local, will experience declines over the year.

The setup is boding nicely for these smaller social media stocks and that is not to say stocks like Meta and Google will perform poorly.

Realistically, the Nasdaq can’t move higher without the Magnificent 7, but based on pure percentage gains, I do believe Snap and Pinterest have a good chance to beat out the heavyweights next year.

There is a high likelihood that tech will lead this next bull market because they are the largest winner from the lowering of interest rates.

Not only will tech IPOs be back in vogue, but the prototypical tech zombie firms that burn cash will pop up again showing that investors reserve large amounts of capital for potential tech growth companies.

Part of the capital allocation will be to Snap and Pins which are solid companies with a great brand image.

I believe 2024 will be a year where investors pile into these 2 stocks much like how investors piled into Uber in 2023.

Mad Hedge Technology Letter

January 19, 2022

Fiat Lux

Featured Trade:

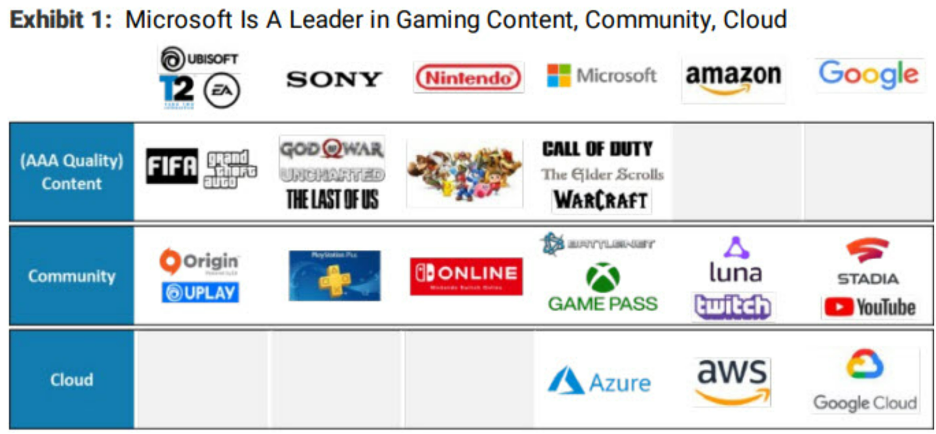

(MICROSOFT TAKES A GIANT LEAP FORWARD)

(MSFT), (ATVI), (PINS), (GOOGL), (AAPL), (AMZN)

CEO of Microsoft (MSFT), Satya Nadella, and his management team have made an aggressive step towards making inroads to the metaverse.

Gaming will be the launching pad to the metaverse that will first start as digital communities and later evolve into interoperable and integrated digital worlds.

The rest of the metaverse will germinate via these gaming communities and Microsoft knows that which is why they purchased Activision (ATVI) in cash for $68 billion and change.

The price was 3X higher than what they paid for LinkedIn but equally as strategic as many tech behemoths look forward to the next “big thing.”

The deal will mean MSFT will be one of the biggest gaming companies in the world just nudging out China’s Tencent and Japan’s Sony.

In the U.S., they will be by far the biggest gaming company and Nadella has made it a point of emphasis to navigate the gaming world by tapping M&A.

Remember, it was Nadella who built the MSFT cloud from scratch and Microsoft possessing its own stand-alone cloud asset dovetails nicely with their deep dive into gaming.

There are intrinsic synergies resulting from owning both.

The lack of native cloud infrastructure was a critical reason why ATVI gave up, as Chief Executive Officer Bobby Kotick said in an interview, “You look at companies like Facebook and Google and Amazon and Apple, and especially companies like Tencent — they're enormous and we realized that we needed a partner in order to be able to realize the dreams and aspirations we have,” he said.

This was the best Kotick could have wished for and I’ve mentioned this overarching trend of the best Silicon Valley companies getting stronger and now it’s even more pronounced as we are on the verge of exiting this pandemic this year.

In a higher interest rate environment, cash hoarders like Microsoft, Apple (AAPL), and Amazon (AMZN) simply have more ammunition than these smaller outfits who get penalized because of a harder route to access cheap capital making future cash flows costlier.

Now many of these smaller companies are realizing that they need to stand on their own two feet and that’s a scary thought for many CEOs who have been accustomed to tapping the capital markets to paper over the cracks.

What’s good about ATVI?

Activision owns mobile-gaming studio King, maker of Candy Crush, one of the most popular mobile games of all time.

Microsoft has almost zero presence in mobile gaming.

Nadella wants his gaming empire to facilitate direct payment like Apple’s App Store.

That’s effectively the holy grail of today’s gaming.

Microsoft has been at war with Apple and Google, over the fees the app stores charge for games.

It’s no surprise that Microsoft wants complete control over its ability to distribute games and content.

The deal also allows Microsoft an access point to secure an influential pool of gamers creating their own gaming content and worlds.

After adding Minecraft, LinkedIn, and GitHub, Nadella has been on the hunt for a game-changing asset that will drive the bottom line of MSFT via a large community of creators.

He failed to land social video service TikTok, while negotiations with Pinterest (PINS) and Discord were rebuffed.

ATVI is really a feather in the cap for Nadella, who won’t stop there and knows it’s just one battle of a greater war for tech supremacy.

These high-quality assets don’t get cheaper over time either.

Simply put, Microsoft loves subscription businesses, and gaming is among the best of them, and they are the stickiest around with recurring revenue that makes predicting future cash flows that much easier.

The ATVI pickup will raise the price of buying gaming assets across the board as I foresee a rush into these types of assets where not only can a company purchase the content, licenses, and gaming platform, but they can also add top-notch gaming developers which are equally as important as Microsoft tries to outmuscle Apple and Google.

This move is highly bullish for MSFT, so much so, that anti-trust regulators might cast a suspicious eye on this deal.