Mad Hedge Technology Letter

August 16, 2021

Fiat Lux

Featured Trade:

(HOW TO BE A TECH ANGEL INVESTOR)

(FB), (PINS), (LYFT), (TWTR), (BTC)

Mad Hedge Technology Letter

August 16, 2021

Fiat Lux

Featured Trade:

(HOW TO BE A TECH ANGEL INVESTOR)

(FB), (PINS), (LYFT), (TWTR), (BTC)

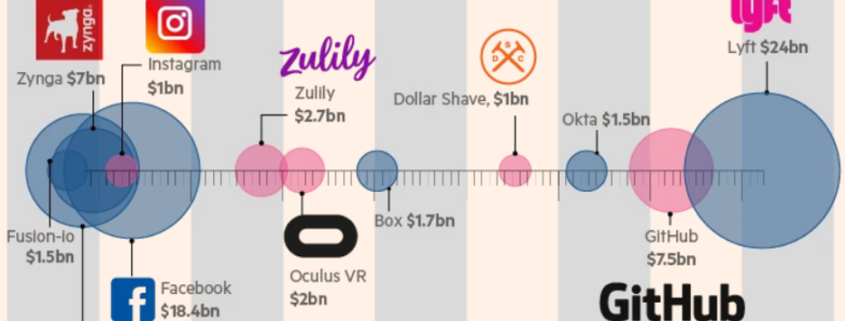

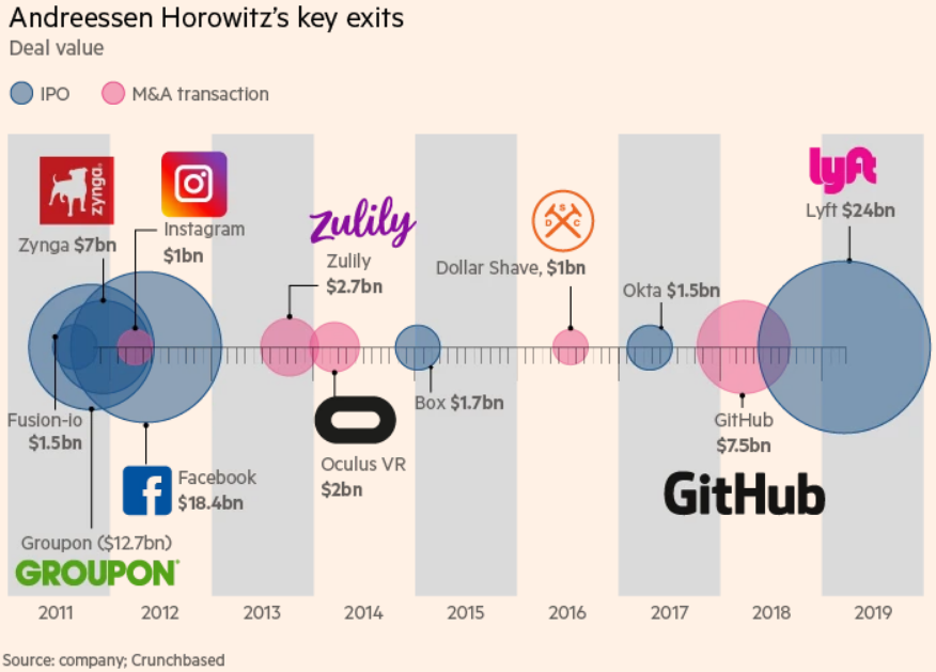

It’s not easy to be the genius who doled out early seed money to Facebook (FB), Foursquare, GitHub, Pinterest (PINS), Lyft (LYFT) and Twitter (TWTR), among others.

These investments turned out to be highly successful. If someone even miraculously hit on one of these, your grandchildren would know about it.

This person even acquired a majority stake in Skype for $2.75 billion which was considered highly risky at the time and offloaded it to Microsoft in 2011 for $8.5 billion.

Not everyone can do this like Silicon Valley tech investment maestro Marc Andreessen.

Behind the public markets is angel investing and the data says that these investments fail over 50% of the time for the best of breed like Andreesen.

There are simply too many variables that can derail these profit models which nobody can predict.

To lose over half the time and claim to be an outsized winner means relying on those 10 or 100-baggers or might I even say 1,000-baggers to drag up the portfolio performance.

These are the guys who were buying bitcoin (BTC) at 10 cents on the dollar.

Truthfully, investing in startup companies is not for everyone considering there is over a 50% chance a company will end at a 0 or pennies on the dollar.

However, it can be highly gratifying if and when the investments do pay off and investors get a front seat to the forefront of the tech innovation cycle, which you simply don’t get by trading Facebook and Google from your Fidelity account on your computer screen.

These investors can also get direct access to the chatter while creating a rich network of tech know-how; and I do believe that’s half the value in it too, since it can propel angel investors to the next super app or guy behind the next super app.

I mean who could have ever predicted a global health crisis that’s going into its 3rd year soon? And who will be able to nail the knock-on effects of climate change.

That is why risking losing one’s shirt is a real possibility if they bet the ranch on an unknown entity.

Everybody wants the next Tom Brady to quarterback their team, but who knows who the next Tom Brady is at 18 years old?

Even though Andreessen hits on less than 50% of his ideas, the industry median is around 17%, showing how superior his performance is.

He definitely has this thing figured out on relative terms.

Let’s define Angel Investor.

An angel investor is a high-net-worth individual who provides financial backing for small startups or entrepreneurs, typically in exchange for ownership equity in the company.

The funds that angel investors offer could be one-off investments to help the business get off the ground or in drip injection form to support and carry the company through its difficult early stages, which means burning cash.

Most of these companies don’t make money for the first 10-years and that time is usually a referendum on the quality of the idea; very few stand the test of time.

The potential to make 100-baggers is out there with subsectors like fintech already worth half a trillion dollars in 2020 and with a predicted annual growth rate of 35%.

Angel investors typically require a 35-40% return on the money they invest in a company minus costs and inflation to call it a winner.

But Venture Capitalists may take even more, especially if the product is still in development. For example, an investor may want 50% of the business to compensate for the high risk it is taking by investing in a startup.

Angel investors do the jobs of banks.

Traditional banks would never lend to an entity based on a half-built product or even a genius idea.

Proof of income and debt to income ratios are realities at banks.

When net profits are negative, the balance sheet is too ugly for banks to even think about doing any business with these startups.

Therefore, there are limited pathways for entrepreneurs to find capital, and many turn to Angel investors to help startups take their first steps.

Who Can Be an Angel Investor?

Angel investors are normally individuals who have gained "accredited investor" status, but this isn’t a prerequisite. The Securities and Exchange Commission (SEC) defines an "accredited investor" as one with a net worth of $1M in assets.

Essentially these individuals both have the finances and chutzpah to provide funding for startups. This is welcomed by cash-hungry startups who find angel investors to be far more appealing than other, more predatory, forms of funding.

These private funds usually draw up opportunities for a defined exit strategy, acquisitions or initial public offerings (IPOs).

Liquidity events is what makes everyone happy at the end except for the investors who missed the boat.

It’s even possible that an angel investor only sees growth in the first 5 years and unloads the “idea” to another private investor for a profit.

Private market deals are common because of the excess of liquidity brought on by the U.S. Central Bank lowering interest rates for a prolonged amount of time.

What I do know is that America is the framework within which almost all unicorns prosper, and I do not envision any monumental shift to Europe or China, these other places simply have more problems than the U.S.

How does the normal Joe get it on the action?

Andreesen has said the only way he usually does business is with a “warm” introduction which can be hard to come by if one doesn’t rotate in the same social circles as these heavy hitters.

Scoring a warm introduction also means getting boots on the ground in California which is ebbing and flowing between its colossal wildfires and public health issues like many other places.

Honestly speaking, if might be difficult to get the best of the best angel opportunities even if the gunpowder is loaded.

It’s accurate to believe that probably guys like Andreesen get the best of the best ideas in front of them and if they pass on it, the likes of Sequoia, Benchmark, and Softbank have very smart people as well who get similar type of presentations and opportunities.

Like you correctly guessed, this private group of capital is quite incestuous and tight-knit. It’s a copycat league of the ages.

The one avenue that might be of interest is a platform that has democratized angel investing who on the last count had close to 1,000 companies looking for start-up capital.

This platform is called https://angel.co/angel-investing and some are even actively hiring on the same platform.

I won’t stand here saying this is the cream of the crop because it’s not, but I will say that sometimes companies are overlooked, or the industry consensus has shifted too far in one direction offering undiscovered dark horses a chance.

Lastly, this forum of angel companies on offer does give analysts insight into where money is funneled to and the current hot sub-sector of the tech industry.

This platform even offers an Angel index fund if a reader wants to take the aggregate performance of 150-200 companies with a $50,000 minimum.

If a reader wants access to facilitate angel investing by a deal-by-deal offer from the Angel list as a professional investor, then $500,000 is required.

Mad Hedge Technology Letter

March 15, 2021

Fiat Lux

Featured Trade:

(2020 MADE THIS TECH COMPANY)

(PINS)

Do you want to invest in a tech company that added 100 million new accounts in 2020?

Well, you’ve meandered down the right alley and I will show you the way.

Clearly, in the year 2020, the pandemic obviously threw a massive wrench in everything and for a second, I too held my breath for tech companies.

But it luckily shook out the right way for us, as I understand it, tech firms throughout the mayhem evolved to drive incremental use cases for the users and that was what won out.

Pinterest (PINS), a U.S. media sharing and social media service designed to enable saving and discovery of information on the internet, was an unheralded beneficiary of this outsized pivot to lockdown and quarantines.

In fact, it was only just before the public health crisis that I believed this firm was languishing big time, unable to outperform against the big boys, but good enough to be faintly relevant.

Well, they became comparably relevant on a global scale from March 2020, and they have taken their path of opportunity and ran down it.

So how successful are we talking about?

Pinterest grew total revenue 76% year over year in 2020 with adjusted EBITDA margins of 42%.

That’s homerun stuff right there after only being able to expand in the high teens pre-virus environment.

The huge gap up in performance is also here to stay with upper management envisioning the next quarter as growth of “low 70s percent range year over year in the first quarter.”

Not too shabby, right?

Certainly, it’s an understatement to say that 2020 was the ultimate acid test to whether a public tech company could stand on its two feet or not.

No doubt they were aided by a giant sea swell of stimulus money which they are more than happy not to apologize for.

So, what’s the game plan now for the Pinterest crew?

The public health crisis uncorked the pathway to international revenue after focusing on “mature” markets for the first part of its history.

In 2020, international business grew 145% year over year on the back of strong advertising demand. International markets now represent 17% of total revenue.

The company rolled out a function able to take advantage of the “insight” into selling to consumers.

Sales and marketing teams built an insights-led go-to-market program over the course of 2020 that helped Pinterest deliver against Q4 seasonal comps.

This development helps make Pinterest more attractive to advertisers because they can understand their verticals better.

Let’s run down a few examples to show the use cases.

The LEGO Company created a holiday campaign based on popular search terms on Pinterest, seeing increasing search trends for creative kids’ gifts allowed the LEGO company to optimize and serve ads at the right moment ahead of the holiday season.

Another example is the luxury coffee company, Nespresso. They partnered with Pinterest teams to unearth key consumer trends around the holiday season, including search trends and consumer habits around holiday gifting, coffee recipes, and seasonal flavors.

With a better understanding of both auction dynamics and Pinner behavior, Nespresso delivered effective advertising campaigns that also showed positive results in a third-party brand study.

As 2021 does feel like another shelter-at-home year, I would warn investors to keep their powder dry for this one because the comparisons for mid-end 2021 will be tough to beat.

I do believe after a period of consolidation; Pinterest’s stock price will be back in full-out bullish mode.

There is just too much runway out there if you consider, these are the early innings of Pinterest transforming from an image company to a video-centric company.

There has been a significant uptick in video views and uploads. And PINS is beginning to expand that by enabling users to publish directly onto the platform.

This change will drive digital experiences for users, both in the U.S. and internationally, with some of the less mature web content ecosystems the U.S. relied upon.

That's a significant focus and makes the product more useful.

And they certainly did make the platform more useful in 2020 with enormous surge in product search that went up about 20 times last year alone.

PINS is also at the stage of supporting a diversified advertiser base and is really focused on making it easier for mid-market advertisers to manage SMBs to scale their spend.

But as they fine-tune automation, these SMB and mid-tier contracts will turn into Fortune 500 contracts like many of the larger tech sharks out there.

On the risk side, privacy issues could disrupt their rise as privacy measurements are diminished which could lessen their attractiveness to ad buyers.

This company is still a pure ad seller company where the user is the product ala Facebook.

Also, there is the risk that lockdown and quarantine measures are dismissed, and the world opens up which could damage the incremental use case for PINS that was so strong during lockdowns.

It’s hard to view that new sneaker in the shop window when the shops are closed, and I predict a 10% correction if investors feel the world is about to open up unfettered.

However, the long-term runway is healthy for PINS and I do expect a slow grind up as the company switches to predominate video and ad companies pile money into their platform because of the “brand safety” of PINS in a world where the internet is increasingly becoming a murkier place to deploy capital blindly.

2020 MADE PINS RELEVANT

Mad Hedge Technology Letter

November 4, 2019

Fiat Lux

Featured Trade:

(THE CHICKENS COME HOME TO ROOST WITH SMALL TECH),

(AAPL), (MSFT), (AMZN), (GOOGL), (WDC), (TXI), (ANET), (PINS)

The tech story is still intact, but the edges are losing its shine.

That is the takeaway from the recent slew of earnings reports from many of the prominent yet second-tier tech companies.

On one hand, companies like Apple (AAPL) have been holding the fort as it blasts through to new highs even amid the backdrop of the Chinese trade war that has dragged many of the strong tech names into the mud.

What we did see lately was a magnificent swan dive by chip names like Western Digital (WDC) and Texas Instruments (TXI) which were blindsided by 10-15% haircuts because of lackluster guidance.

The agony didn’t stop there with second rate cloud names like Pinterest (PINS) and Arista Networks, Inc. (ANET) reaching for scapegoats for their weak guidance. These took instant 20% haircuts.

The problem with smaller stocks like these besides having narrower spreads, they are slaves to just a few contracts and when one goes, their guidance and revenue estimates implode in their faces.

Arista slid more than 25% on news that they expect quarterly revenue of $540 million-$560 million, with the midpoint about 20% below the previous Street consensus at $686.2 million.

Arista CEO Jayshree Ullal said in a statement that the company expects “a sudden softening in Q4 with a specific cloud titan customer.”

That is Facebook who comprise about 10% of Arista’s revenue composition because Facebook has pulled back the reigns on cloud spend to cut costs amid a murky global backdrop and regulatory minefield.

Unfortunately, second tier cloud names must accept that they do not offer the best pricing when directly competing with the superior cloud names of Google Cloud, Microsoft Azure, and Amazon Web Services (AWS) because they simply can’t scale as well to the extent these monopolistic FANGs can.

Data storage often comes down to whoever has the cheapest cost of capital to pile into server farms allowing pricing to be ultra-cheap and these three companies win out.

If these firms lose one contract like Walmart’s switch over to Microsoft Azure from Amazon, it’s not a big deal.

It doesn’t put a 10% black hole in the revenue stream like for Arista.

Pinterest was one of the most overhyped IPOs of 2019 promising growth, growth and more growth.

Its digital ad business needs to deliver accelerating growth for its share price to rise and when the latest earnings report showed year-over-year growth slow from 62% to 47%, investors saw the writing on the wall.

The company only grew its users 8% in the lucrative North American market and 38% abroad.

But the foreign markets were tainted by the gruesome underbelly of earning only 13 cents per foreign users.

There is user growth but at the cost of an inferior quality of growth.

Analysts can clearly observe the accelerated erosion of Pinterest, and I can say from a personal point of view that the website isn’t that useful.

Management’s excuse was a tough comparison to the prior year but if a growth firm has a superior model, they should be able to grow past any minor problems if the secular trends stay hemmed in.

Weak excuses now and probably weak excuses next quarter as the global tech landscape gets squeezed even more at the periphery.

What does this all mean?

There has been a flight to tech quality into the Teflon names like Microsoft and Apple.

Names that are showing growth headaches saddled with too much competition and structural softness are getting killed.

Don’t even think about investing in the marginal names like Pinterest and Arista.

Better to be safe on your perch inside the moat than outside isolated from the drawbridge.

Not all tech is created equal and it's rearing its ugly face in a frothy market.

Global Market Comments

July 16, 2019

Fiat Lux

Featured Trade:

(THE BIGGEST TELL IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT),

(POPULATION BOMB ECHOES),

(CORN), (WEAT), (SOYB), (DBA), (MOS)

Mad Hedge Technology Letter

April 15, 2019

Fiat Lux

Featured Trade:

(XXXXX)

(SNAP), (FB), (PINS), (TWTR), (GOOGL)

America is full – that is what domestic social media growth is telling us.

The once mesmerizing service that captured the imagination of the American public has soured in the country that created it.

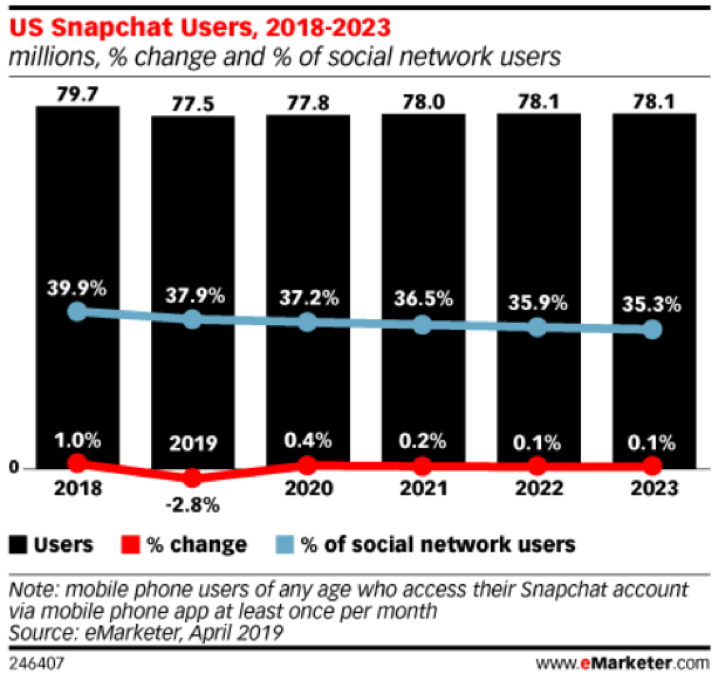

Online advertising consultant emarketer.com issued a report showing that Snapchat (SNAP), the worst of the top social media outlets, will lose users in 2019.

The 77.5 million users forecasted by the end of 2019 represents a 2.8% YOY decrease.

This report differs greatly from the report eMarketer issued just past August showing that Snapchat was preparing for a rise of 6.6% YOY in 2019.

The delta, rate of change, represents a massive downshift in expectations and the sentiment stems from the widespread saturation of social media assets.

Market penetration has run its course and the players have run out of bullets mainly targeting Generation Z.

These platforms have given up on baby boomers and Snap feels that pursuing the millennial demographic would be an exercise in futility.

Even more disheartening is that between 2020-2023, there will be only a minor uptick of user growth by 600,000 users clamping down on the impetus of a comeback of sorts shackling the business model.

The trend is not mutually exclusive to Snap, Twitter or Facebook, social media as a group will only expand the overall user base by 2.4% in 2020 hardly satisfying the appetite for growth that these companies publicly advertise.

Remember that much of Instagram’s growth originates from borrowing Snapchat users by way of copying their best features.

Even with this dirty tactic, growth seems to be petering out.

Snap’s shares have made a nice double after peaking shortly over $25 after the IPO.

But the double was a case of investors believing that management and execution had hit rock bottom – the proverbial dead cat bounce in full effect.

Now investors will pause to reassess whether there is another reasonable catalyst to drive the stock higher.

First, investors will need to ask themselves, is Snap in for another double?

Absolutely not.

So where does Snap go from here?

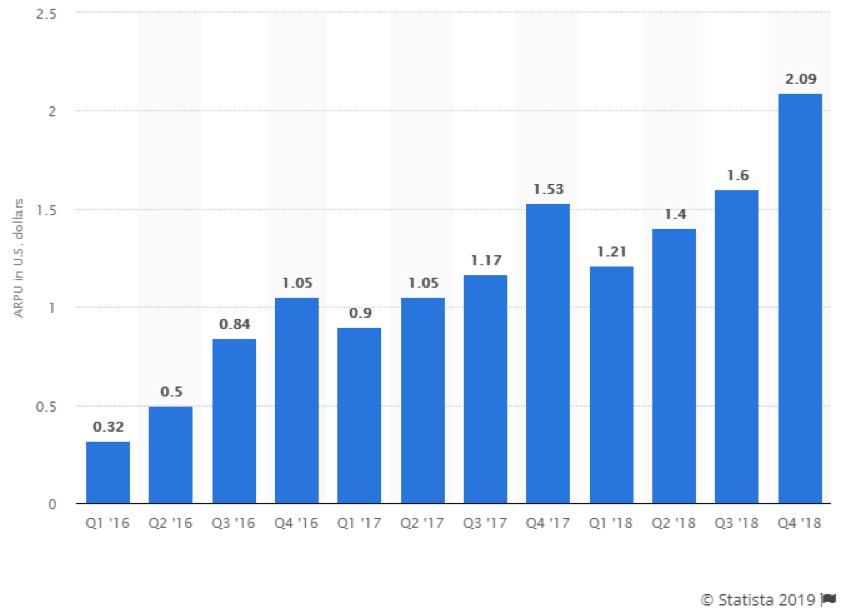

I believe they will borrow from the playbook of Mark Zuckerberg and attempt to emphasize supercharging average revenue per user (ARPU).

Whether the company arrives at this conclusion by chance or strategy, they must confront the reality that there are almost no other levers to pull if they want to perpetuate this growth story.

M&A is also off the table because the company is burning through cash.

Facebook’s (ARPU) came in at $7.37 last quarter indicating how Snap needs to make substantial headway in this metric with last quarter’s paltry (ARPU) at $2.09.

Essentially, management will conclude that each user isn’t absorbing enough ads because of declining user engagement.

Snap CEO Evan Spiegel will need to improve the pricing power charging advertisers at higher rates.

Obviously, the lack of an attractive platform resulting from poor execution and engineering problems needs a quick turnaround.

It’s not all smooth sailing for Facebook either, they keep chopping and reshaping strategy by the day attempting to minimize costs as the regulation burdens rot at the bottom line.

On the bright side, regulation hasn’t been as bad as initially thought – usership hasn’t dropped by orders of magnitudes.

In fact, Facebook’s users have shown a resurgent indifference to Facebook chopping up their data and repackaging it to 3rd parties, meaning Facebook has come through rather unscathed in the face of a PR storm.

There have even been recent reports of Zuckerberg being persuaded to start paying journalists for original content, a vast pivot for his hyped-up propaganda machine of being in the distribution business.

Juicing up (ARPU) is the lowest hanging fruit on offer for Snapchat and Facebook right now, overperforming in this sphere will improve financials and keep the mosquitoes away while affording them time to ponder how to reaccelerate user growth.

One outsized negative trend is that 90% of user growth appears to originate from undeveloped nations with a lack of discretionary spending power showing that this strategy has its limits.

Searching for another tool in its toolkit will redefine Snapchat, Twitter, and Facebook as we know it.

I would even classify it as an existential crisis.

Instagram have bought Facebook the most time to readjust its future direction highlighting that stealing Snapchat’s audience is still effective, expecting user growth to climb to 106.7 million US users, up 6.2% from 2018.

Instagram will continue its expansion by adding nearly 19 million new US users by 2023, but as much as it adds to its new social media asset, Facebook will be struggling for new net adds.

Snapchat is in dire straits and the stock market bubble could support the share price for up to another 8-12 months, but when the guillotine drops on Snapchat, the blood will smatter everywhere.

The company also plans to introduce a gaming service to take advantage of the popularity with its core users, Generation Z.

This should be the trick that breathes life into operating margins and (ARPU) which is why I believe the stock will hold up for the next period of time.

But with the gaming initiatives also comes rampant competition with the likes of Alphabet (GOOGL) and don’t forget Fortnite is still the 800-pound gorilla.

These trends also bode negatively for Pinterest (PINS) who might be going public as the last shot of tequila is downed at the after party.

Mad Hedge Technology Letter

March 26, 2019

Fiat Lux

Featured Trade:

(PINTEREST COMES OUT)

(PINS), (FB), (AAPL), (GOOGL), (AMZN)