Below please find subscribers’ Q&A for the September 8 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Do you think we’ll see the under $130 in the United States Treasury Bond Fund (TLT) before January 2022?

A: I don’t think so; I think we could go below $140, maybe below $135. But $130 would be a brand new low in the move and would be a stretch. We basically lost 4 months on this trade due to the countertrend rally, which just ended. I would come out of your (TLT) $130-$135 vertical bear put spreads right here while they still have time value, but keep the $135-$ 140s, the $140-$145’s, and especially the $150-$155’s. The idea was that you just keep averaging up and up until the market turns, and then you make back any loss. We move into accelerated time decay on those deep out of the money put spreads in December, so I would take the money and then offset it with the gains you made in those positions.

Q: Does Palantir (PLTR) look like it’ll hit $100 by year-end?

A: No, the stock has been dead, and management has not been doing anything to promote it. We did get a move up to $45 but it failed. It’s still a great long-term idea as they are growing at 50% a year. Also, they did buy $50 million worth of gold bars as a hedge. But as a short-term trader, Palantir isn’t working. If you have an options position on that I would probably get out of it or roll it forward to 2023.

Q: PayPal (PYPL) is fluctuating up and down with Bitcoin. Do you like PayPal?

A: Absolutely, but it obviously is being dragged down by Bitcoin. It is a temporary down move caused by a one-time-only event in El Salvador. Buy the dip in PayPal. It is a leader in the whole move into a digital financial system.

Q: When is Freeport McMoRan (FCX) likely to move up?

A: As soon as we shift out of the tech trade into the domestic recovery trade, which could be in weeks or months at the latest. We’ll switch from one side of the barbell to the other.

Q: Where do you see Tesla (TSLA)?

A: It keeps going up, so my guess is we top $800 by the end of the year, and maybe $850. The big news here is that Tesla has gone into the chip business, making its own chips in-house which is easy for them to do in Silicon Valley. But it does make them the first global car maker that is also a chip maker, and therefore the stock deserves a higher premium. The stock went up $30 on the news and is great for all Tesla holders. I hope you have the 2023 LEAPS.

Q: Too late to buy Tesla LEAPS?

A: Unless you’re really deep in the money, with something like a $600-$650; but the return on that will only be about 50% in 2 years.

Q: The Biden administration just set a goal of 45% solar by the end of 2050. Which solar stock should I buy here?

A: The problem with solar is as soon as Biden started winning primaries, every solar stock took off like a rocket, figuring he’d win, which he did. All of them went up 6-fold or more as a result of that, then gave up one-third of their gains and are now moving sideways. So if you look at the charts, the classic one to buy here is the Invesco Solar ETF (TAN), a basked of the top solar companies. All of these peaked in February and have been doing sideways “time” corrections since then, which means they eventually want to go higher. The other two that have charts that look like they’re finally starting to break out to the upside are First Solar (FSLR) and SunPower (SPWR) after 8 months of consolidation.

Q: Why is the second half of September almost always bad? Is it due to institutional repositioning?

A: Not really, the cash comes into the market at certain times of the year, like end of the year, beginning of the year, and end of each quarter. September seems like the month where they kind of just run out of money. But there's actually also a historical reason for that. For most of American history, we had an agricultural economy. Farmers were more than half the population, and the period of maximum distress for farmers is September, where they put all the money into seed and fertilizer and labor into the field, but they haven't harvested it yet. So, traditionally, they always did a lot of borrowing in September, which caused a cash squeeze and interest rate spike, and a stock market panic as a result. So that's the history behind weak Septembers and Octobers. Once the farmers get the crops in and sell them, that resolves the cash squeeze, interest rates fall, and it’s straight up for stocks for the rest of the year most of the time.

Q: SPACs (Special Purpose Acquisition Companies) seem to be losing interest. Do you recommend any or stay away?

A: Stay away—they’re all rip-offs and are simply a means by which managers can increase their fees from 2% to 20%. That's what they did with virtually all of them. This will end in tears.

Q: What's your feeling about satellite internet phone service replacing current internet cell service in the future?

A: It’s in the future, but it may be 10 years off in the future. If it happens sooner, it’s because Elon Musk was able to deliver cheap rocket service. He already has 20,000 satellites in the sky for his own Starlink global cell phone service for internet access.

Q: How does one buy a Bitcoin stock?

A: Well first of all, I highly recommend you buy the Mad Hedge Bitcoin Letter, which you can get in our store. But there's also the Greyscale Bitcoin Trust (GBTC) which allows you to buy a Bitcoin proxy very easily. I’ll even honor the discounted $995 price for my Bitcoin Letter for another day by clicking here.

Q: Is Warren Buffet and his value philosophy something I should be following, or is he outdated?

A: I have to say, buying stocks cheap with high cash flow will never go out of style. Currently, Warren’s big holdings are domestic industrials, banks, and Apple. All of those look like they will do well moving forward. Buffet’s Berkshire Hathaway (BRKB) has a built-in barbell element to it and is the subject of one of our LEAPS recommendations which has already been hugely successful.

Q: Is Home Depot (HD) at $330 a bargain?

A: Well, we just had a selloff and it bounced hard, and now we’re waiting for the domestic post delta recovery. It's hard to imagine both Home Depot and Lowes not doing well in this scenario.

Q: What will happen to tech when interest rates rise?

A: My bet is they go sideways to down small until you get another peak in interest rates (the next peak will be at 1.76% in the ten year US Treasury bond, the 2021 high) and once you hit that, then tech will take off like a rocket again, and in the meantime, you play the domestics while interest rates are rising. That is the game and will continue to be the game for a couple of years.

Q: Should I buy IBM (IBM) on a turnaround story?

A: No, I've been waiting for IBM to turn around for 10 years. They just don’t seem to get it. What they do is whenever a division starts to make money, they sell it and get cash like they did with the PC division and this year with its infrastructure business called Kyndryl. So, they’re not leaving any growth for the actual IBM holders.

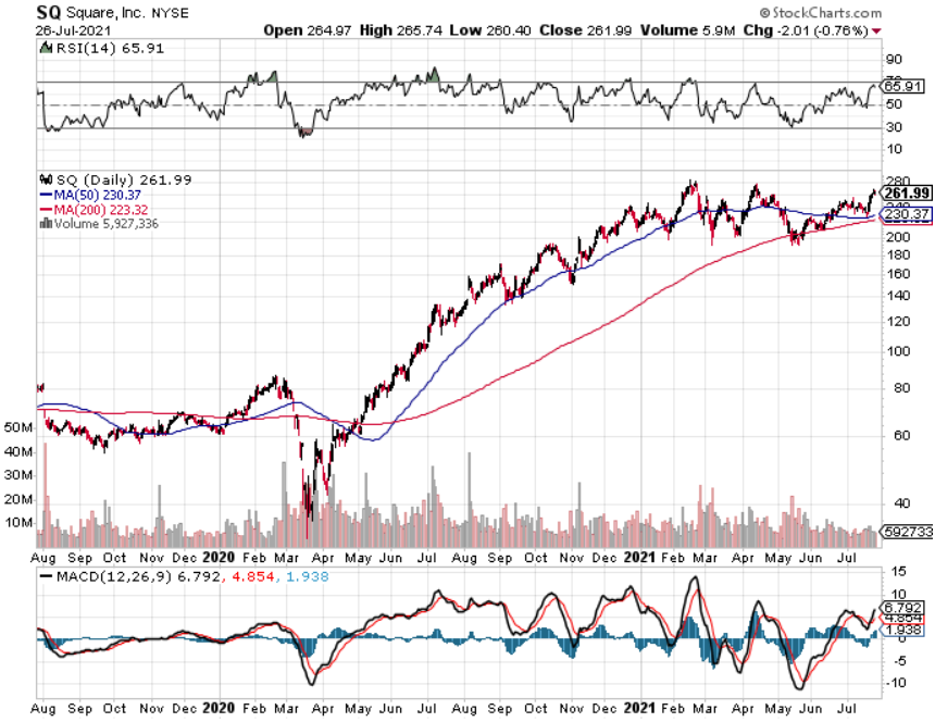

Q: Do you like Square (SQ) at $256?

A: Yes, and that would be a great 2023 LEAPS candidate. All of the digital settlement payment systems are going to do well in the Bitcoin future. They also own quite a lot of Bitcoin. They are leading the charge into a digitized financial system.

Q: What’s a good Ethereum ETF?

A: The Greyscale Ethereum Trust (ETHE) is just the ticket.

Q: So you avoid energy, meaning oil and gas?

A: Yes, alternative energy we like, but it’s had an enormous run already so after a 7-month time correction it’s probably safe to get into solar. Traditional oil and gas (USO) is in a long-term secular bear market that started 13 years ago and will eventually go to zero. Last year’s visit to negative futures prices is just a start. Since 2020, the energy market weighting has gone from 15% to 2%.

Q: Is Natural Gas the only rational core fuel for the grid?

A: No, natural gas (UNG) still produces carbon even though it’s only half the amount of oil. This all gets replaced by solar in the next ten years. That’s why I tell people to stay away from energy like the plague. Would you rather buy natural gas at $4.50/btu or get solar electricity for free? Those are basically going to be the choices in ten years.

Q: Who is the biggest Aluminum producer?

A: Alcoa (AA) which we are a buyer on dips. By the way, if we do have to build 200,000 miles of long-distance transmission lines to cover the electrification of the US energy supply, all of that has to be made of aluminum. You don't use copper for long distances, you use aluminum (aluminum for you Brits).

Q: Would you buy Uber (UBER) at $40 today?

A: Probably, yes; it had a nice 40% correction. However, you are buying into the battle over gig workers—whether they should be treated as full-time or part-time workers. That is going to be a continuing drag on the stock until they win.

Q: What do you think of meme stocks?

A: You're better off buying a lottery ticket. Even with a low payoff, you get a 1:10 chance of winning on a $1 lottery ticket. Meme stocks could double or go to zero with no warning whatsoever—there’s no logic to this market at all.

Q: What do you think of Uranium?

A: Three words come to mind: Chernobyl, Fukushima, and Three Mile Island. I think uranium's time has passed, even though China is building a hundred nuclear power plants. It’s just too expensive to compete against solar on a large scale and impossible to insure. If you still like Uranium though, the Uranium Royalty Corp. (UROY) has had a nice pop recently. But the issue is that nuclear technologies can’t keep up with solar and digital. And they blow up.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

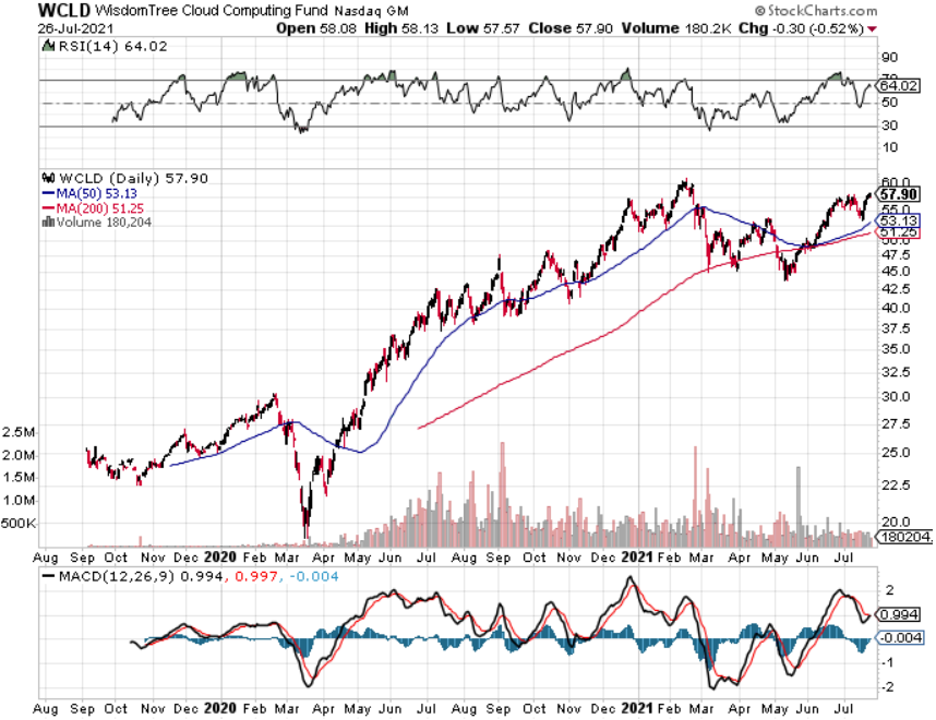

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, instead of scouring the grains of sand to find a diamond, I have a quick fix for you and your friends.

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate ten-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-25 15:02:202021-08-27 17:47:18The Best Way to Alpha Your Tech Portfolio

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance, and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many techportfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a techportfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-30 15:02:502021-08-03 01:47:18The Best Way to Streamline Your Portfolio

Robinhood (HOOD) is an American financial services company headquartered in Menlo Park, California, known for offering commission-free trades of stocks, exchange-traded, and cryptocurrencies via a mobile app introduced in March 2015.

After perusing their S-1, I can’t help but offer the same recommendation I gave readers for the Coinbase (COIN) listing, which proved to be spot on.

Although this is a real company with real revenues, the growth rates are particularly high because of a one-off phenomenon in alternative asset classes.

I would urge readers to not buy shares of HOOD directly after they are public but instead wait for an entry point sometime after the lock-up period expiration which usually coincides with the insiders and long-time employees unloading shares or a partial trove of them.

The same happened to Palantir (PLTR) which saw a meaningful sell-off upon the lock-up expiration and although PLTR shares are higher today than they were the day of lock-up expiration, it’s better to avoid that dip if you can. PLTR had a big dip when the lock-up expired presenting a great entry point into shares.

Lock-up periods are usually 180 days and I firmly believe this company that will be trading under the ticker symbol HOOD, is not worth paying a premium before that 180-day lock-up period is over.

Don’t be that sucker.

To dovetail with my thesis of not buying HOOD too early is the analysis of their inherent high stakes/ high rewards nature of the business.

Let’s not fudge the details, this is a high-risk business and as of now, they have been handsomely rewarded for it, but that might not always be the case.

They pioneered commission-free trading when the likes of Fidelity and Charles Schwab were still charging $15 to execute one side of a trade.

Why can they offer free trading?

Order history is paid for by third-party high-frequency traders, namely Citadel.

Citadel accounts for 27% of payments for Robinhood retail order flow, and Payment for order flow is 81% of total Robinhood revenue.

The thinking behind buying order flow is to then apply the data through machine learning to even front-run orders of normal retail traders and profit off the spread or micromovements in shares.

They even make markets with their liquidity and trade their own proprietary books.

And yes, this is legal in the United States and companies have gone gangbusters in high-frequency trading (HFT) like Virtu Financial founded by Vincent Viola who owns the NHL franchise Florida Panthers and is big into competing for his horses at the Kentucky Derby.

It obviously pays to do HFT, and if done properly, are great businesses and these are the companies propping up HOOD today.

Robinhood has taken advantage of the Millennial lust to go crypto or go home.

The numbers back me up — $11.6 billion of crypto under custody by the end of Q1.

Bitcoin was the HOOD’s most traded asset in 2020 and the first quarter of 2021 and 17% of total revenue came from crypto in Q1, (compared to 4% in Q420)

In the S-1, it said that HOOD’s business “may be adversely affected, and growth in our net revenue earned from cryptocurrency transactions may slow or decline, if the markets for Dogecoin deteriorate or if the price of Dogecoin declines.”

HOOD and its future success are now uniquely levered towards alternative coin Dogecoin which is now 34% of their total crypto revenue in Q1.

This is the altcoin that Elon Musk joked about, and it explains the 54% growth of 2020 revenue in the first 3 months of 2021.

This is an incredibly high-risk growth strategy that won’t work out every quarter.

HOOD now has 18 million cumulative funded accounts showing the popularity of the business and did $522M in 1Q21 revenue vs. $127.6M in 1Q20 and did $958.8M in revenue in '20 reporting $7.5M in net income.

The median age of customers on HOOD’s platform is 31 and over 50% are first-time investors so if they nurture this customer base, this could be a sticky business moving forward.

If they lead them down this treacherous Dogecoin cliff, it could be trouble and result in terrible quarterly earnings.

A few other risks I felt notable was that Robinhood users went from holding/trading $400M of crypto to $11.5B of crypto from March 2020 to 2021, but HOOD intends to potentially never offer delivery of customer crypto purchases.

This means they are exposed to derivative contracts which just layers on high risk on top of high risk.

Robinhood said there is tremendous regulatory risk for its stock with the company fined $70 million by the securities industry's self-regulator, FINRA, for misleading customers and system outages that the agency said hurt Robinhood's customers.

They said they will likely incur similar fines in the future and investors will need to stomach its predisposition to skirt the law.

There is nothing low-risk about HOOD, and I would wait for a big sell-off after the lock-up expiration to get in at a certain discounted price. Readers shouldn’t blindly pay a premium for HOOD, the risk isn’t worth it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-07 13:02:032021-07-13 19:17:01Should You Buy the Robinhood IPO?

Below please find subscribers’ Q&A for the May 26 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Lake Tahoe, NV.

Q: Do you expect a longer pullback for the (SPY) through the summer and into the last quarter?

A: No, this market is chomping at the bit and go up and won’t do any more than a 5% correction. We’ve already tested this pullback twice. We could stay in this 5% range for a few more weeks or months, but no longer. If we make it to August before we take off to the upside, that would be a miracle. It seems to want to break out right now and if you look at the tech stocks charts you can see what I'm talking about.

Q: Why do day orders with spreads not good ‘til canceled (GTC)?

A: Actually, you can do good ‘til canceled on these spreads, it just depends on how your platform is set up. Good ‘til canceled won't hurt you—only if we get a sudden reversal on a stop out which has only happened four times this year.

Q: Disney (DIS) seems to be struggling to get back over $180; am I still safe with my January 2023 $250 LEAPS?

A: Yes, out to 2023 we’ll have two summers until those expire, so those look pretty good—that's a pretty aggressive trade, and I’m betting you’re looking at a 500% profit on those LEAPS. And by the way, I always urge people to go out long on these LEAPS, because the second year is almost free when you check the pricing. So, take the gift and that will also greatly reduce your risk. We could have a whole recession and recovery, and still have those LEAPS make it to $250 in Disney.

Q: Should I add to Freeport McMoRan (FCX)?

A: (FCX) I would not add—in fact, I would have a stop loss if we closed below $40 on (FCX) if you’re a short-term trader. There is a slowdown in the Chinese economy going on as well as a clampdown on commodity speculation. This has affected the whole base metal space, including steel and palladium. If you have the long-term LEAPS, keep them, because I think (FCX) doubles from here. The whole “green revolution story” is still good.

Q: Do you think the United States Treasury Bond Fund (TLT) is going up?

A: No, I think the (TLT) has been going down. I've been buying puts spreads like crazy, and I have a huge chunk of my own retirement fund in long-dated (TLT) LEAPS, so I am praying it will go down. We’ll talk about that when we get to the bond section.

Q: Prospects for U.S. Steel (X)?

A: It’s tied in with the whole rest of the base commodity complex—I think it is due for a rest after a terrific run, which is why I have such tight stop losses on Freeport McMoRan (FCX).

Q: Do you buy the “transitory” explanation for the hot inflation read two weeks ago that the Fed is handing out, or do you think inflation is bad and here to stay?

A: I go with the transitory argument because you’re getting a lot of one-time-only price rises off of the bottom a year ago when the economy completely shut down. Once those price rises work through the system, the inflation rate should go from 4.2% back down to 2% or so. So, I don't see inflation as a risk, which is why I think the stock markets can reach my 30% up target this year. You may get another hot month as the year-on-year comparisons are enormous. But betting on inflation is betting on the reversal of a 40-year trend, which usually doesn’t work out so well.

Q: On your spread trade alerts can we buy less than 25 contracts?

A: You can buy one contract. In fact, I recommend people start with one contract and test out where the real market is. Put a bid for one contract in the middle of the market, and if it doesn’t get done, raise your bid 5 cents, and eventually, your order gets done. Then you can add more if you want to. I always recommend this even for people who buy thousands of contracts, that they test the market with one contract order just to make sure the market is actually there.

Q: Can you recommend a LEAPS for Amazon (AMZN)?

A: The Amazon LEAPS spread is the January 2022 $3150-3300 vertical call debit spread going out 8 months.

Q: When you short the (TLT), how do you do it?

A: I do vertical bear put debit spreads. I buy a near-money put and sell short and an out-of-the-money put so I can reduce the cost, and therefore triple my size. This strategy triples the leverage on the most likely part of the stock move to take place, which is the at the money. For example, a great one to buy here would be a January 2021 (TLT) $135/140 vertical bear put debit spread where you’re buying the $140 and selling short the $135. The potential 8-month profit on this is around 100%. You’ll make far more money on that kind of trade than you ever would just buying puts outright. Some 80% of the time the single option trades expire worthless. You don’t want to become one of those worthless people.

Q: What’s your best idea for avoiding a U.S. Dollar drop?

A: Buy the Invesco Currency Shares Euro Trust (FXE) or buy the Invesco Currency Shares Australian Dollar Trust Trust (FXA), the Australian Dollar to hedge some of your US Dollar risk. The Australian dollar is basically a call option on a global economic recovery.

Q: I’m a new subscriber, but I don’t get all the recommendations that you mention.

A: Please email customer support at support@madhedgefundtrader.com , tell them you’re not getting trade alerts, and she'll set you up. We have to get you into a different app in order for you to get all those alerts.

Q: How about the ProShares UltraShort 20 Year Treasury ETF (TBT)—is that a bet on declining (TLT)?

A: Absolutely yes, that is a great bet and we’re at a great entry point right now on the (TBT) so that is something I would start scaling into today.

Q: Do you still like Palantir (PLTR)?

A: Yes, but the reason I haven't been pushing it is because the CEO says he could care less about the stock market, and when the CEO says that it tends to be a drag on the stock. Palantir has an easy double or triple on it on a three-year view though. However, small tech has been out of favor since February as it is overpriced.

Q: How far down can the (TLT) go in the next 30 days?

A: It could go down to $135 and maybe $132 on an extreme move, especially if we get another hot CPI read on June 10. However, if you hear the word “taper” from a Fed official, then you’re looking at high $120’s in days.

Q: With the TLT going up, why have you not sent out an alert to double up on put spreads?

A: I tend to be a bit of a perfectionist since I’m a scientist and an engineer, so I’m hanging on for an absolute top to prove itself and start on the way down. On the shorts, I like selling them on the way down, and buying my longs on the way up, because there are always surprises, there’s always the unknown, and heaven forbid, I might actually be wrong sometimes! So, I’m still waiting on this one. And we do already have one position that is fairly close to the money now, the June 2021 $141-144 vertical bear put debit spread, so I don't want to double up on that until we have a reversal in the intermediate term trend.

Q: I see GameStop (GME) is spiking again now up to $230—should I get in for a short-term profit?

A: No. With these meme stocks, the trading is totally random. If anything, I would be selling short, but I would do it in a limited risk way by buying a put spread. However, the implied volatility in the options on these meme stocks are so high that it's almost impossible to make any money on options; you’re paying enormous amounts of money up front, so that's my opinion on GameStop and on AMC Entertainment Holdings (AMC), the other big meme stock.

Q: Will business travel come back after the world is vaccinated?

A: Absolutely. Companies don't want to send people on the road, but customers will demand it. All you need is one competitor to land an order because they visited the customer instead of doing a Zoom (ZM) meeting, and all of a sudden business travel will come roaring back. So that's why I was dabbling in Delta Airlines (DAL) and that's why I like American Express (AXP), where 8% of transactions are for first class airline tickets.

Q: As the work-from-home economy stops and workers go back to the office, do you see a 10% correction in the housing market?

A: Actually, in the housing market with real houses, I don't see prices dropping for years, because 30% of the people who went home to work are staying there for good—that the trend out of the cities into the hinterlands is a long-term trend that will continue for decades, now that Zoom has freed us of the obligations to commute and be near big cities. And of course, I’m a classic example of that; I've been working either in my basement in San Francisco or at Lake Tahoe for the last 14 years. Housing stocks on the other hand like Lennar (LEN), Toll Brothers (TOL) and KB Home (KBH) have had a tremendous run and are basically out of homes. Could they have a 10% correction at any time? Absolutely, yes.

Q: Should I avoid buying dips in last year's work-from-home stocks?

A: Yes I would. DocuSign (DOCO) and Zoom (ZM) are the two best ones because they were both up 12X from their lows, and I tend not to chase things that are up 12X unless they are a Tesla (TSLA) or an Nvidia (NVDA) or something like that. In the end, Tesla went up 295 times.

Q: Are you looking at the carbon credits market?

A: No, but I probably should. That market shut down last year. It’s alive again, and it looks like it's growing like crazy.

Q: What’s the ideal volatility for individual options? What do you use to compare?

A: Always look at the implied volatility of the option compared to the realized volatility of the underlying stock; and when the difference gets too big, you get ideal conditions for putting on call and put spreads, which take advantage of this. These are almost volatility neutral because you’re long on one batch of volatility and short on the other.

Q: Is it too late to get involved in the ProShares Ultra Technology ETF (ROM), the 2X long ETF in a spread?

A: The November 2021 $121-125 vertical bull call spread, the farthest expiration you can get for the (ROM), was kind of aggressive—I would go closer to the money. We’re right around mid $80s right now, so maybe do a January 2022 $95-100, and even that will get you something like a 400% gain by November.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH (or Tech Letter as the case may be), then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Summit of Mount Rose at 10,778 feet with Lake Tahoe on the Right

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/john-thomas-skyline-e1608829740615.png375500Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-05-28 09:02:502021-05-28 10:34:22May 26 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.