Global Market Comments

December 14, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ASSET SHORTAGE),

(INDU), (PFE), (MRNA), (PTON), (DOCU), (ETSY), (CAT), (JPM), (BABA), (TSLA), (TLT), (ABNB), (DIS)

Global Market Comments

December 14, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ASSET SHORTAGE),

(INDU), (PFE), (MRNA), (PTON), (DOCU), (ETSY), (CAT), (JPM), (BABA), (TSLA), (TLT), (ABNB), (DIS)

Markets are wonderful arbiters of the laws of supply and demand.

When there is a shortage of a particular security, Wall Street has a magical ability to manufacture more by running the printing presses to meet supply, or in the modern incarnation, open the spreadsheets.

Except for this time.

The amount of new cash created by global quantitative easing and the prolific saving habits of locked up Americans are creating more demand than even this efficient highly process can accommodate.

Which means that prices can only go up.

How long and how far is anyone’s guess. My target for the Dow Average is 120,000 in ten years, but even I don’t expect that to take place in a straight line. So, we are all sitting on our hands waiting for the next pullback to buy into, which may….or may not ever happen.

A lot of Dotcom Bubble memories are rising up from the dead. Analysts in 1999 made outlandish forecasts of stocks rising 50% in a year, which then took place in four days. That happened to Tesla (TSLA) last month and Airbnb (ABNB) last week.

In the meantime, the smartest traders, call them the oldest traders, are taking profits on the best years of their careers.

Of course, the short-term direction of the market will be determined by the January 5 Georgia Senate election, where the polls are in a dead heat. The last time this happened, during the presidential election, the Democrats won by a microscopic 15,000 vote margin.

If history repeats itself, the Biden administration will get an extra $6 trillion to play with to restore the shattered US economy. Think $2 trillion for infrastructure spending in all 50 states, $2 trillion for the rescue of bankrupt states and municipalities, $1 trillion for alternative energy and EV subsidies, and another $1 trillion in odds and ends. Needless to say, much of this will end up in the stock market.

I am getting a lot of questions these days regarding what will end this once-in-a-generation runaway bull market. The pandemic created this bull market by accelerating technology, business evolution, and corporate profitability by ten years. I bet a year ago, you weren’t spending your day on Zoom meetings, as I was.

The great irony is that the Pfizer (PFE) and Moderna (MRNA) vaccines may not only kill Covid-19 but the bull market as well. That’s because money will then come out of stocks and go back to the real economy.

That makes pandemic darlings like Peloton (PTON), DocuSign (DOCU), and Etsy (ETSY) especially risky. But then 6% growing GDPs were never what stock market crashes were made of, so any declines will be modest.

As for my own positions, I have a rare 100% long portfolio, mostly Tesla, but also the (TLT), (CAT), (JPM), and (BABA), 80% of which expires with the option expiration on Friday, December 18.

After that, I’ll take it easy with 10% short (TLT) and 10% long (TSLA) and wait for the market, or Georgians to tell me what to do.

A flood of money is to hit the stock market, says hedge fund legend Ray Dalio. The US is facing a perfect storm in favor of all risk assets. There is no reason why price earnings multiples for American stocks can’t reach 50X, double the current 25X. Buy what the central banks are buying. The funny thing is that I agree with Ray on everything. Buy risk on dips.

Stocks will keep soaring into 2021, says JP Morgan strategist Marko Kolanovik. The more risk the better. The Fed will keep interest rates low for at least another year, and ultra-low rates will force big institutions out of bonds and into stocks. Volatility (VIX) will decline. It all sounds like a great long stock/short bond trade to me. Hmmmmm.

Tesla completed a $5 Billion share issue, after a move to $650, up $142 from my November Mad Hedge BUY recommendation. The stock seems hell-bent on testing the Goldman Sachs $780 price recommendation before the December 18 S&P 500 entry. Elon Musk’s creation is now worth a staggering $608 billion. It’s the best recommendation in the 13-year history of the Mad Hedge Fund Trader.

San Francisco rents dive 35%, as tech workers flee to the suburbs. A lot of remote work is now permanent. Studio apartments are now a mere $2,100, and a one-bedroom can be had for $2,716. For a two-bedroom if you have to ask, you don’t need to know. Shocking!

Sales of million-dollar homes are soaring, as ultra-low interest rates persist and people spend much more time at home. So, bigger for your pod is better. Mortgages over $766,000 are up 57% YOY.

Jamie Diamond says he wouldn’t touch bonds with a ten-foot pole, and nor would I. A 91-basis point yield just doesn’t do it for the chairman of JP Morgan Chase (JPM), one of my recurring longs. Stocks are a much better choice, even if there is a bubble in progress. Keep selling every rally in fixed income, especially the (TLT).

Weekly Jobless Claims soar to 853,000, up a massive 153,000 from the previous week. To see this happen during the Christmas hiring season is heartbreaking. With 200,000 a day falling to Covid-19, I’m surprised it's not higher, which means it will be. This is what peaks look like. Washington has totally given up.

An $800 billion payday for the bay area. That is the amount of wealth created by just two companies, Tesla (TSLA) and Airbnb (ABNB), since March. And the great majority of shareholders live in the San Francisco Bay Area, including its venture capital and pension funds. No wonder home prices in the suburbs are up 20% YOY. The great irony is that (ABNB) received a massive government bailout only in March. I hope they repay the loans early.

Is Cuba the next big play? A Biden détente could lead to the emerging market investment opportunity of the decade with the $43 million Herzfeld Caribbean Basin Fund (CUBA). It just had its best month in 11 years (like many of us). With Fidel Castro long dead, what’s the point in continuing a 60-year-old cold war. A big market for American products and services beckons, not to mention the tourism and cruise opportunities. But can Biden afford to lose the Florida Cuban vote in the next election?

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

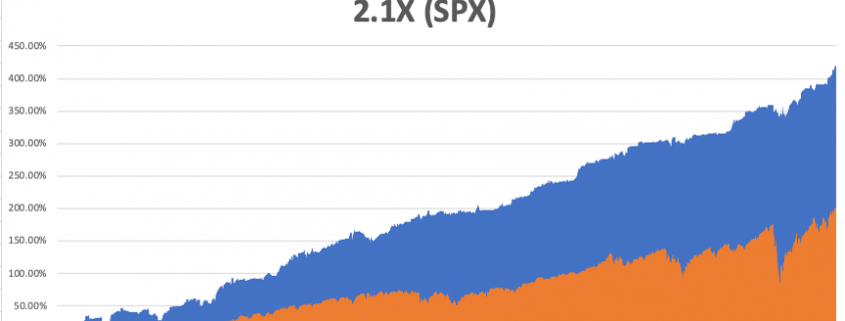

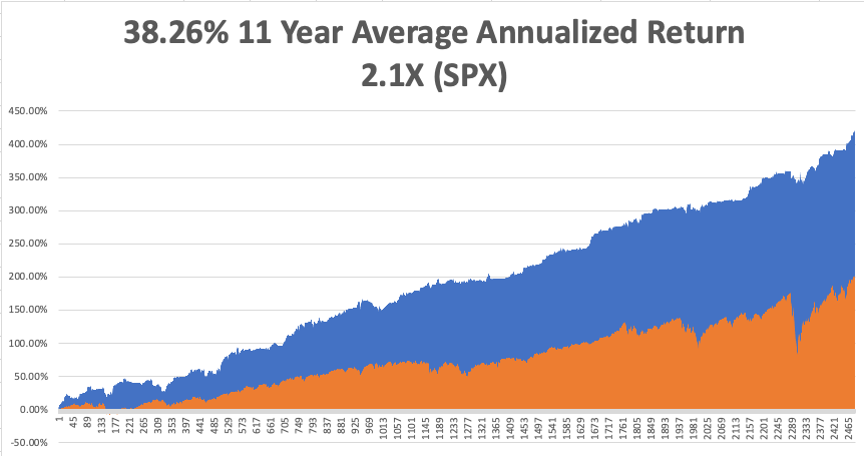

My Global Trading Dispatch catapulted to another new all-time high. December is up 8.55%, taking my 2020 year-to-date up to a new high of 64.99%.

That brings my eleven-year total return to 420.90% or more than double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.26%. My trailing one-year return exploded to 66.30%, the highest in the 13-year history of the Mad Hedge Fund Trader.

The coming week will be a slow one on the data front. We also need to keep an eye on the number of US Coronavirus cases at 16 million and deaths 300,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, December 14 at 12:00 PM EST, US Consumer Inflation Expectations for November are released.

On Tuesday, December 15 at 11:00 AM, the New York Empire State Manufacturing Index for December are published.

On Wednesday, December 16 at 8:00 AM, US Retail Sales for November are printed.

On Thursday, December 17 at 8:30 AM, the Weekly Jobless Claims are published. We also get November Housing Starts.

On Friday, December 18, at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I was stunned to learn that 84 million people are watching The Mandalorian, the latest Star Wars installment Disney (DIS) launched in its hugely successful streaming service a year ago.

It reminds me of when I first saw Star Wars in 1977. I was changing planes in Vancouver, Canada on the way to Tokyo and used a long layover to take a taxi to the nearest theater to catch a film I’d heard so much about.

I was amazed when I realized that the guy sitting in the next seat had memorized the entire script and was mouthing all the words. The only other time I have ever seen this happen was sitting on the benches at Shakespeare’s Globe Theater in London. At least then, they were reciting Romeo and Juliet.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

September 16, 2020

Fiat Lux

Featured Trade:

(THE LEGITIMIZING OF DIGITAL FITNESS CONTENT)

(PTON)

Peloton (PTON) is a tech company I once hated, but that is now undergoing a renaissance because the pandemic has created a surge in demand for home exercise solutions.

In its most recent earnings report, revenue frothed to 172% to $607.1 million, crushing both the consensus estimate of $580 million and the company's own guidance.

Connected Fitness subscribers more than doubled to 1.09 million, and Digital memberships more than tripled to nearly 320,000.

Peloton quite simply is struggling to keep up with demand, like many other winners in the shelter-at-home tech trade.

Peloton has been pedal to the metal expanding manufacturing capacity at third-party contract manufacturers and its in-house manufacturing operations.

Peloton had acquired Tonic, one of its bike manufacturers, a little less than a year ago as part of a vertical integration pivot.

CEO John Foley also noted that the company had to balance the trade-offs with how it allocated capacity.

Peloton recently introduced a new Tread that's more affordable, but it also needed to ramp unit volume.

Foley commented, "While we had hoped to launch our new Tread more quickly and in greater supply, we had to make some tough decisions regarding supply chain resource allocation due to the surge in demand we've been experiencing for our Bike."

Connected Fitness subscriber growth is starting to become constrained at the back half of the quarter, but that was largely due to ongoing supply constraints as opposed to a lack of demand.

The resurgence in coronavirus cases over the summer contributed to another spike in demand for the products so imagine what a winter spike could mean for the company too.

The flip side is that the surge in virus cases has made it challenging to meaningfully reduce order delivery time frames in the US.

Peloton has materially increased production capacity in recent months and continue to grow manufacturing capabilities, but do not expect a normalized order to delivery windows in the U.S. prior to the end of Q2 fiscal '21.

Peloton's financial performance for the rest of 2020 will center around its ability to ramp production in order to satisfy demand.

Conversely, some of the biggest losers in the economy are gyms, and Peloton is feasting on this opportunity.

It’s becoming clearer that connected fitness has a massive runway for growth, especially with over 180 million people around the globe that—prior to the health crisis —belonged to a gym.

Quarterly workouts surged to almost 77 million in the quarter. That’s 25 workouts per connected fitness subscription on average per month.

That is the differentiation that Peloton is myopically focused on because that leads to low churn, that leads to great word of mouth and, frankly, it’s what I believe has changed this category of fitness because there’s finally something that is sustainable and located in the safety of one’s house.

Workouts per subscription have basically doubled from a year ago due to improvements in digital content offerings across non-bike formats like strength training and yoga.

Another tailwind is the accessibility of that content on Roku, Fire TV, Apple TV, Android TV right at the touch screen of the Peloton Bike.

It’s almost as if the coronavirus saved this company and Peloton hasn’t looked back.

Although I was discouraged about Peloton before the pandemic, it appears like a rejuvenated company during the virus era.

Luck sometimes needs to fall on your side and trading pullbacks from the long side makes sense with Peloton right now.

Considering it achieved its first profitable quarter, this exercise-from-home revolution has legs, and incremental revenue gains are highly probable moving forward.

They were just a marginal tech company before, but although not a juggernaut, they have come closer to respectability which is saying a lot for Peloton.

Remember that daily volatility is high in Peloton, I would not hold it until the next crash. Sell for profits and wait for a pullback to get a lower cost basis. Rinse and repeat.

Mad Hedge Technology Letter

March 4, 2020

Fiat Lux

Featured Trade:

(THE BEST TECH STOCKS TO BUY AT THE BOTTOM)

(NFLX), (ZM), (PTON), (AMZN), (OKTA), (WORK), (ATVI), (EA), (TTWO)

Tech stocks that are begging to be picked up on the back of the coronavirus pandemic are Netflix (NFLX), Zoom Video Communications (ZM), workplace collaboration service Slack Technologies (WORK), and Peloton Interactive (PTON), the spin bike company.

Their short-term outperformance indicates that these stocks work well during mass pandemics shelving most outdoor activity and commerce.

The basket of 3 stocks has easily beat the S&P 500 since the coronavirus emerged as a threat in mid-January.

Home sitting doesn’t generate a net output of business activity unless that job is digital.

The majority of workers still commute in a physical car only to sit in an office, restaurant, or some other type of self-contained space.

That is the underlying problem that has no solution, and any rate cut by the Fed cannot ultimately solve consumers holed up in their house.

If the companies that could opt to go pure digital do take up the option, the number of remote workers would rise and digital products would be the ultimate beneficiary of this trend.

Companies that promote remote working such as Slack (WORK) and Google Hangouts are in pole position to reap the rewards.

These services include video conferencing software, logistical services, administrative services, network security services, ecommerce and any service that aids in generating digital content like Adobe and its umbrella of assets.

The trend was already transforming American culture, but the virus vigorously pulls forward a trend that was already in overdrive.

Enabling information workers to produce outside the traditional office environment is one of the lynchpins of the Silicon Valley model.

Companies will ultimately realize that spending big bucks on business travel to meet face to face for 30 minutes is probably not an optimal allocation of resources.

Business travel is getting cut with a cleaver such as Amazon.com (AMZN) who are forcing employees to avoid all nonessential travel for now, including within the U.S. Much of that travel could be replaced by video calls.

Other companies will get in on the action by directing their employees to work from home in the coming weeks.

Coronavirus mania has reached the U.S. shores with consumers stocking up on all the essentials at the local Costco.

If this gets worse, there is no solution unless a viable medical solution starts improving the health crisis.

There are still only 7 known fatalities from the coronavirus, all in the state of Washington, and limiting that number is critical to the health of the tech market.

Another company is Okta (OKTA), a leader in authentication security cloud software.

The company’s offering allows employees to use corporate applications on-site and remotely and protecting their access to their digital services is just as important as the work itself.

As consumer spurn movie theaters, concerts, and gyms, the entertainment space will give way to digital entertainment that includes Netflix (NFLX) and Roku (ROKU).

Roku is a great place to hide out in the world where Covid-19 meets daily consumers in the U.S. in a more meaningful way during 2020.

Netflix is a company that has defied gravity this year by bull-rushing its way through the competition and proving there is space for everyone.

The increase in incremental demand for digital content will only help Netflix claim a bigger part of the pie.

We can also lump the videogame industry into this cohort such as Activision Blizzard (ATVI), Electronic Arts (EA), and Take-Two Interactive Software (TTWO).

They have faced serious headwinds from gaming phenomenon Fortnite, but prolonged home sitting will even boost their shares.

The spine of digital services will receive a boost as well from the usual cast of characters such as Microsoft (MSFT), Apple (AAPL), Alphabet (GOOGL), and Facebook (FB).

As investors wait for the climax of the coronavirus and the Central Bank has indicated that they are open to more accommodative policy, we could be ripe for more volatility.

Chinese coronavirus cases have started to taper off and if the rest of the world trends in a similar fashion, this virus scare could be in the history books in 2-3 months.

However, the trajectory of the virus is still a massive unknown in the U.S. and winning the health battle is the only panacea to this dilemma.

Mad Hedge Technology Letter

December 16, 2019

Fiat Lux

Featured Trade:

(THE PELETON BUBBLE IS ON)

(PTON), (PLNT), (NFLX), (AMZN)

Own a Peloton (PTON) bike, but don’t buy the stock.

That is the conclusion after deep research into this wellness tech company.

Peloton is an American exercise equipment and media company that bills itself as a tech company.

It was founded in 2012 and launched with help from a Kickstarter funding campaign in 2013. Its main product is a stationary bicycle that allows users to remotely participate in spinning classes that are digitally streamed from the company's fitness studio and are paid for through a monthly subscription service.

Peloton is wildly overpriced with the enterprise value of each subscriber at $15,631.

Contrast that with other comparable firms such as Planet Fitness (PLNT) whose enterprise value per subscriber is $553 or even streaming giant Netflix (NFLX) whose enterprise value per subscriber comes in at $895.

There are three massive deal breakers with this company – software, hardware, and the management team.

The management team acts as a bunch of cheerleaders overhyping a simple exercise bike with a screen that has no deeper use case and in turn an unrealistic valuation that has disintermediated from all reality in the post-WeWork tech world.

What’s the deal with the hardware?

Some recognition must be given to Peloton for creating a nice bike and interactive classes that mesh with it. That idea was fresh when it came out.

The marketing campaigns were attractive and allured a wave of revenue and these customers were paying elevated prices.

But the bike itself has not developed and advanced in a meaningful way since it debuted in 2014 and back then the valuation of the company was $100 million.

The first-mover advantage was a godsend at the beginning, but the lack of differentiation is finally catching up with the business model and now you can get your own Peloton carbon copy on Amazon (AMZN) for $500 instead of $2,300.

Instead of focusing on the meat and bones of the company, Peloton has doled out almost $600 million over the last 3 years in marketing to capture the low hanging fruit that they most likely would have seized without marketing while competition was low.

Competition has intensified to the point that some of its competitors are giving away bikes for free justifying to never cough up cash for a $500 exercise bike let alone a $2,300 genuine Peloton bike.

The first-mover advantage when Peloton had the best exercise bike is now in the past and the company is attempting to move forward with a stagnant bicycle.

The Peloton treadmill came out much later but has not caught on and has many of the barriers to success I just talked about.

What about the case for owning the stock for the software?

Peloton is charging an overly expensive $39 per month for a “connected experience” to anyone who has bought the $2,300 Peloton bike.

But if the user happens to not buy the bike, they can download the digital app and pay $12.99 per month for the same connected experience.

Why would someone pay $2,300 for an overpriced exercise bike when they can just sign up to a full-service gym and just use the Peloton app with some headphones for $12.99 per month?

This illogical strategy means that less than 10% of Peloton subscribers have bought their bike.

Peloton’s competitors have shredded apart their strategy by essentially underpricing their bike and mentioning that they can use the Peloton app with their bike.

And even if you thought that Peloton’s live streaming fitness classes were the x-factor, users can just add a nice little removable iPad holder to the exercise bike and stream YouTube for free or any other digital content on demand.

The cost of adding an iPad holder is about $13-$15 which is a cheap and better option than paying $12.99 or $39 per month for Peloton’s fitness classes.

Users will eventually migrate towards cheaper packaged content because of the overpriced nature of Peloton’s digital content.

Is Management doing a good job?

Peloton’s CEO John Foley most recently told mainstream media that the company is profitable when it is not.

He has repeated this claim several times throughout the years as well. The company has never been profitable and lost $50 million on $228 million of revenue last quarter.

Each quarter before that has also lost between $30 million to $50 million as well, and Foley is outright dishonest by saying the company is profitable.

Peloton relies on top 100 billboard songs to integrate with their fitness streaming classes and the company just got slammed with a $300 million lawsuit from music publishers claiming they have never actually paid for music licensing.

Music is core to their streaming product and without the best songs, users won’t tune in just for the instructor.

Working out and live music go hand in hand and stiffing the music industry on licensing fees is just another example of poor management.

In March 2020, the lockup expires and top executives are free to dump shares which will happen in full force.

Management has one unspoken mandate now – attempt to buoy the stock any way possible until they can cash out next March.

This group of people is only a few months away from their payday.

There is no software or hardware advantage and management is holding out for dear life until they can kiss the company goodbye.

Do not buy shares and I would recommend aggressively shorting this pitiful attempt of a tech company.

Peloton is a $6 stock – not a $30 stock.