For all the cryptocurrency haters in the world, it’s getting harder to take that stand.

I’ll tell you why.

Coinbase (COIN) was the first major crypto business to go public in the U.S. when it began trading at $381 Wednesday morning on the Nasdaq and its IPO symbolizes the acceptance of an alternative digital asset class in technology.

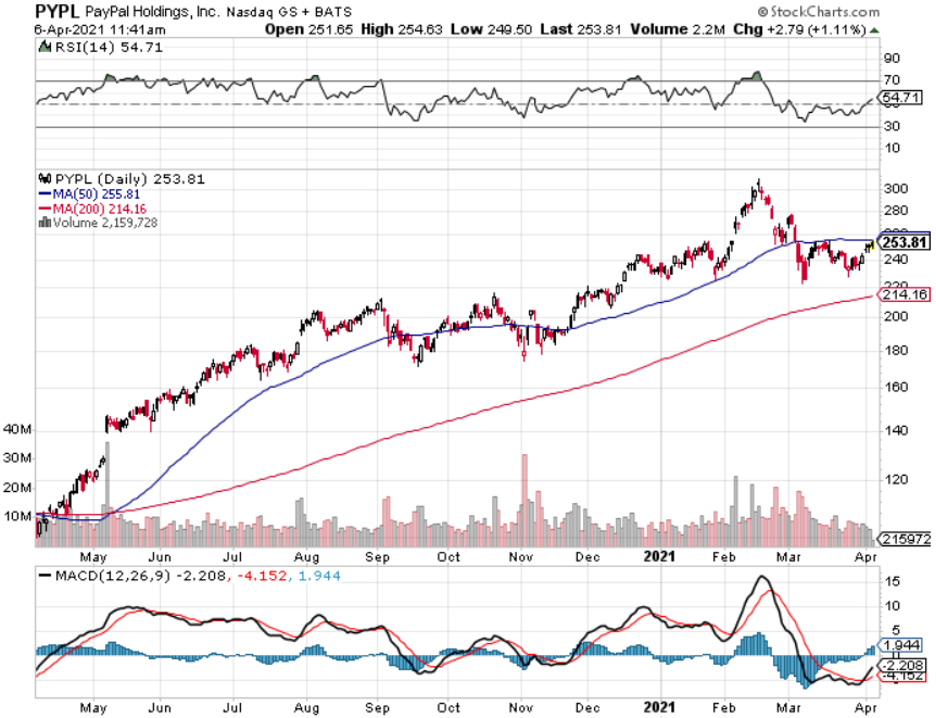

Prior to this watershed moment, the only way to play crypto was through second derivatives plays like PayPal (PYPL) and Square (SQ) who have been handsomely rewarded through higher share prices.

Now, we get the biggest U.S. cryptocurrency exchange trading publicly that will allow exposure to mainstream stock-market investors.

The event has also been tabbed as a catalyst that might drive the adoption of incremental digital assets.

At the very least, this lays down a marker for further crypto-related companies eyeing the Nasdaq after Coinbase’s blowout success.

This also shows that the cryptocurrency infrastructure is developing rapidly and its budding credibility is something that needs to be acknowledged.

The Coinbase IPO was also the catalyst in sending bitcoin prices to almost $65,000.

No doubt that the appreciating asset has been the most attractive use case for the incremental investor and cryptocurrency buyer.

Many early investors who got into bitcoin at 20 cents are now billionaires many times over.

After such stunning success, it’s hard to believe that any fintech or cryptocurrency start-up would ever consider doing their IPO anywhere else but New York.

New York has the liquidity, the US dollar, and the capacity to receive such type of growth companies in bulk.

This is not only an emphatic victory for digital assets, but also for the US tech sector and a stamp of validation for the Nasdaq market.

Ironically enough, even during this trade war, Chinese tech companies are clamoring to go public in New York and not mainland China for the above reasons.

Here are a few other highly positive data points to digest that were talking points in their S-1 filing.

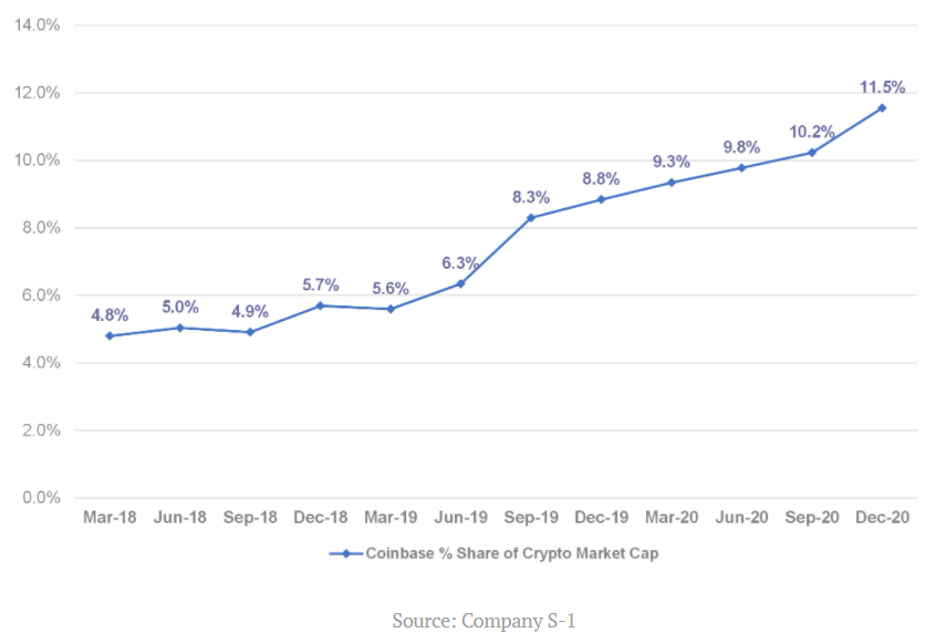

The overall market capitalization of crypto assets grew from less than $500 million to $782 billion between December 31, 2012, and December 31, 2020, representing a CAGR (compound annual growth rate) of over 150%.

Over the same period, Coinbase retail users grew from less than 13,000 to 43 million, a 175% CAGR.

I believe the total market cap of crypto is now around $2 trillion in April 2021.

And more recently, Coinbase has experienced significant growth in the number of institutions on their platform, increasing from over 1,000 as of December 31, 2017, to 7,000 as of December 31, 2020.

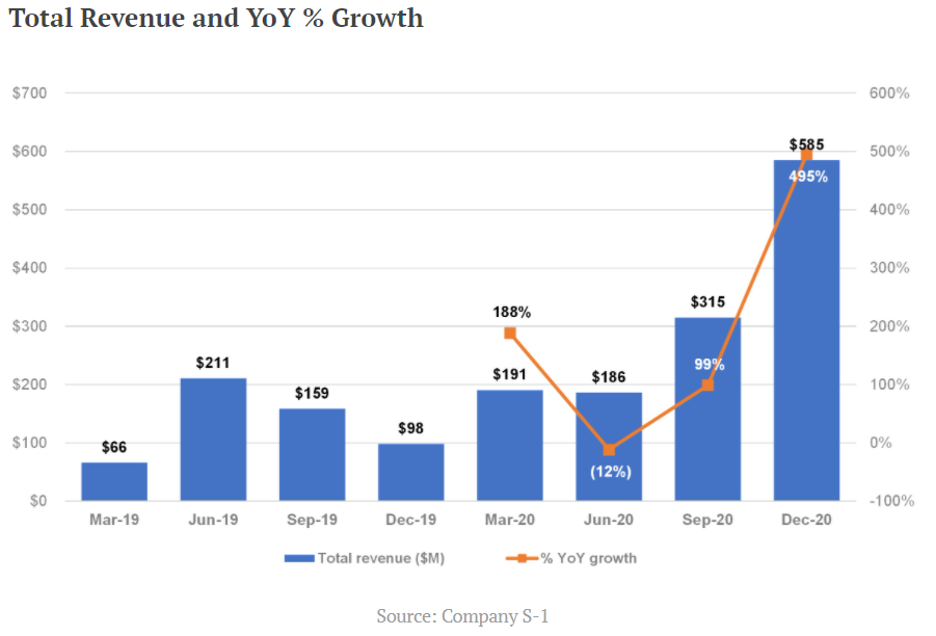

Bitcoin reported a nine-fold increase in Q1 revenue, to $1.8B, up from $190.6M the previous year.

Just like Google and Facebook benefit from a duopoly, Coinbase will benefit from being the only pure cryptocurrency option on the Nasdaq and that will put a floor under shares in the short-term.

The growth metrics of the company are also robust via a helping hand by the increasingly expensive price of bitcoin.

No doubt that this company’s prospects are tied to the hip with the prices of cryptocurrencies.

If the price of bitcoin retraces to $30,000, which it could because of the high volatility of it, expect Coinbase shares to dive with it.

This for all intents and purposes is a bet on the health and price trajectory of bitcoin for better or worse until other crypto-based choices are introduced which would give more layers and complexity to this sub-sector.

Bitcoin calls out Binance which they state as a competitor and Kraken is another exchange that is large and vying for the same capital.

I believe these two companies have a chance to go public and that is when you will really see the institutions jump on this crypto bandwagon.

More options and a foundational investment base will also promote stability in this new technology sub-sector.

Should you buy Coinbase today?

No.

I understand Coinbase’s growth metrics are off the charts with revenue growing 900%, but it’s not worth $100 billion market cap on just $1.8 billion of quarterly sales.

Investors would need solid tailwinds such as bitcoin passing $100,000 in 2021 for this company to be worth $100 billion and I just don’t see it.

Then also understand the cybersecurity and possible regulations are two risks that could blow up the business model at any moment which would take down the premium in the stock.

Yes, the meteoric rise of crypto at the start of 2021 has turned heads, but as the economy reopens, I do believe money will rotate from crypto back into traditional technology that is underpinned by cash cow businesses.

Highly profitable companies that aren’t FANGs are also set to deliver share appreciation to shareholders such as Salesforce (CRM) or a company like Adobe (ADBE) who earn profits of $5.27 billion on $13 billion of annual revenue.

I acknowledge that Coinbase’s IPO was the perfect time to go public.

They are taking advantage of easy money and low rates while the acceptance of this alternative asset class has never been higher.

However, I don’t see any more incremental growth in the short term and the stock is more than fully priced today.

The risk-reward is not favorable to pile into this stock now unless you have a bullish 50-year view on crypto and can’t wait.

This stock will go through volatility because of the inherent dynamics they are tied to and I would seriously look at buying Coinbase only on a massive sell-off.

Don’t go chasing unicorns.

At the end of the day, this is a real company with real revenue growth of 900% year-over-year. Slice it up anyway, and these numbers are numbers that attract investors, but the stock is too expensive right here.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/trading-surges.png348890Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-16 14:02:322021-04-20 00:31:08Should I Buy Coinbase Today?

As vaccine shots hit a peak of 4 million on Easter Weekend, this means the return of the mall and retail, right?

Surely, a reopening bounce for retail is in the cards?

Think again.

A new report from a major bank suggests that 80,000 retail stores will close in the U.S. over the next few years.

This is not a wild guess or speculative bet on what will happen, this is starting to become a consensus.

By 2026, the worst-case scenario is 200,000 stores closing and by 2030, the worst-case scenario entails 300,000 stores closing highlighting the impactful nature of the situation.

As I took a fine-tooth comb to the latest earnings’ data, I can’t help but see that every tech CFO sees the accelerated digital transformation as one of the legacies of the pandemic.

But it will not be an invisible virus keeping shoppers away from the mall in the future, consumers are just satisfied with ordering from home and this economic behavior will become embedded in the new post virus world.

In 2020, 17 major retailers filed for bankruptcy – including Lord & Taylor, Century 21 and Brooks Brothers.

Countless are on the verge of defaults underscoring the pitiful shape of many retailers.

On the other side of the pandemic, blighted malls and unpaid rental payments is what will be left for much of retail.

Many of these malls won’t be able to rent out spaces for pennies on the dollar.

Many stores have gone 100% digital, even restaurants, that haven’t been able to offer dine-in options.

Online retail’s market share of the full retail landscape climbed from 14% in 2019 to 18% in 2020, and by 2025, that number will grow close to 30.

Average household spending online has grown the past five years from $5,800 to $7,100 from 2019 to 2020 highlighting how U.S. shoppers are increasingly comfortable ordering volume online.

Now armed with more stimulus money, I highly doubt there will be a renaissance in brick-and-mortar retail.

One possibility in the future is that many brick-and-mortar stores will double dip, both selling and fulfilling online orders from the same location.

Also, some goods simply aren’t made for click, order, and collect at home like shoes and dresses but others are such as home improvement, grocery, and auto parts.

The silver lining is awfully thin for the retail sector and odds are, if retailers don’t have a digital footprint by now, they are already toast.

The mall vacancy rate rose to 10.5% in the fourth-quarter 2020 from 10.1% in the third quarter and 9.7% a year ago.

This is unlikely to reverse in the short, medium, or long term and another concept for malls will need to be carefully thought out.

Considering further deterioration of non-digital retail, this should directly lead many investors to conclude that pouring money in ecommerce and fintech companies is the right thing to do.

It absolutely is.

The thesis for outperformance is so obvious that many tech investors need to seriously capture part of this sustainable megatrend.

On top of my list of fintech firms are Square (SQ) and PayPal (PYPL).

Square expanded sales 141% year-over-year last quarter and have been profitable for the past two quarters with EPS growing 39% year-over-year last quarter.

PayPal has a much bigger business meaning the law of numbers start to work against them.

They expanded sales 23% year-over-year last quarter and improved EPS by 30% year-over-year.

These two fintech stocks should be considered on every substantial dip because profitability increases have a clear path for the foreseeable future and the robustness of in-house products have not disappointed over time.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-07 12:02:172021-04-11 14:48:41The Disappearing U.S. Retail Store

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

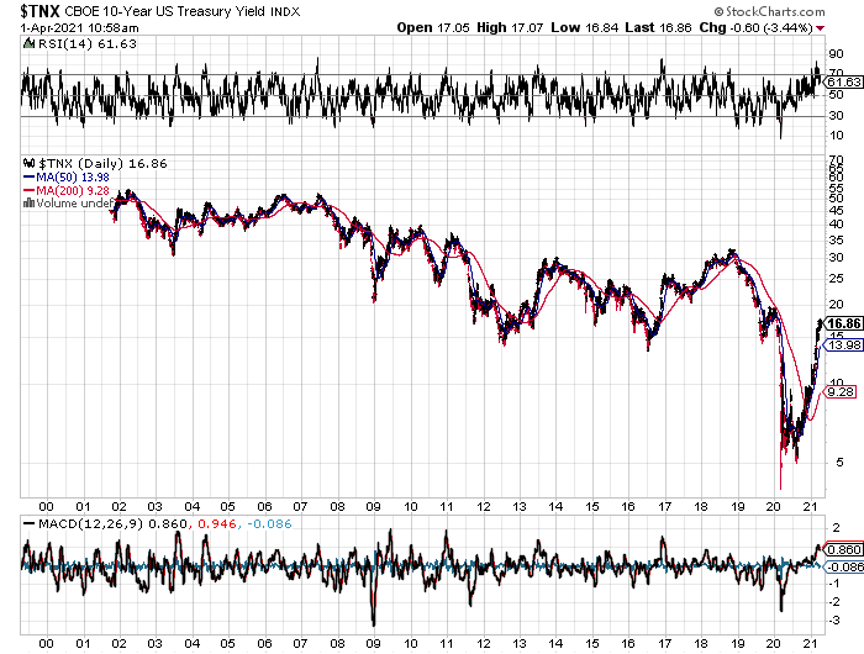

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & HealthcareLetter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/john-thomas-lakeshore-e1608229033313.png338450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-01 11:02:522021-04-01 14:14:23March 31 Biweekly Strategy Webinar Q&A

After a deluge of positive vaccine news, the bottom line is that there will be more work in 2021.

It has always been about the work.

As much as it seems recently that social media is taking over and that the marketing of work will solve economic problems from Guatemala to Zanzibar instead of the work itself, I have news for you: it won’t.

It is still about the work, and for tech newsletters like this one, it’s about the content and always will be.

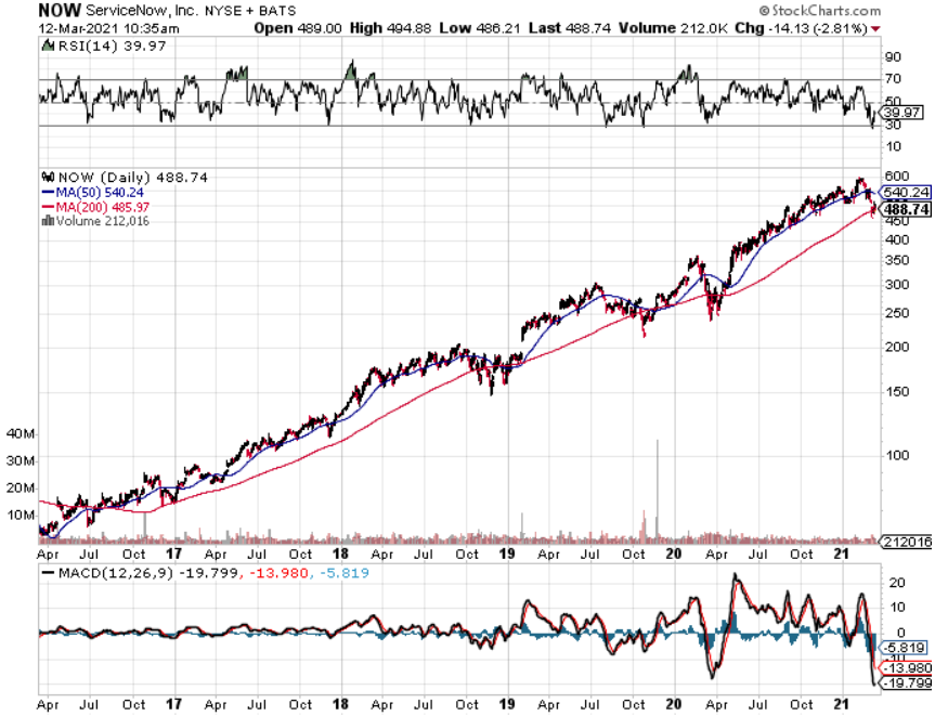

Vaccine-based health solutions will release a torrent of new work opportunities, and tech stock readers need to jump into this workflow automation cloud stock called ServiceNow (NOW).

Digital investments are at an all-time high and are expected to continue expanding.

This is the best place to park investment money betting on future digital-based work growth.

According to IDC, worldwide digital transformation investments will total more than $7.4 trillion by 2044.

The digital economy is firing on all cylinders and ServiceNow is the platform company for digital business.

A quick review of 2020 indicates outperformance.

They significantly beat expectations across the board, bringing heightened momentum into 2021 and beyond.

NOW delivered over 30% organic top line growth, 25% operating margins and $1.4 billion in free cash flow.

Their achievement is a testament to ServiceNow’s strong work culture.

The secular tailwinds of digital transformation, cloud computing, and business model innovation have all intersected at a perfect moment in time.

A paradigm shift is occurring worldwide.

In 2020, for the first time in history, digital transformation spending accelerated despite GDP declining globally.

ServiceNow is enabling a comprehensive solution for the schedule and reporting of vaccination for Scotland's most vulnerable citizens.

Within 12 hours of rollout, the NHS (National Health Service) in Scotland booked over 220,000 appointments.

NOW is literally all about the business workflow maximizing enterprise digital transformation with how every organization in every sector in every location.

Workers are adapting, growing, creating new business models, and empowering themselves to be productive in any environment and in condition.

NOW grew billings by more than 40% year over year organically.

They delivered 89 deals greater than $1 million and now have close to 1,100 customers paying over $1 million annually.

This bounty of sales included landing the largest deal in NOWs history and deal sizes overall keep getting larger.

NOW's renewal rate remained best in class at 99%.

In 2020, they added nearly 700 net new customers, ending the year with almost 6,900 enterprises.

The number of giant deals continues uninterrupted with customers paying NOW $5 million or more in annual contract value (ACV) grew over 40% in fiscal 2020.

One of the U.K.'s big four banks is using multiple ServiceNow products, including a purpose-built new financial services operations product to help transform the way it operates and to deliver better customer experiences.

The bank has seen a 70% uptick in efficiency and improvement of payment processing by integrating the Now Platform into its core banking systems.

These bankers moved from cut and paste, swivel chair manual processes to efficient, automated workflows.

In one case, employees went from managing 10 requests an hour to 10,000 requests in three minutes on the Now Platform.

PayPal (PYPL) recently expanded their relationship with ServiceNow as a key partner for elements of their digital transformation.

Nike is another big name who is using the Now Platform to create better customer and employee experiences.

Other additive deals that are noteworthy are in key sectors such as Booking.com in travel and hospitality, BP in energy, Santander U.K. in banking.

Most cloud stocks are high growth and trot out even higher losses, but now NOW!

They run a tight ship with Q4 operating margin of 22%, a 100-basis-point beat versus guidance, fueled by strong top line outperformance.

For full year 2020, operating margin was 25%, up 300 basis points year over year.

Looking forward, only optimism can be described in the corridors of NOW and for Q1, the company expect subscription revenues between $1.275 billion and $1.28 billion, representing 28% to 29% year-over-year growth.

The cloud revolution is still in the early innings and this company has guaranteed $10 billion in annual sales representing a more than doubling of revenue from the $4.52 billion in 2020.

NOW has a strong product portfolio, a deep focus on building deep customer relationships, and a robust commitment to enabling digital transformation.

This cloud company must be in your top 20 of ones to own and the stock price will benefit from this dynamic business.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/automation.png304934Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-12 15:02:002021-03-22 15:30:37ServiceNow is Now

I cannot overstate the importance of digital financial innovation to the success of PayPal (PYPL) and Synchrony Financial (SYF).

Consumers are rapidly adopting technologies that enable contactless commerce and expect engagement along their digital purchase journeys.

These fintech firms are leveraging robust digital assets and continuously investing to ensure their partners are well-positioned in this rapidly evolving dynamic.

These investments include the capabilities to empower SaaS and seamless integration with partners' digital assets, enable customer choice at the point of sale, enhance contactless experiences, facilitate a seamless and easy application process, bring the in-store experience to a customer's digital devices for applications and payment, and integrate financing office throughout the entire digital shopping experience.

They also continue to make headway in digital penetration of all aspects of the customer journey.

Lockdown requirements and 14-day quarantine are forcing consumers to resort to online transactions for payment networks, online lending, money transfers, business-to-business payments, personal finance, banking, and more.

The key factor driving the growth of the fintech market is high investments in technology-based solutions by banks and other financial institutions. In addition, infrastructure-based technology and APIs (application programming interface) are reshaping the future of fintech.

The behavioral changes induced by the pandemic, such as online shopping and cashless payments, are here to stay and will continue to propel fintech’s growth this year and beyond.

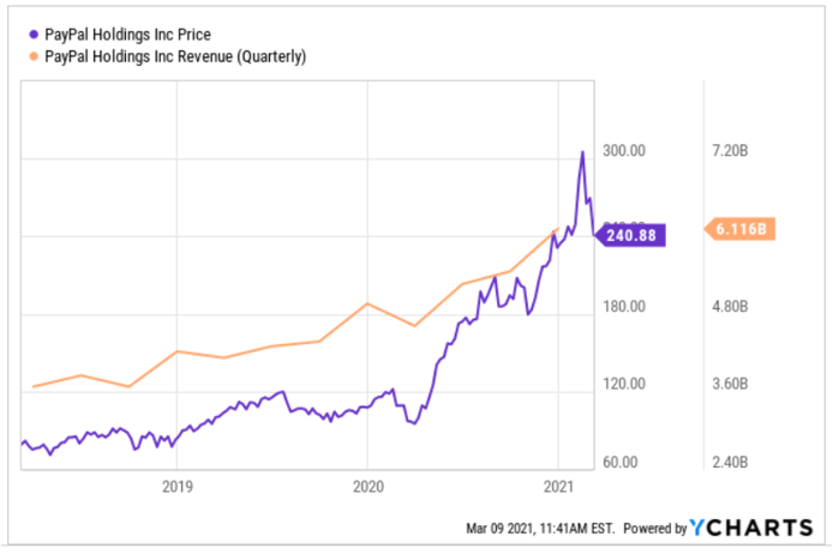

PYPL is one of the most entrenched digital payment operating technology platforms that enables digital and mobile payments on behalf of consumers and merchants worldwide.

It has more than 361 million active users globally and is available in more than 200 markets around the world, enabling consumers and merchants to receive money in more than 100 currencies.

The overperformance of late is not a fluke, in just the last quarter, PYPL added more than 15.2 million new accounts. Its top-line has increased 25% year-over-year to $5.46 billion.

The company is now doing total payment volume (TPV) of $247 billion, growing 38% from the year-ago quarter.

Profitability is another check off the list with EPS for the third quarter coming in at $0.86, rising 121% year-over-year.

The company has been propelled by a spike in e-commerce sales and is one of the preeminent fintech stocks in the U.S.

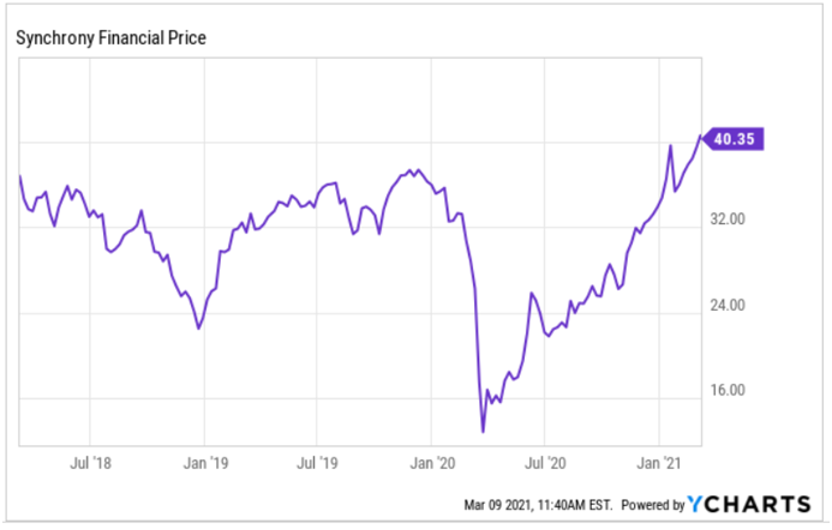

A less entrenched name but worth a speculative look is Synchrony Financial (SYF).

SYF delivers a wide range of specialized financing programs as well as innovative digital banking products across key industries including retail, home, auto, travel, and pet care.

They have a private labeled credit card business with around 60% of SYF applications done digitally during the fourth quarter and grew 18% in mobile channel applications. In Retail Card, 51% of total sales occurred online. Finally, approximately 65% of payments were made digitally.

Synchrony is the 10th-largest credit card issuer in the U.S., with a roughly 2% market share.

But unlike other issuers, Synchrony primarily issues store credit cards, which offer users rewards and benefits.

Synchrony offers more than 100 of these store cards, including the Amazon.com Store Card, which can only be used for Amazon purchases, as well as cards from Lowe's, Banana Republic, Ashley Furniture, and Sam's Club.

Synchrony also offers about 30 store-branded cards that can be used on the broader Mastercard (MA) or Visa (V) network. Among them are the Nissan Visa card and the PayPal Cashback Mastercard.

Synchrony saw earnings plummet to $286 million in the first quarter, down from $731 million in the fourth quarter of 2019. Then, earnings dropped to a low of $46 million in the second quarter before climbing back up to $313 million in the third quarter.

But they rebounded in the fourth quarter of 2020 with earnings surging to $738 million signifying an expansion from pre-pandemic performances.

The Venmo card is also a huge growth opportunity and the possibility of linking up with other fintech groups to create attractive products.

Synchrony added 25 new relationships in 2020, including two major deals that should drive growth in 2021 and beyond.

One was with PayPal to launch the Venmo credit card fueled by Visa.

Venmo is PayPalʻs hugely popular mobile app to send and receive money.

The Venmo credit card, which can be used virtually, provides Venmo users with cashback on purchases and comes with a QR code that allows contactless payments.

Synchrony also signed two other major credit card deals with Walgreens and Verizon.

The Walgreens relationship gets Synchrony into the health space, which allows people to pay for health and wellness expenses at some 225,000 different healthcare providers.

The company also acquired Allegro Credit, a provider of point-of-sale consumer financing for audiology products and dental services, to be part of the growing CareCredit network.

The other big move last year was launching the Verizon Visa card, which offers benefits and discounts for Verizon customers.

Synchrony and PayPal are dynamic fintech companies with savory futures.

PayPal is the bigger and safer bet of the two, but Synchrony will benefit more if their risks turn out well because the law of large numbers isn’t counting against them yet.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/synchrony.png530832Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-10 12:02:422021-03-15 19:14:412 Fintech Bets to Jump On

Mad Hedge Technology Letter February 24, 2021 Fiat Lux

Featured Trade:

(THE LARGEST RISK TO TECH GROWTH SHARES)

(PYPL), (SQ), (GOOGL), (BTC), (TSLA), (FOMO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-24 11:05:372021-02-24 11:34:14February 24, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.