Mad Hedge Technology Letter

December 21, 2020

Fiat Lux

Featured Trade:

(THE BEST WAY TO SUPERCHARGE YOUR TECH PORTFOLIO)

(NVDA), (PLTR), (AMD), (APPL), (OTC:SFTBF), (INTC), (QCOM)

Mad Hedge Technology Letter

December 21, 2020

Fiat Lux

Featured Trade:

(THE BEST WAY TO SUPERCHARGE YOUR TECH PORTFOLIO)

(NVDA), (PLTR), (AMD), (APPL), (OTC:SFTBF), (INTC), (QCOM)

Superiority is mainly about taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

Well, if you thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

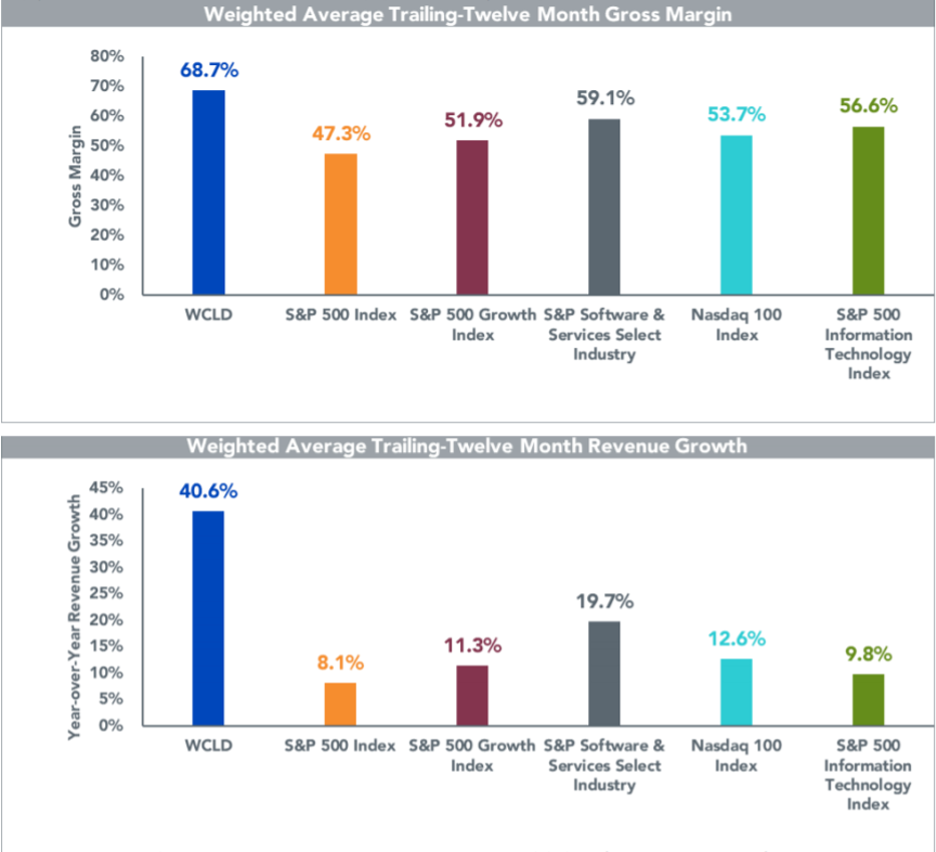

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot in 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deploying via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can more easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue streams making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to better margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD stock are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a direct play on cloud computing, but the elements of its cloud business are nothing short of brilliant.

But ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more risk because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger.

One stock that has the chance of a 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations, and my call was to buy them at $10 after it’s IPO, it's up to $26 and has an easy pathway to $50.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations even though its CEO Alex Karp has been caught on video making fun of the current administration’s leaders.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner and don’t forget about PLTR while you’re at it.

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

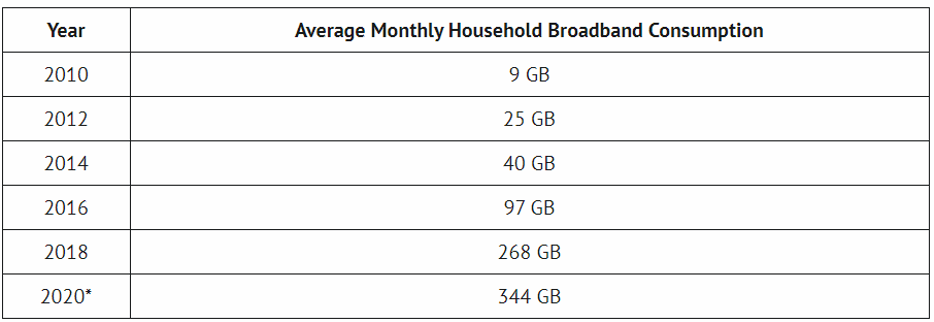

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Mad Hedge Technology Letter

December 14, 2020

Fiat Lux

Featured Trade:

(NVIDIA’S SHOW OF FORCE)

(NVDA), (AMD), (APPL), (OTC:SFTBF), (INTC), (QCOM)

One of the best buy and hold tech stock has to be Nvidia (NVDA).

They are positioned at the vanguard of every major cutting-edge technology in the world such as self-driving technology, data center, and artificial intelligence.

Their cash cow business of manufacturing GPUs (graphics processing unit) which are essential to video gaming has been bolstered by the shelter-at-home movement.

Video games as an activity or something to just pass the time has never been so popular and Nvidia is the best of breed in this department.

The key takeaway from Nvidia’s asset portfolio is the diversity.

They aren’t beholden to any one division and I wouldn’t bet anytime soon that video games are going to go out of fashion because of the generational tailwind occurring.

In fact, the underlying Nvidia stock has risen more than 120% in 2020 and semiconductors have proven to be an astute place to put your money in during the pandemic.

The same goes for competitive rivals such as Advanced Micro Devices (AMD), Intel (INTC), and Qualcomm (QCOM) who explore some of those same markets.

Nvidia counts Amazon (AMZN) Web Services as a customer for data-center chips. It is partnering with VMware (VMW) and Amazon on an AI-driven cloud platform for big businesses.

Be mindful that semiconductor stocks are volatile because of the boom-bust nature of their business cycle.

Global chip sales cratered in late 2018 and fell 12% in 2019.

They rallied early this year on signs of an industry recovery and on a U.S.-China trade deal, then sold off on coronavirus fears.

The trade war has also thrown a spanner in the works of global chip production.

Production was first halted in China and then put global economies under strain.

Despite the pandemic, the semiconductor industry will return to growth in 2020.

Chip sales will rise by 5.1% to $433 billion this year and accelerate to 8.4% in 2021.

The spread of 5G wireless networks is a key catalyst.

Moving forward, it’s highly likely that U.S. lawmakers maintain an anti-China doctrine, and Nvidia and AMD derive only 1% to 2% of revenue from Huawei.

In fact, other companies are more exposed like Cisco and Intel.

How well is Nvidia doing?

They increased revenue by 57% year over year in the third quarter predominately due to its data center business, which grew revenue by 162% over the same period.

In Q3, the data center division accounted for $1.9 billion of the company's $4.7 billion of revenue.

Nvidia is also growing through acquisitions with its blockbuster pending $40 billion acquisition of chip design licensor ARM Holdings from Softbank (OTC:SFTBF).

ARM’s acquisition will help NVIDIA maintain the best of breed quality through 2021 and beyond.

That is important because the semiconductor industry is becoming more cutthroat with many big players sourcing chips in-house after deeply investing in this technology.

Apple (AAPL) recently unveiled its own stable of Mac processors, the M1, making its debut in late 2020. Manufacturing chips is historically a capital-intensive activity, and new chips don’t roll out that fast. In any case, cash-rich companies the size of Google and Apple have the firepower to pull this off.

ARM holds many unique patents forcing many companies to license from them, Apple can customize those designs, and the actual fabrication is outsourced to Taiwan Semiconductor (TSM), the largest and most technologically advanced semiconductor fabricator in the world.

In this specific case, Intel is the direct loser from the production of Apple M1 chips and at this point, this is becoming an existential crisis for Intel.

The acquisition of ARM is a gamechanger, and not just because NVIDIA would gain access to new markets like CPUs for mobile as early as 2021.

Integrating with ARM signals NVIDIA's future shift toward licensing of technology - a far more stable business model than the traditionally cyclical nature of semiconductor industry sales driven by upgrade cycles.

It all comes down to the quality of NVIDIA's chips which remain highly competitive in secular growth areas of tech, such as data centers and artificial intelligence. This alone should keep NVIDIA high up investors' list for years to come.

Demand for the new Nvidia GeForce RTX GPU has been “overwhelming” and the company completed its Mellanox acquisition, a tech firm that sells adapters, switches, software, cables, and silicon for markets including high-performance computing, data centers, cloud computing, computer data storage, and financial services, in April, helping it to double down on their revenue drivers.

Sales for Nvidia's chips remain robust across some of the most desirable end markets and there is nothing meaningful out there to suggest that Nvidia won’t continue its overperformance next year even if the shelter-at-home economy stops.

I am highly bullish on Nvidia stock into 2021 and beyond.

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 8 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Is it premature to be buying long-term LEAPS?

A: Absolutely not—a long-term leap is a bet that your stock will recover beyond your strike prices in two years, which I certainly believe is the case with all of the quality tech and biotech names. These are pretty illiquid so the only way to get a good price is to have a bid in place on one of those absolute puke out days. You will never buy these at the bottom.

Q: Do you see a rally in the stock market in the fourth quarter of this year after the election?

A: For sure—we should be well clear of the pandemic by then, and all of the $6 trillion stimulus will be hitting at the same time.

Q: With the rally in the S&P 500, would you double up on the (SPY) put spread—the May $300-$310?

A: No, keeping your leveraged positions small is crucial in this kind of environment, and the big short play is basically behind us. Better to add the 2X ProShares Ultra Short S&P 500 (SDS) to catch a smaller move down.

Q: Will gold work if the market sells off as a safety trade?

A: Yes, it will. Gold (GLD) had that big 15% selloff a couple of weeks ago when it looked like all financial markets worldwide were going to completely freeze up, and everyone got margin calls all at the same time. We are clear of that now and I expect gold and other traditional hedges like shorting volatility, for example, to also work as a hedge. Gold is going to a new all-time high soon. Buy (GLD), (GDX), (GOLD), and (NEM).

Q: When do you think international borders will open up again, and will that have a positive effect on the economy?

A: Absolutely. You can expect the market to rally 10% into the opening of borders, and then another 10% afterwards depending on where the starting point for the market is in that. As for timing, they may open up in June, and then close up in again in the fall when a second Corona wave hits.

Q: Will you teach us how to buy LEAPS?

A: Just go to my website, type in LEAPS in all caps, and everything you need to know about leaps is there. I will also be following up soon with more individual stock LEAPS ideas, but I don’t want to put them out now because we have just had a $5,000-point rally on the Dow.

Q: Please talk about 5G.

A: The best play is Qualcomm (QCOM). They have a near-monopoly on a 5G chip which virtually the entire world has to buy. The stock has also held up incredibly well. Buy two-year LEAPS on Qualcomm with probably a $90 or $100 strike price.

Q: What level in the S&P do you think this will fail?

A: I think it will fail right around here, so that's why I have been adding on the short positions on every rally. We are exactly at halfway point between the February high and the March low, which is a perfect bear market rally.

Q: What’s the definition of the next big dip?

A: You give up the 5000-point rally we just had, and whether we give up 4000 or 6000 of it, at these kinds of conditions, 1000 points in the Dow (INDU) is a round lot, like the daily move. So, looking at the charts and these lows, it could be a $19,000, $18,000, or $17,000.

Q: Fundamentals may tell you the virus may be peaking, but the worst of the economy is yet to come.

A: True. Do all the markets follow fundamentals now? No, they will look at the virus numbers. Economic numbers are utterly meaningless and out of date here. I wouldn’t depend on them at all, just look at the new cases every day from the Johns Hopkins website, and that gives you a better buy signal than any economic indicator can.

Q: Are all the good shorts are over?

A: When I say shorts are over, from here you’re not going to get the 80% and 90% down moves that we have seen so far; those are gone. The reason I bought the 2X ProShares Ultra Short S&P 500 (SDS) is to play for the bottom end of the range, which could be down 2000 to 4000 points from here, and also to hedge the short volatility (VXX) puts that I already have. A rising market should make the (VXX) go down, and a falling market will make the (VXX) and the (SDS) go up. So, it's both a hedge and a view on a range of a market.

Q: Could the Federal Reserve buy shares?

A: Yes, they have done that already in Japan, with no success whatsoever in helping the economy, but I doubt the Fed will buy shares here. The government will take minority share ownerships in the troubled industries like the airlines, much like they did with (GM) and the top 20 banks during the 2008-09 crash and sell them later at huge profits. I don't expect them to go beyond that. The Fed here has too many other things to buy, like all of our different bond and money markets; those don't exist in other countries like Japan or Europe. Stocks are often the only thing they can buy, and in Japan’s case, they already own the entire government bond market, so they had nothing else left to buy besides stocks.

Q: How about buying Boeing (BA)?

A: I would buy Boeing LEAPS here, something like a $170-$180. If you’re going to make a 1,000% return on LEAPS on any one stock, it's going to be Boeing. That company will be around somehow, and you could get literally a 10-fold return just by going 50% out of the money on two-year LEAPS.

Q: How is liquidity on 2-year 30% out of the money LEAPS?

A: It is practically nonexistent. You have to put in a limit order and then wait for a dump in the market to get filled. That’s how all the people who have been doing LEAPS have been getting them. Put in a bid and when you get these cataclysmic, down-1,000-point days, they hit any bid. The algos go in there and they just say hit any bid, and you can get done at incredible prices in those situations.

Q: Are the fees on (SDS) a problem?

A: No, your standard equity commission is all you should be paying. They trade like water.

Q: Would you short junk bonds short-term?

A: No, because you short the (HYG) or the (JNK), you are shorting a 7.5% yield which you have to pay if you’re short, so the great short in junk bond play was in February when it was yielding 4.5%. It’s too late now.

Q: Will treasuries go to zero?

A: They could, but we’re close enough to zero where you might as well think of them at zero.

Stay healthy all.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 9, 2020

Fiat Lux

Featured Trade:

(TEN LONG TERM LEAPS TO BUY AT THE BOTTOM)

(MSFT), (AAPL), (GOOGL), (QCOM), (AMZN),

(V), (AXP), (NVDA), (DIS), (TGT)

I am often asked how professional hedge fund traders invest their personal money. They all do the exact same thing. They wait for a market crash like we are seeing now, and buy the longest-term LEAPS (Long Term Equity Participation Securities) possible for their favorite names.

The reasons are very simple. The risk on LEAPS is limited. You can’t lose any more than you put in. At the same time, they permit enormous amounts of leverage.

Two years out, the longest maturity available for most LEAPS, allows plenty of time for the world and the markets to get back on an even keel. Recessions, pandemics, hurricanes, oil shocks, interest rate spikes, and political instability all go away within two years and pave the way for dramatic stock market recoveries.

You just put them away and forget about them. Wake me up when it is 2022.

I put together this portfolio using the following parameters. I set the strike prices just short of the all-time highs set two weeks ago. I went for the maximum maturity. I used today’s prices. And of course, I picked the names that have the best long-term outlooks.

You should only buy LEAPS of the best quality companies with the rosiest growth prospects and rock-solid balance sheets to be certain they will still be around in two years. I’m talking about picking up Cadillacs, Rolls Royces, and even Ferraris at fire sale prices. Don’t waste your money on speculative low-quality stocks that may never come back.

If you buy LEAPS at these prices and the stocks all go to new highs, then you should earn an average 131.8% profit from an average stock price increase of only 17.6%.

That is a staggering return 7.7 times greater than the underlying stock gain. And let’s face it. None of the companies below are going to zero, ever. Now you know why hedge fund traders only employ this strategy.

There is a smarter way to execute this portfolio. Put in throw-away crash bids at levels so low they will only get executed on the next cataclysmic 1,000-point down day in the Dow Average.

You can play around with the strike prices all you want. Going farther out of the money increases your returns, but raises your risk as well. Going closer to the money reduces risk and returns, but the gains are still a multiple of the underlying stock.

Buying when everyone else is throwing up on their shoes is always the best policy. That way, your return will rise to ten times the move in the underlying stock.

If you are unable or unwilling to trade options, then you will do well buying the underlying shares outright. I expect the list below to rise by 50% or more over the next two years.

Enjoy.

Microsoft (MSFT) - March 18 2022 $180-$190 bull call spread at $2.67 delivers a 274% gain with the stock at $190, up 16% from the current level. As the global move online vastly accelerates the world is clamoring for more computers and laptops, 90% of which run Microsoft’s Windows operating system. The company’s new cloud present with Azure will also be a big beneficiary.

Apple (AAPL) – June 17 2022 $210-$220 bull call spread at $6.47 delivers a 55% gain with the stock at $226, up 14% from the current level. With most of the world’s Apple stores now closed, sales are cratering. That will translate into an explosion of new sales in the second half when they reopen. The company’s online services business is also exploding.

Alphabet (GOOGL) – January 21 2022 $1,500-$1,520 bull call spread at $7.80 delivers a 28% gain with the stock at $226, up 14% from the current level. Global online searches are up 30% to 300%, depending on the country. While advertising revenues are flagging now, they will come roaring back

QUALCOMM (QCOM) – January 21 2022 $90-$95 bull call spread at $1.55 delivers a 222% gain with the stock at $95, up 23% from the current level. We are on the cusp of a global 5G rollout and almost every cell phone in the world is going to have to use one of QUALCOMM’s proprietary chips.

Amazon (AMZN) – January 21 2022 $2,100-$2,150 bull call spread at $17.92 delivers a 179% gain with the stock at $2,150, up 15% from the current level. If you thought Amazon was taking over the world before, they have just been given a turbocharger. Much of the new online business is never going back to brick and mortar.

Visa (V) – June 17 2022 $205-$215 bull call spread at $3.75 delivers a 166% gain with the stock at $215, up 16% from the current level. Sales are down for the short term but will benefit enormously from the mass online migration of new business only. They are one of a monopoly of three.

American Express (AXP) – June 17 2022 $130-$135 bull call spread at $1.87 delivers a 167% gain with the stock at $135, up 28% from the current level. This is another one of the three credit card processors in the monopoly, except they get to charge much higher fees.

NVIDIA (NVDA) – September 16 2022 $290-$310 bull call spread at $6.90 delivers a 189% gain with the stock at $310, up 19% from the current level. They are the world’s leader in graphics card design and manufacturing used on high-end PCs, artificial intelligence, and gaining. They befit from the soaring demand for new computers and the coming shortage of chips everywhere.

Walt Disney (DIS) – January 21 2022 $140-$150 bull call spread at $2.55 delivers a 55% gain with the stock at $116, up 31% from the current level. How would you like to be in the theme park, hotel, and cruise line business right now? It’s in the price. Its growing Disney Plus streaming service will make (DIS) the next Netflix.

Target (TGT) – June 17 2022 $125-$130 bull call spread at $1.40 delivers a 257% gain with the stock at $130, up 16% from the current level. Some store sales are up 50% month on month and lines are running around the block. Their recent online growth is also saving their bacon.

Mad Hedge Technology Letter

March 23, 2020

Fiat Lux

Featured Trade: (THE CORONA DRAG ON 5G)

(VZ), (T), (AAPL), (NFLX), (NVDA), (XLNX), (QRVO), (QCOM)