Global Market Comments

May 15, 2019

Fiat Lux

(SPECIAL CHINA ISSUE)

Featured Trade:

(WHY CHINA IS DRIVING UP THE VALUE OF YOUR TECH STOCKS)

(QCOM), (AVGO), (AMD), (MSFT), (GOOGL), (AAPL), (INTC), (LSCC)

Global Market Comments

May 15, 2019

Fiat Lux

(SPECIAL CHINA ISSUE)

Featured Trade:

(WHY CHINA IS DRIVING UP THE VALUE OF YOUR TECH STOCKS)

(QCOM), (AVGO), (AMD), (MSFT), (GOOGL), (AAPL), (INTC), (LSCC)

Reduce the supply on any commodity and the price goes up. Such is dictated by the immutable laws of supply and demand.

This logic applies to technology stocks as well as any other asset. And the demand for American tech stocks has gone global.

Who is pursuing American technology more than any other? That would be China.

Ray Dalio, founder and chairman of hedge fund Bridgewater Associates, described the first punch thrown in an escalating trade war as a “tragedy,” although an avoidable one.

Emotions aside, the REAL dispute is not over steel, aluminum, which have a minimal effect of the US economy, but rather about technology, technology, and more technology.

China and the U.S. are the two players in the quest for global tech power and the winner will forge the future of technology to become chieftain of global trade.

Technology also is the means by which China oversees its population and curbs negative human elements such as crime, which increasingly is carried out through online hackers.

China is far more anxious about domestic protest than overseas bickering which is reflected in a 20% higher internal security budget than its entire national security budget.

You guessed it: The cost is predominantly and almost entirely in the form of technology, including CCTVs, security algorithms, tracking devices, voice rendering software, monitoring of social media accounts, facial recognition, and cloud operation and maintenance for its database of 1.3 billion profiles that must be continuously updated.

If all this sounds like George Orwell’s “1984”, you’d be right. The securitization of China will improve with enhanced technology.

Last year, China’s communist party issued AI 2.0. This elaborate blueprint placed technology at the top of the list as strategic to national security. China’s grand ambition, as per China’s ruling State Council, is to cement itself as “the world’s primary AI innovation center” by 2030.

It will gain the first-mover advantage to position its academia, military and civilian areas of life. Centrally planned governments have a knack for pushing through legislation, culminating with Beijing betting the ranch on AI 2.0.

China possesses legions of engineers, however many of them lack common sense.

Silicon Valley has the talent, but a severe shortage of coders and engineers has left even fewer scraps on which China’s big tech can shower money.

Attempting to lure Silicon Valley’s best and brightest also is a moot point considering the distaste of operating within China’s great firewall.

In 2013, former vice president and product spokesperson of Google’s Android division, Hugo Barra, was poached by Xiaomi, China’s most influential mobile phone company.

This audacious move was lauded and showed China’s supreme ability to attract Silicon Valley’s top guns. After 3 years of toiling on the mainland, Barra admitted that living and working in Beijing had “taken a huge toll on my life and started affecting my health.” The experiment promptly halted, and no other Silicon Valley name has tested Chinese waters since.

Back to the drawing board for the Middle Kingdom…

China then turned to lustful shopping sprees of anything tech in any developed country.

Midea Group of China bought Kuka AG, the crown jewel of German robotics, for $3.9 billion in 2016. Midea then cut German staff, extracted the expertise, replaced management with Chinese nationals, then transferred R&D centers and production to China.

The strategy proved effective until Fujian Grand Chip was blocked from buying Aixtron Semiconductors of Germany on the recommendation of CFIUS (Committee on Foreign Investment in the United States).

In 2017, America’s Committee on Foreign Investment and Security (CFIUS), which reviews foreign takeovers of US tech companies, was busy refusing the sale of Lattice Semiconductor, headquartered in Portland, Ore., and since has been a staunch blockade of foreign takeovers.

CFIUS again in 2018 put in its two cents in with Broadcom’s (AVGO) attempted hostile takeover of Qualcomm (QCOM) and questioned its threat to national security.

All these shenanigans confirm America’s new policy of nurturing domestic tech innovation and its valuable leadership status.

Broadcom, a Singapore-based company led by ethnic Chinese Malaysian Hock Tan, plans to move the company to Delaware, once approved by shareholders, as a way to skirt around the regulatory issues.

Microsoft (MSFT) and Alphabet (GOOGL) are firmly against this merger as it will bring Broadcom intimately into Apple’s (APPL) orbit. Broadcom supplies crucial chips for Apple’s iPads and iPhones.

Qualcomm will equip Microsoft’s brand-new Windows 10 laptops with Snapdragon 835 chips. AMD (AMD) and Intel (INTC) lost out on this deal, and Qualcomm and Microsoft could transform into a powerful pair.

ARM, part of the Softbank Vision Fund, is providing the architecture on which Qualcomm’s chips will be based. Naturally, Microsoft and Google view an independent operating Qualcomm as healthier for their businesses.

The demand for Qualcomm products does not stop there. Qualcomm is famous for spending heavily on R&D — higher than industry peers by a substantial margin. The R&D effort reappears in Qualcomm products, and Qualcomm charges a premium for its patent royalties in 3G and 4G devices.

The steep pricing has been a point of friction leading to numerous lawsuits such as the $975 million charged in 2015 by China’s National Development and Reform Commission (NDRC) which found that Qualcomm violated anti-trust laws.

Hock Tan has an infamous reputation as a strongman who strips company overhead to the bare bones and runs an ultra-lean ship benefitting shareholders in the short term.

CFIUS regulators have concerns with this typical private equity strategy that would strip capabilities in developing 5G technology from Qualcomm long term. 5G is the technology that will tie AI and chip companies together in the next leg up in tech growth.

Robotic and autonomous vehicle growth is dependent on this next generation of technology. Hollowing out CAPEX and crushing the R&D budget is seriously damaging to Qualcomm’s vision and hampers America’s crusade to be the undisputed torchbearer in revolutionary technology.

CFIUS’s review of Broadcom and Qualcomm is a warning shot to China. Since Lattice Semiconductor (LSCC) and Moneygram (MGI) were out of the hands of foreign buyers, China now must find a new way to acquire the expertise to compete with America.

Only China has the cash hoard to take a stand against American competition. Europe has been overrun by American FANGs and is solidified by the first mover advantage.

Shielding Qualcomm from competition empowers the chip industry and enriches Qualcomm’s profile. Chips are crucial to the hyper-accelerating growth needed to stay at the top of the food chain.

Implicitly sheltering Qualcomm as too important to the system is an ink-drenched stamp of approval from the American government. Chip companies now have obtained insulation along with the mighty FANGs. This comes on the heels of Goldman Sachs (GS) reporting a lack of industry supply for DRAM chips, causing exorbitant pricing and pushing up semiconductor companies’ shares.

All the defensive posturing has forced the White House to reveal its cards to Beijing. The unmitigated support displayed by CFIUS is extremely bullish for semiconductor companies and has been entrenched under the stock price.

It is likely the hostile takeover will flounder, and Hock Tan will attempt another round of showmanship after Broadcom relocates to Delaware as an official American company paying American corporate tax. After all, Tan did graduate from MIT and is an American citizen.

The chip companies are going through another intense round of consolidation as AMD (AMD) was the subject of another takeover rumor which lifted the stock. AMD is the only major competitor with NVIDIA (NVDA) in the GPU segment.

The cash repatriation has created liquid buyers with a limited amount of quality chip companies. Qualcomm is a firm buy, and investors can thank Broadcom for showing the world the supreme value of Qualcomm and how integral this chip stalwart is to America’s economic system.

Mad Hedge Technology Letter

May 14, 2019

Fiat Lux

Featured Trade:

(CHINA’S COUNTERATTACK)

(AAPL), (MSFT), (ADBE), (PYPL), (QCOM), (MU), (JD), (BABA), (BIDU)

Ratcheting up the trade tensions, China is pulling the trigger on retaliatory tariffs on $60 billion worth of U.S. goods, just days after the American administration said it would levy higher tariffs on $200 billion in Chinese goods.

American President Donald Trump accused China of reneging on a “great deal.”

The mushrooming friction between the two superpowers gives even more credence to my premise that hardware stocks should be avoided like the plague.

I have stood out on my perch in 2019 and proclaimed to buy software stocks and if you need one name to hide out in then I would confidently choose Microsoft (MSFT).

Microsoft has little exposure to China and will be rewarded the most on a relative basis.

The last place you want to get caught out is buying hardware stocks exposed to China and Apple is quickly turning into the largest piece of collateral damage along with airplane manufacturer Boeing.

Remember that 20% of Apple’s revenue comes from China and Apple bet big to solidify a complex supply chain through Foxconn Technology Group in China.

When history is recorded, CEO of Apple Tim Cook not hedging his bets exposing Apple’s revenue machine could go down as one of the worst ever managerial decisions by tech management.

The forced intellectual property transfers in China from western corporations was the worst kept secret in corporate America.

Being an operational guru as he is, and the hordes of data that Apple have access to, this was a no brainer and Cook should have mitigated his risks by investing in a supply chain that was partially outside of China, and not incrementally spreading out the supply chain through other parts of Asia is coming back to bite him.

China's most recent tariffs will come into effect on June 1, adding up to 25% to the cost of U.S. goods that are covered by the new policy from China's State Council Customs Tariff Commission.

The result of these newly minted tariffs is that importers will probably elect to avoid absorbing the costs themselves and pass the price hikes to the consumer sapping demand.

The American consumer still retains its place as the holy grail of the American economic bull case, but this will test the thesis.

For the short term, it would be foolish to hang out to Chinese companies listed in New York through American depository receipts (ADR) such as JD.com (JD), Alibaba (BABA).

Baidu (BIDU) is a company that I am flat out bearish on because of a weakening strategic position versus Alibaba and Tencent in China.

Even with no trade war, I would tell investors to short Baidu, and the chart is nothing short of disgusting.

Wei Jianguo, a former vice-minister at the Chinese Ministry of Commerce who handled foreign trade, said to the South China Morning Post that “China will not only act as a kung fu master in response to U.S. tricks but also as an experienced boxer and can deliver a deadly punch at the end.”

It is clear that any goodwill between the two heavyweight powers has evaporated and the hardliners inside the communist party pulled all the levers possible to back out at the last second.

Many of us do not understand, but there is a complicated political game perpetuating inside the Chinese communist party pitting reformists against staunch traditionalists.

This is not only Chairman Xi’s decision and appearing weak on the global stage is the last concession the communist government will subscribe to.

Along with the iPhone company, semiconductor stocks will be ones to avoid.

The list starts out with the chip companies leveraged the most to Chinese revenue as a proportion of total sales including Qualcomm (QCOM) with 65% of revenue in China, Micron (MU) who has 57% of sales in China, Qorvo who has half of sales from China, Broadcom who has 48% of sales from China, and Texas Instruments rounding out the list with 43% of total revenue from China.

The first 5 months of the year saw constant chatter that the two sides would kiss and makeup and chip stocks benefitted from that tsunami of positive momentum.

The picture isn’t as pretty when you flip the script, and chip stocks could suffer a gut-wrenching summer if the two sides drift further apart.

After Microsoft, other software names I would take comfort in with the added bonus of strong balance sheets are Veeva Systems (VEEV), PayPal (PYPL), and Adobe (ADBE).

The new tariffs will burden American households to up to $2 billion per month going forward, and new purchases for discretionary items like extra electronics will be put on the back burner extending the refresh cycle and saddling chip companies and Apple with a glut of iPhone and chip inventory.

Buy software companies on the dip.

Mad Hedge Technology Letter

April 24, 2019

Fiat Lux

Featured Trade:

(WHO BEAT WHOM IN THE APPLE/QUALCOMM BATTLE)

(QCOM), (INTC), (AAPL)

The 5G bonanza is slithering towards us in a slow yet predictable motion – that was the takeaway from Apple finally conceding that its bargaining positioning was weaker than initially thought.

Apple made amends with chipmaker Qualcomm (QCOM) in the nick of time, let me explain.

Qualcomm is the leader of 5G chip technology, and the two firms decided on a six-year pact that will allow Qualcomm to sell patent licensing to Apple while becoming a crucial supplier of 5G modems to the new iPhone that will roll-out to consumers in the back half of 2020.

Envisioning this 2 for 1 special a few weeks ago was impossible as the brouhaha spilled over into the national media with top executives exchanging barbs.

Qualcomm, to its credit, stayed steadfast on its position and was the bigger winner of the spat.

The rapid reaction in the stock price has vindicated Qualcomm’s initial reluctance to make a cut-price deal with Apple.

The new contract locks in Apple at around $9 per phone in licensing fees, almost double what many analysts were predicting.

Apple also paid a one-time fee of the backlog of patent usage from the past two years that many specialists estimate to be in the $6 billion range.

Qualcomm has previously stated that Apple owes them $7 billion from the kerfuffle and Apple’s refusal to pay stemmed from their belief that Qualcomm was “double dipping” – a claim based on Qualcomm charging a fee for each iPhone using its patents as well as a fee for the technology itself which Apple felt extortionate.

Ultimately, the jousting wasn’t worth the trouble as the best-case scenario of Apple saving $1 billion in patent fees was overshadowed by the opportunity cost which was significantly higher.

The updated terms see a substantial improvement for Qualcomm over the $7.50 per phone that Apple was paying before.

The end of the saga smells of desperation on CEO of Apple Tim Cook’s behalf, realizing that time was ticking down and competitors such as Huawei have already launched 5G-supported phones.

Apple is, in fact, late to the party and one of the main root causes was the logjam with Qualcomm.

If Apple didn’t come to terms with Qualcomm, suppliers and designers wouldn’t have enough time or supply to prepare to meet the fall 2020 deadline causing Apple to delay the new iPhone.

The worst-case scenario that became a realistic threat was that the new iPhone wouldn’t have been ready until 2021 – Apple shares would have dropped 20% in a heartbeat if this played out.

Avoiding this doomsday scenario is a massive bullish signal for Apple shares and brings forward revenue demand into 2020.

The new iPhone with ironically Qualcomm’s 5G modem technology is also the selling point for iPhone lovers to upgrade to a newer and faster iPhone iteration.

It’s a headscratcher that Tim Cook played his cards in the way that he did, another misstep in a long record of fumbles in the red zone.

Inevitably, scrunching up the production schedule heaps loads of pressure on the existing engineering teams to produce a flawless iPhone.

Apple simply couldn’t wait any longer and CEO of Qualcomm Steven Mollenkopf understood that, leading me to solely blame Tim Cook for this calculated error.

Where do the chips lie after this recent shakeout?

First, this piece of news is demonstrably bullish for Qualcomm and its business model while backloading around $6 billion or so in revenue onto its balance sheet.

In short, Qualcomm hit it out of the park and set itself up for the upcoming insatiable demand for 5G chips while publicly demonstrating they are best in show for 5G infrastructure equipment.

It might turn out to be Qualcomm’s best day in the history of the company and one that employees will never forget inside its headquarters.

This will embolden Qualcomm in the future to fight for the revenue that is rightfully theirs and they won’t be frightened by bigger sharks attempting to persuade them that they should receive a lesser share of the pie.

For Mollenkopf, this is his crowning moment and a pathway to another big-time job, the one day grabbing of the spoils has elevated his reputation.

Apple is a minor winner because of the adequate supply of chips that Qualcomm will provide that guarantees Apple’s engineers clarity instead of dragging itself deeper into a courtroom battle with a company that supplies an integral component to their iPhone.

Hours after the news hit the press, Intel (INTC) waived the white flag issuing a short response admitting they are exiting the 5G smartphone business, a bitter pill to swallow for a legacy company finding it difficult to stay with the big boys.

And if you remember, Intel was initially thought to be the one to provide memory to the 5G smartphone but now that notion is dead as a doornail.

Intel will hope they can capture a fair share of the 5G PC business to make up for the lost opportunity, but as consumers migrate away from PCs, shareholders could sense Intel could be left holding the bag.

Qualcomm has strengthened its stranglehold on the 5G smartphone modem market in an industry that will morph into a worldwide addressable market of $20 billion by 2025.

Even though Huawei just announced they would be willing to sell their 5G chips to Apple, Huawei and South Korea’s Samsung mainly produce chips for their in-house branded smartphones and shun feeding competitors like Apple who require the same chips.

Apple hoped to create some leveraging power to get a better 5G chip deal and loosen the jaws that gave Qualcomm a powerful position over Apple, but Intel quitting this segment left Apple with a series of bad choices and they chose the lesser of the evils.

What does this boil down to?

Qualcomm outmuscled Intel producing faster and better performing chips that supported longer battery life.

Qualcomm simply has better engineering talent.

Intel had an uphill battle in the first place, but it is clear they cut their losses because the writing was on the wall leaving Qualcomm to reap all the benefits.

Global Market Comments

April 23, 2019

Fiat Lux

Featured Trade:

(LAS VEGAS MAY 9 GLOBAL STRAGEGY LUNCHEON)

(APRIL 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXI), (RWM), (IWM), (VXXB), (VIX), (QCOM), (AAPL), (GM), (TSLA), (FCX), (COPX), (GLD), (NFLX), (AMZN), (DIS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 17 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What will the market do after the Muller report is out?

A: Absolutely nothing—this has been a total nonmarket event from the very beginning. Even if Trump gets impeached, Pence will continue with the same kinds of policies.

Q: If we are so close to the peak, when do we go short?

A: It’s simple: markets can remain irrational longer than you can remain liquid. Those shorts are expensive. As long as global excess liquidity continues pouring into the U.S., you’ll not want to short anything. I think what we’ll see is a market that slowly grinds upward until it’s extremely overbought.

Q: China (FXI) is showing some economic strength. Will this last?

A: Probably, yes. China was first to stimulate their economy and to stimulate it the most. The delayed effect is kicking in now. If we do get a resolution of the trade war, you want to buy China, not the U.S.

Q: Are commodities expected to be strong?

A: Yes, China stimulating their economy and they are the world’s largest consumer commodities.

Q: When is the ProShares Short Russell 2000 ETF (RWM) actionable?

A: Probably very soon. You really do see the double top forming in the Russell 2000 (IWM), and if we don’t get any movement in the next day or two, it will also start to roll over. The Russell 2000 is the canary in the coal mine for the main market. Even if the main market continues to grind up on small volume the (IWM) will go nowhere.

Q: Why do you recommend buying the iPath Series B S&P 500 VIX Short Term Futures ETN (VXXB) instead of the Volatility Index (VIX)?

A: The VIX doesn’t have an actual ETF behind it, so you have to buy either options on the futures or a derivative ETF. The (VXXB), which has recently been renamed, is an actual ETF which does have a huge amount of time decay built into it, so it’s easier for people to trade. You don’t need an option for futures qualification on your brokerage account to buy the (VXXB) which most people don’t have—it’s just a straight ETF.

Q: So much of the market cap is based on revenues outside the U.S., or GDP making things look more expensive than they actually are. What are your thoughts on this?

A: That is true; the U.S. GDP is somewhat out of date and we as stock traders don’t buy the GDP, we buy individual stocks. Mad Hedge Fund Trader in particular only focuses on the 5% or so—stocks that are absolutely leading the market—and the rest of the 95% is absolutely irrelevant. That 95% is what makes up most of the GDP. A lot of people have actually been caught in the GDP trap this year, expecting a terrible GDP number in Q1 and staying out of the market because of that when, in fact, their individual stocks have been going up 50%. So, that’s something to be careful of.

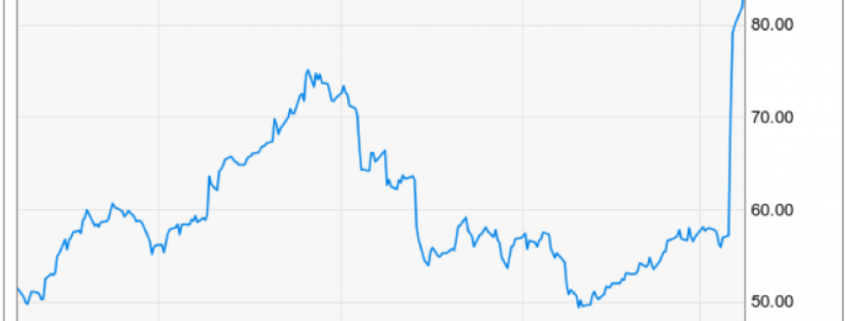

Q: Is it time to jump into Qualcomm (QCOM)?

A: Probably, yes, on the dip. It’s already had a nice 46% pop so it’s a little late now. The battle with Apple (AAPL) was overhanging that stock for years.

Q: Will Trump next slap tariffs on German autos and what will that do to American shares? Should I buy General Motors (GM)?

A: Absolutely not; if we do slap tariffs on German autos, Europe will retaliate against every U.S. carmaker and that would be disastrous for us. We already know that trade wars are bad news for stocks. Industry-specific trade wars are pure poison. So, you don't want to buy the U.S. car industry on a European trade war. In fact, you don’t want to buy anything. The European trade war might be the cause of the summer correction. Destroying the economies of your largest customers is always bad for business.

Q: How much debt can the global economy keep taking on before a crash?

A: Apparently, it’s a lot more with interest rates at these ridiculously low levels. We’re in uncharted territory now. We really don't know how much more it can take, but we know it’s more because interest rates are so low. With every new borrowing, the global economy is making itself increasingly sensitive to any interest rate increases. This is a policy you should enact only at bear market bottoms, not bull market tops. It is borrowing economic growth from futures year which we may not have.

Q: Is the worst over for Tesla (TSLA) or do you think car sales will get worse?

A: I think car sales will get better, but it may take several months to see the actual production numbers. In the meantime, the burden of proof is on Tesla. Any other surprises on that stock could see us break to a new 2 year low—that's why I don’t want to touch it. They’ve lately been adopting policies that one normally associates with imminent recessions, like closing most of their store and getting rid of customer support staff.

Q: Is 2019 a “sell in May and go away” type year?

A: It’s really looking like a great “Sell in May” is setting up. What’s helping is that we’ve gone up in a straight line practically every day this year. Also, in the first 4 months of the year, your allocations for equities are done. We have about 6 months of dead territory to cover from May onward— narrow trading ranges or severe drops. That, by the way, is also the perfect environment for deep-in-the-money put spreads, which we plan to be setting up soon.

Q: Is it time to buy Freeport McMoRan (FCX) in to play both oil and copper?

A: Yes. They’re both being driven by the same thing: China demand. China is the world’s largest new buyer of both of these resources. But you’re late in the cycle, so use dips and choose your entry points cautiously. (FCX) is not an oil play. It is only a copper (COPX) and gold (GLD) play.

Q: Are you still against Bitcoin?

A: There are simply too many better trading and investment options to focus on than Bitcoin. Bitcoin is like buying a lottery ticket—you’re 10 times more likely to get struck by lightning than you are to win.

Q: Are there any LEAPS put to buy right now?

A: You never buy a Long-Term Equity Appreciation Securities (LEAPS) at market tops. You only buy these long-term bull option plays at really severe market selloffs like we had in November/December. Otherwise, you’ll get your head handed to you.

Q: What is your outlook on U.S. dollar and gold?

A: U.S. dollar should be decreasing on its lower interest rates but everyone else is lowering their rates faster than us, so that's why it’s staying high. Eventually, I expect it to go down but not yet. Gold will be weak as long as we’re on a global “RISK ON” environment, which could last another month.

Q: Is Netflix (NFLX) a buy here, after the earnings report?

A: Yes, but don't buy on the pop, buy on the dip. They have a huge head start over rivals Amazon (AMZN) and Walt Disney (DIS) and the overall market is growing fast enough to accommodate everyone.

Q: Will wages keep going up in 2019?

A: Yes, but technology is destroying jobs faster than inflation can raise wages so they won’t increase much—pennies rather than dollars.

Q: How about buying a big pullback?

A: If we get one, it would be in the spring or summer. I would buy a big pullback as long as the U.S. is hyper-stimulating its economy and flooding the world with excess liquidity. You wouldn't want to bet against that. We may not see the beginning of the true bear market for another year. Any pullbacks before that will just be corrections in a broader bull market.

Good Luck and Good Trading

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

If you can’t handle the heat, then get out of the kitchen.

Well, the kitchen is getting a little bit toasty right now.

Apple (AAPL) was handed down a demonstrably negative verdict when a regional Chinese court ruled that they infringed on two patents belonging to Qualcomm (QCOM).

The Qualcomm chips were connected to photo editing and another to swiping on a touch-screen device.

This means that Apple won’t be able to sell legacy iPhone models in China which is a damaging blow to revenue prospects because older iPhone models in China offer attractive price points to wallet-light Chinese.

And when you add this all up, the ban includes over half of the iPhones on sale in China.

In general, less affordable, sleeker, fresher iterations price out many Chinese who want a piece of the Apple dream.

Even though this was a nice victory for Qualcomm, it spells trouble for the broader tech sector.

Apple’s myriad of chip suppliers who have grappled with a torrent stream of woeful news this year relating to Apple’s supply of iPhones and supply forecast of iPhones are first on the chopping block.

It’s also an excruciating blow to American business in China and this could potentially rule out any American management taking future business trips to China.

Apple looks set to join its chip company compadres on the sidelines as a stock to avoid like the plague at the moment.

Apple is a great company and a perfect hold to eternity stock, but this is not the time to jump in and out of it.

Let me explain why.

The trade war centered on future technological hegemony is directly connected to the domination of current technology in artificial intelligence, chip development, and 5G.

China has been furiously catching up to American tech the last two decades through its vast program of foreign technological forced transfers and outright intellectual property theft.

I remember testing my first shoddy Chinese smartphone from the Chinese company Coolpad to gauge a sample of the burgeoning Chinese consumer device market on a blistering hot day in Beijing in the summer of 2010.

It was one of the first iterations of Chinese smartphones on the local market and the 3G smartphone was simply terrible.

The hardware was iffy, software was untenable, design was hodgepodge and it ceased working after 3 painstaking months of testing.

I breathed a sigh of relief because I knew it would be years before Chinese tech could ever produce something material.

Since then, China and the love given to its tech sector through the state protecting its homegrown companies have come a long way since those teething years filled with shabby products and inferior expertise of yesteryear.

Chinese cell phones are now comparable to iPhones for a fraction of the cost especially the new Huawei and Xiaomi models and the companies want recognition for their success.

I have interviewed scores of Huawei engineers who describe a life of grinding out a modest existence in mega-cities dotted around China.

They lament the 12-hour back-breaking work days, suffocating authoritarian management style, and the 3am on-call staff meetings, but they rejoice in the accomplishment of collecting that down payment for a standard Chinese apartment in a subpar constructed building.

They earn 30% of what Apple engineers make per year just to seize an average life in a second-tier Chinese city.

They don’t complain and accept it as a consequence of cut-throat competition in a country of 1.3 billion trying to hustle the best they can.

These unbearable timelines and the crunch to develop the national brand of Huawei and its other protected tech behemoths is how China rose up from the ashes of irrelevancy to become arguably competitive with the American tech machine that is Silicon Valley.

Even through all of the local hyper-growth, there was one unwritten rule that allowed one squeaky clean American company from Cupertino to evade all of the fractious competition and make an absolute killing in China.

Apple was protected in China before until now that is.

I find it dubious that the timing of the court verdict was the first business day after the arrest of CFO of Huawei Meng Wanzhou.

By connecting the dots, this appears as if it was an indirect ruling from the higher-ups signaling that Apple won’t be handed a free pass anymore and a warning shot fired to Washington.

Even worse, the Chinese regulatory environment is opaque at best-giving discretion to Chinese authorities to do as they see fit.

The opaque nature of Chinese regulation can draw out cases for years potentially drowning out the sales of iPhones and banishing Apple and its products in China to the history books.

That is the worst-case scenario that probably won’t happen.

For Apple to even appeal this ruling offers Steve Jobs' brainchild a rare dose of reality in China, and the bruised Apple brand will go back to the drawing board after receiving severe harm to its previous image of an ultra-luxury brand on the Chinese mainland.

For other American companies, there is no way to flush out additional clarity, and they will get stonewalled if they want more details regarding the path forward and that in itself will damage the price action of stocks tilted towards China because of the wave of uncertainty.

At the extreme minimum, this escalation of pressure will make it arduous to maneuver to some sort of trade agreement let alone in the abbreviated 90-day window agreed on in Buenos Aires.

The Chinese national psyche cares a great deal about saving face and this dig at its national prize will be hard to forget.

And China has a habit at looking at these types of events as inclusive actions tallied up broadly inside a comprehensive portfolio labeled and pigeonholed as America, Canada, and so on.

This conspicuous move has pushed forward Canada into the forefront of the firing line which could become the silver lining to this quagmire because Canada will have more incentive to join in on the China rebukes with America if they get blacklisted by Beijing.

Uniting together as one pan-North American and the European task force would be the best method to combat China’s stealthy business acumen whose capital and influence are far-flung and hard to quantify because of its various gateways to global western pressure points.

I can tell you right now that after doing a quick jaunt of Belarus, the Ukraine, and Hungary this winter, China’s deep pockets and nationals have completely taken over Central and Eastern Europe.

Chinese companies and products are plastered all over the place in each Russified city center and cityscapes built in the Soviet era.

Chinese students and workers have flooded these markets as they line up around the fringes of the Western world armed with gobs of capital and a land-grab mentality that borders Amazon’s ambition.

The Budapest property market has been cornered by Chinese citizens looking for the cheapest entry point to permanent residence in the Eurozone.

If you want to rent a flat in Budapest, odds are a Chinese owner will be glad to accept your monthly rent payments.

China believes that to truly have its tentacles deep inside the Western apparatus, they must initially corner the peripheries of the Western World that thirst for capital to build up local economies to match the power and stature of the Western big boys.

This has all added up to the Chinese government having an influential voice in European affairs because they have direct sway with conservative Prime Minister of Hungary Viktor Orban who has accepted Chinese capital.

US executives are praying to the celestial heavens that Meng is not extradited to America and made the scapegoat of the broader trade war.

This would be a bitter pill to swallow for Huawei’s founder Ren Zheng Fei whose family is considered royalty inside the upper-level Chinese establishment.

I assume that Ren will not back down quietly and is pushing and pulling the behind-the-scenes levers to do what he can for his daughter.

What does this all mean?

Headline risk has shot through the roof and investors could hear any day of the rumblings to the next chapter of the trade saga that is enveloping more and more corporate collateral damage.

Apple’s next quarter’s earnings are also on the line, and CEO of Apple Tim Cook could conveniently use it as a throwaway quarter hyping its progression as a new software and subscriptions company which is indeed in the works.

I figure this is the base case for Apple especially if there is no quick solution to this new iPhone ban.

The transition has been dramatically painful and happened a year or two too early for Apple’s liking.

Consequently, Apple reigning in its expectations has crushed the stock recently.

Certain global banks could set to be punished after the Wall Street Journal reported that HSBC and Standard Chartered facilitated the illegal payments for Huawei.

The British bank problems don’t stop there with Britain as a country barreling towards a complete ban of Huawei products after New Zealand just announced their own ban.

The three biggest Japanese telecommunication companies dumped fuel on Huawei’s bonfire citing security issues for excluding Huawei products from Japanese 5G development.

The roller-coaster action could also give impetus to Chairman Xi to execute a power grab on Chinese domestic technology sector gifting him additional control over tech behemoths in the name of national security fortifying his multiplying power in China.

He did the same with the People Liberation’s Army and I see no reason why he wouldn’t do the same with the Chinese tech sector especially if western countries avoid Huawei products.

The Chinese regulatory presence has already reared its ugly head banning new video game licenses to Tencent slashing revenue streams in 2018.

That is why Tencent shares have grossly underperformed this year.

Theoretically, Xi could use this moment as a springboard to seize the reigns of Huawei citing illegal payments to Iran which would calm the trade tensions but beef up his clout in the tech community, a net negative for Silicon Valley.

In any case, there is substantial amount of uncertainty permeating the heart of the technology movement that could potentially splinter off violently into an American tech and Chinese tech world.

This hard landing would deprive China-based revenue and kill supply chains for American technology that have spent decades procuring these intricate systems.

For Chinese technology, they could be cut off from the important components required to develop the technology and chips they need to achieve its “Made in China 2025” state-subsidized targets aimed at rapidly expanding its high-tech sectors and developing its advanced manufacturing base.

The next few months will reshape the 2019 Silicon Valley landscape and certain companies are hoping their business models aren’t fully destroyed.

I can’t lie but I saw this coming when I became aware of the complicated relationship between foreign tech companies and its precious Chinese revenue, and I also never bought another Coolpad smartphone.

Mad Hedge Technology Letter

November 13, 2018

Fiat Lux

Featured Trade:

(NO BIWEEKLY STRATEGY WEBINAR FOR WEDNESDAY NOVEMBER 14)

(WHY I HATE CHIP STOCKS)

(AAPL), (CY), (TXN), (LRCX), (KLAC), (LITE), (QCOM), (MU), (SWKS), (LSCC)