Global Market Comments

January 22, 2021

Fiat Lux

Featured Trade:

(JANUARY 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (IWM), (SPY), (ROM), (BRK/A), (AMZN), NVDA), (MU), (AMD), (UNG), (USO), (SLV), (GLD), ($SOX), CHIX), (BIDU), (BABA), (NFLX), (CHIX), ($INDU), (SPY), (TLT)

Tag Archive for: (QQQ)

Below please find subscribers’ Q&A for the January 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV.

Q: What will a significant rise in long term bond yields (TLT) do to PE ratios in general, and high tech specifically?

A: Well, the key question here is: what is “significant”. Is “significant” a move in a 10-year from 120 to 150, which may be only months off? I don’t think that will have any impact whatsoever on the stock market. I think to really give us a good scare on interest rates, you need to get the 10-year up to 3.0%, and that might be two years off. We’re also going to be testing some new ground here: how high can bond interest rates go while the Fed keeps overnight rates at 25 basis points? They can go up more, but not enough to hurt the stock market. So, I think we essentially have a free run on stocks for two more years.

Q: What about the Shiller price earnings ratio?

A: Currently, it’s 34.5X and you want to completely ignore anything from Shiller on stock prices. He’s been bearish on stocks for 6 years now and ignoring him is the best thing you can do for your portfolio. If you had listed to him, you would have missed the last 15,000 Dow ($INDU) points. Someday, he’ll be right, but it may be when the market goes from 50,000 to 40,000, so again, I haven't found the Shiller price earnings ratio to be useful. It’s one of those academic things that looks great on paper but is terrible in practice.

Q: Do you see any opportunity in China financials with the change of administration, like the (CHIX)?

A: I always avoid financials in China because everyone knows they have massive, defaulted loans on their books that the government refuses to force them to recognize like we do here. So, it’s one of those things where they look good on paper, but you dig deeper and find out why they’re really so cheap. Better to go with the big online companies like Baidu (BIDU) and Alibaba (BABA).

Q: Is it too late to enter copper?

A: No, the high in the last cycle for Freeport McMoRan (FCX) was $50 dollars and I think we’re only in the mid $ ’20s now, so you could get another double. Remember, these commodity stocks have discounted recovery that hasn’t even started yet. Once you do get an actual recovery, you could get another enormous move and that's what could take the Dow to 120,000.

Q: Do you see the FANGs coming back to life with the earnings results?

A: I think it'll take more than just Netflix to do that. By the way, Netflix (NFLX) is starting to look like the Tesla of the media industry, so I’d get into Netflix on the next dip. You could get a surprise, out-of-nowhere double out of that anytime. But yes, FANGs will come to life. They've been in a correction for five months now, and we’ll see—it may be the end of the pandemic that causes these stocks to really take off. So that's why I'm running the barbell portfolio and buying the FANGs on weakness.

Q: Are you recommending LEAPS on gold (GLD) and silver (SLV)?

A: Absolutely yes, go out two years with your maturity, you might buy 120% out of the money. That's where you get your leverage on the LEAPS. Something like a (GLD) January 2023 $210-$220 in-the-money vertical bull call spread and generate a 500% profit by expiration.

Q: Do you foresee a cool off for semiconductors ($SOX) even though there's been recent news of shortages?

A: No, not really. There are so many people trying to get into these it’s incredible. And again, we may get a time correction where we sideline at the top and then break out again to the upside. This is classic in liquidity-driven markets, which is what we have in spades right now. Thanks to 5G, the number of chips in your everyday devices is about to increase tenfold, and it takes at least two years to build a new chip factory. So, keep buying (NVDA), (MU), and (AMD) on dips.

Q: Where are the best LEAPS prospects (Long Term Equity Participation Securities)?

A: That would have to be in technology—that's where the earnings growth is. If you go 20% out of the money on just about any big tech LEAPs two years out, to 2023 those will be worth 500% more at expiration.

Q: What about SPACs (Special Purpose Acquisition Company) now, as we’re getting up to five new SPACs a day?

A: My belief is that a SPAC is a vehicle that allows a manager to take out a 20% a year management fee instead of only 1%. And it's another aspect of the current mania we’re in that a lot of these SPACs are doubling on the first day—especially the electric vehicle-related SPACs. Also, a lot of these SPACs will never invest in anything, but just take the money and give it back to you in two years with no return when they can't find any good investments…. If you’re lucky. There's not a lot of bargains to be found out there by anyone, including SPAC managers.

Q: Does natural gas (UNG) fall into the same “avoid energy” narrative as oil?

A: Absolutely, yes. The only benefit of natural gas is it produces 50% less carbon dioxide than oil. However, you can't get gas without also getting oil (USO), as the two come out of the pipe at the same time; so I would avoid natural gas also. Gas and oil are also about to lose a large chunk, if not all, of their tax incentives, like the oil depletion allowance, which has basically allowed the entire oil industry to operate tax-free since the 1930s.

Q: What about hydrogen cars?

A: I don't really believe in the technology myself, and when you burn hydrogen, that also produces CO2. The problem with hydrogen is that it’s not a scalable technology. It’s like gasoline—you have to build stations all over the US to fuel the cars. Of course, it produces far less carbon than gas or natural gas, but it is hard to compete against electric power, which is scalable and there's already a massive electric grid in place.

Q: If you inherited $4 million today, would you cost average into (QQQ), (IWM), or (SPY)?

A: I would go into the ProShares Ultra Technology ETF (ROM), which is double the (QQQ); and if you really want to be conservative, put half your money into (QQQ) or (ROM), and then half into Berkshire Hathaway (BRK/A), which is basically a call option on the industrial and recovery economy. I know plenty of smart people who are doing exactly that.

Q: Is it weird to see oil, as well as green energy stocks, moving up?

A: No, that's actually how it works. The higher oil and gas prices go, the more economical it is to switch over to green energy. So, they always move in sync with each other.

Q: I heard rumors that Amazon (AMZN) is likely to raise Prime’s annual fee by $10-20 a year in 2021. Will that be a catalyst for the stock to go higher?

A: Yes. For every $10 dollars per person in Prime revenue, Amazon makes $2 billion more in net profit. I would say that's a very strong argument for the stock going up and maybe what breaks it out of its current 6-month range. By the way, Amazon is wildly undervalued, and my long-term target is $5,000.

Q: Do you think that the spike in Apple (AAPL) MacBook purchases means that computers will overtake iPhones as the revenue driver for Apple in 2021, or is the phone business too big?

A: The phone business is too big, and 5G will cause iPhone sales to grow exponentially. Remember, the iPhones themselves are getting better. I just bought the 12G Pro, and the performance over the old phone is incredible. So yeah, iPhones get bigger and better, while laptops only grow to the extent that people need an actual laptop to work on in a fixed office. Is that a supercomputer in your pocket, or are you just glad to see me?

Q: Share buybacks dried up because of revenue headwinds; do you think they will come back in a massive wave, giving more life to equities?

A: Absolutely, yes. Banks, which have been banned from buybacks for the past year, are about to go back into the share buyback business. Netflix has also announced that they will go buy their shares for the first time in 10 years, and of course, Apple is still plodding away with about $100 or $200 million a year in share buybacks, so all of that accelerates. The only ones you won't see doing buybacks are airlines and Boeing (BA) because they have such a mountain of debt to crawl out from before they can get back into aggressive buybacks.

Q: Interest rates are at historic lows; the smartest thing we can do is act big.

A: That’s absolutely right; you want to go big now when we’re all suffering so we can go small later and run a balanced budget or even pay down national debt if the economy grows strong enough. The last person to do that was Bill Clinton, who paid down national debt in small quantities in ‘98 and ‘99.

Q: What do you think about General Motors (GM)?

A: They really seem to be making a big effort to get into electric cars. They said they're going to bring out 25 new electric car models by 2025, and the problem is that GM is your classic “hour late, dollar short” company; always behind the curve because they have this immense bureaucracy which operates as if it is stuck in a barrel of molasses. I don’t see them ever competing against Tesla (TSLA) because the whole business model there seems like it’s stuck in molasses, whereas Tesla is moving forward with new technology at warp speed. I think when Tesla brings out the solid-state battery, which could be in two years, they essentially wipe out the entire global car industry, and everybody will have to either make Tesla cars under license from Tesla—which they said they are happy to do—or go out of business. Having said that, you could get another double in (GM) before everyone figures out what the game is.

Q: Will you update the long-term portfolio?

A: Yes, I promise to update it next week, as long as you promise me that there won’t be another insurrection next week. It’s strictly a time issue. After last year being the most exhausting year in history, this year is proving to be even more exhausting!

Q: Do you see a February pullback?

A: Either a small pullback or a time correction sideways.

Q: Do you think the Zoom (ZM) selloff will continue, or is it done now that the pandemic is hopefully ending?

A: It’s natural for a tech stock to give up one third after a 10X move. It might sell off a little bit more, but like it or not, Zoom is here to stay; it’s now a permanent part of our lives. They’re trying to grow their business as fast as they can, they’re hiring like crazy, so they’re going to be a big factor in our lives. The stock will eventually reflect that.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 13, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COME HERD IMMUNITY),

(INDU), (TSLA), (SPY), (GLD), (JPM), (IBB), (QQQ), (AAPL), (MSFT), (DCUE), (NVDA)

The US passed a single-day record of 70,000 new cases for Covid-19 over the weekend, with Florida bringing in an astounding 15,300.

We missed a chance to stop the epidemic in January because we were blind. Then we missed again in April because we were lazy, when New York City was losing nearly 1,000 souls a day and ignored the lessons therein.

So, we relentlessly continue our march towards herd immunity, when two-third of the population gets the disease, protecting the remaining one third. That’s about a year off.

That implies total American deaths will reach 2.2 million, more than we have lost from all our wars combined.

The faster people die, the closer we are to the end of the plague, which is good news for everyone.

And the stock market keeps going up every day, the worse the news, the faster. That may be happening because the more severe the shock to the system, the faster companies must evolve to survive, making them ever more profitable.

Out with the Old America, in with the new. The future is happening fast.

We here at Mad Hedge Fund Trader have just delivered the most astonishing quarter in our 13-year record, up some 41.98% from the March 16 low.

That makes me cautious. Things never stay that good for long. Just because I can’t see the next black swan doesn’t mean it isn’t going to happen.

If stocks rise when corona cases are exploding, what do they do when cases fall? Do they fall too, or do they rise even faster?

That’s above my pay grade. I’m only a captain, not a general.

So, I will be moving to a 100% cash position in coming days and then let the next black swan tell me what to do. If we suffer a severe dive, and 10%-20% is entirely possible, then I’ll jump back in with my “BUY” hat on. That means testing the lower up of my six-month (SPX) 2,700-$3,200 range.

If we suddenly surge to far greater heights and new all-time highs, then I will be selling short as fast as I can write the trade alerts.

In the meantime, we have Q2 earnings to look forward to in the coming week, which will certainly be one for the history books. The bullish view is that they will be down only 44% from a dismal Q1. The bearish view is far worse. Banks (JPM) kick off on Tuesday.

NASDAQ (QQQ) hit a new high at 10,622, with Apple (AAPL) and Microsoft (MSFT) leading the charge. Elon Musk is now looking at another $1.7 billion payday with his shares touching $1,500. I’m moving to 100% cash, peeling off one profitable position a day as each option play reaches its maximum profit. I just had the best quarter in a decade, up an eye-popping 40%, and I’m just not that smart to keep it going. Humility always wins in the long-term.

Goldman Sachs chopped its growth forecast in the face of soaring Covid-19 cases, paring their Q3 prediction from +33% to +25%. Political campaign rallies are spreading the disease faster than expected. Q1 most likely came in at negative -5%. Expect worse to come. If the stock market can’t break at 135,000 corona deaths, it will at 260,000 or 520,000, which is certainly coming.

NVIDIA topped Intel as most valuable chip company. No surprise here. High-end graphics cards are worth a lot more money than plain commodity processors. Keep buying dips on (NVDA) which we’ve been loading the boat with now for four years. There’s an easy double from here.

Warren Buffet bought Dominion Energy (DCUE), in one of the only distressed sales available this year, thanks so much to government support. With natural gas prices at all-time lows, the big boys are throwing in the towel. Immense public pressure is forcing public utilities to abandon fossil fuels. Warren will sell all of his newfound energy in the $10 billion deal to China. It’s the beginning of the end for carbon. Buy (TSLA) on dips.

Dividend Cuts will drive stock trading in H2. Energy, airline, cruise lines, casinos, movie theaters, and hotels are most at risk, while big technology companies like Apple are the safest. Currently, the S&P 500 is yielding 2.0%, while the ten-year US Treasury bond is paying out 0.65%. Room for a cut?

Tesla to reach $100 billion in annual revenue by 2025, says San Francisco-based JMP Securities. The logic goes that if they can produce 90,000 vehicles a quarter during a pandemic, 140,000 a quarter should be no problem by yearend. The news delivered a move in the shares to a new all-time high of $1,549. Inclusion of (TSLA) in the S&P 500 would also deliver a lot of forced institutional buying, which might take the shares up 40% more. The future is happening fast. Keep buying (TSLA) on dips for a 2021 target of $2,500. If this keeps up, we may see it next week. Remember, I traded Tokyo in 1989. Nothing is impossible.

US student visas were canceled in ostensibly an administration coronavirus-fighting measure, but really in the umpteenth measure to shut foreigners out. “America first” is turning into “America only.” Midwestern schools in particular will be hurt by the loss of 400,000 full tuition-paying international students, especially when state education budgets are getting cut to the bone. That’s down from 800,000 three years ago. If they’re already here, how does this help us? Most colleges are moving to online-only models to limit infections.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch enjoyed another blockbuster week, up an astounding +2.28. It was a week when everything worked in the extreme….again.

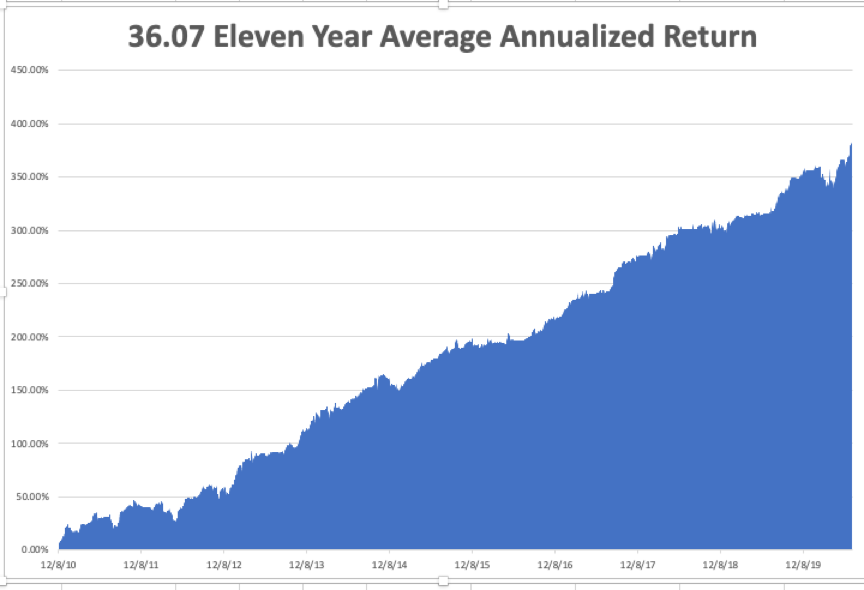

My eleven-year performance rocketed to a new all-time high of 381.74%. A triple weighting in biotech and a double weighting in gold were a big help. A foray into the banks proved immediately successful. I seem to have the Midas touch these days.

That takes my 2020 YTD return up to an industry-beating +25.83%. This compares to a loss for the Dow Average of -8.8%, up from -37% on March 23. My trailing one-year return popped back up to a record 66.22%, also THE HIGHEST IN THE 13-YEAR HISTORY of the Mad Hedge Fund Trader. My eleven-year average annualized profit recovered to a record +36.07%, another new high.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here. It’s jobs week and we should see an onslaught of truly awful numbers.

On Monday, July 13 at 10:00 AM EST, the June Inflation Expectations are out.

On Tuesday, July 14 at 7:30 AM EST, US Core Inflation for June is published

On Wednesday, July 15, at 7:30 AM EST, US Industrial Production for June is announced. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, June 16 at 8:30 AM EST, Weekly Jobless Claims are announced. At 7:30 AM, US Retail Sales for June is printed.

On Friday, June 17, at 7:30 AM EST, the US Housing Starts for June are released.

The Baker Hughes Rig Count is out at 2:00 PM EST.

As for me, I am training hard for my upcoming 50-mile hike with the Boy Scouts, knocking off 10 miles a day at 9,000 feet on the Tahoe Rim Trail. I have to confess that I’m feeling the knees like never before.

As they used to say in the Marine Corps, “Pain is fear leaving the body.” More than knowledge comes with age. Pain is there as well.

Marine Corps to Boy Scout leader. It’s been a full life.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Years Have Not Been Kind

Mad Hedge Technology Letter

July 7, 2020

Fiat Lux

Featured Trade:

(JULY 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (VIX), (TLT), (GLD), (IBB), (QQQ), (SPY), (NEM)

(TESTIMONIAL)

Below please find subscribers’ Q&A for the July 1 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: You obviously do well with deep-in-the-money call and put spreads, but I struggle to get your prices.

A: Raise the strike prices or raise the price that you’re bidding for them closer to my limit. It’s really hard to keep current prices in this market with such extreme volatility (VIX), especially when you’re having melt-ups going on in Tesla (TSLA) and so on. Our trade alerts are just a starting point to get you going in the right direction in the right stock. The people who make the most money with the trade alert service are those who use my market timing to buy futures, either at the money risk reversals on stocks (long the call and short the put), or outright futures in gold (GLD), currencies (FXE), and bonds (TLT).

Q: How high can Tesla go?

A: My immediate target is $1200 (which has already been hit), and the rumors I'm hearing is that they will be good if you factor in the two months that the Fremont factory was closed. And after that, it’s $2,500 and then there's Ron Baron’s target of $5,000, who’s been in the stock himself since it was at $100 a share. Ron was a little late in finding my research on the company. I first got in at $16.50 after I toured the Fremont factory.

Q: Is it possible there will be a national mandate to wear masks, which could boost stocks?

A: Not under this president. Do not expect help from this administration on this pandemic. They've figured out they can’t beat it so they are just walking away and leaving the states to figure out what they can. You’ll have to wait for another president to get a national mask mandate if we’re still alive by that time. I am getting a lot of emails from Europe complaining that the United States is extending the pandemic by having so many people refusing to wear masks here or admit that the disease even exists. They are horrified.

Q: What do you think about the biotech ETF (IBB)?

A: I’d be buying it with both hands. Even without the pandemic, a new bull market started last September in biotech because the fundamentals long term were fantastic. But you had to be a scientist to see it back then. They really had the highest earnings growth with the lowest price earnings multiples in the entire stock market. The pandemic just gave it a supercharger. That’s why I started the Mad Hedge Biotech & Healthcare Letter (click here).

Q: Which ETF should I use for biotech?

A: The iShares NASDAQ Biotechnology ETF (IBB). It's a basket of the top 20 global biotech firms but will underperform single biotech stock picks by half, as any basket does.

Q: What about the long-term portfolio?

A: I will get to it. It seems like our long-term portfolio is changing every week, so it’s difficult to really look at anything in the long term. These days, long term is a week with all the volatility we’re getting. I imagine I’d be getting rid of any energy stocks on this rally though. I see oil going back to zero.

Q: You say stay long NASDAQ (QQQ) and short S&P 500 (SPY) for the rest of the year, but you project new highs for the S&P 500?

A: Yes, both can go up, but NASDAQ will go up faster, and that’s what hedge funds are doing. That gives you a market neutral position, sucks a lot of the risk out of that position, and it’s even crash-proof as we saw in the winter when the markets were melting down. And like hedge funds, you can leverage that up 5 or 10 times. So yes, that trade will work all day long, even if both indexes go to new highs. I imagine NASDAQ will outperform on the upside relative to SPY by a factor of two or three to one.

Q: Is there a good substitute to use versus your deep-in-the-money alerts if you have a smaller account?

A: You can just buy the stocks. Or, you can just buy the stocks on margin, which is 2 to 1—50% margin requirement there. There are many ways to skin a cat. The call spreads actually give you the most bang per buck because you get a lot of leverage with a small dollar amount upfront and limited risk.

Q: I heard that hedge funds have huge shorts. Is this setting up another short squeeze? Will they eventually be right?

A: Yes, that may have been what happened on Monday and Tuesday, a squeeze on the shorts driving prices much higher. They will eventually be right a little bit, but you’re certainly not going to get the major declines we saw in February/March because of all the QE and government support. The pandemic is no longer a surprise.

Q: Will COVID-19 fears keep volatility elevated until there is a vaccine?

A: Absolutely, yes. That’s great news for our options strategy, which is why we’re 100% invested almost all the time these days because higher volatility doubles the premiums you get for options. My current strategy is that once a position hits 90% of its maximum profit, I dump it and put on another position to take in an extra $1,500-$2,000. I did that with Tesla and gold (GLD) last week. This is the golden age of the in-the-money put and call spread strategy and we are better at executing it than anyone else.

Q: What do you have to say about the jobs report?

A: The entire US economic data system is breaking down because we’re seeing such immense swings month to month. Reporting lags are getting amplified one hundredfold. The June Nonfarm Payroll Report showed an increase of 4.8 million jobs and an unemployment rate of only 11.1% (I never thought I’d ever say “only 11.1%”). However, the state jobless claims are indicating an unemployment rate of at least 22%. Go walk down the Main Street of any town and you’ll see that the state figures are right. All the forecasting is relatively pointless. How can we get a fall in unemployment when nothing is open?

Q: Are you recording this webinar?

A: Yes, we usually post the recorded webinar on the site 2 hours after we finish so our many international subscribers don’t have to stay up until the middle of the night to watch it. That’s how long it takes to convert the webinar into a video format we can post online.

Q: When setting up LEAPS (Long Term Equity Participation Securities), do you buy straight calls at-the-money or in-the-money?

A: You buy deep, out-of-the-money spreads. Let's say you bought a (TSLA) $1,500/$1,550 deep-in-the-money call spread, and it expires at the maximum profit point with the stock over $1,550. You’ll make about a 500% return on that because it’s so far out of the money; the leverage is enormous. Will Tesla close over $1,550 in two years? Probably.

Q: How do I get into Tesla?

A: Close your eyes and buy at market, and hope we get $1,200 tomorrow on great Q2 sales numbers. Or, wait for another one of these huge selloffs—Tesla does have a history of selling off 50% at any given time, and then you go into a LEAPS there and get a 500% return. Most investors prefer the latter if they know about LEAPS. Remember, our last “BUY” into Tesla was a year ago when the stock was at $180. By the way, a lot of the shorts in Tesla stock were financed by big oil money and when oil crashed, they lost the ability to post more margin. So, they were forced to cover their shorts at gigantic losses, creating this super spike in the share price. Elon Musk, who owns 20% of the company, is laughing all the way to the bank.

Q: How do we pick the best strike prices for long-term LEAPS?

A: Go 30% out-of-the-money. There you get your 500% return. If you really want to be aggressive and you think the stock has 50% of upside, then go 50% out-of-the-money. There your return will be about a 1,000% profit over 2 years.

Q: How long are these trades for? I haven’t received any trade alerts.

A: Please contact customer support and we’ll find out if they are being filtered out by your spam folder. Global Trading Dispatch is sending out trade alerts virtually every day for all asset classes, so you should have received several of them by now. The Mad Hedge Technology Letter sends out fewer because they are confined to a narrow part of the market.

Q: What is your favorite stock in the gold space?

A: Newmont Mining (NEM). They have the strongest balance sheet of the major gold companies because they engage in fewer takeovers than the other big gold companies.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 28, 2020

Fiat Lux

Featured Trade:

(FEBRUARY 26 BIWEEKLY STRATEGY WEBINAR Q&A),

(VIX), (VXX), (SPY), (TLT), (UAL), (DIS), (AAPL), (AMZN), (USO), (XLE), (KOL), (NVDA), (MU), (AMD), (QQQ), (MSFT), (INDU)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 26 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: There’s been a moderation of new coronavirus cases in China. Is this what the market needs to find a bottom?

A: Absolutely it is; of course, the next risk is that cases keep increasing overseas. The final bottom will come when overseas cases start to disappear, and that could be a month or two off.

Q: How low will interest rates go after the coronavirus?

A: Well, interest rates already hit new all-time lows before the virus became a stock market problem. The virus is just giving it a turbocharger. Our initial target of 1.32% for the ten-year US Treasury bond was surpassed yesterday, and we think it could eventually hit 1.00% this year.

Q: What is the best way to know when to buy the dip?

A: When the Volatility Index (VIX) starts to drop. If you can get the volatility index down to the mid-teens and stay there, then the market will stabilize and start to rise fairly sharply. A lot of the really high-quality stocks in the market, like United Airlines (UAL), Walt Disney (DIS), Apple (AAPL) and Amazon (AMZN), have really been crushed by this selloff. So those are the names people are going to look at for quality at a discount. That’s going to be your new investment theme, buying quality at a discount.

Q: Do recent events mean that Boeing (BA) is headed down to 200?

A: I wouldn't say $200, but $280 is certainly doable. And if you get to $280, then the $240/$250 call spread all of a sudden looks incredibly attractive.

Q: What does a Bernie Sanders presidency mean for the market?

A: Well, if he became president, we could be looking at like a 50-80% selloff—at least a repeat of the ‘09 crash. However, I doubt he will get elected, or if elected, he won’t have control of congress, so nothing substantial will get done.

Q: Is this the beginning of Chinese (FXI) bank failures that will cause an economic crisis in mainland China?

A: It could be, but the actual fact is that the Chinese government is doing everything they can to rescue troubled banks and companies of all types with short term emergency loans. It’s part of their QE emergency rescue package.

Q: Can you explain what lower energy prices mean for the global economy?

A: Well, if you’re an oil consumer (USO), it’s fantastic news because the price of gas is going down. If you’re an oil producer (XLE), like for people in the Middle East, Texas, Louisiana, Oklahoma, and North Dakota, it’s terrible news. And if you’re involved anywhere in the oil industry, or own energy stocks or MLPs, you’re looking at something like another great recession. I have been hugely negative on energy for years. I’ve seen telling people to sell short coal (KOL). It’s having a “going out of business” sale.

Q: Should I aggressively short Tesla (TSLA) here? Surely, they couldn’t go up anymore.

A: Actually, they could go up a lot more. I would just stay away from Tesla and watch in amazement—there’s no play here, long or short. It suffices to say that Tesla stock has generated the biggest short-selling losses in market history. I think we’re up to about $15 billion now in short losses. Much smarter people than us have lost fortunes trying in that game.

Q: Was that an Amazon trade or a Google trade?

A: I sent out both Amazon and an Apple trade alert this morning. You should have separate trade alerts for each one.

Q: Are chips a long term buy at today’s level?

A: Yes, but companies like NVIDIA (NVDA), Micron Technology (MU), and Advanced Micro Devices (AMD) may be better long-term buys if you wait a couple of weeks and we test the new lows that we’ve been talking about. Chips are the canary in the coal mine for the global economy, and we have not gotten an all-clear on the sector yet. If you’re really anxious to get into the sector, buy a half of a position here and another half 10% down, which might be later this week.

Q: When will Foxconn reopen, the big iPhone factory in China?

A: Probably in the next week or so. Workers are steadily moving back; some factories are saying they have anywhere from 60-80% of workers returning, so that’s positive news.

Q: Are bank stocks a sell because of lower interest rates?

A: Yes, absolutely. If you think the 10-year treasury is running to a 1.00% yield as I do, the banks will get absolutely slaughtered, and we hate the sector anyway on a long-term basis.

Q: What about future Fed rate cuts?

A: Futures markets are now pricing in possibly three more rate cuts this year after discounting no more rate cuts only a few weeks ago. So yes, we could get more interest rates. I think the government is going to pull all the stops out here to head off a corona-induced recession.

Q: Once your options expire, is it still affected by after-hours trading?

A: If you read the fine print on an options contract, they don’t actually expire until midnight on a Saturday night after options expiration day, even though the stock market stops trading on a Friday. I’ve never heard of a Saturday exercise, but you may have to get a batch of lawyers involved if you ever try that.

Q: What’s the worst-case scenario for this correction?

A: Everything goes down to their 200-day moving averages, including Indexes and individual stocks. You’re talking about Apple dropping to $243 and Microsoft (MSFT) to $144, and NASDAQ (QQQ) to 8,387. That could tale the Dow Average (INDU) to maybe 24,000, giving up all the 2019 gains.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 16, 2019

Fiat Lux

Featured Trade:

(DON’T MISS THE AUGUST 21 GLOBAL STRATEGY WEBINAR),

(WHY CRASHING YIELDS COULD BE SIGNALING AN END TO THE STOCK SELLOFF),

(TLT), (QQQ), (DBA), (EEM), (UUP)

Global Market Comments

May 6, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR HERE’S ANOTHER BOMBSHELL),

(DIS), (QQQ), (AAPL), (INTU), (GOOGL), (LYFT), (UBER), (FCX))