Global Market Comments

August 22, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE PARTY IS OVER)

(SPY), (QQQ), (TLT), (VIX)

Global Market Comments

August 22, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE PARTY IS OVER)

(SPY), (QQQ), (TLT), (VIX)

It’s been one heck of a party for the last two months. We’ve been wearing lampshades on our heads, dancing the Lindyhop, and drinking hopium by the barrel.

But even the best of parties must come to an end.

It's time to put the empty bottles into the recycling bin. I’ve called Uber for the guests who can no longer walk. The hangovers have already started. The cleaning lady is probably going to fire me tomorrow.

The Party is Over, at least for now, as are the big money vacations at the Hamptons, Aspen, and Lake Tahoe. This year, wildly overbought markets are perfectly coinciding with peak vacation time.

September brings bigger worries with a Fed rate rise, doubled QT, and a looming election. I’m now net short for the first time since March.

A Volatility Index (VIX) at $19, a Mad Hedge Market Timing Index at 51, and a rally worth half of this year’s losses are telling you to stay away in droves.

Cash is king right now. Just sit back and count all the money you made with me this year. The reality is that there is a honking great dilemma in the market right now. The Fed is talking hawkish, while traders are trading dovish. The Fed ALWAYS wins this kind of bust-up.

I’m looking for stocks to give up at least half their heroic (SPY) 70-point June-August gains. That would take us down to (SPY) 50-day Moving Average at $395.

After that, we might bounce between the 50-day moving average at $395 and the 200-day at $432 all the way until the November midterm elections. Thereafter, we will launch on a meteoric yearend rally that could take us all the way up to (SPY) $480.

It couldn’t go any other way because there is too much cash lying around. In fact, short term positioning is only at 10% of historical norms, and there is still at least $500 billion worth of company share buybacks still in the pipeline, especially in tech.

That’s all fine with me because at $395, the free money trades start to set up again. At (SPY) $395, the (VIX) should be back up to $30. That means you can set up call spreads, assume we will double bottom at (SPY) $362, and STILL make the maximum potential profit. Such is the magic of vertical bull call debit spreads.

In the meantime, we might be able to squeeze out $30 or $40 worth of short-term trading profits in short positions. This will be the only place to make money for the next month or two. If you’re interested, I’m currently short the (SPY), (QQQ), and (TLT).

Yes, trading is all about alternating pain and pleasure. That’s why you must be a sadomasochist to be a great trader.

It all totally works for me.

It's no surprise that the second the yield on the ten-year US Treasury yield recovered 3.00%, the stock market rally promptly died. Message: watch the ten-year US Treasury yield like an eagle.

Tesla (TSLA) Production Tops 3 million and Elon Musk is aiming for 100 million by 2030. Mine was chassis number 125 and my name is still on the Fremont factory wall. They have driven 40 million miles since 2010, pushing their autonomous learning program far down the road when compared to others. Tesla is the third largest car maker in China. It was worth a $40 pop in the stock. The shares split 3:1 on Friday, sucking in meme interest.

Oil (USO) Collapses to New Two-Month Low to $88 a barrel, down $44, or 33% from the highs. There’s another 50-cent decline in gasoline prices in the cards. Disastrous battlefield setbacks for Russia have been the real driver. Putin has resorted to clearing out the prisons to reinforce his army. He is also forcing Ukrainian POWs to fight their own countrymen. Maybe he'll let our woman’s basketball star go free?

The Fed Minutes are out from the last meeting six weeks ago. Interest rates will rise, but not as much as expected. A pivot to flat or lower interest rates may come sooner than expected. Look for 3.50% for the overnight rate sometime in 2023, up 100 basis points from here.

Why Isn’t the Fed Balance Sheet Falling? It’s still stuck at $9 trillion, despite a massive reduction on bond buybacks via QT. The dam is about to break, with $2-$3 trillion in bond buybacks disappearing in the coming months.

Money Supply Growth Has Ground to a Halt, showing zero growth so far in 2022. It is about to start shrinking dramatically, once QT doubles up to $95 billion a month in September. This could deliver our next buying opportunity for stocks, but also might give us a recession.

Housing Starts Collapse, down 9.6% YOY in July. Labor costs are still soaring while affordability has been shattered. If you’re thinking of buying stocks now, lie down and take a long nap first, a very long nap.

Existing Home Sales Dive 6%, off for the sixth consecutive month. Sales dropped to a seasonally adjusted 4.81 million units. It’s no surprise that we are now in a housing recession while the rest of the economy remains small. Homebuyers are also still contending with tight supply. There were 1.31 million homes for sale at the end of July, unchanged from July 2021. At the current sales pace, that represents a 3.3-month supply.

20 Electric Vehicles Will Get the $7,500 Tax Credit on Day One, Biden just signed the climate bill, with Tesla far and away the leader. Only cars with 70% or more of its parts coming from the US qualify. Used EVs get a $4,000 tax credit. MSRPs must be below $55,000 and individual income no more than $150,000. The credit begins in 2023. Left out in the cold are EVs made in Japan and South Korea.

Bitcoin Hits Three-Week Low, as “RISK OFF” returns. Suddenly, stocks, oil prices, and interest rates have started going the wrong way. Avoid Crypto.

Why the IRS is Not Interested in You. Treasury secretary Yellen says the priorities will be clearing the backlog of unprocessed tax returns and improving customer service, overhauling technology, and hiring workers.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil prices now rapidly declining, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the market volatility (VIX) now dying, my August month-to-date performance appreciated to +3.96%.

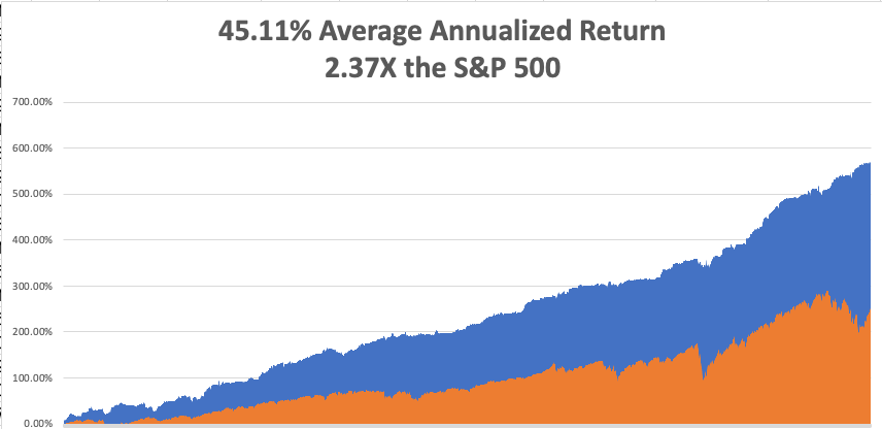

My 2022 year-to-date performance ballooned to +58.79%, a new high. The Dow Average is down -5.91% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +73.78%.

That brings my 14-year total return to +571.35%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.11%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases soon reaching 94 million, up 300,000 in a week and deaths topping 1,040,000. You can find the data here.

On Monday, August 22 at 8:30 AM, the Chicago Fed National Activity Index for July is released.

On Tuesday, August 23 at 7:00 AM, New Home Sales for July are out.

On Wednesday, August 24 at 7:00 AM, Durable Goods for July are published.

On Thursday, August 25 at 8:30 AM, Weekly Jobless Claims are announced. US GDP for Q2 is released.

On Friday, August 26 at 7:00 AM, the Personal Income and Spending are disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, I have met countless billionaires, titans of industry, and rock stars over the last half-century, and one of my favorites has always been Sir Richard Branson.

I first met Richard when I was living in London’s Little Venice neighborhood in the 1970s. He lived on a canal boat around the corner. I often jogged past him sitting alone on a bench and reading a book at Regent’s Park’s London Zoo, far from the maddening crowds.

Richard was an entrepreneur from day one, starting a magazine when he was 16. That became the Virgin magazine reviewing new records, then the Virgin record stores, and later the Virgin Megastore where he built his first fortune.

When the money really started to pour in, Richard moved to a mansion in Kensington in London’s West End. It wouldn’t be long before Richard owned his own Caribbean Island.

In 1984, Branson was stuck in the Virgin Islands because of a cancelled British Airways flight. He became so angry that he chartered a plane and started Virgin Airlines on the spot, which soon became a dominant Transatlantic carrier and my favorite today.

A British Airways CEO later admitted that they did not take Branson seriously because “He did not wear a tie.” The British flag carrier resorted to unscrupulous means to force Virgin out of business. They hired teams of people to call Virgin customers, cancel their fights, and move them over to BA.

When British Airways got caught, Branson won a massive lawsuit again BA over the issue. He turned the award over to his employees.

Richard would do anything to promote the Virgin brand. He attempted to become the first man to cross the Atlantic Ocean by balloon, making it as far as Ireland.

When he opened a hotel in Las Vegas, he jumped off the roof in a hang glider. The wind immediately shifted and blew him against the building, nearly killing him.

Richard later went on to start ventures in rail, telecommunications, package tours, and eventually space.

When I flew to Moscow in 1992 for my MiG 29 flight, I picked Virgin Atlantic, one of the few airlines flying direct from London to Moscow (I never trusted Aeroflot). Who was in the first-class seat next to me but Richard Branson. We spent hours trading aviation stories, of which I have an ample supply.

As we approached Sheremetyevo Airport, he invited me up to the cockpit and told the pilot “This is my friend Captain Thomas. Would you mind if he joined you for the landing?”

He handed me a headset so I could listen in on a rare Moscow landing. When the tower called in the field air pressure, they were off by 1,000 feet. If we were flying under instrument flight rules, we would have crashed. I pointed this out to the pilot, and he commented that this was not the first time they had had a problem landing in Moscow.

Richard once confided in me that he was terrible at math and didn’t understand the slightest thing about balance sheets and income statements. A board member once tried to explain that business was like using a net (company) to catch a fish (profit) but to no avail.

Branson had built up his entire business empire through relationships, using other people to run the numbers. He was the ultimate content and product creator.

I always thought of Richard Branson as a kindred spirit. He is just better at finding and retaining great people than I am. That is always the case with billionaires, both the boring and the adventurous, iconoclastic kind.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 7, 2022

Fiat Lux

Featured Trade:

(THE SECOND AMERICAN INDUSTRIAL REVOLUTION),

(INDU), (SPY), (QQQ), (GLD), (DBA),

(TSLA), (GOOGL), (XLK), (IBB), (XLE)

Global Market Comments

May 20, 2022

Fiat Lux

Featured Trade:

(MAY 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(C), (FXI), (BABA), (TSLA), (AAPL), (AMZN), (TGT), (FLR), (QQQ),

(FB), (ARKK), (TSLA), (WYNN), (UAL), (ALK), (DAL)

Below please find subscribers’ Q&A for the May 18 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: When do you see the banks returning to glory?

A: When recession fears go away, which should happen this summer. A recession will either have come and gone, or we will have confirmation by the end of summer that there is no recession in sight for the next few years at least. This will likely trigger a monster rally in the banks, which could all jump 50% from here. Obviously, Warren Buffet is putting his money where his mouth is by loading up on Citibank (C) yesterday. This would take us to new all-time highs by the end of the year. So, again, use these down-1000-point days to go cherry-picking among the generals who have been executed. If that’s not mixing metaphors, I don’t know what is!

Q: Should I listen to CNBC?

A: No, do not listen to the talking heads on TV. They are on TV because they don’t know how to make money. If they did know how to make money, they’d be locked up in a dark basement somewhere like me, grinding out millions for their firms. In fact, watching TV is the perfect money destruction machine because on down days, they bring out the uber bears, and on up days they bring up the hyper bulls. They are trying to egg you to get you to do the exact opposite of what you should be doing. They’re not interested in you making money; they’re interested in getting traffic on their websites and making money for themselves. CNBC can be highly dangerous to your financial health.

Q: Will we get stagflation?

A: No, because I think that once the year-on-year comparisons kick in—literally in a month or two—inflation will drop from the current 8.3% to down maybe 4% by the end of the year. That also is another factor in your monster second-half rally.

Q: Do you think the bounce in the market yesterday is the beginning of an upward trend or a dead cat bounce?

A: Definitely a dead cat bounce. I expect we’ll keep chopping around in the current range for the next 3, 4, and 5 months, and then we catapult into a monster year-end rally. That is a typical bottoming-type process.

Q: Is the wisdom “Go away in May” still alive or is your best bet that this year may prove different and the market goes up in the latter part of the year?

A: Actually, you should have gone away in November. That’s when all tech stocks peaked; only energy went up after that. If you’d gone away in November and said “come back in August” that would have been a good strategy because I think that’s when the year-end rally begins. If anything, May could be the bottom of the entire move.

Q: Is it time for LEAPS (Long Term Equity Anticipation Securities)?

A: Not yet—it’s too soon for LEAPS territory. You only want to do LEAPS when you are on a sustained long-term uptrend in a stock. We are nowhere near sustained anything, we are still in a bottoming phase, and could be there for months. At the end of those months is when we’ll be looking at LEAPS, where you can double your money every 6 months.

Q: Is it time to start nibbling on China stocks (FXI) now that COVID news is marginally better?

A: I’m going to avoid Chinese stocks because the American ones are so much better. You want to buy the quality at the discount, not the marginal, high-risk political footballs at a discount. And China will remain high-risk as long as they are abandoning capitalism. If you have to buy one Chinese stock, I would say Alibaba (BABA); you could get a double on that. But remember it is a high-risk trade—if the Chinese government wants to roll Jack Ma up in a carpet and kidnap him to Western Chinese re-education camp, the stock will get slaughtered. And that’s been happening increasingly with the heads of major companies in the Middle Kingdom.

Q: When this current route comes to an end, should we look to enter the market with 50% margin on stocks like Tesla (TSLA)?

A: It’s never sensible to go to 50% margin because if the stocks drop 50%, you are completely wiped out—you’ve lost everything. Plus, coming back from a loss is one thing; coming back from zero is impossible. So, I would not recommend that. You might do a safe stock like Apple (APPL), with a 2% dividend, and then at least you’re getting a double dividend. You only do the 50% margin on the safest, high dividend stocks.

Q: Amazon (AMZN) is on its way down. What is your expectation for the $3200/$3400 vertical bull call spread in January 2023?

A: I think you could make money on that. It may not be the full amount of the spread, but you’ll definitely get a big increase from current levels, because when we do get a second half rally, it will be tech-led, and Amazon has already had a horrific decline. What you might consider is rolling your strike down, taking the loss on the 3200/3400 and rolling down to like a $2,000/$2,200 in twice the size, and you’ll make your money back that way.

Q: For those of us thinking about LEAPS, how should we start to buy in—20, 30, 50% right now?

A: Well, first of all, you only do them on down days like today, when the market is down 800, and you scale in. 20% now, 20% higher or lower, and 20% again higher or lower. But you really want to be saving cash for days like this because You want to feel smarter than everybody else, and they absolutely will hit any bid on a down day, and that's where your LEAPS fills are really excellent, is on a down day like this.

Q: Can the Fed avoid another policy mistake? Because it seems that not only are they heading for high inflation, but layoffs are coming as well, and even with that I’m sure they will perform a soft landing of sorts.

A: For sure, when you take massive amounts of stimulus out of the economy, as we have in the last year, that is recessionary. In fact, the US government is close to running a balance budget right now because Biden can’t get anything through Congress other than money for Ukraine. Good for Ukraine economy, not for ours. And yes, they can do a soft landing, but has it ever been done before? No. Though this is the Fed that just keeps on surprising, so who knows. In the meantime, I'm willing to trade the ranges, and that may be all you get to do for a while.

Q: Target (TGT) shares are down 25%, as they cited higher costs that will result in rising prices for their customers. Would you buy the dip?

A: No, I generally don’t like retailers anyway. It’s a business that operates on a 2% profit margin. I like 40 or 50% profit margin businesses—those tend to be technology stocks.

Q: Would you buy retailers going into a recession?

A: No, that’s the worst thing in the world to own.

Q: Could Fluor Corp (FLR) be a Ukraine infrastructure stock?

A: Yes, once the war ends there will be a massive effort to rebuild Ukraine. Every company in the world will be involved, and Fluor and Bechtel will be the biggest, though Fluor is the only one where you can buy the stock. We already have the money to do this with all of the money that was seized from Russia. I predict discount sales on mega yachts.

Q: Why do you think all that money is going to Ukraine?

A: Because a weakened Russia is in the national interest of the United States, and it’s better that their soldiers are doing the dying than ours. I’ve done the latter and definitely prefer the former, using the other country's’soldiers as cannon fodder.

Q: On down days like today, should I be putting on one-month trades like the June options?

A: Yes, because the minimizes your risk and cuts the cost of mistakes. Waiting for the second half of the year when we get a prolonged uptrend to look at LEAPS—that is the correct way to do it.

Q: Over the next 12 months, do you think the S&P 500 will outperform Nasdaq?

A: No—for the next 3 months the S&P 500 will outperform NASDAQ. After that, NASDAQ will become an enormous outperformer for the rest of the decade. So, choose your entry points wisely.

Q: Do you think that housing is peaking out and will start to decline?

A: No, we still have a long-term structural shortage of 10 million homes in the US and I think we will flatline housing for years until we catch up with that shortfall.

Q: What are your thoughts on the Metaverse?

A: Too soon. Right now, the Metaverse involves spending only—no revenues. It could be years before you actually see any profits. So that’s why I'm avoiding Meta or Facebook (FB). But then, you could have made the same argument about the internet 25 years ago and semiconductors 50 years ago. If you waited long enough, however, you obviously made a fortune.

Q: China is hoarding 69% of their wheat reserves. Is this because they plan to invade Taiwan?

A: No, it’s because there’s a global food crisis going on. Many countries, like India, have banned exports of food to protect themselves. People miss this about China: China will never have a war or invade anybody, because the second they do, their food supplies get cut off by us, who are the world’s largest producer of food. Plus, their trade would get shut off to pay for it, so they can’t buy it from somewhere else, and that’s done with us also. So, they need to be in our good graces in order to eat. That's the bottom line and that’s why Taiwan will never get invaded. Russia’s economy can operate independently for a while, but China’s can’t.

Q: Is the baby food shortage further evidence of a food crisis?

A: No, the baby formula crisis is being caused by a monopoly of three companies that control 100% of the baby food market; and the largest of these companies, accounting for a 40% market share of the baby food making, is producing baby food that is poisonous. That's why they got shut down. This has been going on for years, and for some reason, they got a free pass on regulation and inspections by the previous administration, which is ending now, and all of a sudden we’re finding out that 40% of the country’s baby food is contaminated and is being pulled off the market. So, it really has nothing to do with the global food crisis. That’s more related to Climate change—surprise, surprise—as it’s not raining in the right places like California, the war in Ukraine, which removed 13% of the world’s calories practically overnight.

Q: Should I bet the farm here with the ARK Innovation Fund (ARKK)? I like Cathie Woods’ bet on innovation or five-year time horizon. It’s a great thing, don’t you think?

A: Not so great when you drop 70% in the last year. And it is a high-risk bet that of her ten largest holding companies, you only need one of them to work for the fund to bring in a decent return. Of course, you may have to write off nine other companies to do that. But yes, it’s a great thing to own on the way up, not so great on the way down. I know some people who started scaling into ARK in November and came to regret it. I would wait on it—this is your highest leverage technology play, and if you really want some punishment, there’s a hedge fund that’s bringing out a 2X long ARK fund in the next couple of months. Then it’s basically option money you’re throwing out. If you want to put some money in that, you could get a 10x on the 2x ETF if you’re playing a recovery in ARK. So watch it; don’t touch it now because ARK is having another heart attack today, but something to consider if you like gambling.

Q: I am full up with a thousand shares of PayPal (PYPL). It’s now down 76%. What should I do?

A: I recommend you learn the art of stop losses. I stopped out of this thing last fall, and it’s continued to go down virtually every day. Whenever you buy a new position, automatically enter into your spreadsheet your stop loss for that position. Because things can drop by 80 or 90% and you work too hard for your money to throw it away on these big losses.

Q: What do you think about Steve Wynn and Wynn Hotels?

A: I’d be buying down here down 62%; it was announced today that Steve Wynn has secretly been acting as an agent for the Chinese government where (WYNN) has a major part of its operations. Who knew? With all those high rollers being flown in on private jets from China, sitting at the tables in the closed rooms. So yes, this is a recovery play and it will do just as well as all other recovery plays, but remember it’s a China recovery play. And I think, in any case, his ex-wife owns a big part of the company anyway. So I don’t think Steve Wynn is that closely connected with Wynn hotels because of past transgressions with the female staff.

Q: Is it time to scale into Freeport-McMoRan (FCX)?

A: I’d say yes. On a longer-term view, I expect (FCX) to go to $100. And for those who have the May $32/$35 call spread that expires on Friday, my bet is that you get the max profit—but you may not sleep before then.

Q: What do you have to say about a post-Putin scenario and impact on the market?

A: The day Putin dies of a heart attack, you can count on the market being up 10%, if that happens right now—less if it happens at a later date. But it would be hugely bullish for the entire global stock market, and oil would also collapse, which is why I refuse to put on oil plays here. That is a risk. Putin can give up, have an accident, or get overthrown. When the Russian people see their standard of living decline by 90%, this is a country that has a long history of revolutions, putting their leaders in front of firing squads and throwing the bodies down wells. So, if I were Putin, I wouldn't be sleeping very well right now.

Q: What's the reason for air tickets (UAL), (ALK), (DAL) going up sharply?

A: 1. Shortage of airplanes 2. Soaring fuel costs 3. Labor shortages and strikes 4. It is all proof of an economy that is definitely NOT going into recession.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

With Lieutenant Uhuru

Global Market Comments

March 25, 2022

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT VIDEOS ARE UP!)

(MARCH 23 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (TSLA), (BA), (DEER), (CAT),

(AAPL), (SLV), (FCX), (TLT), (TBT)

Below please find subscribers’ Q&A for the March 23 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: What is the best way to keep your money in cash?

A: That’s quite a complicated answer. If you leave cash in your brokerage account, they will give you nothing. If you move it to your bank account they will, again, give you nothing. But, if you keep the money in your brokerage account and then buy 2-year US Treasury bills, those are yielding 2.2% right now, and will probably be yielding over 3% in two years, so we’re actually being paid for cash for the first time in over ten years. And, as long as it’s in your brokerage account, you can then sell those Treasury bonds when you’re ready to go back into the market and buy your stock, same day, without having to perform any complicated wire transfers, which take a week to clear. Also, if your broker goes bankrupt and you hold Treasury bills, they are required by law to give you the Treasury bills. If you have your cash in a brokerage cash account, you lose all of it or at least the part above the SIPC-insured $250,000 per account. And believe me, I learned that the hard way when Bearings went bankrupt in the 1990s. People who had the Bearings securities lost everything, people who owned Treasury bills got their cashback in weeks.

Q: Is the pain over for growth stocks?

A: Probably yes, for the smaller ones; but they may flatline for a long time until a real earnings story returns for them. As for the banks, I think the pain is over and now it’s a question of just when we can get back in.

Q: Why did you initiate shorts on the Invesco QQQ Trust Series (QQQ) and SPDR S&P 500 ETF Trust (SPY) this week, instead of continuing with the iShares 20 Plus Year Treasury Bond ETF (TLT) shorts?

A: We are down 27 points in 10 weeks on the (TLT); that is the most in history. And every other country in the world is seeing the same thing. That is not shorting territory—you should have been shorting above $150 in the (TLT) when I was falling down on my knees and begging you to do so. Now it’s too late. If we get a 5-point rally, which we could get any time, that’s another story. It is so oversold that a bounce of some sort is inevitable. I’d rather be in cash going into that.

Q: Do you think Tesla (TSLA) has put in a bottom, or do you still see more downside? Is it time to buy?

A: The time to buy is not when it is up 50% in 3 weeks, which it has just done. The time to buy is when I sent out the last trade alert to buy it at $700. This was a complete layup as a long three weeks ago because I knew the German production was coming onstream very shortly; and that opens up a whole new continent, right when energy prices are going through the roof—the best-case scenario for Tesla. And the same is happening in the US—it’s a one-year wait now to get a new Model X in the US. In fact, I can sell my existing model X for the same price I paid for it 3 years ago, if I were happy to wait another year to get a replacement car.

Q: Will the Boeing (BA) crash in China damage the short-term prospects? And as a pilot, what do you think actually happened?

A: Boeing has been beat-up for so long that a mere crash in one of its safest planes isn’t going to do much. It could have been a maintenance issue in China, but the fact that there was no “mayday” call means only two or three possibilities. One is a bomb, which would explain there being no mayday call—the pilots were already dead when it went into freefall. Number two would be a complete structural failure, which is hard to believe because I’ve been flying Boeings my entire life, and these things are made out of steel girders—you can’t break them. And number three is a pilot suicide—there have been a couple of those over the years. The Malaysia flight that disappeared over the south Indian Ocean was almost certainly a pilot suicide, and there was another one in Germany and another in Japan about 20 years ago. So, if they come up with no answer, that's the answer. It’s not a Boeing issue, whatever it is.

Q: Is John Deer (DEER) or Caterpillar (CAT) a better trade right now?

A: It’s kind of six of one, half a dozen of the other. Caterpillar I’ve been following for 50 years, so I’m kind of partial to CAT, and Caterpillar has a much bigger international presence, but that could be a negative these days in a deglobalizing world.

Q: Apple (AAPL) has really caught fire past $170. Should I chase it here or wait until it’s too overbought?

A: I never liked chasing. Even a small dip, like we’re having today, is worth getting into. So always buy on the dips.

Q: Is Silver (SLV) still a good long-term play?

A: Yes, because we do expect EV production to ramp up as fast as they can possibly do it. Too bad the American companies don’t know how to make electric cars—they just haven’t been able to get their volumes up because of production problems that Tesla solved 12 years ago. So, long term, I think it will do better, but right now the risk-on move is definitely negative for the precious metals.

Q: How low will the iShares 20 Plus Year Treasury Bond ETF (TLT) go in April before the next Fed meeting?

A: I think we’re bottoming for the short term right around here. That’s why I had on that $127-$130 call spread in the (TLT) that I got stopped out of. And I may well end up being right, but with these call spreads, once you break your upper strike, the math goes against you dramatically. You go from like a 1-1 risk profile to like a 10-1 against you. So, you have to get out of those things when you break your upper strike, otherwise, you risk writing off the entire position with 100% loss. As long as Jay Powell keeps talking about successive half-point rate cuts, we will get lower lows, and my 2023 target for the TLT is $105, or about $20.00 points below here.

Q: Do you think we retest the bottoms?

A: Absolutely, yes; it just depends on where the test is successful—with a double bottom or with a retrace of half the recent moves. Keep in mind that stocks go up 80% of the time over the last 120 years, and that includes the Great Depression when they hardly went up at all for 10 years, so selling short is a professional’s game, and I wouldn’t attempt it unless you had somebody like me helping you. You're betting against the long-term trend with every short position. That said, if you’re quick you can make decent money. Most of the money we’ve made this year has been in short positions, both in stocks and in bonds.

Q: Where can we find this webinar?

A: The recording for this webinar will be posted on the website in about two hours. Just log into your account and you’ll find them all listed.

Q: When should I sell my tradable ProShares UltraShort 20+ Year Treasury ETF (TBT)?

A: You don’t have an options expiration to worry about, so I would just keep in until we hit $105 in the (TLT). If you do want to trade, I’d take a little bit off here and then try to re-buy it a couple of points lower, maybe 10% lower.

Q: What do you think of a Freeport McMoRan (FCX) $55-$60 vertical bull call spread?

A: The market has had such a massive move, that I’m reluctant to do out of the money call spreads from here unless we get a major dip. So, don’t reach for the marginal trade—that’s where you get your head handed to you.

Q: Will yield curve inversions matter this time and foretell a recession?

A: I think no, because corporate earnings are still growing, and by the summer, we probably will have a yield curve inversion.

Q: There seems to be some huge breakthrough in battery technology where batteries could be recharged within four minutes. I believe it’s the Chinese who have the tech, if so how will that impact on Tesla?

A: Every day of the year someone presents Tesla with a revolutionary new battery technology. It either doesn’t work, can’t be mass-produced, or is wildly uneconomical. So, I’ll confine my bet that Tesla will be able to eventually mass produce solid state batteries and get their 95% cost reduction that way.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

March 7, 2022

Fiat Lux

Featured Trade:

(SHORT TERM PAIN FOR SILICON VALLEY TECH)

(NFLX), (QQQ), (EPAM), (SNAP), (TDOC), (ARKK)

The American tech sector has largely been overshadowed by the events across the world.

Many would question why that would even matter.

What does that even have to do with an American smartphone or devices that permeate our society?

We deal with American tech stocks for this newsletter, and not with moral outrage or foreign policy matters.

So we stay in our lane and deal with various exogenous stocks that come our way as it relates to the Nasdaq (QQQ).

I don’t get to pick these shocks – they come in fits and starts and in different sizes.

The end of omicron was almost to the point of visualization, but we roll into yet another macro crisis of many groups’ makings.

Tech doesn’t operate in a vacuum, and politics, more often than I would like to admit, sometimes do overlap a great deal.

The world has changed dramatically in the past 14 days and the knock-on effects mean that American tech companies and their trillion dollars business models are pulling out of Russia, a country with a population close to 150 million, in droves.

It is what it is, and life moves on.

Netflix (NFLX) has been in operation in Russia since 2016 and the decision to vacate Russian business means they will lose around 1 million subscribers.

Most likely the worst tech company to work for right now in the world must be EPAM Systems (EPAM).

The internal chaos going on mainly stems from the 58,000 employees, with 14,000 of them in Ukraine and more than 18,000 staff in Belarus and Russia, according to company filings with the U.S. Securities and Exchange Commission.

EPAM’s stock is down 74% YTD in 2022 and is a stock that epitomizes the situation in Eastern Europe right now.

When workers refuse to work with each other, it’s hard to imagine that much gets done at all.

And this is just the tip of the iceberg.

The American tech withdrawals encompass all shapes and sizes.

Apple and Microsoft both said no bueno to selling products in Russia.

Game maker EA pulled the plug as well.

Google and Twitter have suspended advertising in Russia.

It’s a terrible time to monetize a YouTube channel in Russia because Google won’t pay you for it.

Likewise, Snap (SNAP) has pulled its marketing dollars from Russia too.

Another sonic boom hit Russian tech when Airbnb room-rental service suspended all operations in Russia and Belarus and has said its nonprofit subsidiary will offer free temporary housing to 100,000 Ukrainian refugees.

It's also waived host and guest fees for bookings in Ukraine, as people worldwide use Airbnb as a way to provide income directly to Ukrainians.

Adobe is halting sales of new Adobe products and services in Russia. In addition to making sure its products and services are not being used by sanctioned entities, Adobe is also cutting Russian government-controlled media outlets off from its cloud services.

What is emerging as quite black and white is that American technology companies hoping to apply their business model in autocratic states doesn’t integrate as well as first thought.

The weak rule of law along with all-powerful demagogue leaders make it hard to sustain any sort of business carve-out for the long term.

Eventually, many American companies are forced to abandon their ambitions in these marginal states.

The next question a tech investor must ask is will the American tech sector follow the lead from Russia and pull out from China.

Obviously, this has major implications for companies like Apple, Micron, and a handful of American tech companies that are entrenched in the Chinese economy and society.

Many people think this will blow over and tech will come back front and center, but short-term, this is highly negative for American tech stocks.

The more this situation drags out, the higher risk American tech is more involved in this mess from a different gateway.

The tech portfolio has been outright short recently and it was the perfect call to sell the dead cat bounce in growth tech like Teladoc (TDOC) and ARKK funds (ARKK).

Global Market Comments

March 4, 2022

Fiat Lux

Featured Trade:

(MARCH 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (TSLA), (FCX), (JPM), (BAC), (MS), (TLT),

(TBT),(BA), UPS (UPS), (CAT), (DIS), (DAL),

(GOLD), (VIX), (VXX), (CAT), (BA)