Mad Hedge Technology Letter

January 22, 2024

Fiat Lux

Featured Trade:

(TAKE A DEEP BREATH WITH AI)

(NVDA), (QRVO), (GOOGL), (AMZN), (AMD), (AVGO), (AAPL), (AI)

Mad Hedge Technology Letter

January 22, 2024

Fiat Lux

Featured Trade:

(TAKE A DEEP BREATH WITH AI)

(NVDA), (QRVO), (GOOGL), (AMZN), (AMD), (AVGO), (AAPL), (AI)

Stocks and firms tethered to artificial intelligence won’t always have a one-way joyride to profits.

The honest truth is that the road will be met with drawbacks some years and the sector will need time to digest the new developments.

Mainstream tech has made most people believe that AI can do no wrong in the short-term future.

There is a consensus that it’s the panacea for everything and anything.

The Magnificent 7 tech firms are priced for an AI boom and the hype is there, but it will take some time for AI to really filter into meaningful balance sheet development.

We are still in the beginning stages.

It’s not surprising that the Massachusetts Institute of Technology published a study that sought to address fears about AI replacing humans in a swath of industries and found that artificial intelligence can’t ACTUALLY replace the majority of jobs right now in cost-effective ways.

It’s important to note this report because much of AI has been celebrated with no mention of cost control or benefit versus the price or expenses incurred.

Any corporate tech will need to evaluate whether it’s worth gutting whole divisions to replace it with AI.

In many cases in early 2024, this type of strategy to a workforce could turn into an unmitigated disaster.

For instance, a new AI study found only 23% of workers, measured in terms of dollar wages, could be effectively supplanted. In other cases, because AI-assisted visual recognition is expensive to install and operate, humans did the job more economically.

The adoption of AI across industries accelerated last year after OpenAI’s ChatGPT and other generative tools showed the technology’s potential. Tech firms from Microsoft and Alphabet in the US to Baidu and Alibaba in China rolled out new AI services and ramped up development plans which could serve as a canary in the coal mine for things to come. Fears about AI’s impact on jobs have long been a central concern.

Computer vision is a field of AI that enables machines to derive meaningful information from digital images and other visual inputs, with its most ubiquitous applications showing up in object detection systems for autonomous driving or in helping categorize photos on smartphones.

The cost-benefit ratio of computer vision is most favorable in segments like retail, transportation, and warehousing.

The study was funded by the MIT-IBM Watson AI Lab and used online surveys to collect data on about 1,000 visually assisted tasks across 800 occupations. Only 3% of such tasks can be automated cost-effectively today, but that could rise to 40% by 2033 if data costs fall and accuracy improves.

When getting academic about the subject, many projections feel way too ambitious.

AI won’t take over the workforce in the next few years and will struggle to make inroads before 2030.

That doesn’t mean firms like Nvidia, AMD, Qorvo, and Broadcom will not sell AI-based chips promising better AI.

That doesn’t mean firms like Google, Apple, Microsoft, Amazon, and Meta won’t feel a small AI bump in revenue.

There certainly will be some changes, but wholesale transformation is a ways off.

I believe the AI hype has gotten too far over its skis.

Tech needs to slow down and make sure it’s properly implemented and the real effects will be seen after 2030.

Mad Hedge Technology Letter

May 22, 2023

Fiat Lux

Featured Trade:

(BUY EMERGING CHIP COMPANIES ON BIG DIPS)

(SWKS), (CRUS), (QRVO)

So what about these small chip companies that attach themselves to Apple’s future?

The ones like Qorvo (QRVO), Skyworks Solutions (SWKS), and Cirrus Logic (CRUS).

Many refuse to invest in them because they are too reliant on Apple.

I would argue the exact opposite.

It’s exactly because they have strong relationships with Apple that readers need to invest in these stocks.

The issue is that they are highly volatile and missing the optimal entry point can mean the difference between a profit and a loss.

Apple can’t develop everything internally.

It’s just too much to do.

I don’t believe the tech giant could gradually replace most of its third-party components with first-party ones.

Furthermore, I do not see Apple abruptly swapping suppliers or canceling an existing supplier's orders with its competitors to secure lower prices.

As a result, most of Apple's suppliers can negotiate favorable terms.

For 2023, iPhone shipments appear stable as the market continues to recover from weak demand and ongoing macroeconomic challenges, but I believe this is just a short-term blip.

Cirrus Logic mainly sells audio converters and chips, but it also develops other mixed-signal processing chips for wireless headsets, wearables, augmented reality/virtual reality (AR/VR) headsets, notebook computers, and mobile devices. Apple installs Cirrus' audio chips and IC controllers in its iPhones, iPads, and Macs.

Skyworks produces a wide range of wireless chips for the mobile, automotive, home automation, wireless infrastructure, and industrial markets. Apple installs Skyworks' wireless chips in its iPhones, iPads, Macs, Apple Watches, and other devices.

Lumentum is a diversified supplier of optical chips for service providers, 3D-sensing chips which are used in mobile devices, cars, 3D printers, and other industrial machines, as well as commercial lasers for manufacturing various products. Apple uses Lumentum's 3D-sensing chips and lasers to power its Face ID features.

These companies bask in the glory of being connected to Apple when many other chip companies wish they were in the same position.

Cirrus relied on Apple for 79% of its revenue in 2022 and the gains from this contract are precisely why it is great to hold this company's stock.

Skyworks generated 58% of its revenue from Apple in fiscal 2022, while Lumentum generated 29% of its revenue from Apple in 2022.

The semiconductor industry has been prone to cycles. Periods of soaring demand are followed by periods of drought, causing some wild swings in many chip stocks. But some news reports predict that because of the demand for chips throughout the economy, these boom-bust cycles might be over.

Semiconductors are now going into various devices between 5G, cloud datacenters, phones, PCs, laptops, cars are using more and more semiconductors that the demand is becoming so diversified and that supply is becoming so expensive to bring on. It's going to be much more of a steadier business going forward, more like a steady growth business rather than a cyclical business with booms and busts.

Don’t believe the naysayers who urge investors to stay out of chip stocks because of overreliance. That is like saying Warren Buffet is too reliant on Apple which is false.

Wait for a big dip of 15% or 20% to invest in these small chip stocks.

Mad Hedge Technology Letter

November 5, 2021

Fiat Lux

Featured Trade:

(LET THE DUST SETTLE FOR THIS CHIP STOCK)

(QRVO)

This is not an uncertainty at the end of the tunnel turning out to be a train-like situation with chip company Qorvo, Inc. (QRVO).

Hardly so.

The 17% sequential decline QRVO is guiding for their mobile business in December isn’t something investors will dance in the streets about.

The chip sector is an anomaly because of the boom-bust nature of the semiconductor cycle.

Here at the Mad Hedge Technology Letter, we find it more conducive to trade in annuity-like software revenue where CFOs have a better handle on predicted cash flow and state of the balance sheet.

Qorvo, Inc. (QRVO) decreased its December revenue forecast by about $150 million, and about $135 million of that was in mobile chips.

The balance of the decrease was also in Infrastructure and Defense Products (IDP).

Of the $135 million roughly in mobile, QRVO has been wrought by supply constraints, specifically meaning their suppliers not delivering supply for them.

Sucks, right?

The result is QRVOs customers not receiving their allotment of chipsets, thus not able to build their product and use QRVOs products, a type of vicious cycle of being empty pocketed for everyone.

The earnings’ quarter for Qorvo epitomizes the 2021 economy and that’s not only for semiconductor chips — the master word being supply constraints.

The demand part of the equation has also been affected particularly in parts of Asia but is secondary to the supply headwinds.

I am disappointed with the December guide, but it’s not the death of QRVO as I see it.

They need to reinforce a commitment to keep the product channel healthy and give a guide that most accurately describes the supply/demand fronts.

It’s never just cut and dry, but admittedly, visibility is cloudy now and that must be reflected in the management rhetoric and prognosis.

Generally speaking, Qorvo has a great business with best-of-breed products, and we shouldn’t lose sight of that.

Regarding the supply environment, it’s been tough sledding for 1.5 years, almost two years now so it’s not just a 1-day hangover.

The supply environment deteriorated, but inventories are still healthy.

Trying to sort out the internal calculus, I have full faith in QRVO to get their shop in order and meaningfully cast a better light in the March quarter.

I feel that is right around the corner.

The silver lining is that QRVO’s gross margin outlook is intact around 52%.

Opex is in control, and they’re investing in the future of the business.

These investments entail both the traditional parts of the business and newer parts of the business.

And in the end, EPS continuity is hardly affected so we can still count on the same type of elevated profitability which is a hallmark of a good company.

Most chip companies aren’t like crappy loss-making Uber and firms of that ilk.

Absorbing a bit of a correction is nothing to freak out about, but I would say it's the right thing for them to do and will curry investment trust over the long haul.

I can confidently say that I feel great about QRVO’s strategic position as we creep closer to 2022.

They wield premium technology and products, serving attractive end markets growing double-digits, and I fully expect them to outperform next year.

Operations are like a well-oiled machine with sustained margins over 52%, expanding operating margins, and the underlying strength of the company is nothing to diminish.

Considering the concrete evidence, this will be a great semiconductor firm to buy on the dip once the stock settles down from its cringeworthy sell-off.

Granted, the 22% drop from its peak is precipitous, but these smaller chip companies have heightened embedded volatility because of their diminutive size.

That’s not to say they are bad.

The stock has still more than doubled since early 2020 and once the stock levels off, there will be a massive tranche of buyers bidding this chip company back up which should see the stock blast past $200 and beyond.

This could happen by the back half of 2022 and by that time you’ll be glad you bought at discount levels.

Mad Hedge Technology Letter

March 23, 2020

Fiat Lux

Featured Trade: (THE CORONA DRAG ON 5G)

(VZ), (T), (AAPL), (NFLX), (NVDA), (XLNX), (QRVO), (QCOM)

It will be inevitable – the 5G shift in 2020 will be delayed.

Last year, 5G was available on only about 1% of phones sold in 2019 and demand has cratered this year because of exogenous variables.

Up to just recently, Apple (AAPL) was the bellwether of the success of tech with wildly appreciating shares due to the expected ramp-up to a new 5G phone later this year.

Well, things are more complicated now.

I will be the first one to say it - the new Apple 5G iPhone will be delayed until 2021 – the project has been thrown into doubt because of a demand drop off and headaches with the supply chain in China.

The phenomenon of 5G cannot blossom until consumers can upgrade to 5G devices.

Concerning all the media print of China Inc. going back to work, don’t believe a word of it.

People of the Middle Kingdom are sitting at home just like you and me by navigating around top-down government edicts.

Instead of the perilous commute in a country of 1.4 billion people, Chinese workers are fabricating attendance figures per my sources.

Overall data is grim - global smartphone shipments dropped 38% year-over-year during February from 99.2 million devices to 61.8 million - the largest fall ever in the history of the smartphone market and that is just the tip of the iceberg.

The new data point underscores the magnitude of how the coronavirus is sucking the vitality out of the tech ecosystem in China and thus the end market for global consumer electronics.

The statistic also foreshadows imminent trouble in the smartphone market as other regions have now shut down not only in China but the manufacturing hubs of South East Asia.

The outbreak squeezes both supply and demand.

Factories in Asia are unable to manufacture phones as usual because of obligatory government shutdowns and complexities securing critical components from the supply chain.

5G has been hyped up as the great leap forward for wireless technology that will usher in unprecedented new use cases supercharging global GDP — from driverless transport to robotic automation to smart football stadiums.

And coronavirus is just that Godzilla destroying 5G momentum down.

Mass quarantines, social distancing, remote work, and schooling have been instituted in American cities, meaning that the current network carriers are swamped and overloaded with a surge in data usage.

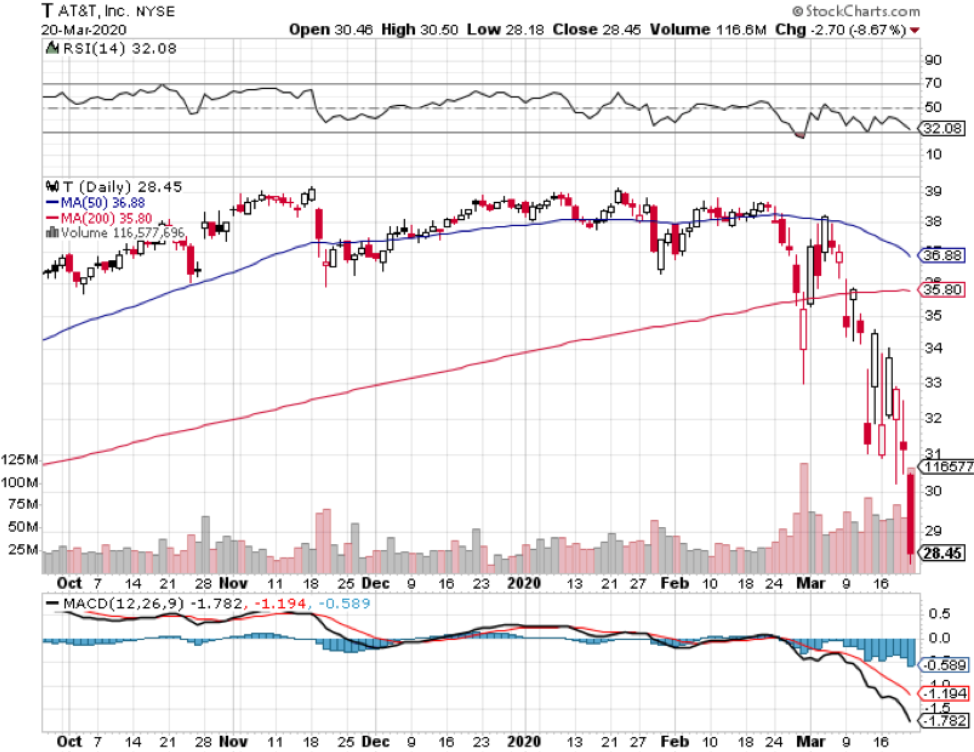

The Verizon’s (VZ) and the AT&T (T) Broadbands of America are currently focused on maintaining their current core customers, adding extra broadband to handle the increased load, and making sure the health of the network stays intact.

This is a poor climate to upsell products to beleaguered Americans who have just lost income and possibly their house because they cannot pay mortgages.

Services such as YouTube and Netflix (NFLX) have even decreased the quality of streaming on their platforms to handle the dramatic spike in extra usage in Europe with the whole continent locked down.

The Chinese consumer was the Darkhorse catalyst to ramp up the global economic expansion during the last economic crisis, picking up world spending in 2009.

On the contrary, this group of super spenders is less inclined to save the global economy this time around because they are saddled with domestic debt.

Just as unhelpful to Silicon Valley revenues, the technology relationship at the top of the governments are poised to worsen because of the health scare.

The U.S. administration has already banned the use of Chinese components in the U.S. 5G network amid suspicions the devices would be used for espionage.

Back stateside, I believe the U.S. telecoms will explicitly detail a sudden slowdown in the 5G network rollout during their next earnings report.

The telecom companies have been able to successfully handle the extra incremental load, but it has had to allocate resources to service the extra volume.

In the meantime, companies will shift to doing infrastructure and site preparation in anticipation of the re-build up to 5G, but that could be next to be put on ice if crisis management moves to the forefront.

Considering every 5G base station is being manufactured in Asia, one must be naïve in believing all is well and they will probably need to do what the 2020 Tokyo Olympics will shortly do – postpone it.

It’s not business as usual anymore.

This time it’s different.

The world just isn’t ready to digest such a shift in global business as 5G until the fallout of the coronavirus is in the rear-view mirror.

The 5G phenomenon underlying effect is to supercharge globalization into smaller networks of interconnectivity and that is not possible during a black swan event like the coronavirus which is the antithesis of globalization and interconnected business.

Just take the situation across the Atlantic Ocean in Europe, UBS Group AG, and Credit Suisse Group AG required clients to post additional collateral, and money managers in New York are preparing term sheets for ultra-rich Americans to urgently meet margin calls.

Many people are scurrying back to their doomsday’s shelter and that does not scream global business.

If you thought gold was the safe haven – wrong again – it experienced back-to-back weekly losses as margin pressures force fire sales of gold to raise cash.

Another glaring example are the assets of Eldorado Resorts Inc., controlled by the founding Carano family, which burned $28.7 million of stock in the casino entity to meet a margin call to satisfy a bank loan.

Things are that bad now!

Sure, telecom players might argue that a sudden influx of workers from home necessitates more investment in 5G, but if they have no income, all bets are off.

The capacity of 4G home broadband has proved it is good enough for today’s demands and it means the last stage of 4G will be a high data consumption longer phase before business lethargically pivots to 5G in 2021.

Verizon’s CEO Hans Vestberg said last year that half the U.S. will have access to 5G by the end of 2020, and I will say that is now impossible.

This sets up a generational buy in the Silicon Valley chip names involved in 5G after coronavirus troubles peak such as Nvdia (NVDA), Xilinx (XLNX), Qorvo (QRVO), and QUALCOMM Incorporated (QCOM).

Mad Hedge Technology Letter

January 29, 2019

Fiat Lux

Featured Trade:

(WHATS BEHIND THE NVIDIA MELTDOWN),

(QRVO), (MU), (SWKS), (NVDA), (AMD), (INTC), (AAPL), (AMZN), (GOOGL), (MSFT), (FB)

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.