Mad Hedge Technology Letter

December 20, 2018

Fiat Lux

Featured Trade:

(MICRON TECHNOLOGY BOMBS AGAIN)

(MU), (FDX), (UPS), (AAPL), (QRVO), (SWKS), (NXPI), (CRUS), (LITE),

Mad Hedge Technology Letter

December 20, 2018

Fiat Lux

Featured Trade:

(MICRON TECHNOLOGY BOMBS AGAIN)

(MU), (FDX), (UPS), (AAPL), (QRVO), (SWKS), (NXPI), (CRUS), (LITE),

If there was ever a canary in the coal mine, we got one with chipmaker Micron (MU) delivering weak earnings results missing on the top line but squeaking through a one-cent beat on the bottom line.

Love them or hate them, chip companies are susceptible to the boom-bust cycle that is a hallmark of the chip industry.

The beginning of the bust stage of the cycle is upon us with management detailing an “inventory adjustment” that put a damper on revenue.

Micron followed that up by reducing capex for next year and it will take 2-3 quarters to work off this bloated inventory channel.

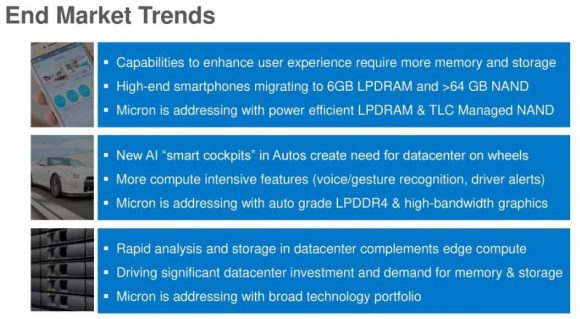

The perpetrator to the inventory backlog is the smartphone industry.

President and CEO of Micron Sanjay Mehrotra particularly noted “high-end smartphones” as the malefactor tugging down the demand.

This is another damming testament to the prospects of Apple’s (AAPL) suppliers Quorvo (QRVO), Skyworks Solutions (SWKS), NXP Semiconductors (NXPI), Cirrus Logic (CRUS), and Lumentum Holdings (LITE) who can’t catch a break.

The last six months have fired a barrage of poison-tipped arrows at their core business and these stocks are squarely in the no-fly zone until Apple and the trade war can conjure up some good news.

To say these shares are oversold is an understatement, but we are in an extreme trading environment with volatility shooting up the wazoo.

Further reducing the glimmer, Chinese tariffs took up a worrying amount of the conference call dialogue. Investors found out that tariffs pinged half a percent of gross margins.

I have been outright bearish the chip industry from the middle part of the year and Micron is heavily reliant on China for about half of its revenues which is a death sentence in December 2018.

As the China risks have spiked after each head fake détente, so have the execution risks to chip companies with an overly reliant manufacturing process in China.

Not only has the execution risk ratcheted up, but the regulatory risk through costly tariffs is now eroding Micron’s margins.

If you thought that was a downer, then FedEx (FDX) made sure the nail was in the coffin by its ghastly earnings report.

The stock sold off hard confirming fears that global growth is decelerating.

Management did not mince their words about the state of the world and investors usually listen because FedEx is a reliable yardstick of the bigger global economy.

CEO of FedEx Fred Smith offered an olive branch painting a picture of a “solid” US economy, but the conundrum is that the US economy and any other country don't exist in a vacuum and that has been highly evident in Britain who is engaging in economic suicide by disengaging from the globalized world.

Smith cited Europe as a stumbling block and blamed the bulk of weak guidance on “bad political choices”, a thinly veiled dig at the poor level of governance carried out around the world lately.

I might chime in that it is quite strange when political parties and sovereign nations adopt the game of chicken as the leading political strategy applying it to everything and anything.

The side effects to business have been startling with management unable to assuage investor sentiment and business plans shredded apart because of impulsive policy moves.

Politicians aren’t grasping fully that stock market moves are inherently tied to the news cycle and the overwhelming volume of bad news that shouldn’t be as bad as it should be, has a multiplier effect on the stock market algos that go haywire.

It truly is the world of the algos and humans are living in their world and not the other way around.

The most important takeaway from FedEx is what they didn’t say.

Early development of the de-facto Amazon Airlines has already cost FedEx up to 3% of total volume growth.

And this is just the beginning.

Amazon is still feeling around for the rocks at the bottom while it tries to cross the river.

Once it masters logistics, expect a radical swivel towards the integration of their own airline into the bulk of Amazon.com’s package deliveries.

And when FedEx’s management claims that the market has gotten it wrong about the Amazon threat, that means the market is completely correct.

The market is always right.

Amazon’s master plan is to vertically integrate every last process down to the last mile, the doorbell, and now the microwave as Amazon has rolled out a myriad of smart home products.

FedEx management has to be blind to understand this won’t damage future sales.

It is materially false if FedEx thinks Amazon is not competing with them, and the sad part of this is there is not much FedEx can do about it.

The shipping giant cut its 2019 earnings forecast between $15.50 and $16.60 per share — from $17.20 to $17.80 a share.

FedEx’s goal of eclipsing $1.5 billion in operating income by fiscal 2020 has been shelved disappointing investors. FedEx cratered 12% on a day that saw the Fed do its best body slam imitation on the market.

The first phase of the logistics swivel is taking delivery of 40 planes and constructing a hub that will be able to operate 100 planes, then it will do as Amazon does with everything – scale it to the hills.

FedEx and UPS have a few years to figure out how to counteract this existential crisis and not decades.

Technology moves that fast now in this interconnected world.

Domestic volume comprises 17% of revenues at UPS and 19% at FedEx, management won’t be able to hide this problem under the carpet as the drag becomes highly visible like a sore thumb.

Analysts expect Amazon Air to offer more than slim savings to its business model saving between $2 to $4 per package next year.

The annual savings add up from $1 billion to $2 billion or 3% to 6% of its global shipping costs.

It is spot-on to admit that over the last few years, the explosion of packages during the holiday shopping season has put higher levels of stress on the U.S. Postal Service, UPS (UPS), and FedEx.

Even though overloaded with business, all three carriers have posted record levels of on-time deliveries and they appear to be handling the surge in volume.

But there will come a moment in time when an inflection point will give Amazon the keys to the car.

They will suddenly stop offering their e-commerce packages to these three carriers and business will drop off a cliff for them.

That is the future these three are confronted with and there is nothing they can do unless they build their own Amazon.com which is a pie in the sky dream at this point.

Amazon is out to prove they can execute the logistic part of their business cheaper and faster than anyone else because of the superior management and mountain of data they can act on.

I believe it will happen.

Part of stretching themselves with a new army of minions in Washington D.C., New York, and Nashville is partly about fulfilling the job of comprehensively and vertically integrating their e-commerce platform.

It will take a horde of workers to make this happen.

If the prophecy from FedEx management comes true and the global economy indeed softens next year, the stock will bear the brunt of the downside momentum and UPS too.

Stay away from the trio of deliverers. There are healthier fishes in the sea.

And as for the chip sector and Apple, wait on the sidelines for some good news.

Mad Hedge Technology Letter

May 24, 2018

Fiat Lux

Featured Trade:

(MICRON'S BLOCKBUSTER SHARE BUYBACK)

(MU), (AMZN), (NFLX), (AAPL), (SWKS), (QRVO), (CRUS), (NVDA), (AMD)

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

Growth - Check. Accelerating Revenue - Check. Margins - Check. Earnings beat - Check. Guidance hike - Check.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

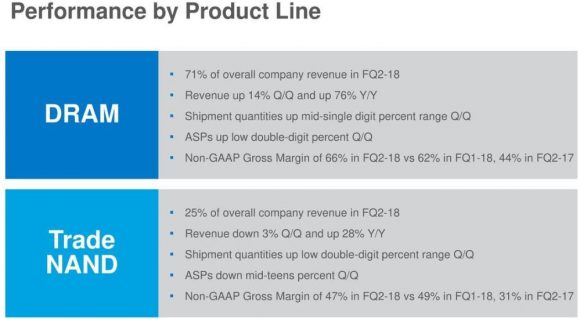

Half way into 2018, and there is still a dire shortage of DRAM chips.

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

_________________________________________________________________________________________________

Quote of the Day

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.

Mad Hedge Technology Letter

April 23, 2018

Fiat Lux

Featured Trade:

(HOW NETFLIX CAN DOUBLE AGAIN),

(NFLX), (AMZN), (IQ), (ORCL), (MU), (AMAT), (CRUS), (QRVO), (IFNNY), (NVDA), (JD), (BABA), (MSFT)

The first batch of earnings numbers are trickling in, and on the whole, so far so good.

A spectacular earnings season will further cement tech's position at the vanguard of the greatest bull market in history.

The bull case for technology revolves around two figures indicating "RISK ON" or "RISK OFF".

The first set of numbers from Netflix (NFLX) emanated sheer perfection.

Netflix has gambled on its international audience to drive its growth and unceasing creation of premium content to reach these lofty targets set forth.

It worked.

Consensus was that domestic subscription growth had peaked, and Netflix would have to lean on overseas expansion to beat earnings estimates.

American subscription growth knocked it out of the ballpark, beating expectations by 480,000 subscriptions. The street expected only 1.48 million new adds. The 1.96 million shows the American online streamer is resilient, and the migration toward cord-cutting is happening faster than initially thought.

International adds were pristine, beating the 5.02 million estimates by 440,000 million new subscribers.

Content is king as Netflix has proved time and time again (we notice that here at Mad Hedge Fund Trader, too). Netflix plans to fork out about 700 original series in 2018.

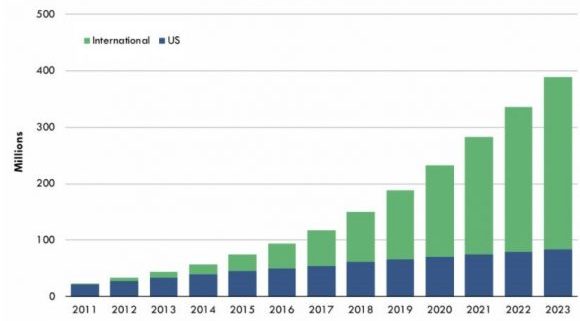

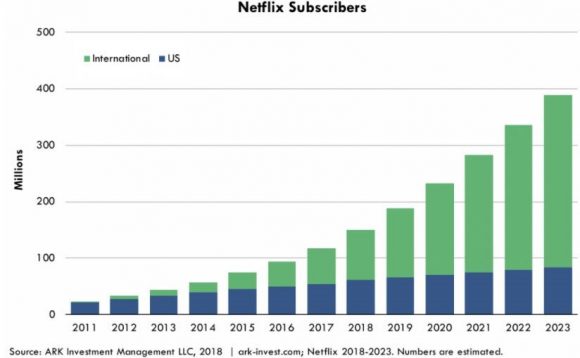

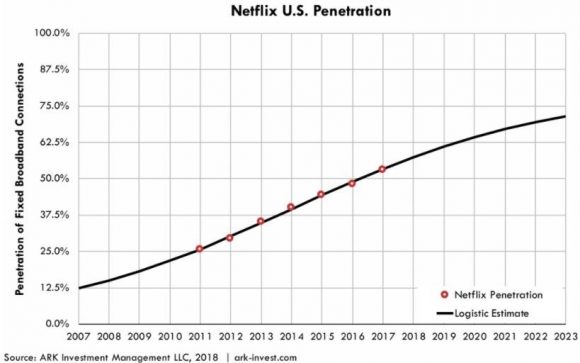

By 2023, Netflix could grow its subscriber base to close to 400 million. The potential for international advancement is immense considering foreign companies are playing catch-up and cannot compete with the level of Netflix's content.

The earnings report coincided with Netflix announcing a forceful push into Europe, doubling its allocated content-related investments to $1 billion.

All of Netflix's estimates take into consideration that it is shut out of the Chinese market. Ironically, the Netflix of China, named iQIYI (IQ), just recently went public on the Nasdaq.

Amazon Web Services (AWS), the cloud-arm of Amazon (AMZN), revenue numbers are the other numbers that are near and dear to the pulsating heartbeat of the bull market.

Jeff Bezos, Amazon's CEO, penned a letter to shareholders that Amazon prime subscribers blew past the 100 million mark.

The positive foreshadowing augurs nicely for Amazon to surprise to the upside when it reports earnings next week on April 26.

Expect more of the same from cloud companies that are overperforming.

The few glitches in tech are minor. It is mindful to stay on the right side of the tracks and not venture into marginal names that haven't proved themselves.

For instance, Oracle (ORCL) had a good, not great, earnings report but shares still cratered after CEO Safra Catz dissatisfied analysts with weak cloud forecasts of just 19%-23% growth.

The street was looking for cloud guidance over 24%. Oracle is still being punished for its legacy tech segments.

The chip sector got pummeled after several chip manufacturers announced weak supply order from Apple.

This is hardly a surprise with Apple slightly missing iPhone estimates last quarter by 1%.

Chip stocks such as Lam Research (LRCX), Micron (MU), and Applied Materials (AMAT) look like affordable bargains. They should be seriously considered after share prices stabilize buttressed by support levels.

The outsized problem is that hardware suppliers have headline risks because of large cap tech's preference toward vertically integrating.

Along with price efficiencies, vertically integration aids design aspects and streamline product production time horizons.

This is not the end of chips.

Consumers need the silicon to generate and extract all the data coming to market.

Particularly, Apple (AAPL) went over its skis trying to push expensive smartphones to a saturated market when all the rip-roaring growth is at the low end of the market.

Apple still managed to sell more than 77 million iPhones, but the trade war rhetoric will deter Chinese consumers from purchasing American tech products. Until now, Apple has counted on China as its best growth prospect. The administration had other ideas.

Any noteworthy Apple supplier has gotten punched in the nose, but crucially, investors must stay out of the SMALLER chip players that rely on narrow revenue sources to keep them afloat.

Bigger chip companies can withstand the shedding of a few revenue sources but not Cirrus Logic (CRUS).

(CRUS) shares have been beaten mercilessly the past year sliding from $68 to a horrifying $37.74 today.

(CRUS) produces audio amplifier chips used in iPhone devices, and weak iPhone X guidance is the cue to bail out of this name.

The company extracts more than 75% of its revenues by selling audio chips used in iPhone devices. Ouch!

Last quarter saw horrific performance, stomaching a 7.7% decline in revenues due to tepid demand for smartphones in Q4 2017.

Cirrus Logic provided an underwhelming outlook, and it is not the only one to be beaten into submission behind the woodshed.

Apple has signaled to its suppliers that it will view production in a different way.

Imagination Technologies, a U.K. company, was informed that its graphic chips are not needed after 2018.

Dialog Semiconductor, another U.K.- based operation, shared the same destiny, as its power management chip was cut out of the production process, sacrificing 74% of revenue.

To top it all off, Apple just announced it plans to manufacture its own MicroLED screens in Silicon Valley, expunging its alliance with Samsung, Sharp, and LG, which traditionally yield smartphone screens for Apple. And Apple plans to make its own chips, phasing out Intel's chips in Apple's MacBook by 2020.

Qorvo (QRVO), Apple's radio frequency chips manufacturer, also can be painted with the same brush.

Apple was responsible for 34% of the company's total revenues in 2017.

Weak iPhone guidance set off a chain reaction, and the trembles were most felt at the bottom feeder group.

Put Infineon Technologies (IFNNY) in the same egg basket as Qorvo and Cirrus Logic. This company installs its cellular basebands in iPhones.

FANG has split into two.

Netflix and Amazon continue producing sublime earnings reports, and Apple and Facebook have hit a relative wall.

It will be interesting if the government's harsh rhetoric toward Amazon amounts to anything.

One domino that could fall is Amazon's lukewarm relationship with the US Postal Service.

Logistics is something the Chinese Amazon's JD.com (JD) and Alibaba (BABA) have successfully adopted. Look for Amazon to do the same.

However, I will say it is unfair that most tech companies are measured against Netflix and Amazon, even for Apple, which earned almost $50 billion in profits in 2017.

It is insane that companies tied to a company that prints money are reprimanded by the market.

But that highlights investors' pedantic fascination with pandemic growth, cloud, and big data.

Making money is irrelevant today. Investors should be laser-like focused on the best growth in tech such as Amazon, Netflix, Lam Research, Nvidia (NVDA), and Microsoft (MSFT), which know how to deliver the perfect cocktail of results that delight investors.

__________________________________________________________________________________________________

Quote of the Day

"$500? Fully subsidized? With a plan? That is the most expensive phone in the world. And it doesn't appeal to business customers because it doesn't have a keyboard. Which makes it not a very good email machine." - said former CEO of Microsoft Steve Ballmer on the introduction of the first iPhone.