Mad Hedge Biotech and Healthcare Letter

April 10, 2025

Fiat Lux

Featured Trade:

(THE $5 BILLION SECRET I SPOTTED IN MY DOCTOR'S WAITING ROOM)

(AMGN), (NVO), (LLY), (MRK), (REGN)

Mad Hedge Biotech and Healthcare Letter

April 10, 2025

Fiat Lux

Featured Trade:

(THE $5 BILLION SECRET I SPOTTED IN MY DOCTOR'S WAITING ROOM)

(AMGN), (NVO), (LLY), (MRK), (REGN)

Last Tuesday, my orthopedist kept me waiting 40 minutes past my appointment time – just long enough for me to witness what Wall Street's finest analysts have somehow managed to miss.

As I sat thumbing through a dog-eared copy of Golf Digest from 2018, I counted eight different patients called in for Prolia injections.

By the sixth one, I'd put down the magazine and started taking notes on my phone. By the eighth, I was already mentally calculating position sizes for my portfolio.

"You know what you just saw?" my doctor asked when he finally saw me. "That's Amgen's cash cow – $5.4 billion in sales last year for a twice-yearly injection. And guess what? Half these patients will be on it for life."

When I pressed him on competing drugs, he just laughed. "Their sales reps bring the best lunches. But seriously, it works, patients tolerate it, and insurance covers it. In medicine, that's the holy trinity."

While half of Wall Street hyperventilates about which pharmaceutical giant will dominate the weight loss market, and the other half chases whatever shiny tech story came out this morning, they're all missing Amgen (AMGN) – a money-printing machine trading at just 14.9 times earnings with a 3.1% dividend that grows like clockwork.

I've been investing in pharmaceutical companies since I covered Merck's (MRK) explosive growth for The Economist in the late 1970s, and one lesson has remained constant: the market consistently underestimates companies with proven track records during transitions.

Amgen, trading at $307, is a textbook example of this phenomenon right now.

The headline numbers don't initially spark excitement – management is guiding for modest 5% revenue growth and 4% EPS growth this year. But having analyzed hundreds of pharma companies over five decades, I know these conservative guidance figures are often the prelude to significant outperformance.

What matters more is their $5.9 billion R&D investment last year (up 25% from 2023) and the underappreciated potential of their pipeline.

Look beyond the surface, and you'll find Amgen has quietly built something remarkable. While everyone's fixated on Novo Nordisk’s (NVO) Ozempic and Wegovy, few have noticed that Amgen's existing product portfolio is delivering solid results.

Inflammation drug TEZSPIRE grew 71% year-over-year and is approaching the $1 billion annual sales milestone. Oncology drug BLINCYTO jumped 41%, and their cholesterol drug Repatha, combined with bone health treatment EVENITY, delivered $1 billion in year-over-year growth.

The real hidden value lies in Amgen's obesity program. The anti-obesity market that barely existed a few years ago has exploded to $2.2 billion and is projected to grow at 30% annually through 2030.

Eli Lilly (LLY) and Novo Nordisk have seen their market caps soar into the stratosphere on the strength of their GLP-1 drugs, but Amgen's market valuation doesn't reflect any meaningful potential from MariTide, their Phase 3 obesity candidate.

This reminds me of 2012 when I began accumulating Regeneron (REGN) while the market was completely missing the potential of Eylea. That position delivered a 580% return over the following three years.

What's particularly attractive about Amgen is the margin of safety it offers. With a 3.1% dividend yield (backed by a manageable 45% payout ratio and 13 consecutive years of growth), a forward P/E of just 14.9, and a fortress-like 46.3% operating margin, you're being paid to wait for the pipeline to deliver.

The company has been aggressively paying down the debt from its Horizon Therapeutics acquisition, reducing long-term obligations by $6.6 billion last year alone.

Their financial discipline stands in stark contrast to many of the speculative biotech plays I've been pitched recently. At a dinner with venture capitalists in Boston last week, I listened to presentation after presentation about pre-clinical assets with billion-dollar valuations and no revenue in sight.

Meanwhile, Amgen generated $33.4 billion in sales last year with industry-leading EBITDA margins of 45%.

Of course, there are risks. The upcoming patent expiration of osteoporosis drug Prolia this year creates a revenue gap that needs filling.

The Trump administration's Department of Government Efficiency (DOGE) initiative could potentially impact FDA testing labs, slowing approval timelines. But these concerns are already priced into the stock, while the potential upside from MariTide and other late-stage candidates is not.

Having navigated multiple market cycles since the 1970s, I've learned that the best investments often come when solid companies are temporarily overlooked during market rotations. Amgen remains a proven pharmaceutical innovator with strong cash flows, growing dividends, and a promising pipeline that offers compelling value.

I started building a substantial position in Amgen at around $260 during the post-election pharmaceutical sell-off and have continued to accumulate shares on weakness.

With a reasonable valuation, strong pipeline optionality, and dividend income that beats 10-year Treasury yields, Amgen represents the kind of steady compounder that has consistently outperformed over full market cycles.

In my decades of investing, I've found that buying excellent businesses during periods of unwarranted pessimism is the closest thing to a guaranteed winning formula.

With Amgen, you're essentially being paid a 3.1% annual dividend to own a company that could deliver a major surprise in the obesity market – the same market that transformed Novo Nordisk and Eli Lilly into two of the world's most valuable companies.

Sometimes the smartest investments are like colonoscopies – nobody's excited to talk about them at parties, but they'll save your financial health in the long run.

Mad Hedge Biotech and Healthcare Letter

February 25, 2025

Fiat Lux

Featured Trade:

(WALL STREET'S MYOPIA IS YOUR OPPORTUNITY)

(REGN), (RHHBY), (AMGN), (AZN), (ABBV), (LLY)

While preparing my presentation for this week's Online Traders Conference, I came across a pattern that made me stop cold. You see, I've been gathering examples of how institutional investors quietly accumulate positions while retail traders are looking the other way.

And there it was, right in front of me - Regeneron Pharmaceuticals (REGN), displaying exactly the kind of setup I'll be warning traders about starting February 24.

You see, while everyone's been obsessing over the latest AI darlings, Regeneron has been quietly crushing it. Their Q4 revenue hit $3.79 billion, up 10.5% year-on-year.

But here's where it gets interesting - they beat consensus estimates by $43 million, and that's with their flagship eye drug Eylea taking a hit.

Speaking of Eylea, let's address the elephant in the room. Its sales dropped 11% to $1.19 billion, thanks to Roche's (RHHBY) Vabysmo muscling into their territory and Amgen's (AMGN) biosimilar crashing the party.

Four more biosimilars are waiting in the wings, held back only by patent disputes. Normally, this would send investors running for the hills.

But here's what the panic-sellers are missing.

Despite Eylea's challenges, Regeneron's non-GAAP EPS still climbed to $12.07, beating analyst expectations by 88 cents.

In fact, they've been playing jump rope with analyst estimates, leaping over them in 10 of the last 12 quarters. Yet their stock price has been doing its best impression of a sleeping cat - just lying there, barely moving.

As someone who's spent decades watching market cycles, I recognize this pattern.

We're in what technical analysts call an “accumulation phase.” While retail investors yawn and look elsewhere, institutional money is quietly building positions.

It's like watching a spring being compressed - boring until it isn't.

But here's what really got my attention: Regeneron just joined the dividend club. Starting March 20, they're paying $0.88 per quarter. Sure, the yield won't make income investors swoon, but that's not the point.

It reminds me of how AstraZeneca (AZN) played it - first, dominate growing markets, then gradually turn on the dividend spigot to attract the steady-money crowd.

They're also backing up the dividend with a $3 billion share buyback program.

With $9 billion in cash and short-term investments, they've got more dry powder than a Revolutionary War armory.

In Q4 alone, Regeneron spent $1.23 billion buying back shares - up 64.1% from last year.

And here's where it gets even more interesting. Their oncology franchise, led by Libtayo, is looking like a dark horse winner. Libtayo sales jumped 50.4% year-over-year to $367 million.

While that might not sound earth-shattering compared to cancer drug heavyweights like Merck's (MRK) Keytruda, Libtayo just pulled off something remarkable.

In their Phase 3 C-POST trial for high-risk skin cancer patients, Libtayo reduced death and disease recurrence risk by 68% compared to placebo.

Even better? Merck's competing trial for Keytruda in the same indication fell flat on its face. In this business, that's like watching your main competitor trip at the Olympic finals.

Looking ahead to 2029, I'm seeing revenue hitting $20.4 billion - think high single-digit growth each year. That would bring their price-to-sales ratio down from 5.12x to 3.53x.

Their non-GAAP EPS should hit $76.5, implying double-digit growth most years. With the stock currently trading at just 14.76x earnings - below most peers like AbbVie (19.06x) and Eli Lilly (64.96x).

On top of these, 2025 is packed with potential catalysts - clinical trial results and FDA decisions that could light a fire under the stock.

Analysts' average target is $929.37, suggesting about 38% upside. But in my experience, when you combine strong fundamentals, multiple growth drivers, and a market that's sleeping on the story, those targets often end up looking conservative.

Remember, the market loves nothing more than a comeback story.

With Regeneron, we might just be watching one unfold in slow motion. The question is: will you be holding shares when the spring finally releases?

For those who want to learn more about spotting these kinds of opportunities, I'll be diving deeper into institutional accumulation patterns at the Online Traders Conference running February 24 through March 1.

But don't wait for my presentation to take a serious look at Regeneron - the smart money isn't.

Mad Hedge Biotech and Healthcare Letter

January 16, 2025

Fiat Lux

Featured Trade:

(THE EYES HAVE IT)

(REGN), (SNY), (PFE), (BMY)

Last week, while waiting for my annual eye exam, I couldn't help but notice the parade of elderly patients shuffling in for their regular Eylea injections. My optometrist tells me these folks show up like clockwork every 4-8 weeks, rain or shine.

That's about to change, and therein lies a multibillion-dollar story.

You see, when Regeneron reported Q3 earnings on Halloween, boy, they sure had some treats for investors. Revenue hit $3.72 billion, up 11% YoY, with EPS coming in at a sweet $11.54.

But here's what really caught my attention: their cost of revenue was $1.762 billion, while R&D and SG&A expenses ran $1.271 billion and $714.4 million respectively.

Net income? A cool $1.34 billion. Not too shabby for a company whose main product is under siege from copycats.

Speaking of copycats, let's talk about Eylea. The original formula saw revenues drop 21% YoY to $1.145 billion – that's what happens when biosimilars crash your party.

This is where it gets interesting though: Eylea HD (think of it as Eylea's muscled-up big brother) jumped from a mere $43 million to $392 million YoY.

Sure, about $40 million of that came from wholesalers stocking up like it's Black Friday at Costco, but still – that's what I call a growth story.

I've been watching Regeneron since they were just a gleam in Wall Street's eye, and they've always had a knack for turning scientific breakthroughs into cold, hard cash.

Take Dupixent, their inflammation blockbuster co-developed with Sanofi (SNY). It just got FDA approval for COPD with an eosinophilic phenotype.

Why does this matter? Because we're talking about a $6 billion market opportunity here, folks.

About 36% of COPD patients have this particular flavor of the disease and trust me, there are more of them than you'd think still wheezing away on their old inhalers.

Want to know what else is cooking in their labs? They're working on antibodies that could make blood clots a thing of the past – think better than Eliquis, which pulls in $10 billion annually for Pfizer (PFE) and Bristol Myers Squibb (BMY). Their secret? Something called Factor XI, which could be a game-changer for the 1 in 5 patients at high risk for bleeding.

And because no self-respecting biotech can resist the siren call of the obesity market, they're also cooking up their own weight loss cocktail. Results won't drop until late 2025, but if they crack the code on keeping weight off AFTER stopping treatment, they'll have something Wegovy and Zepbound can't match.

The financials are rock solid, too: $2.012 billion in cash, $7.785 billion in marketable securities, and current assets of $19.334 billion versus current liabilities of just $3.661 billion.

They've generated $3.158 billion from operations in the first nine months of 2024 alone.

Yes, there's $1.984 billion in long-term debt, but with cash flow like that, it's about as worrying as a paper cut.

I've already started nibbling at Regeneron, and I'm looking to add more if it dips further. After all, this is a company that's proven it can grow revenues at upper single digits year over year while maintaining 25% free cash flow margins - the kind of numbers that make a value investor's heart skip a beat.

Sure, there are risks lurking around every corner – biosimilars nipping at Eylea's heels, Medicare negotiations that could squeeze margins, and clinical trials that might go sideways.

But with multiple growth catalysts and a pipeline that reads like a wish list for modern medicine, Regeneron's got more upside than my daughter's college tuition bills.

As my optometrist likes to say - in the land of the blind, the one-eyed man is king. But in the land of biotech, Regeneron's got a 20/20 vision for what's coming next.

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

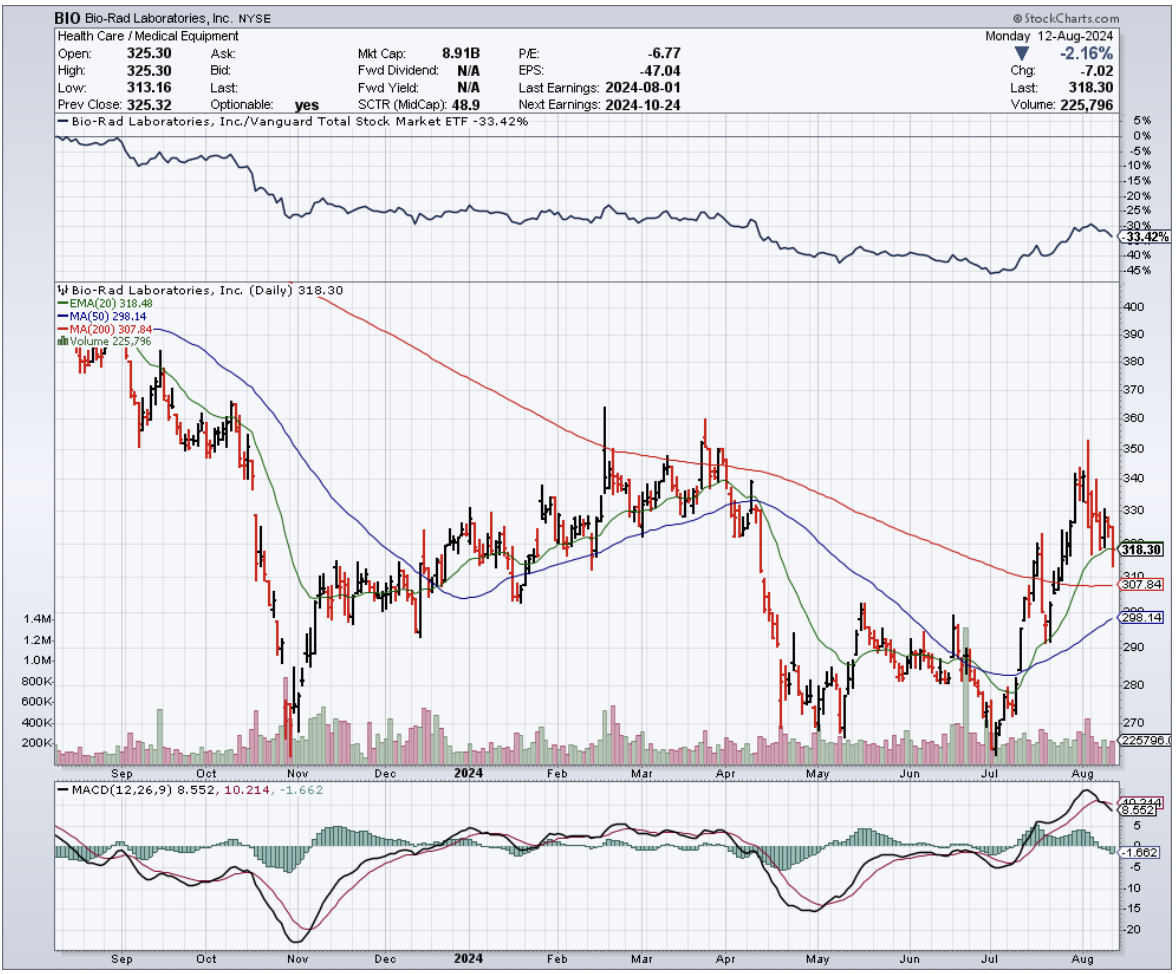

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?

Mad Hedge Biotech and Healthcare Letter

May 16, 2024

Fiat Lux

Featured Trade:

(THE COMEBACK KID OF VACCINES)

(NVAX), (SNY), (BNTX), (PFE)

Mad Hedge Biotech and Healthcare Letter

May 14, 2024

Fiat Lux

Featured Trade:

(EARS TO THE GROUND)

(REGN), (LLY), (FENC)