The biotechnology world started the week right with a milestone announcement from its gene therapy sector.

Intellia Therapeutics (NTLA), along with its partner Regeneron (REGN), developed a potential cure for a genetic liver disease that previously had no cure.

Using the Nobel Prize-winning Crispr technology, Intellia was able to come up with the first-ever treatment for a disease that had been known to be extremely progressive and even fatal.

This achievement has been described to “open up a whole new area of therapies for patients that wasn't there.”

This is because instead of simply treating the symptoms of particular diseases, Intellia was able to demonstrate that it is possible to use gene editing to come up with a cure.

As expected, shares of Intellia shot up the moment the news broke, rising by 40% by the start of the week.

While this is definitely an incredible update for its investors, what’s even more impressive is the fact that this achievement marks the beginning of a revolution in the way we treat diseases.

Intellia’s treatment, called NTLA-2001, is delivered intravenously into the patient’s body. It’s designed to specifically target a progressive form of liver disease called ATTR amyloidosis. This disorder, while rare, is often fatal.

Right now, there are two companies working on this fast-growing segment. Pfizer (PFE) has Vyndagel and Vyndamex, while Alynlam Pharmaceutical (ALNY) has Onpattro. All these treatments are administered through infusions.

At this point, Alnylam holds the gold standard for ATTR treatment with Onpattro, as it delivers 80% capacity for blocking harmful proteins and reducing blood levels. Patients also need to go in every three weeks for dosing.

In comparison, Intellia’s NTLA-2001 is a one-time treatment. That in itself is a massive advantage for the company.

To add to that lead, Intellia’s candidate also showed an ability to drop protein levels by as high as 96% within just a matter of weeks, with no adverse side effects observed in patients.

This is possibly because the gene therapy was delivered directly to the patient’s liver, which is the source of the issue.

While the results are already promising, Intellia believes that it can achieve better outcomes in the future. According to its researchers, the company is looking into using a bone marrow delivery system to boost the efficacy rate of NTLA-2001.

So far, Intellia has received additional funding via a grant from the Bill & Melinda Gates Foundation to pursue the bone marrow delivery system idea.

If that works out, then the same system can be used to develop treatments for reverse sickle cell anemia and even cover other cardiovascular indications.

Although there’s still no word about the pricing for NTLA-2001, we can use Onpattro as reference for now. Alnylam’s treatment is priced at roughly $450,000 annually.

ATTR holds a fairly huge market. Going back to 2020, Onpattro generated over $300 million in revenue and is estimated to rake in more than $400 for 2021.

Considering that Intellia offers a one-and-done option, we can reasonably assume that the demand would be much higher for NTLA-2001.

Overall, ATTR’s total addressable market is estimated to be at $15 billion. However, ATTR is only the tip of the iceberg.

Studying the liver alone would reveal several genetic diseases that Intellia could address with its technology. Other than those, Crispr could still be applied to dozens of disorders linked to solid tumors.

In fact, the market for solid tumors is actually where the fortunes lie in the gene-editing field, with the sector projected to grow to $424.6 billion by 2027.

Another lucrative market is the genetic disorder segment, with estimated sales anticipated to reach $47.7 annually by 2023.

So far, there appear to be only three companies focused on utilizing Crispr technology to develop cures for these diseases: Intellia, Editas Medicine (EDIT), and of course, CRISPR Therapeutics (CRSP).

Considering the incredibly broad market and the limited number of companies addressing these needs, I say there’s more than enough room for all of them to flourish.

If Intellia continues to discover ways to effectively treat these, then this biotechnology company will not only be considered a godsend to humanity as a whole but also transform into a waterfall of cash for its shareholders.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-29 15:00:082021-07-03 00:47:39Breaking New Ground With This Biotech Stock

Building a retirement portfolio is different from when you’re aggressively playing the market. With this, you’d want something with less risk and more stability. A healthy helping of income definitely wouldn’t hurt either.

Taking these into consideration, a particular stock that offers a well-balanced mix of income and capital appreciation comes to mind: Merck (MRK).

The biggest news for Merck recently is its $1.2 billion deal with the US government involving its experimental COVID-19 antiviral.

The treatment, called Molnupiravir, is expected to cost about $700 per course, putting the total of the order from the US to 1.7 million courses.

This is just the beginning though. According to Merck and its partner, Ridgeback Biotherapeutics, they can produce at least 10 million courses of Molnupiravir by the end of 2021.

If we use the same pricing as the US, then we can expect approximately $7.1 billion in sales for Molnupiravir alone this year.

Still, the $1.2 billion deal with the US is already a massive win for Merck as experts initially estimated that Molnupiravir sales would only reach $25 million this year.

What makes Molnupiravir unique and more advantageous than its competitors is that the drug is taken orally.

The convenience alone easily edges out the other monoclonal antibody therapies from the likes of Regeneron (REGN), GlaxoSmithKline (GSK), and Eli Lilly (LLY)—all of which need to be administered intravenously.

If Molnupiravir does gain emergency use authorization from the FDA, its sole competitor in the market today is Veklury from Gilead Sciences (GILD).

To offer an idea on the size of the market for this treatment, Gilead recorded $2.8 billion in sales of Veklury in 2020. This figure is even projected to go up to $2.9 billion for this year.

Apart from its COVID-19 program, Merck has always been a favorite among value investors.

It’s a great dividend stock and has gained a reputable name in the industry as being one of the biggest and oldest companies in this field.

It’s also the force behind blockbuster treatments like the top-selling cancer drug Keytruda, HPV vaccine Gardasil, and of course, the diabetes medication Januvia.

In fact, Keytruda is estimated to become the No. 1 selling drug in the world by 2023—an achievement that Merck has lots of time to capitalize on considering that the treatment’s patent exclusivity lasts until 2028.

Keytruda is a key revenue generator for Merck, with the cancer drug showing off a 19% jump to reach $3.9 billion in sales in the first quarter of 2021.

This puts it on track to rake in roughly $16 billion in sales for this year, showcasing an 11% increase from 2020.

By 2026, Keytruda is estimated to generate $24.32 billion in sales annually.

Apart from Keytruda, Merck has been boosting its pipeline as well. For example, Bridion, one of its newer drugs, raked in $1.2 billion in sales in the first quarter, which is up 6% year-over-year.

Looking at its history, Merck has repeatedly shown that it can compete aggressively in the biopharmaceutical industry.

In 2020, the company still managed to generate $48 billion in sales despite the pandemic, with an earnings per share of $5.94—a value that’s 65% stronger than it was just five years ago.

Its strong profit growth and promising pipeline programs have allowed the company to boost its dividend payout at an impressive 7.1% pace over the past years.

This is a performance that most blue-chip companies, regardless of their size and market cap, struggle to keep up with.

Merck isn’t as exciting as the other stocks in the biotechnology and healthcare market, but that’s a comforting thought for investors who are on the lookout for a stable business.

Although Merck stock is not dirt cheap, I think it’s attractive for those who have extra cash or are hesitant to roll the dice on more volatile companies today.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-15 16:00:352021-06-17 18:28:53A Stock to Add to Your Retirement Portfolio

The biotechnology and healthcare sectors have become attractive investment targets for investors who recognize the value and essence of these industries along with the possible risks associated with them.

While not all companies in these areas are great investments, some offer remarkable growth opportunities.

One company worth considering is Regeneron (REGN), with its strong and stable investment thesis and steady organic growth.

Regeneron joins the ranks of Pfizer (PFE) and Johnson & Johnson (JNJ) as one of the handful of biopharmaceutical companies to release solid first quarter results this 2021 compared to other big names in the industry, including Amgen (AMGN), Bristol Myers Squibb (BMY), Gilead Sciences (GILD), Merck (MRK), and Eli Lilly (LLY).

The New York-based company reported a 38% boost in its revenue compared to the same period in 2020, reaching $2.5 billion for the first quarter of 2021 alone.

Virtually all of Regeneron’s products generated solid growth during this period, with the company’s COVID-19 antibody cocktail REGEN-COV delivering the highest sales at $262 million.

To underscore just how significant REGEN-COV is to Regeneron this quarter, its absence from the roster would take away 18% from the company’s overall revenue growth.

Riding the momentum of its COVID-19 program, Regeneron has developed Inmazeb, which is a treatment for Ebola virus infection.

Aside from its COVID-19 antibody cocktail, Regeneron also saw an impressive boost in the performance of its atopic dermatitis drug Dupixent.

Dupixent, which Regeneron sells in partnership with Sanofi (SNY), generated $1.26 billion in sales in the first quarter, showing off a notable 48% increase from its 2020 report.

Although Dupixent is a shared product with Sanofi, this dermatitis drug holds incredible promise for Regeneron.

To date, only 6% of eligible patients are being treated with Dupixent. This indicates a massive space that is yet to be explored by both companies.

Taking into consideration the pace at which Dupixent has been growing so far, this drug is projected to peak at roughly $12.5 billion in sales in the coming years.

Another high-selling drug for Regeneron is wet age-related macular degeneration (AMD) treatment Eylea.

Sales for this drug, which was developed in collaboration with Bayer (BAYRY), went up from $1.2 billion in the first quarter of 2020 to $1.3 billion this year.

The increase in sales for Eylea is a welcome surprise for both Regeneron and Bayer, especially since more and more competitors are attempting to topple the drug as the top product in the niche.

Cornering the AMD segment is an attractive venture for any biopharmaceutical company.

After all, Eylea generated $4.9 billion in sales in 2020 from the US market alone.

Thus far, two main competitors have come forward as the strongest.

One is Novartis (NVS), which released Beovu in 2019.

The second, and possibly the stronger competitor between the two, is Roche (RHHBY) with Faricimab.

To ensure its dominance in the AMD market, Regeneron has been expanding the use of Eylea.

The latest development is the drug’s enrollment in the Phase 3 program, which would allow extended periods in between treatments but still deliver the same level of efficacy and safety.

Aside from these, Regeneron is looking into additional revenue streams ahead.

One growth segment is its oncology program, particularly its cancer drug Libtayo, which may soon be marketed to cover a fourth type of cancer.

Regeneron aims to submit Libtayo for review as a treatment for advanced cervical cancer.

On top of this, the drug is also a strong contender in the development of several antibody treatments.

Thus far, the company has 12 oncology antibodies under clinical development.

Overall, Regeneron’s strong results for the first quarter of 2021 highlighted its continuous evolution into a company carrying multiple and diverse portfolios of products and pipeline programs that address an extensive range of serious diseases, from COVID-19 and rare diseases to cancer.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-05-20 15:00:332021-05-29 19:53:46Regenerated Regeneron

The last six months have been the most successful in my 52 years of trading. The only thing that comes close were the last six months of 1989 when the Tokyo market went straight up and hit a 30-year peak.

Everything I tried worked. The trades I only thought about worked. And the 50 trade alerts I abandoned on the floor because the market moved too fast worked as well. That’s how I missed Facebook (FB) and Amazon (AMZN).

It is believed that if you set a team of monkeys loose, randomly hitting keys on typewriters, they would eventually produce Romeo and Juliet. In this market, they have been producing the entire works of Shakespeare on a daily basis.

It has been that good.

President Biden has been looking pretty good too, having presided over the best starting three-month stock market results since 1933. That is no accident. The massive stimulus and the remaking of the country he has proposed have Franklin Roosevelt’s New Deal-inspired handwriting all over them.

Yet, traders have been puzzled, perplexed, and befuddled by companies that announce the best earnings in history only to see their shares sell-off dramatically. However, the market has shown its hand.

We’ve now seen three quarters of tremendously improving earnings and stock dives. It’s a 12-week cycle that keeps repeating. Shares rally hard for six weeks into earnings, peak, and then go nowhere for six weeks. Wash, rinse, repeat, then go to new all-time highs.

But stocks don’t fall enough to justify getting out and back in again, especially on an after-tax basis. Therefore, it’s just best to lie back and think of England while your stocks do nothing.

If my analysis is correct, then it's best to imagine the rolling green hills of Kent and Wiltshire, the friendly neighborhood pub, and Westminster Cathedral until June. If you want to get aggressive, you might even sell short an out-of-the-money call option or two to protect your portfolio. The Fed leaves rates unchanged, indicating that the economy is improving, but that interest rates are going nowhere. No surprise here. Jay Powell is still going for maximum dove. Strong Biden policy support and the rollout of the vaccine are major positives. $120 billion in bond buying continues. The Fed will keep interest rates at zero until the US economy reaches maximum employment by adding 8.4 million jobs. That could be a long wait as I suspect those jobs have already been destroyed by technology. Stocks popped on the news. The Bull lives!

Q1 GDP eExploded by 6.4%, and upward revisions are to come. That explains the 25% gain in the stock market during the first three months of the Biden administration, the best in 75 years. Coming quarters will show even stronger growth as the economy shakes off the pandemic and massive government spending kicks in. We will recover 2019 GDP peaks in the next quarter. Virtually, all economic data points will set records for the rest of 2021. Buy everything on dips.

Weekly Jobless Claims dive again to 553,000, a new post-pandemic low. One of a never-ending series of perfect data. It augurs well for next week’s April Nonfarm Payroll Report.

New Home Sales up a ballistic 20.7% YOY in March on the basis of a signed contract. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

Pending Home Sales fell 1.9%, far below expectations, but are still up 23% YOY. Higher prices and record low supply are the problems. The Midwest leads.

Amazon sales soar by 44% in Q1, producing some of the best earnings in American corporate history. Jeff is expecting sales to reach a staggering $110-$116 billion in Q2. That’s why he hired 500,000 last year, the most of any company since WWII. Prime subscribers have grown to 200 million, including me. Ad revenues jumped an eye-popping 77%. The shares of the huge pandemic winner leaped $140 on the news. It’s all another step toward my $5,000 target.

Tesla revenues explode for 74%, and earnings soar to an eye-popping $438 million. Sales are to double or more in 2021 and are up 104% YOY. Q1 is usually the slowest quarter of the year for the auto industry. Global demand is increasing far beyond production levels. It is ducking around chip shortages by designing in a new generation that is currently available. Production of high-end X and S Models has ceased to allow more focus on the profitable Y and 3 Models. Those will resume in Q3. The shares were unchanged on the news. Keep buying (TSLA) on dips. It’s headed for $10,000.

Copper hits new 10-year high, lighting a fire under Freeport McMoRan (FCX) which we are long. We still are in the early innings of a major commodity supercycle. The green revolution goes nowhere without increasing copper supplies tenfold. A copper shock is imminent.

US Capital Spending leaps ahead, up 0.9% in March and up 10.4% YOY. The stimulus spending is working. All is well in manufacturing land, which is 12% of the US economy.

Case-Shiller explodes to the upside, the National Home Prices Index soaring 12% in February. That’s the best report in 15 years. Phoenix (+17.4), San Diego (+17.0%), and Seattle (15.4%) continue to be the big winners. This was in the face of a 50-basis point jump in home mortgage interest rates during the month. The rush to buy homes is pulling forward future demand. The perfect storm continues. The Fed could start tapering its $120 billion a month in bond purchases as early as October, believes the Blackrock’s (BLK) Rick Rieder. When it does, expect the sushi to hit the bond market. Keep piling on those bond shorts, as I have been doing monthly, and am currently running a triple short position. Keep selling short the (TLT) on every opportunity. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 13.54% gain during April on the heels of a spectacular 20.60% profit in March.

I used the post-earnings dip in Microsoft (MSFT) to add a new position there. I also picked up some Delta Airlines (DAL) taking advantage of a pullback there.

That leaves me 100% invested, as I have been for the last six months.

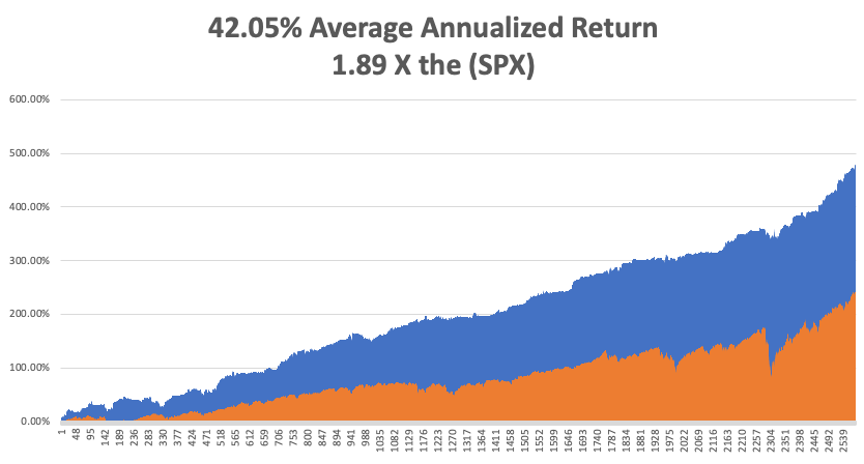

My 2021 year-to-date performance soared to 57.63%. The Dow Average is up 11.8% so far in 2021.

That brings my 11-year total return to 480.18%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.05%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 133.91%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, May 3, at 10:00 AM, the US ISM Manufacturing Index is published. Merck (MRK) and Estee Lauder (EL) report.

On Tuesday, May 4, at 8:00 AM, total US Vehicle Sales for April are out. Union Pacific (UNP) and Pfizer (PFE) report.

On Wednesday, May 5 at 2:00 PM, the ADP Private Employment Report is released. General Motors (GM) and PayPal (PYPL) report.

On Thursday, May 6 at 8:30 AM, the Weekly Jobless Claims are printed. Regeneron (REGN) and Roku (ROKU) report.

On Friday, May 7 at 8:30 AM, we learn the all-important April Nonfarm Payroll Report. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I received calls from six readers last week saying I remind them of Earnest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens, I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete works.

I visited his homes in Key West and Ketchum Idaho. His Cuban residence is high on my list, now that Castro is gone.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Earnest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was still being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are glued to the tables.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Life is a Bed of Roses Right Now

https://www.madhedgefundtrader.com/wp-content/uploads/2019/10/john-flowers.png375499Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-05-03 10:02:112021-05-03 12:12:45The Market Outlook for the Week Ahead, or The Stair Step Market is Here

Since the great 2007 financial crisis, many companies have been coping to recapture their former glory. The healthcare industry is not spared of this struggle.

This makes the continuous growth of Merck (MRK) all the more impressive, with the company reaching $195 billion in market capitalization and sustaining its rise for over 130 years.

Curiously, Merck’s share price is still in the mid-$70s.

Meanwhile, other large-cap biopharmaceutical companies that offer similar products and services are trading higher.

For instance, the share price for Abiomed (ABMD) is over $330 while Illumina (ILMN) is nearly $400, and Align Technology (ALGN) is at a whopping $600.

Like Merck, investors gravitate towards Abiomed, Illumina, and Align because of their capacity to generate long-term sustainable revenues and boost earnings.

Notably, though, none of them hold the same depth or even breadth of products and services that Merck offers.

Recently, Merck disclosed some of its initiatives to boost the company’s earnings in the near- and long term.

One of the most visible efforts is its collaboration with Johnson & Johnson (JNJ) to help with the manufacturing of JNJ-78436735, in which Merck received federal funding.

While JNJ is one of the biggest healthcare companies across the globe, with a market capitalization of roughly $425 billion, joining forces with Merck will substantially boost its vaccine manufacturing capacity.

For context, JNJ’s goal prior to Merck’s help is to deliver 100 million doses by the end of the second quarter of 2021.

With Merck’s assistance, JNJ can now realistically manufacture up to 3 billion doses in 2022 alone.

This means that JNJ can implement a massive vaccination drive in the next two years since its manufacturing capacity ensures that it can deliver shots to over one-third of the population.

This is obviously good news for everyone as it means that the virus will be contained, but the enhanced manufacturing capacity also means profit accretion for both JNJ and Merck.

This partnership with JNJ is possibly a key factor in Merck’s move to invest heavily in the vaccine business.

Merck recently announced its plans to allocate $20 billion to expand its global vaccine manufacturing network from 2021 to 2024. This would mean an annual investment of $5 billion.

Part of this global vaccine plan is Merck’s acquisition of Pandion Therapeutics (PAND) in 2020.

Another recent initiative of the company is its joint effort with Gilead Sciences (GILD) to develop long-lasting HIV treatments.

Gilead will be in charge of the US market, while Merck will handle the EU and the rest of the international markets.

For starters, the companies will focus on a combination of Merck’s Islatravir and Gilead’s Lenacapavir to create a long-lasting and well-tolerate HIV treatment.

Outside these partnerships, Merck has been working on strengthening its oncology segment.

In fact, its top-selling drug, Keytruda, can be used to medicate an extensive range of indications, which include colorectal, esophageal, and even lung cancers.

At this point, Keytruda is generating north of $16 billion in sales every year and exhibiting roughly 30% growth annually.

Since the drug continues to gain approvals for additional indications, it looks like its growth runway is definitely far from over.

Keytruda is poised to reach $24 billion in annual sales in a few years’ time, which puts it on track to become the best-selling drug in the world by 2023.

Although Keytruda will be under patent protection until 2028, Merck remains active in expanding its oncology pipeline.

By then, Merck is projected to have multiple immunotherapy staples in its portfolio not only derived from its own R&D but also via partnerships like its 2020 collaboration with Alkermes (ALKS) to work on an ovarian cancer study and Immunovaccine (IMV) to cooperate on a blood cancer study.

The total oncology market is estimated to be $200 billion annually, with over 30 million cases projected to be added by 2040.

Overall, Merck is a well-oiled company that continues to deliver good results thanks to strategic acquisitions and partnerships neatly tied up together in a particular domain.

While its rival biotechnology and pharmaceutical companies become hot properties in the market and pose higher price tags, Merck silently moves forward in the shadows of sustainability and familiarity.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-13 14:00:492021-04-19 23:11:39Mega Cap Pharma Up for Grabs

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-08 16:02:232021-04-08 18:48:42April 8, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.