Mad Hedge Biotech and Healthcare Letter

April 17, 2025

Fiat Lux

Featured Trade:

(THIS BIG PHARMA'S GRAND DIVORCE SHOWS PROMISE)

(NVS), (SDZNY), (MRK), (RHHBY)

Mad Hedge Biotech and Healthcare Letter

April 17, 2025

Fiat Lux

Featured Trade:

(THIS BIG PHARMA'S GRAND DIVORCE SHOWS PROMISE)

(NVS), (SDZNY), (MRK), (RHHBY)

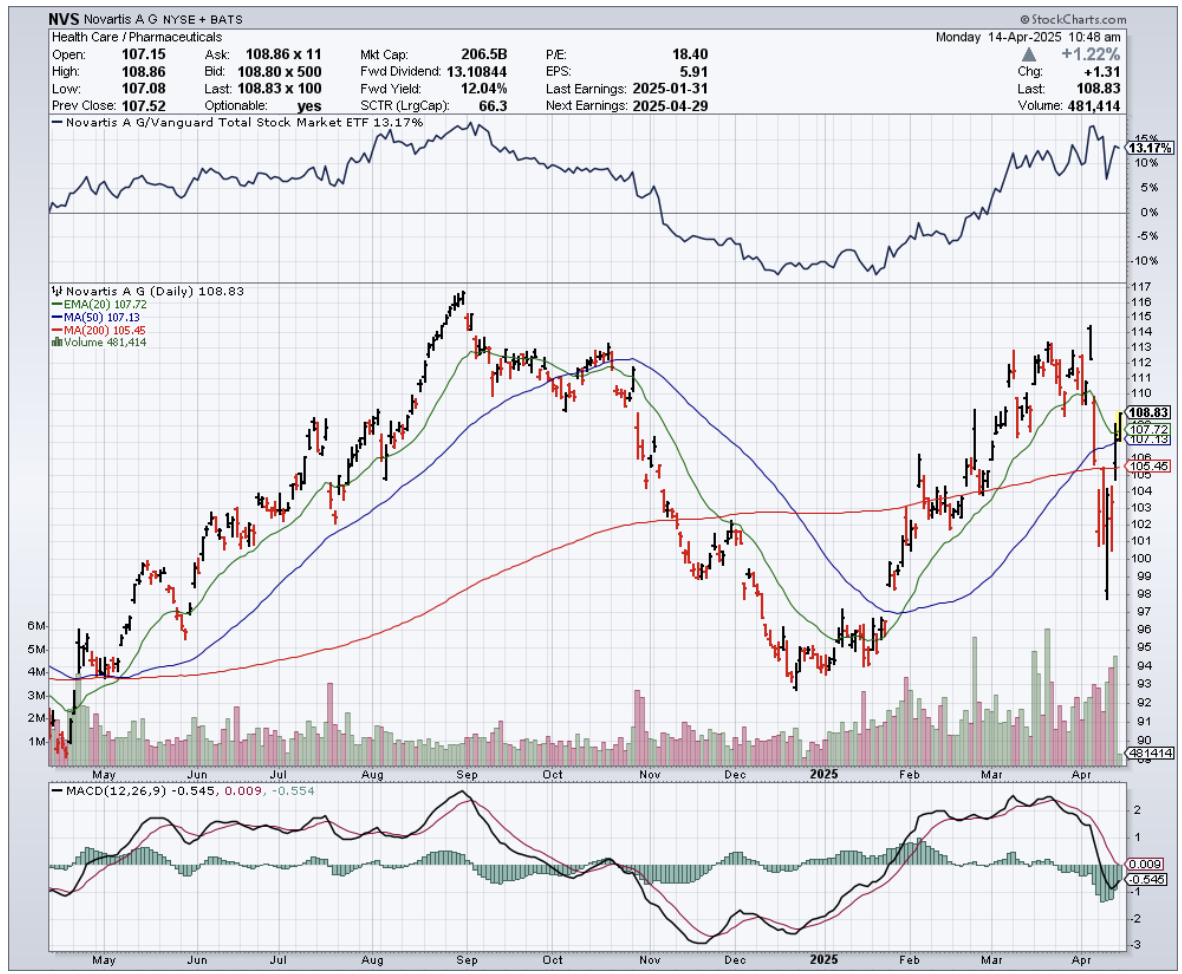

While most corporate breakups end with shareholders reaching for antacids, Novartis (NVS) investors are popping champagne instead.

The Swiss pharmaceutical giant's 2023 divorce from its generics business Sandoz (SDZNY) has transformed the company from a pharmaceutical conglomerate into a focused innovation machine – and the numbers would make even the most jaded among us whistle in appreciation.

I've watched pharmaceutical reorganizations for decades, and most resemble rearranging deck chairs on the Titanic. But Novartis has executed something genuinely transformative.

By jettisoning vaccines, ophthalmology, and generics, they've engineered a corporate metamorphosis that delivered 10% revenue growth to $51.7 billion in 2024.

Novartis now operates with laser focus on four therapeutic areas. Entresto, their heart failure medication, generated $7.8 billion in 2024 – up 31% year-over-year. That's roughly the GDP of Montenegro flowing from a single pill.

Cosentyx pulled in $6.1 billion (up 25%), while Kisqali and Kesimpta both jumped nearly 50%. These aren't merely drugs; they're annuities with patent protection.

The scale defies easy comprehension: nearly 300 million patients worldwide received Novartis medications in 2024. That's treating almost every American, then adding Japan for good measure. When pharma executives dream of market penetration, this is what they see before their alarm clocks rudely interrupt.

What separates Novartis from the pack is their capital allocation strategy. They're investing $9 billion annually in R&D – not throwing darts at a scientific board but methodically advancing a pipeline designed to replace blockbusters as patents expire.

Their 2024 acquisition of Chinook Therapeutics exemplifies this approach: precise, strategic, and focused on enhancing their nephrology portfolio rather than empire-building.

The geographic distribution of Novartis's revenue reveals similar strategic clarity. While 43% comes from the United States, their China strategy deserves special attention. Sales there surged over 20% in local currency during 2024.

Having tracked emerging markets throughout my career, I recognize the pattern – Novartis is positioning itself at the confluence of demographic shifts, increasing chronic disease prevalence, and expanding healthcare access.

For those who prefer hard numbers to market philosophy, Novartis delivered EBIT growth of 29% to $16.3 billion, with operating margins expanding to 31.55%. Net profit jumped to $11.9 billion, with margins at 23% – among the industry's highest.

Despite returning $15.9 billion to shareholders through dividends and buybacks, their balance sheet remains fortress-like.

Net debt stands at just $18 billion, with a Net Debt/EBITDA ratio below 1x – meaning they could extinguish their entire debt in less than a year with current cash flows.

Unlike pharmaceutical giants that bet everything on a single therapeutic area, Novartis has positioned itself as a formidable player across multiple high-value niches.

In oncology, rather than challenging Merck (MRK) or Roche (RHHBY) directly, they've developed unique assets like Pluvicto and Kisqali that face minimal head-on competition.

For cardiology, while Entresto faces patent expiration in 2025, they're already advancing next-generation therapies like Leqvio.

Meanwhile, the global prescription drug market exceeded $1.7 trillion in 2024 and should grow at 7.7% annually through 2030. Novartis has strategically positioned itself precisely where that growth curve steepens most dramatically.

No investment thesis is complete without acknowledging risks, and Novartis faces several significant challenges.

Entresto's patent cliff in 2025 creates a $7.8 billion revenue gap that needs filling. Cosentyx follows in 2027-2028.

Without Sandoz, they can't offset these losses with their own generics. Pricing pressure from Medicare and competition from other pharmaceutical giants present additional headwinds.

And pharmaceutical innovation remains inherently unpredictable – even with billions in R&D, clinical trials fail with alarming regularity.

Despite these concerns, Novartis shares still appear undervalued after rising nearly 19% over the past year.

The company trades at a P/E of 18.69x – substantially below the industry average of 55.91x. Its EV/EBITDA ratio of 10.97x represents a significant discount to peers.

Throughout my market-watching career, I've developed healthy skepticism toward corporate transformations. They typically generate more PowerPoint slides than actual results.

But Novartis has delivered tangible financial improvements that flow directly to shareholders. For those seeking healthcare exposure without betting on clinical-stage biotechs with binary outcomes, Novartis offers a compelling package of growth, income, and relative stability wrapped in Swiss precision. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

March 20, 2025

Fiat Lux

Featured Trade:

(EVEN A PIG COULD MAKE MONEY HERE)

(OGN), (MRK), (RHHBY), (BAYRY), (PFE), (AZN)

I was camped out in Kyiv the other month when news of Organon's (OGN) earnings hit my phone.

While Russian drones buzzed overhead, I was studying pharmaceutical balance sheets—talk about surreal. Did I mention I've led a strange life?

In mid-February, Organon pleasantly surprised me with Q4 2024 results. Hadlima, their biosimilar to Humira, rocketed to $44 million in quarterly sales, up 83.3% year-on-year.

Meanwhile, Organon's dividend yield sits at a whopping 7.32%, blowing away the healthcare sector average.

Let me be blunt: this is an income investor's dream hiding in plain sight.

Organon emerged in 2021 when Merck (MRK) spun off its women's health, biosimilars, and off-patent drugs businesses. This allowed Merck to focus on its immunology and oncology pipeline while Organon became a pure-play commercial entity.

These spinoffs often create enormous value that the market misses in the early years.

Organon's share price has been trading sideways since early 2025 despite several wins: commercializing Hadlima, acquiring Dermavant, and maintaining a 23% operating margin even as some medications face generic competition.

The market clearly isn't paying attention. When stocks with this kind of dividend yield maintain solid margins, my antennae start twitching.

Their recent Phase 3 ADORING 3 study showed that even 79.8 days after stopping Vtama treatment, atopic dermatitis remained mild. That's patient retention gold, folks.

When patients can stop medication and still see benefits almost three months later, that's the kind of sticky customer base pharmaceutical execs dream about.

Revenue hit $1.59 billion in Q4 2024, down just 0.63% year-over-year but up 0.63% quarter-over-quarter.

Renflexis sales reached $64 million, down 16.9% due to competition from other Remicade biosimilars and superior new medications like AbbVie's (ABBV) Skyrizi.

But here's where things get interesting—this sales decline was expected and already priced in. Organon isn't being valued in Renflexis's future.

The real stars? Nexplanon and Vtama. Nexplanon sales reached $258 million in Q4, up 11.7% year-on-year.

Even better, its patent protection runs until August 2030. CEO Kevin Ali expects it to "comfortably get beyond $1 billion in 2025."

When a CEO uses words like "comfortably" about billion-dollar projections, I tend to listen.

Vtama, acquired in the $1.2 billion Dermavant purchase, brought in $12 million in partial Q4 sales.

The FDA expanded its label in December 2024 to include atopic dermatitis in patients over age 2—a condition affecting 31.6 million Americans. This approval significantly expands its market potential.

Remember, blockbuster drugs don't announce themselves with trumpets—they sneak up on you through expanded indications and growing prescriber bases.

Now, many folks will point to Organon's debt—$8.36 billion at 2024's end. But that's lazy analysis.

Look deeper and you'll see its net debt/EBITDA ratio improved from 5.01x to 4.74x over 12 months. They're steadily strengthening their financial position.

I've watched this happen before with pharma spin-offs—initial debt concerns gradually fade as strong cash flows tackle the balance sheet.

Management knows what they're doing. For 2025, they forecast a slight revenue dip but improved EBITDA margins of 31-32%, outperforming competitors like Perrigo, Alvotech, and Amneal.

In the broader pharmaceutical landscape, Organon competes with heavyweights like Roche (RHHBY), Ferring Pharmaceuticals, Bayer (BAYRY), Pfizer (PFE), and AstraZeneca (AZN)—but with a more specialized focus that gives them maneuverability these giants lack.

Wall Street's average price target is $20.50, suggesting a 33.9% upside. When was the last time you saw a 7.32% dividend yield with 33.9% upside potential?

I project non-GAAP EPS to reach $4.52 by 2029, slightly above analyst estimates, driven by Hadlima, Nexplanon, and Vtama growth, plus upcoming biosimilars HLX14 and HLX11. My friends at major healthcare funds are starting to take notice, but the broader market hasn't caught on yet.

At $15.31 per share, Organon trades at a non-GAAP P/E of 3.39x—80.8% below the sector median and 25.7% below its 5-year average. That's not just cheap—that's backing up the truck cheap.

You know what they say about bears and bulls making money, while pigs get slaughtered? Well, at these valuations, even a pig could make money on Organon.

Mad Hedge Biotech and Healthcare Letter

February 25, 2025

Fiat Lux

Featured Trade:

(WALL STREET'S MYOPIA IS YOUR OPPORTUNITY)

(REGN), (RHHBY), (AMGN), (AZN), (ABBV), (LLY)

While preparing my presentation for this week's Online Traders Conference, I came across a pattern that made me stop cold. You see, I've been gathering examples of how institutional investors quietly accumulate positions while retail traders are looking the other way.

And there it was, right in front of me - Regeneron Pharmaceuticals (REGN), displaying exactly the kind of setup I'll be warning traders about starting February 24.

You see, while everyone's been obsessing over the latest AI darlings, Regeneron has been quietly crushing it. Their Q4 revenue hit $3.79 billion, up 10.5% year-on-year.

But here's where it gets interesting - they beat consensus estimates by $43 million, and that's with their flagship eye drug Eylea taking a hit.

Speaking of Eylea, let's address the elephant in the room. Its sales dropped 11% to $1.19 billion, thanks to Roche's (RHHBY) Vabysmo muscling into their territory and Amgen's (AMGN) biosimilar crashing the party.

Four more biosimilars are waiting in the wings, held back only by patent disputes. Normally, this would send investors running for the hills.

But here's what the panic-sellers are missing.

Despite Eylea's challenges, Regeneron's non-GAAP EPS still climbed to $12.07, beating analyst expectations by 88 cents.

In fact, they've been playing jump rope with analyst estimates, leaping over them in 10 of the last 12 quarters. Yet their stock price has been doing its best impression of a sleeping cat - just lying there, barely moving.

As someone who's spent decades watching market cycles, I recognize this pattern.

We're in what technical analysts call an “accumulation phase.” While retail investors yawn and look elsewhere, institutional money is quietly building positions.

It's like watching a spring being compressed - boring until it isn't.

But here's what really got my attention: Regeneron just joined the dividend club. Starting March 20, they're paying $0.88 per quarter. Sure, the yield won't make income investors swoon, but that's not the point.

It reminds me of how AstraZeneca (AZN) played it - first, dominate growing markets, then gradually turn on the dividend spigot to attract the steady-money crowd.

They're also backing up the dividend with a $3 billion share buyback program.

With $9 billion in cash and short-term investments, they've got more dry powder than a Revolutionary War armory.

In Q4 alone, Regeneron spent $1.23 billion buying back shares - up 64.1% from last year.

And here's where it gets even more interesting. Their oncology franchise, led by Libtayo, is looking like a dark horse winner. Libtayo sales jumped 50.4% year-over-year to $367 million.

While that might not sound earth-shattering compared to cancer drug heavyweights like Merck's (MRK) Keytruda, Libtayo just pulled off something remarkable.

In their Phase 3 C-POST trial for high-risk skin cancer patients, Libtayo reduced death and disease recurrence risk by 68% compared to placebo.

Even better? Merck's competing trial for Keytruda in the same indication fell flat on its face. In this business, that's like watching your main competitor trip at the Olympic finals.

Looking ahead to 2029, I'm seeing revenue hitting $20.4 billion - think high single-digit growth each year. That would bring their price-to-sales ratio down from 5.12x to 3.53x.

Their non-GAAP EPS should hit $76.5, implying double-digit growth most years. With the stock currently trading at just 14.76x earnings - below most peers like AbbVie (19.06x) and Eli Lilly (64.96x).

On top of these, 2025 is packed with potential catalysts - clinical trial results and FDA decisions that could light a fire under the stock.

Analysts' average target is $929.37, suggesting about 38% upside. But in my experience, when you combine strong fundamentals, multiple growth drivers, and a market that's sleeping on the story, those targets often end up looking conservative.

Remember, the market loves nothing more than a comeback story.

With Regeneron, we might just be watching one unfold in slow motion. The question is: will you be holding shares when the spring finally releases?

For those who want to learn more about spotting these kinds of opportunities, I'll be diving deeper into institutional accumulation patterns at the Online Traders Conference running February 24 through March 1.

But don't wait for my presentation to take a serious look at Regeneron - the smart money isn't.

Mad Hedge Biotech and Healthcare Letter

February 4, 2025

Fiat Lux

Featured Trade:

(TOO RICH TO FAIL, TOO EXPENSIVE TO SUCCEED)

(MRNA), (TSLA), (NVS), (SNY), (JNJ), (BNTX), (RHHBY), (REPL), (CRSP), (ORCL)

Last weekend, while organizing my home office, I stumbled across an old COVID vaccination card. Remember those? It got me thinking about Moderna (MRNA), the biotech darling that went from relatively unknown to household name faster than you can say "messenger RNA."

Now, in early 2025, this once up-and-coming company is already facing what my grandmother would call "champagne problems" - too much cash to be broke, but burning through it faster than a Tesla (TSLA) on Ludicrous mode.

First, let's talk about this biotech's cash burn. In just nine months of 2024, Moderna torched through over $4 billion - that's the same amount they burned in all of 2023, suggesting their cash cremation rate is actually accelerating.

This acceleration in spending wouldn't be as worrying if they had endless reserves, but their current position shows $7 billion in cash and $2 billion in non-current investments.

The math isn't complex: at this burn rate, their runway is shorter than many investors realize.

The recent Health and Human Services (HHS) grant of $176 million in July 2024 for bird flu research barely registers on their financial statements.

While we've seen about 70 bird flu cases in the U.S. with one fatality in an elderly patient with underlying conditions, this isn't going to be another COVID-style revenue stream.

I've analyzed enough pharmaceutical companies to know that betting on another pandemic windfall is like expecting lightning to strike twice in the same spot.

What really interests me is Moderna's position in the competitive landscape. I spent last week analyzing patent data and geographic reach metrics across the industry.

First, you've got the old-guard pharma giants like Novartis (NVS), Sanofi (SNY), and Johnson & Johnson (JNJ), who have been at this game since before mRNA was a gleam in a scientist's eye.

Then, there are companies like BioNTech (BNTX) and Roche (RHHBY) with significantly higher geographic reach, while Replimune Group (REPL) and CRISPR Therapeutics (CRSP) demonstrate superior application diversity.

In comparison, Moderna's position in this landscape shows relatively low scores on both metrics - not exactly what you want to see from a company burning cash at this rate.

Stéphane Bancel, Moderna's CEO, recently outlined their pipeline: 2 approved medicines, 7 Phase 3 trials, and 45 candidates in development. They're also targeting $1.1 billion in annual R&D cost reductions by 2027.

But here's what keeps bothering me: their SG&A expenses have ballooned to nearly 10 times their pre-COVID levels, yet management is focusing on R&D cuts instead of addressing this administrative bloat.

The insider trading patterns since early 2024 haven't exactly inspired confidence either.

When I see heavy selling from insiders while a company is promising future breakthroughs, I can't help but remember all the biotech stories I've covered where the promise didn't match the reality.

Speaking of promises, Oracle's (ORCL) Larry Ellison recently made headlines talking about 48-hour personalized cancer vaccines using AI and robots.

While the technology sounds promising, I'm more interested in the practical path to profitability. Moderna isn't alone in this race, and their well-capitalized competitors have the luxury of funding similar development programs while maintaining positive cash flow.

Given Moderna's cash burn trajectory, their next three quarters will be telling.

I'll be watching that $4 billion nine-month burn rate closely, along with their progress on cost reductions - particularly those inflated SG&A expenses that management seems reluctant to address.

I'm keeping my old vaccination card as a reminder of Moderna's impressive COVID-19 achievement, but I'm not ready to bet on lightning striking twice.

Sometimes the hardest part of investing is knowing when to appreciate history without banking on its repeat performance.

Mad Hedge Biotech and Healthcare Letter

January 28, 2025

Fiat Lux

Featured Trade:

(READY, RESET, GO)

(JNJ), (AAPL), (PFE), (ABBV), (RHHBY), (AZN), (SNY), (NVS)

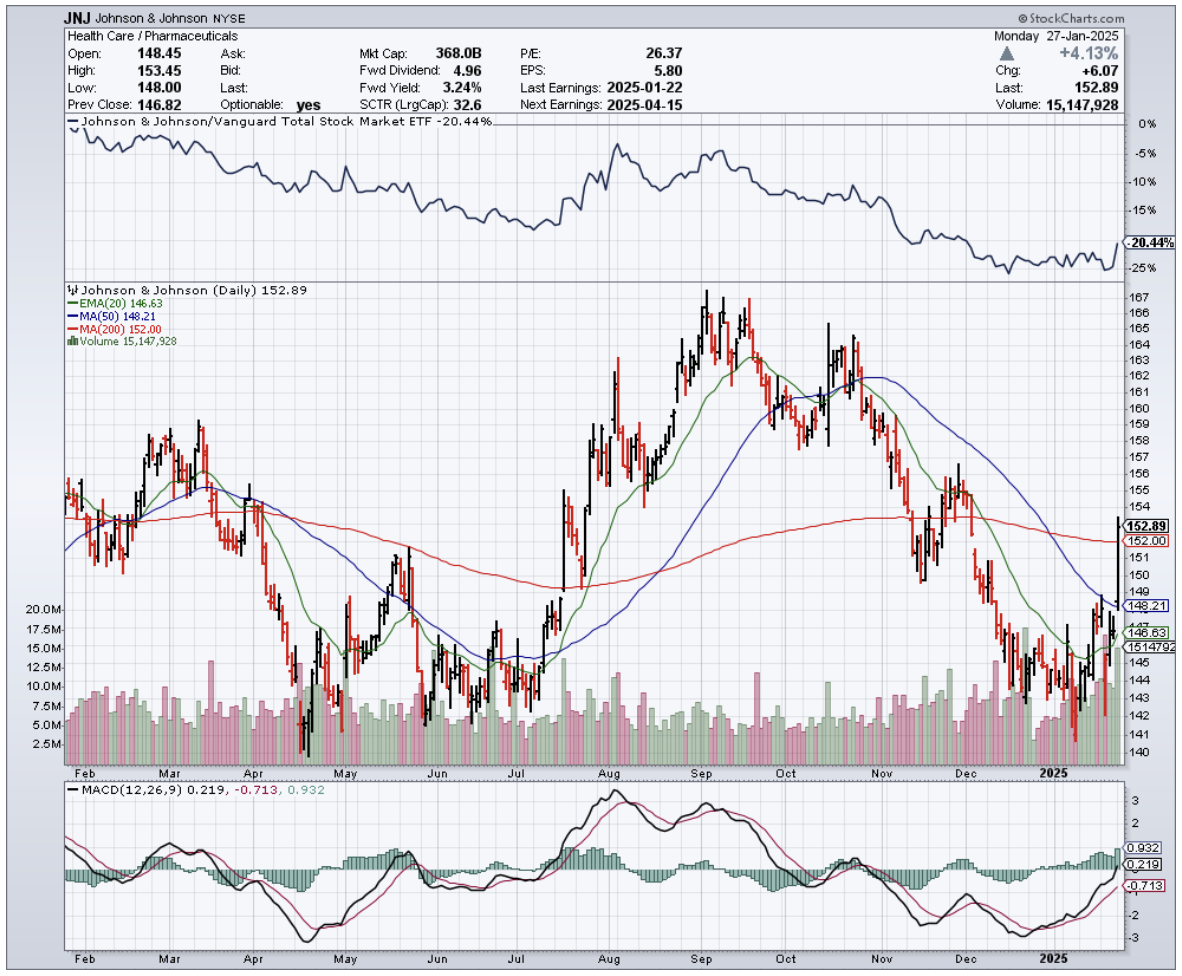

I had to laugh when I saw Johnson & Johnson's (JNJ) Q4 earnings hit my screen earlier this month.

Here we have Wall Street wringing its hands over a slight revenue miss, sending shares down 3.5%, while management is busy plotting its path to pharma industry dominance.

The numbers tell an interesting story.

Q4 revenues grew 5.3% (or 5.7% on an adjusted operational basis) to $22.5 billion. Wall Street got the vapors because earnings came in at $1.41 per share, well below their $2.04 consensus.

Reminds me of the time analysts completely missed Apple's (AAPL) transformation into a services company.

For the full year 2024, JNJ delivered 4.3% sales growth (5.4% operational) to $88.8 billion, with earnings per share landing at $5.79, or $9.98 adjusted after swallowing a $(0.67) hit from acquired IPR&D charges.

Not too shabby for a company in transition.

Looking into 2025, management is guiding for 2.5-3.5% operational sales growth ($90.9-91.7 billion) and adjusted operational EPS of $10.75-$10.95.

That's 8.7% growth at the midpoint, though they're careful to hedge around legal proceedings and acquisition costs.

And here's where it gets interesting.

During last week's JP Morgan Healthcare Conference, CEO Joaquin Duato was practically bouncing in his chair about their drug pipeline. Let's look at what's got him so excited.

Darzalex, their multiple myeloma superstar, raked in $11.67 billion in 2024, up 20%.

The new kid Carvykti exploded 93% higher to $963 million. Tecvayli landed $550 million in its rookie year.

Depression med Spravato jumped 56% to hit the magic $1 billion mark. Tremfya, their Stelara successor, grew 17% to $3.7 billion.

Speaking of Stelara – there's the elephant in the room.

JNJ's crown jewel is losing patent protection, already showing up in Europe with a >12% sequential decline in Q4 to $2.35 billion. Expect a 30% "haircut" this year.

But here's what Wall Street is missing: JNJ saw this coming years ago.

They just dropped $14.6 billion on Intracellular Therapies, mostly debt-funded (they can afford it with only $31.3 billion in long-term debt and $19.98 billion in cash).

This brings them Caplyta, an antipsychotic med with blockbuster potential that's already approved for schizophrenia and bipolar disorders.

The medical device business isn't sitting still either.

Q4 worldwide revenues jumped 6.7% year-on-year. While Surgery was flat at $2.5 billion and Orthopedics grew a modest 2.5% to $2.32 billion, Vision popped 9% to $1.3 billion.

But the real story? Cardiovascular surged 24% to $2.1 billion. Those Shockwave and Abiomed acquisitions are looking pretty smart right about now.

For the year, MedTech grew 4% to $31.56 billion. Operating margins slipped a bit – Innovative Medicines down from 42% to 39.4%, MedTech from 23.7% to 21.6%.

Late-stage pipeline products nearing approval should ease R&D expenses in 2025, just as JNJ gears up for its next growth phase.

The foundation looks rock solid - $19.98 billion in cash, $31.3 billion in long-term debt, 2025 adjusted EPS guidance of $10.75-$10.95, and that reliable $1.24 quarterly dividend.

But forget the current numbers - the real money's in what's coming next.

Here's what the market is missing: JNJ is promising 5-7% compound annual growth between 2025-2030, with ten drugs hitting $5+ billion in annual sales by decade's end.

Sound ambitious? Maybe. But they've got the pipeline to back it up – from immunology stars nipocalimab and icotrokinra to neuroscience contenders seltorexant and aticaprant, plus oncology plays like TAR-200 for bladder cancer.

I've seen this movie before with AbbVie (ABBV), which navigated the loss of $20+ billion Humira without missing a beat.

And JNJ looks even better positioned - their pharma division is targeting $58 billion in 2024 revenues, which would make them the biggest player in Big Pharma, ahead of Pfizer (PFE), AbbVie (ABBV), Roche (RHHBY), AstraZeneca (AZN), Sanofi (SNY) and Novartis (NVS).

The only real wildcard? That pesky talc litigation.

JNJ's latest move – spinning the lawsuits into Red River Talc LLC and filing for bankruptcy – could cap the damage at $8.5 billion. They claim 75% of claimants are on board, with a court ruling expected this month.

So, what's my take? I think JNJ's 2025 will be a "reset" year, especially the first half. But just like buying straw hats in winter, there might be an opportunity here for patient investors. Management says the back half will be stronger, setting up 2026 for what could be a very interesting guidance call.

While the market frets about Stelara's patent cliff, smart money is quietly building positions. That's why I'm maintaining my stand to buy the dip.

After all, sometimes the best trades are the ones that make you a bit uncomfortable at first. And if you're worried about patent cliffs, just ask any AbbVie shareholder how that worked out for them.