Global Market Comments

November 5, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE MAD HEDGE FUND TRADER HITS A NEW ALL TIME HIGH),

(AAPL), (FB), (RHT), (GE), (VXX), (AMZN), (SPY), (IWM), (CRM)

Global Market Comments

November 5, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE MAD HEDGE FUND TRADER HITS A NEW ALL TIME HIGH),

(AAPL), (FB), (RHT), (GE), (VXX), (AMZN), (SPY), (IWM), (CRM)

I used to do a lot of skydiving from 20,000 feet. There’s nothing like a freefall, feeling the wind rip at your jumpsuit as you plunge towards the earth at terminal velocity of 125 miles per hour. In the beginning, the ground looks very far away. Then it suddenly gets very close, very fast.

I used to do this during the 1960s with WWII surplus silk parachutes with a “double L” cut. You hit the ground like a ton of bricks. Sometimes, we’d swing back and forth from the wings of the airplane before letting go just to have fun and freak out the pilot who had no chute.

Over time, you develop a very accurate sense of how fast the ground is approaching and when to pull the ripcord. If you’re wrong, you die.

That’s how I felt when markets went into freefall last Monday. However, after a half-century of trading, I have a highly developed sense of where the bottom is.

So, I piled on the “bet the ranch” longs in technology stocks and shorts in the bond market right at the absolute bottom. And to make sure everyone to a man got in, shares swooshed down one final time when rumors spread that Trump was escalating the trade war with China once again.

By Wednesday morning, the Mad Hedge Fund Trader model portfolio had booked its largest two day gain since the inception of this letter 11 years ago, some 12%. By miracle of miracles, we ended up positive for October, virtually the only one to do so in the entire hedge fund industry.

I would like to think that 50 years of toil in the markets is finally starting to pay off for me. The truth is, the harder I work, the luckier I get.

Stocks lost $2 trillion in market value in October, off 6.9%. Other than that, how was the play, Mrs. Lincoln? Tech took the worst hit in a decade, with many favorites down 20%-30%.

I am raising as much cash as I can ahead of the Midterm Elections tomorrow. Democrats seizing the House of Representatives is priced into the market already.

If the Republicans end up keeping the House, you can count on at least a 1,000-point rally in the Dow Average in the next few days as the door is now open for more tax cuts, more deregulation, and more deficit spending.

If the Democrats end up taking both the Senate and the House you can look for a 1,000 point drop in the Dow. That would bring on a huge “flight to safety” bid in the bond market and yet another opportunity to sell short at great prices.

Either way, I want more dry powder with which to take advantage of any extreme moves that may take place. “Extreme” seems to be the order of the day.

By the way, we are so far in the money with our remaining positions that even with a 1,000 point drop we should still reap the maximum profit with the November 16 option expiration in only 9 trading days.

Not that it matters, but October Nonfarm Payroll Report came in at a red-hot 250,000. The headline Unemployment Rate remained at a two-decade low at 3.7%. The Broader U-6 “Discouraged worker” unemployment rate fell 0.1% to 7.4%.

For the first time in yonks, no sector lost jobs last month. HealthCare added 36,000 jobs, Manufacturing 32,000 jobs, and Leisure & Hospitality 42,000 jobs.

However, the real blockbuster was that Average Hourly Earnings exploded to a 3.1% YOY rate, the highest in ten years. Yes, ladies and gentlemen, this is what inflation looks like, up close and ugly.

The number immediately knocked the wind out of the bond market taking it to a new low for the year. Yes, this is what double short positions in bonds are all about. I saw this coming a mile off.

The backdrop for the bond market is looking worse than ever. The budget deficit is about to break $1 trillion for the first time since the 2009 crash. Rising interest rates mean the government’s debt burden is about to grow by leaps and bounds, eventually becoming its largest expenditure.

The US Treasury is hitting the markets daily with massive new issuance, and the Chinese are dumping what US bonds they have to support the Yuan, now at a ten-year low. This is what Armageddon looks like in slow motion.

Last week was dominated by a China trade war that was on again, then off, then on one more time. The stock market ratcheted four-digit figures every time this happened.

Apple (AAPL) announced record profits yet again but countered with cautious forward sales guidance. Social media pariah Facebook (FB) delivered an earnings report beyond all expectations popping the stock $10.

IBM took over Red Hat (RHT) for $33 billion, the third largest merger in history. It’s too little too late for Big Blue as the stock falls on the news. It all reeks of a “Hail Mary.”

General Electric (GE) cut its dividend from 12 cents a share to one cent after reporting a breathtaking $22.8 billion loss. The Feds have opened a criminal investigation into accounting practices. This may define the final bottom in the stock. Take another look at those long-term LEAPS.

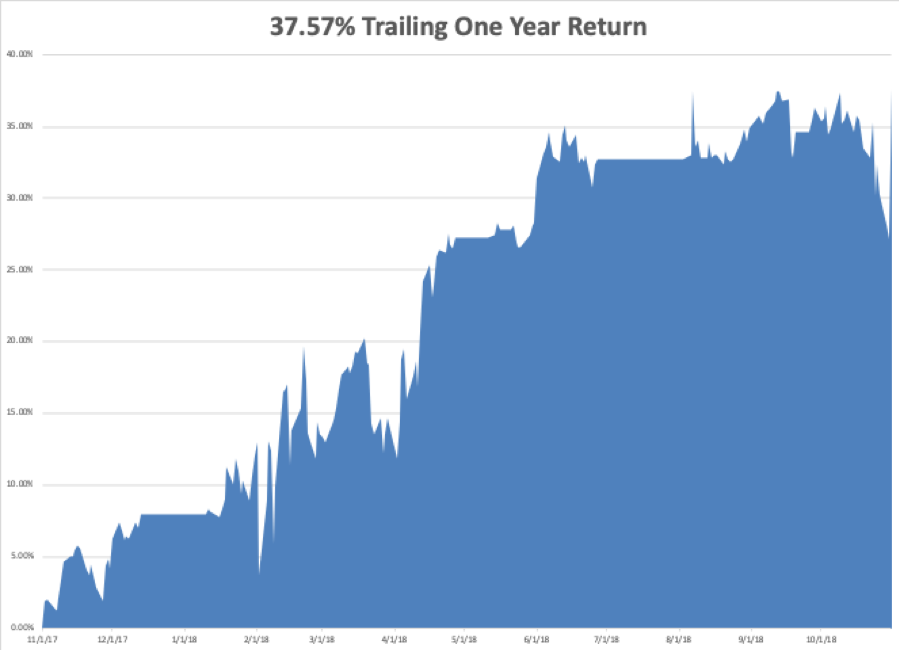

My year-to-date performance rocketed to a new all-time high of +33.17%, and my trailing one-year return stands at 37.57%. October finished at +1.24% and that includes an ill-fated -4.23% loss in the iPath S&P 500 VIX Short Term Futures ETN (VXX).

And this is against a Dow Average that is up a miniscule 1.9% so far in 2018. So far in November, we are up an eye-popping +3.54%.

Incredible as it may seem, the Mad Hedge Fund Trader has been up 18 consecutive months. That’s what you pay for and that’s what you’re getting. There’s nothing more fulfilling in life than making promises to friends, then delivering in spades.

As the market collapses, I scaled into longs in Amazon (AMZN), the S&P 500 (SPY), the Russell 2000 (IWM), and Salesforce (CRM). I used the flight to safety bid in the bond market to double up my short position there, and am kicking myself for not going triple weight.

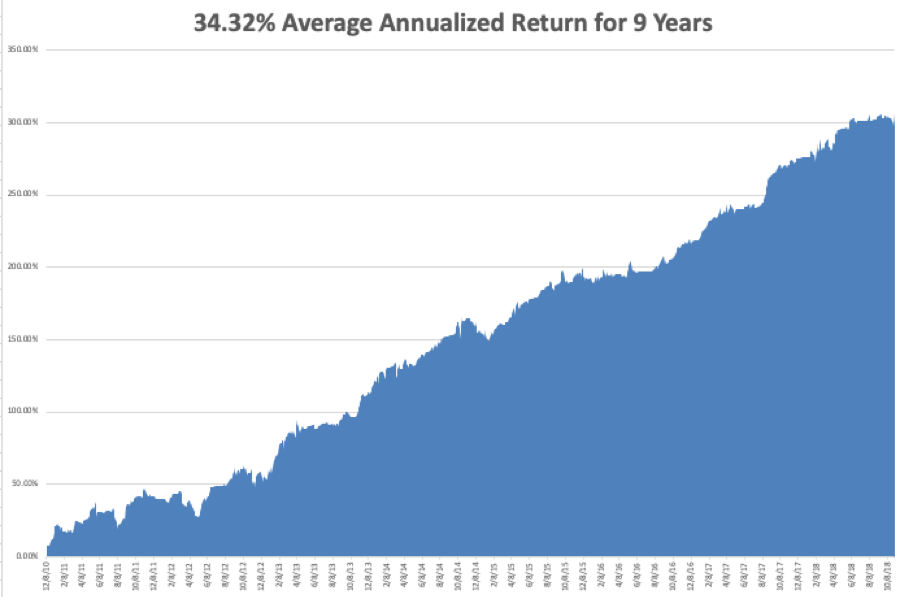

My nine-year return ballooned to 309.64%. The average annualized return stands at 34.72%.

All the BSDs are done reporting Q3 earnings and only a few tag ends are left to report. The carnage is over until we restart the cycle once again in February. In any case, economic data pales in comparison to the election in terms of market impact.

On Monday, November 5 at 10:00 AM, the ISM Manufacturing Index is out.

On Tuesday, November 6 is Election Day. Trading will be a subdued affair and the results will start coming out at 11:00 EST after the west coast polls close.

On Wednesday, October 24 we have the election aftermath to deal with. Up 1,000, down 1,000, or unchanged, who knows?

At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. The Federal Open Market Committee meets to discuss interest rates but will take no action.

On Friday, October 26, at 8:30 AM, the October Producer Price Index is out, an important read on inflation.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I made a massive amount of money personally in the October crash. I am going to plop down $150,000 and buy a brand new Tesla Model X for myself. The ashtrays are full on the old one, and besides, there is a tiny nick in the windshield from driving up to Lake Tahoe. I hear the new one has new “Summon” technology that allows it to drive into a parking lot by itself and drive around until it finds an empty space, then back into it, all untouched by human hands.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 1, 2018

Fiat Lux

Featured Trade:

(LOOK AT ZENDESK FOR YOUR NEXT TEN BAGGER)

(ZEN), (RHT), (AMZN), (MSFT), (CRM), (IBM), (SNAP)

At the recent Mad Hedge Lake Tahoe Conference, I pinpointed software companies as a robust group of tech stocks that are the perfect late cycle investment in the economic environment we find ourselves in now.

To add some granularity about my thesis, I would like to start elaborating on an up-and-coming software stock that I find compelling and in the middle of a growth sweet spot.

And with the rapacious pullback, the tech sector has experienced as of late, this high-octane growth stock is poised to rev back up, albeit with more than your average volatility attached to its stock symbol.

If you can stomach the volatility, then Zendesk (ZEN) is the company for you to dip your toe in.

Zendesk is a customer service software offering solutions to clients through a flexible platform revolving around customer service tickets.

This $6 billion market cap tech firm thriving in the dodgy San Francisco Tenderloin district only need to be reminded of how fast a tech firm can be disrupted by stepping out of the office and experiencing ground zero of the San Francisco homeless movement in the scruffy Tenderloin.

I usually get lambasted for the lack of time I spend following budding tech firms, but you cannot blame me when the bulk of this year’s stock market gains have been extracted by the biggest and mightiest tech titans.

That does not mean all small tech is dead, but they certainly do have heightened existential risk because of the Amazons (AMZN) and Microsofts (MSFT) of the world, spreading their network effects far and wide.

International Business Machines Corporation’s (IBM) purchase of cloud company Red Hat (RHT) underscores the value of applying M&A to grow the top and bottom line, and the chronic bidders of these smaller minnows are usually the Amazons and Microsofts themselves who have the cash to dole out.

Salesforce (CRM) is always adding to its arsenal of integrated software companies that can scale up in the cloud, and Marc Benioff’s M&A strategy has thrived to devastating effect boosting the bottom and top line.

I must admit, tech does get the rub of the green over other industries because of the scaling effect afforded to profit poor tech companies.

The ample time to prove to investors they can snatch a growing user base, enhance product offerings, and develop an eco-system intertwined with recurring subscription products is not fair to other industries who are judged on different metrics mainly profits and profits now.

Well, life isn’t fair.

The addressable market is usually massive causing investors to stick with these burgeoning tech firms through thick and thin.

Zendesk is another company burning money, but let me tell you, they are no Snapchat (SNAP).

Operating margins are marching towards positive territory, meaning this outfit is well-run.

It was only at the beginning of 2015 when Zendesk’s operating margin registered -53%, and since then, they have dramatically reduced it to -36% at the end of 2016 and now -24% in 2018.

Gross margins next quarter will be hit a bit with its acquisition of Base CRM, headquartered in Mountain View, California and R&D offices in Krakow, Poland, offering a web-based all-in-one sales platform featuring tools for email, phone dialing, pipeline management, and forecasting.

Improving service offerings in the tech world usually means nabbing niche cloud companies that can easily be integrated into the larger eco-system and Base CRM, even though it has lower margins than Zendesk, is a nice pickup for the company boosting the top line while expanding cross-selling activities.

Then there is the sales revenue growth demonstrating all the hallmarks powerful software companies live up to with its 39% quarterly revenue growth.

Zendesk’s management has remarked that they fully expect to hit $1 billion in total sales by 2020 which is more than double the 2017 annual revenue of $430 million.

This year, Zendesk is forecasted to post just shy of $600 million in sales.

Large clients keep piling in hoping to modernize their customer service operations and wean themselves off the siloed legacy systems.

Disruption by some fresh newcomer in a disruptive industry that they operate in is usually the trigger forcing companies to spruce up their customer service software.

This path of migration will healthily continue for Zendesk reaffirming management’s thesis of $1 billion in sales by 2020.

Zendesk, flaunting off their innovation skills, identified the universal popularity of messenger app WhatsApp as an effective platform for its services and rolled out a product that integrates Zendesk services with WhatsApp.

This will allow businesses to manage customer service interactions and engage with customers directly on WhatsApp.

The customized integration links conversations between businesses and their customers on WhatsApp within Zendesk.

This move will allow Zendesk to stretch their tentacles further and wider while being able to provide faster support for customer service tickets which are incredibly time-sensitive.

Since management highlighted that WhatsApp is the go-to messenger in Asia Pacific and Latin America, there was no reason not to extend their offerings in a way that captures this vital userbase.

The WhatsApp pivot has been a nice addition with Zendesk’s management remarking that they “handle over 20% of our order status inquiries daily with WhatsApp and Zendesk, which is much faster than traditional methods.”

Omnichannel support within Zendesk’s platform will be key to securing the growth it needs to reach its $1 billion of sales milestone.

Innovation is the crucial ingredient in constructing the perfect products that can maximize customer service performance.

Its overseas exploits are not just a flash in the pan with its services supported in 30 languages and offices in 15 different countries. It all makes sense considering half their revenue is outside of America.

With IBM’s recent acquisition of Red Hat, buyers are still hunting for the right pieces to add to their portfolio.

The Red Hat purchase proved that demand still eclipses supply by a far margin.

Zendesk is one of those in the queue for a big buyer to swoop in with a mega offer.

It’s no guarantee that a company will pay a 63% premium like IBM did, but some sort of premium will be definitely warranted.

Zendesk offers the type of robust growth and premium cloud services that could easily fit into a bigger cloud player looking to improve their assortment of cloud tools.

This type of tailwind itself will naturally boost the stock by 5-10% alone if the macro picture can somehow manage to gain footing for the rest of the year.

As with the rest of tech, Zendesk dipped about 20% in the last 30 days but by no means does that mean this is a bad company with a weak future.

I would very much argue the opposite.

The weakness in sales offers a prime entry point in a fast-growing company that is part of the software and cloud movement that I have incessantly harped about.

If this company can show continued operating margins growth, maintain sales growth of above 30% YOY, and demonstrate product innovation, this stock will break out to higher levels.

As of now, that is exactly the road they are headed down.

Business abroad is doing so well that Zendesk recently splurged on a Europe, Middle East and Africa (EMEA) headquarters in Dublin, Ireland coined as the “the tech capital of Europe.”

Zendesk started with two employees in Dublin in 2012 and now boast over 300 employees occupying 58,000 square feet in a new office costing $10 million.

By 2020, Zendesk expects to build their Dublin branch to over 500 employees implying that the overseas pipeline is ripe for the taking.

I am highly bullish Zendesk and recommend that readers check out this attractive growth story.

![]()

Mad Hedge Technology Letter

October 31, 2018

Fiat Lux

Featured Trade:

(IBM’S PUTS ON A RED HAT)

(RHT), (IBM), (AMZN), (MSFT), (GOOGL), (ORCL)

What took you so long, Ginni?

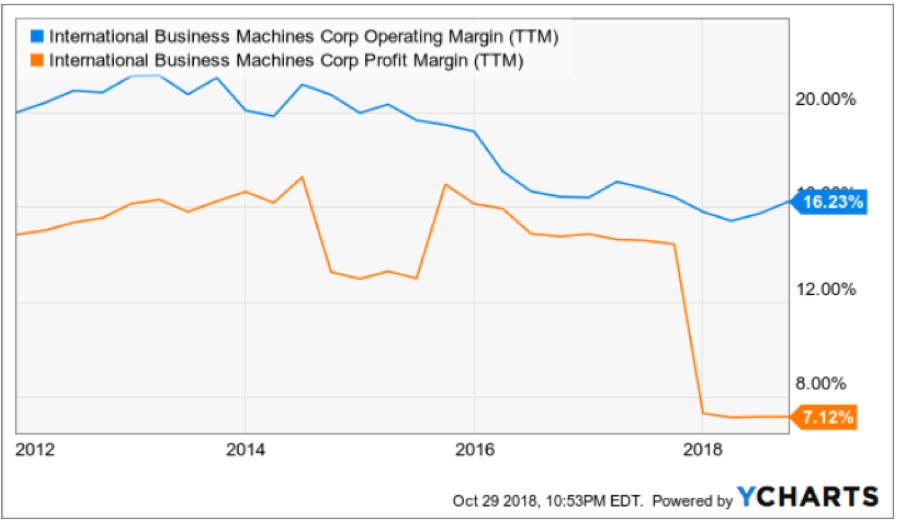

That was my first reaction when I heard International Business Machines Corporation (IBM) was making a big strategic shift by purchasing open source cloud company Red Hat (RHT) in a landmark $34 billion deal.

Ginni Rometty, IBM’s CEO since 2012, has presided over persistent negative sales growth and has done zilch for investors to conjure up some type of lasting hope for this company.

Not only has Rometty failed to grow the top line, but with an underwhelming 3-year EPS growth rate of -2%, the execution and performance haven’t been there as well.

Somehow and someway, she has maintained an iron-clad grip on her job at the helm of IBM and her legacy at IBM will be wholly determined by the failure or success of this Red Hat acquisition.

IBM shares sold off on the news as shareholders digested this bombshell.

Rometty took a hatchet to share buybacks and suspended them for 2020 and 2021 alienating a segment of their loyal shareholder base.

I can tell you one thing about this move – it smells of desperation and it won’t vault IBM into the conversation of Amazon (AMZN) Web Services or the Microsoft (MSFT) Azure.

The biggest winner of this deal is Red Hat’s CEO Jim Whitehurst who has been dangling the company for sale for a while.

Alphabet (GOOGL) was in the mix and had the opportunity to snag a last-second deal, but it never came to fruition.

The 63% premium IBM must pay for a company who only grew quarterly sales 14% YOY and quarterly EPS by 10% is expensive, but that is where we are with IBM.

Clearly overpaying was better than doing nothing at all.

IBM continues to hemorrhage sales and stopping the blood flow is the first step.

Rometty was responsible for the utter failure of artificial intelligence initiative Watson whose terrible management was a key reason for its implosion.

Analyzing this historic company gave me insight into the pitiful causing me to write a bearish story on IBM last month. To read that story, please click here.

Not only was the agreed price exorbitant, but Red Hat’s stock was trending south even before the interest rate induced sell-off rocked the tech sector of late.

Red Hat missed on sales revenue forecasts and offered weak guidance.

It could be the case that Whitehurst was actively seeking a buyer because he felt that Red Hat would go ex-growth in the next few years.

Red Hat was rumored to be on the market for quite a while looking to fetch a premium price for a company starting to stagnate with its visions of grandeur growth.

Rometty’s career-defining moment is high-risk and high-reward and is born out of being cornered by leading tech companies leaving IBM in their dust.

The deal finally allows IBM to return back to sales growth which will occur two years later, and Rometty will finally have that monkey off her back for now.

But the bigger question is will Rometty still have her job in two years if this experiment becomes toxic.

My guess is that Red Hat CEO Jim Whitehurst is automatically the next in line for the IBM throne if Rometty missteps, and piling on pressure will force IBM to evolve or die out.

And even though they will return back to growth, 2% growth is no reason to do cartwheels over.

The real work starts now and it will take years to turn around this dinosaur.

On the brighter side, the massive deals instantly improve sentiment that was flagging for years and puts IBM back on the map.

The synergies between IBM and Red Hat could be robust.

Red Hat can surely help IBM become a higher-quality hybrid cloud solutions company.

Models like this are the industry standard as luring a company into your cloud is one thing, but being able to cross-sell a plethora of extra add-on software services in the cloud is the necessary path to raising profitability.

IBM also inherits a slew of talented software engineers that it can mobilize for innovative cloud products. Red Hat’s products such as JBoss middleware and the OpenShift software for deploying applications in virtual containers could make IBM’s hybrid cloud more appealing and could help retain customers with the additional offerings.

Doubling down on the software side of the business was a strategy I pinpointed at the Mad Hedge Lake Tahoe conference and deals like this highlight the value of this type of assets.

There is a hoard of legacy tech companies like Oracle (ORCL) that is in dire need of such strategic injections and fresh ideas.

This won’t be the last deal of 2018, other cloud deals could shortly follow.

On the other side of the coin, hardware deals have turned rotten quickly with stark examples such as Hewlett-Packard’s (HPQ) $25 billion acquisition of Compaq, Microsoft’s $7.2 billion disastrous buy of Nokia’s mobile handset business and Google’s unimpressive $12.5 billion deal for Motorola Mobility that they later unloaded to Chinese PC company Lenovo.

Investors must be patient if IBM has any chance of completing this turnaround.

Listening to Rometty talk about this deal clearly reveals that she is hyping it up for something way bigger than it actually is.

Let’s not forget that Rometty’s tenure as CEO began in 2012 when IBM shares were trading north of $200 and she has presided over the company while the stock got pulverized by almost 30%.

It pains me that she is the one given the chance to turn the company around after years of underperformance.

Let’s not forget that at the end of 2017, IBM only had a 1.9% share of the cloud infrastructure, about 25 times smaller than Amazon Web Services.

The costly nature of the deal could also put a dent into IBM’s dividend, alienating another swath of its hardcore shareholder base.

Historically, IBM has had minimal success with transformative M&A and the industry competitors dominating IBM magnify the poor management performance headed by Rometty.

Rometty declaring that this deal means IBM will be “no. 1 in hybrid cloud” is overly optimistic, but this is a move in the right direction and could keep IBM spiralling out of control.

A return to sales growth might help stem the bleeding of its downtrodden share price, but Amazon and Microsoft are too far ahead to catch.

Investors will need to wait and see if the synergies between IBM’s and Red Hat’s products are meaningful or not.

Mad Hedge Technology Letter

June 26, 2018

Fiat Lux

Featured Trade:

(THE CHIP DILEMMA)

(MU), (NFLX), (AMZN), (NVDA), (AMD), (RHT)

The hawks are circling around 2019 chip guidance and that is bad news for chip equities.

Perusing through recent earnings reports, it's not a surprise that investors are uncertain whether tech can bail the rest of the equity market out of this slow macro malaise.

The deterioration in the macro climate has given added dependence to the tech vanguard with investors piling into large cap tech as a flight to quality ensues.

It helps when the tech sector is at the heart of every and any future business.

Names such as Amazon (AMZN) and Netflix (NFLX) are so far above their 50-day and 100-day moving averages that investors will take this mild sell-off as a healthy sign of consolidation.

This also means that traders will pin down Netflix's and Amazon's 50-day and 100-day moving averages as the line in the sand for technical support.

The equity weakness underscores that not all tech names are created equal, and firms without moats have been the leakiest.

Red Hat, the up-and-coming enterprise cloud company, became the scapegoat for mid-cap cloud companies triggering a massive sell-off dipping 14.23% instigated by weak guidance.

It was one of the first cloud snafus for a few quarters fueling an intense risk off surge in cloud and chip names.

It seems not a day goes by where the administration does not announce another provocative countermeasure to the tit-for-tat trade skirmish being played out at the highest levels of government.

Analysts have been trigger-happy as the few bears out there are incentivized to be the first one to call the peak of the chip market.

Careers are made and lost with these bold calls.

As bad as the Red Hat (RHT) miss was to the tech narrative, Micron (MU) made a big splash on its quarterly earnings report boding well for large cap tech names.

Micron beat estimates and surprised on the upside on guidance.

Micron was the first recommendation of the Mad Hedge Technology Letter at a cheap $41.

To read the first article of the Mad Hedge Fund Technology Letter about Micron, please click here.

The stock rocketed to more than $60 at the end of March and the end of May, each time dragged down by big picture headwinds.

Micron is a great long-term hold and the volatility in the stock is not for everyone.

If you want to avoid mind-numbing volatility, then stay away from chip stocks as the boom-bust nature of this sector has created a paranoia bias among analysts generating stock downgrades.

Cloud stocks are succinct, zeroing in on the few growth metrics that matter.

The guesswork involved in chip stocks is the perfect formula that leads to downgrades, because the silicon is distributed to other companies for end products of which are hard to keep tabs.

Hence, the chips industry has experienced a tidal wave of wrong analysts calls that unfairly taint chip stocks and the price action that follows.

Micron's data center cloud revenue, a huge driver of DRAM chips, were up 33% QOQ.

The cornerstone of Micron's business and the reinvestment into cloud products has made this stock best of breed in the chip sector and a top 3 chip stock of the Mad Hedge Technology Letter.

The only other stocks that compare with this outstanding growth story and that are at the cutting edge of innovation are hands down Nvidia (NVDA) and Advanced Micro Devices (AMD) in that order.

Next year's profit margins are the next conundrum for the chip industry.

The huge sums of money required to stay ahead of competition could crush profitability.

Pricing is currently stable but stagnant.

The additional marginal costs could be the reason for investors to flee.

More specifically DRAM pricing for 2019 is under the microscope and soft numbers could spell doom for a company that extracts 71% of its revenue from DRAM chips.

All these negative whispers come at a time where DRAM chips are lifting Micron shares to the heavens. And if there was no international friction, the share price would be substantially higher than it is today.

As of today, the chip industry is still grappling with DRAM supply shortages causing costs per unit to spike.

When you consider that DRAM demand is so healthy that China is once again investigating large cap chip companies, investors should be jumping for joy.

These probes are unfounded and are brought about because DRAM pricing is one of the main inputs to setting up data centers and self-driving technology among other businesses.

If China is forced to pay exorbitant prices for groundbreaking chips that can only be found at American and Korean companies, it makes producing every digital end product costlier. infuriating Chinese management.

SK Hynix, Samsung, and Micron comprise more than 90% of the DRAM market, to which Chinese companies need unfettered access.

DRAM chips, unlike other hardware components, are traded on a transparent public market and the probe highlights the building anxiety if Chinese companies are priced out of this sector.

China views the price spike phenomenon in chips as entirely favoring foreign companies that lap up the DRAM profits like money falling from the sky.

Micron carves out half its sales from China, but it is untouchable because loads of chips are required to fuel its global technological supremacy initiative, which is being chipped at by the administration.

CEO of Micron Sanjay Mehrotra has continued to brush off the China threat because he knows Chinese firms cannot fabricate its products.

If this ever happened, kiss the preferential DRAM pricing goodbye, because China would flood the market with substitutes, which has happened to various end markets in the digital and non-digital ecosphere.

The investigation could end in some sort of monetary slap on the wrist and could be payback for blasting a massive hole in Chinese telecommunications hardware conglomerate ZTE's business model.

The administration's heavy-handed response to ban Chinese investment in technology is a long-term victory for Micron, SK Hynix, and Samsung, which have the DRAM market cornered.

These three companies will corner the market even more going forward thanks to help from Washington, widening each moat.

China is not short on funds; it is short on technological expertise because a generation of copy and paste youth cannot compete with the best and brightest minds in Silicon Valley.

Not only can it not compete, it cannot lure the best and brightest to the mainland capitulating local innovation standards.

Its only hope was to pay premium prices for emerging American technology and now that spigot has been turned off.

Technology is in its infancy and is in the early innings of a stunning growth trajectory with a one-way ticket to singularity.

There will be zigs and larger zags on the way. If you thought the Chinese could just ignore Micron and buy from the Koreans, you were wrong.

The relentless demand for DRAM chips is wilder than a British soccer hooligan. Cutting off access to one massive avenue of DRAM chips would be a death knell for any scalable production process that relies on heavy shipments of DRAM chips.

Although markets have been haywire lately, these developments are incredibly bullish, unless China can suddenly produce high-quality chips, which won't be anytime soon.

For the short term, try to pick up the best chip names at yearly lows as tech will not stay suppressed forever.

If you want to scale down the risk, park your funds in the best cloud tech names to weather the storm.

_________________________________________________________________________________________________

Quote of the Day

"We've had three big ideas at Amazon that we've stuck with for 18 years, and they're the reason we're successful: Put the customer first. Invent. And be patient," - said founder and CEO of Amazon Jeff Bezos.

Mad Hedge Technology Letter

May 31, 2018

Fiat Lux

Featured Trade:

(HOW SALESFORCE RAN OVER ORACLE),

(CRM), (ORCL), (MU), (RHT), (MSFT), (INTC), (AMZN), (GOOGL)

Modern tech has an unseen dark side to it.

Coders relish the opaqueness surrounding the industry infatuated with developing the next big thing to take Silicon Valley by storm.

There is nothing opaque about the Mad Hedge Technology Letter.

I grind out recommendations and you follow them. Period. End of story.

To put it mildly, the letter has gotten off to a flying start since its inception in February 2018, and there is no looking back, only looking forward.

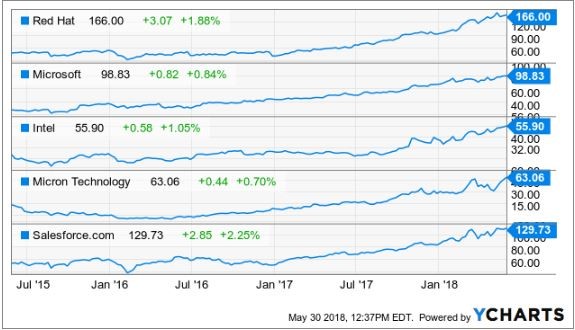

Micron (MU), Red Hat (RHT), Microsoft (MSFT), and Intel (INTC), just to name a few, have been solid recommendations standing up to all the nonsense and mayhem permeating throughout the periodically irrational markets.

Have you noticed lately when you open up the morning paper while sipping on a steaming mug of Blue Bottle Coffee, that almost every story is about technology?

It's not a mistake. I swear.

Technology is permeating into the nooks and crannies of our society and the leaders of this movement are laughing all the way to the bank.

One of those aforementioned pioneers is no other than local lad, Salesforce CEO and perennial Facebook basher Marc Benioff.

I recommended Salesforce at $110 and it was one of the first positions in the Mad Hedge Technology portfolio.

You can't blame me.

I saw this stock pick from a million miles away and I will explain why.

Salesforce set ambitious targets that nobody thought were realistic at the time.

How high in the sky does Benioff want to build his castles?

By 2022, Marc Benioff set out sales targets of a colossal $20 billion per year.

Then Benioff gushed that Salesforce would pass the $40 billion mark, done and dusted by 2028 and $60 billion by 2034.

Remember that tech CEOs are incentivized to forecast ludicrous sales targets because it lures in the unknowledgeable investor.

Unknowledgeable or pure genius, it does not matter, Salesforce is an emphatic buy.

Salesforce is the ultimate growth stock.

In 2016, annual revenue came in at $6.67 billion, which is about the same size as a middle level semiconductor company.

They followed that up with $8.38 billion in 2017, demonstrating the parabolic shaped trajectory of the company.

At the end of fiscal year 2017, Salesforce announced that it expects revenue of around $12.60 billion in 2019.

The latest earnings report, Benioff disclosed full year guidance of $13.13 billion.

This puts Salesforce in the running to achieve its lofty aspirations.

Apparently, the castles Benioff is building aren't in the sky after all.

Theoretically, if Benioff expands the business into a $16 billion to $16.5 billion business by 2019, Salesforce will have a more than likely chance to pass the $20 billion mark by the end of 2020, a full two years than initially thought.

Salesforce will have ample wiggle room on the way to $20 billion if it is 2022 for which it aims.

Why am I rambling on about revenue?

It's the only metric that Salesforce investors value.

The company registered two straight years of less than $200 million in profits then followed it up with a less than stellar 2016 where it lost almost $50 million.

Don't expect any dividends from this neck of the woods anytime soon especially after acquiring MuleSoft, an integration software company, for $6.5 billion last quarter.

This purchase will add another $315 million of annual revenue to Salesforce's quest of eclipsing its future sales targets. This was after MuleSoft made $296.5 million in 2017 before it became a part of Marc Benioff's stable.

Benioff has proved a shrewd dealmaker, taking advantage of cheap capital to add suitable parts to his business.

Since 2016, Benioff has snapped more than 50 niche software companies that he rebrands as Salesforce products and sells them as add-on products.

This is further evidence that any funds available will be allocated toward reinvestment into products and services deeming any future dividend inconceivable, especially with the elevated revenue targets to surpass.

As for the business. Do we still need to talk about it?

Rip-roaring growth was seen across the board with total revenue increasing 25%.

Investors should stay away from any cloud company that is growing less than 20%.

Market intelligence firm International Data Corporation (IDC) voted Salesforce as the No. 1 client relationship management (CRM) platform for the fifth consecutive year.

It is the industry leader in sales, marketing, service, and increased market share in 2017, more than its closest competitors.

Larry Ellison must be tearing his hair out as Oracle's (ORCL) share price has been excommunicated to purgatory indefinitely.

Oracle is a company that I have been pounding on the tables to stay away from.

The Mad Hedge Technology Letter seldom recommends legacy companies that are still legacy companies.

Driving past his former estate, emanating from a sparkling perch in Incline Village overlooking Lake Tahoe, my neighbor gives me the goose bumps.

The property was later sold for $20.35 million. All told, Larry has around $100 million invested in real estate dotted around Incline Village. I sarcastically mentioned to him last time we bumped into each other to call me immediately when his $90 million estate in Kyoto, Japan, hits the market.

Oracle's position in the pecking order is a telltale sign of the inability to land the creme de la creme government contracts that ostensibly fall into Amazon (AMZN), Alphabet (GOOGL), and Microsoft's lap.

And it's not surprising that Larry is spending more time tending to his vast array of glittering luxury properties around the world rather than running Oracle.

Oracle is like a deer caught in the headlights and Marc Benioff is at the wheel.

On the Forbes 500 rankings, Salesforce has moved up almost 200 spots.

This position will rise as Salesforce is under contract booking a further $20.4 billion of commitments driven by its subscription services offering cloud products.

On the domestic contract front, it was much of the same for Salesforce, which inked premium deals with the U.S. Department of Agriculture, Kering, and sports apparel giant Adidas.

International companies such as Philips and Santander UK are expanding their relationships with Salesforce. A firm nod of approval.

Salesforce has been voted in the top three of most innovative companies for the past eight years by reputable Forbes magazine. The list was started in 2011, and it has never dropped out of the top three.

The gobs of innovation are the main logic behind the top five financial institutions expanding their relationship with Salesforce by an extra 70%.

Once companies start using the CRM platform, they become mesmerized with the premium add-ons that help companies run more efficiently.

Benioff has been a huge proponent of artificial intelligence (A.I.) and is an outsized catalyst to product enhancement gains.

Salesforce has taken Einstein, it's A.I. platform, and allowed all the applications to run through it.

The integration of Einstein has resulted in more than 2 billion correct predictions per day paying homage to the quality of A.I. engineering on display.

Instead of hiring a whole team of in-house data scientists, Salesforce is A.I. functionality by the bucket full and it is easy to use on its platform.

In some cases, incorporating Salesforce's A.I. into the business has bolstered other companies' top line by 15%.

Often, Salesforce's A.I. tools are declarative meaning the technology can identify solutions without a fixed formula.

Benioff has choreographed his strategy perfectly.

He is betting the ranch on unlocking data from legacy companies that migrate to his platform.

MuleSoft will help in this process of extracting value, then A.I. will supercharge the data, which is being unlocked.

What does this mean for Salesforce?

Higher revenue and more clients leading to accelerated growth. The share price has powered on north of $130, and after I recommended it at $110, I am convinced this stock will surge higher.

Salesforce is an absolute no-brainer buy on the dip.

Growth Means Shiny New Office Buildings

_________________________________________________________________________________________________

Quote of the Day

"If we become leaders in Artificial Intelligence, we will share this know-how with the entire world, the same way we share our nuclear technologies today." - said current President of Russia, Vladimir Vladimirovich Putin.