Mad Hedge Technology Letter

April 29, 2022

Fiat Lux

Featured Trade:

(TELADOC IMPLODES)

(ARKK), (SARK), (TDOC), (ROKU), (SHOP), (ZM)

Mad Hedge Technology Letter

April 29, 2022

Fiat Lux

Featured Trade:

(TELADOC IMPLODES)

(ARKK), (SARK), (TDOC), (ROKU), (SHOP), (ZM)

The Cathie Wood circus keeps making new lows as digital doctor platform Teladoc (TDOC) recorded the biggest drop in shares since its IPO.

At one point, shares were down 45% and this was the day after buying another tranche of over $200 million worth of shares before the earnings came out.

TDOC was a pandemic darling and since then, the stock has done nothing but dive lower.

There is even an inverse ETF to jump on the anti-Cathie Wood bandwagon called Tuttle Capital Short Innovation ETF (SARK).

SARK is almost up 100% year to date showing that as market conditions distort, traders must distort with them.

To stay long tech growth is like throwing money off an apartment balcony.

The lack of understanding Cathie Woods exhibits about the stock market is hard to fathom.

Her go-to excuse is that others “aren’t doing the research.”

We were smack dab in a low-rate environment for a decade when even marginal tech companies would get the benefit of the doubt.

As the goalposts have moved and narrowed, Wood is still sticking to her 5-year time horizon and still explaining to investors that other analysts “aren’t doing their homework.”

This really is a case of the emperor having no clothes if I have ever seen it.

To add insult to injury, she has gone on public television to speak about how she believes the global economy is experiencing deflationary pressures.

No matter what changes to the trading environment, she sticks to her narrow story of deflation and her 5-year time horizon while her investors lose money.

If that’s not enough, she blames the market for not understanding her ARKK fund which is down more than 50% this year.

She claims that many people are “devaluing innovation” and just do not understand innovation like she does.

With an unrelenting belief in her growth strategy, miraculously, another $1.5 billion of inflows have juiced up her fund in 2022.

There are many out there that still think she is a great money manager after her one call of Tesla going up was correct.

Investors have chosen to back her further even with mounting losses and that has now backfired as ETF ARK Innovation ETF (ARKK) appears as if the market has not recognized how smart Cathie Wood is.

ARKK is Teladoc’s largest shareholder with a 12% stake worth.

It’s not just TDOC, but other investments like Roku (ROKU), Zoom Video Communications (ZM), and Shopify (SHOP) whose shares have experienced cataclysmic meltdowns of epic proportions.

Why did TDOC shares perform so poorly?

Higher advertising expenses in the mental health market, as well as an “elongated sales cycle” in chronic conditions as employers and providers of healthcare plans evaluate strategies.

TDOC’s services aren’t as good as first thought.

TDOC also took a $6.6 billion charge for impairment of goodwill, a non-cash charge the company excluded from its adjusted results.

The competition also has increased significantly and many of these first-move advantages are not holding up like they used to in tech.

The recent performance has been met with a bevy of analyst downgrades and tech growth as a sub-sector will have a hard time recovering until a lower interest rate sentiment comes back to sweep up the market.

Still, not a peep out of Cathie Wood on modifying her controversial strategies and that’s when we are staring down a barrel of multiple 50 basis point interest rate rises.

She was photographed partying in the Bahamas at some beach parties the day before the TDOC debacle, apparently, she isn’t bothered that much by her followers losing generation wealth.

If readers want to get back into tech growth after an easing of credit conditions, avoid buying ARKK and just buy a collection of strong tech growth yourself.

Mad Hedge Technology Letter

April 20, 2022

Fiat Lux

Featured Trade:

(PEAK EYEBALLS)

(DIS), (CURI), (ROKU), (PTON), (ZM), (WBD), (FUBO), (NFLX)

Online streamers now have no pricing power.

Remove jacking up prices from the equation and streamers like Netflix (NFLX) and Disney (DIS) look quite mediocre and that’s what the 35% drop in NFLX shares are telling us.

NFLX Ahh factor has vanished.

It used to be that they knew they could raise prices whenever they wanted and that tool in their kit kept investors on board.

CNN+’s dismal foray into pay tv was another red flag when owner Warner Bros. Discovery (WBD) decided to pull all marketing spend because of the paltry viewing results.

There’s just too much competition out there and instead of creating more leeway, growth was pulled forward the past 2 years, and now the chickens are coming home to roost.

Shelter-at-home stocks like Peloton (PTON) and Zoom (ZM) are now surplus to requirements.

It was just not that long ago, that fresh streaming TV options launched at a frenzied pace.

With many subscription services available, streaming entertainment became ubiquitous in U.S. homes as consumers spent large quantities of time and money on streaming media.

As economies reopen following the end of the health situation, and consumers spend more time outside of their homes, there still are just other things to do like going outside.

The idea that there are still many years of streaming growth lie ahead for the streaming industry has turned out to be an utter fallacy.

These are some tech companies impacted.

The much-anticipated Disney+ streaming service was launched in late 2019, just in time for the health situation.

It added tens of millions of subscribers worldwide in its first year and quickly became the second-largest subscription streaming service after Netflix. Disney also owns the streaming services Hulu and ESPN+ in the U.S. but they still don’t turn a profit on many of these streaming assets yet.

It is unlikely that new content will reverse generating excessive losses.

Better Disney stick to the amusement parks.

Streaming TV has been a boon for the smart TV and streaming device maker.

Roku has become the largest TV platform in the U.S., distributing content via The Roku Channel and acting as a hub for households to manage all of their streaming subscriptions.

Roku distributes its smart TV software and streaming devices at minimal cost, making money instead on advertising and by managing subscriptions.

With peak eyeballs on streaming, don’t expect any explosive growth from Roku, in fact, they could go with a whimper and wait for a buyout.

This is a warning sign for any tech company that chooses to not produce their own in-house content and relying on others to draft the narrative of future health is awfully dangerous in a zero sum game.

Streaming service fuboTV, a relative newcomer to the streaming media industry, went public in 2020.

This small service has gained popularity as a live TV platform, and it’s a top option for those who want to watch live sporting events.

The smaller they come, the harder they fall.

Smaller streaming companies have little recourse when multiple exogenous forces impact the company.

fuboTV is nowhere near profitability and has lost close to half a billion dollars in each of the past 2 years.

Public companies are often harangued for going ex-growth the second they are tradable in New York, and this is the epitome of what I am talking about.

The stock has gone from $35 to $5 today in the past 5 months.

Don’t catch a falling knife here.

CURI is another newbie to the dying streaming industry.

This streaming media company focuses on documentaries and science content and was founded by Discovery’s

CURI is competing against some well-entrenched rivals in the non-fiction TV space, including Discovery and Disney’s National Geographic (available on Disney+).

The young company keeps its content creation costs relatively low since it focuses on educational material and partners with universities, but who really wants to see this type of content anyway.

This company sounds boring and naïve.

CURI’s stock price has gone from $17 to $2 in the past 5 months.

Avoid like the plague!

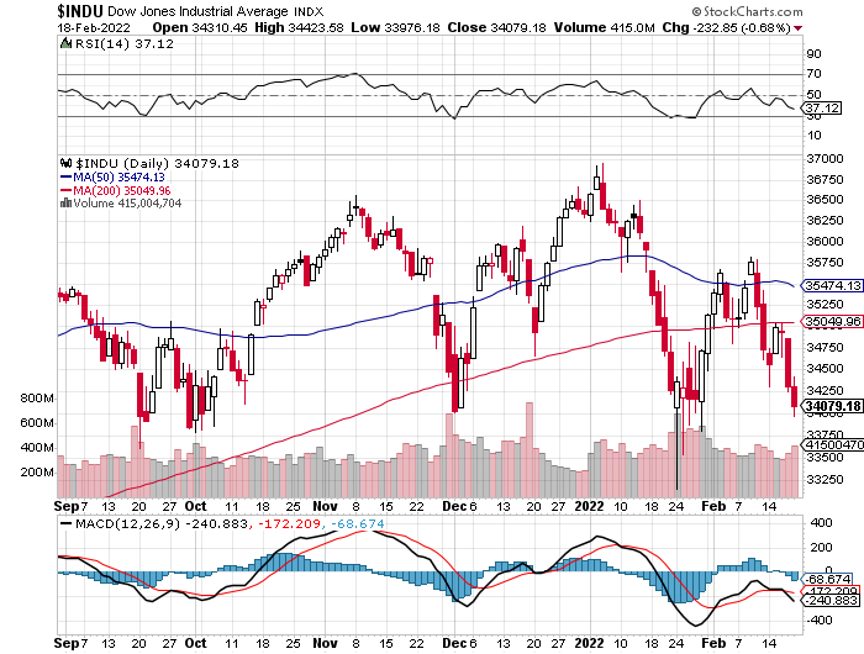

Global Market Comments

February 22, 2022

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or BUYING AT THE SOUND OF THE CANON),

(SPY), (TLT), (TBT), (BRKB), (MSFT), (GOOGL),

(NFLX), (ZM), (DOCU), (ROKU), (VMEO)

“Buy at the sound of the canon.”

That was the sage advice Nathan Rothschild, ancestor of my former London neighbor Jacob Rothschild, gave to friends about trading stocks during the Napoleonic Wars.

Of course, information moved rather slowly back in 1812, pre-internet. Rothschild relied on carrier pigeons to gain his unfair advantage.

You have me.

Somehow, you have descended into Dante’s seventh level of hell. You have to wake up every morning now, wondering if it will be Jay Powell or Vladimir Putin who is going to eviscerate your wealth, postpone your retirement, and otherwise generally ruin your day.

Every price in the market already knows we’re in a bear market except the major indexes.

The roll call of the dead looks like a WWI casualty report: (NFLX), (ZM), (DOCU), (ROKU), (VMEO). It’s like the bid offer spread has suddenly become 25%. Companies are either reporting great earnings and seeing their shares go through the roof. Or they are sorely disappointing and getting sent to perdition on a rocket ship.

The most fascinating thing to happen last week was a new low in the bond market, since you’re all short up the wazoo, courtesy of a certain newsletter. Ten-year US Treasury yields tickled 2.05%, a two-year high, then retreated to 1.92%. That means bonds have completed their $20 swan dive from their December high, a repeat of the 2021 price action.

Trading has gotten too easy, so I think bonds will stall out here for a while. I even added a small long. And please stop calling me to ask if you should sell short bonds down $20. It’s perfect 20/20 hindsight. You can’t imagine how many such calls I’ve already received.

Our old friend, the barbarous relic, returned from the dead last week too. All it needed was for bitcoin to die a horrible death for gold to recover its bid. A prospective war in the Ukraine helped take it to a one-year high.

However, I think it’s safe to say that has lost its value as an inflation hedge for good. If a move in the CPI from 2% to 7.5% can’t elicit a pulse in the yellow metal now, it never will.

The US dollar was another puzzler last week. While the fixed income markets went from discounting three rate hikes this year to six, the greenback flatlined. It was supposed to go up, as currencies with rapidly rising interest rates usually do.

Maybe the buck just forgot how to go down. Or maybe this is the beginning of the end, when sheer over-issuance destroys the value of the US dollar. Some $30 trillion in the national debt will do that to a currency.

I know you will find this difficult to believe, but there are some outstanding money-making opportunities setting up later in the year. The crappier conditions look now, the better they will become later. But you are going to have to practice some extreme patience to get to the other side.

I hope this helps.

Goldman Sachs Chops 2022 Market Forecast, taking the S&P 500 goal from $5,100 down to $4,900. A tighter interest rate picture is to blame, with the year yields topping 2.05% on Friday. Higher interest rates devalue future corporate earnings and kill the shares of non-earning companies.

Oil Hits Seven-Year High, to $94.44 a barrel, up 3.3% on the day. Putin’s strategy of talking oil prices up with Ukrainian invasion threats is working like a charm. That’s what this is all about. Texas tea accounts for 70% of Russian government revenues.

Fed to Front-Load Rate Rises, says St. Louis Fed president Bullard. The drumbeat for a more hawkish central bank continues. Bonds were knocked for two points.

Wholesale Prices Rocket 1% in January and are up a nosebleed 9.7% YOY. Inflation has clearly not peaked yet. Look for stocks to get punished once the current short-covering rally runs out of gas.

Retail Sales Soar by 3.8%, in January indicating that the economy is stronger than it appears. The rapid shift to an online economy is accelerating. Inflation is the turbocharger. When stocks overshoot on the downside load the boat.

Weekly Jobless Claims Jump, to 248,000. The weird thing is that the economic data says the opposite, that the economy is strengthening. Expect flip-flopping data and markets all year.

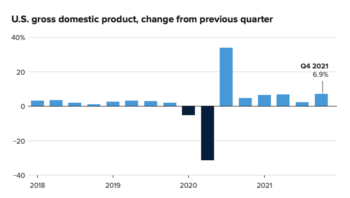

US GDP Jumped by 6.9% in Q4, well above estimates. Consumers are spending like drunken sailors. Eventually, the stock market will notice this, but not before we see lower lows first.

Gold Catches a Bid, off the back of the unrelenting Ukraine crisis. This may continue as a drip for months. Watch it collapse when peace is declared.

Existing Home Sales Jump 6.7%, to 6.5 million units, far better than expected. Inventory is down to yet another record low of 16.5%, an incredibly short 1.6-month supply. The Median Home Price has risen to $350,300, with the bulk of sales on the high end. Million-dollar plus homes are up 39% YOY.

Bond Yields Dive to a 1.93% Yield after failing at 2.05%. There is another nice (TLT) put spread setting up here. Let’s see if war breaks out over the weekend. The threats continue.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

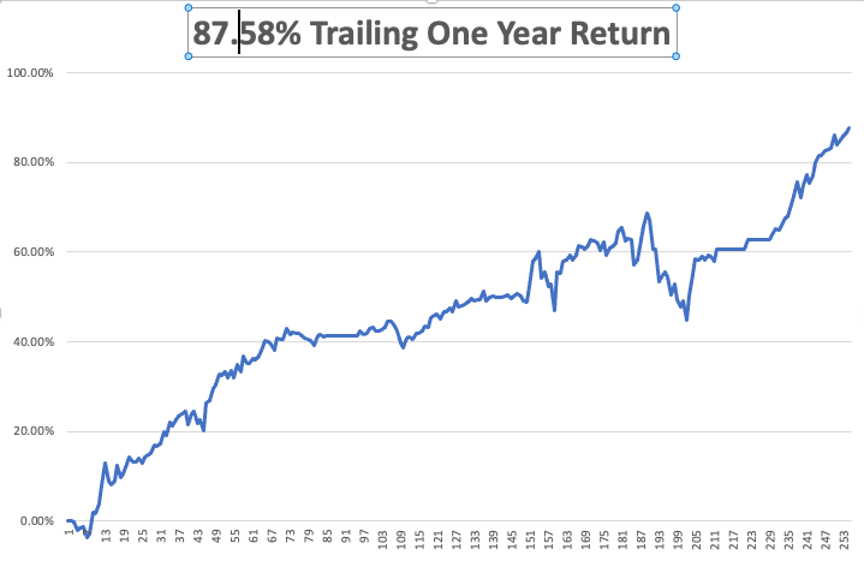

With seven options positions expiring at max profit on Friday, my February month-to-date performance rocketed to a blistering 10.37%. My 2022 year-to-date performance has exploded to an unbelievable 24.90%. The Dow Average is down -7.9% so far in 2022. It is the great outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

With 30 trade alerts issued so far in 2022, there was too much going on to describe here. Check your inboxes.

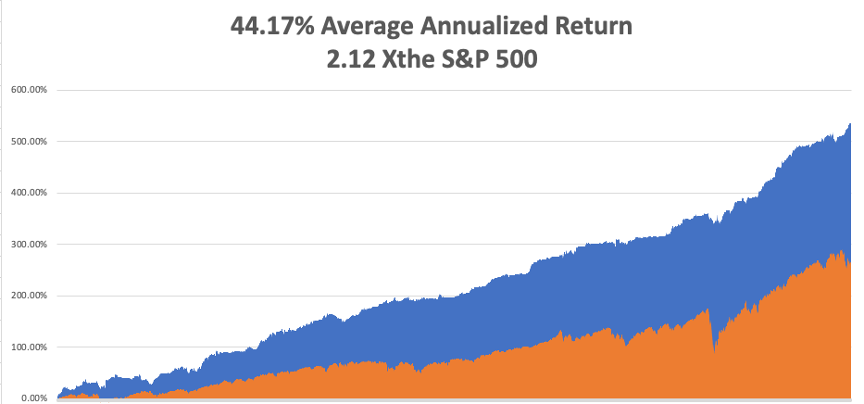

That brings my 13-year total return to 537.46%, some 2.00 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.17% for the first time. How long it will keep rising I have no idea, but as long as it is, I’m not complaining. When you’re hot, you have to be maximum aggressive. That’s me to a tee.

We need to keep an eye on the number of US Coronavirus cases at 78.5 million, down 67% from the January peak, and deaths close to 936,000, off 20% in two weeks, which you can find here.

On Monday, February 21 markets are closed for Presidents Day.

On Tuesday, February 22 at 8:30 AM, the S&P Case Shiller National Home Price Index for December is announced.

On Wednesday, February 23 at 1:30 PM, API Crude Oil Stocks are released.

On Thursday, February 24 at 8:30 AM, Weekly Jobless Claims are published. The second estimate for Q4 GDP is also disclosed.

On Friday, February 25 at 7:00 AM, Personal Income & Spending for January is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, in the seventies, Air America was not too choosy about who flew their airplanes at the end of the Vietnam War. If you were willing to get behind the stick and didn’t ask too many questions, you were hired.

They didn’t bother with niceties like pilot licenses, medicals, or passports. On some of their missions, the survival rate was less than 50% and there was no retirement plan. The only way to ignore the ratatatat of bullets stitching your aluminum airframe was to turn the volume up on your headphones.

Felix (no last name) taught me to fly straight and level so he could find out where we were on the map. We went out and got drunk on cheap Mekong Whiskey after every mission just to settle our nerves. I still remember the hangovers.

When I moved to London to set up Morgan Stanley’s international trading desk in the eighties, the English had other ideas about who was allowed to fly airplanes. Julie Fisher at the London School of Flying got me my basic British pilot’s license.

If my radio went out, I learned to land by flare gun and navigate by sextant. She also taught me to land at night on a grass field guided by a single red lensed flashlight. For fun, we used to fly across the channel and land at Le Touquet, taxiing over the rails for the old V-1 launching pads.

A retired Battle of Britain Spitfire pilot named Captain John Schooling taught me advanced flying techniques and aerobatics in an old 1949 RAF Chipmunk. I learned barrel rolls, loops, chandelles, whip stalls, wingovers, and Immelmann turns, everything a WWII fighter pilot needed to know.

John was a famed RAF fighter ace. Once he got shot down by a Messerschmitt 109, parachuted to safety, took a taxi back to his field, jumped into his friend’s Spit, and shot down another German. Every lesson ended with a pint of beer at the pub at the end of the runway. John paid me the ultimate compliment, calling me “a natural stick and rudder man,” no pun intended.

John believed in tirelessly practicing engine-off landings. His favorite trick was to reach down and shut off the fuel, telling me that a Messerschmitt had just shot out my engine and to land the plane. When we got within 200 feet of a good landing, he turned the fuel back on and the engine coughed back to life. We practiced this more than 200 times.

When I moved back to the US in the early nineties, it was time to go full instrument in order to get my commercial and military certifications. Emmy Michaelson nursed me through that ordeal. After 50 hours flying blindfolded in a cockpit, you get very close with someone.

Then came flight test day. Emmy gave me the grim news that I had been assigned to “One Engine Larry” the most notorious FAA examiner in Northern California. Like many military flight instructors, Larry believed that no one should be allowed to fly unless they were perfect.

We headed out to the Marin County coast in an old twin-engine Beechcraft Duchess, me under my hood. Suddenly, Larry shut the fuel off, told me my engines failed, and that I had to land the plane. I found a cow pasture aligned with the wind and made a perfect approach. Then he asked, “How did you do that?” I told him. He said, “Do it again” and I did. Then he ordered me back to base. He signed me off on my multi-engine and instrument ratings as soon as we landed. Emmy was thrilled.

I now have to keep my many licenses valid by completing three takeoffs and landings every three months. I usually take my kids and make a day of it, letting them take turns flying the plane straight and level.

On my fourth landing, I warn my girls that I’m shutting the engine off at 2,000 feet. They cry “No dad, don’t.” I do it anyway, coasting in bang on the numbers every time.

A lifetime of flight instruction teaches you not only how to fly, but how to live as well. It makes you who you are. Thus, my insistence on absolute accuracy, precision, risk management, and probability analysis. I live my life by endless checklists, both short and long term. I am the ultimate planner and I have a never-ending obsession with the weather.

It passes down to your kids as well.

Julie became one of the first female British Airways pilots, got married, and had kids. John passed on to his greater reward many years ago. I don’t think there are any surviving Battle of Britain pilots left. Emmy was an early female hire as United pilot. She married another United pilot and was eventually promoted to full captain. I know because I ran into them in an elevator at San Francisco airport ten years ago, four captain’s bars adorning her uniform.

Flying is in my blood now and I’ll keep flying for life. I can now fly anything anywhere and am the backup pilot on several WWII aircraft including the B-17, B-24, and B-25 bombers and the P-51 Mustang fighter.

Over the years, I have also contributed to the restoration of a true Battle of Britain Spitfire, and this summer I’ll be taking the controls at the Red Hill Aerodrome for the first time.

Captain John Schooling would be proud.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain John Schooling and His RAF 1949 Chipmunk

A Mitchell B-25 Bomber

A 1932 De Havilland Tiger Moth

Flying a P-51 Mustang

The Next Generation

Mad Hedge Technology Letter

January 12, 2022

Fiat Lux

Featured Trade:

(JUMP OFF THE ROKU BANDWAGON)

(ROKU), (GOOGL), (AMZN)

Many “experts” have been advising investors to buy the dip in Roku (ROKU) since it dropped to $370 from the peak of $480 it reached in July 2020.

These experts kept banging the drum to buy the dip on Roku as it slid to $350 then $320.

The calls for dip-buying continue as Roku nosedived to $280 then most recently on a downgrade, Roku fell all the way to $177.

Painful as it feels to be an investor in Roku, this is not the time to double down on high-tech growth stocks.

Growth tends to usually overshoot to the upside as investors give a pass to growth for losing money and selectively put a premium on high growth rates.

But that deal is only valid in a low-interest rate environment and what we are witnessing is the reverse happen as investors are bolting from Roku like stallions out the back of a stable.

At a micro level, there is somewhat distaste at the ever-increasing competition Roku is facing and the lack of growth prospects overseas.

Overseas is usually the growth engine for many of these streaming cohorts, but the dilemma here is that margins are lower because of a poor purchasing power profiles for the median consumer overseas.

That’s not to say it’s easy to succeed in the U.S. — hardly so.

However, Roku’s business in the United States has been highly successful, but the issue here is that the market is getting somewhat saturated and since the stock market is priced based on future cash flow, where does the incremental buying come from to save Roku’s stock?

Roku faces a perilous uphill challenge to convince the incremental platform user to install its Roku stick at a time when Amazon (AMZN) and Google (GOOGL) are using their greater clout and sharper elbows to get rid of the tech peons.

Amazon reported sales of over 150 million Fire TV devices recently. Roku has over 56 million active accounts, although it’s not a direct comparison because Amazon’s figure counts sold devices and includes Fire TV devices that are not being used.

There is no possible way that Roku can secure 50% of the market here and 40% would be a stretch capping its ceiling.

Another leery signal came when smart television maker TCL who have partnered to make the Roku smart TV decided to jump ship to Google.

This could represent a red flag as these bigger companies have the capacity to poach talent, know-how, and convince suppliers to jump ship with a more lucrative contract for a larger install base.

This could be the first point of contact that could eventually lead to Google buying out TCL and cutting off Roku from a source of a hardware supplier.

TCL has now claimed to be one of the biggest sellers of sets featuring Google’s connected TV operating system and the partnership will take precedence over anything Roku is involved with.

In the short term, readers need to stay away from Roku as we need more commentary on how it plans to shake off Google and Amazon and how it plans to navigate a perceived saturation in its domestic business while underperforming overseas.

Granted, it’s intimidating to go up against Google and Amazon because there are less tools available in the tool kit in terms of stacking resources and convincing consumers that they are indeed a higher quality product.

Long term, I don’t see it for Roku.

Short term, it’s dicey at best.

This stock promises to be volatile in the next three months and actively trading this stock will probably mean selling sharp rallies and avoiding dips.

The first-mover advantage was stellar for a while and Roku rode that donkey up the mountain of success, but now as reality sets in and the first-mover advantage dissipates, they need a miracle or should just negotiate to sell itself while the stock price is still near $200.

It’s sink-or-swim at this point.

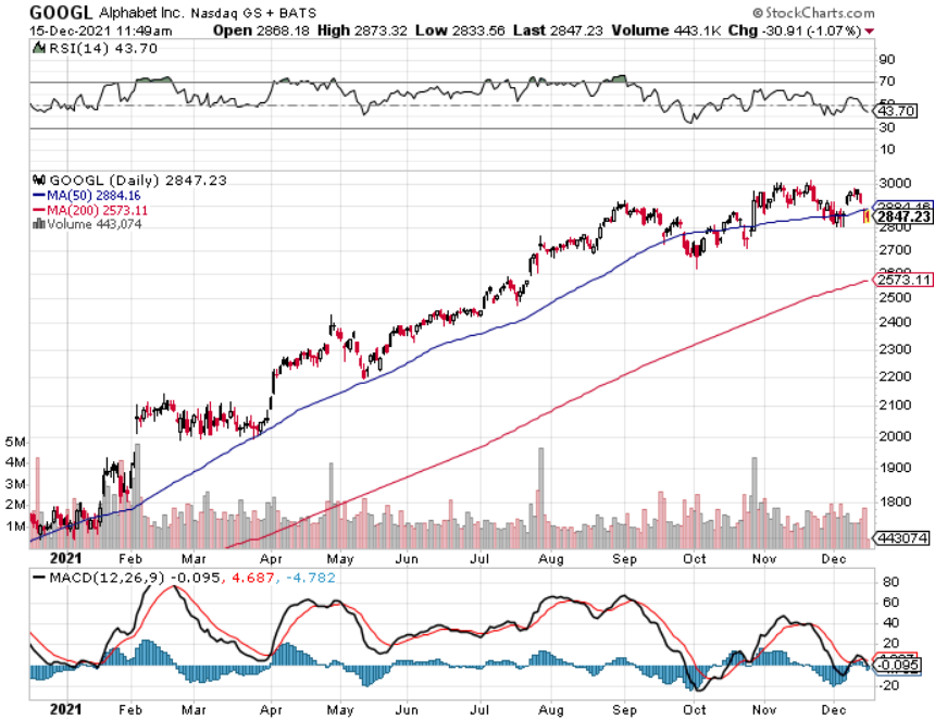

Mad Hedge Technology Letter

December 15, 2021

Fiat Lux

Featured Trade:

(BUY THE DIP IS BEING CHALLENGED)

(PTON), (ROKU), (TSLA), (GOOGL), (FB), (DOCU), (TDOC)

Ominous signals have started to emerge in the short-term patterns of tech stocks over the past few weeks.

We have essentially traded a Santa Claus rally to sell the spiked peaks as inflation numbers have come in way too hot for anyone to handle.

The poor inflation numbers have triggered a cascade of algorithmic selling.

Why is this important?

These stock patterns will offer us clues to how tech stocks will react in a quickly changing backdrop where the Fed is backing away from the cheap money cauldron as fast as it can.

For over ten years now, as tech stocks have bulldozed their way to higher highs and as Apple inches closer to $2.9 trillion in market cap and on its way to $3 trillion, investors have been systematically conditioned to buy the dip.

The Fed is doing its best to recreate a new type of conditioning where the dip is not bought and that is awful for tech stock prognosticators.

This effectively means a large layer of buyers on down days will be stripped away from the tech markets.

Any idiot would understand this means that tech stocks will not go as high as they could if dip buying is conditioned.

The tech market is trying to figure out the new rules of the game and that is resulting in choppy patterns almost in whipsawing fashion.

March 2022 is the new consensus for an interest rate rise which is bad news for tech stocks because pulling forward interest rate rises coincides with higher volatility in the short term.

The Fed could make another interest rate move in the second half of 2022.

This means that anyone dallying in the speculative area of the tech market needs to pull the reigns in immediately.

Stocks like Peloton (PTON), essentially a stationary bike with a tablet pasted on the dashboard, will historically underperform in the new environment.

Another tech stock I love to bully is Pinterest (PINS), by far the worst social media platform I have ever seen, will need to face reality without the Fed punchbowl that was most likely their biggest tailwind.

Tech stocks must now stand on their two feet and that’s scary news for all tech stocks not named Tesla, Facebook, Apple, Amazon, Microsoft, and Google.

After these top 5, the quality dwindles fast and expect a slew of rapid downgrades that will throttle the non-elite software stocks.

Adobe’s stock had its second-worst day of the year on Tuesday, as analysts jumped on the higher rates bandwagon and cited high valuations.

Valuations are now “high” even if these business models are the same as they were a few days ago.

Expect poor guidance from management with earnings growth, free cash flow, and annual revenue downgrades in the pipeline.

Other notable sell-offs this week include shares of cybersecurity companies Zscaler and Cloudflare, which crumbled 7.8% and 9%, respectively.

Zscaler had been up 55% for the year, prior to Tuesday, and has an enterprise value to revenue multiple for 2022 of 39. Cloudflare was up 91% and trades at a multiple of 61.

Tech growth works both ways in which they get the benefit of the doubt in a low-rate environment and vice versa in a tightening environment.

Case in point is a company I really like Roku (ROKU) whose shares are down a hideous 230% since mid-July.

The weakness in the secondary names has been biggest secret untold in tech for quite a while and the confirmation of a tough 2022 was what happened in the first two weeks of December.

And it gets worse when looking at the shelter-at-home darlings of 2020 Teledoc (TDOC) and DocuSign (DOCU) who have been totally neglected this year.

This goes to show that every year is different and as the stock market is levered to the skies, the slightest nudge by the Fed does a lot to wobble the trajectory of tech.

Luckily, tech still has the 6 big tech stocks to rally around and even if the best of the rest must go into hibernation in 2022, we still got guys like Mark Zuckerberg, Tim Cook, Elon Musk powering us through the sludge.