Mad Hedge Technology Letter

December 6, 2021

Fiat Lux

Featured Trade:

(THE HAWKS ARE HERE)

(ROKU), (ZM), (TWLO), (SNAP), (SQ), (MSFT), (CRM), (ADBE)

Mad Hedge Technology Letter

December 6, 2021

Fiat Lux

Featured Trade:

(THE HAWKS ARE HERE)

(ROKU), (ZM), (TWLO), (SNAP), (SQ), (MSFT), (CRM), (ADBE)

Higher inflation is something this tech bull cycle hasn’t dealt with, and it’s starting to rear its ugly head in the form of volatility and spades of it.

The Fed will have to increase interest rates or face runaway inflation that will crash the economy, but increasing interest rates will also make lives harder for tech companies.

As we try to understand the pace of interest hikes, certain tech companies will fare much better in this inflationary environment than others. To deduce the winners from the losers, investors should understand exactly how inflation affects each particular tech company.

Talk has gone from the Fed moving early to raise short-term rates, to the Fed moving even in early spring which in turn is spooking risk markets from cryptocurrencies, the S&P, and the Nasdaq.

Fed Chair Jerome Fed has done a poor job communicating his sudden hawkish tone and the market has had to quickly reprice risk assets because of the surprising nature of the hawkishness.

In the short-term, tech stocks will need some time to digest this new expectation, which I see as quite healthy, but short-term tough to swallow.

Fed Cleveland President Loretta Mester told the media she is “very open” to scaling back the Fed’s asset purchases at a faster pace so it can raise interest rates a couple of times next year if needed so this isn’t just one guy in Powell trying to move the needle.

Clearly, the Fed is moving in unison, and they threaten to become a major force in moving markets which is all we care about.

All that pressure is causing component and labor costs to rise. Companies that don't have enough pricing power to pass those costs on to their customers will likely see their gross and operating margins shrink.

This matters because tech companies offer some of the most generous salaries in the U.S. and substantial increases in pay hurts them the most.

Higher interest rates attract more consumers and businesses to put more money in higher-yield bonds and savings accounts.

There are 3 ways that higher rates are actually a gut punch to tech growth companies.

First, they increase the costs of borrowing incremental capital to expand a business. In more cases than not, tech growth companies rely on borrowed money because their operation is not yet sustainably profitable. That's bad news for high-growth tech companies, which are burning cash with widening losses.

Second, it reduces the long-term estimates for a company's earnings and free cash flow (FCF) growth meaning their underlying stock price is rerated downwards in the anticipation of this new reality.

Loss accruing tech companies commonly suffer an exodus as their underlying shares are repriced to reflect higher costs.

Just this morning we saw Roku (ROKU), Zoom Video Communications (ZM), Snap (SNAP), Twilio (TWLO), Square (SQ) breach 52-week lows.

The breadth of the market has been hollowed and the goalposts have indeed narrowed because of the hawkish tone at the Fed.

Lastly, higher interest rates drive institutional money into fixed income.

They do this largely by taking profits from crypto, tech stocks, or moving their stash on the sidelines then resurfacing the money into “safer” assets that anticipate weakening bond yields at the longer end of the curve.

So I won’t sit here and say sell all and every tech stock, it’s more nuanced than that.

I executed one position in December and that was Microsoft (MSFT) and it got pulled down with the broader market.

More importantly, I didn’t bet the ranch.

Ultimately, we still bask in the ideology that the tech bull market isn’t over yet because it isn’t, but this aggressiveness out of the blue has forced the overall tech market to temporarily rest with growth tech suffering major drawdowns.

In doing that, the ceiling for a Santa Claus rally is somewhat capped to the upside.

The Fed could have waited until January.

Sure, there will still be winners in tech and the odds of these winners are driven firmly behind the biggest and best like Microsoft, Amazon, Google, and Apple.

These are the type of companies that have the pricing power to raise prices and get away with it because consumers will be willing to pay it.

Other potential winners include cloud service giants like Salesforce (CRM) and Adobe (ADBE). These again are top-quality software stocks that can pass up higher enterprise software costs to the firms that can pay for it.

It’s entirely possible that the Fed could end up walking back some of these aggressive stances in the interest-raising process next year.

Don’t fight the Fed and don’t expect tech growth stocks to reverse until we receive more clarity with interest rate policy, if a reverse is triggered, it will play out with Apple, Amazon, Google, and Facebook, and Microsoft leading the way higher.

Mad Hedge Technology Letter

October 4, 2021

Fiat Lux

Featured Trade:

(IT WILL JUST TAKE LONGER)

(ROKU), (TSLA), (FB), (AMZN), (AAPL)

The “Buy the Dip” strategy in tech stocks hasn’t failed — it will just take longer than it used to.

Much of this Nasdaq rally has been represented by the resiliency of large cap tech stocks — every mini dip was bought with a vengeance.

This go-to playbook drove tech shares higher after the March 2020 meltdown.

These past 30 days have really tested that thesis and signals that we, as market participants, have arrived at a crossroads because if the dip isn’t bought soon, we could either fall off a ledge and barrel into a harrowing correction or we could initiate a sideways correction and trade in a fixed range.

It’s hard to ignore the near-term weakness in many of the household names like Apple (AAPL), Amazon (AMZN), and Facebook (FB).

The upper echelon of tech leadership is signaling imminent decelerating growth and tightening financial conditions.

I do believe much of it is in the price, yet it’s cognizant to know there could be meaningful spillover from the Evergrande debt implosion in China into other asset classes.

External events are shaping the narrative around the Nasdaq dip buyers.

It also doesn’t help that a Facebook whistleblower came forward to tell the press about its malpractices and less than ideal tendencies to put profit over safety, but everyone already knew that about Facebook.

What I am surprised about is that investors usually look through the bad Facebook press and prioritize the metrics which hasn’t been happening the past month.

Facebook shares are still waiting to be bought after the dip.

The lack of Facebook shoppers on the pullback is definitely one area of concern because the U.S. government still has done very little to stop Facebook in its stubborn practices.

The U.S. government will not crack down through legislation on social media companies in the short term.

Much of the negative Nasdaq price action in the short term can be attributed to the worries about China taking a machete to its susceptible tech sector and crushing it even more.

Many don’t think the cudgeling is over.

In this scenario, a flight to safety could be in the cards, which would suppress interest rates offering an olive branch for the dip-buyers.

Ultimately, I do believe it’s a matter of time before we get some recovery price action in the leadership tech stocks; but yes, it could take 1-3 weeks.

Much of this second half of the year was consolidating tech shares that overshot themselves last year.

That’s why tech firms like Tesla (TSLA) had almost a zero percent chance of repeating last year’s performance.

Take ad tech stock Roku (ROKU) for instance, shares are down 23% YTD and that doesn’t mean it’s a bad stock.

Hardly so.

When one considers that Roku shares ended 2020 up 300%, then giving back 23% or 50% in 2021 is worth the annoyances.

These stocks can’t go up in a straight line even if they almost feel like they can sometimes.

This all sets up for a brilliant 2022, as many of these high-quality names will finally have gotten through the consolidation phase and will be buttered up to initiate their next leg up in early 2022.

In the broad scheme of things, tech won the pandemic over any other sector, and 2021 is turning into a rest year.

Sometimes one needs to go backwards one step to take the next three forward.

Global Market Comments

August 16, 2021

Fiat Lux9

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MY REVOLUTIONARY NEW STRATEGY,

(SPY), (TLT), (NVDA), (ROKU), (HOOD), (GS), (JPM)

Friday saw the stock market’s lowest volume day of the year, and shares rose almost every day last week to new all-time highs.

The way this usually ends is that the slow grind explodes into a high-volume spike marking an interim market top. That makes new investment now extremely risky.

August usually markets the best buying opportunity of the year with a cataclysmic selloff. Remember the 2010 flash crash, down 1,100 points in two hours? So far, no cigar.

I have tons of people asking me what to buy right now. That is usually another market-topping indicator. I tell them to keep their cash. Cash is a position. A dollar at a market top is worth $10 at a market bottom.

Under an index that is making excruciatingly slow gains are constant sector rotations bring pretty dramatic moves. Play those dramatic moves.

May saw money suddenly shift into tech stocks, with the best, like NVIDIA (NVDA) leaping 56%.

The day the ten-year US Treasury yield (TLT) bottomed at 1.10%, tech went back to sleep. While big tech ground sideways, small tech brought more heart-rending downside moves, such as the 27% plunge in Roku (ROKU).

In the meantime, financials and commodities have moved to the fore. Goldman Sachs (GS) melted up 20% off of blockbuster earnings, while Freeport McMoRan popped 26%, thanks to a Chilean copper union strike.

Let me propose a revolutionary new investment strategy to you. It’s called “buy low, sell high.” Everybody talks about it but actually executes the opposite.

I employ this money-making ploy through my “barbell” strategy, with equal weightings in technology and domestic recovery stocks like financials, industrials, and commodities.

It's quite simple. You just sell whatever has just delivered the most recent spectacular upside gains and roll that money into what has recently become ignored, cheap, and out of favor.

It is a market approach that is really devoid of the thought process.

All eyes will be on Jackson Hole, Wyoming next week, the annual meeting of the world’s top central bankers. That is when we get the next hint about the intentions of the Federal Reserve as to, not "if", but "when" they reduce quantitative easing.

You would think that a 6.5% GDP growth rate and a 5.4% inflation rate would do it, but these days, nothing is certain. A hot jobs report in September would do it for sure.

We may have to wait until then before we see any serious move in stocks and a return of volatility (VIX). In the meantime, catch up on reading your research, pay your bills, and work on your golf swing.

Bitcoin staged a recovery for the ages, rallying 55% in two weeks. The “battle of $30,000” is over and the cryptocurrency won. It really is becoming too big to fail. I might have to do something about that.

July Inflation Read at a hot 5.4%, but core inflation showed a small decline. In June, used car prices accounted for a third of the total price increases, but last month, it was zero. So far, there is no move in rents, but it’s coming. All Fed eyes will remain laser-focused on this number.

Taper talk is back! With the ballistic increase in the July Nonfarm Payroll report and the 2 ½ point dive in the bond market. I think the top is in for finds and the bottom for long term rates. It means tech stocks will lag from now, while interest rate sensitives like banks, brokers, and fund managers will lead. Buy (JPM), (MS), (V), and (GS) on dips.

US Budget Deficit hits a record $302 Billion in July. Covid benefits are remaining high, while tax revenues are lagging YOY. Keep selling those (TLT) rallies. The generational crash may have just begun.

Fed’s Rosengren Says QE is not creating jobs, causing bonds to drop a full point in the after-market. No kidding. I have been arguing that our nation’s central bank has been pushing on a string all year. Atlanta Fed governor Bostic couldn’t agree more. Time for more action than words?

Gold Hits four-month low, breaking key support. Bitcoin is clearly stealing its thunder, which has risen by 50% in two weeks. If you’re considering gold, go take a long nap first.

Oil dives on delta surge, off $9, or 12% in a week, the lowest in three weeks. Delta is now rampaging throughout China, the world’s largest consumer of Texas tea., putting $63 in play.

Weekly Jobless Claims hit 375,000, down 12,000 on the week. Moving in the right direction but still incredibly high.

Berkshire Hathaway announces solid earnings, but scales back share buybacks at these elevated levels. Oracle of Omaha Warren Buffett bought back $6 billion of his own stock in Q2, leaving him with a staggering $144 billion in cash. Almost no stocks meet Buffett’s value standards in the current environment. Buy (BRKB) on dips. It’s a high-class problem to have.

Ed Yardeni is bullish, along with David Kostin, and is the only manager who comes close to my own $475 target for the (SPY) by the end of the year. The U.S. economy will be in nominal terms around 8% higher this year than pre-pandemic 2019. Sales for the S&P 500 companies will be 15% higher and earnings will be 34% higher. That is a representation of the operating leverage that exists in so many companies. The Roaring Twenties lives!

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +4.86% in July. My 2021 year-to-date performance appreciated to 74.07%. The Dow Average was up 16.00% so far in 2021.

I stuck with three positions, a long in (JPM) and a double short in the (TLT), all of which expire on Friday. My double short in the (SPY) punched me in the nose, forcing me to stop out for losses when I hit the lowest strike prices.

I then jumped into a very deep in-the-money call spread in Robinhood (HOOD) made possible only by the stock’s astronomically high volatility. Its 44% drop helped too. I also added a third short in the bond market.

That leaves me 30% in cash. I’m keeping positions small as long as we are at extreme overbought conditions.

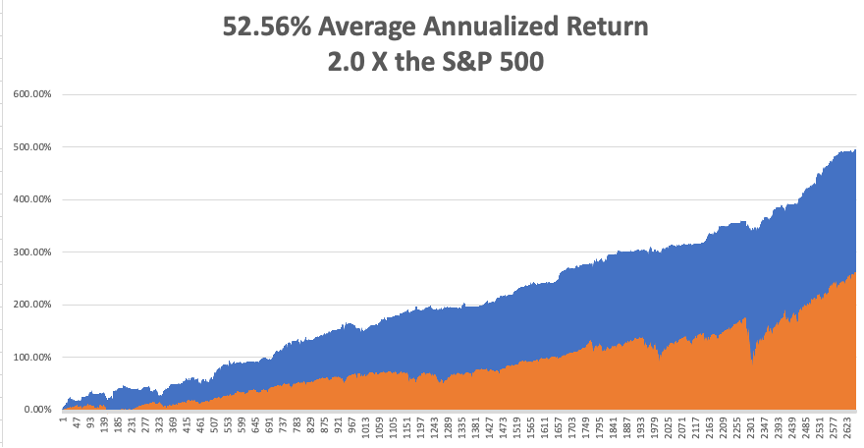

That brings my 11-year total return to 496.62%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 12.56%, easily the highest in the industry.

My trailing one-year return retreated to positively eye-popping 106.69%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 36.7 million and rising quickly and deaths topping 622,000, which you can find here at https://coronavirus.jhu.edu.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 16 at 7:00 AM, the New York Empire State Manufacturing Index is out.

On Tuesday, August 17 at 7:30 AM, US Retail Sales for July are published.

On Wednesday, August 18 at 5:30 AM, the Housing Starts for July are printed. At 2:00 PM, the minutes from the last FOMC are released.

On Thursday, August 19 at 8:30 AM, Weekly Jobless Claims are announced. Square (SQ) reports.

On Friday, August 20 at 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, upon graduation from high school in 1970, I received a plethora of scholarships, one of which was for the then astronomical sum of $300 in cash from the Arc Foundation.

By age 18, I had hitchhiked in every country in Europe and North Africa, more than 50. The frozen wasteland of the North and the Land of Jack London beckoned.

After all, it was only 4,000 miles away. How hard could it be? Besides, oil had just been discovered on the North Slope and there were stories of abundant high-paying jobs.

I started hitching to the Northwest, using my grandfather’s 1892 30-40 Krag & Jorgenson rifle to prop up my pack and keeping a Smith & Wesson .38 revolver in my coat pocket. Hitchhikers with firearms were common in those days and they always got rides. Drivers wanted the extra protection.

No trouble crossing the Canadian border either. I was just another hunter.

The Alcan Highway started in Dawson Creek, British Columbia, and was built by an all-black construction crew during the summer of 1942 to prevent the Japanese from invading Alaska. It had not yet been paved and was considered the great driving challenge in North America.

The rain started almost immediately. The legendary size of the mosquitoes turned out to be true. Sometimes, it took a day to catch a ride. But the scenery was magnificent and pristine.

At one point, a Grizzley bear approached me. I let loose a shot over his head at 100 yards and he just turned around and lumbered away. It was too beautiful to kill.

I passed through historic Dawson City in the Yukon, the terminus of the 1898 Gold Rush. There, abandoned steamboats lie rotting away on the banks, being reclaimed by nature. The movie theater was closed but years later was found to have hundreds of rare turn-of-the-century nitrate movie prints frozen in the basement, a true gold mine.

Eventually, I got a ride with a family returning to Anchorage hauling a big RV. I started out in the back of the truck in the rain, but when I came down with pneumonia, they were kind enough to let me move inside. Their kids sang “Raindrops keep falling on my head” the entire way, driving me nuts. In Anchorage, they allowed me to camp out in their garage.

Once in Alaska, there were no jobs. The permits required to start the big pipeline project wouldn’t be granted for four more years. There were 10,000 unemployed.

The big event that year was the opening of the first McDonald’s in Alaska. To promote the event, the company said they would drop dollar bills from a helicopter. Thousands of homesick showed up and a riot broke out, causing the stand to burn down. It was rumored their burgers were made of moose meat anyway.

I made it all the way to Fairbanks to catch my first sighting of the wispy green contrails of the northern lights, impressive indeed. Then began the long trip back.

I lucked out catching an Alaska Airlines promotional truck headed for Seattle. That got me free ferry rides through the inside passage. The driver wanted the extra protection as well. The gaudy, polished tourist destinations of today were back then pretty rough ports inhabited by tough, deeply tanned commercial fishermen and loggers who were heavy drinkers always short of money. Alcohol features large in the history of Alaska.

From Seattle, it was just a quick 24-hour hop down to LA. I still treasure this trip. The Alaska of 1970 no longer exists, as it is now overrun with summer tourists. It now has more than one McDonald’s. And with runaway global warming, the climate is starting to resemble that of California than the polar experience it once was.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Alcan Highway Midpoint

The Alaska-Yukon Border in 1970

Mad Hedge Technology Letter

June 18, 2021

Fiat Lux

Featured Trade:

(A CROWN JEWEL OF AD TECH)

(ROKU)

If Apple is a $2.2 trillion company, then Roku growing from today’s $47 billion to $100 billion is highly likely.

I would agree that the digital migration and transformation are mainly funneled into the profit models of the big tech players, but tech companies created from the ilk of Roku aren’t shabby either.

The TV streaming platform Roku has a 3-year revenue growth rate of 54% showing they are a true growth firm no matter what metric you want to measure them against.

The pandemic supercharged their business with revenue growth rates soaring to a record 79% year over year to $574.2 million.

Roku users streamed 18.3 billion hours in the quarter, an increase of 49% year over year. Platform monetization continued to increase with average revenue per use (ARPU) of $32.14 on a trailing 12-month basis, up 32% year over year.

This was in large part because they added 2.4 million incremental active accounts in Q1, ending the quarter with 53.6 million.

The success can also be attributed to a secular shift in the advertising industry.

Historically, the biggest impediment or headwind to Roku’s ad business growth has been TV buyers' buying patterns.

Buyers traditionally tend to prefer traditional linear TV versus a bold new phenomenon-like streaming.

Certainly, there's a gap there as viewers move over to streaming versus the ad dollars.

That gap is now closing and there’s still room to expand.

For example, according to Nielsen, in March ratings, linear TV ratings for adults 18 to 24 were down 22%. Q1 TV ad spending was down 11%, according to MediaRadar. Meanwhile, Roku was able to double monetized video ad impressions on the platform.

Ad spending by major agency holding companies with Roku more than doubled. We saw strength really up and down Roku’s ad business. An area of strength is inevitably the entertainment side of Roku’s ad business and it’s to the point where every major direct-to-consumer service has launched.

Those launches have created great opportunities for Roku to partner with major service providers, HBO Max, Discovery Plus, and the who’s who to really drive the adoption of these services, and these partners are leaning in closely and investing with Roku to promote their services to Roku’s users.

Another example is Home Chef, a performance-based advertiser, who invested with Roku and saw 2.4 times return on ad spend and then came back and significantly invested more with Roku after the preliminary success.

Similar case studies pop up like that left and right.

What we are seeing now is the reallocation of TV budgets, as well as digital and social budgets toward streaming and it is here to stay.

As the sales growth rate has gone from the mid 50% to the high 70%, Roku forecasts the same type of outperformance which calls for robust growth with total net revenue of $615 million at the midpoint, up 73% year over year; and total gross profit of $300 million at the midpoint, up 104% year over year, implying an overall gross margin of approximately 49%.

As streaming becomes the dominant source of entertainment around the globe, advertisers are moving much of their traditional TV budgets to over-the-top media services (OTT). The need for programmatic, measured, and scalable advertising opportunities across devices is more important than ever.

This bodes well for continuing to be able to command premium cost per mille (CPMs).

Advertisers will increasingly be looking not just at the top-line CPM that they buy the media at, but the effective cost, cost per site visit, cost per product purchase.

And what that means long term is that, unlike traditional TV, streaming CPMs aren't just going to be sort of one price rules them all type scenario, but rather a whole spectrum of prices where the pricing into the auction is ultimately dictated by the tactic that the advertiser is executing on and the outcome that they're trying to drive.

As Roku delivers enhanced tools to navigate this type of auction and pricing and allow effective strategies to flourish, they will benefit from all of this.

One note investors need to take heed of is that even though Roku anticipates revenue growth rates in the second half of 2021 will be robust, they will be “at a slower rate than the first half.”

The reason they give for this is because they expect the “outperformance of content distribution to normalize in Q2 and in the back half of the year.”

If we look at Roku’s stock chart, Roku has come back drastically from $470 in mid-February to $350 today as the market had to absorb perceived higher interest rate fears and accelerating inflation.

There was a swift rotation out of high growth names during this period causing a rapid pullback in Roku.

Theoretically, the upside is capped in 2021 in the second half because growth rates will moderate, and the stock will be reliant on a Nasdaq lunge forward as in index to carry them back to the highs of February.

The low-hanging fruit has been harvested because the premium entertainment deliverers have already signed up for the Roku platform.

Thus, don’t expect any paradigm-shifting announcement in 2021 but expect solid earnings and higher profitability.

I would put new capital to work around the support levels of $315 or $300.

Roku is still performing at growth rates in the high 70% year-over-year and has been a profitable company since Q3 2020.

These two trends will stick and if you remember in 2018, I recommended this stock at $26 and still love it at around $300.

Global Market Comments

May 3, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE STAIR STEP MARKET IS HERE),

(SPY), (TLT), (MRK), (EL), (UNP), (PFE), (GM), (PYPL), (REGN), (ROKU)

The last six months have been the most successful in my 52 years of trading. The only thing that comes close were the last six months of 1989 when the Tokyo market went straight up and hit a 30-year peak.

Everything I tried worked. The trades I only thought about worked. And the 50 trade alerts I abandoned on the floor because the market moved too fast worked as well. That’s how I missed Facebook (FB) and Amazon (AMZN).

It is believed that if you set a team of monkeys loose, randomly hitting keys on typewriters, they would eventually produce Romeo and Juliet. In this market, they have been producing the entire works of Shakespeare on a daily basis.

It has been that good.

President Biden has been looking pretty good too, having presided over the best starting three-month stock market results since 1933. That is no accident. The massive stimulus and the remaking of the country he has proposed have Franklin Roosevelt’s New Deal-inspired handwriting all over them.

Yet, traders have been puzzled, perplexed, and befuddled by companies that announce the best earnings in history only to see their shares sell-off dramatically. However, the market has shown its hand.

We’ve now seen three quarters of tremendously improving earnings and stock dives. It’s a 12-week cycle that keeps repeating. Shares rally hard for six weeks into earnings, peak, and then go nowhere for six weeks. Wash, rinse, repeat, then go to new all-time highs.

But stocks don’t fall enough to justify getting out and back in again, especially on an after-tax basis. Therefore, it’s just best to lie back and think of England while your stocks do nothing.

If my analysis is correct, then it's best to imagine the rolling green hills of Kent and Wiltshire, the friendly neighborhood pub, and Westminster Cathedral until June. If you want to get aggressive, you might even sell short an out-of-the-money call option or two to protect your portfolio.

The Fed leaves rates unchanged, indicating that the economy is improving, but that interest rates are going nowhere. No surprise here. Jay Powell is still going for maximum dove. Strong Biden policy support and the rollout of the vaccine are major positives. $120 billion in bond buying continues. The Fed will keep interest rates at zero until the US economy reaches maximum employment by adding 8.4 million jobs. That could be a long wait as I suspect those jobs have already been destroyed by technology. Stocks popped on the news. The Bull lives!

Q1 GDP eExploded by 6.4%, and upward revisions are to come. That explains the 25% gain in the stock market during the first three months of the Biden administration, the best in 75 years. Coming quarters will show even stronger growth as the economy shakes off the pandemic and massive government spending kicks in. We will recover 2019 GDP peaks in the next quarter. Virtually, all economic data points will set records for the rest of 2021. Buy everything on dips.

Weekly Jobless Claims dive again to 553,000, a new post-pandemic low. One of a never-ending series of perfect data. It augurs well for next week’s April Nonfarm Payroll Report.

New Home Sales up a ballistic 20.7% YOY in March on the basis of a signed contract. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

Pending Home Sales fell 1.9%, far below expectations, but are still up 23% YOY. Higher prices and record low supply are the problems. The Midwest leads.

Amazon sales soar by 44% in Q1, producing some of the best earnings in American corporate history. Jeff is expecting sales to reach a staggering $110-$116 billion in Q2. That’s why he hired 500,000 last year, the most of any company since WWII. Prime subscribers have grown to 200 million, including me. Ad revenues jumped an eye-popping 77%. The shares of the huge pandemic winner leaped $140 on the news. It’s all another step toward my $5,000 target.

Tesla revenues explode for 74%, and earnings soar to an eye-popping $438 million. Sales are to double or more in 2021 and are up 104% YOY. Q1 is usually the slowest quarter of the year for the auto industry. Global demand is increasing far beyond production levels. It is ducking around chip shortages by designing in a new generation that is currently available. Production of high-end X and S Models has ceased to allow more focus on the profitable Y and 3 Models. Those will resume in Q3. The shares were unchanged on the news. Keep buying (TSLA) on dips. It’s headed for $10,000.

Copper hits new 10-year high, lighting a fire under Freeport McMoRan (FCX) which we are long. We still are in the early innings of a major commodity supercycle. The green revolution goes nowhere without increasing copper supplies tenfold. A copper shock is imminent.

US Capital Spending leaps ahead, up 0.9% in March and up 10.4% YOY. The stimulus spending is working. All is well in manufacturing land, which is 12% of the US economy.

Case-Shiller explodes to the upside, the National Home Prices Index soaring 12% in February. That’s the best report in 15 years. Phoenix (+17.4), San Diego (+17.0%), and Seattle (15.4%) continue to be the big winners. This was in the face of a 50-basis point jump in home mortgage interest rates during the month. The rush to buy homes is pulling forward future demand. The perfect storm continues.

The Fed could start tapering its $120 billion a month in bond purchases as early as October, believes the Blackrock’s (BLK) Rick Rieder. When it does, expect the sushi to hit the bond market. Keep piling on those bond shorts, as I have been doing monthly, and am currently running a triple short position. Keep selling short the (TLT) on every opportunity.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 13.54% gain during April on the heels of a spectacular 20.60% profit in March.

I used the post-earnings dip in Microsoft (MSFT) to add a new position there. I also picked up some Delta Airlines (DAL) taking advantage of a pullback there.

That leaves me 100% invested, as I have been for the last six months.

My 2021 year-to-date performance soared to 57.63%. The Dow Average is up 11.8% so far in 2021.

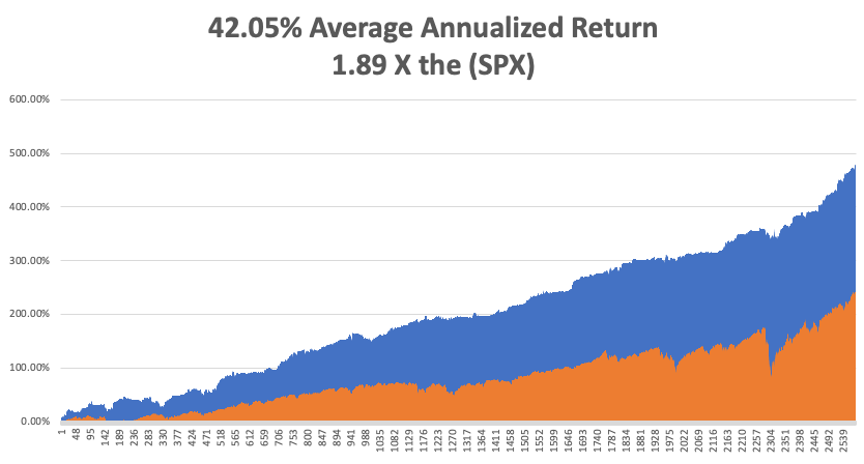

That brings my 11-year total return to 480.18%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.05%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 133.91%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9 million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, May 3, at 10:00 AM, the US ISM Manufacturing Index is published. Merck (MRK) and Estee Lauder (EL) report.

On Tuesday, May 4, at 8:00 AM, total US Vehicle Sales for April are out. Union Pacific (UNP) and Pfizer (PFE) report.

On Wednesday, May 5 at 2:00 PM, the ADP Private Employment Report is released. General Motors (GM) and PayPal (PYPL) report.

On Thursday, May 6 at 8:30 AM, the Weekly Jobless Claims are printed. Regeneron (REGN) and Roku (ROKU) report.

On Friday, May 7 at 8:30 AM, we learn the all-important April Nonfarm Payroll Report. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I received calls from six readers last week saying I remind them of Earnest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens, I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete works.

I visited his homes in Key West and Ketchum Idaho. His Cuban residence is high on my list, now that Castro is gone.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Earnest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was still being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are glued to the tables.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Life is a Bed of Roses Right Now