(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:04:402021-04-26 10:44:52April 26, 2021

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

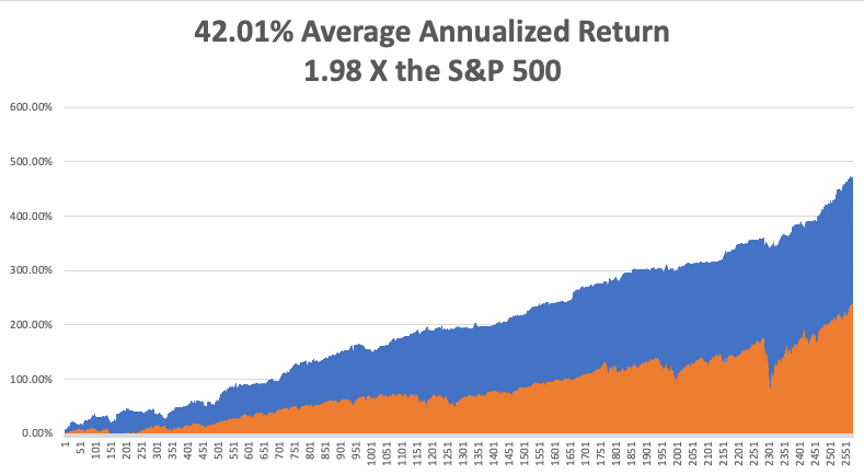

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/g-bebe-e1647874970894.png295450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:02:432021-04-26 10:45:23The Market Outlook for the Week Ahead, or The Correction is Over

Monopolies. In any industry, they’re typically called rule breakers.

For healthcare, these are rule-making stocks that ultimately rise to dominance that they eventually win government-sanctioned monopolies and establish massive networks.

For biotechnology and healthcare investors who like to err on the side of caution but still want to take a dip on monopoly-like players, one stock stands out: Teladoc Health (TDOC).

Teladoc, which currently has a market capitalization of $30 billion, is one of those groundbreaking companies that use technology to disrupt the way we live.

The company’s potential is actually getting compared to the likes of other tech movers such as (SQ), Shopify (SHOP), Roku (ROKU), and Tesla (TSLA).

So far, Teladoc stock has gone up 144% over the past 12 months.

On a year-over-year basis, the total number of visits for Teladoc more than doubled from 4.14 million to reach a whopping 10.59 million. Even the international visits rose by 71%.

As expected, the COVID-19 pandemic served as a major boon to its already thriving business.

Although it wasn’t as popular at the time, the company’s operating model offered a myriad of benefits for the healthcare industry.

For one, telehealth visits are way more convenient for the patients. Since the visits won’t take as much time and effort from their end, the patients would be more motivated to regularly check in with their doctors.

In turn, the doctors would be able to offer higher-quality care since the cooperation of the patients means they can also monitor the symptoms and progress better.

Best of all, the patients are typically billed at cheaper rates compared to office visits.

I think the last one makes Teladoc an attractive winner in the eyes of practically all health insurers.

Teladoc is the biggest telehealth services provider in the United States, and one of the major steps that the company took to cement its reputation as a virtual health leader is its splashy $18.5 billion merger with Livongo in 2020.

If you haven’t heard of Livongo, this company was growing incredibly faster than Teladoc even before the merger.

Basically, Livongo collects copious amounts of information from patients. Using artificial intelligence, the company then sends personalized tips and reminders to their enrolled members with the goal to improve their overall quality of life.

Most of the patients suffer from chronic conditions, which means they would require regular nudges to ensure that they take the proper medications on time.

For example, some of Livongo’s users have diabetes. The company monitors them via wireless glucose meters, guiding the users to follow a positive lifestyle when their blood sugars begin to spike.

At the time of the merger, Livongo has already secured over 500,000 enrolled members for its diabetes platform.

This is impressive as it represents roughly 2% of the entire diabetes pool in the United States.

Aside from diabetes, Livongo has also been working on other chronic conditions like hypertension and weight management.

Considering that hypertension accounts for 7.6 million deaths per year worldwide and the extensive list of health problems associated with obesity, such as coronary heart disease and end-stage renal disease, I think Livongo has developed a highly sustainable business model that’s perfect for the “new normal.”

More importantly, the combination of Livongo and Teladoc will now allow the two companies to cross-sell their services to their users.

As for those who think that Teladoc is only a pandemic play, the company didn’t really need the pandemic for its business model to succeed.

Prior to COVID-19, its sales have been growing by an average of 75% per annum since 2013.

With its merger with Livongo, I think Teladoc has developed a stronger all-weather model for growth.

Teladoc is a rule maker and a first-mover, with the company moving the multi-trillion dollar healthcare industry to the internet.

At this point, it is the dominant name in the arena and the undisputed leader in telehealth. With everything it has to offer, I believe Teladoc is a long-term investing opportunity and it would be a good idea to buy on the dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-01 15:00:252021-04-07 16:31:12A Rule Maker in Healthcare

I have prudently ignored investing in tech stocks for the past seven months, and justly so.

Tech has been peddling hard on the business front, but the shares have been going nowhere in a hurry. Many of the leading names are down 30%-50% from their peak prices.

As a result, they are rapidly approaching value territory. When growth becomes cheap and value gets expensive, it’s time to shift from one side of the barbell strategy to the other.

I’m not saying that tech stocks have bottomed. But we are getting close, perhaps within 10% in the best names. It’s now time to lists of stocks to pounce on when the big turn inevitably comes.

Fortunately, Arthur Henry’s Mad Hedge Technology Letter has already done that job for you. See below his list of recommendations.

By the way, if you want to subscribe to Arthur’s groundbreaking, cutting-edge service, please click here.

It’s the best read on technology investing in the entire market.

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Here are the names of five of the best stocks to slip into your portfolio in no particular order when the next downside whoosh occurs.

Remember, tech ALWAYS comes back.

Apple

Steve Job’s creation is weathering the gale-fore storm quite well. Apple has been on a tear reconfirming its smooth pivot to software services tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $200 billion in shares by the end of 2021. Get into this stock while you can as entry points are few and far between.

Oh, and their 5G phones are selling like hotcakes. Some one billion need to be replaced to bring consumers into the new high-speed 5G world.

Amazon (AMZN)

This is the best company in America hands down and commands 5% of total American retail sales or 49% of American e-commerce sales. The pandemic has vastly accelerated the growth of their business.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then oozing innovation and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2021 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter and that is a good thing.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox-related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business.

Microsoft Azure grew 87% YOY last quarter. The previous quarter saw Azure rocket by 98%. Shares are cheaper than Amazon and almost as potent.

Square (SQ)

CEO Jack Dorsey is doing everything right at this fin-tech company blazing a trail right to the doorsteps of the traditional banks.

The various businesses they have on offer make me think of Amazon’s portfolio because of the supreme diversity. The Cash App is a peer-to-peer money transfer program that cohabits with a bitcoin investing function on the same smartphone app.

Square has targeted the smaller businesses first and is a godsend for these entrepreneurs who lack immense capital to create a financial and payment infrastructure. Not only do they provide the physical payment systems for restaurant chains, but they also offer payroll services and other small loans.

The pipeline of innovation is strong with upper management mentioning they are considering stock trading products and other bank-like products. Wall Street bigwigs must be shaking in their boots.

Roku (ROKU)

Benefitting from the broad-based migration from cable tv to online steaming and cord-cutting, Roku is perfectly placed to delectably harvest the spoils.

This uber-growth company offers an over-the-top (OTT) streaming platform along with the necessary hardware and picks up revenue by selling digital ads.

Founder and CEO Anthony Woods owns 21 million shares of his brainchild and insistently notes that he has no interest in selling his company to a Netflix or Apple.

Viewers are reaffirming the obsession with on-demand online streaming content with hours streamed on the platform increasing 58% to 5.5 billion.

The Roku platform can be bought for just $30 and is easy to set-up. Roku enjoys the lead in the over-the-top (OTT) streaming device industry controlling 37% of the market share leading Amazon’s Fire Stick at 28%.

The runway is long as (OTT) boxes nestle cozily in only 40% of American homes with broadband, up from a paltry 6% in 2010.

They are consistently absent from the backbiting and jawboning the FANGs consistently find themselves in partly because they do not create original content and they are not an offshoot from a larger parent tech firm.

This growth stock experiences the same type of volatility as Square.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/02/John-thomas-air-niugini.png410525Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-24 11:02:022021-03-24 11:35:56Five Tech Stocks to Buy at the Market Bottom

Invitae (NVTA) is one of the biggest, albeit erratic, movers in 2020, but only a handful of investors know about the stock.

In March 2020, the stock was trading at $7.43 per share only to shoot to a whopping $61 by mid-December.

A year since then, Invitae stock sits somewhere at $40—a price that could go right up again in the months to come.

Despite the volatility, Invitae continues to generate excitement among its investors.

In fact, Invitae, which has $7.6 billion in market capitalization, is grouped in with bigger healthcare and biotechnology companies like CRISPR Therapeutics (CRSP), valued at $9.36 billion, and Teladoc Health (TDOC), valued at $28.7 billion.

Its potential is even said to match the likes of up-and-coming tech stocks such as Roku (ROKU), Square (SQ), and Shopify (SHOP), which have market capitalizations of $45.7 billion, $103.07 billion, and $134.6 billion, respectively.

Given its growth in the past months and its impressive 226.8% three-year revenue increase, the projections for Invitae look well-grounded.

In fact, I think it’s reasonable to say that Invitae could be the Tesla (TSLA) of the genetic testing industry.

The genetic testing market is estimated to be worth over $21 billion by 2027, growing at a compound annual growth rate of 10% until then.

In 2020, Invitae reported a 29% year-over-year increase in revenue at $279.6 million.

The company also saw a rise in its testing volume by roughly 41% to reach 659,000 billable units—this, despite the headwinds brought about by the COVID-19 pandemic, when the demand for genetic tests took a back seat to make way for COVID-19 diagnostic and other related medical concerns.

Although some of the tests offered by Invitae are covered by insurance carriers, those that are not covered can be availed for as low as $99 for services like noninvasive prenatal screening and $250 for diagnostic, carrier, or proactive testing.

To put things in perspective, people nowadays are more than willing to shell out at least $100 to discover their ancestry, which in most cases is something they already have an idea about.

So, why would these people be reluctant to spend a bit more than $100 to check if they have to take particular precautions to keep themselves safe from diabetes or heart disease?

In the future, Invitae is well-positioned to offer high-quality genetic tests at more affordable prices as well as cater to higher volumes.

One of the most notable moves by Invitae so far is buying ArcherDX for $1.4 billion in cash and stock in October 2020.

This is a telling move for Invitae in terms of its plans for the future.

ArcherDX is another genetic testing company, which specializes in oncology.\

Specifically, ArcherDX focuses on personalized cancer monitoring as well as liquid and tissue biopsy analysis.

Simply put, ArcherDX specializes in developing tests that determine the most suitable drugs to use for cancer treatments.

To date, there’s already a growing number of competition in the genetic testing market, making Invitae’s acquisition of ArcherDX is a smart move.

Most of them are bigger companies like Roche (RHHBY) with a market cap of $269.57 billion, Illumina (ILMN) with $58.28 billion, Abbott (ABT) with $205.28 billion, and Quest Diagnostics (DGX) $15.6 billion.

Invitae, which only has a market capitalization of $7.6 billion, is considered as one of the minor players.

With the addition of ArcherDX in its portfolio, Invitae’s growth could be fast-tracked as the combined companies could ramp up sales on top of queuing additional genetic tests in their current lineup.

Invitae’s shares have jumped by almost 100% in 2020 but saw an over 25% fall last month. Although it has yet to turn a profit since its creation in 2013, Invitae remains an attractive investment thanks to its top-line growth.

Digging into their numbers, Invitae has actually managed to cut down on its cash burn by roughly $20 million from the first quarter of 2020 through the last quarter, excluding the ArcherDX deal.

That’s a notable improvement for a company and indicative of its capacity to veer towards the right direction.

Invitae has a very strong cash position at the moment, with a massive equity offering just last January. Right now, the company’s stockpile is nearly $800 million, which could carry them for quite some time.

Looking at its path of profitability, the company is also projected to be on track for a 50% to 60% growth in the next few years.

For 2021, Invitae is looking at over $450 million in annual revenue, which is 61% higher than 2020.

At this point, Invitae offers an attractive purchasing opportunity for those who want to get in on the industry before it explodes.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-11 13:00:152021-03-15 19:22:48The Tesla Stock of Genetic Testing

The electric vehicle market is blossoming into a mega tech growth industry and we are just entering the sweet spot of it.

Just take a look at the variety of options now on the market.

China has been doing its best to catch up to the standard bearer Tesla (TSLA) with generous government subsidies spawning a tidal wave of new investment.

A Chinese company partnering with GM has been able to introduce an electric vehicle (EV) selling in China for $4,500 and is now miraculously outselling Tesla's posher cars.

The compact car is proving a home run for state-owned SAIC Motor, China's top automaker.

The Hong Guang Mini EV is being built as part of a joint venture with US car giant General Motors (GM) and yes, this is the same joint venture where Chinese companies “borrow” the proprietary intellectual property.

This is just another example of the breadth of options out there and the insatiable popularity of the mode of transport in a world of climate change and the broad-based pivot to sustainable ecological business.

According to Fortune Business Insights, the global electric vehicle market will be worth $985.72 billion by 2027, growing at a compound annual growth rate (CAGR) of 17.4% over the next six years.

Electric vehicle sales are poised to surpass the highest level on record in 2021.

Edmunds data shows that EV sales made up 1.9% of retail sales in the United States in 2020 and that number is expected to surge to 2.5% this year.

Edmunds analysts anticipate that 30 EVs from 21 brands will become available for sale this year, compared to 17 vehicles from 12 brands in 2020.

Notably, this will be the first year that these offerings represent all three major vehicle categories: Consumers will have the choice among 11 cars, 13 SUVs, and six trucks in 2021, whereas only 10 cars and seven SUVs were available last year.

As it is true that compact vehicles will rule the road in China, Americans have a love affair with trucks and SUVs, to the detriment of compact cars.

Each EV manufacturing decision will need to have localization in mind.

This isn’t to say that China can produce EVs at the quality of Tesla, but it shows that alternative models of EV battery capabilities, range, and performance also have a strong place in the consumer world.

This isn’t just a Tesla world with everyone living in it.

The Chinese government has bet the ranch on EVs as it reduces the smog-induced megacity pollution that has been public enemy one, two, and three.

Clean air is a sensitive topic among Chinese urban dwellers.

The Chinese communist party offers EV license plates for free and they are guaranteed. In many cities, it can take years to receive a license plate for a petrol engine through various lottery systems.

The Tesla Model 3 sells for about $39,000 in China factoring in price cuts due to its local production.

So what does this mean for the short-term future of EVs?

First, they are showing growth numbers that almost every cloud executive would love to put on the radar for many tech investors.

Second, Elon Musk’s Tesla and The Hong Guang Mini EV are primed to be flooded in all markets overseas creating an ironic situation where Europeans are buying a cheaper EV from China instead of the homegrown stalwarts of BMW, Audi, and Mercedes.

China has been adamant that they want to secure higher manufacturing ground and this phenomenon is coming hard and fast for the Europeans and everyone else who have continuously kowtowed to Chinese business.

Reports have linked these Chinese mini EVs to a Latvian automaker who could sell an iteration of the car in Europe. However, the price is likely to be twice as high due to European environmental requirements.

This also paves the way for Tesla to eventually roll out a compact car to sell in the German market and the entire European Union.

Tesla Gigafactory Berlin-Brandenburg is a European manufacturing plant under construction in Grünheide, Germany and the campus is 20 miles south-east of central Berlin on the Berlin–Wrocław railway.

Of course, at first, they will produce the American models of the Tesla, but my guess after that is they will start right-sizing their models for the local market in all shapes and sizes.

This would be the new contact point in terms of funneling Tesla products into Europe and instead of SUV/Pick-up trucks, they will create something more akin to a Fiat-sized car to suit the European market.

Although the EV market is still in its infancy, Tesla not only has first-mover advantage and the best of breed stamp of quality, but has the manufacturing prowess in terms of battery and knowhow that others don’t.

That being said, beneath the robustness of Tesla, a lot of movement is taking place as we speak and we still do not have the 2nd or 3rd Teslas emerging from the pack and we will gain more insight into who that is in the next few years.

For the next 10X bagger, potential start-ups that could take the EV market by storm is where readers should put their money, but this comes with great risk.

But I’ve been pretty good at guessing 10 baggers with recommendations such as Roku (ROKU) and Palantir (PLTR) on the way to achieve 10 bagger status.

As many understood from the first pandemic year of 2020, just throw money into Tesla and watch it explode higher.

Tesla is still an incredibly bullish tech story and I wouldn’t want to get in the way of its up moves.

The moment Tesla’s quality starts to erode and Chinese low-quality EVs catch up, that would be the cue to take profits on Tesla, but that day is long off.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-26 13:02:062021-03-04 13:21:50EV Industry Goes from Hot to Hotter

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.