To be honest, I was worried when it dipped all the way down to $25 last year because it was a stock that was prime for liftoff.

Liftoff has happened but a little later than I first surmised.

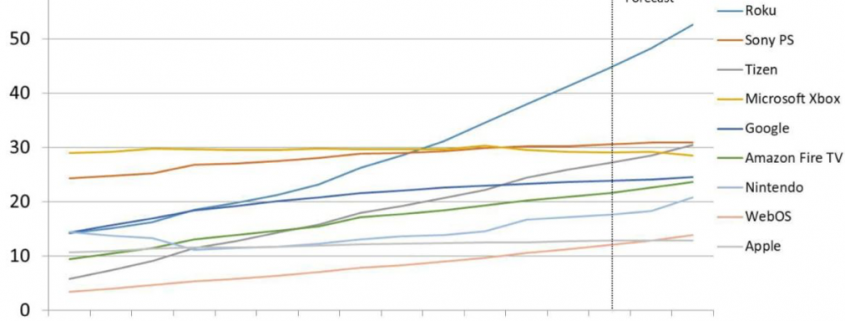

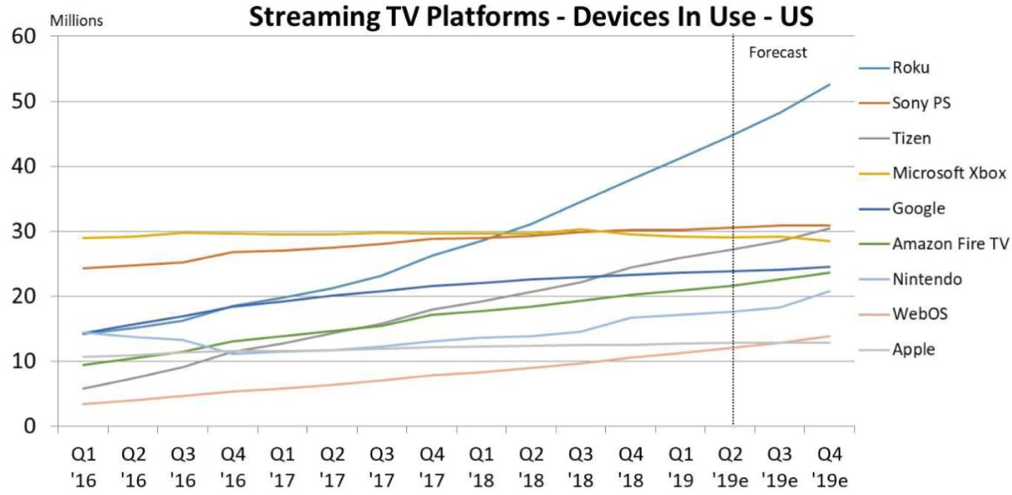

Roku had a blowout quarter crushing estimates with expanding their pie 59% year-over-year to $250 million scorching consensus estimates of $224 million.

The outperformance doesn’t stop there with the company rapidly adding users to 30.5 million active users during the quarter, up 39% year-over-year.

The monetization side showed the same outperformance with average revenue per user (ARPU) up to $21.06, up $2.00 year-over-year.

For all the doubters out there, who dismissed the potential of Roku because they weren’t part of an Amazon, Google, Facebook, or Apple group, then you were wrong.

What we have seen in the past year is the potential transforming in real-time into high octane outperformance.

The x-factor that put the company’s business model over the edge was the “onslaught” of new streaming assets coming online this year and in 2020 from Disney, NBCUniversal, and HBO.

Recent surveys suggest that Amazon’s Fire TVs haven’t been able to keep up with Roku.

And as Disney and NBC roll out gleaming new streaming assets, Roku will be able to do what is does best – sell digital ads.

Roku being independent doesn’t care who streams what because selling ads can be sold on any streaming program.

This makes me believe that Roku is in a better position not being a Fang because of a lack of conflict of interest.

For example, Google and Amazon have skirmished about different crossover partnerships such as YouTube on the Amazon Kindle and so on.

They plainly don’t want to help each other

Part of the DNA of these big tech companies is bringing each other down.

In my mind, Roku has definitely benefited from the first-mover advantage and have perfected selling digital ads over over-the-top (OTT) boxes.

It just so happens that Roku has prepared itself to extract maximum profits from the intersection of integrating online streaming assets and the consumer quitting analog cable.

The timing couldn’t have been better if they tried.

In its infancy, Roku’s revenue was reliant on selling the physical hardware, but that revenue has trailed off at the perfect time because of the explosion of digital ad growth in the industry boosting its other business.

Perhaps even more impressive is the loss of 8 cents last quarter when the company was expected to lose 22 cents.

This signals to investors that profitability is just around the corner for Roku and after years of burning cash, they are finally ready to turn the page and start a new chapter in the history of Roku.

Roku bottomed out at $25 and is now trading over $125, an extraordinary feat and one of the stories of the tech industry in 2019.

I wouldn’t chase the stock here, but I will say the momentum is palpable and Roku will end the year higher than where it is now.

It’s a great stock with an even more compelling story and about to harvest and monetize the new streaming assets that are coming through the pipeline.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/08/streaming-tv-platforms.png4951012Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-12 01:02:412019-09-16 10:29:45Unstoppable Roku

Apple has endured a tumultuous last six months, but the company and the stock have turned the page on the back of the anticipation of the new Apple streaming service that Apple plans to introduce next week at an Apple event.

The company also recently announced a partnership with Goldman Sachs (GS) to launch an Apple-branded credit card.

In the deal, Goldman Sachs will pay Apple for each consumer credit card that is issued.

These new initiatives indicate that Apple is doing its utmost to wean itself from hardware sales.

Effectively, Apple's over-reliance on hardware sales was the reason for its catastrophic winter of 2018 when Apple shares fell off a cliff trending lower by almost 35%.

This new Apple is finally here to save the day and will demonstrate the high-quality of engineering the company possesses to roll out such a momentous service.

Frankly speaking, Apple needs this badly.

They were awkwardly wrong-footed when Chinese consumers in unison stopped buying iPhones destroying sales targets that heaped bad news onto a bad situation.

I never thought that Apple could pivot this quickly.

Apple's move into online streaming has huge ramifications to competing companies such as Roku (ROKU).

In 2018, I was an unmitigated bull on this streaming platform that aggregates online streaming channels such a Sling TV, Hulu, Netflix and charges digital advertisers to promote their products on the platform through digital ads.

I believe this trade is no more and Roku will be negatively impacted by Apple’s ambitious move into online streaming.

What we do know about the service is that channels such as Starz and HBO will be subscription-based channels that device owners will need to pay a monthly fee and Apple will collect an affiliate commission on these sales.

Apple needs to supplement its original content strategy with periphery deals because Apple just doesn’t have the volume to offer consumers a comprehensive streaming product like Netflix.

Only $1 billion on original content has been spent, and this content will be free for device owners who have Apple IDs.

Apple's original content budget is 1/9 of Netflix annual original content budget.

My guess is that Apple wants to take stock of the streaming product on a smaller scale, run the data analytics and make some tough strategic decisions before launching this service in a full-blown way.

It's easier to clean up a $1 billion mess than a $9 billion mess, but knowing Apple and its hallmarks of precise execution, I'd be shocked if they make a boondoggle out of this.

Transforming the company from a hardware to a software company will be the long-lasting legacy of Tim Cook.

The first stage of implementation will see Apple seeking for a mainstay show that can ingrain the service into the public's consciousness.

Netflix was a great example, showing that hit shows such as House of Cards can make or break an ecosystem and keep it extremely sticky ensuring viewers will stay inside a walled pay garden.

Apple hopes to convince traditional media giants such as the Wall Street Journal to place content on Apple's platform, but there has already been blowback from companies like the New York Times who referenced Netflix’s demolition of traditional video content as a crucial reason to avoid placing original content on big tech platforms.

Netflix understands how they blew up other media companies and don’t expect them to be on Apple’s streaming service.

They wouldn’t be caught dead on it.

Tim Cook will have to run this race without the wind of Netflix’s sails at their back.

Netflix has great content, and that content will never leave the Netflix platform come hell or high water.

Apple is just starting with a $1 billion content budget, but I believe that will mushroom between $4 to $5 billion next year, and double again in 2021 to take advantage of the positive network effect.

Apple has every incentive to manufacture original content if third-party original content is not willing to place content on Apple's platform due to fear of cannibalization or loss of control.

Ultimately, Apple is up against Netflix in the long run and Apple has a serious shot at competing because of the embedment of 1 billion users already inside of Apple's iOS ecosystem that can easily be converted into Apple streaming service customers.

If you haven't noticed lately, Silicon Valley's big tech companies are all migrating into service-related SaaS products with Alphabet (GOOGL) announcing a new gaming product that will bypass traditional consoles and operate through the Google Chrome browser.

Even Walmart (WMT) announced its own solution to gaming with a new cloud-based gaming service.

I envision Apple traversing into the gaming environment too and using this new streaming service as a fulcrum to launch this gaming product on Apple TV in the future.

The big just keep getting bigger and are nimble enough to go where internet users spend their time and money whether it's sports, gaming, or shopping.

Apple is no longer the iPhone company.

I have said numerous times that Apple's pivot to software was about a year too late.

The announcement next week would have been more conducive to supporting Apple’s stock price if it was announced the same time last year, but better late than never.

Moving forward, Apple shares should be a great buy and hold investment vehicle.

Expect many more cloud-based services under the umbrella of the Apple brand.

This is just the beginning.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/netflix-mar25.png564972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-25 02:06:312019-07-10 21:39:03Apple's Big Push Into Services

As 2019 christens us with new technological trends, building our portfolio and lives around these themes will give us a leg up in battling the algorithms that have upped the ante in our drive to get ahead.

Now it’s time to chronicle some of these trends that will permeate through the tech universe.

Some are obvious, and some might as well be hidden treasures.

Smart Areas Will Conspicuously Advance

American consumers will start to notice that locations they frequent and the proximities around them will integrate more smart-tech.

The hoards of data that big tech possesses and the profiles they subsequently create on the American consumer will advance allowing the possibilities of more precise and useful products.

These products won’t just accumulate in a person’s home but in public areas, and business will jump at the chance to improve services if it means more revenue.

Amazon and Google have piled money into the smart home through the voice assistant initiatives and adoption has been breathtaking.

The next generation will provide even more variety to integrate into daily lives.

Location-based Dispersion Will Ramp Up

The gains in technology have given the consumer broader control over their lives.

The ability to practically manage one’s life from a remote location has remarkably improved leaps and bounds.

The deflation of mobile phone data costs, the advancement of high-speed broadband internet services in developing countries, more cloud-based software accessible from any internet entry point, and the development of affordable professional grade hardware have made life easy for the small business owners.

What a difference a few years make!

This has truly given a headache for traditional companies who have failed to evolve with the times such as television staples who rely on analog advertising revenue.

Millennials are more interested in flicking on their favorite YouTuber channel who broadcast from anywhere and aren’t locally based.

Another example is the quality of cameras and audio equipment that have risen to the point that anybody can become the next Justin Bieber.

Music executives are even using Spotify to target new talent to invest in.

Overhyped Bitcoin Will Finally Take A Siesta From The Mainstream

Blockchain technology has the makings of transforming the world we live in.

And the currency based on the blockchain technology had a field day in the press and backyard summer barbecues all over the country.

Well, 2019 will finally put this topic on the backburner even though Bitcoin won’t disappear into irrelevancy, the pendulum will swing the other direction and this digital currency will become underhyped.

The rise to $20,000 and the catastrophic selloff down to $4,000 was a bubble popping in front of us.

It made a lot of people rich like the Winklevoss brothers Cameron and Tyler who took the $65 million from Facebook CEO Mark Zuckerberg and spun it into bitcoin before the euphoria mesmerized the American public.

On the way down from $20,000, retail investors were tearing their hair out but that is the type of volatility investors must subscribe to with assets that are far out on the risk curve.

The volatility that FinTech leader Square (SQ) and OTT Box streamer Roku (ROKU) have are nothing compared to the extreme volatility that digital currency investors must endure.

E-Sports Will Become Even More Popular

Video games classified as a spectator sport will expand up to 40% in 2019.

This phenomenon has already captivated the Asian continent and is coming stateside.

This is a bit out of my realm as standard spectator sports don’t appeal to me much at all, and watching others play video games for fun is something I am even further removed from.

But that’s what the youth like and how they grew up, and this trend shows no signs of stopping.

Industry experts believe that the U.S. is at an inflection point and adoption will accelerate.

Remember that kids don’t play physical sports anymore because of the risk to head trauma, blown ligaments, and the sheer distances involved traveling to and from venues turn participants away.

Franchise rights, advertising, and streaming contracts will energize revenue as a ballooning audience gravitates towards popular leagues, tapping into the fanbase for successful video game series such as Overwatch.

The rise of eSports can be attributed to not only kids not playing physical sports but also younger people watching less television and spending more time online.

Soon, there will be no difference in terms of pay and stature of pro athletes and video gaming athletes.

The amount of money being thrown at the world’s best gamers makes your spine tingle.

Data Regulation Will Tighten

The era of digital data regulation is upon us and whacked a few companies like Google and Facebook in 2018.

Well, this is just the beginning.

The vacuum that once allowed tech companies to run riot is no more, and the government has big tech in their cross-hairs.

The A word will start to reverberate in social circles around the tech ecosphere – Antitrust.

At some point towards the end of 2019, some of these mammoth technology companies could face the mother of all regulation in dismantling their business model through an antitrust suit.

Companies such as Amazon and Facebook are praying to the heavens that this never comes to fruition, but the rhetoric about it will slowly increase in 2019 because of the mischievous ways these tech companies have behaved.

The unintended consequences in 2018 were too widespread and damaging to ignore anymore.

Antitrust lawsuits will creep closer in 2019 and this has spawned an all-out grab for the best lobbyists tech money can buy.

Tech lobbyists now amount to the most in volume historically and they certainly will be wielded in the best interest of Silicon Valley.

Watch this space.

Software Favored To Hardware

The demand for smart consumer devices will fall off a cliff because most of the people who can afford a device already are reading my newsletter from it.

The stunting of smart device innovation has made the upgrade cycle duration longer and consumers feel no need to incrementally upgrade when they aren’t getting more bang for their buck.

The late-cycle nature of the economy that is losing momentum because of a trade war and higher interest rates will see companies look to add to efficiencies by upgrading software systems and processes.

This bodes well for companies such as Microsoft (MSFT), Salesforce (CRM), Twilio (TWLO), PayPal (PYPL), and Adobe (ADBE) in 2019.

Logistics Gets A Boost From Technology

This is where Amazon has gotten so good at efficiently moving goods from point A to point B that it is threatening to blow a hole in the logistic stalwarts of UPS and FedEx.

Robots that help deploy packages in the Amazon warehouses won’t just be an Amazon phenomenon forever.

Smaller businesses will be able to take advantage of more robotics as robotics will benefit from the tailwind of deflation making them affordable to smaller business owners.

Amazon’s ramp-up in logistics was a focal point in their purchase of overpriced grocer Whole Foods.

This was more of a bet on their ability to physically deliver well relative to competition than it was its ability to stock above average quality groceries.

If Whole Foods ever did fail, Amazon would be able to spin the prime real estate into a warehouse located in wealthy areas serving the same wealthy clientele.

Therefore, there is no downside short or long-term by buying Whole Foods. Amazon will be able to fine-tune their logistics strategy which they are piling a ton of innovation into.

Possible new logistical innovations include Amazon attempting to deliver to garages to avoid rampant theft.

This is all happening while Amazon pushes onto FedEx’s (FDX) and UPS’s (UPS) turf by building out their own fleet.

Innovative logistics is forcing other grocers to improve fast giving customers better grocery service and prices.

Kroger (KR) has heavily invested in a new British-based logistics warehouse system and Walmart (WMT) is fast changing into a tech play.

Tech Volatility Won’t Go Away

Current Chair of the Federal Reserve Jerome Powell unleashed a dragon when he boxed himself into a corner last year and had to announce a rate hike to preserve the integrity of the institution.

Markets whipsawed like a bull at a rodeo and investors lost their pants.

Tech companies who have been leading the economy and trot out robust EPS growth out of a whole swath of industries will experience further volatility as geopolitics and interest rate rhetoric grips the world.

Apple’s revenue warning did not help either and just wait until semiconductors start announcing disastrous earnings.

The short volatility industry crashed last February, and the unwinding of the Fed’s balance sheet mixed with the Chinese avoiding treasury purchases due to the trade war will insert even more volatility into the mix.

Powell attempted to readjust his message by claiming that the Fed “will be patient” and tech shares have had a monstrous rally capped off with Roku exploding over 30% after news of positive subscriber numbers and news of streaming content platform Hulu blowing past the 25 million subscriber mark.

Volatility is good for traders as it offers prime entry points and call spreads can be executed deeper in the money because of the heightened implied volatility.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/01/warehouse-robots.png512852Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-09 01:06:182019-07-09 04:58:15Top 8 Tech Trends of 2018

As an astute purveyor of technology, it is my job to share with you the upcoming tech trends of 2019.

Some might be easily discernable and some might be a headscratcher, but all must be tabbed up and considered in the current tech outlook that is unpredictable and fluctuating, to say the least.

Part of the moody tech sentiment has been influenced by a changeable macro landscape - the tech sector’s winter freeze was woefully volatile and unfairly capsized good companies with the bad.

There is no means to get around it – the administration's delicate situation as it relates to Beijing and the American tech sector is front and center, and any movement of tech stocks must carefully absorb the ongoings from this complicated relationship.

The number of obstacles that confront this sensitive situation means that the 90-day window granted to solve the trade quagmires appear too brief of a timeframe to really knock out every single disagreement on the table.

The uncertainty over trade policy has really ruffled some of tech’s strongest feathers such as America’s pride and joy Apple (AAPL).

Apple is a great long-term story, but it does not preside over many short-term positive catalysts that can resuscitate the stock.

Analysts' downgrade after downgrade has been most harrowing for the chip components that make up Apple and other consumer electronic devices such as televisions and tablets.

This scenario is expected to extend into 2019 with Bank of America Merrill Lynch (BAC) slashing their price target by nearly 30% on electronics retailer Best Buy (BBY) then sticking the fork in them by downgrading it to underperform.

The premise behind this downgrade was that Best Buy carved out 25% of revenue from television sales and even though Adobe (ADBE) analytics has calculated record online sales in the holiday season, the follow-through has largely been without television sales participating in the seasonal bonanza.

Piggybacking on this trope, I believe electronic device sales could be hard-pressed to eke out growth next year and are set up for a rude awakening.

Therefore, it is sensible to extrapolate this idea out and assume that smart hardware competing against the big boys such as smart speaker firm Sonos (SONO), who I urged readers to stay away at $16 in September, is set up for a painstaking 2019.

The stock is now trading at $11 and a mix of weakening consumer device demand layered with the domination that is the Amazon Alexa has pushed up this company’s risk-reward levels to untold heights.

Rounding out the negatives is that content streaming platform Roku has also debuted its own version of a smart speaker.

Roku (ROKU) is one of my favorite long-time tech plays but has been dragged down by the broader trade war because a portion of its revenue is still captured by hardware such as the new speakers and Roku OTT boxes.

Differing from Apple, Roku earns most of their revenue from targeted ads on their proprietary platform, and this is its reason why most investors are in this stock that is set to capture a secular migratory wave of cord-cutters traversing to online streaming.

However, Roku TVs made by Chinese company TCL still draw in small portion of revenue and even though the China revenue is not as high on a relative basis as Apple’s 20%, the stock has floundered in the short-term.

If disruptors such as Roku can get hit savagely with a small portion of revenues from China, then I am convinced that any tech investor going into 2019 should stay away from hardware and hardware that is made in China.

The consensus is that the drawn-out trade war could become the X-factor in the 2020 election because the Chinese are willing to wait for the next guy on the carousel searching for a better deal.

If you thought Chinese supply chains had a tough time of it in 2018, then 2019 is poised to be even more treacherous.

What 2018 convincingly demonstrated was that the late economic price action is getting into later and later stages boding negative for tech stocks.

To construct a healthy tech portfolio going into 2019, the change in the tech partiality has made the pivot towards software much more important.

Investors need to mitigate Chinese supply chain risk and seek out domestic software plays.

That should be the playbook as tech investors are on pins and needles going into the new year.

The domestic economy is robust and tech investors should be attracted to top-quality cloud-based enterprise stocks that are profitable.

The FANG story collapsing in our face signaled to investors that it is time to cautiously consider whether to invest heavily into deep loss-maker tech growth stories.

A healthy rotation to premium quality tech with superior cash flow is one way to lock up stocks and slyly deflect the external factors shaking up the tech momentum.

PayPal (PYPL) is a stock that has large international exposure mainly in Europe, but none in China whose 3-year EPS growth rate is 26% and still driving sequential sales in the mid-20% range.

This is just one example of a stock that has the correct make-up in a harsh and brutal tech environment planted with invisible booby traps.

And the most tell-tale sign that the American economy is in for an all-out software frenzy is the number of head-spinning investments from big tech companies looking to expand their footprint into new talent spots around the country.

First, the farcical Amazon beauty pageant came to an end with the e-commerce giant announcing a three-part package deploying new operations in New York, Washington D.C., and Nashville as the next phase of digital growth ramps up.

Google (GOOGL) followed that up by plopping a software office in New York City devouring a huge chunk of the Chelsea neighborhood aimed at doubling the 7,000 employees already there.

Then it was Apple’s turn choreographing a significant investment in Austin, Texas that will cost them $1 billion along with juicing up operations in Seattle, San Diego, and Los Angeles.

They weren’t finished there and promised to double down its presence in Pittsburgh, New York and Boulder, Colorado over the next three years.

It’s clear that big tech has finally understood that it’s not invincible and milking the China supply chain for all its worth is now a taboo business practice that has bipartisan support firmly against it.

Like I said before, the trade war came 1-2 years too early for Apple, and these headline-grabbing talent investments in data centers and its staff underscore the sense of urgency to fully and comprehensively pivot towards a software and services company.

The transition has certainly been an excruciating process exposing the weak spots at a brilliant company at the worst possible time.

I blame CEO of Apple Tim Cook who is the operations expert in the building grappling with Apple overextending themselves in the Middle Kingdom that has come back to haunt him at night.

You would have thought that with the troves of big data on their hands, Apple’s consultants might have found a country allied with America to invest in such a massive supply chain.

This leads me to communicate with conviction that Microsoft (MSFT) is my favorite tech stock going into 2019 because it is the purest, scalable, high-quality software name with minimal hardware drag devoid of weak spots in its armor.

That was what the investment in GitHub for $7.5 billion was about, highlighting the value of owning the meeting place for coders, literally buying up a stash of over 28 million users and 57 million coding repositories in which 28 million are public.

Microsoft has also bought up six video game studios in 2018 attempting to capture a bigger piece of the pie for the video game market that has been throttled by Fortnite.

If the Microsoft baby gets thrown out with the bathwater, then the tech bear market is upon us in full force.

If you didn’t really believe content is king in 2018, then you will really feel the phenomenon further embedded into the economy and society in 2019.

Next year, almost all tech investments will result in more data centers and software engineers in the hope of pumping out the best content and data, whether it’s enterprise software, video games, or pure data storage.

In 2019, I am bullish on companies with a cloud-based bedrock able to grind out the best content in the world, backed by a strong balance sheet that dovetails nicely with a lack of China-based revenue exposure.

The uber-growth models could be taking a rest boding negatively for Uber, Lyft, and Airbnb who must convince a more skeptical tech audience with tighter purse strings as they inject yet another unique dimension into the tech world next year.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-18 01:06:302018-12-17 18:35:08The Big Technology Trends of 2019

Gazing into the future, investors know it’s time to deploy strategies to make money in 2019.

This year has been a bizarre one for technology stocks.

The industry was overwhelmed by a relentless geopolitical circus that had more sway on tech stock’s price action than in any year that I can remember.

Technology stocks have never been more intertwined with politics.

The so-called FANGs have really been taken out behind the woodshed and beaten, and their get-out-of-jail card is no longer free to access with politicians eyeing them as take down targets.

They are no longer invincible even if they still earn bucket loads of money.

A good amount of the public animosity towards the big tech companies has been directed to socially awkward CEO of Facebook Mark Zuckerberg and his negligence towards the concept of personal data.

Facebook was once the best company in technology to work, I can tell you now that prospective applicants are scrutinizing Facebook’s actions with a gimlet eye and turning to other opportunities.

Current Facebook employees are putting in feelers out to former colleagues planning optimal exit strategies.

Remember that it’s not my job to always tell you which tech stocks are going up, but also to tell you which tech stocks are going down.

One stock poised to outperform in 2019 is international FinTech company PayPal (PYPL).

The stock has proven to be Teflon-like deflecting the pronounced volatility that has soured the tech sector in the second half of the year.

The pendulum of regulation-flipping will concoct new winners for 2019 and I believe PayPal is one of them.

PayPal is in a dominant market position with a core customer base of 254 million users and growing.

The company is so dominant that it processes almost 30% of all global payments excluding China where foreign companies are barred from operating in the FinTech space.

The quality of the product is demonstrated by a recent note from research firm Nielsen offering data showing that on average, PayPal customers complete transactions 88.7% of the time.

This astoundingly high number for PayPal checkout conversion is about 60% better than “other digital wallets” and 82% better than “all payment types."

PayPal’s home country, United States, is still vastly unmonetized in terms of the breadth of penetration of online and e-commerce payments.

America has failed so far to adopt the amount of FinTech that Chinese consumers have rapidly embraced.

The great news is that late-stage adoption of FinTech services will offer PayPal a path to profits that bodes well for the earnings and its share price in 2019 and beyond.

Investors can expect total payment volumes (TPV) consistently nudging up in the mid-20% range.

The firm helmed by Dan Schulman is just scratching the surface on pricing power.

PayPal has changed its approach of ‘one‐size‐fits‐all’ in merchant contracts to a dynamic pricing model reflecting the value‐add of recently acquired products that are more powerful.

Jetlore, launched in 2014, is a provider of predictive artificial intelligence for retail companies able to comb through the data to help boost sales.

Hyperwallet distributes payments to those that sell online, and its purchase was centered around protecting the company's core business, enabling marketplaces to pay into PayPal accounts.

iZettle, an international mobile point-of-sale (POS) provider, is better known as the Square of Europe and has a large footprint. The relationship in PayPal has sounded alarm bells in Britain for being too dominant.

Simility, an AI-based fraud prevention specialist, round out a comprehensive list of new tools and services to PayPal’s all-star caliber lineup that can offer upgrades to businesses through a hybrid solution.

This positivity surrounding the sum of the parts will allow the company to build custom solutions for merchants of all sizes.

Augmenting a solid, stable business is a start-up inside of PayPal’s umbrella of assets with enormous growth potential called Venmo making up one of PayPal’s large future bets.

Venmo is a peer-to-peer payment app acquired by PayPal in 2013.

It is a favorite and mainstay of Millennial users who have gravitated towards this FinTech platform.

PayPal is intently focused on monetizing Venmo and the strategy is paying dividends with last quarter seeing 24% of Venmo traffic monetized which is up sequentially from 17% the quarter before.

Part of the increase in profits can be attributed to integrating Uber Eats into the platform, tacking on a charge for instant money transfers linked to bank accounts, and a Venmo debit card rolled out to the masses.

This innovation was not organic and in fact borrowed from FinTech Square, a great company led by Jack Dorsey, but the stock is incredibly volatile scaring off a certain class of investors.

Former CFO of Square Sarah Friar left her post at Square to boldly take on a CEO job at Nextdoor, a social network app, illustrating that an executive management job at Square is a golden credential able to springboard workers to a CEO job in Silicon Valley.

Shares of Square have doubled in 2018 and 2017, and the recent weakness in shares is more of a case that Square went too far over its skis than anything materially wrong with the company as well as a harsh macro climate that stung most of tech.

The price action can sometimes be breathtaking with 7% moves up and down all in a few days.

If you are searching for a slow grinder on the way up, then Microsoft (MSFT) would be a better tech play to plop your money into.

In my eyes, Microsoft is the most durable, all-terrain tech stock that will weather any type of gale-force squall in 2019.

For me, CEO of Microsoft Satya Nadella is the best CEO out there in the tech industry minus Jeff Bezos at Amazon (AMZN).

The Azure Cloud business is ferociously nipping at Amazon’s heels and Nadella has created a subscription-based monster out of legacy components left behind by failure Steve Ballmer who almost sunk Microsoft.

The stock has risen three-fold since Nadella took the reins, and I believe that Microsoft will soon surpass the trillion-dollar market capitalization level and end 2019 as the most valuable tech company.

Microsoft is indestructible because it’s a hybrid mashup of a growth company whose legacy products are also still delivering fused with a top-notch gaming division and a chance at catching the Amazon cloud.

The only company that can compare in terms of potency is Amazon.

Microsoft is not a one-trick pony like Apple, Facebook, Netflix and the way I see it, there are only two top companies in the tech landscape that will leave the last three companies I mentioned in the rear-view mirror.

Echoing Microsoft, PayPal has adopted a similar magical formula with its legacy core growing at 20% yet has growth levers with Venmo layered with targeted add-on companies that will enhance the firm’s offerings.

Moving forward, tech companies that have one or more growth drivers funded by a successful legacy base will become the ultimate tech stocks.

Playing on the same trope, Adobe (ADBE) is another company that has a software-based iron-clad legacy twinge to it and has the potential to spread its wings in 2019.

PayPal, Microsoft, and Adobe do not have the potential to double like Square or Roku next year, but they have minimal China trade war risk if things turn ugly, highly profitable with growing EPS, and are pure software companies whose CEOs put a massive emphasis on software development.

Expect this trio to melt up in 2019, and be prepared to strap on call spreads at advantageous entry points.

Another pure software service stock I love for 2019 is Twilio (TWLO) who I chronically use when I call an Uber to shuttle me around and take weekend getaways on Airbnb.

I would also lump Salesforce (CRM) into the discussion for stocks to buy in 2019 too.

Notice that all the stocks I favor next year are heavily weighted towards software and not hardware.

Hardware is going out of fashion at warp speed, the China tariffs just exacerbated this trend since most of the hardware supply chains are based in China.

Currently, the Mad Technology Letter has open positions in Microsoft and PayPal and if you are like most people online, you will probably use their service next year and more than a few times.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-13 05:16:372018-12-13 05:18:14How PayPal is Destroying Legacy Banking

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.