Global Market Comments

November 30, 2018

Fiat Lux

Featured Trade:

(NOVEMBER 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(VXX), (VIX), (GE), (ROKU), (AAPL),

(MSFT), (SQ), (XLK), (SPLS), (EWZ), (EEM)

Global Market Comments

November 30, 2018

Fiat Lux

Featured Trade:

(NOVEMBER 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(VXX), (VIX), (GE), (ROKU), (AAPL),

(MSFT), (SQ), (XLK), (SPLS), (EWZ), (EEM)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader November 28 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

Q: Is it time to get out of semiconductor stocks?

A: The time to get out is before it drops 60%, not afterwards. So, if you have semiconductor stocks, I would look for the next major rally to get out. I think we will get one of those rallies into December/January. We went negative on this sector in June, took all our profits, and didn’t go back in until last week.

Q: Is it time to buy semiconductor stocks?

A: No, that is the group you want to buy at the absolute bottom of the next recession which might be next year sometime. They lead on the downside, and they will lead on the upside as soon as they sniff a recovery in the economy.

Q: I held on to my position in Square (SQ). Should I sell now for a small profit?

A: Yes, in recessions, big companies prosper much more than small companies like Square; that’s why it had such a tremendous selloff; down 55% in six weeks. A small technology stock is not what you want to own in a recession. Big companies slow down, small ones die. At least that’s how conservative investors see it.

Q: What do you make of Fed comments this morning that asset prices are high?

A: I agree with them. They were certainly overpriced with a P/E multiple of 20 that we saw in September; they’re moderately priced now with a P/E multiple of 14.9. I think real estate markets are the overpriced assets that the Fed is talking about though, far more than the stock market, and markets like San Francisco, Seattle, and Vancouver are still way too high.

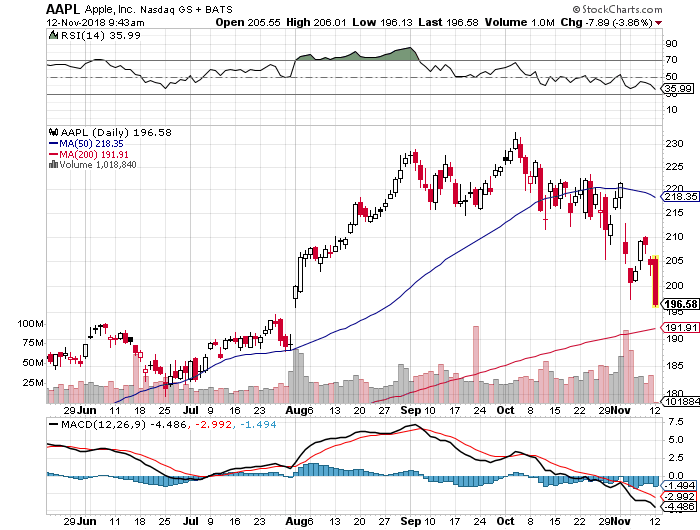

Q: What are your comments on Apple (AAPL)?

A: There’s an interesting thing going on here; you’ve just had a massive move out of hardware stocks like Apple, which basically makes phones and computers, into software stocks like Microsoft (MSFT), which is growing their cloud business like crazy. You may see this as a long-term industry trend, out of hardware stocks into software stocks. It’s all about the cloud now. The future is in software and that is where Apple is going to with services like the cloud, iTunes, streaming, and advertising, although they are doing it slowly.

Q: Will Trump be able to persuade Fed Chair Powell to stop hiking interest rates?

A: He will not, Powell is one of the few principled people in the government. He’s going to stick to his discipline, only look at the data, and that is going to require him to keep raising interest rates. One of the big black swans for 2019 may be that Trump fires Powell and gets a friendly rent-a-Fed chair in there who lowers interest rates on command. If Trump can hold on for nine months though, even Powell will see the economy’s in trouble and will have to respond accordingly by capping or even lowering interest rates.

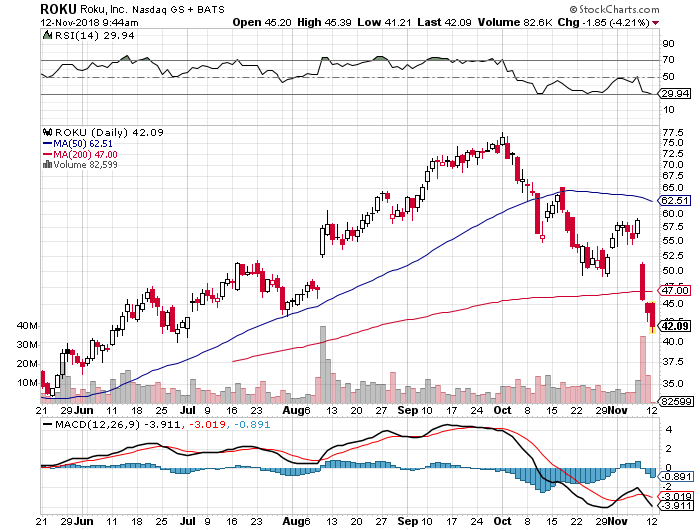

Q: Why are you not stopping out of Roku (ROKU)?

A: We haven't yet approached our upper strike price on the December $30-$35 vertical bull call spread. That’s usually where I bail out; I like to give stocks plenty of room to do the right thing. Stocks have to breathe and I pick strike prices to compensate for that. Otherwise, you’d be stopping out of every trade immediately.

Q: Should we close the iPath S&P 500 VIX Short Term Futures ETN (VXX) trade or leave it open?

A: I’m looking for a bit more of a rally in stocks and a drop in the Volatility Index (VIX); then we’ll try to grab whatever additional couple of pennies we can get out of that.

Q: What do you think of Brazil (EWZ)?

A: Avoid emerging markets (EEM) as long as the U.S. is raising interest rates and the dollar is strong. Rising dollar means rising debt for emerging markets and less ability to service that debt, all bad for business.

Q: Morgan Stanley (MS) says “buy emerging markets”; are they nuts?

A: For the short term yes, for the multi-year long term they are a screaming buy. They are at historical lows in terms of valuation and already have a recession priced into them. But jumping in too soon could be painful.

Q: What are your expectations for the yield curve?

A: I expect all levels of the fixed income market to drop in price and rise in yield with the sharpest move in overnight rates. This eventually leads to a very steep inverted yield curve which causes recessions and bear markets.

Q: Thoughts on Master Limited Partnerships?

A: They could be relatively safe now that oil is at $50. There have been big selloffs recently. The yield on these are high and there is going to be big infrastructure building for energy going forward. I would say don’t put all your eggs in one basket and diversify your risk. In the Great Recession, many of these went bankrupt. I would look at the Alerian MLP (AMLP), which has fallen 15% in six weeks.

Q: Should I be rotating out of the Tech (XLK) stocks on rallies into more defensive stocks like Staples (SPLS)?

A: That’s half right. You should be rotating out of Tech stocks and rotating into cash which yields up to 2-3% these days. Nothing does well in a real bear market except cash. Defensive stocks still go down, just at a slower rate.

Q: Is General Electric (GE) good for the long term?

A: Yes, if anyone can turn around GE it’s the current management. That said, it could be a long-term slog—that’s why I had a long-term leap in this thing before it collapsed. It could turn around and still go up but these are throwaway, chapter eleven level type prices that we’re getting now. And now they are going to have to do a turnaround going into a recession.

Q: Do you see GE as good for a long-term trade?

A: Long term and trade don’t belong in the same sentence; but I’d say for a long-term investment at these levels, probably yes. It certainly is a bargain from $30 down to $7.40 in a year.

Q: Is this webinar archived?

A: A: Yes, they are always posted on the website within two hours of recording. Just go to www.madhedgefundtrader.com/, login and then hover your cursor over “MY ACCOUNT” click on “GLOBAL TRADING DISPATCH,” “Mad Hedge Technology Letter” or “Newsletter” depending on your membership then click on the Webinars button. The last ten years of webinars should show up, with the most recent one at the top.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 26, 2018

Fiat Lux

Featured Trade:

(WILL THE FAANGS FINALLY KILL OFF TELEVISION?)

(AMZN), (DIS), (FOX), (ROKU), (FB), (AAPL), (GOOGL)

Mad Hedge Technology Letter

November 19, 2018

Fiat Lux

Featured Trade:

(ROKU’S UNASSAILABLE LEAD)

(TIVO), (ROKU), (NFLX), (AMZN), (CHTR), (DISH), (FB), (AAPL), (GOOGL)

Shake off the rust.

That is exactly what management of a fast-growing tech company doesn’t want to hear.

Losing money isn’t fun. And investors only put up with it because of the juicy growth trajectories management promises.

Without the expectations of hard-charging growth, there is no attractive story in a world where investors need stories to rally behind.

Setting the bar astronomically high in the approach to management’s execution and product development will always be, the single most important element in a tech company.

This is the secret recipe for thwarting entropy and rising above the rest.

You might be shocked to find out that most tech firms die a harrowing death, the average Joe wouldn’t know that, with constant headlines glorifying our tech dignitaries.

Just look at the pageantry on display that was Amazon’s (AMZN) quest to find a second headquarter.

According to Apex Marketing, the hoopla that coalesced around Amazon’s year-long search netted Amazon $42 million in free advertising by tracking the absorbed inventory of exposure from print, TV, and online.

Social media traffic by itself rung up $8.6 million of freebies.

These days, tech really does sell itself, and I didn’t even mention the billions in tax breaks Amazon will harvest from their Willy Wonka and the Chocolate Factory style headquarter search.

The only thing I would have changed would have been extending the contest into the second year.

Amazon’s brand is probably the most powerful in the world, and that is not because they are in the business of only selling chocolate bars.

One company that might as well sell chocolate bars and has been stymied by the throes of entropy is TiVo (TIVO).

TiVo was once the darling of the technology world.

It was way back in 1999 when TiVo premiered the digital video recorder (DVR).

It modernized how television was consumed in a blink of an eye.

Broad-based adoption and outstanding product feedback were the beginning of a long love affair with diehard users wooed by the superior functionality of TiVo that allowed customers to record full seasons of television shows, and, the cherry on top, fast-forward briskly through annoying commercials.

The technology was certainly ahead of its time and TiVo had its cake and ate it for years.

The stock price, in turn, responded kindly and TiVo was trading at over $106 in August of 2000 before the dot com crash.

That was the high-water mark and the stock has never performed the same after that.

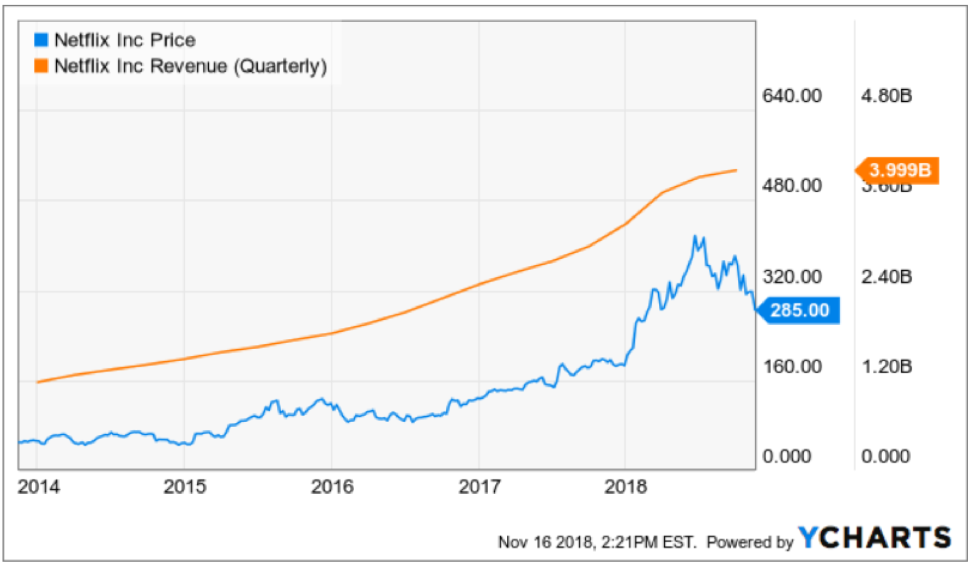

TiVo’s cataclysmic decline can be traced back to the roots of the late 90’s when a small up and coming tech company called Netflix (NFLX) quickly pivoted from mailing DVD’s to producing proprietary online streaming content.

Arrogant and set in their old ways, TiVo failed to capture the tectonic shift from analog television viewers cutting the cord and migrating towards online streaming services.

Consumer’s viewing habits modernized, and TiVo never developed another game-changing product to counteract the death of a thousand cuts to traditional television and its TiVo box that is still ongoing as I write this.

Like a sitting duck, Charter Communications (CHTR) and Dish Network (DISH) devoured TiVo’s market share in the traditional television segment constructing DVR’s for their own cable service.

And instead of licensing their technology before their enemies could build an in-house substitute, TiVo chose to sue them after the fact, resulting in a one-time payment, but still meant that TiVo was bleeding to death.

Enter Project Griffin.

Netflix (NFLX) spent years developing Project Griffin, an over-the-top (OTT) TV box that would host its future entertainment content and poured a bucket full of capital into the software and hardware of this revolutionary product.

Making the leap of faith from the traditional DVD-by-mail distribution model that would soon be swept into the dustbin of history was an audacious bet that looks even better with each passing year.

This Netflix branded OTT box was specifically manufactured for Netflix’s Watch Instantly video service.

In 2007, Netflix was just week’s away from rolling out the hardware from Project Griffin when CEO of Netflix Reed Hastings decided to trash the project.

His reason was that a branded Netflix box would hinder the software streaming content confining their growth trajectory to only their stand-alone platform.

This would prevent their streaming service to populate on other networks.

To avoid discriminating against certain networks was a genius move allowing Netflix to license digital content to anyone with a broadband connection, and giving them chance to make deals with other companies who had their own box.

It was the defining moment of Netflix that nobody knows about.

Netflix became ubiquitous in many Millennial households and Roku (ROKU) was spun-out literally bestowing new CEO of Roku Anthony Woods with a de-facto company-in-a-box to build on thanks to old boss Reed Hastings.

Woods cut his teeth borrowing TiVo’s technology and developed the digital video recorder (DVR) as the founder of ReplayTV before he joined Netflix and was the team leader of Project Griffin.

Now, he had a golden opportunity dropped into his lap and Woods ran with it.

Woods quickly became aware that hardware wasn’t the future of technology and switched to a digital ad-based platform model allowing any and all streaming services to launch from the Roku box.

No doubt Woods understood the benefits of being an open platform and not playing favorites to certain networks in a landscape where Apple (AAPL), Google (GOOGL), Facebook (FB), and Amazon have made “walled gardens” an important part of their DNA.

Democratizing its platform was in effect what the internet and technology were supposed to be from the onset and Roku has excavated value from this premise by playing nice with everyone.

This also meant scooping up all the ad dollars from everyone too.

At the same time, Wood’s mentor Hastings has rewritten the rules of the media industry parting the sea for Roku to mop up and dominate the OTT box industry with Amazon and Apple trailing behind.

Roku was perfectly positioned with a superior finished product, but also took note of the future and zigged and zagged when they needed to which is why ad sales have surpassed their hardware sales.

By 2021, over 50 million Americans will say adios to cable and satellite TV.

The addressable digital ad market is a growing $80 billion per year market and Roku will have a more than fair shot to secure larger market share.

The rock-solid foundations and handsome growth story are why the Mad Hedge Technology Letter is resolutely bullish on Roku and Netflix.

Roku and Netflix have continued to evolve with the times and TiVo is now desperately attempting to sell the remains of itself before the vultures feast on their corpse.

What is left is a portfolio of IP assets that brought in $826 million in 2017, and they have exited the hardware business entirely halting production of the iconic TiVo box.

Digesting 100% parabolic moves up in the share price is a great problem to have for Roku and Netflix.

These two are set to lead the online streaming universe and stoked by robust momentum to go with it.

The Mad Hedge Technology Letter currently holds a Roku December 2018 $30-$35 in-the-money vertical bull call spread bought at $4.35, and it is just the first of many tech trade alerts that will be connected to the rapidly advancing online streaming industry.

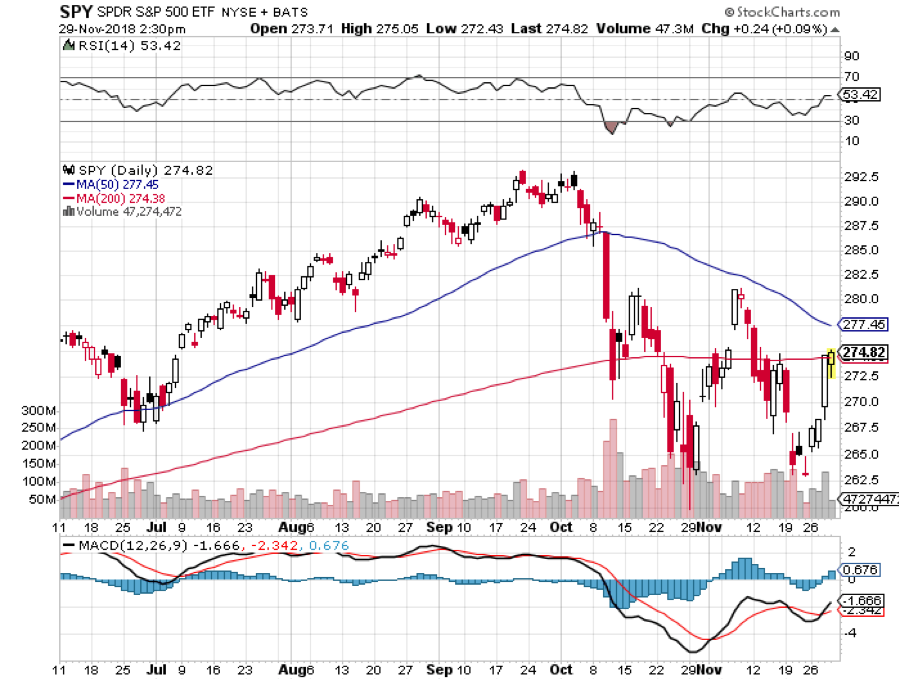

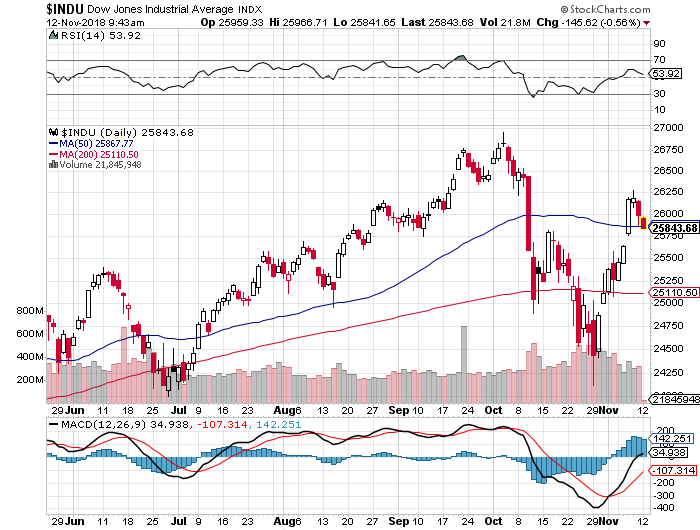

Global Market Comments

November 12, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S FINALLY OVER),

(SPY), (TLT), (AAPL), (ROKU), (USO)

Could it have been the election all along?

Did the massive uncertainty created by the midterm elections hold back investors for all of ten months?

That’s what it looks like now. In a mere three days, shares made back half of what they lost in October, one of the worst trading months in stock market history.

All the market did was trade in a giant range until the day before we trudged out to our local ballot boxes. After that, it was off to the races. Who was the big winner? The people who want to make Donald Trump’s life miserable who now have countless means with which to do so.

Now that the wraps are off, the way is clear for markets to forge on to new all-time highs which they will do by yearend, or early 2019 at the latest.

The Mad Hedge Market Timing Index saw the sharpest rally in 30 years, from 4 to 29 in a week. I told you the market was cheap!

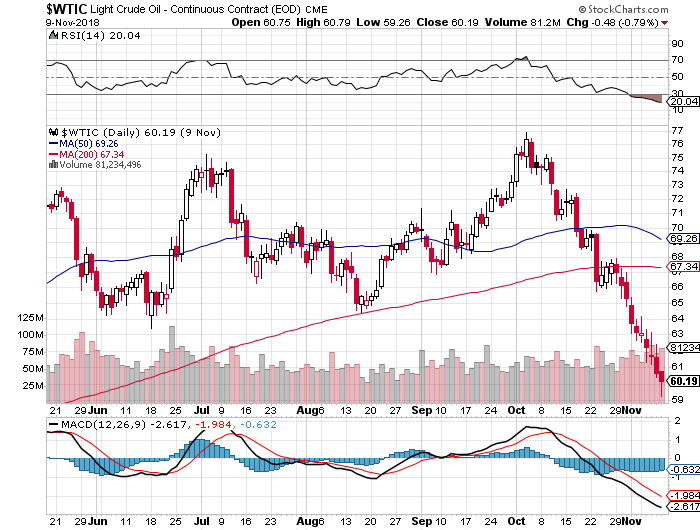

Oil prices (USO) are telling us we are already in recession. Prices are in free fall hitting $60 a barrel, a nine-month low. China certainly is hurting and they are the largest marginal new buyer of Texas tea.

What we are really seeing is a massive unwind of wrong-footed hedge fund oil longs who expected oil prices to soar with the implementation of new sanctions on Iran. They didn’t.

US Exports plunged 26% in September while tariffs paid by US companies soared by an eye-popping 54%. The destruction of American international trade is well underway. When will it end? Who’s benefiting?

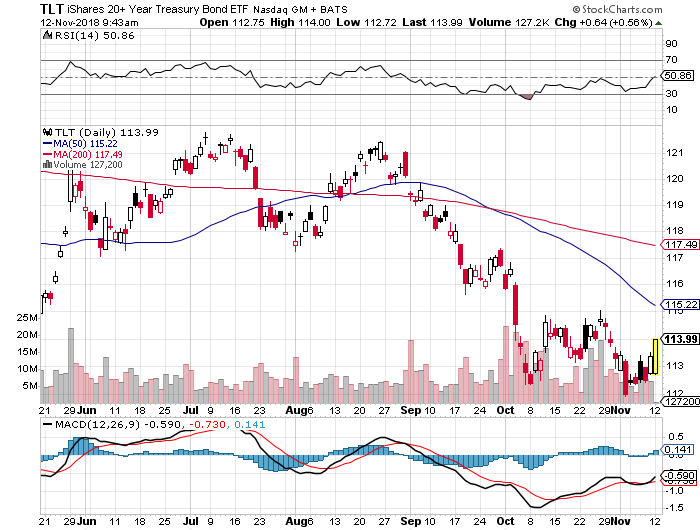

Asians are boycotting US Treasury sales and the US needs to sell to staggering $1.3 trillion in new debt in 2019. Keep hammering the (TLT) with those short positions, your new rich uncle trade.

The Producer Price Index Soared in October, up 0.6% versus 0.2% expected. Yikes, and double yikes! Inflation is here. Keep selling short those bonds (TLT)!

Trump threatened anti-trust action against all of big tech. Market yawned, with Amazon down only $50 after an enormous run-up. A 1% market share against falling prices and enormous customer satisfaction never triggered an anti-trust action before. Jeff Bezos is not the robber baron John D. Rockefeller. Could it be political?

The Number of Job Openings exceeded workers by 1 million in August, with 7.01 million openings versus 5.96 million unemployed. It’s the first time since the Dotcom Bubble top. Are we headed for a 3% Headline Unemployment Rate?

The Golden Age of Gridlock began with the Dems taking the House by flipping 40 seats and the Republicans holding the Senate. Now you can turn off your TV and focus on trading for the next two years. Buy stocks on dips, sell bonds on rallies. Oh, and the 2020 presidential election starts tomorrow.

Housing Sentiment hit a one year low, down a humongous five points, the second fastest drop in history. Rising interest rates have driven a stake through the heart of this once rip-roaring market, but it’s no 2008 replay.

November Share Buy Backs are poised to be the largest in history. Of course, you knew this was going to happen a month ago if you read Mad Hedge Fund Trader. Gotta love that tax reform!

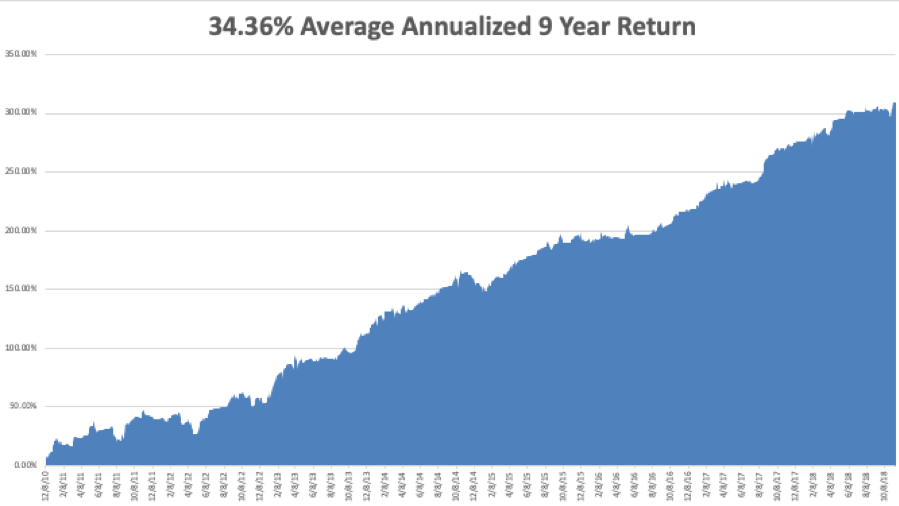

My year-to-date performance rocketed to a new all-time high of +32.94%, and my trailing one-year return stands at 35.33%. November so far stands at +3.31%. And this is against a Dow Average that is up a pitiful 4.43% so far in 2018.

My nine-year return ballooned to 309.41%. The average annualized return stands at 34.72%. 2018 is turning into a perfect trading year for me, as I’m sure it is for you.

In the week before the election, I strapped on the most aggressive long portfolio of this year. It worked like a charm. I then went almost entirely in cash before election day, locking a 12% gain for the model trading portfolio.

I lasted in cash on two days. On the first down 300 point Dow day, I started adding positions in the old familiar names, including Apple (AAPL), Roku (ROKU) for the Mad Hedge Technology Letter, and a short in the (TLT). Bonds could really get crushed going into yearend targeting a 3.50% yield.

Q3 earnings have finished with a whimper and the blackout periods for share buybacks are now over. Let the buying begin! Some $200 billion has to hit the market by yearend, mostly in technology stocks.

After all the recent fireworks, this will be a quiet week on the data front. The October CPI will be the big one, out on Wednesday.

Monday, November 12 is Veterans Day. Stock markets are open but bonds are closed.

On Tuesday, November 13 at 6:00 AM EST, the NFIB Small Business Optimism Index is released.

On Wednesday, November 14 at 8:30 EST, we have the all-important Consumer Price Index announced. How hot will it be?

At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 15 at 8:30, we get Weekly Jobless Claims. At the same time, October Retail Sales are put out.

On Friday, November 16, at 9:15 AM, the October Industrial Production is published.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I am on standby to volunteer as a pilot and serve as spotter for Calfire for the latest Northern California wildfires. I put my name on the waiting list last year, and they only just got around to calling me. There were 2,000 other volunteer pilots on the waiting list ahead of me.

You gotta love America.

Good luck and good trading.

Captain John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 6, 2018

Fiat Lux

Featured Trade:

(THE GREAT TECH COMPANY YOU’VE NEVER HEARD OF)

(TWLO), (ROKU), (MSFT), (SQ), (AMD), (CRM), (SEND)

As volatility rears its hideous head, it’s not necessarily the best time to catch a falling knife as tech companies have been scrutinized harshly lately.

But the market is always right, and waiting for them to drop into your lap will serve you in good stead, even more so for the higher beta tech names that can behave more petulant than a little child.

Roku (ROKU), AMD (AMD), and Square (SQ) are a few of these smaller names with prodigious growth stories backed by secular tailwinds.

These up-and-comers regularly experience 5-7% setbacks, while sturdier names such as Microsoft (MSFT) pull back 1-2% allowing you to sleep soundly at night.

Another influential company taking the liberty to infiltrate the backend of every global and local company is no other than communications software company Twilio (TWLO).

Many of you might not have heard of them, and it doesn’t sound like such a sexy company right off the bat but I am sure you have heard of companies such as Uber, Lyft, and Airbnb.

Why do I mention these three private tech companies that are on the verge of going public next year?

Because this trio of unicorns are all powered by Twilio’s communication technology that is best of breed in their genre of cloud software.

More specifically, Twilio is a platform as a service (PaaS) firm offering programmatic phone call functions, can automate sending and receiving text messages, and performs other communication functions using its web service APIs.

When your Uber driver calls asking you to reveal yourself out of a concrete apartment block or your lavish gated community, this is all facilitated by Twilio’s technology.

At the recent Twilio Signal Conference in San Francisco, Twilio indicated that its latest “call center in a box” product called Flex was up and running after announcing it this past March.

Prior to Twilio’s roll-out, this type of call center functionality was only reserved for the Fortune 500 companies that could afford expensive software to serve its minions of customers.

The small guy was left out in the cold as usual.

Twilio has reshaped the call center and, at $1 per hour or $150 per month, has made itself a gamechanger for SMEs who don’t have the manpower or capital to fund exorbitant back-end operations.

Twilio is really going after anyone with a light or bulky-shaped wallet as you see from their all-star lineup of customers. U-Haul, real estate website Trulia, and data analytic firms Scorpion and Centerfield are just a few of their customers proving the incredible flexibility of the software.

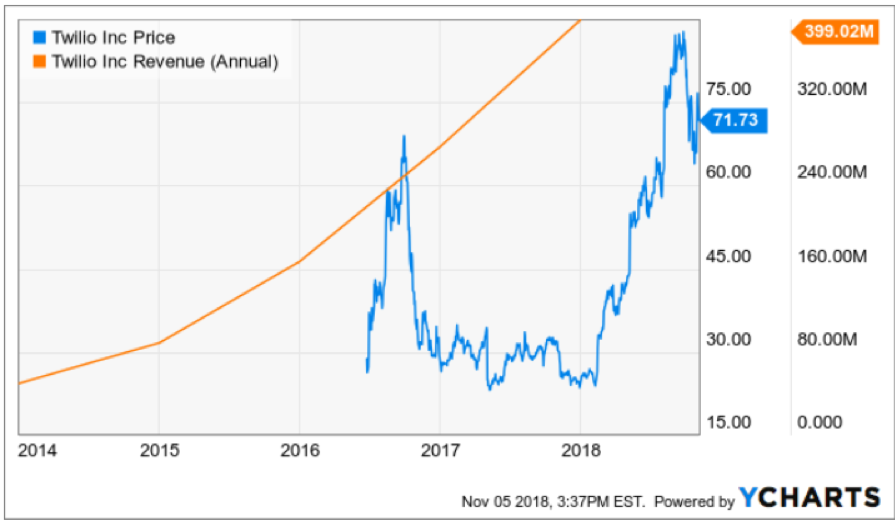

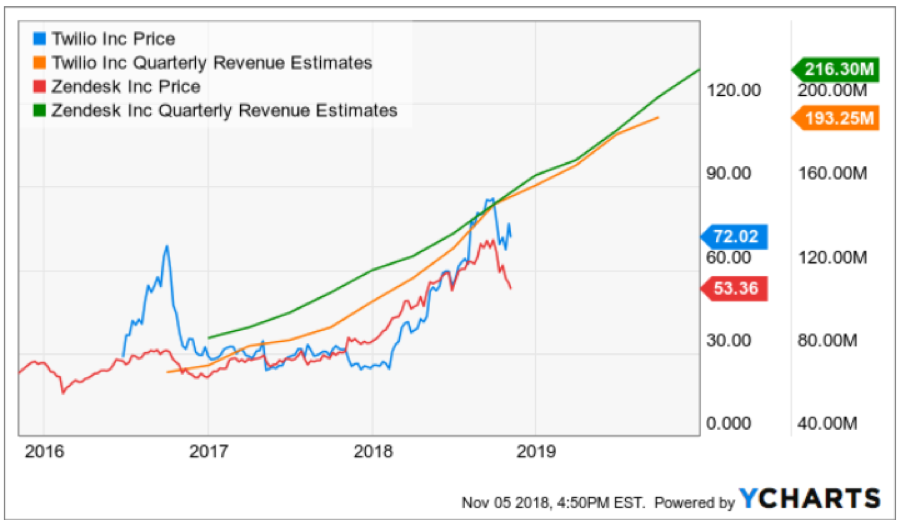

It’s not a shock that this stock has gone ballistic in 2018 surging over 200% and I must admit, investors need to wait for this molten hot stock to cool down.

But how can you blame a company that habitually tears apart any expectation of them devouring expectations because of its super growth model and rapid broad-based adoption?

From the fourth quarter of last year, revenue accelerated to 48% YOY and Twilio followed that up with a blistering 54% YOY quarter.

Then they pulled a shocker guiding down only expecting 35% to 37% growth but dismantled any whiff of jangling investors' nerves by posting another quarterly growth rate of 54%.

If you average out the three-year sales growth rate, few can topple the 57% Twilio has registered.

Performance has been fantastic, to say the least, and Flex could be the product that cements their industry lead and widens the moat around them.

Airbnb, Uber, and Lyft will avoid tinkering with the back end of their operations before their 2019 IPOs boding well for Twilio who are on a hot streak scoring a series of big contracts.

Twilio has been embroiled in further recent stock weakness as they gobbled up SendGrid (SEND), a mass-email marketing software service, for $2 billion.

SendGrid is growing sales at a lower rate in the mid-30%, and this move will add to top line growth.

Synergies from this acquisition are numerous and Twilio will be able to cross-sell to SendGrid’s customers who can apply other communication tools to use.

Telecommunication product in the past was truly unaffordable for the bulk of companies and now that Twilio can bring in all the smaller companies, the SME landscape is poised to change.

Software is becoming powerful to the point where one person living in a basement will have the access to a software that could convince customers a 100-man team is putting this product altogether.

Flex allows customers to personalize this contact-center-in-a-box software for each specification.

It can even quickly integrate into CRM platforms like Salesforce (CRM) which is a wildly popular interface for companies around the world.

Twilio Autopilot, Twilio’s oral conversational AI tool, offers machine learning bots who deliver automated voice-activated functions to customers.

Companies can easily type what they want bots to orate to customers and simply paste it into the code with ease and minimal hassle.

Twilio’s updated payment capabilities offer a new API for building payment experiences by contacting center agents who can now securely accept credit card payments from customers over the phone without the agents ever getting a whiff of the actual numbers.

Effectively, this allows any business in the world to professionalize their communications and backend department to a point they could have never imagined a few years ago.

The saying rings true when industry experts note that it’s the best time to become a billionaire and worst time to become a millionaire because the power of leveraging these robust software programs could potentially fuel the rapid rise of anyone in the world who will eat everybody else’s lunch.

If you break down the numbers, most companies are still holding on to their legacy systems of yore.

Being saddled with outdated hardware and software will doom companies going forward as the explosion of brilliant software modernizes companies in a few clicks of the mouse.

Twilio has added another 15,000 developers to the 35,000 already on the books and the purchase of SendGrid can no doubt be attributed partially to a talent grab of developers who have deep experience building communication-based products.

These types of developers don’t grow on trees.

Last year saw Twilio bring in about $400 million in sales and I am modeling for around $1 billion in sales by 2021.

This $7 billion market cap tech darling has a long runway ahead of itself and investors looking for high-volatility, high-reward stocks can tuck this one away in their sheath.

With earnings coming up and an already 200% plus pop this year, there will be better entry points into this ebullient company if investors are patient.

Wait for a dip to get in on the best communication-based cloud company on the market.

Mad Hedge Technology Letter

November 5, 2018

Fiat Lux

Featured Trade:

(GET READY FOR ANOTHER BITE OF THE APPLE)

(AAPL), (ROKU), (MSFT), (PYPL)