Mad Hedge Technology Letter

March 7, 2025

Fiat Lux

Featured Trade:

(APPLE LOOKING TO FIND ITS MOJO)

(AAPL), (SAMSUNG), (CHINA)

Mad Hedge Technology Letter

March 7, 2025

Fiat Lux

Featured Trade:

(APPLE LOOKING TO FIND ITS MOJO)

(AAPL), (SAMSUNG), (CHINA)

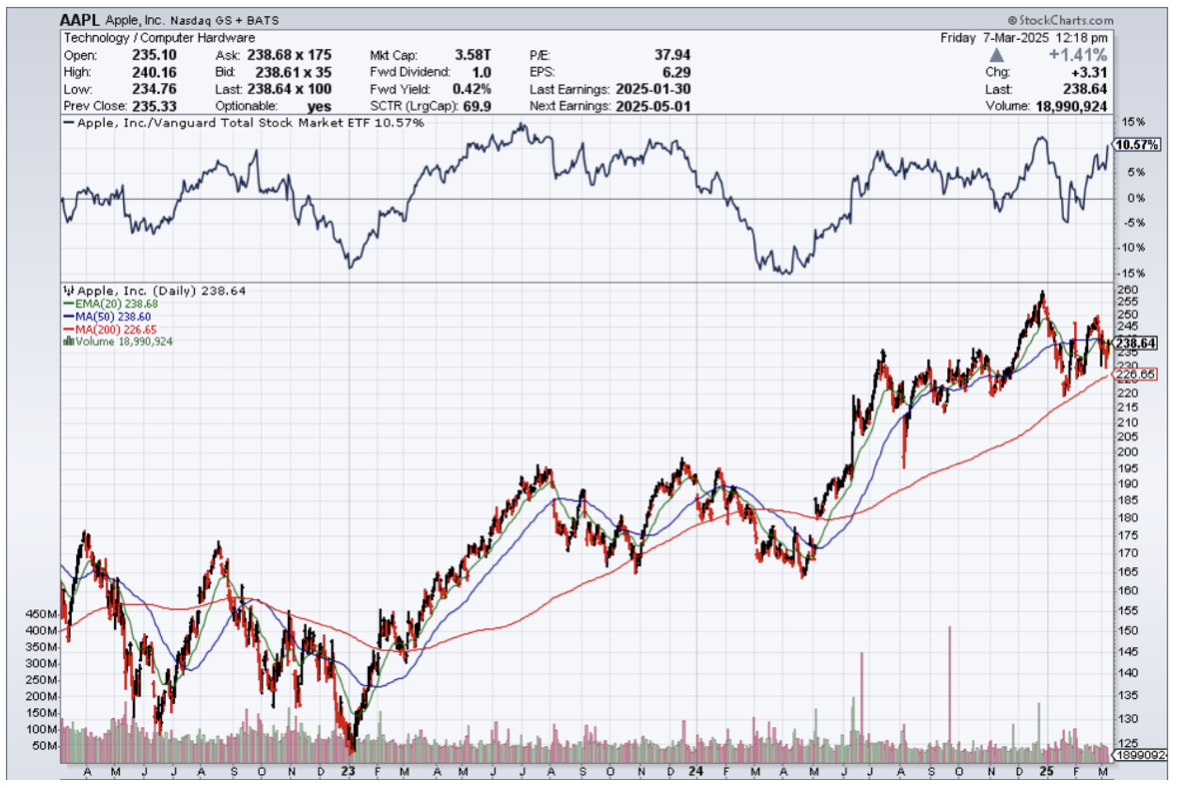

Not only is Apple losing its edge, but they are failing miserably against the Chinese.

China, with its state-supported behemoths, is the bully on the playground, and Apple can’t too diddlysquat.

Apple has been selling the same product for the past 13 years, and the last iterations have been underwhelming, to say the least.

People don’t want to upgrade, forcing to elongate of the refresh cycle.

It’s now so bad that Apple even ceded 5% market share in the final quarter last year to Chinese competition.

Apple is also very late in integrating AI features, signaling that Apple’s software game is behind the times and mediocre at best.

Apple risks falling behind quickly, and the Chinese have really nailed the consumer tech and muscled into this industry.

They are poised to dominate EVs, smartphones, and other value-added tech in the upcoming years.

They plan to seize the moment and squeeze American companies out of the way for good.

Samsung also has been going through a disastrous down cycle after their Android flagship phone peaked a few years ago.

This new trajectory is a slippery slope, and if Apple goes on the cost-cutting path, there will be little talent left to innovate out of this problem.

The iPhone slipped a point to 18% worldwide market share in 2024.

Apple marked a 2% sales decline for the full year at a time that the wider market grew 4% globally.

China’s smartphone makers are all developing their own in-house AI tools and agents, including services that can perform tasks on a user’s behalf.

Samsung also gave up share to faster-growing Android device makers from China, led by Xiaomi and Vivo. Apple marked a 2% sales decline for the full year.

The situation paints a picture of the non-Chinese smartphone markets in a world of hurt.

I believe that Apple and Samsung have nobody to blame but themselves, as those years of forced technological know-how transfer are coming back to bite them where it hurts.

My friends’ kids have these new Chinese smartphones, and I can tell you that I was surprised about how good they perform.

They are run on Android, which is very different from IoS, but they were premium.

German car companies are also feeling this bitter pill as Chinese companies have taken their own technology and implemented it in a more affordable way.

In aggregate, this latest news is a bad omen for Apple’s earnings season.

They are barely jumping over a lower bar, and that will keep happening until something major is revamped in the product lineup.

I believe any steep sell-off would be a nice opportunity to execute a short-term trade to the upside, but those years of buying and holding Apple until eternity is gone.

Readers must really nitpick what this company is doing because management presides over a dull model, and their China business is falling apart as we speak, all while they helped the local Chinese competition over many years take market share with forced technological transfers.

Surprisingly, the stock has done well during the tariff rhetoric and has trudged along sideways while other stocks have really felt the full brunt of the trade escalation.

If we get a smooth patch, I would advocate for a tactical trade to the upside in AAPL.

Mad Hedge Technology Letter

January 13, 2025

Fiat Lux

Featured Trade:

(APPLE DROPS THE BALL)

(AAPL), (SAMSUNG), (CHINA)

Not only is Apple losing its edge, but they are failing miserably against the Chinese.

China, with its state-supported behemoths, is the bully on the playground and Apple can’t too diddlysquat.

Apple has been selling the same product for the past 13 years and the last iterations have been underwhelming, to say the least.

People don’t want to upgrade forcing them to elongate the refresh cycle.

It’s now so bad that Apple even ceded a 5% market share in the final quarter last year to Chinese competition.

Apple is also very late in integrating AI features signaling that Apple’s software game is behind the times and mediocre at best.

Apple risks falling behind quickly and the Chinese have really nailed the consumer tech and muscled into this industry.

They are poised to dominate EVs and smartphones and other value-added tech in the upcoming years.

They plan to seize the moment and squeeze American companies out of the way for good.

Samsung also has been going through a disastrous downcycle after their Android flagship phone peaked a few years ago.

This new trajectory is a slippery slope and if Apple goes on the cost-cutting path, there will be little talent left to innovate out of this problem.

The iPhone slipped a point to 18% worldwide market share in 2024.

Apple marked a 2% sales decline for the full year, at a time when the wider market grew 4% globally.

China’s smartphone makers are all developing their own in-house AI tools and agents, including services that can perform tasks on a user’s behalf.

Samsung also gave up its share to faster-growing Android device makers from China, led by Xiaomi and Vivo. Apple marked a 2% sales decline for the full year.

The situation paints a picture of the non-Chinese smartphone markets in a world of hurt.

I believe that Apple and Samsung have nobody to blame, but themselves as those years of forced technological know-how transfer are coming back to bite them where it hurts.

My friends’ kids have these new Chinese smartphones and I can tell you that I was surprised about how good they perform.

They are run on Android, which is very different from IoS, but they are premium.

German car companies are also feeling this bitter pill as Chinese companies have taken their own technology and implemented it in a more affordable way.

In aggregate, this latest news is a bad omen for Apple’s earnings season.

They are barely jumping over a lower bar and that will keep happening until something major is revamped in the product lineup.

I believe any steep sell-off would be a nice opportunity to execute a short-term trade, but those years of buying and holding Apple until eternity are gone.

Readers must really nitpick what this company is doing because management presides over a dull model and their China business is falling apart as we speak all while they helped the local Chinese competition over many years take market share with forced technological transfers.

Not a good look and things could get worse as we move deeper into the year.

Mad Hedge Technology Letter

October 30, 2024

Fiat Lux

Featured Trade:

(LACK OF AI ROCKS THE KOREAN HEAVYWEIGHT)

(SAMSUNG), (SK HYNIX)

It’s not just about smartphones for Samsung anymore, their stalwart chip business is in full-blown crisis mode as they have been too slow to adapt to the artificial intelligence revolution.

It shows that if a company is asleep at the wheel, how quickly and how far they can fall back.

Samsung is Korea’s flagship tech company, and it is like the Titanic in a way because it is hard to turn around with the amount of employees it has.

Old habits die hard, and management simply wasn’t prepared for the giant leap forward in semiconductor chips.

Remember when their flagship smartphone, named the Galaxy, was the best phone in the world?

Oh, have times changed?

Concerns are piling up that the company is losing out to smaller rival SK Hynix in AI memory and failing to gain on Taiwan Semiconductor Manufacturing.

Overseas investors have sold about $10.7 billion worth of the South Korean company’s shares on a net basis since the end of July.

That hope has been snuffed out with the company admitting delays with its latest-generation HBM chips in early October, soon after SK Hynix said it had begun volume production. Meanwhile, US rival Micron Technology is stepping up efforts in HBM as well and has reported strong demand for its offerings.

Beyond its lag in AI memory, Samsung has struggled with a costly, yearslong effort to close the gap with TSMC in the foundry business. Like Intel— which has run into similar difficulty with plans to expand its outsourced chipmaking operations — the Korean firm is now moving to cut jobs and make other efforts to stop the bleeding.

Jay Y. Lee — a grandson of Samsung’s founder who was appointed executive chairman two years ago — was acquitted of stock manipulation charges in February after years of legal issues. Three months later, the company unexpectedly replaced its semiconductor division head with Jun Young-hyun, a memory chip veteran.

Samsung executives and engineers are now in full unison, heading towards the exits, looking for greener pastures, and that is a massive red flag.

It certainly isn’t a good optics when the best talent is looking for another job, but that is where we are at with Samsung.

In the short term, I don’t expect a quick turnaround because the management problems are real, and to get competitive in AI is a tall order.

Just look at AMD, they are about a year behind Nvidia, and Samsung isn’t even in the ballpark.

I expect a slow slide into irrelevancy and foreign shareholders dumping big swaths of Samsung stock backs this theory.

In the short term, readers shouldn’t get too fancy with picking AI stocks because there is a massive risk to the downside, considering how expensive the equity market is right now.

Samsung won’t be the last company to be swept up by the dustbin of tech firms.

In the U.S., it is clear which companies are behind and which are leading.

Microsoft is definitely one to buy the dip on.

I definitely envision at least one fiercer rally in AI stocks as we cruise past the U.S. election.

Mad Hedge Technology Letter

September 29, 2023

Fiat Lux

Featured Trade:

(WHAT TO DO ABOUT MICRON)

(MU), (SAMSUNG), (SK HYNIX), (SOXX)

The chip maker Micron Technology (MU) fell 5% yesterday, but the stock is amazingly up 4% today.

The see-saw moves are a feature of this strategically important stock to the tech ecosystem and not just a symptom of it.

The stock is highly volatile which is emblematic of a stock that needs to constantly navigate around unstable geopolitics.

The stock's latest whipsaw action stems from the company predicting a steeper loss than anticipated in the current quarter, indicating that an industry slowdown is still weighing on the largest US maker of memory

For chip companies (SOXX), Samsung Electronics Co., and SK Hynix Inc., 2023 has been a crushing time after the glory period of the healthcare lockdown years.

September has been a month where we are experiencing weakening fundamentals as the US consumer is truly stretched.

Customers in big US markets for personal computers and smartphones have slashed orders as they cope with lackluster demand and stockpiles of excess parts.

Many are continuing to dive deeper into debt to make ends meet and that trend will not go away as the US middle class shrinks further as they grapple with soaring inflation.

The lack of consumer strength will mean it will take longer for Micron to return to profits.

Prices for Micron’s products are going up, and the rate of the price jump is increasing and we can probably say that about prices in most industries.

Sales have fallen for five straight quarters. In the three months ended in August, Micron’s revenue declined 40% to $4.01 billion.

The forecast suggests sales will begin to grow again in the fiscal first quarter, which runs through November.

Beijing has proved a thorn in Micron’s side.

This negative headwind has already cut into the US company’s revenue in China — the largest market for semiconductors — in what management has previously called a “significant headwind.”

The outlook remains mixed in the short term. In traditional servers — the computers that are still the mainstay of most data centers — demand remains tepid at best.

Both personal computers and smartphones will return to growth next year, with units increasing by a percentage in the low- to mid-single digits.

To cope with the slowdown, Micron and its peers reined in production, severely reducing supply and helping prices bottom out.

Micron will be demonstrably below peak 2022 output for the foreseeable future. The company plans to continue to run factories at less than full capacity well into calendar 2024. Micron also will further reduce spending on new equipment next year.

These are bad signs in the short term, but the strategic importance of MU puts a solid bid under the stock price.

I wholeheartedly expect the industry outlook to brighten considerably by 2025 — especially as artificial intelligence systems demand new types of more expensive memory chips.

Therefore, every big dip is a buying opportunity in Micron because this stock is resilient.

Luckily, big dips are common in MU and readers should be patient to wait for optimal entry points.

This is a good one to buy and hold for the long term.

Mad Hedge Technology Letter

September 13, 2023

Fiat Lux

(A GREAT CHIP STOCK TO BUY AND HOLD)

(QCOM), (APPL), (SOC), (SAMSUNG), (TSM)

If there is a company I would tell my grandkids to work for then it would be semiconductor company Qualcomm (QCOM).

Why?

Even Apple (APPL) can’t replace them so easily and that counts for a lot in this day and age.

We learned just as much as Qualcomm said that it will supply Apple with 5G modems for smartphones through 2026.

Qualcomm expected to lose the Apple smartphone business, because they expected Apple to use an internally developed 5G modem starting in 2024.

They couldn’t develop the product fast enough so it is back snapping up modems with QCOM.

QCOM is the best of breed for smartphone chips and they can be found in every flagship Android device.

I am specifically referring to QCOM’s Snapdragon products which are a suite of system on a chip (SoC) semiconductor products for mobile devices.

The Snapdragon's central processing unit (CPU) uses the ARM architecture.

This line of chips is incredibly competitive and one of the foundational reasons to hold the stock.

Samsung’s SoC competitor named the Exynos is still a far cry from the Snapdragon no matter how hard they try and it seems like each iteration of the Exynos flagship SoC is always a generation behind the Snapdragon.

Apple do use their own SoC with the newest one named the Apple A17 Bionic, but QCOM will still monopolize the Android market with their own Snapdragon that is actually slightly better than the A17 Bionic chip.

The Snapdragon 8 Gen 3 beats the CPU clock speed of the A17 Bionic.

This doesn’t always translate to better real-world performance, but it’s still an impressive feat.

People believe the new Taiwan Semiconductor Manufacturing Company (TSM) 3 nanometer (nm) processing can lose to the advanced 4nm node on the 8 Gen 3.

However, Apple will probably maintain a CPU lead, thanks to better software tuning and more transistors in the same area thanks to a smaller 3-nanometer node.

Basically, Snapdragon is a little faster but Apple has higher performance because of its superior software.

There is no denying that Apple has fantastic software.

On the revenue side, this is great news for the staying power of Snapdragon products and continued sales to Apple will boost Qualcomm’s handsets business, which reported $5.26 billion in sales in the past quarter and could soften the blow of potentially losing a critical customer.

About 21% of Qualcomm’s fiscal 2022 revenue of $44.2 billion came from Apple.

APPL purchased Intel’s smartphone modem division in 2019 to build its own modem. However, evidence suggests that it will be challenging for Apple to move away from Qualcomm’s chips because of their complexity.

Qualcomm also makes money from Apple through cellular licensing fees, which were about $1.9 billion in 2022.

Qualcomm continues to collect royalties from Apple under a six-year agreement. That agreement was struck at the end of a legal battle between Apple and Qualcomm over royalties that was settled in 2019.

Qualcomm says that it expects to only supply 20% of the modems needed for Apple’s 2026 smartphone launch, signaling that it likely still expects the Apple business to eventually decline.

Apple’s new iPhone called iPhone 15 uses QCOM modems as do many other high-end smartphones.

It’s hard to believe that QCOM’s market capitalization is only $125 billion. The eye test alone makes me think this is a half a trillion-dollar company.

Revenue is accelerating and they offer a 2.9% dividend yield.

I can’t talk more about the high quality of products made by QCOM.

This company will have staying power and even if Apple decides to move on, there are a slew of companies ready to gobble up QCOM chips.

Readers shouldn’t trade this stock, but they should buy and hold for the long haul.