I think it is safe to say that the banking crisis is now in the market. You saw this in the ritual Friday selloff of bank stocks, which last week made back two-thirds of its losses by the end of the day.

Treasury Secretary Janet Yellen has made it clear that she will use her emergency authority to bail out the depositors of any US banks and leave the shareholders drifting in the wind. That’s OK as long as failures happen in ones and twos and not hundreds.

So after this coming dead, data-less week, we may launch into a serious rally next month, often the strongest of the year, back up to the top of the recent trading range. After that, it will be time to “Sell in May and go away,” and not come back until an interest rate collapse is imminent.

Personally, I have suites on the Queen Mary II and the Orient Express waiting for me. How about you?

And what happens when a crisis winds down? The need for protection ebbs as well. That means that big tech stocks with large balance sheets which had a great March will be due for a rest.

You see this in other flight-to-safety assets, like gold (GLD), which gave up some of its recent gains.

Given the failure of the Volatility Index ($VIX) to maintain a sustainable rally this year, it is clear that something important has changed in that market. That would be same-day options, which are stealing the thunder of the old ($VIX).

Instead of panicking and buying the ($VIX) at market, hedge fund algorithms are now programmed to buy individual same-day stock put options. That vastly increases the volatility of single stocks, with one day 10%-15% moves becoming normal.

When a piece of bad news erupts about the banking system, same-day put options across the entire sector rocket, regardless of whether any individual bank is having problems or not.

Needless to say, as ($VIX) opportunities fade, spectacular new trades are opening up in single stocks which Mad Hedge is happily taking advantage of. As a result, the profitability of our trading strategy has near doubled. This has produced the blowout numbers which I list below.

When panic put buying tanks a stock, we pile on call spreads, as we did two weeks ago with many bank and broker stocks. When fears of recession drive bond prices insanely high, we buy (TLT) put spreads.

Buy low, sell high, it’s my new investment strategy. I’m thinking of patenting it.

With some of the most extreme volatility of the year, Mad Hedge continued on up tear, with March up an eye-popping +12.52%.

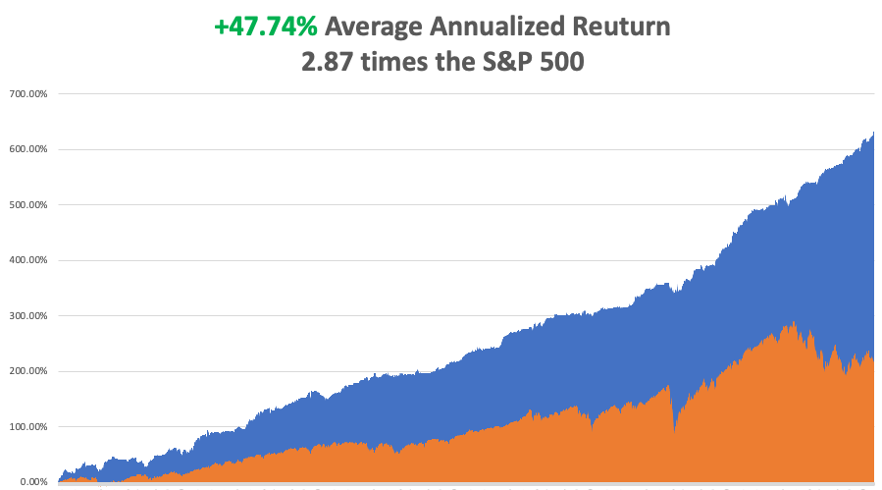

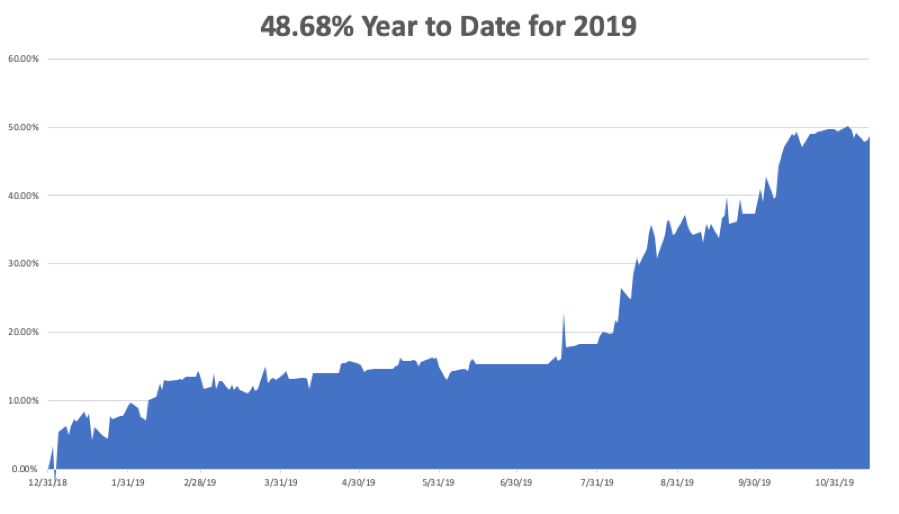

My 2023 year-to-date performance is now at an incredible +38.28%. The S&P 500 (SPY) is up a miniscule +0.77% so far in 2023. My trailing one-year return maintains a sky-high +95.52% versus -10.23% for the S&P 500.

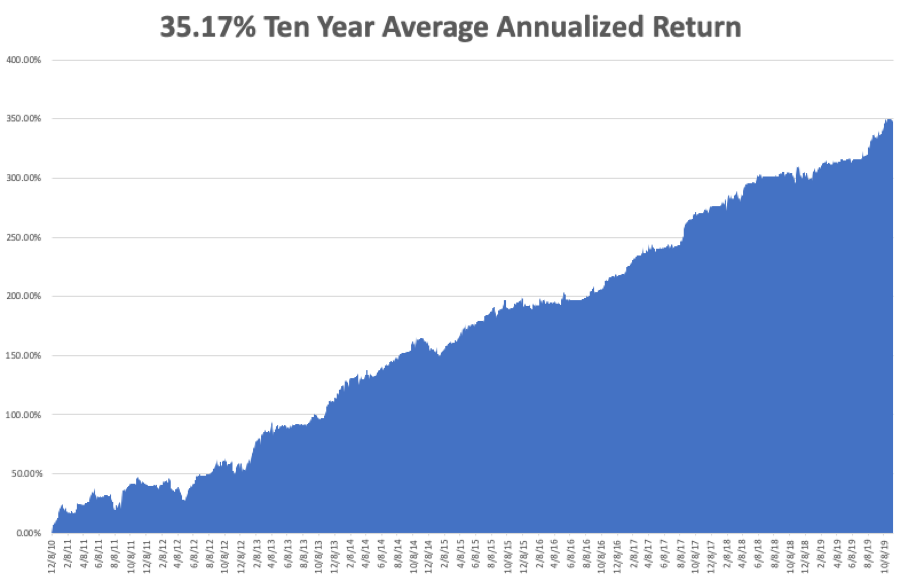

That brings my 15-year total return to +635.47%, some 2.8 times the S&P 500 (SPY) over the same period. My average annualized return has recovered to +48.26%, another new high.

I executed only two trades last week, content to leave alone my remaining eight positions that are profitable. I used a bond selloff to take profits with my bond short (TLT). A frenetic 25% rally prompted me to close out my long in Charles Schwab (SCHW) as we were nearing our maximum profit.

Fed Raises Interest Rates 25 basis points, to an overnight range of 4.75% to 5.00%, a 15-year high. But it left the door open to a further 25 basis points on May 3. The statement substantially weakened the prospect for future interest rate hikes, a de facto pause. Stocks loved the move, especially brokerage and technology stocks. Powell said the US banking system is sound and announced further support measures for small banks.

Yellen to Guarantee Deposits if More Banks Fail, which traders are taking to the bank as a nationwide government backstop. That explains the ballistic moves in financials yesterday. Today, Fed governor Jay Powell plays his hand.

Will the Banking Crisis End the Bear Market? I think so, as a drop in interest rates is the only possible solution. The Fed may have to guarantee all US bank deposits for a year to get there. Bank and technology stocks certainly think so, which have been on a tear this week.

Fed Window Increases By $94 Billion on the Week, and $400 billion in two weeks, in its so far successful effort to float the banking system. Some $60 billion went to foreign borrowers. It has to be viewed as a positive and the emergency need for funding is declining.

Netflix (NFLX) Soars 10%, by ending password sharing in Canada. The United States is expected to be next. The move is expected to boost paid subscriptions. I took profits on my long in (NFLX).

Oil (USO) Dives 1%, as the US energy secretary says it may take “years” to refill the Strategic Petroleum Reserve. How about never?

Existing Home Sales Soar 14.5% in February, a three-year high on a signed contract basis. The annualized rate was 4.58 million according to the National Association of Home Builders. Inventories shrink to an incredible 2.6 months or 980,000 homes. The median home prices fell 0.2% to $363,000, the first decline in 11 years. The sharp drop in interest rates last week will further turbocharge sales. Cash sales were 28% of total sales.

Gold (GLD) Tops $2,000 an Ounce, as the flight to safety bid continues. Lower interest rates sooner will also provide less yield competition for precious metals. Silver will provide the higher beta from here, as it always does.

UBS Buys Credit Suisse (CS) for $3.25 Billion, less than half of where it traded on Friday, eliminating another threat to the global financial system. It looks like there were $5 billion in hidden trading losses. Some $17 billion in lower tier bonds were written down to zero, which several US bond funds like Pimco owned. The deal includes a sweetheart $100 billion loan facility from my friends at the Swiss National Bank. The forced marriage will create one of the largest banks in Europe. Some 9,000 CS jobs will get axed.

Berkshire Hathaway Steps up Share Buybacks, totaling $1.8 billion in 2022. The three-year total is an incredible $60 billion. It explains why (BRK/B) was unchanged in an otherwise horrific year. Buffet still holds a stunning $147 billion in cash, most of which is invested in US Treasury short terms bills.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 27 at 7:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, March 28 at 6:00 AM, the S&P Case Shiller National Home Price Index is announced.

On Wednesday, March 29 at 7:00 AM, the Pending Home Sales for February are printed.

On Thursday, March 30 at 8:30 AM, the Weekly Jobless Claims are announced. The final read on Q4 GDP is disclosed.

On Friday, March 31 at 8:30 AM, the Personal Income & Spending are released.

As for me, not a lot of people get a chance to board a WWII battleship these days. So when I got the chance, I jumped at it.

As part of my grand tour of the South Pacific for Continental Airlines in 1981, I stopped at the US missile test site at Kwajalein Atoll in the Marshall Islands, a mere 2,000 miles west southwest of Hawaii and just north of the equator.

Of course, TOP SECRET clearance was required and no civilians are allowed.

No problem there, as clearance from my days at the Nuclear Test Site in Nevada was still valid. Still, the FBI visited my parents in California just to be sure that I hadn’t adopted any inconvenient ideologies in the intervening years.

I met with the admiral in charge to get an update on the current strategic state of the Pacific. China was nowhere back then, so there wasn’t much to talk about in the wake of the Vietnam War.

As our meeting wound down, the admiral asked me if I had been on a German battleship. “It’s a bit before my time,” I replied. “How would you like to board the Prinz Eugen?" he responded.

The Prinz Eugen was a heavy cruiser, otherwise known as a pocket battleship built by Nazi Germany. It launched in 1938 at 16,000 tons and with eight 8-inch guns. Its sister ship was the Admiral Graf Spee, which was scuttled in the famous Battle of the River Platte in South America in 1939.

Early in the war, it helped sink the British battleship HMS Hood and damaged the HMS Prince of Wales. The Prinz Eugen spent much of the war holed up in a Norwegian fjord and later provided artillery support for the retreating German Army on the eastern front. At the end of the war, the ship was handed over to the US Navy as a war prize.

The US postwar atomic testing was just beginning so the Prinz Eugen was towed through the Panama Canal to be used as a target. Some 200 ships were assembled, including those from Germany, Japan, Britain, and even some American ships deemed no longer seaworthy like the USS Saratoga. One of the first hydrogen bombs was dropped in the middle of the fleet.

The Prinz Eugen was the only ship to remain afloat. In the Navy film of the explosion, you can see the Prinz Eugen jump 200 feet into the air and come down upright. The ship was then towed back to Kwajalein Atoll and put at anchor. A typhoon came later in 1946, capsizing and sinking it.

It was a bright at sunny day when I pulled up to the Prinz Eugen in a small boat with some Navy divers. There was no way the Navy was going to let me visit the ship alone.

The ship was upside-down, with the stern beached to the bow in 300 feet of pristine turquoise water. The propellers had recently been sent off to a war memorial in Germany. The ship’s eight cannons lay scattered on the bottom, falling out of their turrets when the ship tipped over.

The small part of the Prinz Eugen above water had already started to rust through. But once underwater it was like entering a live aquarium.

A lot of coral, seaweed, starfish, and sea urchins can accumulate in 36 years and every inch of the ship was covered. Brightly tropical fish swam in schools. A six-foot mako shark with a hungry look warily swam by.

My diver friends knew the ship well and showed me the highlights to a depth of 50 feet. The controls in the engine room were labeled in German Fraktur, the preferred prewar script. Broken dishes displayed the Nazi swastika. Anti-aircraft guns frozen in time pointed towards the bottom. No one had been allowed to remove anything from the ship since the war, and in the Navy, most men follow orders.

It was amazing what was still intact on a ship that had been blown up by a hydrogen bomb. You can’t beat “Made in Germany.” Our time on the ship was limited as the hull was still radioactive, and in any case, I was running low on oxygen.

A few years later the Navy banned all diving on the Prinz Eugen. Three divers had gotten lost in the dark, tangled in cables, and downed. I was one of the last to visit the historic ship.

I checked with my friends in the Navy and the Prinz Eugen is still there, but in deteriorating condition. When the ship started leaking oil in 2018 and staining the immaculate beaches nearby, the Navy launched a major effort to drain what was left from the 80-year-old tanks. No doubt a future typhoon will claim what is left.

So if someone asks if you know anybody who’s been on a German battleship, you can say “Yes,” you know me. And yes, my German is still pretty good these days.

Vielen dank!

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Prinz Eugen in 1940

The Prinz Eugen Today