Global Market Comments

June 19, 2019

Fiat Lux

Featured Trade:

(TUESDAY, JULY 2 NEW DELHI, INDIA STRATEGY LUNCHEON)

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE)

Global Market Comments

June 19, 2019

Fiat Lux

Featured Trade:

(TUESDAY, JULY 2 NEW DELHI, INDIA STRATEGY LUNCHEON)

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE)

Global Market Comments

March 8, 2019

Fiat Lux

Featured Trade:

(MARCH 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (SDS), (TLT), (TBT), (GE), (IYM),

(MSFT), (IWM), (AAPL), (ITB), (FCX), (FXE)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Are you sticking to your market top (SPY), (SDS) by mid-May?

A: Yes, at the rate that economic data is deteriorating, and earnings are falling, there’s no prospect of more economic stimulation here, my May top in the market is looking better than ever. Europe going into recession will be the gasoline on the fire.

Q: Where do you see interest rates (TLT) in 1-2 years?

A: Interest rates in 2 years could be at zero. If interest rates peaked at 3.25% last year, then the next move could be to zero, or negative numbers. The world is awash in cash, and without any economic growth to support that, you could have massive cuts in interest rates.

Q: Will (TLT) be going higher when a market panic sets in?

A: It will, which is why I’m being cautious on my short positions and why I’m only using tops to sell. You can be wrong in this market but still make money on every put spread, as long as you’re going far enough in the money. That said, when the stock market starts to roll over big time, you want to go long bonds, not short, and we may do that someday.

Q: Do you see a selloff to stocks similar to last December?

A: As long as the Fed does not raise interest rates, I don’t expect to get a selloff of more than 5% or 6% initially. If we do get a dramatic worsening of economic data and it looks like we’re headed in that direction, the Fed will start cutting interest rates, the recession signal will be on and only then will we drop to the December lows—and possibly as low as 18,000 in the Dow.

Q: General Electric has gone from $6 to $10; what would you do now?

A: Short term, sell with a 66% gain in a stock. Long term, you probably want to hold on. However, their problems are massive and will take years to sort out, probably not until the other side of the next recession.

Q: Microsoft (MSFT): long term hold or sell?

A: Absolutely long-term hold; look for another double in this company over the next 3 years. This is the gold standard in technology stocks today. Short term, you’re looking at no more than $15 of downside to the December low.

Q: Would you short banks (IYF) here since interest rates have failed to push them higher?

A: I would not; they’ve been one of the worst performing sectors of the market and they’re all very low, historically. You want to short highs like I’m doing now in the (SPY), the (IWM), and Apple (AAPL), not lows.

Q: Is the China trade deal (FXI) a ‘sell the news’ event?

A: Absolutely; there’s not a hedge fund out there that isn’t waiting to go short on a China trade deal. The weakness this week is them front-running that news.

Q: Do you see emerging markets (EEM) pushing higher from the 42 level, or will a global recession bring it back to earth?

A: First of all, (EEM) will go higher as long as interest rates in the U.S. are flatlining, so I expect a rally to last until the spring; however, when a real recession does become apparent, that sector will roll over along with everything else.

Q: Would you buy homebuilders (ITB) if this lower interest rate environment persists?

A: I wouldn’t. First of all, they’ve already had a big 28% run since the beginning of the year— like everything else—and second, low-interest rates don’t help if you can’t afford the house in the first place.

Q: Would you short corporate bonds if you think there’s going to be a recession next year?

A: I’m glad you asked. Absolutely not, not even on pain of death. I would buy bonds because interest rates going to zero takes bond prices up hugely.

Q: Should you buy stocks in front of a blackout period on corporate buybacks?

A: Absolutely not. Corporate buybacks are the number one buyers of shares this year, possibly exceeding $1 trillion. Companies are not allowed to buy their own stocks anywhere from a couple of weeks to a month ahead of their earnings release. By removing the principal buyer of a share, you want to sell, not buy.

Q: What are the chances the China trade deal (FXI) breaks down this month and no signing takes place?

A: I have a feeling Trump is desperate to sign anything these days, and I think the Chinese know that as well, especially in the wake of the North Korean diplomatic disaster. He has to sign the deal or we’ll go to recession, and that would be tough to run on for reelection.

Q: Which stock or ETF would you short on real estate?

A: If you short the iShares US Home Construction ETF (ITB), you short the basket. Shorting individual stocks is always risky—you really have to know what’s going on there.

Q: What’s the best commodity play out there?

A: Copper. If China is the only country that’s stimulating its economy right now, and China is the largest consumer of copper, then you want to buy copper. The electric car boom feeds into copper because every new vehicle needs 20 pounds of copper for wiring and rotors. Copper is also cheap as it is coming off of a seven-year bear market. What do you buy at market tops? Only cheap stuff.

Q: Why did you go so far in the money in the Freeport-McMoRan (FCX) call spread with only a 10% profit on the trade in five weeks?

A: In this kind of market, I’ll take 10% in 5 weeks all day long. But additionally, when prices are this high, I want to be as conservative as possible. Going deep in the money on that is a very low-risk trade. It’s a bet that copper doesn’t go back to the December lows in five weeks, and that’s a bet I’m willing to make.

Q: Will a new round of QE in Europe affect our stock market?

A: Yes, it’s terrible news. It will weaken the Euro (FXE), strengthen the dollar (UUP), and force US companies to lower earnings guidance even further. That is bad for the market and is a reason why I have been selling short.

Global Market Comments

February 21, 2019

Fiat Lux

Featured Trade:

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE),

Global Market Comments

January 15, 2019

Fiat Lux

SPECIAL ARMAGEDDON ISSUE

Featured Trade:

(HERE’S THE WORST-CASE SCENARIO),

($INDU), (SPY), (SDS), (TLT), (TBT), (FXE), (FXY),

(UUP), (DDP), (USO), (SCO), (GLD), (DGZ), (ITB)

Yesterday, I listed my Five Surprises of 2019 which will play out during the first half of the year prompting stocks to take another run at the highs, and then fail.

What if I’m wrong? I’ve always been a glass half full kind of guy. What if instead, we get the opposite of my five surprises? This is what they would look like. And better yet, this is how financial markets would perform.

*The government shutdown goes on indefinitely throwing the US economy into recession.

*The Chinese trade war escalates, deepening the recession both here and in the Middle Kingdom.

*The House moves to impeach the president, ignoring domestic issues, driven by the younger winners of the last election.

*A hard Brexit goes through completely cutting Britain off from Europe.

*The Mueller investigation concludes that Trump is a Russian agent and is guilty of 20 felonies including capital treason.

*All of the above are HUGELY risk negative and will trigger a MONSTER STOCK SELLOFF.

It’s really difficult to quantify how badly markets will behave given that this scenario amounts to five black swans landing simultaneously. However, we do have a recent benchmark with which to make comparisons, the 2008-2009 stock market crash and great recession. I’ll list off the damage report by asset class. I also include the exchange-traded fund you need to hedge yourself against Armageddon in each asset class.

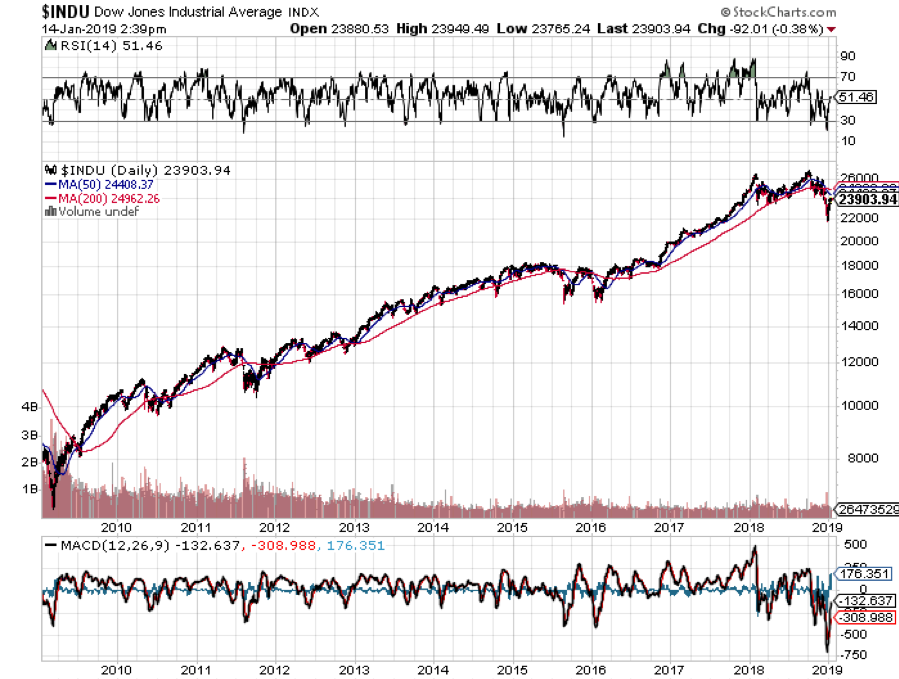

*Stocks – Depending on how fast the above rolls out, you will see a stock market (SPY) collapse of Biblical proportions. You’ll easily unwind the Trump rally that started at a Dow Average of 18,000, down 25% from the current level, and off a gut-churning 9,000 points or 33% from the September top. The next support below is the 2015 low at 15,500, down 11,500 points, or 43% from the top. By comparison, during the 2008-2009 crash, we fell 52%. Everything falls and there is no safe place to hide. Buy the ProShares UltraShort S&P 500 bear ETF (SDS).

*Bonds – With the ten-year US Treasury yield peaking at 3.25% last summer, a buying panic would spill into the bond market. Inflation is nonexistent, we are running at only a 2.2% YOY rate now, so widespread deflation would rapidly swallow up the entire economy. In that case, all interest rates go to zero very quickly. The Fed cuts rates as fast as it can. Eventually, the ten-year yield drops to -0.40%, the bottom seen in Japanese and German debt three years ago. Buy the 2X short bond ETF (TBT) which will rocket to from $35 to $200.

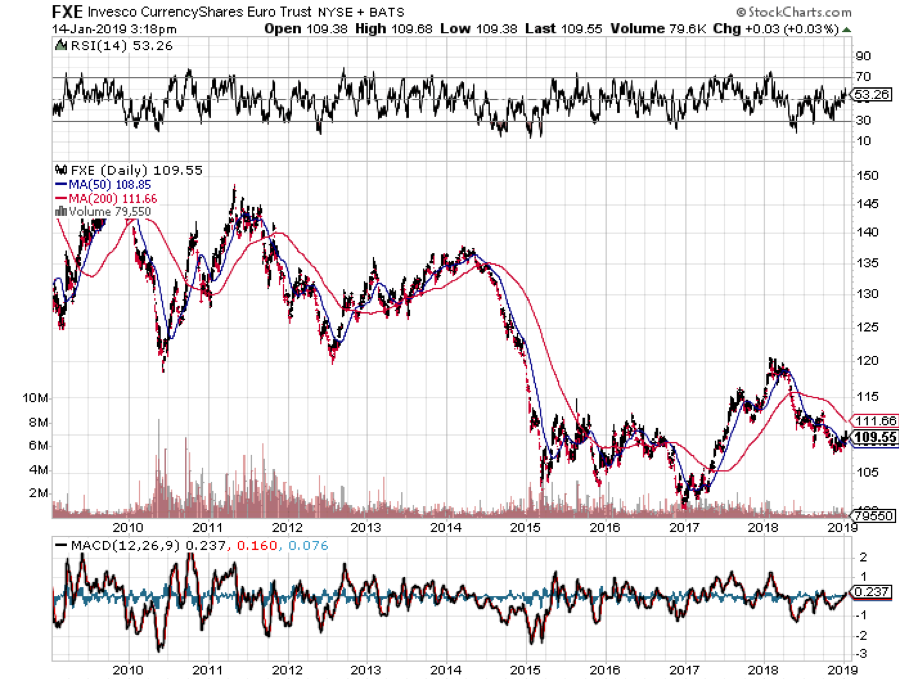

*Foreign Exchange – With US interest rates going to zero, the US Dollar (UUP) gets the stuffing knocked out of it. The Euro soars from $1.10 to $1.60 last seen in 2010, and the Japanese yen (FXY) revisits Y80. Strong currencies then crush the economies of our largest trading partners. Their governments take their interest rates back to negative numbers to cool their own currencies. Cash becomes trash….globally.

*Commodities

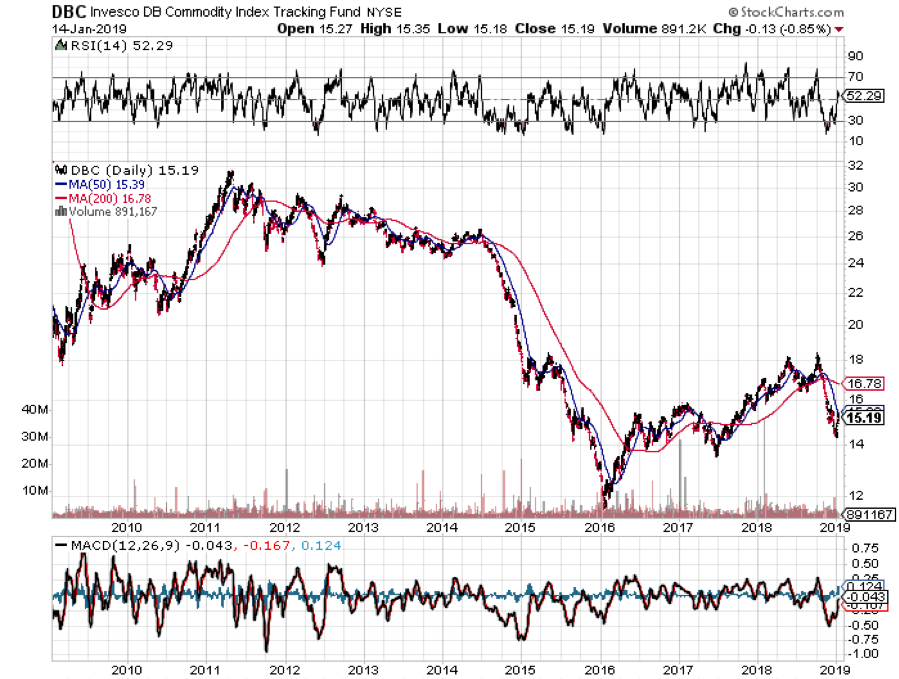

Here’s the really ugly part about commodities. They are only just starting to crawl OUT of a seven-year bear market. To hit them with another price collapse now would devastate the industry. Producer bankruptcies would be widespread. The ags would get especially hard hit as they have already been pummeled by the trade war with China. Midwestern regional banks would get wiped out. Buy the DB Commodity Short ETN (DDP).

*Energy

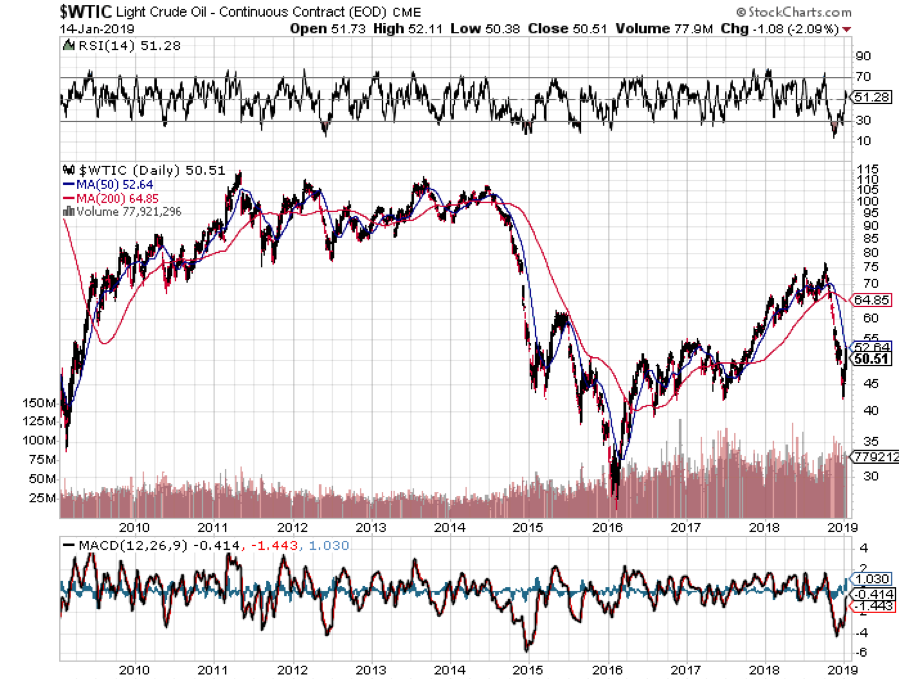

The price of oil (USO) is also just crawling back from a correction for the ages, down from $77 to $42 a barrel in only three months. Hit the sector with a recession now in the face of global overproduction and the 2009 low of $25 becomes a chip shot, and possibly much lower. Those who chased for yield with energy master limited partnerships will get flushed. Several smaller exploration and production companies will get destroyed. And gasoline drops to $1 a gallon. The Middle East collapses into a geopolitical nightmare and much of Texas files chapter 11. Buy the ProShares UltraShort Bloomberg Crude Oil ETF (SCO).

*Precious metals

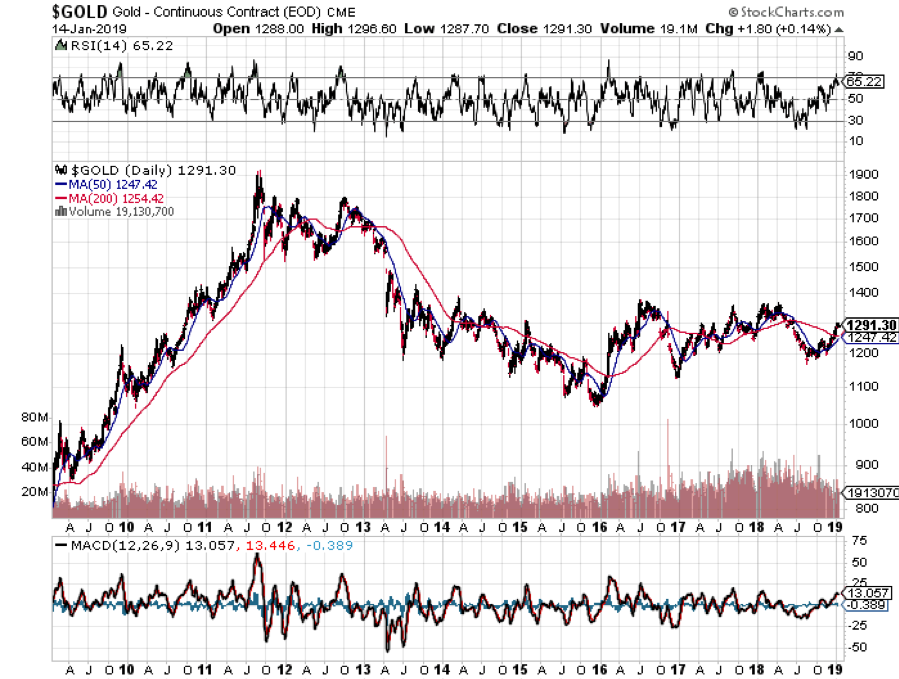

Gold (GLD) initially rallies on the flight to safety bid that we have seen since September. However, if things get really bad, EVERYTHING gets sold, even the barbarous relic, as margin clerks are in the driver’s seat. You sell what you can, not what you want to, as liquidity becomes paramount. This is what took the yellow metal down to $900 an ounce in 2009. Buy the DB Gold Short ETN (DGZ).

*Real Estate

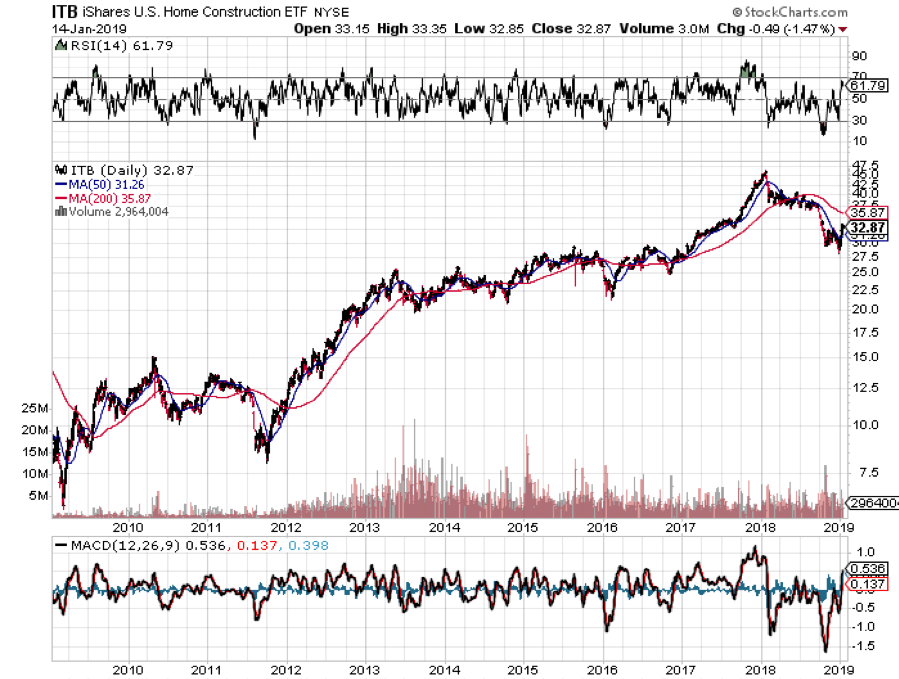

Believe it or not, real estate doesn’t do all that bad in a worst-case scenario. It is perhaps the safest asset class around if a new crisis financial unfolds. For a start, interest rates at zero would provide a huge cushion. The Dodd-Frank financial regulation bill successfully prevented lenders returning to even a fraction of the leverage they used in the run-up to the last recession. We are about to enter a major demographic tailwind in housing as the Millennial generation become the predominant home buyers. I’ve never seen a housing slump in the face of a structural shortage. And homebuilder stocks (ITB) have already been discounting the next recession for the past year. A lot is already baked in the price.

Conclusion

Of course, it is highly unlikely that any of the above happens. Think of it all as what Albert Einstein called a “thought experiment.” But it is better to do the thinking now so you can do the trading later. There may not be time to do otherwise.

Be Careful, They Bite!

Be Careful, They Bite!Global Market Comments

June 12, 2018

Fiat Lux

Featured Trade:

(THE LAST CHANCE TO ATTEND THE THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON)

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE),

Global Market Comments

June 8, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE TUESDAY, JUNE 12, 2018,

NEW ORLEANS, LA, GLOBAL STRATEGY LUNCHEON),

(JUNE 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (TTT), (TBT), (AMLP), (IBB),

(SPY), (SDS), (SH), (GS), (BAC)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader June 6 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: What does the coming Kim Jong-un summit with North Korea mean for the market?

A: It means absolutely nothing for the market. The entire North Korean threat has been wildly exaggerated as a distraction from the chaos in Washington. So, you may get a one- or two-day rally if it's successful. If it's not expect a one- or two-day sell-off, but no more. Whatever North Korea agrees to, we will not see any follow through; they won't buy the Libyan model of denuclearizing North Korea for fear of their leader meeting the same end as Libya's Khadafy (i.e. being hunted and shot in a storm drain.) North Korea will never give up its nuclear weapons.

Q: What do you do at market tops?

A: Well, hopefully if you're reading this letter you're long up the wazoo, so you sell everything you have. Then, wait for a double top in the market (which is clear as day) and falling volume. You start looking at things like the ProShares Ultra Short S&P 500 ETF (SDS). That's the -2X version (there's the (SH), which is the -1X short S&P 500) and you just start buying outright puts on a lot of different things, particularly the overbought sectors of the market, which are generally pretty obvious. It's also good to look for a stock that has made a new high and has negative money flow.

Q: Why are the banks doing so poorly?

A: I believe they fully discounted all of this year's interest rate hikes last year when the stocks nearly doubled. We just talked about a technical setup; Goldman Sachs (GS), Bank of America (BAC), and other stocks had those bear setups. At this point, I believe they're coming down to a place of support and probably getting a decent dead cat bounce. They've had their sell-off, they had their run, and it was triggered by one of the best technical short setup patterns you'll see.

Q: Would you buy financials here?

A: Absolutely not. It's unclear why they're doing so badly, but I would not buy it with anyone's money. Their earnings growth is nowhere what you see with technology stocks.

Q: Is crude oil poised for the next leg up?

A: No, it's not. The oil game may be over if they rush to overproduce once again. It's clearly been artificially boosted to get the Saudi Aramco IPO done. After the end of the quota system, you can get oil back down to the $50s easily. I don't want to touch it here; if anything, I'm more inclined to buy it if we get down to the $50s, which would essentially be the February low.

Q: Is the U.S. dollar overbought here?

A: Yes. The dollar has had a great run all year, which is evident from the rising interest rates. It's done a 10% move up in a fairly short time, which is a lot for the foreign exchange market. It's way overbought; you could easily get a round of profit taking in the dollar, either going into or right after the next Fed interest rate hike in two weeks. I'm staying away from the currencies. There are too many better fish to fry in the equities.

Q: Can you expect Tech to keep going up after this next run?

A: Yes, I expect us to break out to a new high and give back some ground in a retest of the old high. The old high will then hold and then I expect a sort of slow grind up. Tech could well go up for the rest of 2018.

Q: If the S&P 500 is in a trading range, would you sell any rally?

A: Yes, but I'm going to wait for the rally to come to me; I'm not going to reach for any marginal trades. When the (SPY) gets to $280, I'll be looking very closely at the $285-$290 vertical bear put spread one or two months out. So, that peak should hold for the summer and you can make a good 25%-30% on that kind of spread.

Q: Would you buy Biotech here?

A: Yes, the chart setup here is looking very positive, and it's natural for people to rotate out of Tech to Biotech because the earnings growth is so dramatic. That's why I sent out a Trade Alert to buy the NASDAQ Biotechnology ETF (IBB) yesterday. They have been unfairly held back by fears of drug pricing regulation, which has nothing to do with biotech, but it affects their share prices anyway. But so far, it has been all talk from Trump and no action. I think he's busy with North Korea and the trade wars anyway.

Q: My custodian won't let me sell short the United States Treasury Bond Fund (TLT) so I bought the ProShares Ultra Pro Short 20+ Treasury Fund (TTT). Is that alright?

A: You definitely want to be short the Treasury bonds market for the next several years going forward, so you have the right idea. If the 10-year U.S. Treasury bond yield jumps from 2.95% today to 4% in a year as I expect, that takes the (TLT) down from $119 to $97. If you can't make money shorting bonds in that environment you should consider another line of work.

The problem with these 3X leveraged funds is that the cost of carry is very high. In the case of the (TTT) it is three times the 3.0% 10-year bond coupon you are shorting plus a 1% management fee for a total of 10% a year. For that reason, the 3X funds are really only good for day trading. You run into a similar problem with the 2X (TBT). This is why I use non-leveraged put spreads or outright puts for this asset class.

Q: Why are we seeing strength in the Alerian master limited partnership (AMLP) when oil prices are falling, and interest rates are rising? Shouldn't it be going the other way?

A: How about more buyers than sellers? There are so many retirees out there desperate for yield they will take on inordinate amounts of risk to get it. With an 8.0% dividend yield you always have an underlying bid for this ETF. That's why we have been recommending this since April. An 8% dividend can cover up a lot of sins, even when interest rates are rising and oil prices are falling. Also, the U.S. is infrastructure constrained now that production is approaching 11 million barrels a day. That is great for the kind of energy projects (AMLP) finances.

Q: What's the next support price for NVIDIA (NVDA)?

A: With the stock going straight up there is little need for support. Our 2018 target is $300. If you recall, we have been recommending this cutting-edge GPU manufacturer since $68, and people have made fortunes. Those who bought long dated deep out-of-the-money leaps $100 out made 1,000% on this Trade Alert 18 months ago. That said, the 200-day moving average at $213 looks rock solid.

Good luck and good trading to all.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

When climbing peaks in the Alps, the High Sierras, or the Himalayas, you know you?re getting close to the top when the air becomes thin, it is difficult to breathe, and your nose suddenly starts to bleed. I remember trying to smoke a cigarette at 20,000 feet on Mount Everest. If you didn?t keep puffing it went out immediately because of the lack of oxygen.

I am starting to suffer from a similar woozy feeling from the US stock markets. I have long since quit smoking, but the higher the indexes go, the more light headed I feel.

Take a look at the chart below produced last Friday by my friends at StockCharts.com. It shows the NYSE advance-decline ratio smoothed by a five day moving average. We have since blasted through to a new high for the year. The last time we were this high in July, the S&P 500 commenced a 23% swan dive down to 1068.

If you failed to protect yourself from this gut churning plunge, there is a good chance your clients fired you at the end of last year and you are now trolling through Craigslist looking for new employment opportunities. If you did follow the advice of this letter at the time, you sold short the S&P 500, the Russell 2000, gold, the Euro, and the Swiss franc. That enabled you to make a bundle, and your clients are now showering new money upon you.

I was hoping a sweet spot would set up that would allow me to pick up some meaty short positions, like the leveraged short (SDS) and put options, once a squeeze took us up to 1,350 in the S&P 500. Looking at the slow, low volume grind we are getting, I may not get my wish. Instead, we may get a choppy, rolling type top at a lower level that frustrates the hell out of everyone. We could top out as low as 1,312 instead. Every hedge fund trader I know is just sitting on his hands waiting for a decent entry point to present itself.

Aggressive traders may start scaling in short positions from here in small pieces. Until then, discretion is the better part of valor. Only buy here if your clients have a long term view, a very long term view.

Mount Everest 1976

Is It Time to Sell Yet?