Mad Hedge Technology Letter

April 19, 2021

Fiat Lux

Featured Trade:

(AN ECOMMERCE / EGAMING BEHEMOTH TO LOOK AT)

(SEA)

Mad Hedge Technology Letter

April 19, 2021

Fiat Lux

Featured Trade:

(AN ECOMMERCE / EGAMING BEHEMOTH TO LOOK AT)

(SEA)

Do you want to invest in the 3rd most downloaded app in the shopping category globally for 2020?

Well, you can.

And that’s not all this company does, there is more.

This tech company is also part of a wider portfolio that includes Esport assets.

Sea Limited (SEA) is listed on the Nasdaq stock exchange under the ticker symbol SEA.

SEA, previously known as Garina, is headquartered in Singapore and serves the South East Asian and Latin American markets.

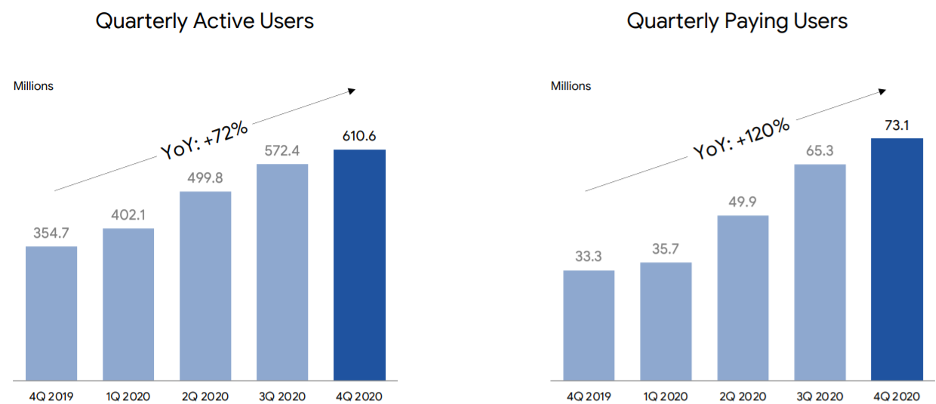

In both the fourth quarter and for the full year, Shopee, SEAs ecommerce division, was ranked the No. 1 in the shopping category across Southeast Asia and Taiwan by average monthly active users, total time spent in-app on Android, and the downloads based on App Annie.

Initially, SEA was a communication platform for video gamers, before distributing games made by Tencent for the Southeast Asian audience.

The company then went on to produce its own in-house game, Free Fire, which became an international phenomenon on the company's first try out of the gate.

Free Fire was once again the top-ranked mobile-only video game and the top-ranked battle royale video game on YouTube in terms of views.

It was also the third-ranked game overall on YouTube by view count. Free Fire-related content recorded over 72 billion view count across YouTube globally over the course of the year.

The game was also named the Esports Mobile Game of the Year at the Esports Award 2020.

They have the in-game titles to accumulate the eyeballs in its ecommerce division.

SEA's ambition went well beyond video games, and the company then launched Shopee in 2015, along with SeaMoney, its digital financial-services arm around the same time.

Shopee has been a winner, overtaking early e-commerce players in the region just as Southeast Asians began to adopt e-commerce at a larger scale.

The pandemic then hit just as Shopee was overtaking its rivals, leading to meteoric growth last year.

It continued to invest in its fintech ambitions by buying Jakarta-based bank Bank BKE. Acquiring a bank signals SEAs ambition to become a swiss army knife of financial services beyond mere e-commerce payments.

Second, Sea Limited has also entered Latin America in a dramatic fashion.

After starting with a small e-commerce presence in Brazil in 2019, Shopee just launched its app in Mexico in February.

The launch signaled that SEA is targeting Latin America for the next phase of incremental growth, where e-commerce is underpenetrated, and where it can cross-market effectively with the many Free Fire players in the region.

Moreover, Latin America has an even bigger population than Southeast Asia, with 2019 GDP of $5.2 trillion, versus Southeast Asia's $3.6 trillion.

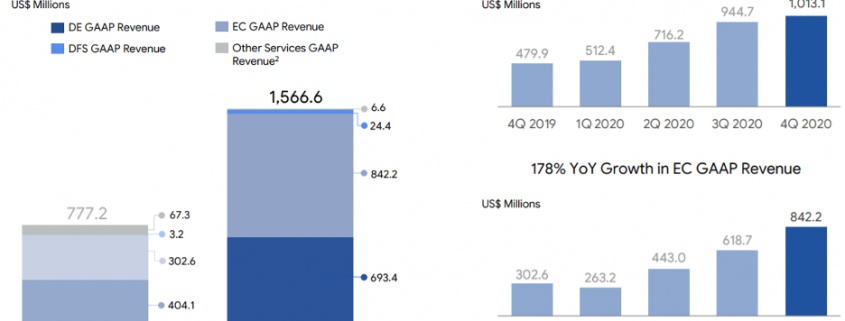

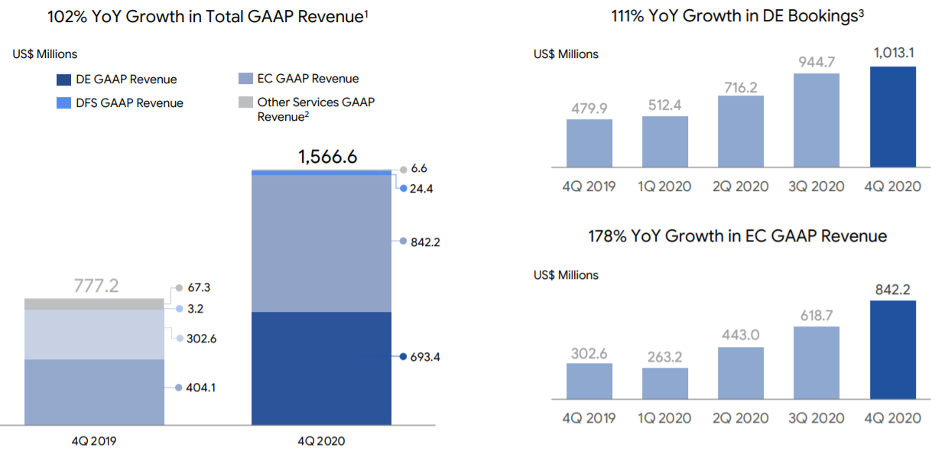

The recent performance is quite breathtaking, to say the least with total revenue increasing 102% year on year to $1.6 billion in the fourth quarter, and 101% year on year to $4.4 billion for the full year of 2020.

This was mainly driven by rapid rate growth in SEAs e-commerce business as they continue to grow tools to better serve users' needs, as well as the growth of the digital entertainment business, especially self-developed game Free Fire.

The proof is in the numbers.

To sustain the momentum in Esports, in the fourth quarter, Phoenix Labs, SEAs triple-A gaming studio based in Vancouver, is adding new offices in Montreal and Los Angeles, alongside its existing - existing bases in Vancouver and Seattle.

Shopee reported 1 billion gross orders, up 135% year on year, and a gross market value (GMV) of $11.9 billion, an increase of 113% year on year resulting in quarterly revenue growing 178% year on year to $842.2 million.

Shopee continued to rank first in Indonesia by average monthly active users, total time spent in-app on Android, and the downloads in the shopping category in the fourth quarter and the for the full year of 2020.

For the full year of 2021, SEA currently expects bookings for digital entertainment to be between $4.3 billion and $4.5 billion, representing 38% year-on-year growth.

Sea Limited also expects that revenue for e-commerce could be between $4.5 billion and $4.7 billion, representing 112% and year-on-year growth as a mid-point of the guidance.

A tech company that grows revenue from $4.38 billion to a projected $9 billion by end of 2021 has caught my eye but there are some major caveats.

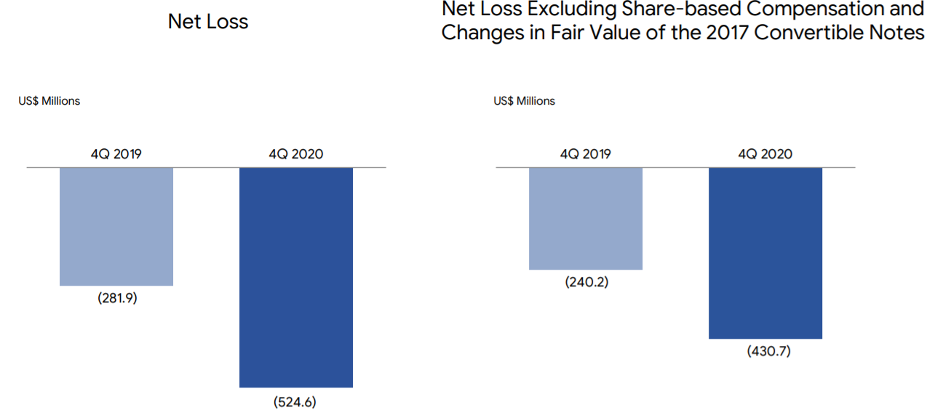

The first major eyesore is the gigantic losses.

Granted, net losses are only half as bad as Uber, but they have a track record of badly missing earnings projections as well.

This would lead me to suggest that the company is not being managed properly if they consistently forecast earnings that are unattainable.

I am quite discouraged by the lack of future profitability rhetoric by management in their earnings call.

Next, they are targeting markets of Latin America and South East Asia that aren’t as lucrative as the North American markets.

Granted, North America is cornered by local incumbents, but that doesn’t change the fact that consumer purchasing power in Mexico, Brazil, and Indonesia is low.

Being a foreign company, regulatory risks are now the order of the day as well.

In the past 365 days, the underlying stock has risen around 500% validating the trajectory of this tech group as a real ecommerce and digital gaming force.

The stock year to date is only up 20% suggesting the pace of appreciation is plateauing and even though annual revenue is projected to double in 2021, I do believe there will be consolidation before the next leg up.

Cut it up any way you want, in a market that pays a premium for big loss-making tech firms, the over 100% in projected revenue growth in 2021 delivers exactly what the tech market desires.

But like other growth stocks ROKU, the ride up will be exhilarating and rocky because unpredictable earnings results are part and parcel of high beta tech stock’s inner workings.

Readers looking for global exposure in a volatile tech name taking advantage of the emerging ecommerce story, take a look at Sea Limited on a meaningful pullback.

The shipping stocks have had an OK year so far in 2015. The big question remains: ?Is it real,? and ?Is it sustainable??

This sector has been down for so long that most investors left it for dead ages ago. All that was missing was the tolling of the Lutine Bell at the Lloyds of London insurance exchange to mark news of a sunken ship.

Lured by the heroin of artificially cheap financing during the 2000?s, the industry massively expanded capacity, believing that international trade would continue to grow at double digit rates forever.

It didn?t.

Sound familiar? Think of it as ?subprime at sea.?

Then the 2008 financial crisis hit, and demand evaporated. International trade, the main driver of freight rates, collapsed. Rates dropped as much as 90%, and share prices even more.

In those dark days, readers delighted in sending me maps of laid up ships with forlorn crews in Singapore harbor, which at the worst, numbered in the hundreds. You could almost walk to neighboring Malaysia and not get your ankles wet.

For most industries, the economy bottomed shortly thereafter and began a long, slow recovery. Not so for shipping.

China, the world?s largest buyer of bulk commodities, saw its economy peak in 2010, with annualized GDP growth halving since then from 13.5% to 7.0%.

This unleashed a second, even more vicious crisis for the shipping industry. With massive capital requirements, order times for new ships lasting three years, and hefty cancellation fees common, recovery delays are not what you want to hear about.

Ships ordered at the peak of the financing bubble suddenly started showing up in large numbers. So, the industry remained with excess capacity of 20%, especially in the dry bulk, container and crude oil tanker segments.

This was happening in the face of steadily rising fuel prices, thanks to events in Iran, Egypt, Libya, Syria, the Ukraine and now Iraq. The China slowdown also caused scrap metal rates to plummet, so downsizing shippers were paid less for junking their older, smaller, less fuel efficient bottoms.

American energy independence, thanks to the ?fracking? boom, means fewer ships are needed to carry oil from a tempestuous Middle East.

It has been the perfect storm of perfect storms. All but seven of the 30 largest shipping companies bled money in 2012, lots of it. Cumulative industry losses amounted to a mind numbing $7 billion over the previous four years. Companies continued to hemorrhage cash, and shareholders suffered.

And then a funny thing happened. The Chinese economic data slowly started to get better. Any price tied to business activity in the Middle Kingdom started marching upward in unison, including those for iron ore (BHP), (RIO), the Australian dollar (FXA), and Chinese and Australian stocks (FXI), (EWA).

This improvement, no matter how uncertain it may be, was not lost on the shipping industry. Capesize charter rates surged from $5,000 to $16,500, while Panamax rates are expected to fly from $8,000 to $9,500 by January.

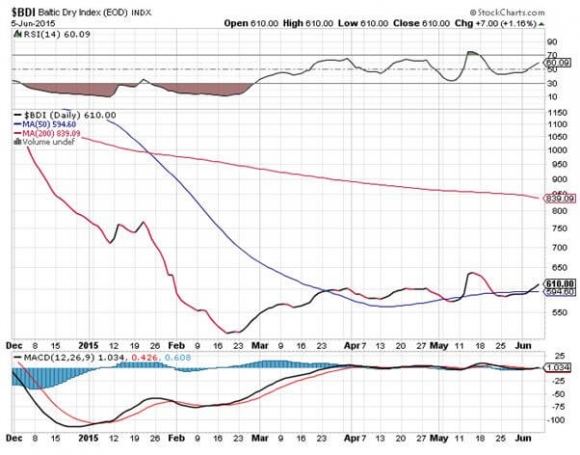

Shipping stocks, the most highly leveraged of asset classes, skyrocketed. This enabled the Baltic Dry Index ($BDI), a measure of the cost of chartering bulk carriers for coal, iron ore, wheat, and other dry commodities, to steadily improve.

Apparently, it is off to the races once again.

I am not normally a person who buys a stock after it has just doubled, unless Costco is running a special on Jack Daniels. But if a share has fallen 99%, a double takes it down to only 98%, leaving it still absurdly cheap.

Shipping stocks fell so far, they were well below long dated option value. That means the market thought all of these guys were going under, which was never going to happen.

This is certainly the case with Dry Ships (DRYS), your poster boy for the Greek shipping industry. Adjusted for splits, the shares cratered from $120 to $0.60. It has just clawed its way up to $0.72. The company?s fleet consists of 38 dry bulk carriers, 10 tankers, and has orders for another four ships.

It has completed a major refinancing that takes the firm out of the fire and puts it back into the frying pan. This should buy (DRYS) some time, while other competitors, like Genco Shipping and Trading (GNK) are expected to go under, removing unwanted overcapacity from the market.

It also wisely diversified into offshore oil drilling right at the bottom of the market, picking up a 59% stake in Ocean Rig (ORIG) and its two semisubmersible rigs.

(DRYS) is not your typical ?widows and orphans? type investment. The web is chock full of allegations of insider trading, nepotism, and self-dealing by senior management.

It is domiciled in the Marshall Islands, so don?t expect much transparency. Pass the smell test, it does not. After all, it is a Greek shipping company.

If (DRYS) scares you, and it should, there are safer ways to play the rebound. The Guggenheim Shipping ETF (SEA) offers a broad mix of industry exposure with lower volatility. It is up a healthy 17% so far this year.

Even in the best-case scenario, shipping will never return to the heady growth rates of the naughts. China is highly unlikely to ever return to the breakneck growth rates of yore. The law of large numbers is kicking in with a vengeance.

It is modernizing its economic strategy, from one led by a low value added commodity exports, to a more domestically driven, services oriented approach. The bad news for shippers: The new model uses fewer bulk commodities, and therefore the ships to carry them.

However, if the China recovery is real, even a modest one, then the shipping industry offers one of the best multiple baggers that I can think of.

Just make sure you don?t get seasick from the volatility.

The Lutine Bell

The Lutine BellTraders are stunned by the performance of the shipping stocks this month, which have been far and away a top market performer. The big questions they are now asking are ?Is it real?? and ?Is it sustainable??

This sector has been down for so long that most investors left it for dead a long time ago. All that was missing was the tolling of the Lutine Bell at the insurance exchange, Lloyds of London.

Lured by the heroin of artificially cheap financing during the naughts, the industry massively expanded capacity, believing that international trade would continue to grow at double digit rates forever. It didn?t.

Sound familiar? Think of it as ?subprime at sea.?

Then the 2008 financial crisis hit, and demand evaporated. International trade, the main driver of freight rates, collapsed. Freight rates dropped as much as 90%, and share prices even more. Readers delighted in sending me maps of laid up ships with forlorn crews in Singapore harbor, which at the worst, numbered in the hundreds. You could almost walk to neighboring Malaysia and not get your ankles wet.

For most industries, the economy bottomed shortly thereafter and began a long, slow recovery. Not so for shipping. China, the world?s largest buyer of bulk commodities, saw its economy peak in 2010, with annualized GDP growth halving since then from 13.5% to 7.5%.

This unleashed a second, even more vicious crisis for the shipping industry. With massive capital requirements, order times for new ships lasting three years, and hefty cancellation fees common, recovery delays are not what you want to hear about. Ships ordered at the peak of the financing bubble suddenly started showing up in large numbers. So, the industry remains with excess capacity of 20%, especially in the dry bulk, container, and crude oil tanker segments.

This was happening in the face of steadily rising fuel prices, thanks to events in Iran, Egypt, Libya, and Syria. The China slowdown also caused scrap metal rates to plummet, so downsizing shippers were paid less for junking their older, smaller, less fuel efficient ships. American energy independence, thanks to the ?fracking? boom, means fewer ships are needed to carry oil from a tempestuous Middle East.

It has been the perfect storm of perfect storms. All but seven of the 30 largest shipping companies bled money in 2012, lots of it. Cumulative industry losses amounted to a mind numbing $7 billion over the past four years. Companies continued to hemorrhage cash, and shareholders suffered.

And then a funny thing happened in August. The Chinese economic data slowly started to improve. Any price tied to business activity in the Middle Kingdom started marching upward in unison, including those for iron ore (BHP), (RIO), coal (KOL), the Australian dollar (FXA), and Chinese and Australian stocks (FXI), (EWA).

This improvement, no matter how uncertain it may be, was not lost on the shipping industry.? Capesize charter rates surged from $5,000 to $16,500, while Panamax rates are expected to fly from $8,000 to $9,500 by January. Shipping stocks, the most highly leveraged of asset classes, skyrocketed. This enabled the Baltic Dry Index ($BDI), a measure of the cost of chartering bulk carriers for coal, iron ore, wheat, and other dry commodities, to rise some 160% since July. Apparently, it is off to the races once again.

I am not normally a person who buys a stock after it has just doubled, unless Costco is running a special on Jack Daniels. But if a share has fallen 99%, a double takes it to down only 98%, leaving it still absurdly cheap. Shipping stocks fell so far, they were well below long dated option value. That means the market thought all of these guys were going under, which was never going to happen.

This is certainly the case with Dry Ships (DRYS), your poster boy for the Greek shipping industry. Adjusted for splits, the shares cratered from $120 to $1.50. It has just clawed its way up to $4.00, and then backed off to $3.67. The company?s fleet consists of 38 dry bulk carriers, 10 tankers, and has orders for another four ships.

It has completed a major refinancing that takes the firm out of the fire and puts it back into the frying pan. This should buy (DRYS) some time, while other competitors, like Genco Shipping and Trading (GNK) are expected to go under, removing unwanted overcapacity from the market. It also wisely diversified into offshore oil drilling right at the bottom of the market, picking up a 59% stake in Ocean Rig (ORIG) and its two semisubmersible rigs.

(DRYS) is not your typical ?widows and orphans? type investment. The web is chocked full of allegations of insider trading, nepotism and self-dealing by senior management. It is domiciled in the Marshall Islands, so don?t expect much transparency. Pass the smell test, it does not. After all, it is a Greek company.

If (DRYS) scares you and it should, there are safer ways to play the rebound. The Guggenheim Shipping ETF (SEA) offers a broad mix of industry exposure with lower volatility. It is up only 25% since April.

Even in the best-case scenario, shipping will never return to the heady growth rates of the naughts. China is highly unlikely to ever return to the breakneck growth rates of yore. The law of large numbers is kicking in with a vengeance.

It is modernizing its economic strategy, from a low value added commodity export led one, to a more domestically driven, services oriented approach. The bad news for shippers: The new model uses fewer bulk commodities, and therefore the ships to carry them.

However, if the China recovery is real, even a modest one, then the shipping industry offers one of the best multiple baggers that I can think of.

Just make sure you don?t get seasick from the volatility.

The Lutine Bell