Mad Hedge Technology Letter

July 1, 2024

Fiat Lux

Featured Trade:

(SOFTBANK BETS THE RANCH ON AI)

(SFTBY), (NVDA)

Mad Hedge Technology Letter

July 1, 2024

Fiat Lux

Featured Trade:

(SOFTBANK BETS THE RANCH ON AI)

(SFTBY), (NVDA)

SoftBank Group raised about $1.86 billion via dollar and euro bond sales in one of the biggest foreign-currency deals by a Japanese company this year.

This is big news.

Softbank is one of the most prominent venture capitalist funds in the world and they plan on deploying the capital solely into generative artificial intelligence.

Many of these heavyweights from Asia, and the Middle East, and other billionaires around the finance world are chomping at the bit to get a piece of American AI firms.

This trend is in the early innings and won’t slow down.

It’s interesting that Softbank raised the currency in dollars and euros which is another bet on the Japanese yen strengthening and the Fed cutting rates.

The Yen has been one of the worst-performing currencies in the past few years and there is a chance this move could blow up in Softbank’s face.

The dollar is strong and has been increasingly strong lately as the Fed stays higher for longer.

However, if the dollar does get stronger, it will mean that Softbank will need to pay higher costs. Even that said, they will still dive head-first into AI.

My belief is that their CEO Masayoshi Son, who I know very well, will bet the ranch on AI considering he sold out of his Nvidia shares in 2022 and calls it the “fish that got away.”

He rues leaving hundreds of billions of dollars in profits on the table and I don’t believe he is willing to allow that to happen again.

So he will approach these new investments as an “all or nothing” all guns blazing type of strategy.

In its first non-yen debt offering since 2021, billionaire Masayoshi Son’s company priced two dollar tranches totaling $900 million and two euro tranches raising €900 million ($964 million).

It’s not only Softbank, it’s also other Japanese companies looking for ample liquidity.

SoftBank joins a bond bonanza by issuers from Asia and elsewhere including even bigger deals from fellow Japanese borrowers such as Takeda Pharmaceutical and Rakuten.

The Japanese firm this year directly invested $200 million into Tempus AI, a startup that analyzes medical data for doctors and patients to come up with better treatments. More recently, it backed Perplexity AI at a $3 billion valuation, betting on a firm that aims to use AI to compete with Alphabet’s Google search.

Longer term, SoftBank is working on a plan to deploy some $100 billion into AI-related chips in a project dubbed Izanagi, Bloomberg News reported in February.

My belief here is that Softbank and other Japanese companies are on the verge of deploying over $1 trillion of new money into generative artificial companies in America.

There is a reason why leading AI companies like Nvidia (NVDA) have surged to the skies and a lot of it is foreign money coming chasing the new hot trend.

I don’t believe this trend will stop will money from all corners of the globe from flooding the US markets chasing the few quality AI companies.

The ultimate takeaway is that the best companies connected the generative artificial intelligence are at the beginning of a huge run in share price that will extend years into the future.

Don’t fight the trend – especially the biggest ones in the world.

Mad Hedge Technology Letter

March 16, 2022

Fiat Lux

Featured Trade:

(THE GENIUS AT SOFTBANK GETS EXPOSED)

(SFTBY), (ARKK), (DIDI), (BABA), (CPNG)

Mad Hedge Technology Letter

November 8, 2021

Fiat Lux

Featured Trade:

(HOW SOFTBANK GOT GLOBALIZATION ALL WRONG)

(SFTBY), (DIDI), (BABA), (CPANG)

Softbank’s Vision Fund, a technology-biased venture capitalist fund, is basically a leveraged massive bet on synchronized bullish behavior on the future earnings of global tech companies.

It assumes that technology is one of the critical underpinnings to global business and it's more or less a wager on an increased rate of harmonic globalization.

I get what they are trying to do, but in 2021, globalization is far from harmonic, and there are many in the camp that the world is wrought by a current phase of deglobalization.

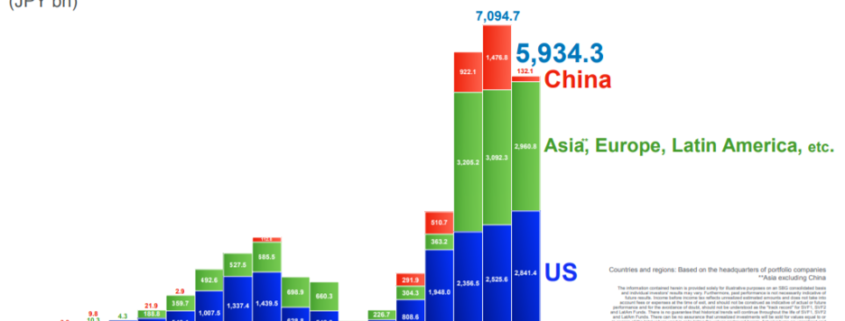

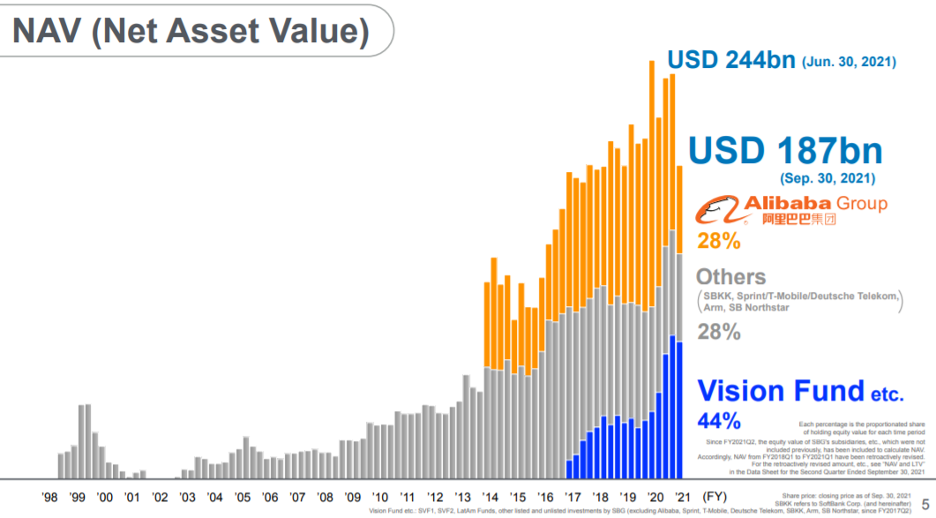

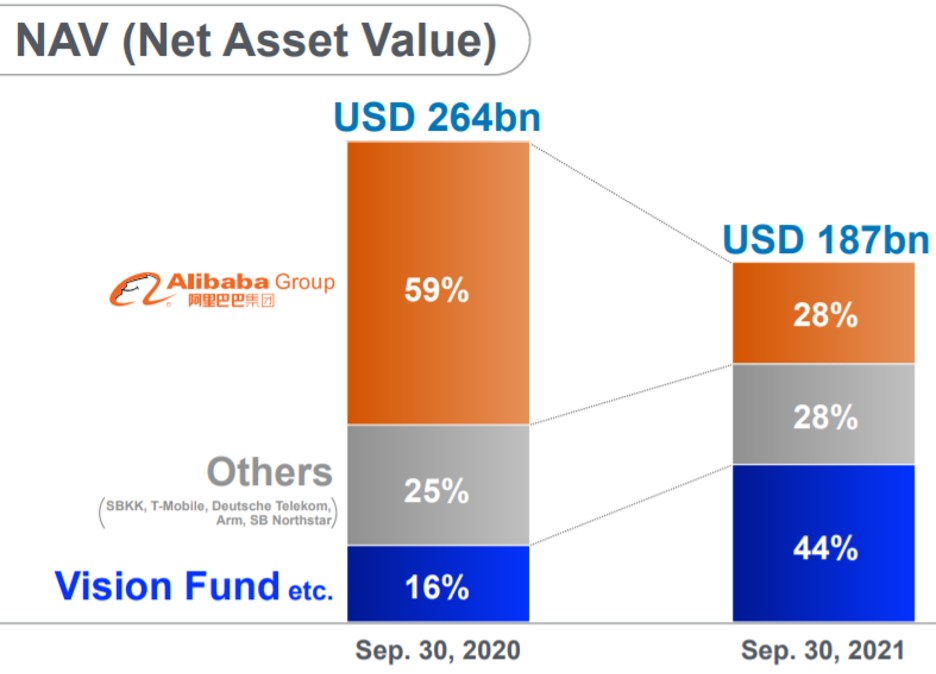

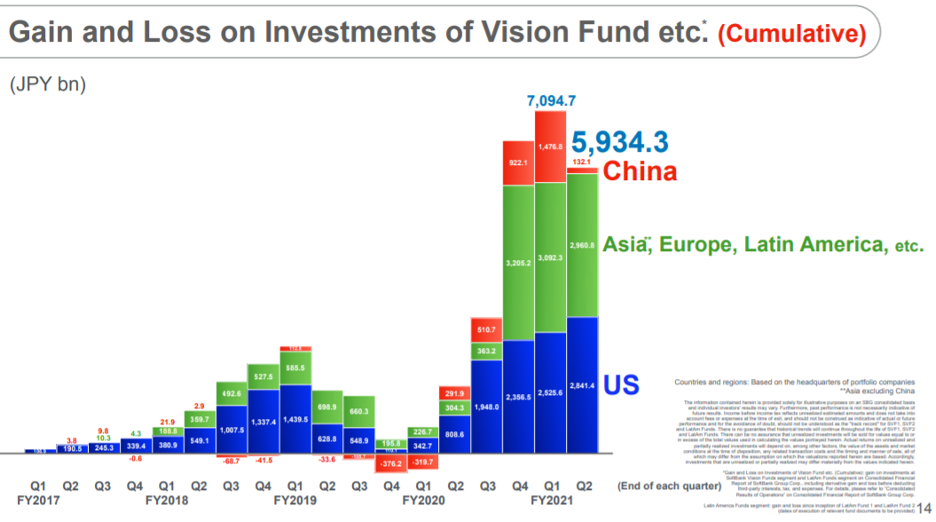

This past quarter, Softbank presided over a precipitous drop in the Net Asset Value of their technology investments from $244 billion to $187 billion.

The -24.6% return and the pain from it were mainly induced from Softbank’s vast array of Chinese investments specifically dreadful performance from its bellwether leader Alibaba (BABA) whose stock has halved since the crackdown started.

CEO of Softbank Masayoshi Son, an ethnic Korean with a Japanese passport, described its current predicament as being “right in the middle of a storm.”

The problem with that is not being in a storm per se, but the timeline into transitioning into sunnier climate because just 1-2 quarters out from now, prospects appear bleak.

If one might remember, DiDi Global Inc. (DIDI), the Chinese ride-sharing platform, was the big shebang going public at a valuation that pegged the company at $68 billion.

Since then, not much has gone right as it was later found out that (DIDI) went public without the tacit approval of the Chinese Communist Party.

Falling out with the good graces of their overlords has meant a halving of the stock and Softbank has taken a loss of $6.1 billion on DiDi.

Even worse for the firm, there appears to be no savior or “next DiDi” IPO to save their Net Asset Value in the upcoming quarters.

That means we could be staring at the high-water mark which occurred 2 quarters ago.

Thank God for the outperformance in Europe and the United States that, in effect, accomplished some damage control for the bottom line.

And their recent short-term track record has been overwhelmingly poor.

Let’s take a glimpse into the other investments that have been chop blocked at the knees.

The losses keep rolling off the tongue with Uber-like trucking startup Full Truck Alliance Co. down $1.2 billion.

KE Holdings Inc., which runs the Beike online property service, lost $2.2 billion of value — the stock is down more than 70% from its peak and is trading below the IPO price.

And the failings weren’t just in China, take a stock that I have extensively bashed on — the biggest ecommerce company in South Kora — Coupang (CPANG).

Their poor past quarter’s performance meant that Softbank booked a quarter performance of a horrific -$6.7 billion.

I told readers to stay away from this one not because it is a bad company.

It was crystal clear in the underlying data that its business was saturated in Seoul, and there are no other big cities in South Korea, and I couldn’t see where the next phase of incremental growth would come from.

The idea was to grow abroad but everywhere else in Asia has been monopolized by local or brand-named ecommerce companies.

That was the bad news, and the silver lining is that ex-China, particularly the United States, they have been doing well and are highly profitable.

Slippage from this Vision Fund is quite notorious, from its misallocation of funds of shared office space company WeWork to overpaying for many other companies with a vanilla idea that technology will overcome any obstacle.

I would say that at a management level, not a lot is well thought out at Softbank.

I would like to remind readers that many of these new China investments by Softbank have just plain out ignored the geopolitical tensions.

They have nobody to blame but themselves because they certainly had time to divest from China and take profits which would have been the right move to do at that time.

Softbank’s parent company’s stock is basically half of what it was in March 2020 thanks to China and the Vision Fund will need to rely on its ex-China investments to pull itself out of this “storm.”

Another big plus is that the China losses are unrealized, but China has offered zero indication that their monumental crackdown on private business is over, and no amount of kowtowing will sway them from their lofty perch.

This could just be the start of their reign of terror over private business and that’s a scary thought right there.

Honestly, I opt for the more conservative stance of never buying Chinese stocks.

Why invest in Chinese tech when United States tech is so much better?

Not enough growth for you?

Then use options.

Softbank should and could have just poured all their investments into Silicon Valley, or just one company like Google, or even the digital gold of Bitcoin.

Good thing there is no ETF that tracks the performance of Softbank!

Invest at your own peril.

Mad Hedge Biotech & Healthcare Letter

September 14, 2021

Fiat Lux

FEATURED TRADE:

(IS THIS THE BIGGEST WINNER IN A WINNER-TAKE-MOST MARKET?)

(NVTA), (ARKK), (ARKG), (SFTBY), (AMZN), (EXAS), (AAPL), (MSFT)

One of the most underappreciated names in the biotechnology sector might just be the biggest winner in a winner-take-most market today: Invitae (NVTA).

Despite being at the receiving end of a seemingly endless flogging since the year started, Invitae remains an attractive stock for the likes of Cathie Woods.

In fact, this San Francisco-based company is one of the Top 20 holdings of ARK Innovation (ARKK) and ARK Genomic Revolution (ARKG).

Described by Woods as "probably one of the most important companies in the genomic revolution," Invitae is the sixth-largest holding of the ARK Investment portfolio with more than $1 billion worth of exposure.

Aside from ARK, Invitae also recently attracted the attention of Japanese tech conglomerate SoftBank (SFTBY), which came in the form of $1.2 billion worth of convertible bond investment.

Amid all these, why is Invitae still under-appreciated?

First, it’s essential to understand that biotech companies opt to target particular niches where they aim to maintain high prices and maximize profitability for as long as possible.

That way, they can maintain and continue to boost their profits.

This results in highly prohibitive costs in the healthcare innovation section, which in turn cause rationing of cases because only a select group of patients can actually afford the exorbitant fees for the innovative drug or therapy.

While rationing care and maximizing profits are obviously great for investors, this makes the innovations inaccessible to people who could not shell out the cash to take the tests or treatments.

This is where Invitae comes in.

Basically, Invitae is taking a completely different approach compared to its peers in the biotechnology world.

According to the company, its mission is "to bring comprehensive genetic information into mainstream medicine to improve healthcare for billions of people."

How will Invitae achieve this?

Instead of choosing a single genetic variant to test, which costs over $1,000 each, the company is developing a testing platform that can identify thousands of genetic variants.

The clincher? This will only cost less than $250 for the entire test panel.

This nonconforming approach to biotechnological innovations is what has primarily led to Invitae’s under-appreciation.

However, Invitae’s mission holds incredible potential.

What it means in medical terms is that the company can help about 1 in 6 people suffering from a medical condition with an inherent genetic factor.

What it means in financial terms is that the company holds the possibility of generating several hundred dollars per year from over 2 billion people—a jaw-dropping market opportunity worth $4 trillion.

One of Invitae’s key ideas is to grant people access to their genetic information and then interpret it for them.

To me, this indicates the company’s goal of doing for genetics what Amazon (AMZN) has done for book buyers.

The next question is this: Can Invitae truly accomplish this?

Let’s consider the company’s growth trajectory along with the catalysts ahead.

So far, three catalysts can push the company towards its goals.

First is the steady growth in testing volume. As with most medical procedures, the volume of genetic testing went down during the COVID-19 pandemic. However, this is now rebounding gradually.

In the first quarter of 2021, the billable volume went up by 72% year over year, with roughly 259,000 tests in that quarter alone.

Traditionally, genetic testing is generally driven by orders from doctors and the cooperation of health plans to cover the tests.

Moving forward, we expect pharmaceutical firms to play more significant roles in promoting and even paying for these tests.

Approximately 90% of the pharma pipelines these days are based on genetic conditions.

As these new and innovative genetic treatments gain FDA approval, the pharma companies would have additional vested interest in ensuring eligible patients receive testing. That way, they can drive demand for the therapies they developed.

The second catalyst comprises the oncology sector.

Genetic testing has become the trend, particularly for cancer—an undoubtedly massive and financially lucrative market.

To leverage this growth, Invitae acquired ArcherDX in 2020 in an effort to expand its offerings.

With this purchase, the company can help major cancer centers implement their testing systems while also offering support to healthcare providers who opt not to do their own testing.

The availability of these comprehensive services will serve as critical drivers of income and profitability considering the historically proven high reimbursement rates in the oncology testing segment.

Apart from this, Invitae recently announced its decision to acquire Ciitizen, a consumer health tech firm, for $325 million.

This move will allow Invitae to expand its patient database through the genomic and clinical information gathered from Ciitizen’s platform.

Thus far, Invitae has announced 13 acquisitions over the past 5 years.

The third catalyst is the continuous global growth of Invitae.

Evidently, the mission of reaching 2 billion people requires worldwide expansion—something that the company has been working on.

In fact, roughly 18% of the total billable volume of Invitae in the first quarter came from international transactions, which have the potential to grow faster than their business in the US.

To date, Invitae has been expanding its operations in Japan, Israel, Europe, and Australia.

Meanwhile, Invitae’s incredible potential has attracted other companies as well. Exact Sciences (EXAS) has been linked to the company for a potential merger among the firms interested.

Admittedly, Invitae’s mission to offer affordable and accessible genetic testing to 2 billion people will require many more years before it comes to fruition.

When that day comes, the company will join Apple (APPL), Amazon, and Microsoft (MSFT) as part of an elite group with $1 trillion and over market cap.

The long wait for Invitae to achieve this ambitious goal would be worth it for patient buy-and-hold investors.

Mad Hedge Technology Letter

August 11, 2021

Fiat Lux

Featured Trade:

(HIGHER HIGHS FOR THE NASDAQ?)

(UBER), (DIDI), (BABA), (COIN), (HOOD), (SFTBY)

The blowback from the Chinese tech crackdown has been quite tough to take for Softbank (SFTBY) because of the decision to maneuver deeply into Chinese tech shares.

It looked good at the time, as China was the center of every Wall Street analyst’s growth proposition short and long term.

However, troubles in China crystallize the massive shift of deglobalization and many investment funds are finding a new world as we turn the page.

Gone are the days when aggressive investors could just dabble in all sorts of exotic markets believing that globalized forces would be a wind at its back.

So much so that nobody ever batted an eye if you told them you had investment theses playing out in Mongolia or Brazil.

Emerging markets are blowing up and now even the passport with which you do business has never been more prominent.

Rich countries are going the way of Europe – that of intense and mind-numbing regulation to make up for a shortage of tax revenues to pay for these costly programs.

The global canary in the coal mine can be traced back to Alibaba’s founder Jack Ma effectively being muzzled by the Chinese Communist Party. This was the nail in the coffin for the China story as it relates to foreign money waterfalling in the Middle Kingdom.

That’s the end of it.

Softbank will need to go back to the drawing board and probably pluck China off the board as top dog and reset their draft board.

The pain is now being found in Softbank’s balance sheet with net profit down 40%.

Let’s look at some of Softbank’s investments which include Chinese e-commerce giant Alibaba (BABA), car-share giant Didi Global (DIDI), and short-video app TikTok owner ByteDance Ltd.

Around 35%-40% of Softbank’s investments are tied up in China and its net profit is down to 761.5 billion yen, equivalent to $6.9 billion.

The incremental buyer has dried up and Softbank is now saddled with an illiquid Chinese tech portfolio they can’t get rid of.

Softbank founder Mr. Son said that SoftBank’s shares have fallen so low that the price is now only around half of the value of the company’s assets, after subtracting debt. Given that discount, SoftBank will unveil more share buybacks at some point, and is now discussing the timing and size.

He also said that SoftBank will continue the furious pace of investment at Vision Fund 2, which has stakes in 161 companies and has been funding startups at a rate of nearly one per day in recent months.

SoftBank’s new investment in pharmaceutical company Roche Holding AG signals that the Japanese company might resort to safer stocks with stable free cash flow.

Compounding the situation might be that Softbank feels that they have been burnt by tech investment one time too many.

The ripple effect of China tech going down affects their assets as a whole and have concluded that the balance sheet needs trimming and re-upping.

Even if Softbank can find some balance sheet rejuvenation - they no longer feel they can take these extraordinary tech risks that achieve high beta which is required to satisfy investors.

Overall, we could be dealing with a dearth of real, legitimate tech opportunities in proven business models which could be a reason for Softbank rotating into sectors like pharmaceuticals.

No doubt I believe they will keep their eye out for tech opportunities, but they aren’t set on it from the beginning like the past 2 decades.

Or perhaps, this could be the segue into riskier investments than before - remember Uber (UBER) was a company that no VC wanted to touch with a 10-feet pole and Softbank took it on and made a lot of money. but where is the next Uber after Uber?

It's possible that there are no real, transformative companies in the pipeline after the Coinbase (COIN), Robinhood (HOOD) IPOs, these investments usually take 10-20 years to take profits from the initial seed funding.

It could also signal further advancements into the derivatives market with the company looking for leverage bets instead of holding vanilla equities and standard ETF index funds.

Their foray into derivate exposure gave them the nickname the “Nasdaq whale” when the company bought a torrent of call options profiting in the billions from the tech lurch up.

Even retail traders have gotten into options with their profit possibilities which are able to surpass any equity trade that only have a 2:1 leverage ratio.

Softbank could be finding tech too overvalued and looking to jump short-term into another industry almost like a day trader, although tech, for them, is something that is a long-term core objective.

We can analyze this whichever way we want but its meaning is clear – the low hanging tech fruit is gone, and it will be harder to fight for your crust of bread even much so that the Nasdaq whale is looking into morphing into the S&P whale or a different type of whale all together.

I can tell you that deep down in the weeds as a trader, I am seeing a rapidly evolving rotation that has rewarded cyclicals that are back from the dead and financials that are breaking out benefiting from the massive amount of stimulus deposits.

We need to acknowledge that the consumer is currently in the best health of our lifetime because of the free payouts, PPP loan forgiveness, and other goodies. And that doesn’t necessarily mean that tech will go up in the short-term as we skim all-time highs.

Technical charts still look positive for tech, but it is true that the sector has cooled off even if the trend will be higher long-term. It’s getting that much harder to eke out higher highs in the Nasdaq.

Mad Hedge Technology Letter

September 9, 2020

Fiat Lux

Featured Trade:

(WHAT’S DRIVING THE NASDAQ?)

(SFTBY)